When non-value added time is greater, manufacturing cycle efficiency is lower.

The financial perspective of the balanced scorecard addresses the things that an

organization needs to do well to meet customer needs and expectations.

Purchases of inventory create a continuous cash outflow each period.

If overapplied factory overhead is immaterial, the account is closed by a credit to Cost

of Goods Sold.

Direct materials are normally considered batch-level costs.

Abnormal spoilage is considered a period cost.

Engineered costs may be either variable or fixed.

The customer value perspective of the balanced scorecard addresses the things that an

organization needs to do well to meet customer needs and expectations.

Negotiated transfer prices are most appropriate for low cost and low volume services.

The accounting rate of return considers the salvage value of an asset.

If the cost of an additive is $5,000 + $0.50 for every unit of solvent produced, the cost

is classified as a step cost.

Variable cost per unit remains constant within the relevant range.

ERP systems are

A. packaged software.

B. methods of examining processes.

C. ways to downsize.

D. ways to expand geographical operations.

The ISO 9000 series refers to

A. international guidelines for quality standards.

B. provisions regarding benchmarking activities in the European Union.

C. guidelines for appropriate expenditures on the various categories of quality costs.

D. all of the above.

Exotic Chocolate Company produces baking chocolate for use by commercial

organizations. The company is analyzing its operations in preparation for reconfiguring

its factory setup.

Currently, each batch of chocolate requires the following processes:

a) Calculate the total cycle time necessary to manufacture a batch of chocolate.

b) Identify the value-added functions

c) Calculate the manufacturing cycle efficiency (MCE) of this process.

d) Assume that a management consultant has established a goal that Exotic Chocolate

Company increase its MCE to 5 percent or greater. Identify three possible areas in

which the company could reduce its cycle time.

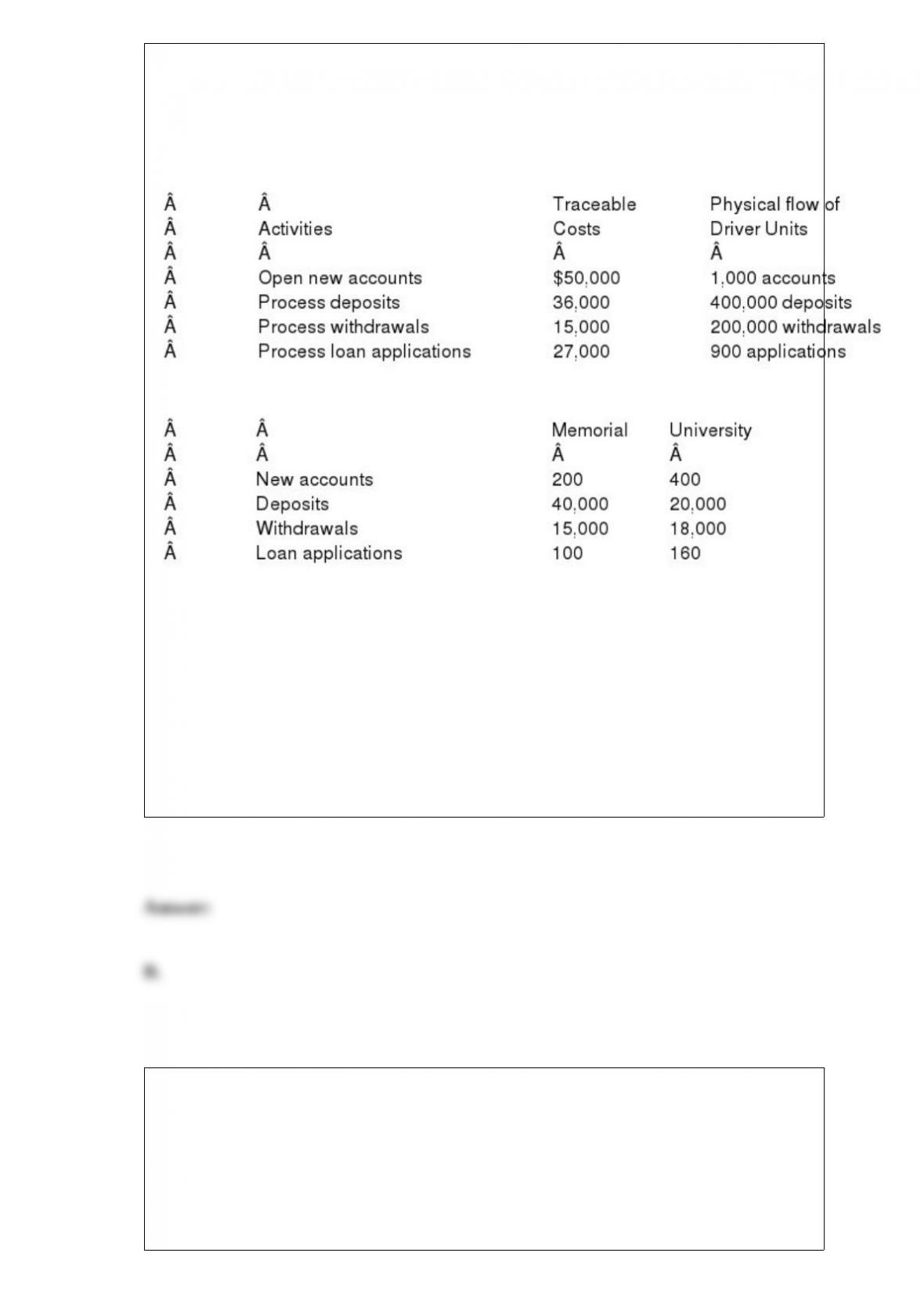

Houston National Bank

Houston National Bank had the following activities, traceable costs, and

physical flow of driver units:

The above activities are used by the Memorial branch and the University branch:

Refer to Houston National Bank. What is the cost per driver unit for the withdrawal

activity?

A. $0.09

B. $0.075

C. $30.00

D. $50.00

Daniels Company started 9,000 units in March. The company transferred out 7,000

finished units and ended the period with 3,500 units that were 40 percent complete as to

both material and conversion costs. Beginning Work in Process Inventory units were

A. 500.

B. 600.

C. 1,500.

D. 2,000.

A project’s after-tax net present value is increased by all of the following except

A. revenue accruals.

B. cash inflows.

C. depreciation deductions.

D. expense accruals.

Which of the following would not be considered a value-added activity in the

preparation of a tax return?

A. printing a copy of the return for the client

B. printing a copy of the return for the IRS

C. installing tax software

D. checking for accuracy

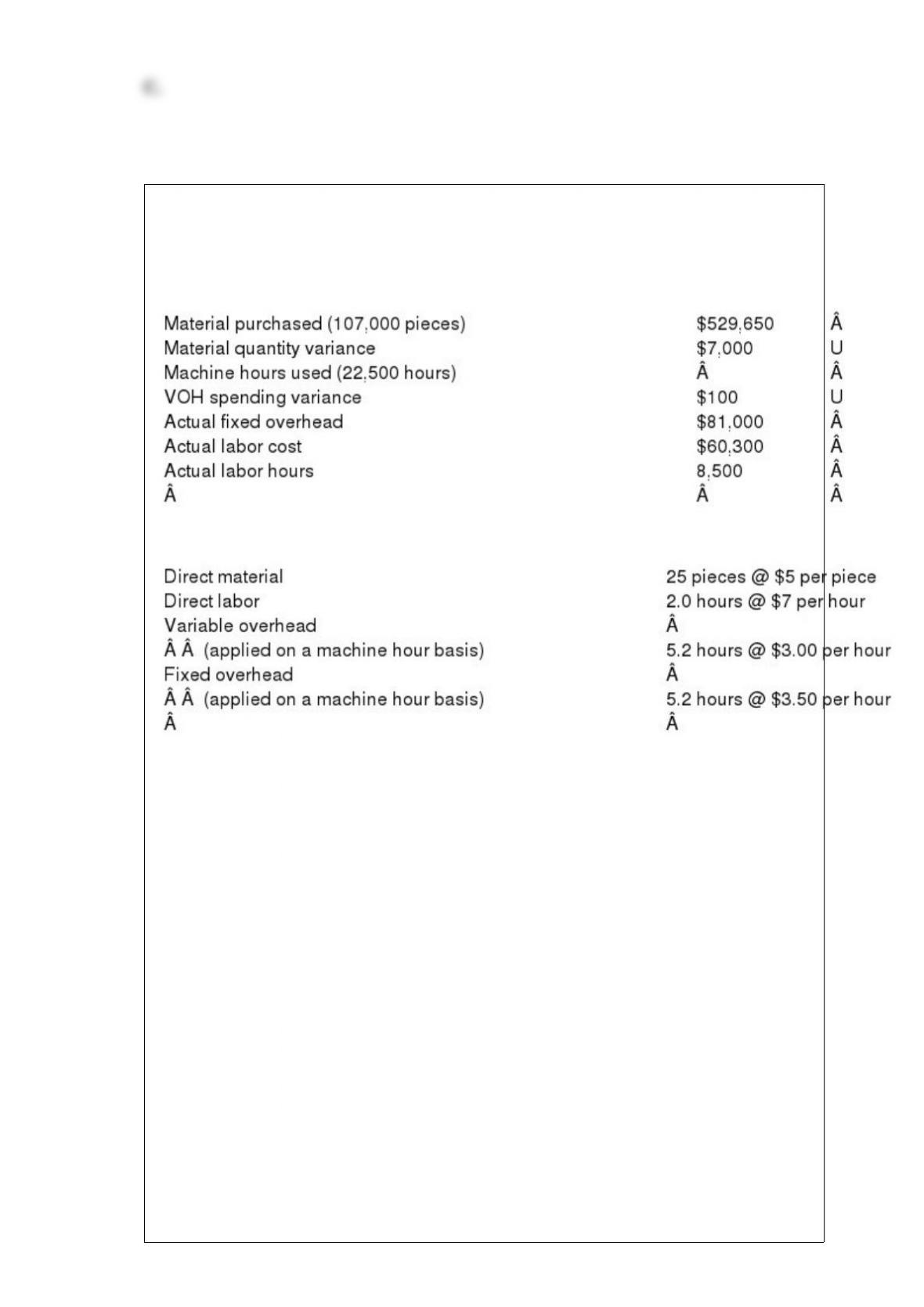

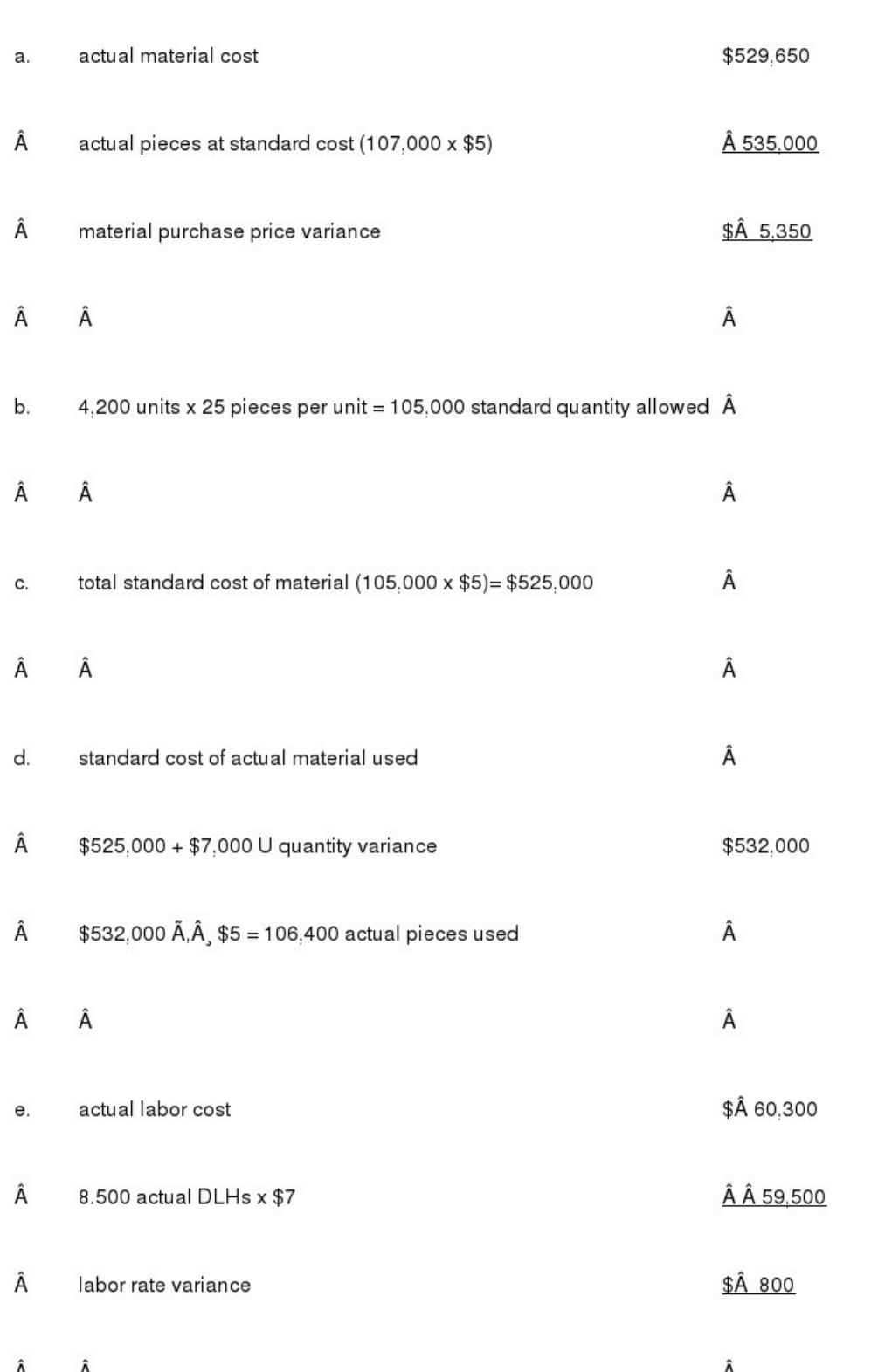

Lubbock Company has made the following information available for its production

facility for the current month. Fixed overhead was estimated at 22,000 machine hours

for the production cycle. Actual machine hours for the period were 22,500; 4,200 units

were produced.

Lubbock Company’s standard costs are as follows:

Determine the following items:

a. material purchase price variance

b. standard quantity allowed for material

c. total standard cost of material allowed

d. actual quantity of material used

e. labor rate variance

f. standard hours allowed for labor

g. total standard cost of labor allowed

h. labor efficiency variance

i. actual variable overhead incurred

j. standard machine hours allowed

k. variable overhead efficiency variance

l. budgeted fixed overhead

m. applied fixed overhead

n. fixed overhead spending variance

o. volume variance

p. total overhead variance

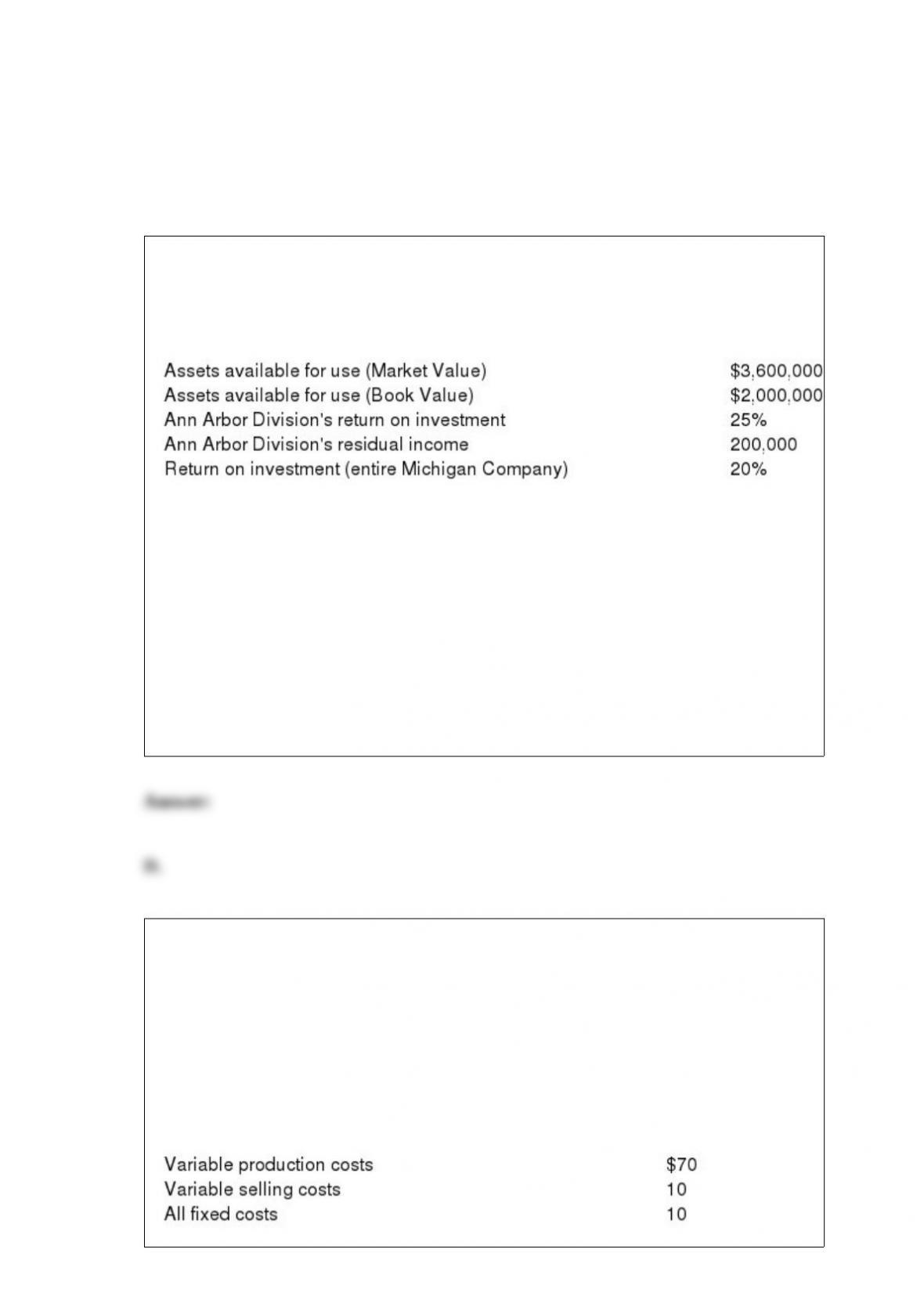

Michigan Company

Ann Arbor Division of the Michigan Company has the following statistics for its most

recent operations:

Refer to Michigan Company. If Michigan Company evaluates its managers on the basis

of return on investment, the manager of Ann Arbor Division would invest in a project

costing $100,000 only if it increased net segment income by at least

A. $10,000.

B. $15,000.

C. $20,000.

D. $25,000.

Magnificent Motor Corporation

The Engine Division of Magnificent Motor Corporation uses 5,000 carburetors per

month in its production of automotive engines. It presently buys all of the carburetors it

needs from two outside suppliers at an average cost of $100. The Carburetor Division

of Magnificent Motor Corporation manufactures the exact type of carburetor that the

Engine Division requires. The Carburetor Division is presently operating at its capacity

of 15,000 units per month and sells all of its output to a foreign car manufacturer at

$106 per unit. Its cost structure (on 15,000 units) is:

Assume that the Carburetor Division would not incur any variable selling costs on units

that are transferred internally.

Refer to Magnificent Motor Corporation. What is the maximum of the transfer price

range for a transfer between the two divisions?

A. $106

B. $100

C. $90

D. $70

The term “discretionary costs” refers to

A. costs that management decides to incur in the current period to enable the company

to achieve objectives other than the filling of orders placed by customers.

B. costs that are likely to respond to the amount of attention devoted to them by a

specified manager.

C. costs that are governed mainly by past decisions that established the present levels of

operating and organizational capacity and that only change slowly in response to small

changes in capacity.

D. amortization of costs that were capitalized in previous periods.

Explain the source of variable overhead spending and efficiency variances and how

these variances are computed.

A system of inventory production where goods are produced in anticipation of

customer orders is referred to as a _________________________.

Costs incurred for monitoring or inspecting products are known as

____________________ costs.

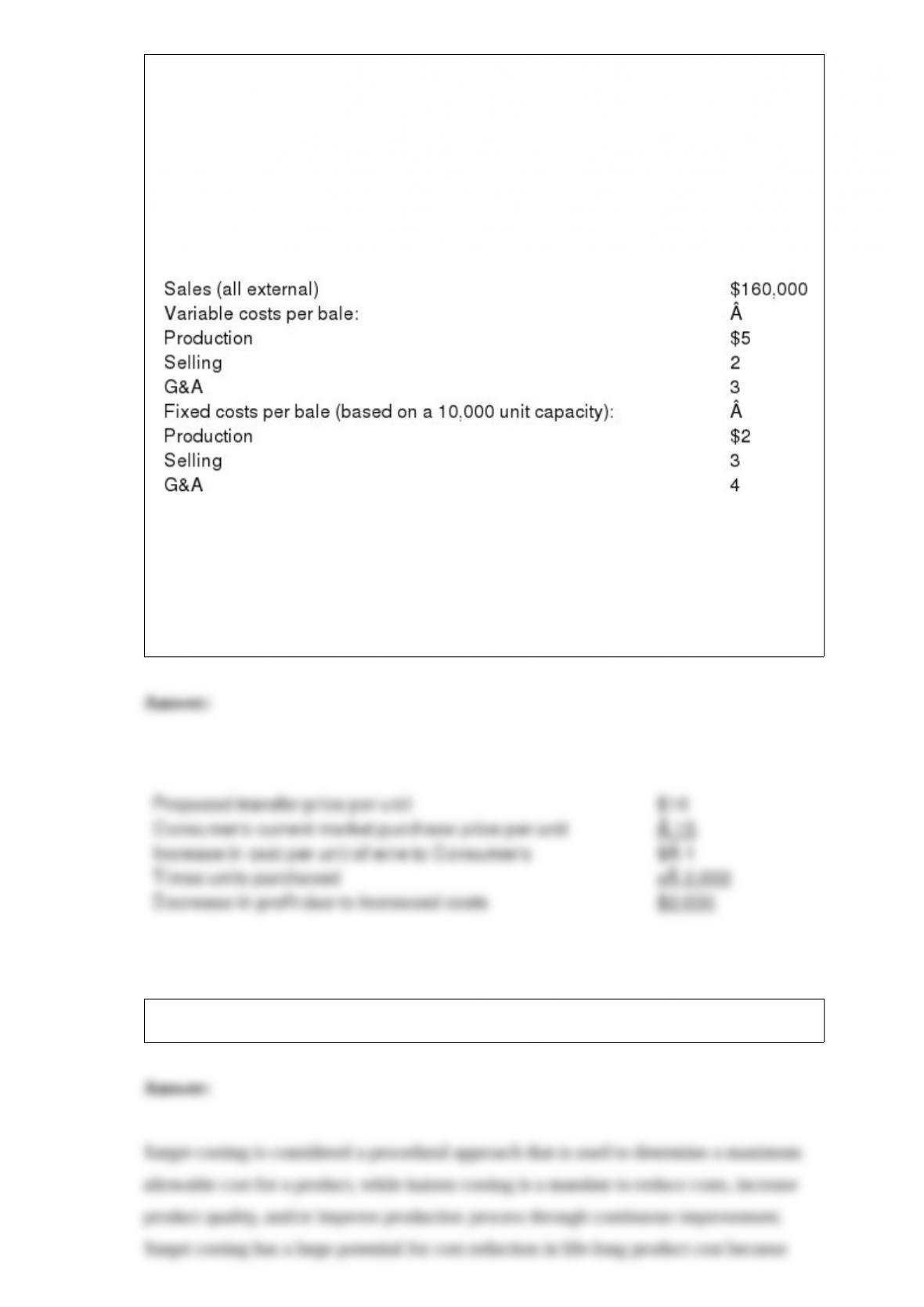

Seminole Wire Corporation

The Wire Products Division of Seminole Wire Corporation produces “bales” of steel

wire that are used in various commercial applications. The bales sell for an average of

$20 each and The Wire Products Division has the capacity to produce 10,000 bales per

month. The Consumer Products Division of Seminole Wire Corporation uses

approximately 2,000 bales of steel wire each month in its production of various

appliances. The operating information for the Wire Products Division at its present level

of operations (8,000 bales per month) follows:

The Consumer Products Division currently pays $15 per bale for wire obtained from its

external supplier.

Refer to Seminole Wire Corporation. If the Consumer Products Division agrees to pay

the Wire Products Division $16 per bale for 2,000 bales this month, what would be

Consumer’s change in total profits?

Discuss differences in approach and potential usage between target and kaizen costing.

How can return on investment result in sub-optimization when it is used as a

performance measure?

A device that alters behavior if the control system indicates a need to do so is referred

to as ____________________.