1) With whom should the auditor communicate whenever he or she determines that

senior management fraud may be present, even if the matter might be considered

inconsequential?

A) PCAOB

B) audit committee

C) an appropriate level of management that is at least one level above those involved

D) the internal auditors

2) The Securities and Exchange Commission has authority to:

A) prescribe specific auditing procedures to detect fraud concerning inventories and

accounts receivable of companies engaged in interstate commerce

B) deny lack of privity as a defense in third-party actions for gross negligence against

the auditors of public companies

C) determine accounting principles for the purpose of financial reporting by companies

offering securities to the public

D) require a change of auditors of governmental entities after a given period of years as

a means of ensuring auditor independence

3) Of the following statements about internal controls, which one is least likely to be

correct?

A) No one person should be responsible for the custodial responsibility and the

recording responsibility for an asset

B) Transactions must be properly authorized before such transactions are processed

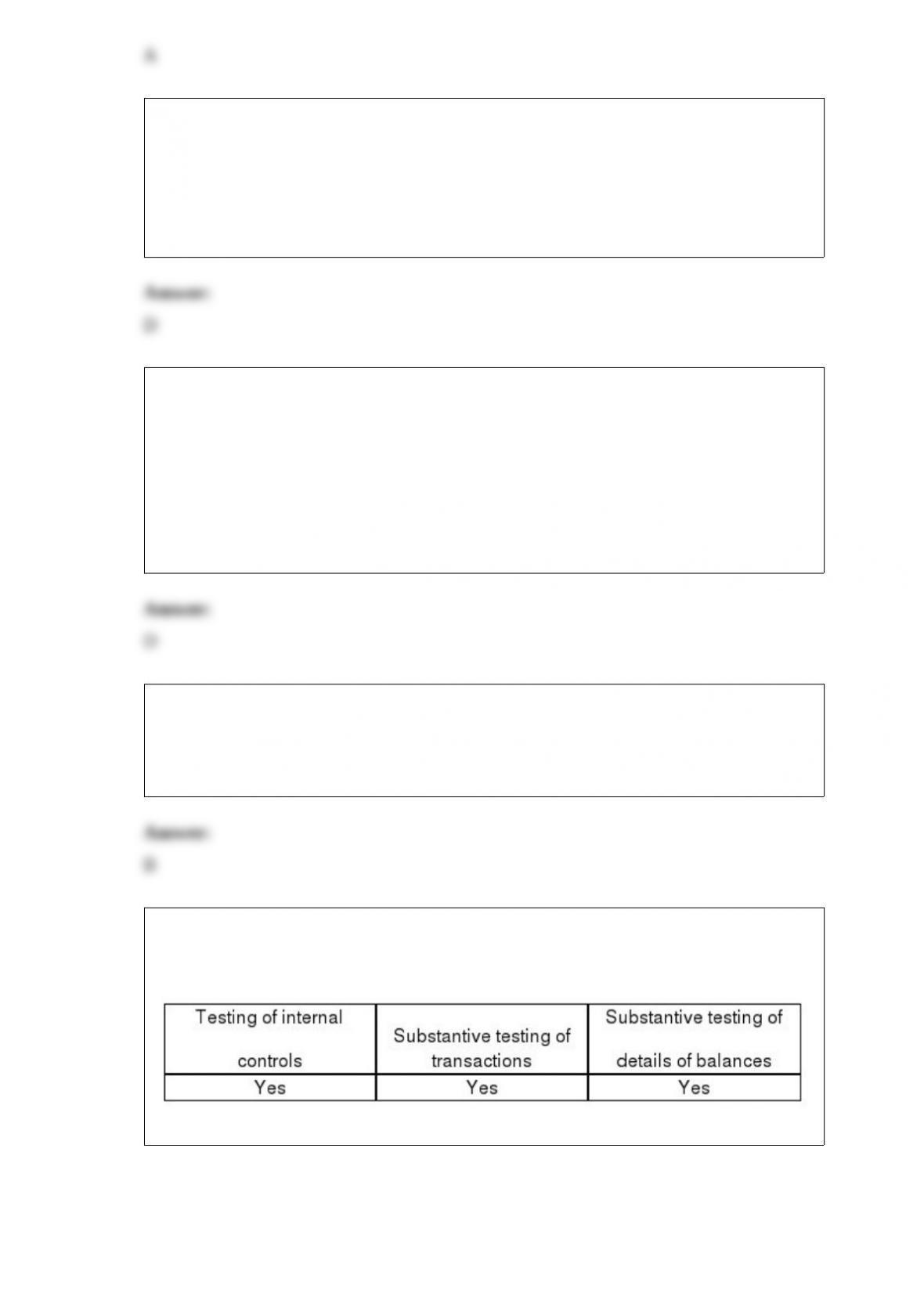

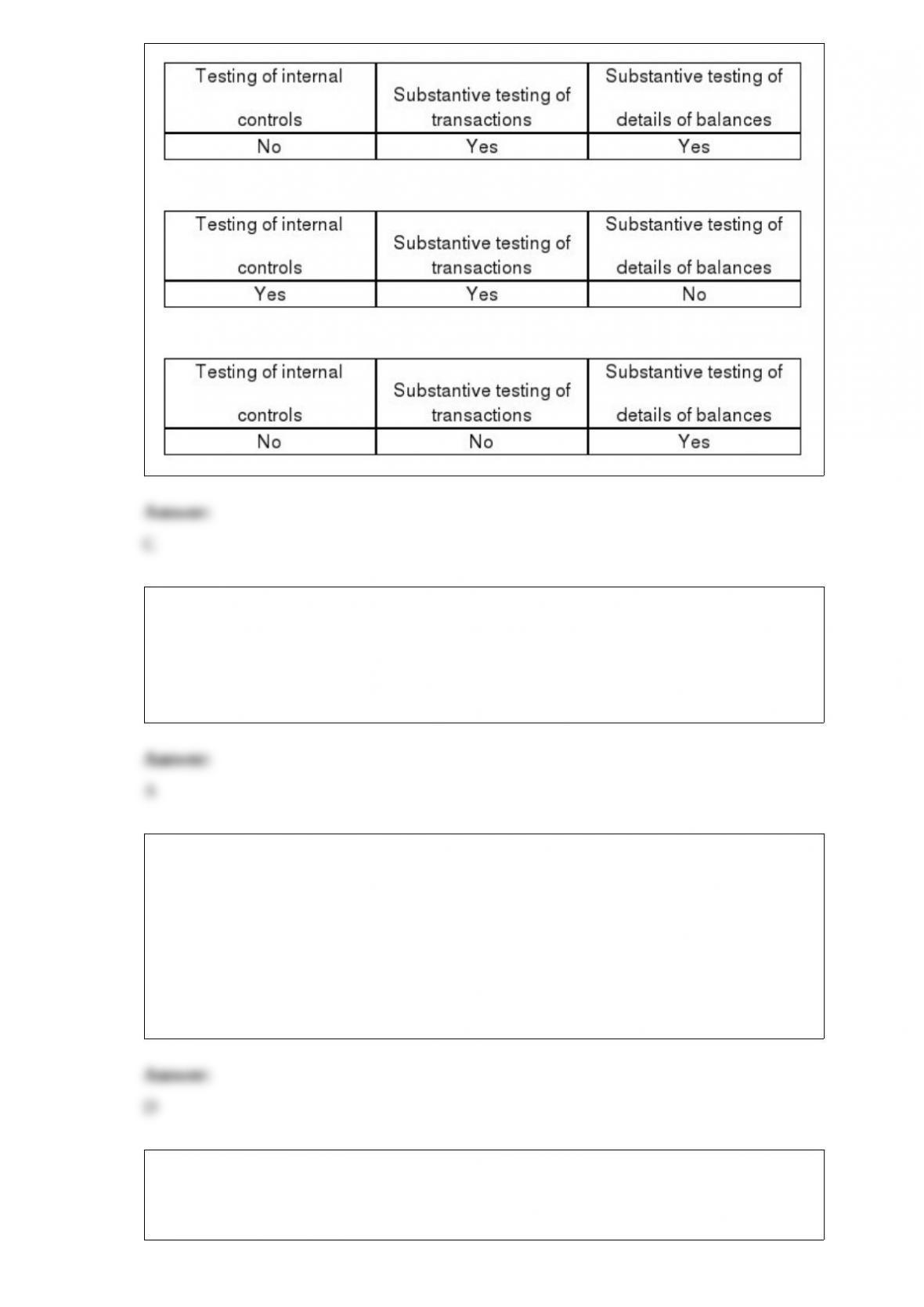

C) Because of the cost-benefit relationship, a client may apply controls on a test basis

D) Control procedures reasonably ensure that collusion among employees cannot occur

4) The general balance-related audit objective that deals with determining that details in

the account balance agree with related master file amounts, foot to the total in the

account balance, and agree with the total in the general ledger is the detail tie-in

objective.

A) True

B) False

5) The restatement of torts approach to the concept of foreseen users states that any

users that the auditor should have reasonably been able to foresee as being likely users

of financial statements have the same rights as those with privity of contract.

A) True

B) False

6) The Auditing Standards Board has concluded that analytical procedures are so

important that they are required during:

A) planning and test of control phases

B) planning and completion phases

C) test of control and completion phases

D) planning, test of control, and completion phases

7) A sales invoice is a document that usually indicates credit approval.

A) True

B) False

8) The overall purpose of the Securities and Exchange Commission is to assist in

providing investors with reliable information upon which to make investment decisions.

A) True

B) False

9) Generally accepted accounting principles require that revenue be reported net of

sales returns and allowances:

A) if practical

B) if required by industry practice

C) if the amounts are material

D) any of the above

10) The highest estimated exception rate in the population at a particular acceptable risk

of assessing control risk too low is:

A) the upper exception rate

B) estimated population exception rate

C) the computed upper exception rate

D) the tolerable exception rate

11) Which of the following is not an important control over notes payable?

A) proper authorization over the issuance of new notes payable

B) notes payable are issued when the business climate is favorable

C) adequate controls exist over repayment of interest and principal

D) there exists proper documents and records

12) While there is no professional requirement to do so on audit engagements, CPAs

frequently issue a formal “management” letter to clients. The primary purpose of this

letter is to provide:

A) evidence indicating whether the auditor is reasonably certain that internal accounting

control is operating as prescribed

B) a permanent record of the internal accounting control work performed by the auditor

during the course of the engagement

C) a written record of discussions between auditor and client concerning the auditor’s

observations and suggestions for improvements

D) a summary of the auditor’s observations that resulted from the auditor’s special study

of internal control

13) Stratified sampling is applicable to difference, mean-per-unit, and ratio estimation,

but it is most commonly used with:

A) ratio estimation

B) discovery sampling

C) difference estimation

D) mean-per-unit estimation

14) Which is usually included in an engagement letter?

A)

B)

C)

D)

15) An auditor performs interim work at various times throughout the year. The

auditor’s subsequent events work should be extended to the date of:

A) the auditor’s report

B) a post-dated footnote

C) the next scheduled interim visit

D) the final billing for audit services rendered

16) Auditors generally allocate the preliminary judgment about materiality to the:

A) balance sheet only

B) income statement only

C) income statement and balance sheet

D) statement of cash flows

17) The effect of a violation of the existence transaction-related audit objective for the

sales account would be an overstatement of that account.

A) True

B) False

18) Tests of which balance-related audit objective are normally performed first in an

audit of the sales and collection?

A) Accuracy

B) Completeness

C) Rights

D) Detail tie-in

19) You are testing controls over accounts receivable and are determining if the

appropriate credit authorization was made by an authorized person. Your sample size is

40 and your computed upper deviation rate is 5%. On the first 10 items sampled you

have found 8 deviations. You would most likely:

A) continue with the other 30 items

B) revisit the sample size calculations

C) increase the tolerable deviation rate

D) stop the test and re-set control risk for accounts receivable

20) Internal auditors should have the authority to require implementation of suggestions

for improvement.

A) True

B) False

21) Tests for rates of occurrence are appropriately used in all but which of the following

situations?

A)

B)

C)

D)

22) If an auditor believes the client will have financial difficulties after the audit report

is issued, and external users will be relying heavily on the financial statements, the

auditor will probably set acceptable audit risk as low.

A) True

B) False

23) An attorney is responding to an independent auditor as a result of the client’s letter

of inquiry. The attorney may appropriately limit the response to:

A) asserted claims and litigation

B) asserted, overtly threatened, or pending claims and litigation

C) items which have an extremely high probability of being resolved to the client’s

detriment

D) matters to which the attorney has given substantive attention in the form of legal

consultation or representation

24) As the amount of misstatements expected in the population approaches tolerable

misstatement, the planned sample size will:

A) decrease

B) increase

C) vary based on characteristics of the population

D) be unaffected

25) The cash account is not part of the acquisitions and payment cycle.

A) True

B) False

26) CPAs must be independent to issue a compilation report.

A) True

B) False

27) The following situations involve a possible violation of the

a. Howard Cunningham & Co., CPAs, designates its firm as “Members of the American

Institute of Certified Public Accountants.” All of the partners of the firm are CPAs.

However, one of the partners has recently chosen to allow her membership to lapse

because of personal reasons.

Rule: ________ Violation? Yes No

Explanation:

b. Brad Long, CPA, was traveling from Orlando to Miami, Florida when he was pulled

over by a police officer on suspicion of driving under the influence. He was convicted

in court of driving while under the influence of alcohol. Because of past convictions,

Brad was sentenced to 5 years in prison.

Rule: ________ Violation? Yes No

Explanation:

c. Kelley Brent, CPA, is a partner in a one-office CPA firm that audits Dane, Inc., a

closely held corporation. Kelley’s sister was recently appointed as the chief financial

officer for Dane, Inc.

Rule: ________ Violation? Yes No

Explanation:

d. Sarah Matrin, CPA, is a senior auditor in the San Francisco office of Cooper &

Howell, CPAs. Sarah’s father is employed as the controller of Line Electronics, a public

company in Detroit, Michigan. Line Electronics is one of the firm’s audit clients.

Neither Sarah nor the San Francisco office is involved in the audit of Line Electronics.

Rule: ________ Violation? Yes No

Explanation:

e. On August 20, 20×6, Hank Anderson, CPA and partner, was offered and accepted the

engagement to audit the annual financial statements of Jernigan Corporation for the

year ended December 31, 20×6. Preliminary work began on the audit on September 15,

20×6 and the engagement ended on March 7, 20×7. Jernigan is regulated by the SEC.

Hank served as controller of Jernigan Corporation from December 1, 20×2, until April

10, 20×6, at which time he terminated his employment with Jernigan.

Rule: ________ Violation? Yes No

Explanation:

28) To issue a report on internal control over financial reporting for a public company,

an auditor must:

A) evaluate management’s assessment process

B) independently assess the design and operating effectiveness of internal control

C) evaluate management’s assessment process and independently assess the design and

operating effectiveness of internal control

D) test controls over significant account balances

29) The use of negative assurance is appropriate in audit reports.

A) True

B) False

30) For which of the following audit procedures would audit sampling not be

appropriate?

A) Review sales transactions for large and unusual amounts

B) Examine a sample of duplicate sales invoices for credit approval

C) Compare the quantity on duplicate sales invoices with the quantity on related

shipping documents

D) Audit sampling is appropriate for each of the above procedures

31) Which of the following would not be classified as an analytical procedure?

A) Benchmarking the company’s profitability ratios against others in the industry

B) Variance analysis of actual versus budgeted amounts for production

C) Reperforming the client’s depreciation expense using the client’s accounting policies

for capital expenditures made during the year

D) Reconciling fixed asset dispositions with the fixed asset ledger

32) Which of the following required an adequate system of internal control for SEC

registrants?

A) Sarbanes-Oxley Act of 2002

B) Securities Act of 1933

C) Foreign Corrupt Practices Act of 1977

D) Securities Act of 1934

33) The amount of time spent verifying owners’ equity is frequently minimal for closely

held corporations because:

A) these companies are so small that it is not necessary to audit the capital section

B) the few owners all have access to the books so the auditor spends more time on

accounts like liabilities, which affect outsiders

C) there are few if any transactions during the year for the capital stock accounts,

except for earnings and dividends

D) there is no public interest in these companies

34) Smith and Jones, CPAs, audited the consolidated financial statements of Concord

Inc. and all but one of its subsidiaries for the year ended September 30, 2012 and are

expressing an unqualified opinion on the financials presented as a whole.

Smith, the engagement partner, instructed Mary, an assistant on the engagement, to

draft the auditor’s report on November 4, 2012, the date of fieldwork completion. In

drafting the report Mary considered the following:

In preparing its financial statements, Concord changed its method of accounting for

research and development costs and properly expensed these amounts. Management

described the change in principle in Note 10 to the consolidated financial statements.

Ball & Brown, CPAs, audited the financial statements of Biotherm, Inc., a consolidated

subsidiary of Concord for the year ended September 30, 2012 . The subsidiary’s

financial statements reflect total assets of 22% and total revenues of 20% of the

consolidated totals. Ball & Brown expressed an unqualified opinion and furnished to

Smith & Jones a copy of their auditor report. Smith & Jones have decided not to assume

responsibility for the work of Ball & Brown insofar as it relates to the expression of an

opinion on the consolidated financial statements taken as a whole because of the

materiality of Biotherm’s financial statements to the consolidated whole. Ball &

Brown’s report will not be presented together with that of Smith & Jones.

Concord is the subject of a grand jury investigation into possible violations of federal

antitrust laws and possible related crimes. Related civil class actions are pending.

Concord’s management has adequately disclosed in Note 12 to their consolidated

financial statements. Because of the early stage of the investigation, the ultimate

outcome of these matters cannot be determined at this time. Therefore, no provision for

any liability that may result has been recorded.

Concord experienced a net loss in 2012 and is currently in default under substantially

all of its debt agreements. Management’s plans in regard to these matters are adequately

disclosed in Note 14 to Concord’s consolidated financial statements. The financials do

not include any adjustments that might result from the outcome of this uncertainty.

These matters rase substantial doubt about Concord’s ability to continue as a going

concern.

Ball reviewed Mary’s draft and indicated in his review notes that there were many

deficiencies in Mary’s Draft. The audit report that Mary drafted follows.

Independent Auditor’s Report

We have audited the consolidated financial statements of Concord, Inc., and

subsidiaries as of September 30, 2012, and the related consolidated statements of

income, changes in stockholders equity and cash flows for the year then ended. These

financial statements are the responsibility of the Company’s management. Our

responsibility is to express an opinion on these financial statements based on our audits.

We did not audit the financial statements of Biotherm, Inc., a wholly-owned subsidiary,

which statements reflect total assets and revenues constituting 22% and 20%

respectively at September 30, 2011 of the consolidated totals. Those statements were

audited by Ball & Brown, CPAs, whose reports have been furnished to us, and our

opinion, insofar as it relates to the amounts included for Biotherm, Inc. is based solely

on their report.

We conducted our audit in accordance with generally accepted auditing standards.

Those standards require that we plan and perform the audit to obtain reasonable

assurance about whether the financial statements are free of material misstatement. An

audit includes examining, on a test basis, evidence supporting the amounts and

disclosures in the financial statements. An audit also includes assessing the accounting

principles used, as well as assessing control risk. We believe our audits provide a

reasonable basis for our opinion.

In our opinion, based on our audit and the report of the other auditors, the consolidated

financial statements referred to above present fairly, in all material respects, the

financial position of Concord Inc., as of September 30, 2012 in conformity with

generally accepted accounting principles, except for the uncertainty, which is discussed

in Note 12 to the consolidated financials.

The accompanying consolidated financial statements have been prepared assuming that

the Company will continue in existence for a reasonable period of time. As discussed in

Note 14 to the consolidated financial statements, the Company suffered a net loss and is

currently in default under substantially all of its debt agreements. Management’s plans

in regard to these matters are also described in Note 14 . The consolidated financial

statements do not include any adjustments that might result from the outcome of this

uncertainty.

Smith & Jones, CPAs

November 4, 2012

Required:

The following items present deficiencies in the drafted audit report noted by Smith. For

each deficiency, indicate whether:

S. Smith’s review note is correct

M. Mary’s draft is correct

B. Both Smith’s review note and Mary’s draft are incorrect

Smith’s Review Notes

1> An explanatory paragraph is required between the scope and opinion paragraphs is

required for the change in accounting principles referring the reader to Note 10 .

2> The names of the other auditors do not need to be explicitly stated in the

introductory paragraph. Only that “other auditors” performed the audit and provided

their report.

3> The opinion paragraph should extend the auditor’s opinion beyond financial position

to include the results of Concord’s operations and flows.

4> The reference to the uncertainty in the opinion paragraph is incomplete. It should

describe the nature of the uncertainty as pertaining to the grand jury investigation into

possible violations of federal antitrust laws.

5> The explanatory paragraph following the opinion paragraph does not include the

terms ‘substantial doubt” and “going concern”. These terms are required to be used in

this paragraph.

6> The explanatory paragraph following the opinion paragraph includes an

inappropriate statement that “the consolidated financial statement6s do not include any

adjustments that might result from the outcome of this uncertainty.” This statement is

misleading and should be omitted.

35) List the four phases of a Financial Statement Audit

36) Auditing standards require the confirmation of accounts receivable in normal

circumstances. What are the three exceptions to this requirement?

37) Briefly explain each management assertion related to presentation and disclosure.

38) What is one audit procedure that may be used to test for proper handling of

terminated employees?

39) What are the two most important balance-related audit objectives in notes payable?

40) What are the three main types of revenue manipulations employed to commit

fraudulent financial reporting and give an example for each type?

41) List at least 3 types of information normally contained in a legal letter to the client’s

attorneys.

42) List and describe the three factors that influence the organizational structure of all

CPA firms. What are the most common forms of CPA firm organization?

43) Explain the effect on sample size of increasing each of the following: (1) tolerable

exception rate, (2) estimated population exception rate, (3) acceptable risk of assessing

control risk too low, and (4) population size.