George Jones is planning on a cruise for his 70th birthday party. He wants to know how

much he should set aside at the beginning of each month at 6% interest to accumulate

the sum of $4,800 in five years. He should use a table for the:

a. Future value of an ordinary annuity of 1.

b. Future value of an annuity due of 1.

c. Future value of 1.

d. Present value of an annuity due of 1.

Asset C3PO has a depreciable base of $16.5 million and a service life of 10 years. What

would the accumulated depreciation be at the end of year five under the

sum-of-the-years’ digits method?

a. $ 4.5 million.

b. $8.25 million.

c. $ 12 million.

d. None of these answer choices are correct.

A discount on a noninterest-bearing note payable is classified in the balance sheet as:

a. An asset.

b. A component of shareholders’ equity.

c. A contingent liability.

d. A contra liability.

On January 1, 2016, Packard Corporation leased equipment to Hewlitt Company. The

lease term is eight years. The first payment of $450,000 was made on January 1, 2016.

Remaining payments are made on December 31 each year, beginning with December

31, 2016. The equipment cost Packard Corporation $2,400,000. The present value of

the minimum lease payments is $2,640,000. The lease is appropriately classified as a

sales-type lease. Assuming the interest rate for this lease is 10%, what will be the

balance reported as a liability by Hewlitt in the December 31, 2017, balance sheet?

a. $1,950,000.

b. $1,509,000.

c. $1,959,000.

d. $1,704,900.

Interest payments and interest received must be reported as operating cash flows

using:

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

The most likely important flaw leading to the demise of the APB was the perceived lack

of:

a. Confidence.

b. Competence.

c. Independence.

d. Importance.

Which of the following is not true about net operating cash flow?

a. It is the difference between cash receipts and cash disbursements from providing

goods and services.

b. It is a measure used in accrual accounting and is recognized as the best predictor of

future operating cash flows.

c. Over short periods, it may not be indicative of long-run cash-generating ability.

d. It is easy to understand and all information required to measure it is factual.

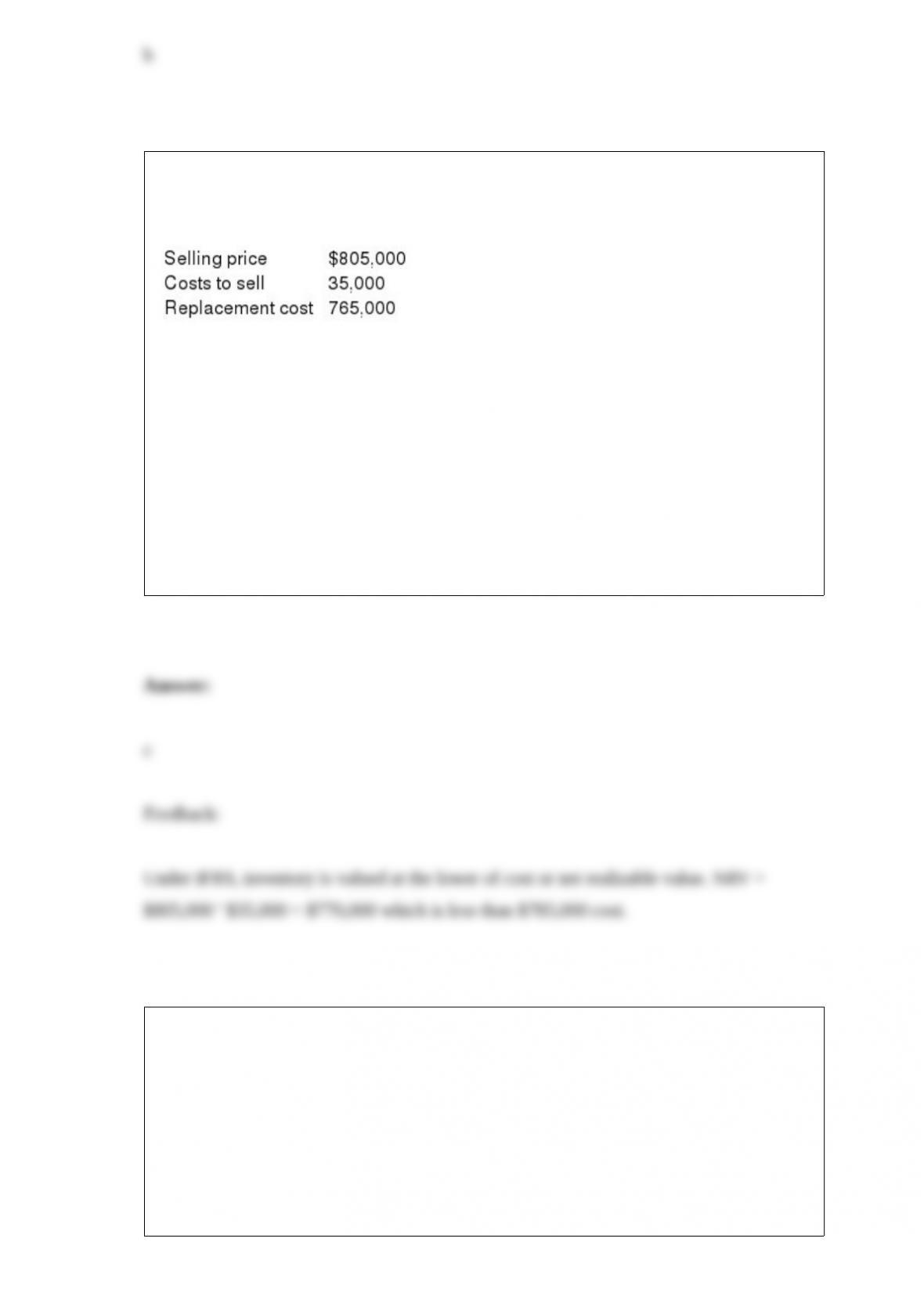

Haskell Corporation has determined its year-end inventory on a FIFO basis to be

$785,000. Information pertaining to that inventory is as follows:

What should be the reported value of Haskell’s inventory if the company prepares its

financial statements according to International Financial Reporting Standards (IFRS)?

a. $765,000.

b. $785,000.

c. $770,000.

d. $750,000.

The capitalized cost of equipment excludes:

a. Maintenance.

b. Sales tax.

c. Shipping.

d. Installation.

Technoid Inc. sells computer systems. Technoid leases computers to Lone Star

Company on January 1, 2016. The manufacturing cost of the computers was $12

million.

This noncancelable lease had the following terms:

-Lease payments: $2,466,754 semiannually; first payment at January 1, 2016;

remaining payments at –June 30 and December 31 each year through June 30, 2020.

-Lease term: five years (10 semiannual payments).

-No residual value; no bargain purchase option.

-Economic life of equipment: five years.

-Implicit interest rate and lessee’s incremental borrowing rate: 5% semiannually.

-Fair value of the computers at January 1, 2016: $20 million.

Collectibility of the rental payments is reasonably assured, and there are no lessor costs

yet to be incurred.

Lone Star Company would account for this as:

a. A capital lease.

b. A direct financing lease.

c. A sales type lease.

d. An operating lease.

Getaway Travel Company reported net income for 2016 in the amount of $50,000.

During 2016, Getaway declared and paid $2,000 in cash dividends on its

nonconvertible preferred stock. Getaway also paid $10,000 cash dividends on its

common stock. Getaway had 40,000 common shares outstanding from January 1 until

10,000 new shares were sold for cash on July 1, 2016. A 2-for-1 stock split was granted

on July 5, 2016. What is the 2016 basic earnings per share (rounded)?

a. $.42.

b. $.47.

c. $.53.

d. $.56.

Orange Co. can estimate the amount of loss that will occur if a foreign government

expropriates some of the company’s assets in that country. If expropriation is reasonably

possible, a loss contingency should be:

a. Disclosed but not accrued as a liability.

b. Disclosed and accrued as a liability.

c. Accrued as liability but not disclosed.

d. Neither accrued as a liability nor disclosed.

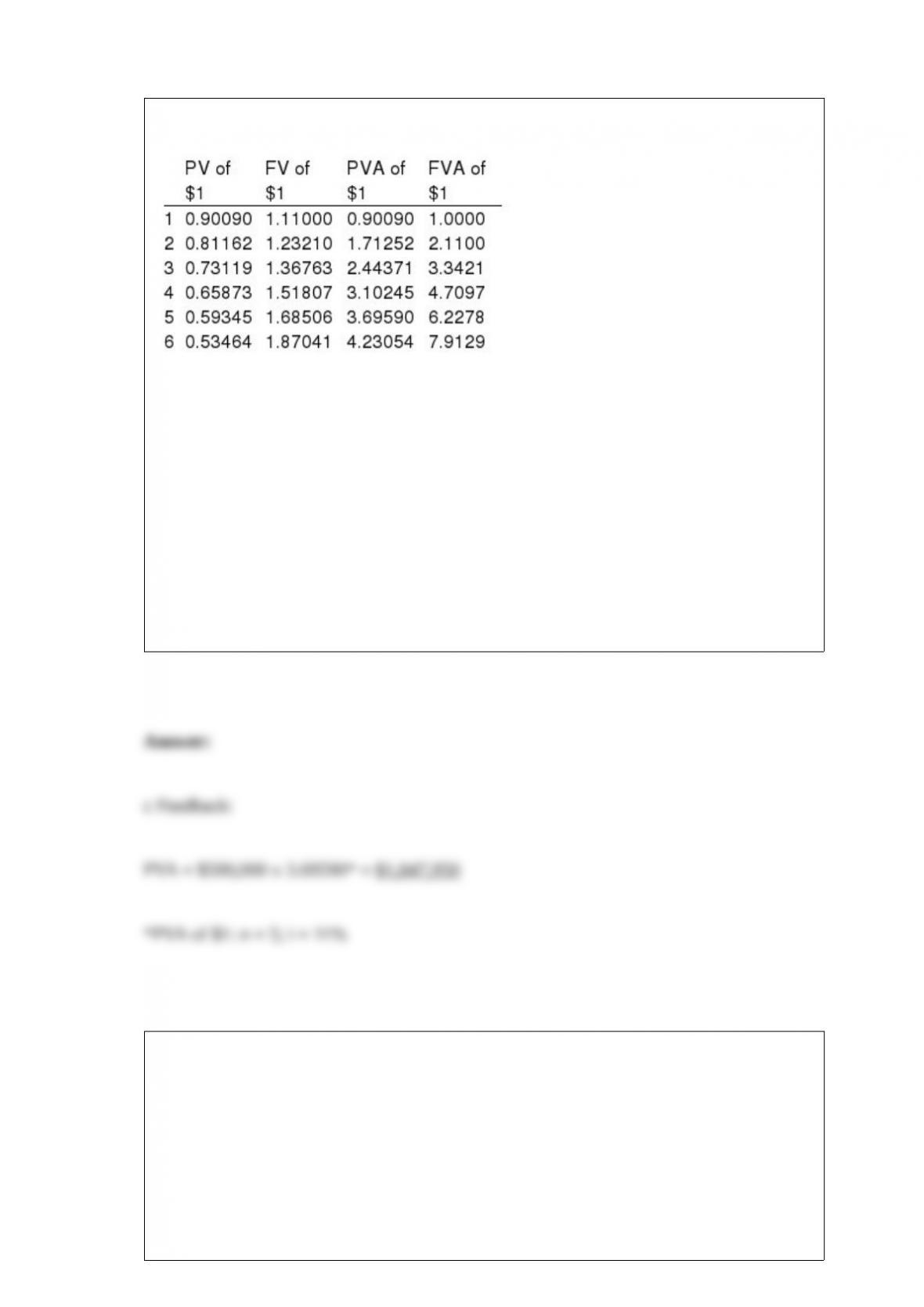

Present and future value tables of 1 at 11% are presented below.

On October 1, 2016, Justine Company purchased equipment from Napa Inc. in

exchange for a noninterest-bearing note payable in five equal annual payments of

$500,000, beginning Oct 1, 2017. Similar borrowings have carried an 11% interest rate.

The equipment would be recorded at:

a. $2,500,000.

b. $2,225,000.

c. $1,847,950.

d. $2,115,270.

ERISA made major changes in the requirements for pension plan:

a. Vesting.

b. Reporting.

c. Taxing.

d. Investing.

Recognizing expected losses immediately, but deferring expected gains, is an example

of:

a. Materiality.

b. Conservatism.

c. Cost-effectiveness.

d. Timeliness.

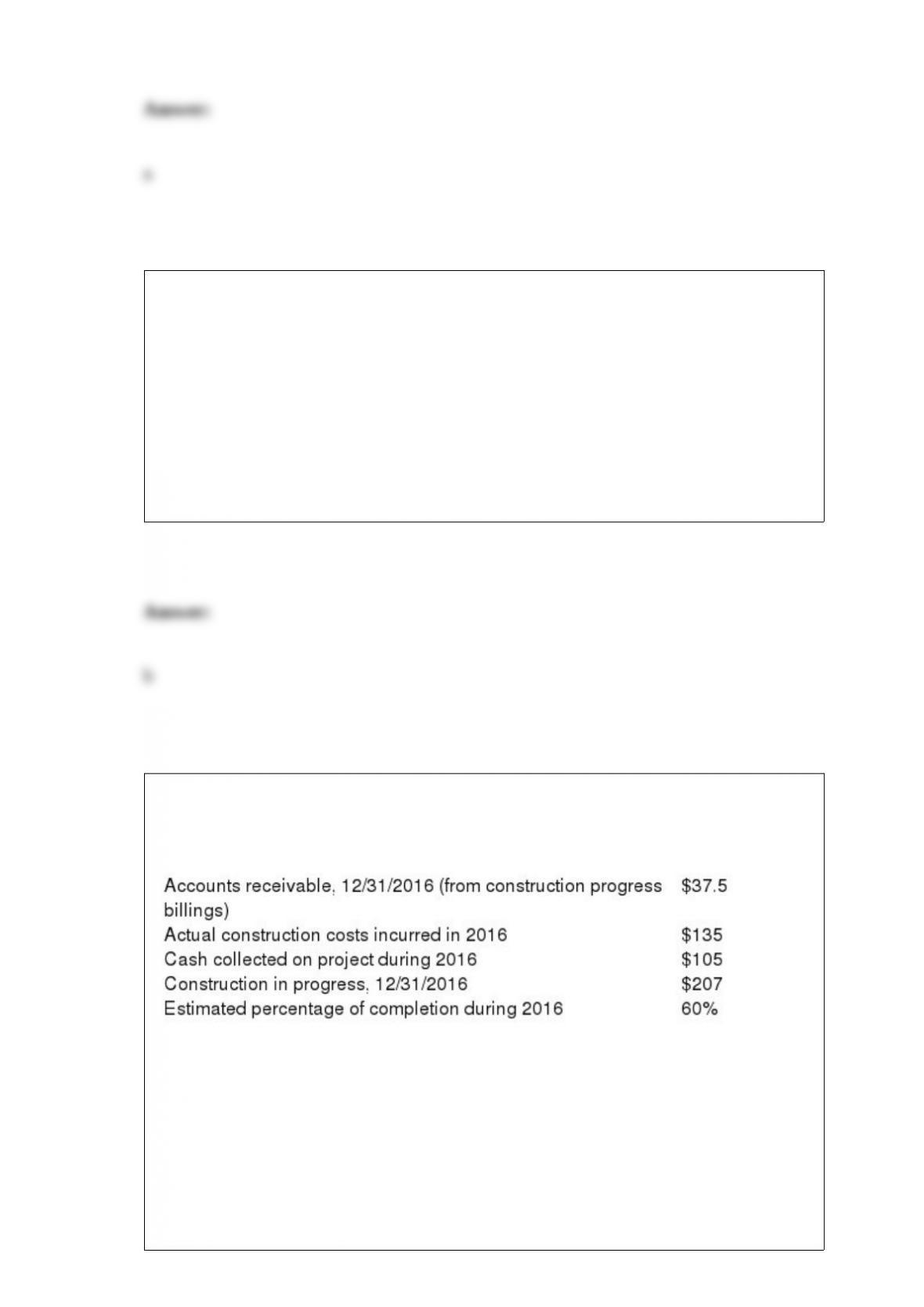

In 2016, Cupid Construction Co. (CCC) began work on a two-year fixed price contract

project. CCC recognizes revenue over time according to percentage of completion for

this contract, and provides the following information (dollars in millions):

What are CCC’s estimated remaining construction costs on the project at the end of

2016?

a. $90 million.

b. $135 million.

c. $225 million.

d. $0.

Axcel Software began a new development project in 2015. The project reached

technological feasibility on June 30, 2016, and was available for release to customers at

the beginning of 2017. Development costs incurred prior to June 30, 2016, were

$3,200,000 and costs incurred from June 30 to the product release date were

$1,400,000. The 2017 revenues from the sale of the new software were $4,000,000, and

the company anticipates additional revenues of $6,000,000. The economic life of the

software is estimated at four years. 2017 amortization of the software development

costs would be:

a. $0.

b. $ 350,000.

c. $1,840,000.

d. $ 560,000.

During the current year, High Corporation had 3 million shares of common stock

outstanding. Five thousand $1,000, 6% convertible bonds were issued at face amount at

the beginning of the year. High reported income before tax of $4 million and net

income of $2.4 million for the year. Each bond is convertible into 10 shares of common.

What is diluted EPS (rounded)?

a. $0.85.

b. $0.86.

c. $0.80.

d. $0.79.

When converting an income statement from a cash basis to an accrual basis, expenses:

a. Exceed cash payments to suppliers.

b. Equal cash payments to suppliers.

c. Are less than cash payments to suppliers.

d. May exceed or be less than cash payments to suppliers.

Portelli Services provides room-cleaning arrangements for hotels in Pennsylvania. On

April 1, Silvia Hotels & Resorts signed an agreement to outsource its room-cleaning

functions to Portelli. The contract specifies the service fee to be $15,000 per month, and

all payments are to be made shortly after the end of each quarter. It also specifies that

Portelli will receive an additional quarterly bonus of $3,000 if, during that quarter,

Silvia receives no more than five complaints from customers about room cleanliness. –

On April 1, based on historical experience, Portelli estimated that there is a 75% chance

that it will earn the quarterly bonus.

– On May 5, Portelli learned that, during March, there were two complaints from

customers related to room cleanliness. Based on this new information, Portelli revised

its estimate downward to 40% that it would earn the quarterly bonus.

– On June 30, Silvia notified Portelli that, for the quarter ended, there were four

complaints associated with room cleanliness, so Portelli would receive the bonus. Two

days later, Portelli received all payments due for all services rendered in the second

quarter, including the bonus. Portelli bases estimates of variable consideration on the

most likely amount it expects to receive.

Prepare Portelli’s April 30 journal entry to account for the revenue earned in April.

The following selected transactions relate to contingencies of Eastern Products Inc.,

which began operations in July 2016. Eastern’s fiscal year ends on December 31.

Financial statements are published in April 2017.

1> No customer accounts have been shown to be uncollectible as yet, but Eastern

estimates that 3% of credit sales will eventually prove uncollectible. Sales were $300

million (all credit) for 2016.

2> Eastern offers a one-year warranty against manufacturer’s defects for all its products.

Industry experience indicates that warranty costs will approximate 2% of sales. Actual

warranty expenditures were $3.5 million in 2016 and were recorded as warranty

expense when incurred.

3> In December 2016, Eastern became aware of an engineering flaw in a product that

poses a potential risk of injury. As a result, a product recall appears inevitable. This

move would likely cost the company $1.5 million.

4> In November 2016, the State of Vermont filed suit against Eastern, asking civil

penalties and injunctive relief for violations of clean water laws. Eastern reached a

settlement with state authorities to pay $4.2 million in penalties on February 3, 2017.

5> Eastern is the plaintiff in a $40 million lawsuit filed against a customer for costs and

lost profits from contracts rejected in 2016. The lawsuit is in final appeal and attorneys

advise that it is virtually certain that Eastern will be awarded $30 million.

Required:

Prepare the appropriate journal entries that should be recorded as a result of each of

these contingencies. If no journal entry is indicated, state why.

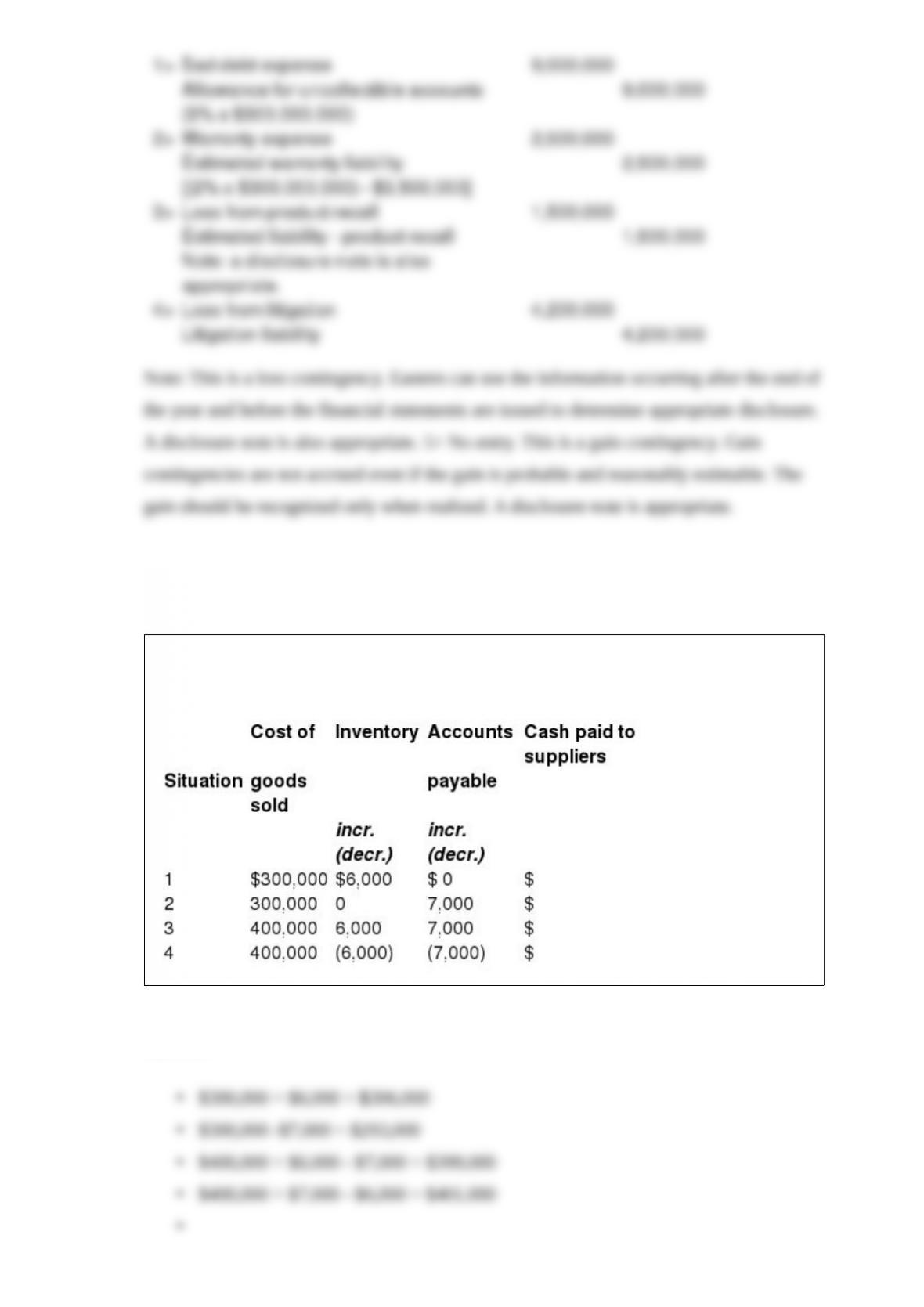

Determine the amount of cash paid to suppliers for each of the four independent

situations below.

Burns Company reported $752.4 million in net income in 2016. On January 1, 2016,

the company had 400 million shares of common stock outstanding. On March 1, 2016,

24 million new shares of common stock were sold for cash. On June 1, 2016, the

company’s common stock split 2 for 1. On July 1, 2016, 8 million shares were

reacquired as treasury stock.

Required:

Compute Burns’ basic earnings per share for the year ended December 31, 2016.

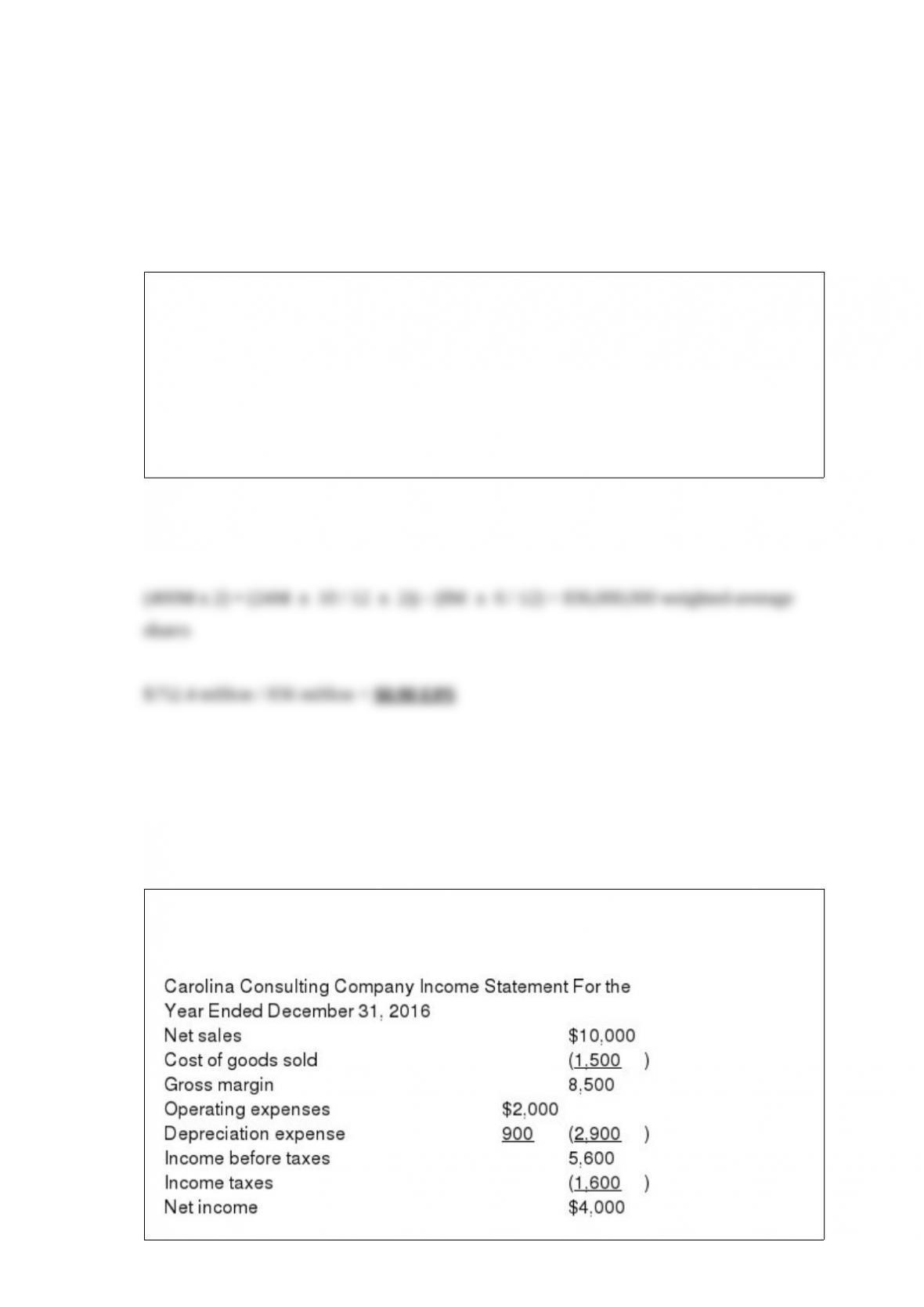

Following are the income statement and some additional information for Carolina

Consulting Company.

All sales were on credit and accounts receivable decreased by $900 in 2016 compared

to 2015. Merchandise purchases were on credit with a decrease in accounts payable of

$700 during the year. Ending inventory was $500 larger than beginning inventory.

Income taxes payable increased $300 during the year. All operating expenses were paid

for in cash.

Required:

Prepare the cash flows from operating activities section of the statement of cash flows

using the direct method.

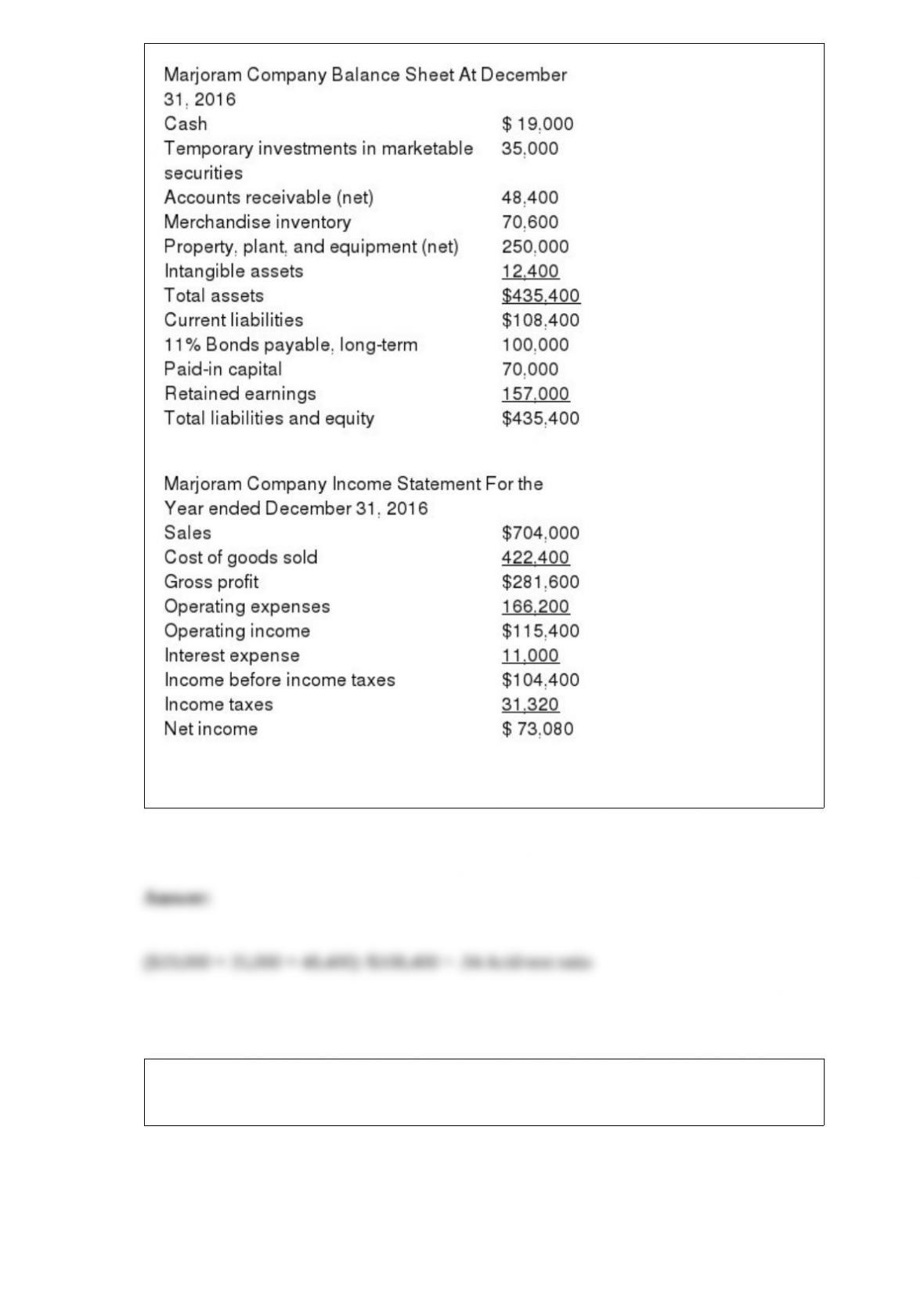

The condensed balance sheet and income statement for Marjoram Company are

presented below.

Compute the acid-test ratio for Marjoram Company. Round your answer to two decimal

places.

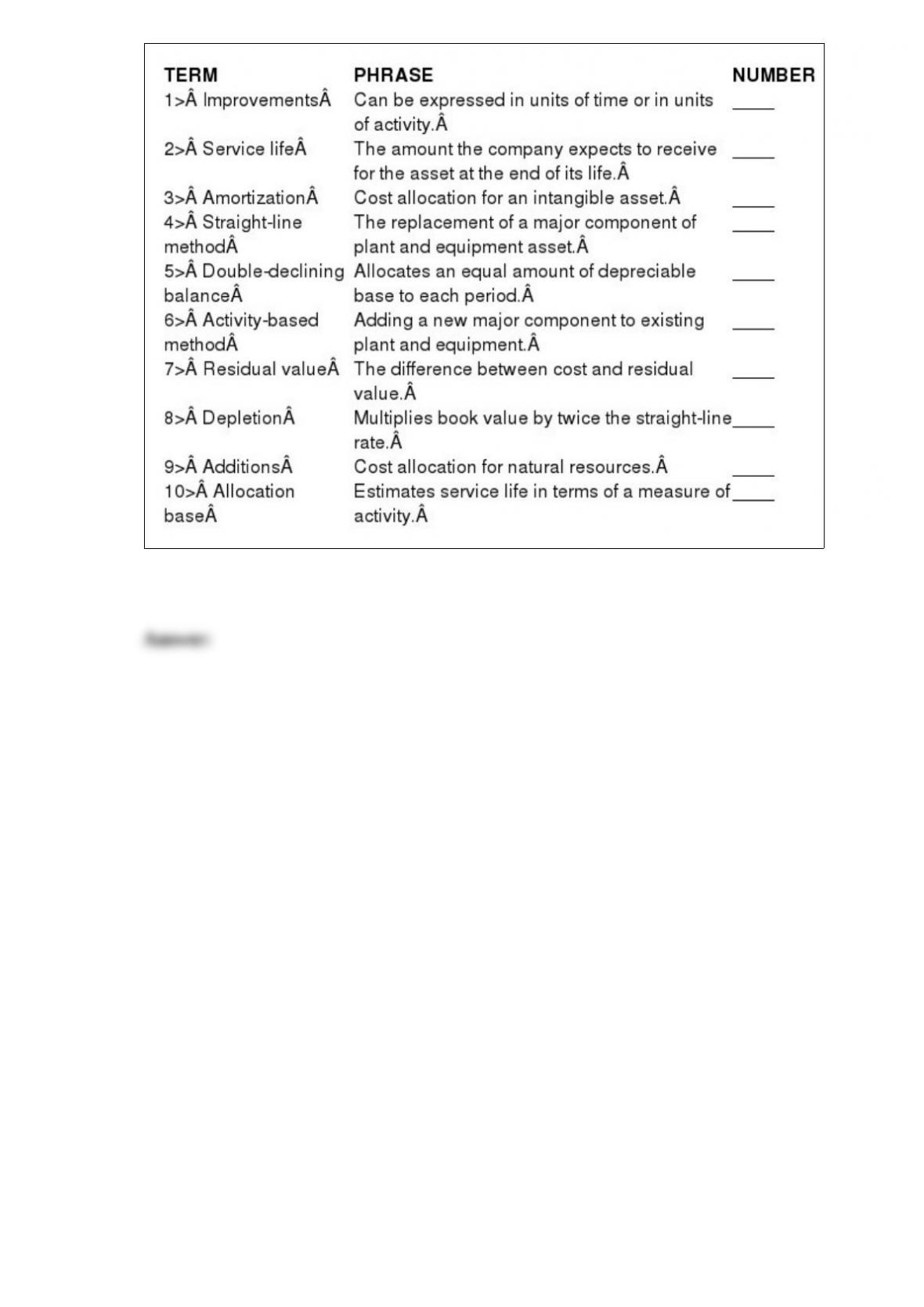

Listed below are 10 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the number for the correct term.

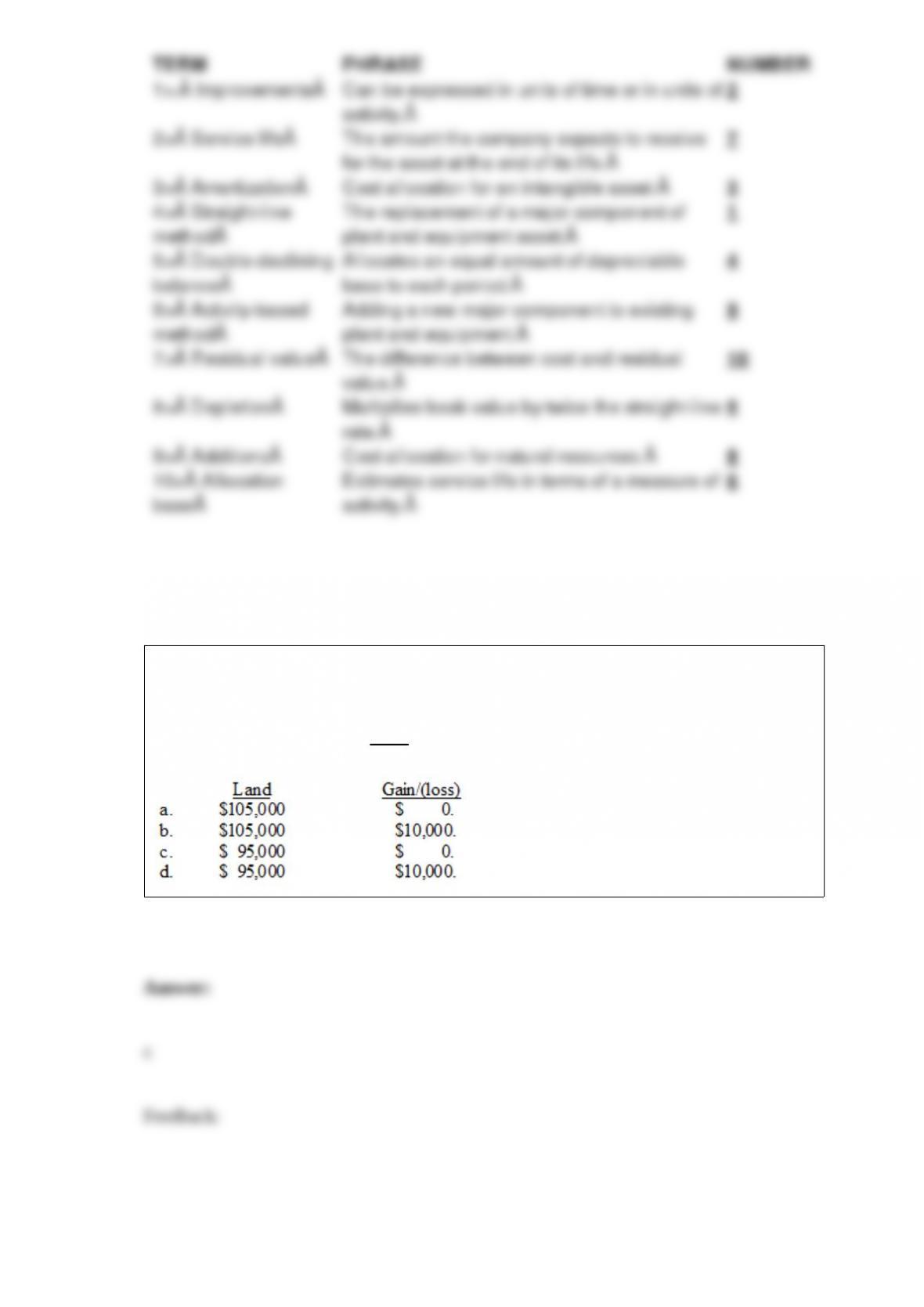

Horton Stores exchanged land and cash of $5,000 for similar land. The book value and

the fair value of the land were $90,000 and $100,000, respectively.

Assuming that the exchange lacks commercial substance, Horton would record

land-new and a gain/(loss) of: