If a stock dividend were distributed, when calculating the current year’s EPS, the shares

distributed are treated as having been issued: A. At the end of the year.

B. At the beginning of the year.

C. On the declaration date.

D. On the date of distribution.

Answer:

The shareholders’ equity of Red Corporation includes $200,000 of $1 par common

stock and $400,000 par value of 6% cumulative preferred stock. The board of directors

of Red declared cash dividends of $50,000 in 2013 after paying $20,000 cash dividends

in 2012 and $40,000 in 2011. What is the amount of dividends common shareholders

will receive in 2013? A. $18,000.

B. $22,000.

C. $26,000.

D. $28,000.

Answer:

If the fair value of a held-to-maturity investment declines for a reason that is viewed as

“other than temporary” because the company intends to sell the investment: A. The

investment is not written down to fair value.

B. The investment is written down to fair value, and the entire impairment loss is

recognized in net income.

C. The investment is written down to fair value, and the entire impairment loss is

recognized in accumulated other comprehensive income.

D. The investment is treated the same way it would be treated if the decline in fair value

was viewed as temporary.

Answer:

Listed below are 10 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term. 1)Sales returns

2)Pledging

3)Cash discount

4)Balance sheet approach

5)Compensating balance

6)Allowance method

7)Income statement approach

8)Direct write-off method

9)Without recourse

10)Accounts receivable aging schedule

A. Bad debt expense is recorded when receivables are written off

B. Reduces the amount paid by a credit customer if paid within a specified time

C. Grouping accounts receivable depending on the length of time outstanding

D. An attempt to satisfy the matching principle for bad debts

E. When merchandise is returned for credit

F. Bad debt expense determined by estimating net realizable value

G. Bad debt expense a % of credit sales.

H. An example of a restriction on cash

I. Using receivables as collateral for a loan.

J. Buyer assumes the risk of uncollectibility

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the most correct term. 1) Lessor’s minimum

lease receipts

2) Sales-type lease

3) Executory costs

4) Sale-leaseback payments

5) Lessee’s guarantee

A. Rent payments plus lessee-guaranteed and 3rd-party-guaranteed residual value

B. Residual value

C. Tax payments

D. The amount paid to retain use of the asset after sale

E. Marketing tool for lessor

Answer:

During 2013, Falwell Inc. had 500,000 shares of common stock and 50,000 shares of

6% cumulative preferred stock outstanding. The preferred stock has a par value of $100

per share. Falwell did not declare or pay any dividends during 2013.

Falwell’s net income for the year ended December 31, 2013, was $2.5 million. The

income tax rate is 40%. Falwell granted 10,000 stock options to its executives on

January 1 of this year. Each option gives its holder the right to buy 20 shares of

common stock at an exercise price of $29 per share. The options vest after one year.

The market price of the common stock averaged $30 per share during 2013.

What is Falwell’s basic earnings per share for 2013, rounded to the nearest cent? A.

$3.14.

B. $4.40.

C. $5.00.

D. None of these is correct.

Answer:

Compared to the ABO, the PBO usually is: A. Larger.

B. More reliable.

C. Less relevant.

D. More material.

Answer:

On January 1, 2013, Badger Inc. adopted the dollar-value LIFO method. The inventory

cost on this date was $100,000. The 2013 ending inventory, valued at year-end costs,

was $126,000. The relative cost index for this inventory in 2013 was 1.05.

What inventory balance should Badger report on its 12/31/13 balance sheet? A.

$126,000

B. $121,000

C. $120,000

D. $100,000

Answer:

Depreciation:A. Is always considered a period cost.

B. Could be a product cost or a period cost depending on the use of the asset.

C. Is usually based on the declining-balance method.

D. Per books is usually higher than MACRS in the early years of an asset’s life.

Answer:

Which of the following is not an indicator that the seller is a principal with respect to a

transaction? A. The seller is primarily responsible for providing the product or service

to the customer.

B. The seller’s primary role is facilitating the sale of the product or service.

C. The seller owns inventory prior to a customer ordering it and after a customer returns

it.

D. The seller has discretion in setting prices and identifying suppliers.

Answer:

On June 4, White Corporation issued $400 million of bonds for $386 million. During

the same year, $1 million of the bond discount was amortized. In a statement of cash

flows prepared by the indirect method, White Corporation should report: A. A financing

activity of $400 million.

B. An addition to net income of $1 million.

C. An investing activity of $386 million.

D. A deduction from net income of $1 million.

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Conventional retail

method

2)Replacement cost

3)Requires retrospective restatement

4)LCM

5)Additional markup

A. Markdowns are not in the calculation of the cost-to-retail percentage

B. Increase in selling price

C. Material inventory error discovered in a subsequent year

D. Losses would be recognized when values decline

E. Market if between ceiling and floor

Answer:

Red Co. recorded a residual asset of $100,000 in a 10-year lease under which no profit

was recorded at commencement by the lessor. The interest rate charged the lessee was

10%. Under the new ASU, the balance in the residual asset after two years will be: A.

$80,000.

B. $90,000.

C. $110,000.

D. $121,000.

Answer:

In the first year of an asset’s life, which of the following methods has the smallest

depreciation? A. Straight-line.

B. Declining balance.

C. Sum-of-the-years’ digits.

D. Composite or group.

Answer:

Research and development (R&D) costs: A. Generally pertain to activities that occur

prior to the start of production.

B. May be expensed or capitalized, at the option of the reporting entity.

C. Must be capitalized and amortized.

Answer:

Ludwig Company’s prepaid rent was $9,000 at December 31, 2012, and $13,000 at

December 31, 2013. Ludwig reported rent expense of $19,000 on the 2013 income

statement. What amount would be reported in the statement of cash flows as rent paid

using the direct method? A. $15,000.

B. $19,000.

C. $23,000.

D. None of the above is correct.

Answer:

Frankenstein Enterprises received two notes from customers for sales that Frankenstein

made in 2013. The notes included:

Note A: Dated 5/31/2013, principal of $120,000 and interest due 3/31/2014.

Note B: Dated 7/1/2013, principal of $200,000 and interest at 8% annually, due on

4/1/2014.

Frankenstein had accrued interest receivable from these notes of $14,400 in its

12/31/2013 balance sheet. What is the annual interest rate on Note A? A. 9.14%.

B. 8%.

C. 9.74%.

D. 9.44%.

Answer:

Compared to the accrual basis of accounting, the cash basis of accounting produces a

higher amount of income by the net decrease during the accounting period of:

A. Option a

B. Option b

C. Option c

D. Option d

Answer:

Listed below are five terms followed by a list of phrases that describe or characterize

five of the terms. Match each phrase with the correct term. 1)Percentage depletion

2)Book value

3)Rearrangements

4)Improvements

5)Date placed in service

A. Cost less accumulated depreciation

B. Triggers commencement of depreciation

C. Only used for tax purposes

D. Expenditures made to restructure an asset without addition, replacement, or

improvement

E. Three methods are employed to record these costs

Answer:

When a product or service is delivered for which a customer advance has been

previously received, the appropriate journal entry includes: A. A debit to a revenue and

a credit to a liability account.

B. A debit to a revenue and a credit to an asset account.

C. A debit to an asset and a credit to a revenue account.

D. A debit to a liability and a credit to a revenue account.

Answer:

Which of the following groups is not among financial intermediaries? A.Mutual fund

managers.

B.Financial analysts.

C.CPAs.

D.Credit rating organizations.

Answer:

Cal Farms reported supplies expense of $2,000,000 this year. The supplies account

decreased by $200,000 during the year to an ending balance of $400,000. What was the

cost of supplies the Cal Farms purchased during the year? A. $1,600,000.

B. $1,800,000.

C. $2,200,000.

D. $2,400,000.

Answer:

Flapper Jack’s Pancake Restaurants Inc. sells franchises for an initial fee of $36,000

plus operating fees of $500 per month. The initial fee covers site selection, training,

computer and accounting software, and on-site consulting and troubleshooting, as

needed, over the first five years. On March 15, 2012, Tim Cruise signed a franchise

contract, paying the standard $6,000 down with the balance due over five years with

interest.

Assuming that the initial services to be performed by Flapper Jack’s subsequent to the

signing are substantial and that collection of the receivable is reasonably assured, the

journal entry required at signing would include a credit to: A. Unearned franchise fee

revenue for $36,000.

B. Unearned franchise fee revenue for $30,000.

C. Franchise fee revenue for $36,000.

D. Franchise fee revenue for $6,000.

Answer:

Interest is eligible to be capitalized as part of an asset’s cost, rather than being expensed

immediately, when:A. The interest is incurred during the construction period of the

asset.

B. The asset is a discrete construction project for sale or lease.

C. The asset is self-constructed, rather than acquired.

D. All of the above are correct.

Answer:

A change in the estimated useful life and residual value of machinery in the current year

is handled as: A. A retrospective change back to the date of acquisition as though the

current estimated life and residual value had been used all along.

B. A prospective change from the current year through the remainder of its useful life,

using the new estimates.

C. A cumulative adjustment to income in the current year for the difference in

depreciation under the new versus old estimates.

D. None of the above is correct.

Answer:

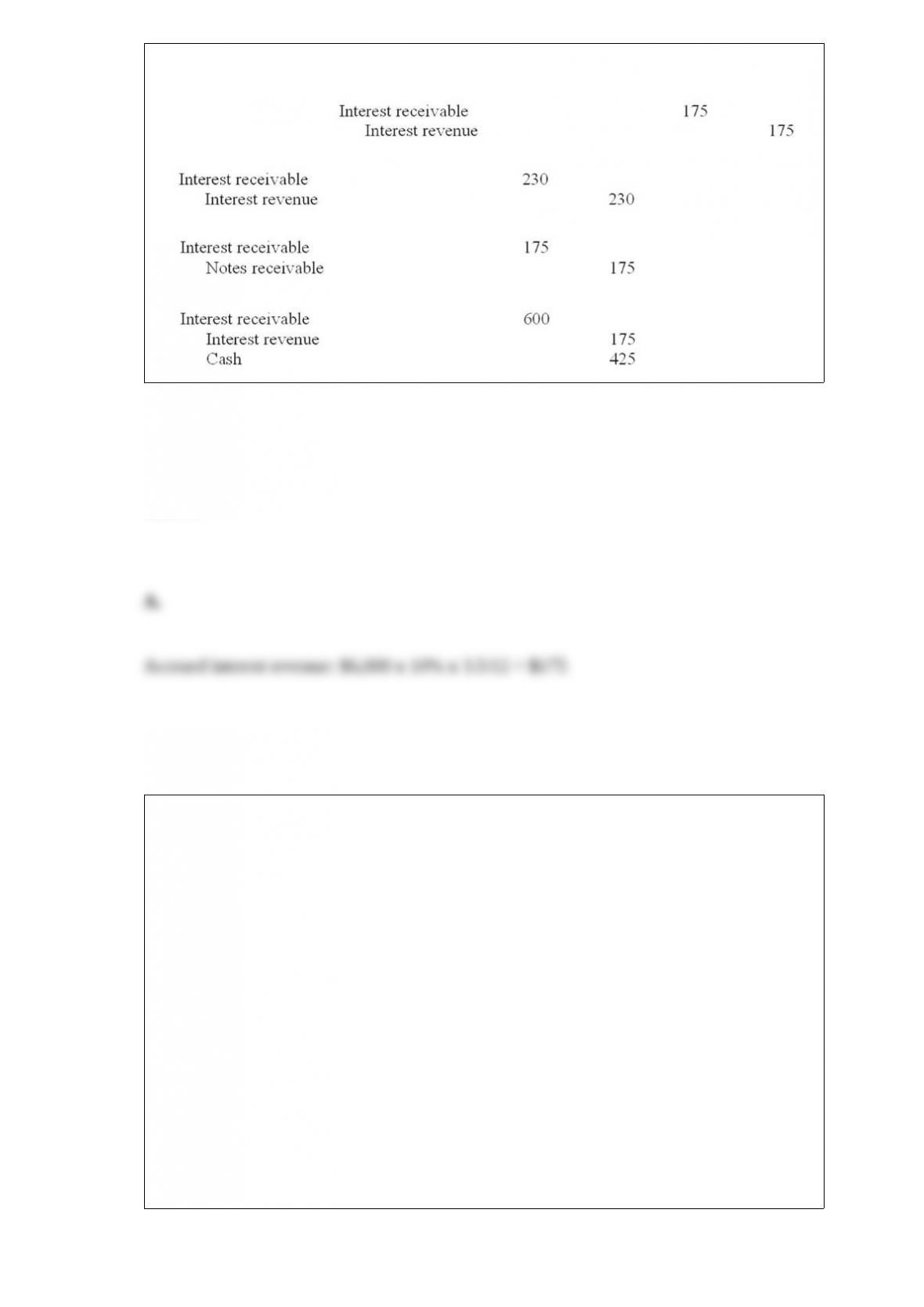

On September 15, 2013, Oliver’s Mortuary received a $6,000, nine-month note bearing

interest at an annual rate of 10% from the estate of Jay Hendrix for services rendered.

Oliver’s has a December 31 year-end. What adjusting entry will the company record on

December 31, 2013? A.

B.

C.

D.

Answer:

On October 28, 2013, Mercedes Company committed to a plan to sell a division that

qualified as a component of the entity according to GAAP regarding discontinued

operations and was properly classified as held for sale on December 31, 2013, the end

of the company’s fiscal year. The division’s loss from operations for 2013 was

$2,000,000.

The division’s book value and fair value less cost to sell on December 31 were

$3,000,000 and $2,500,000, respectively. What before-tax amount(s) should Mercedes

report as loss on discontinued operations in its 2013 income statement? A. $2,000,000

loss.

B. $2,500,000 loss.

C. None.

D. $500,000 impairment loss included in continuing operations and a $2,000,000 loss

from discontinued operations.

Answer:

What is the effect of the error on Berkshire’s 12/31/2013 balance sheet? A. There are no

errors in the 12/31/2013 balance sheet.

B. Assets understated by $600,000 and shareholders’ equity understated by $600,000.

C. Assets understated by $420,000 and shareholders’ equity understated by $420,000.

D. Liabilities understated by $180,000 and shareholders’ equity overstated by $420,000.

Answer:

Grab Manufacturing Co. purchased a 10-ton draw press at a cost of $180,000 with

terms of 5/15, n/45. Payment was made within the discount period. Shipping costs were

$4,600, which included $200 for insurance in transit. Installation costs totaled $12,000,

which included $4,000 for taking out a section of a wall and rebuilding it because the

press was too large for the doorway. The capitalized cost of the 10-ton draw press is: A.

$171,000.

B. $183,600.

C. $187,600.

D. $185,760.

Answer:

XYZ Company leased equipment to West Corporation under a lease agreement that

qualifies as a capital lease to West but not as a result of a bargain purchase option or a

title transfer. The present value of the asset is $600,000. The expected economic life of

the asset is 10 years. The lease term is five years. Using the straight-line method, what

would West record as annual depreciation? A. $120,000.

B. $61,000.

C. $60,000.

D. $0.

Answer:

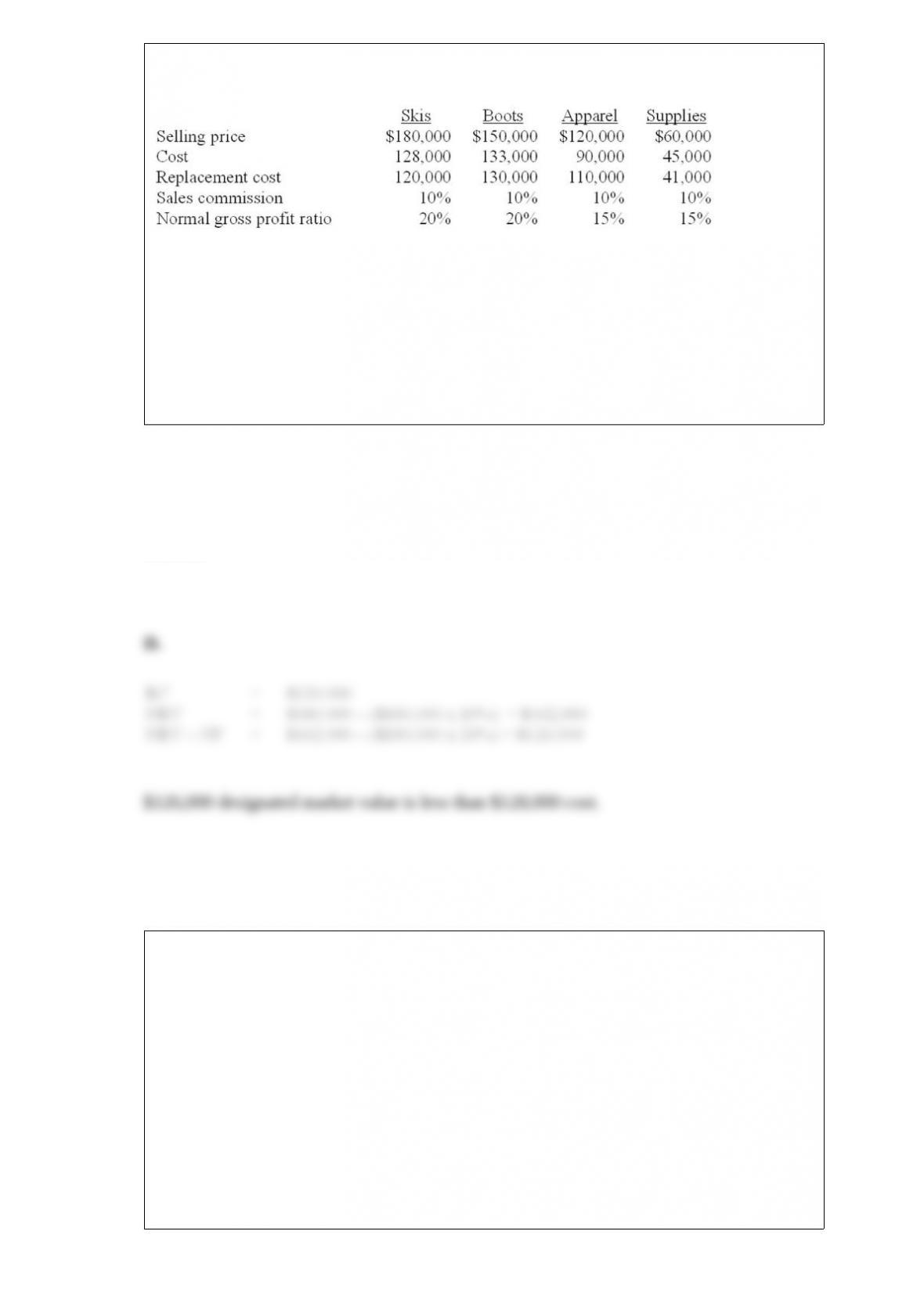

Data related to the inventories of Alpine Ski Equipment and Supplies is presented

below:

In applying the LCM rule, the inventory of skis would be valued at: A. $162,000.

B. $128,000.

C. $120,000.

D. $126,000.

Answer:

Carla Salons leased equipment from SmithCo on July 1, 2013. The present value of the

lease payments discounted at 10% was $80,000. Ten annual lease payments of $12,000

are due at the beginning of each fiscal year beginning July 1, 2013. SmithCo had

constructed the equipment recently for $66,000, and its retail fair value was $100,000.

Following the guidance of the new ASU, the total increase in earnings (pretax) in

SmithCo’s December 31, 2013 income statement would be: A. $27,200.

B. $30,600.

C. $31,600.

D. $31,860.

Answer:

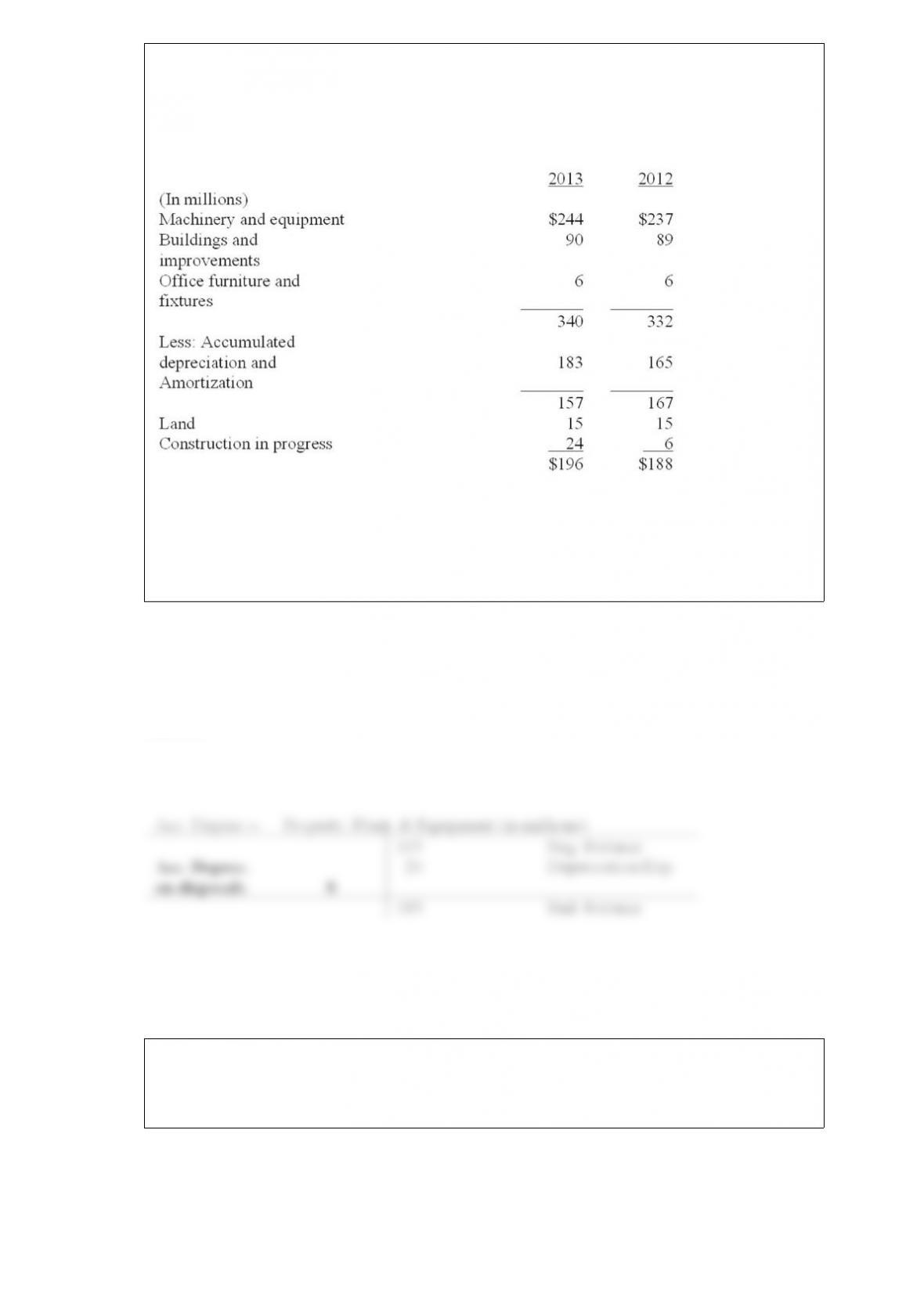

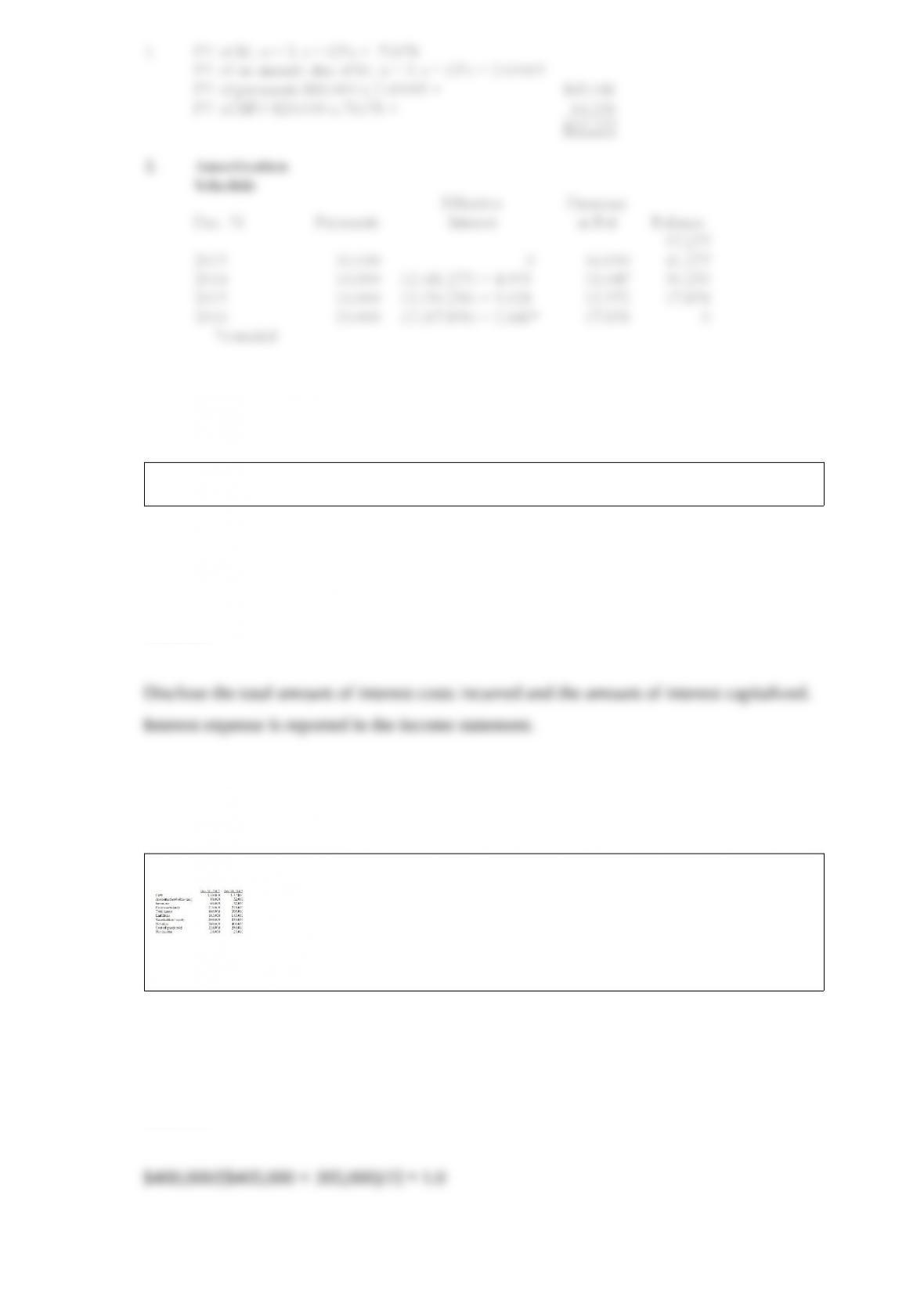

In its 2013 annual report to shareholders, Custard Cup Inc. disclosed the following

footnote:

Note 4 Property, Plant, and Equipment

Property, plant, and equipment (PPE) at December 31, 2013, and December 31, 2012,

consisted of the following:

Depreciation expense for property, plant and equipment was $26 million in

Required:

Compute the Accumulated depreciation on PPE disposed of by Custard Cup during

Answer:

What provisions did the Public Company Accounting Reform and Investor Protection

(Sarbanes-Oxley) Act of 2002 make for performance of nonaudit services by an audit

firm?

Answer:

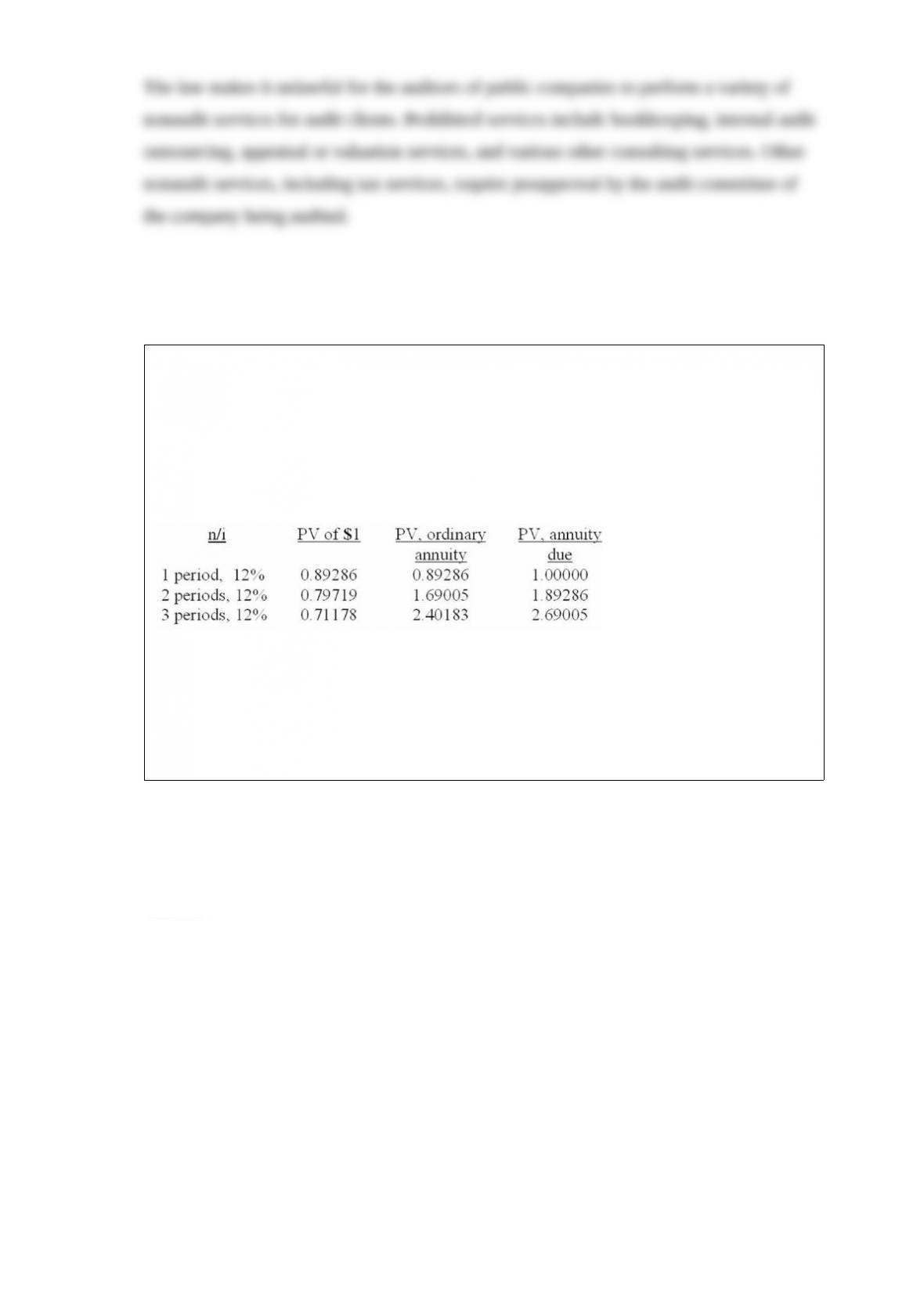

Rumsfeld Corporation leased a machine on December 31, 2013, for a three-year period.

The lease agreement calls for annual payments in the amount of $16,000 on December

31 of each year beginning on December 31, Rumsfeld has the option to purchase the

machine on December 31, 2016, for $20,000 when its fair value is expected to be

$30,000. The machine’s estimated useful life is expected to be five years with no

residual value. Rumsfeld uses straight-line depreciation for this type of machinery. The

appropriate interest rate for this lease is 12%.

Required:

1) Calculate the amount to be recorded as a leased asset and the associated lease

liability.

2) Prepare an amortization schedule for this lease.

Answer:

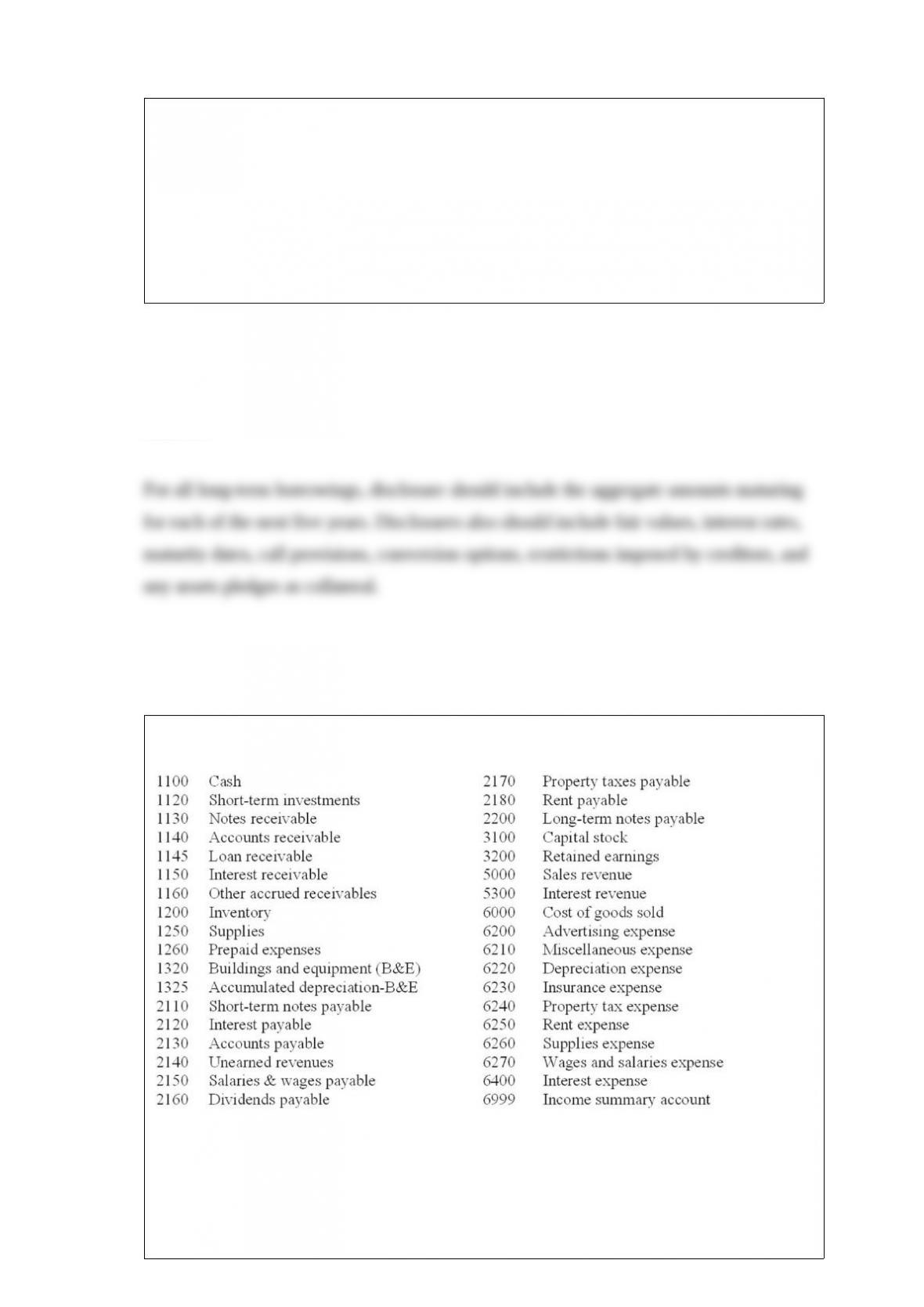

What disclosures are required relative to interest costs incurred during the year?

Answer:

Missoula Inc. reported the following selected financial statement data:

Required: Compute the asset turnover ratio for 2013.

Answer:

A disclosure note in the annual financial statements of Macy’s Inc. for the fiscal year

ended January 31, 2013, included the following:

“Future maturities of long-term debt, other than capitalized leases and premium on

acquired debt, are shown below:”

For how many years subsequent to the current year must Macy’s report these amounts?

Name at least two other items that must be disclosed for a company’s long-term debt.

Answer:

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Declared cash dividends on common stock.

Answer:

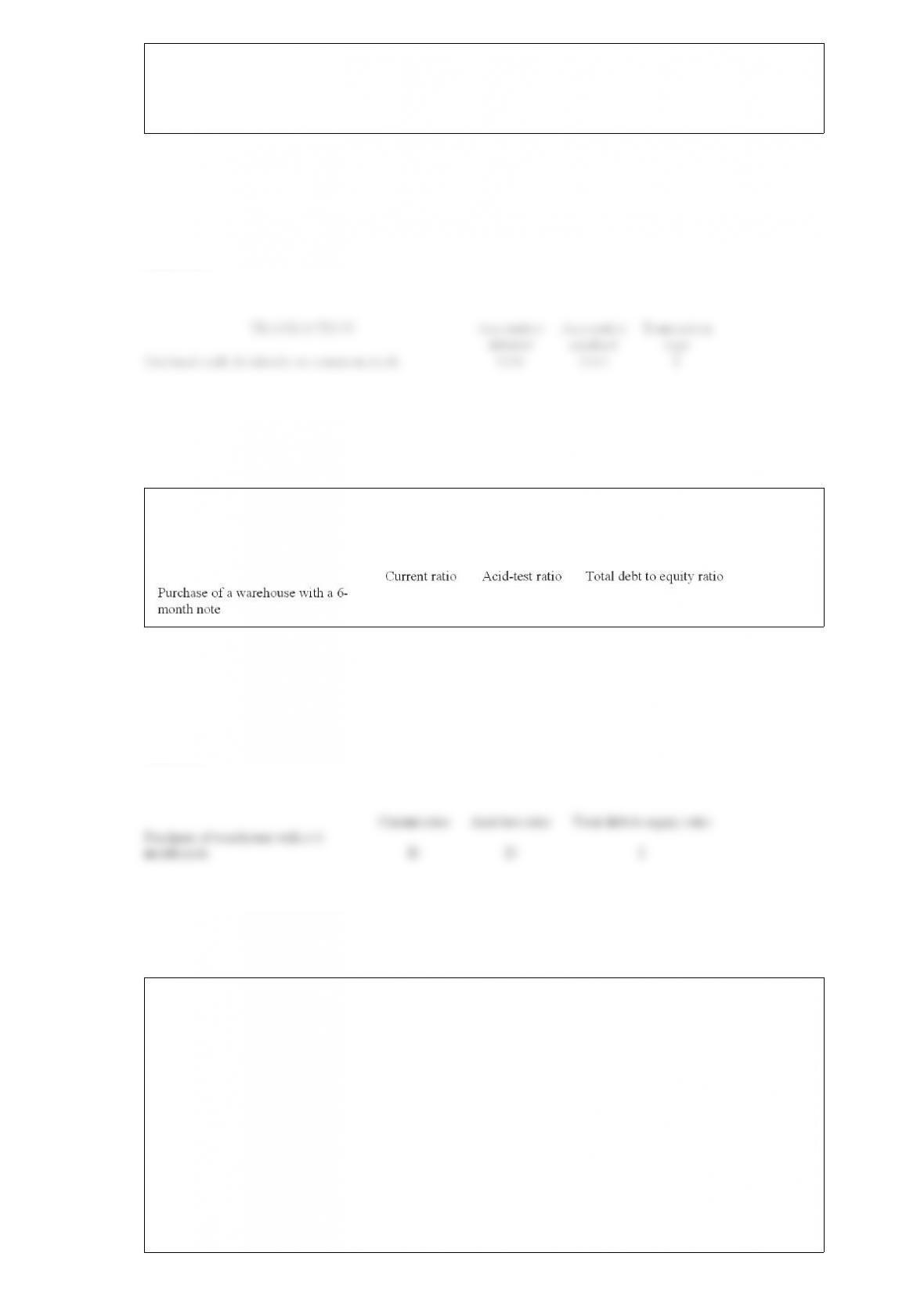

Indicate whether each of the actions listed below will immediately increase (I), decrease

(D), or have no effect (N) on the ratios shown. Assume each ratio is greater than 1.0

before the action is taken.

Answer:

The Peach Corporation provides restricted stock to certain executives. Under the plan,

the company granted 30 million shares on January 1, 2013, which vest in four years.

The fair value of the shares is $14. No forfeitures are anticipated. Ignore taxes.

Required:

1) Determine the total compensation cost pertaining to the restricted stock.

2) Prepare the appropriate journal entry (if any) to record the award of restricted stock

on January 1, 2013.

3) Prepare the appropriate journal entry (if any) to record compensation expense on

December 31, 2013.

Answer:

Hammerstein Corporation offers a variety of share-based compensation plans to

employees. Under its restricted stock award plan, the company, on January 1, 2013,

granted 2 million of its $1 par common shares to various division managers. The shares

are subject to forfeiture if employment is terminated within four years. The common

shares have a market price of $20 per share on the award date.

Required:

(1) Determine the total compensation cost from these restricted shares.

(2) Prepare the appropriate journal entry to record the award on January 1, 2013.

(3) Prepare the appropriate journal entry to record compensation expense on December

31, 2013.

(4) Suppose a 15% forfeiture rate was expected prior to vesting. Determine the total

compensation cost, assuming the company follows the fair value approach and chooses

to anticipate forfeitures at the grant date.

Answer:

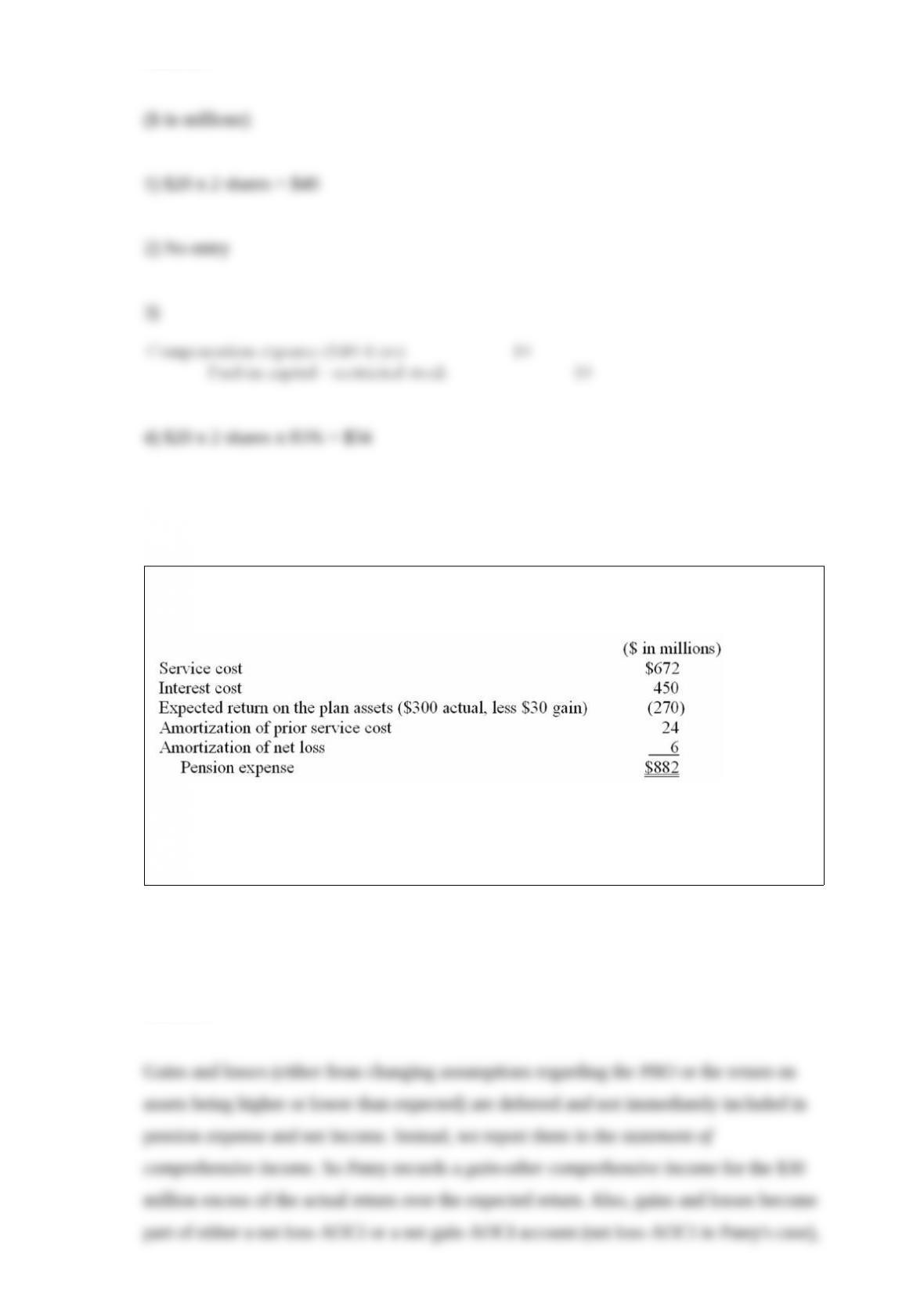

Patey Technologies calculated pension expense for its underfunded pension plan as

follows:

Required:

What is the effect of the components of pension expense on Patey’s statement of

comprehensive income?

Answer:

How are accounting errors treated?

Answer:

Use I = Increase, D = Decrease, or N = No effect, to indicate the effect on total

shareholders’ equity for each of the listed transactions.

____ A net loss for the year.

____ A stock split effected in the form of a stock dividend.

____ A stock split in which the par per share is reduced (but not effected in the form of

a stock dividend).

____ Declaration of a 5% stock dividend.

____ Declaration of a cash dividend.

____ Issue stock for noncash assets.

____ Payment of previously declared cash dividend.

____ Retirement of common stock at a cost greater than the original issue price.

____ Retirement of common stock at a cost less than the original issue price.

____ Resale of treasury stock for less than carrying value.

Answer:

DCL Industries purchased a supply of mechanical components from E Corporation on

November 1, 2013. In payment for the $48,000 purchase, DCL issued a one-year

installment note to be paid in equal monthly payments at the end of each month. The

payments include interest at the rate of 12%.

Required:

1) Prepare the journal entry for DCL’s purchase of the components on November 1,

2013.

2) Prepare the journal entry for the first installment payment on November 30, 2013.

3) What is the amount of interest expense that DCL will report in its income statement

for the year ended December 31, 2013?

Answer:

Many high-tech companies sell products with the opportunity for retailers to return the

merchandise if it is unsold after a certain period. This reduces the retailer’s risk of

inventory obsolescence. Explain the implications on revenue recognition under this

kind of policy. Include a specific example.

Answer:

On January 1, 2013, Wildcat Company purchased $93,000 of 10% bonds at face value.

The bonds are to be held to maturity. The bonds pay interest semiannually on January 1

and July 1.

Required:

(1) Prepare the appropriate journal entry to record the acquisition of the bonds.

(2) Record the first two interest payments (ignore year-end accruals).

Answer:

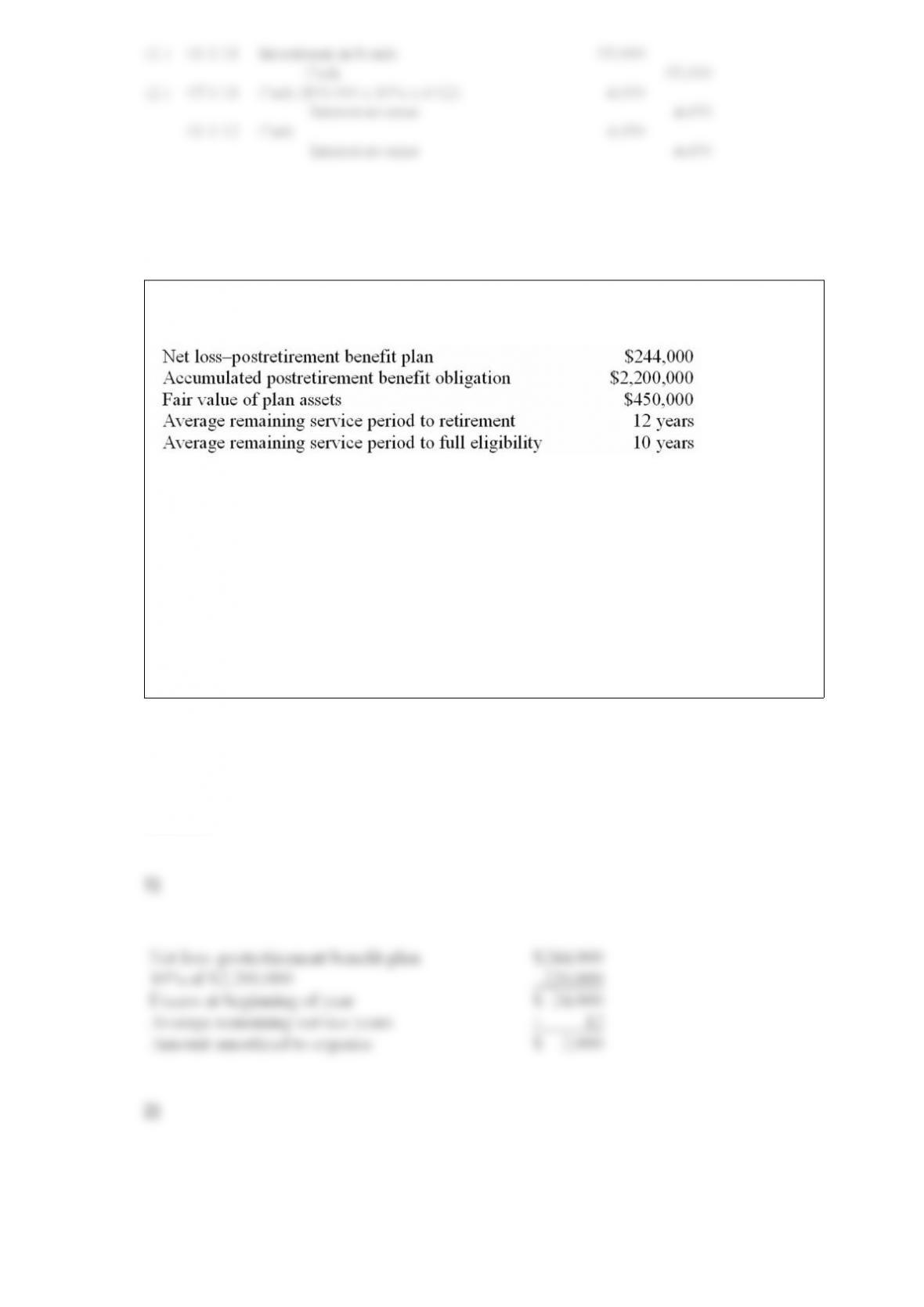

Bazerman Inc. has a postretirement health care benefit plan. On January 1 of the current

calendar year, the following plan-related data were available.

The rate of return on plan assets during the year was 12%. The expected return was

10%. The actuary revised assumptions regarding the APBO at the end of the year,

resulting in a $42,000 increase in the estimate of the obligation.

Required:

1) Calculate any amortization of net loss that should be included as a component of

postretirement benefit expense for the current year.

2) Determine the net loss or gain as of December 31 of the current year.

Answer:

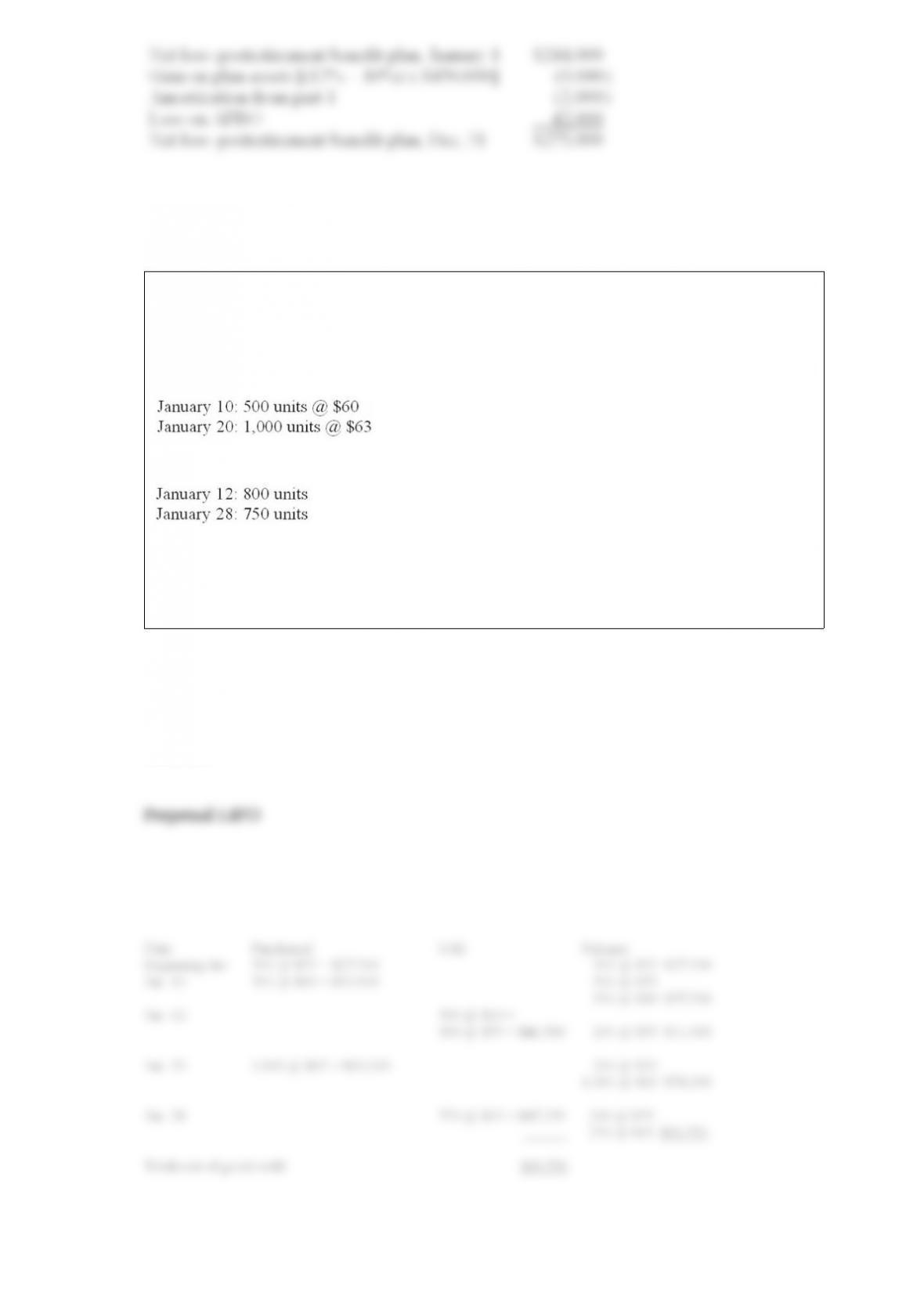

Shown below is activity for one of the products of Denver Office Equipment:

January 1 balance, 500 units @ $55 $27,500

Purchases:

Sales:

Required:

Compute the January 31 ending inventory and cost of goods sold for January, assuming

Denver uses LIFO and a perpetual inventory system.

Answer:

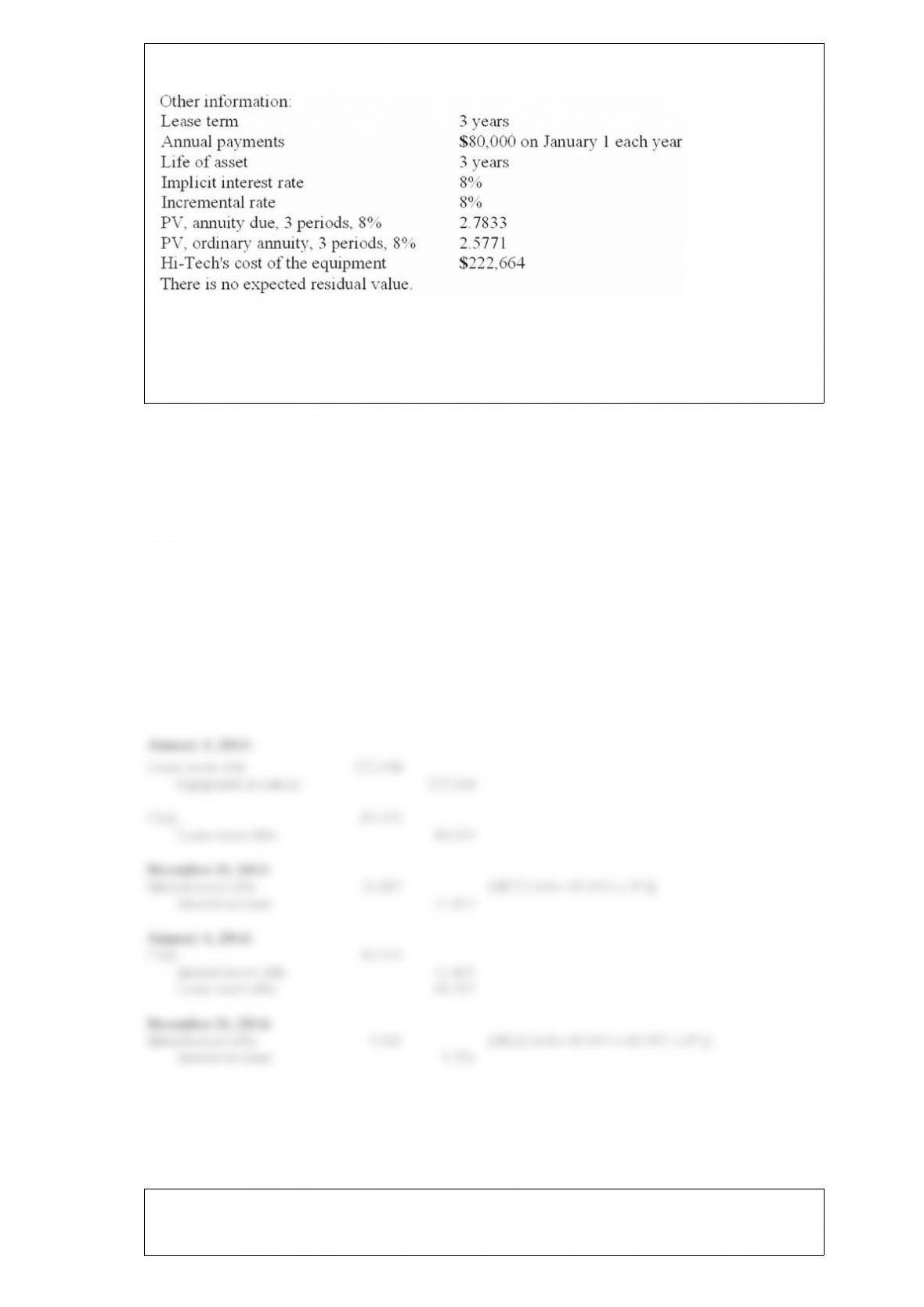

Eastern Edison Company leased equipment from Hi-Tech Leasing on January 1,

Required:

Prepare appropriate journal entries for Hi-Tech Leasing for 2013 and 2014. Assume a

December 31 year-end.

Answer:

On January 1, 2013, Morton Sales Co. issued zero-coupon bonds with a face value of

$6 million for cash. The bonds mature in 10 years and were issued at a price of

$3,050,100. Required:

What will Morton Sales Co. report on these bonds in its December 31, 2013, balance

sheet?

Answer: