The budgeting process is used to effectively communicate planned expectations

regarding profits and expenses to the entire organization.

a. True

b. False

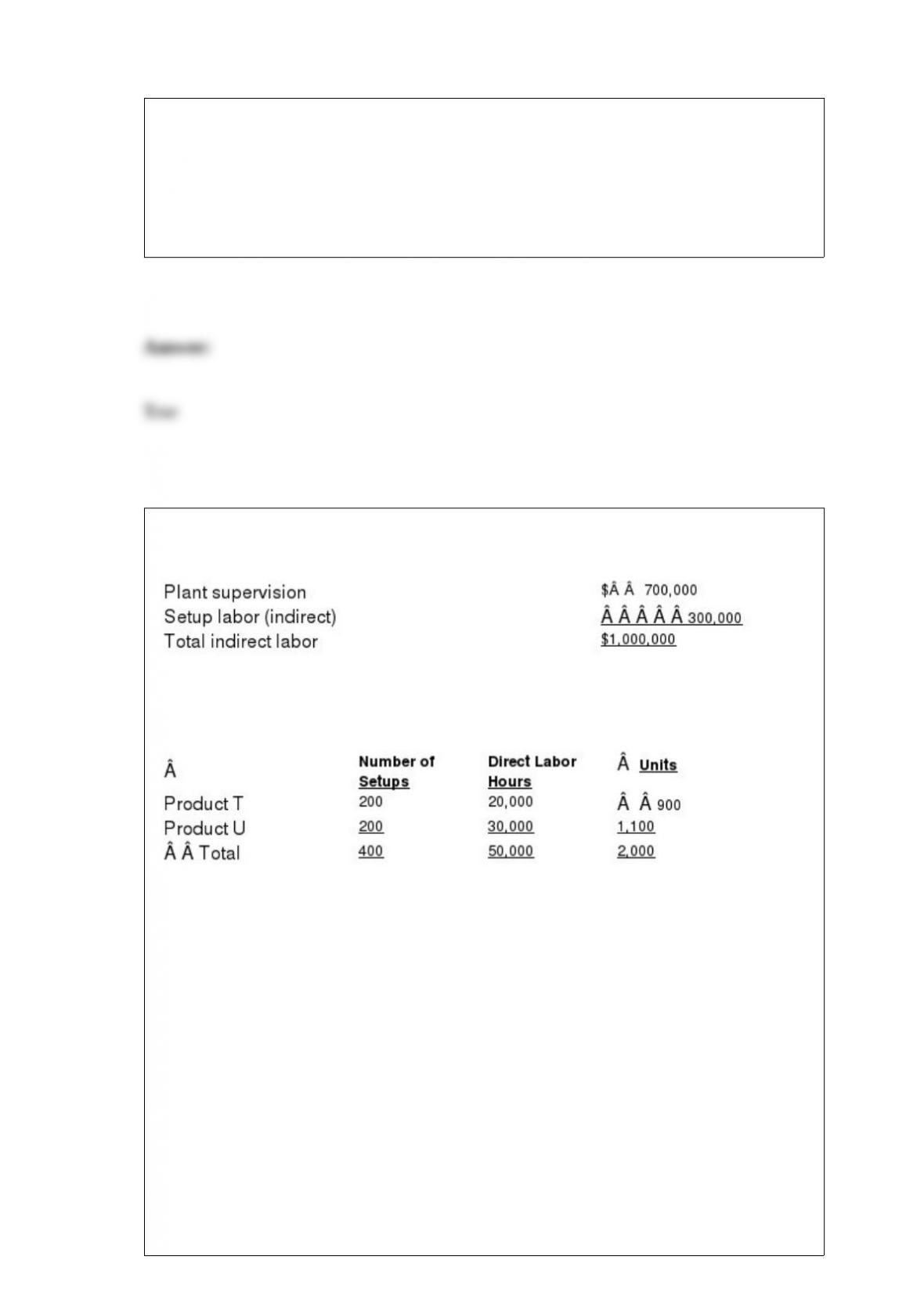

Tulip Company produces two products, T and U. The indirect labor costs include the

following two items:

The following activity-base usage and unit production information is available for the

two products:

(a) Determine the single plantwide factory overhead rate, using direct labor hours as the

activity base.

(b) Determine the factory overhead cost per unit for Products T and U, using the single

plantwide factory overhead rate.

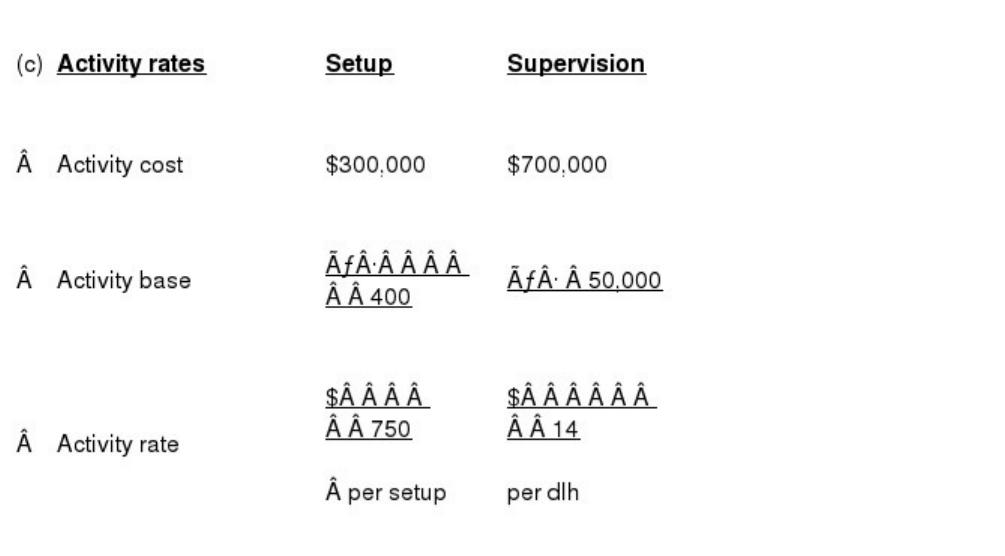

(c) Determine the activity rate for plant supervision and setup labor, assuming that the

activity base for supervision is direct labor hours and the activity base for setup labor is

number of setups.

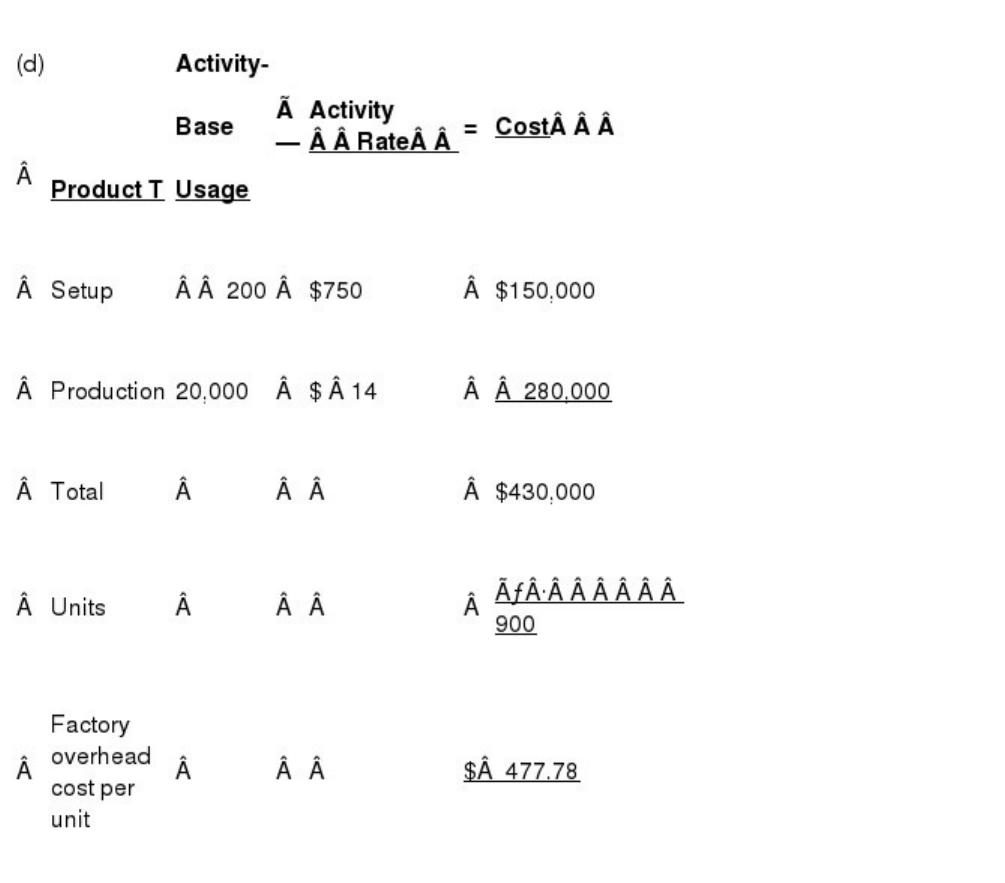

(d) Determine the factory overhead cost per unit for Products T and U, using

activity-based costing.

(e) Why is the factory overhead cost per unit different for the two products under the

two methods?

(Actual price ‘“ Standard price) × Actual quantity

Match the following formulas or descriptions with the term (a-e) it defines.

a. Direct materials price variance

b. Direct labor rate variance

c. Direct labor time variance

d. Direct materials quantity variance

e. Budgeted variable factory overhead

A responsibility center in which the department manager is responsible for costs,

revenues, and assets for a department is called:

a. a cost center

b. a profit center

c. an operating center

d. an investment center

Finished goods inventory is reported on the

a. income statement as a period cost

b. balance sheet as a long-term asset

c. balance sheet as a current asset

d. income statement as revenue

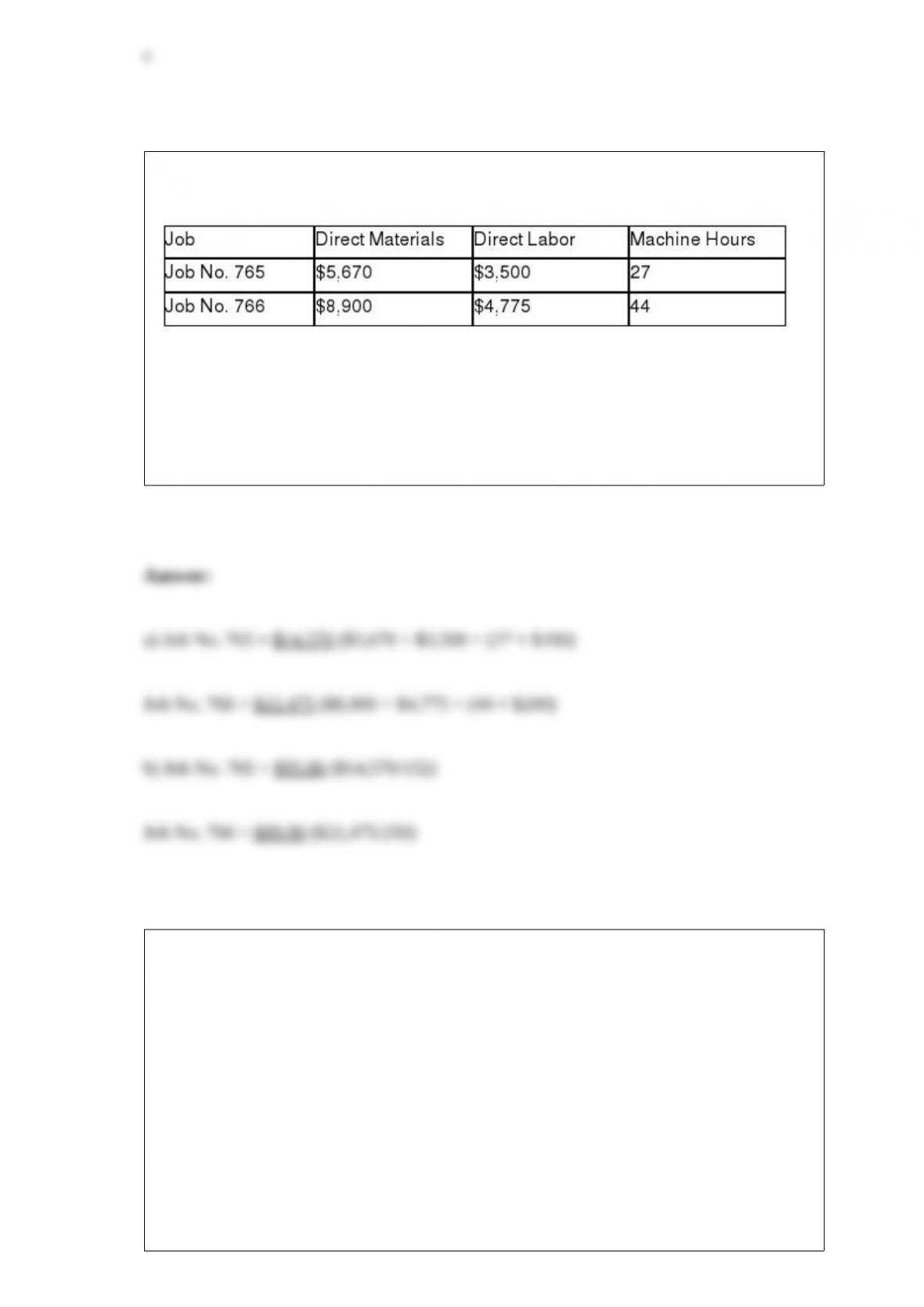

At the end of April, Cavy Company had completed Jobs 766 and 765. The individual

job cost sheets reveal the following information:

Job 765 produced 152 units, and Job 766 consisted of 250 units.

Assuming that the predetermined overhead rate is applied by using machine hours at a

rate of $200 per hour, determine the (a) balance on the job cost sheets for each job, and

(b) the cost per unit at the end of April.

At the beginning of the period, the Cutting Department budgeted direct labor of

$155,000, direct materials of $165,000, and fixed factory overhead of $15,000 for 9,000

hours of production. The department actually completed 10,000 hours of production.

What is the appropriate total budget for the department, assuming it uses flexible

budgeting?

a. $416,000

b. $370,556

c. $368,889

d. $335,000

Which of the following is most associated with managerial accounting?

a. must follow GAAP

b. may rely on estimates and forecasts

c. is prepared for users outside the organization.

d. always reports on the entire entity

A manufacturing company applies factory overhead based on direct labor hours. At the

beginning of the year, it estimated that factory overhead costs would be $360,000 and

direct labor hours would be 30,000. Actual manufacturing overhead costs incurred were

$377,200, and actual direct labor hours were 36,000. The entry to apply the factory

overhead costs for the year would include a

a. debit to factory overhead for $360,000

b. credit to factory overhead for $432,000

c. debit to factory overhead for $377,200

d. credit to factory overhead for $360,000

Investment turnover (as used in determining the rate of return on investment) focuses

on the rate of profit earned on each sales dollar.

a. True

b. False

Required by generally accepted accounting principles.

Match each phrase that follows with the term (a-c) it describes.

a. Absorption costing only

b. Variable costing only

c. Both absorption and variable costing

FastÂFlow Paints produces mixer base paint through a two’“stage process, Mixing and

Packaging. The following events depict the movement of value into and out of

production. Journalize each event if appropriate; if not, provide a short narrative reason

as to why you choose not to journalize the action. Nelson, the production manager,

accepts an order to continue processing the current run of mixer base paint.

(a) Materials worth $27,000.00 are withdrawn from raw materials inventory. Of this

amount, $25,500.00 will be issued to the Mixing Department and the balance will be

issued to the Maintenance Department to be used on production line machines.

(b) Nelson calculates that labor for the period is $12,500.00. Of this amount, $1,750.00

is for maintenance and indirect labor. The remainder is directly associated with mixing.

(c) Nelson, who is paid a salary but earns about $35.00/hour, spends 1 hour inspecting

the production line.

(d) The manufacturing overhead drivers for mixing are hours of mixer time at $575.00

per hour, and material movements from materials at $125.00 per movement. An

inspection of the machine timers reveals that a total of 8 hours has been consumed in

making this product. An inspection of ‘stocking orders” indicates that only one material

movement was utilized to load the raw materials. (Note: All values have been

journalized to Factory Overhead, you need only apply them to the production run.)

(e) Within Fast-Flow, items are transferred between departments at a standard cost. This

production run has created 4,015 gallons of mixer base paint. This paint is transferred to

Packaging at a standard cost of $10.05 per gallon. (Round calculation to nearest whole

dollar.)

(f) Packaging draws $755.00 of materials for packaging of this production run.

(g) Packaging documents that 12 hours of direct labor at $10.25 per hour were

consumed in the packaging of this production run.

(h) Packaging uses a cost driver of direct labor hours to allocate manufacturing

overhead at the rate of $25.00 per hour.

(i) Packaging transfers 4,015 gallons of packaged goods to Finished Goods Inventory at

a standard cost of $10.34 per gallon. (Round calculation to nearest whole dollar.)

In computing the ratio of sales to assets, long-term investments are excluded from

average total assets.

a. True

b. False

The methods of evaluating capital investment proposals can be grouped into two

general categories that can be referred to as (1) methods that ignore present value and

(2) present values methods.

a. True

b. False

Activity rates are determined by

a. dividing the actual cost for each activity pool by the actual activity base for that pool.

b. dividing the cost budgeted for each activity pool by the estimated activity base for

that pool.

c. dividing the actual cost for each activity pool by the estimated activity base for that

pool.

d. dividing the cost budgeted for each activity pool by the actual activity base in that

pool.

Which of the following is a method of analyzing capital investment proposals that

ignores present value?

a. internal rate of return

b. net present value

c. discounted cash flow

d. average rate of return

For a period during which the quantity of product manufactured was less than the

quantity sold, income from operations reported under absorption costing will be larger

than income from operations reported under variable costing.

a. True

b. False

Identify the following costs as (a) prime cost, (b) conversion cost, or (c) both for a cake

factory.

1) Frosting

2) Wages of the baker

3) Sprinkles for the topping (considered an indirect material)

4) Depreciation on oven