A business that has inventory items that are ordinarily interchangeable may use either

the FIFO or moving weighted average methods to assign costs to inventory.

An expense account is normally closed by debiting Income Summary and crediting the

expense account.

The principles of internal control include: ensure transactions and activities are

authorized, maintain records, insure assets, separate recordkeeping and custody of

assets, and perform internal and external audits.

Increases in liabilities are recorded as debits.

The entry to record a cash receipt from a customer when the service to be provided to

earn the cash has not yet been performed involves a debit to an unearned revenue

account.

Good internal control procedures for cash receipts imply that cash receipts by mail

should be opened by an accounting employee who is responsible for recording and

depositing receipts.

Both the accrual basis and the cash basis of accounting increase the comparability of

financial statement information from period to period.

The materiality principle is justification for using the direct-write-off method.

The 12 consecutive months (or 52 weeks) selected as an organization’s accounting

period is called the fiscal year.

The income statement is a financial statement that shows revenues earned and expenses

incurred by a business over a specified period of time.

Financial statements can be prepared directly from the information in the adjusted trial

balance.

The use of an allowance for bad debts is required under the materiality principle.

A bank reconciliation explains the difference between the balance of a chequing

account on the customer’s books and the balance on the bank statement.

Since the revenue recognition principle requires that revenues be earned, there is no

such thing as unearned revenues in accounting.

If an error is discovered in either the journal or the ledger, it must be corrected by

erasing the incorrect amount and entering the corrected amount.

A company that is currently in the process of liquidating is considered to be a going

concern.

The merchandise turnover ratio is used to measure profitability.

TechCom has sales of $350,000 and estimates that 0.5% of its sales are uncollectible.

The amount of bad debt expense is $17,500.

Businesses normally get a full credit for the goods and services tax (GST) and/or

Harmonized Sales Tax (HST) that they have paid.

An abnormal balance in an account refers to a balance on the side where decreases are

recorded.

All material incidental costs of inventory acquisition and handling are assigned to

inventory.

The aim of a post-closing trial balance is to verify that (1) total debits equal total credits

for temporary accounts and (2) all temporary accounts have zero balances.

The accounting equation can be restated as assets – equity = liabilities.

Long-term investments can include land not currently being used in operations.

Enterprise-application software is used primarily for journal entries.

The principle of faithful representation is used by some companies to justify allocating

incidental inventory costs to cost of goods sold.

Closing revenue and expense accounts at the end of the accounting period serves to

make the revenue and expense accounts ready for use in the next period.

The primary objective of accounting is to help people make better decisions.

An understatement of ending inventory will understate cost of goods sold and overstate

net income.

Current liabilities include accounts receivable, unearned revenues, and taxes owed.

The cost principle states that if no cash is involved in a transaction the cash-equivalent

value must be used.

A subsidiary ledger is a listing of individual accounts with a common characteristic.

Toys “R” Us had cost of goods sold of $6,000 million, ending inventory of $2,500

million, and average inventory turnover of $2,000 million. The days’ sales in inventory

is:

A. 152.1.

B. 121.7.

C. 876.

D. 1,095.

E. 30.5.

The accepted method for valuing inventory includes:

A. Counting the units of each product on hand.

B. Multiplying the count for each product by its cost per unit.

C. Adding the costs for all products.

D. Counting the units of each product on hand and multiplying the count for each

product by its cost per unit.

E. All of these answers are correct.

A bookkeeper using a Purchases Journal recorded new store supplies purchased on

account. The subledger that would be impacted as a result of this transaction is the:

A. Accounts payable subledger.

B. Accounts receivable subledger.

C. Merchandise inventory subledger.

D. Sales subledger.

E. Cash receipts journal.

The Unadjusted Trial Balance columns of the work sheet show the balance in the Office

Supplies account at $750. The Adjustments columns show that $425 of these supplies

were used during the period. The amount shown as Office Supplies in the Balance Sheet

columns is:

A. $325 debit.

B. $325 credit.

C. $425 debit.

D. $750 debit.

E. $750 credit.

Profit is another name for:

A. The income statement.

B. Net income.

C. Equity.

D. A business transaction.

E. Assets.

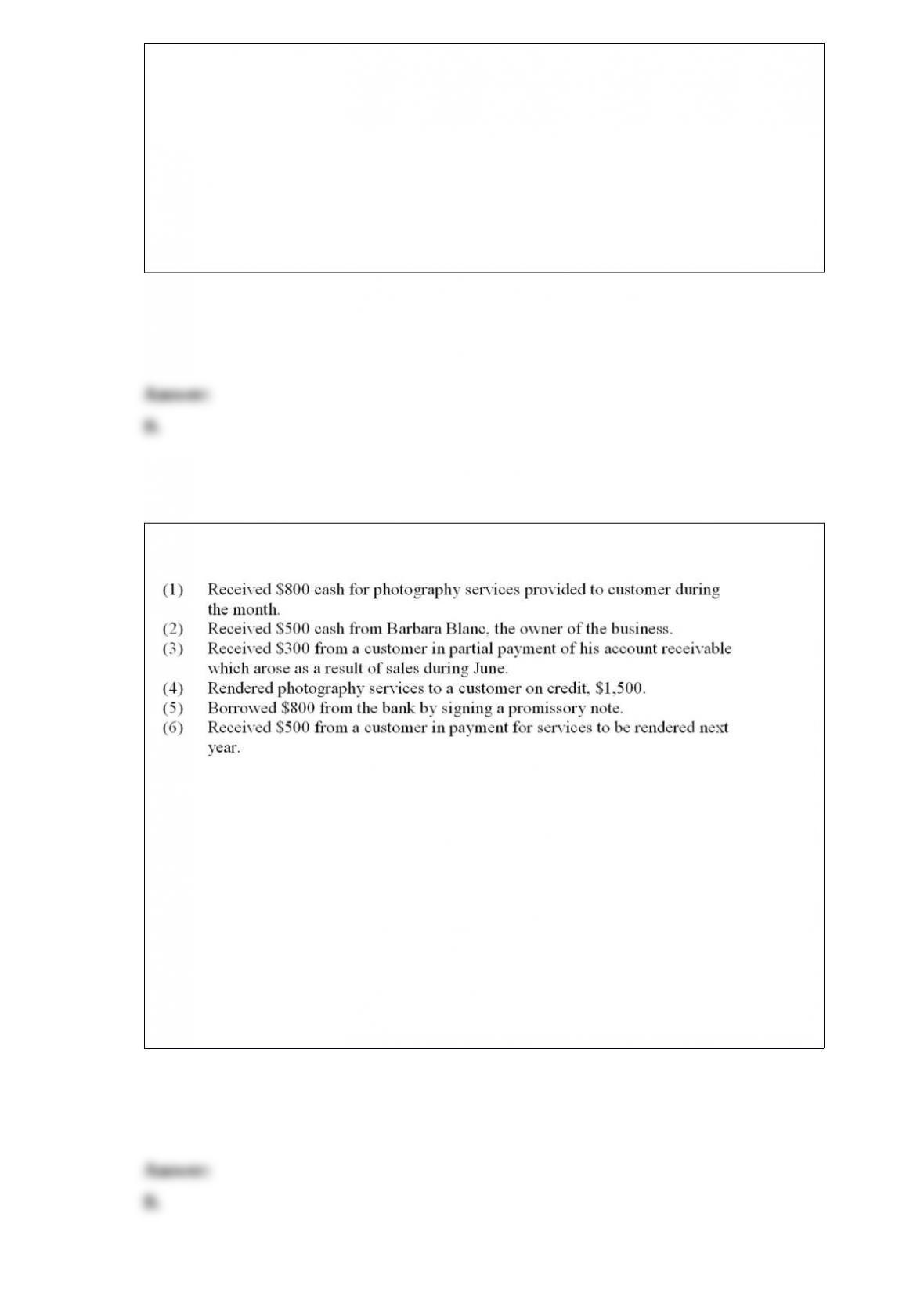

The following transactions occurred during July for Hurley Services:

How much revenue was earned in July?

A. $1,200.

B. $2,300.

C. $2,800.

D. $5,500.

E. $7,000.

A trial balance prepared before any adjustments have been recorded is:

A. An adjusted trial balance.

B. Used to prepare the financial statements.

C. An unadjusted trial balance.

D. Correct with respect to proper balance sheet and income statement amounts.

E. Will not have the debits equal to the credits.

Fees earned by a business in exchange for services provided by the business appear on

which of the following statements?

A. Balance sheet.

B. Income statement.

C. Statement of changes in equity.

D. Statement of cash flows.

E. Statement of financial position.

Merchandising companies must account for:

A. Sales.

B. Sales discounts.

C. Sales returns and allowances.

D. Cost of goods sold.

E. All of these answers are correct.

The primary objective of financial accounting is:

A. To help organizations keep track of financing activities.

B. To provide external reports to help users analyze an organization’s activities.

C. To help an organization define its ideas, goals, and actions.

D. To help an organization to keep track of its buying and selling of resources.

E. To prepare budgets.

The accounting principle that requires that transactions are expressed using units of

money as the common denominator is the:

A. Business entity principle.

B. Monetary unit principle.

C. Going concern principle.

D. Cost principle.

E. Revenue recognition principle.

Which financial statement shows whether the business earned a profit or loss, and also

lists the types and amounts of the revenues and expenses?

A. Balance sheet.

B. Statement of changes in equity.

C. Statement of cash flows.

D. Income statement.

E. Statement of financial position.

During a period of steadily rising prices, which inventory cost flow assumption results

in reporting the highest inventory value?

A. Specific identification.

B. Average cost.

C. Moving weighted average.

D. FIFO.

E. Any of the above.

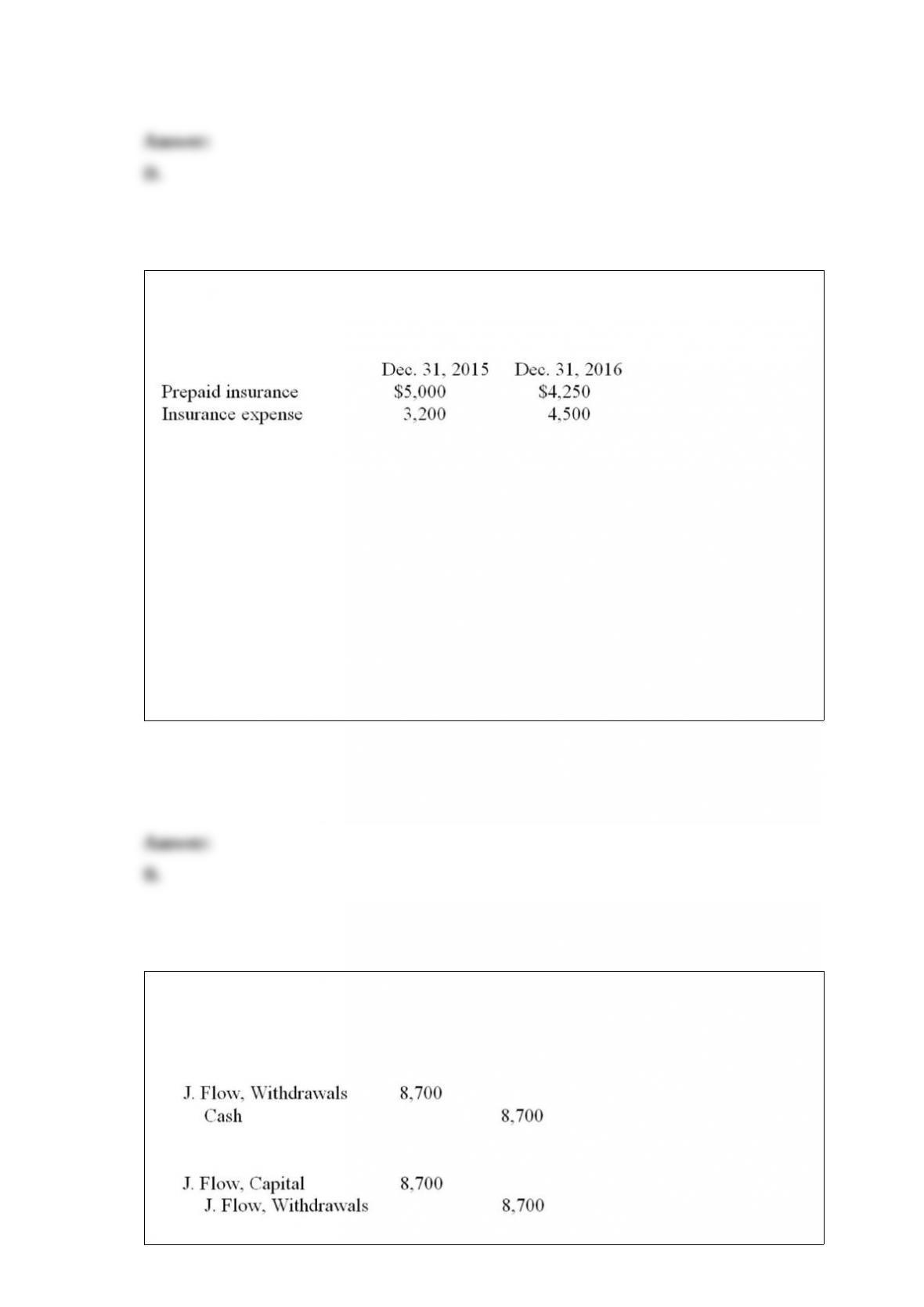

The Creative Company has several insurance policies in force with payments due at

various times. The following information refers to prepaid insurance and insurance

expense on two successive dates.

The amount of cash paid for insurance by Creative Company in 2016 was:

A. $3,250.

B. $3,750.

C. $4,500.

D. $5,000.

E. $8,750.

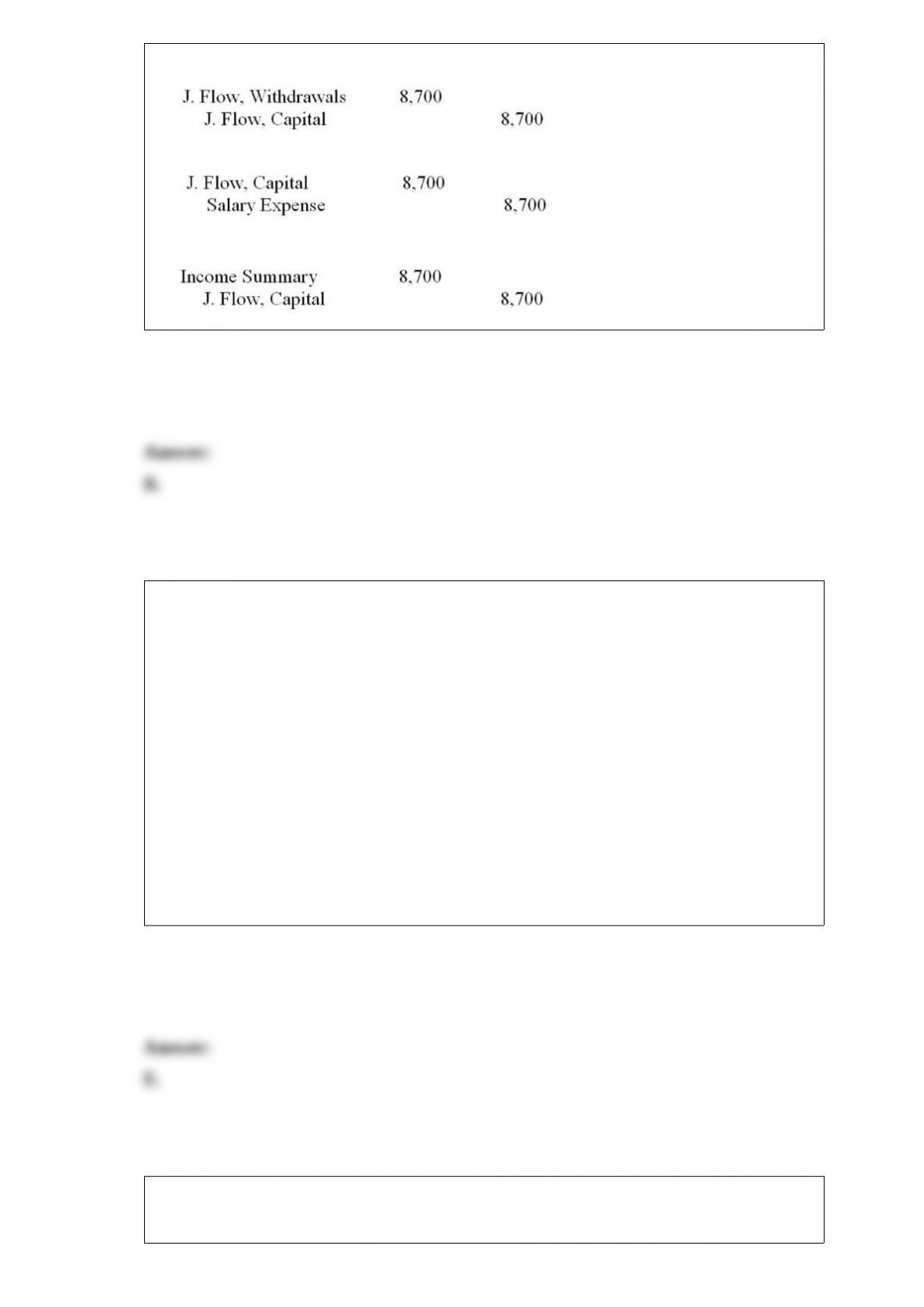

J. Flow, the proprietor of Flow Services, withdrew $8,700 from his business during

2015. These withdrawals will result in which of the following closing entries at the end

of 2015?

A.

B.

C.

D.

E.

Which of the following statements is correct?

A. When an insurance premium is paid in advance, the payment is normally recorded in

a liability account called Prepaid Insurance.

B. Goods and services are commonly sold to customers on the basis of oral or implied

promises of future payment, called promissory notes.

C. Increases and decreases in cash are always recorded in the equity account.

D. An account called Land is commonly used to record increases and decreases in the

land and buildings owned by a business.

E. None of these statements are correct.

A balance sheet that places the liabilities and equity to the right of the assets is called

a(n):

A. Report form balance sheet.

B. Account form balance sheet.

C. Adjusted balance sheet.

D. Unadjusted balance sheet.

E. The accounting equation.

If Girard Don, the owner of Girard’s Software proprietorship, uses cash of the business

to purchase a personal computer, the business should record this use of cash with an

entry to:

A. Debit Salary Expense and credit Cash.

B. Debit Girard Don, Salary and credit Cash.

C. Debit Cash and credit Girard Don, Withdrawals.

D. Debit Girard Don, Capital and credit Cash.

E. Debit Girard Don, Withdrawals and credit Cash.

If the accountant failed to make an adjusting entry at the end of the period to record

depreciation for the period, the omission will cause:

A. An overstatement of expenses.

B. An overstatement of revenues.

C. An understatement of assets.

D. An overstatement of liabilities.

E. An overstatement of assets.

A financial statement providing information that helps users understand a company’s

financial status at a specific date, is called a(n):

A. Balance sheet.

B. Income statement.

C. Statement of cash flows.

D. Statement of changes in equity.

E. Bank statement.

A debit to Sales Returns and Allowances and a credit to Accounts Receivable:

A. Is not possible; it should be a credit to Sales Returns and Allowances and a debit to

Accounts Receivable.

B. Recognizes that a customer returned merchandise.

C. Requires a debit memorandum to recognize the customer’s return.

D. Recognizes a cash discount taken by a customer.

E. All of these answers are correct.

Zang Company had no office supplies on hand at the beginning of the year. During the

year, the company purchased $250 worth of office supplies. At the end of the year, $50

worth of office supplies were on hand. How much should Zang Company report as

office supplies expense for the year?

A. $75.

B. $125.

C. $175.

D. $200.

E. $325.

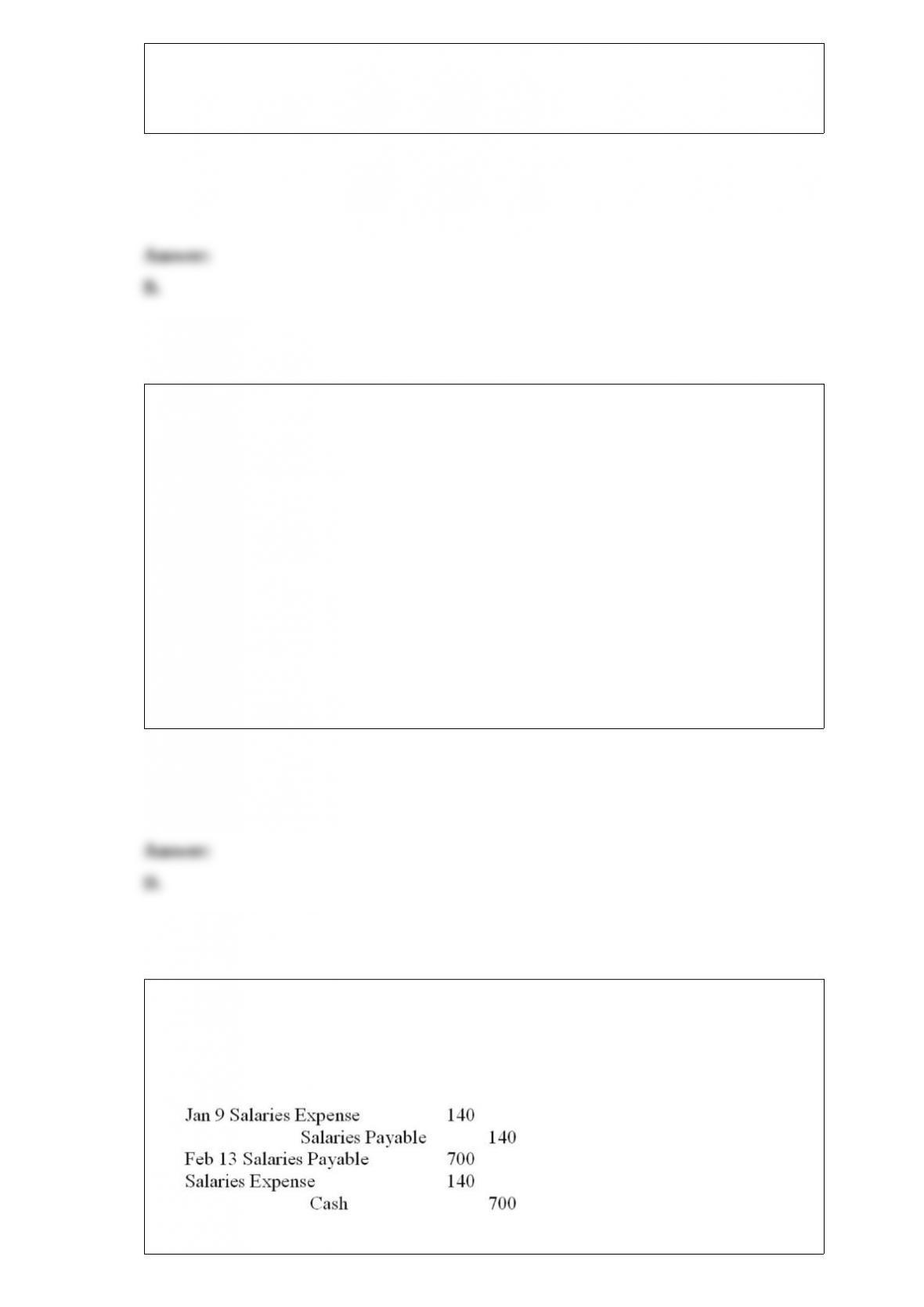

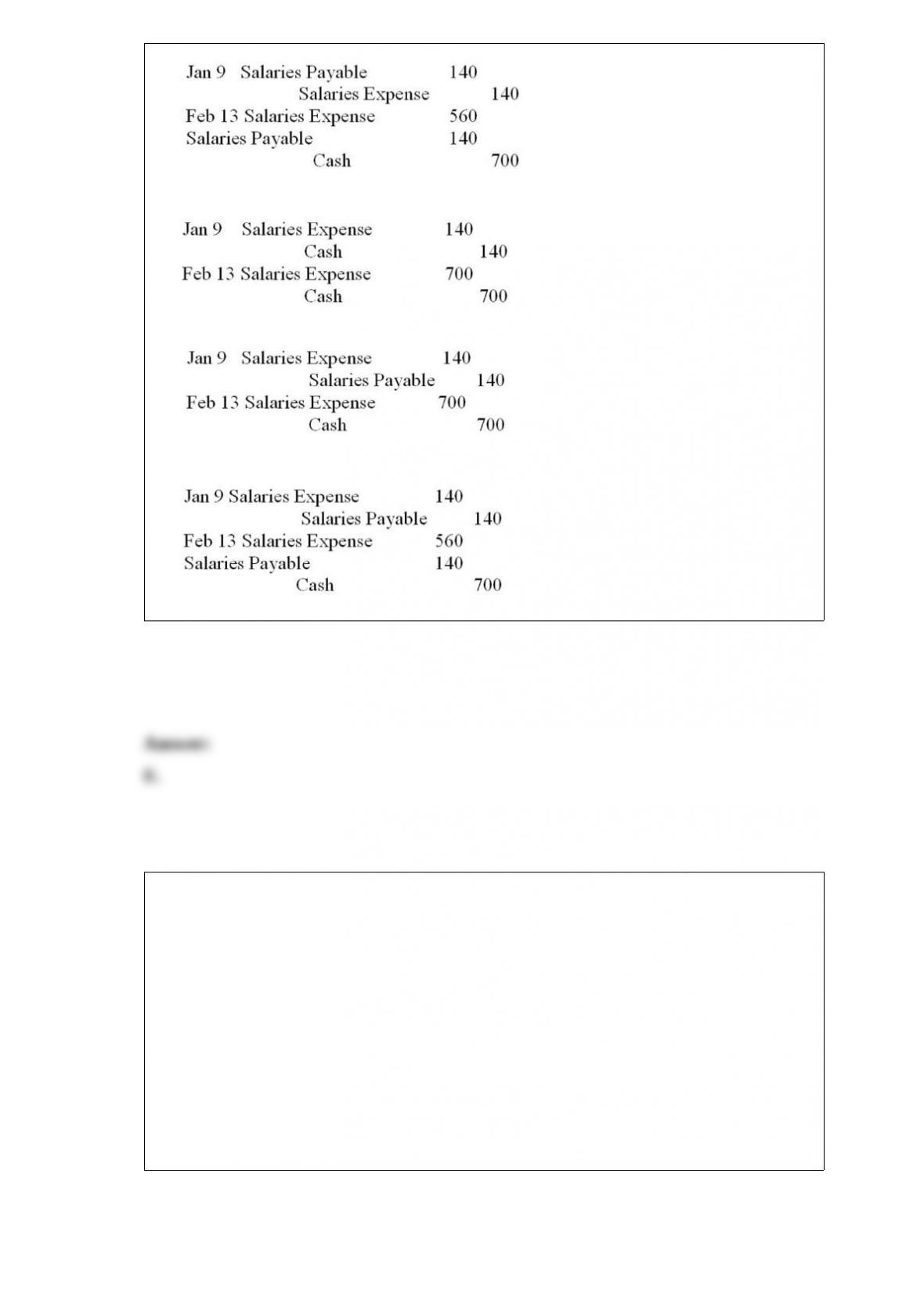

On January 31 of this year, Gallery Corp. recorded 2 days of accrued salaries ($140) for

its employees. On February 13, the company paid its employees a total of $700. The

correct journal entries at January 31 and February 13 are:

A.

B.

C.

D.

E.

Which of the following errors would cause the balance sheet columns of a work sheet to

be out of balance?

A. Entering an asset amount in the Income Statement Debit column.

B. Entering a liability amount in the Income Statement Credit column.

C. Entering an expense amount in the Balance Sheet Debit column.

D. Entering a revenue amount in the Balance Sheet Debit column.

E. Entering a liability amount in the Balance Sheet Credit column.

Credit card expense may be classified as:

A. A discount deducted from sales to get net sales.

B. A selling expense.

C. An administrative expense.

D. All of these answers are correct.

E. A selling expense and an administrative expense.

How would the accounting equation of Lenore Turner’s consulting business be affected

by the billing of a client for $2,000 for consulting work completed?

A. Accounts receivable, $2,000 increase, liabilities, $2,000 decrease.

B. Accounts receivable, $2,000 increase, liabilities, $2,000 increase.

C. Accounts receivable, $2,000 increase, cash, $2,000 increase.

D. Accounts receivable, $2,000 increase, equity, $2,000 increase.

E. Accounts receivable, $2,000 increase, cash, $2,000 decrease.

A business sold some inventory that had cost $5,000 before taxes. The sale is subject to

5% goods and services tax (GST) and 7% provincial sales tax (PST). The business uses

a perpetual inventory system. How much will be credited to the Merchandise Inventory

account as a result of this sale?

A. $5,000

B. $5,300

C. $5,350

D. $5,600

E. None of these answers is correct.

If the liabilities of a business increased $8,000 during a period of time and equity in the

business decreased $4,000 during the same period, the assets of the business must have:

A. Decreased $12,000.

B. Decreased $4,000.

C. Increased $12,000.

D. Increased $4,000.

E. Increased $6,000.

Toys “R” Us had cost of goods sold of $6,000 million, ending inventory of $2,500

million, and average inventory of $2,000 million. The merchandise turnover is:

A. 2.40.

B. 3.00.

C. 0.33.

D. 0.42.

E. 12.00.

Days’ sales in inventory is calculated by:

A. Dividing average merchandise inventory by cost of goods sold.

B. Dividing cost of goods sold by average merchandise inventory.

C. Dividing ending inventory by cost of goods sold times 365.

D. Dividing cost of goods sold by ending inventory times 365.

E. Dividing ending inventory by cost of goods sold.

Which of the following statements is correct?

A. The left side of a T-account is the credit side.

B. Entries that decrease asset and expense accounts, or increase liability, equity, and

revenue accounts are posted as debits.

C. The left side of a T-account is the debit side.

D. The right side of a T-account is the debit side.

E. Entries that increase asset, expense, and revenue accounts are posted as debits.

On March 15, Stark Company’s inventory was destroyed by a tornado. The following

was the only information salvaged:

(1) Inventory, January 1: $31,000

(2) Purchases to Mar 15: $14,000

(3) Sales to Mar 15: $65,000

(4) Sales returns to Mar 15: $7,000

Stark’s average gross profit ratio is 35%. What is the estimated value of the destroyed

inventory?

A. $7,300.

B. $8,500.

C. $9,250.

D. $10,525.

E. $45,000.

Identify several opportunities in accounting and its related fields.

Before purchasing a parcel of land, Ming’s Boutique had the land appraised at $90,000.

The management of Ming’s Boutique purchased the land for $85,000. At what amount

should the land be recorded on Ming’s Boutique’s books? What accounting principle

supports your answer?

Before adjustment, a prepaid expense account would contain an asset amount that is

___________________ and an expense amount that is ___________________.

Explain why the lower of cost and net realizable value rule is used to value inventory.

Calculate the amount of interest that would be owed on a $10,000, 90-day, 5% note

receivable.

Work sheet preparation is a(n) ____________ step in the accounting cycle.

Discuss the differences in the special journals for a perpetual versus a periodic

inventory system.