1) The selection of the factory overhead allocation method is important because the

method selected determines the accuracy of the product cost.

2) The revenue recognition concept states that revenue should be recorded in the same

period as the cash is received.

3) Costs other than direct materials cost and direct labor cost incurred in the

manufacturing process are classified as factory overhead cost.

4) The system of accounting where revenues are recorded when they are earned and

expenses are recorded when they are incurred is called the cash basis of accounting.

5) The difference between a classified balance sheet and one that is not classified is that

the classified one has subheadings.

6) After the sales budget is prepared, the capital expenditures budget is normally

prepared next.

7) The process by which management plans, evaluates, and controls long-term

investment decisions involving fixed assets is called capital investment analysis.

8) In a job order cost accounting system for a service business, materials costs are

normally included as part of overhead.

9) The issuance of common stock affects both paid-in capital and retained earnings.

10) Under the Internal Revenue Code, corporations are required to pay federal income

taxes.

11) Under the cost price approach, the transfer price is the price at which the product or

service transferred could be sold to outside buyers.

12) Explain the meaning of the business entity concept.

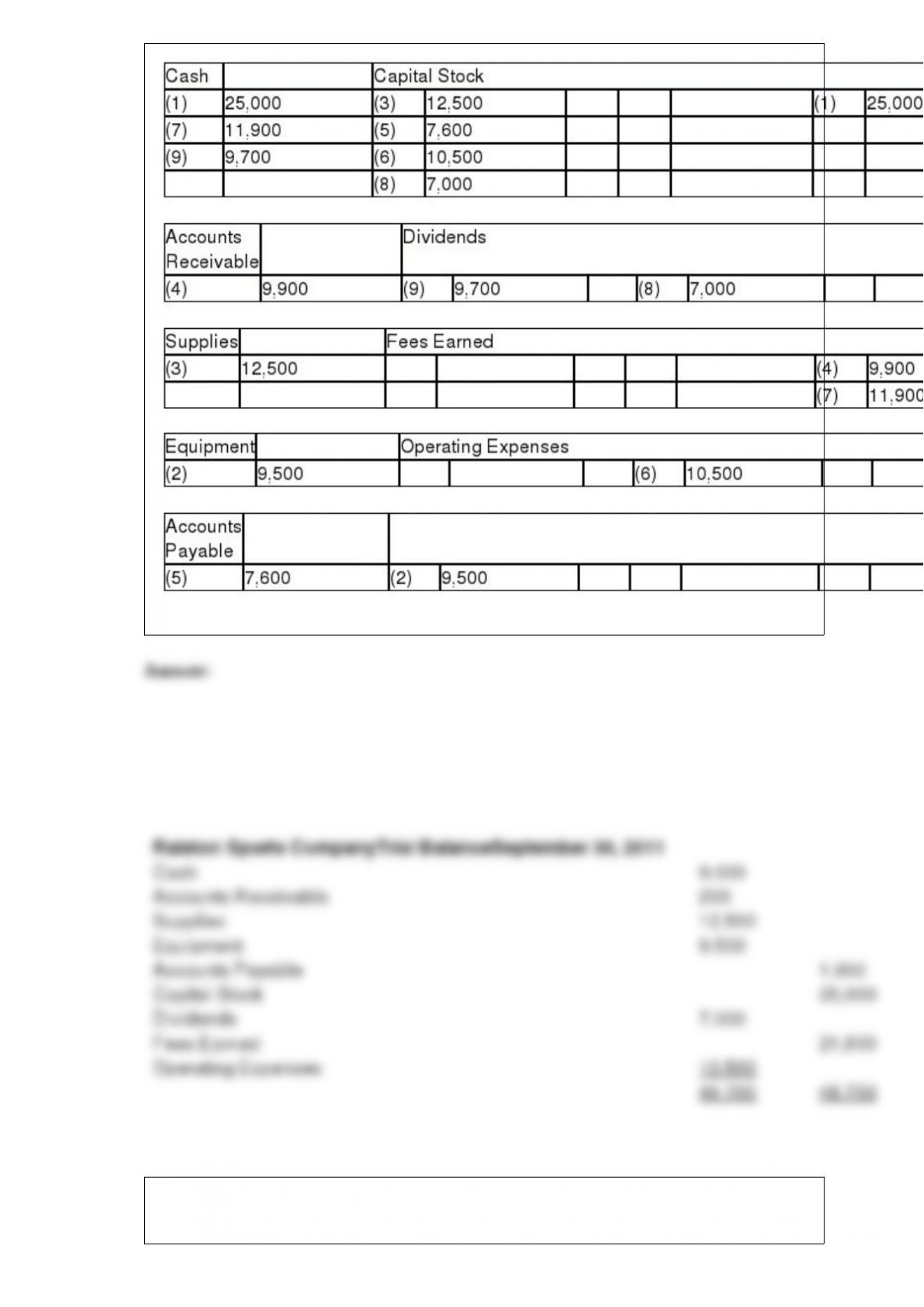

13) All nine transactions for Ralston Sports Co. for September 2011, the first month of

operations, are recorded in the following T accounts:

Refer to Exhibit 2-1. Prepare a trial balance, listing the accounts in their proper order.

14) Donner Company is selling a piece of land adjacent to their business. An appraisal

reported the market value of the land to be $120,000. The Focus Company initially

offered to buy the land for $107,000. The companies settled on a purchase price of

$115,000. On the same day, another piece of land on the same block was sold for

$122,000. Under the cost concept, what is the amount that will be used to record this

transaction in the accounting records?

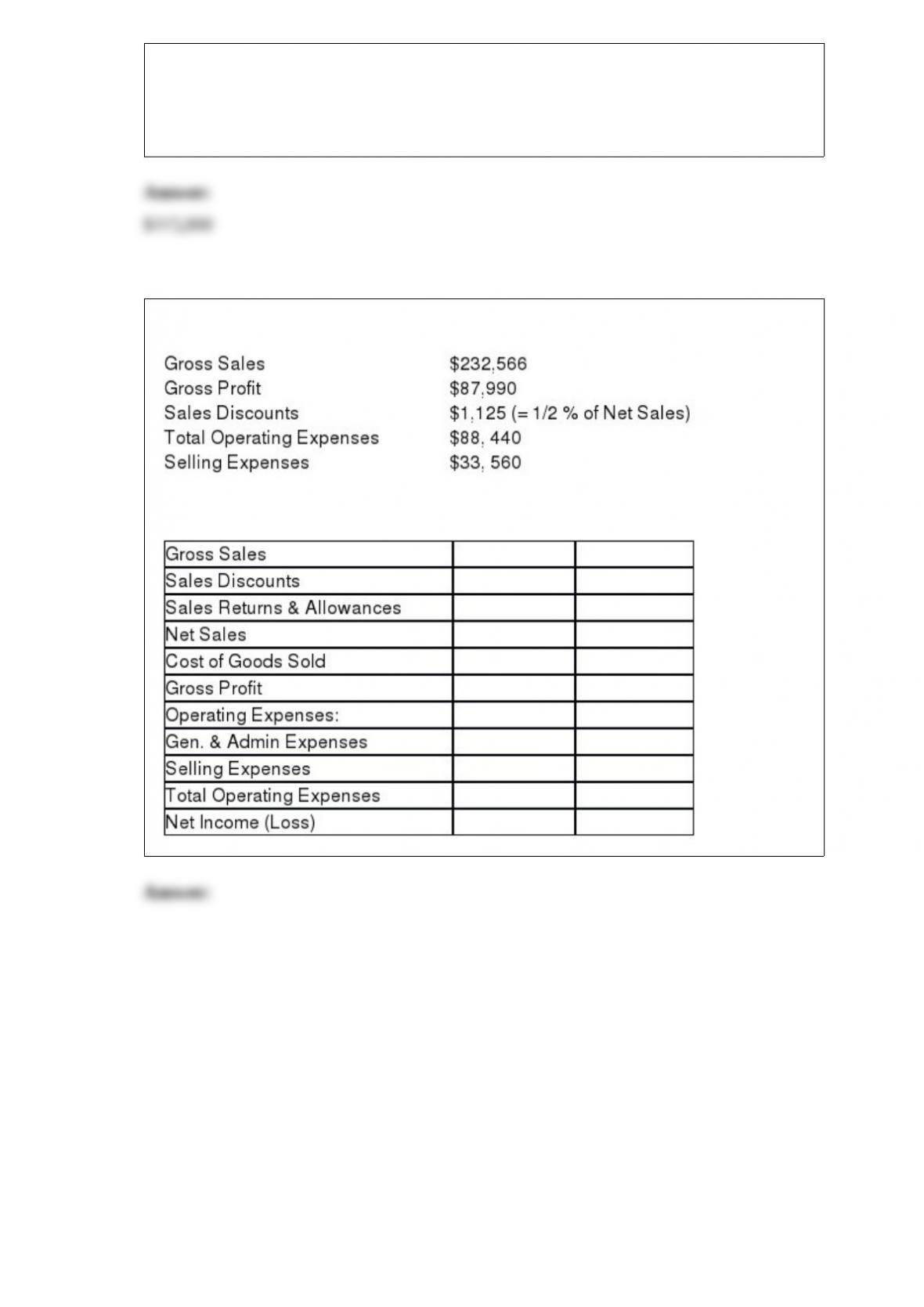

15) The following information was extracted from the Stone Companys records.

Complete the following:

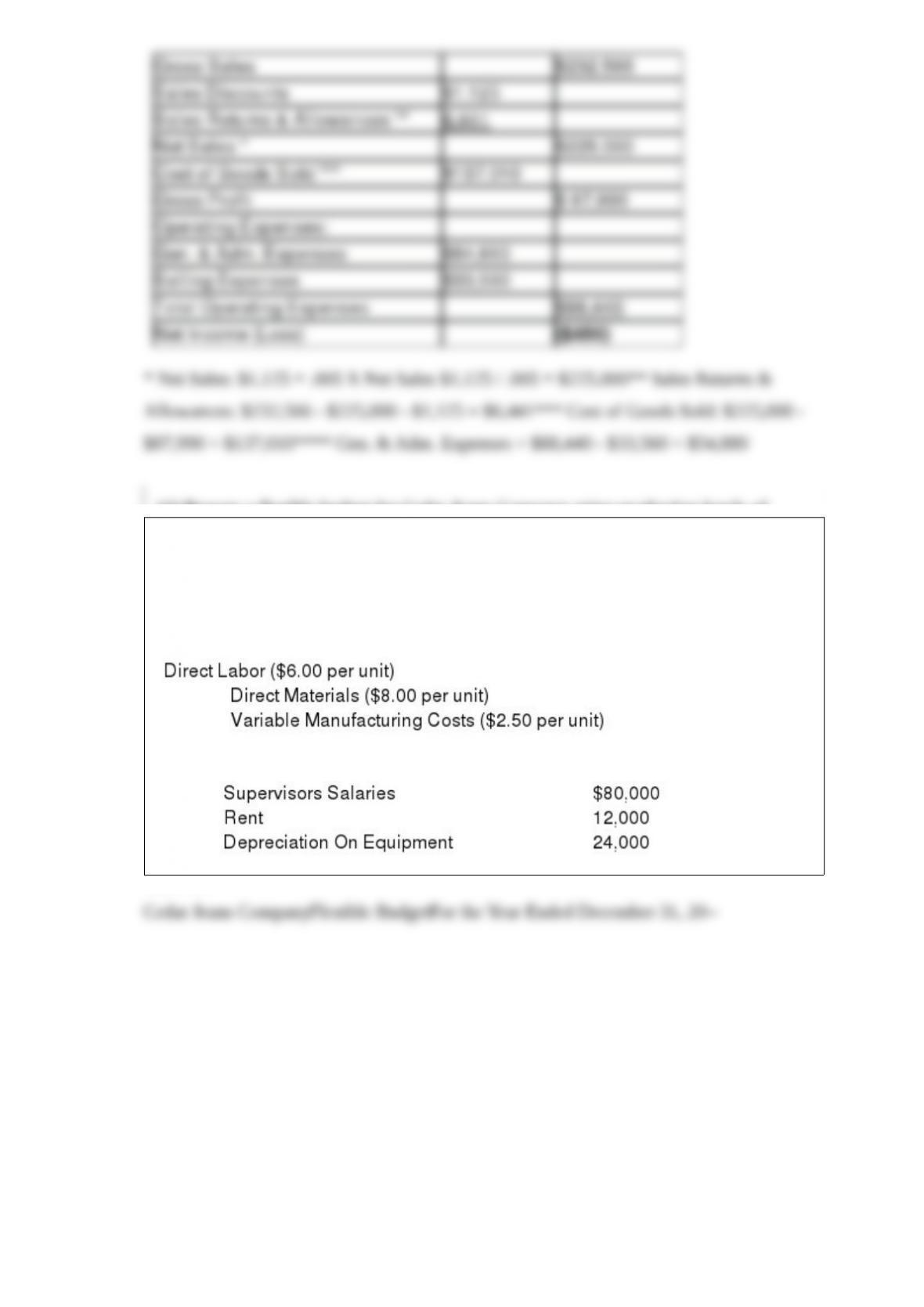

16) Prepare a flexible budget for Cedar Jeans Company using production levels of

16,000, 18,000, and 20,000 units produced. The following is additional information

necessary to complete the budget:

Variable costs:

Fixed costs:

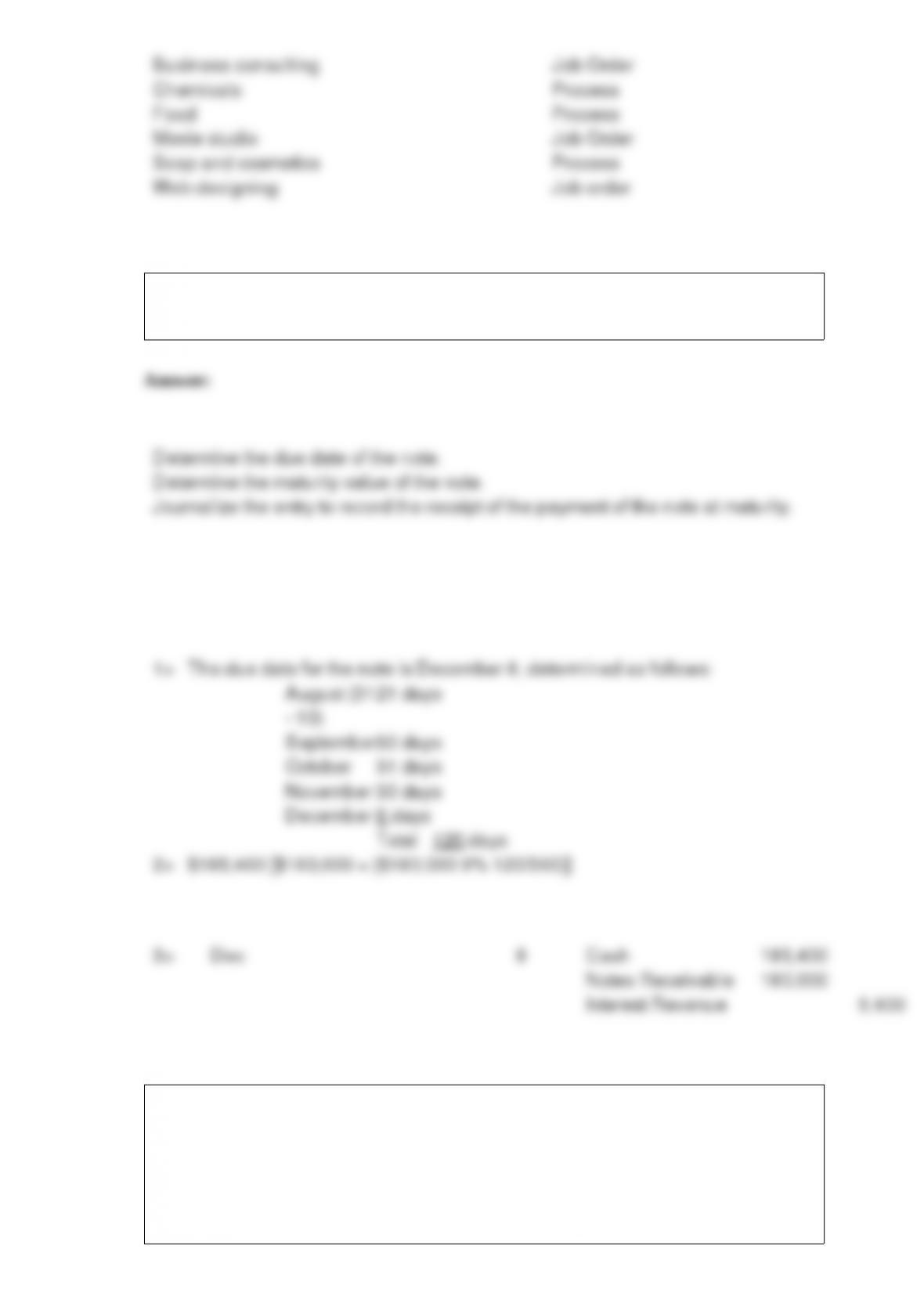

17) Which of the following industries would normally use job order costing systems

and which would normally use process costing systems?

Business consulting

Chemicals

Food

Movie

Soap and cosmetics

Web designing

18) Blackwell Industries received a 120-day, 9% note for $180,000, dated August 10

from a customer on account.

19) The following are inputs and outputs to the help desk.

Operator training

Number of calls per day

Maintenance of computer equipment

Number of operators

Number of complaints

Identify whether each is an input or an output to the help desk.

20) Darnell Company purchased $88,000 of computer equipment from Joseph

Company. Darnell Company paid for the equipment using cash that had been obtained

from the sale of capital stock to Donnie Darnell.

Which entity or entities (Darnell Company, Joseph Company, Donnie Darnell) should

record the transaction involving the computer equipment on their accounting records?

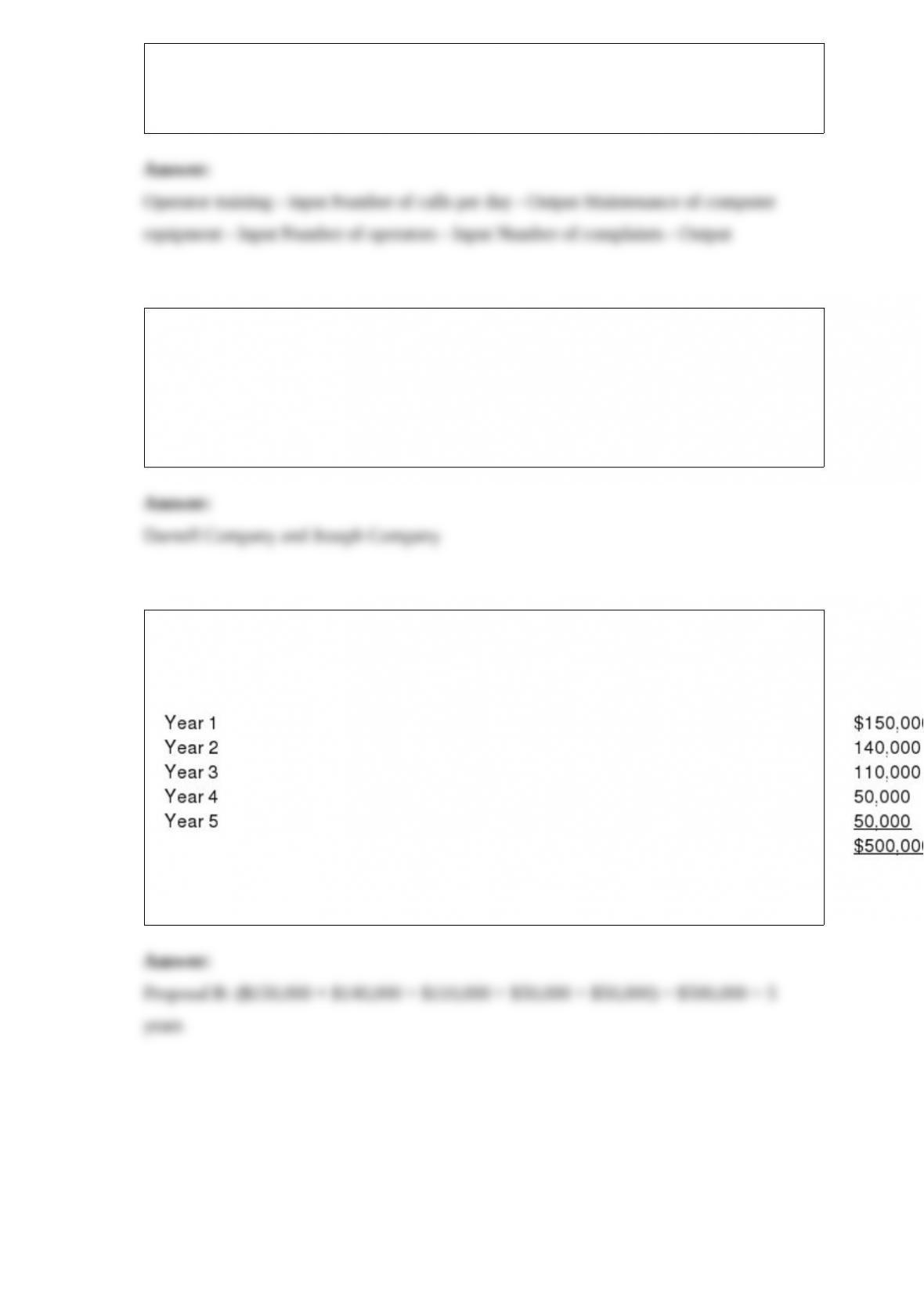

21) Proposals A and B each cost $500,000 and have 5-year lives. Proposal A is expected

to provide equal annual net cash flows of $109,000, while the net cash flows for

Proposal B are as follows:

Determine the cash payback period for each proposal. Round answers to two decimal

places. Proposal A: $500,000/$109,000 = 4.59 years