1) Pregler Inc. has 70% ownership of Sach Company, but should exclude Sach from its

consolidated financial statements if

A) Sach is in a regulated industry

B) Pregler uses the equity method for Sach

C) Sach is in legal reorganization

D) Sach is in a foreign country and records its books in a foreign currency

2) Bertram and Ernest share profits and losses equally after salary and interest

allowances. Bertram and Ernest receive salary allowances of $40,000 and $60,000,

respectively, and both partners receive 10% interest on their average capital balances.

Average capital balances are calculated at the beginning of each month, regardless of

when additional capital contributions or permanent withdrawals are made subsequently

within the month. Partners’ drawings of $3,000 per month are not used in determining

the average capital balances. Total net income for 2011 is $240,000.

BertramErnest

January 1 capital balances$200,000$240,000

Yearly drawings ($3,000 a month)(36,000)(36,000)

Permanent withdrawals of capital:

June 3(24,000)

May 2(30,000)

Additional investments of capital:

July 380,000

October 2100,000

What is the weighted-average capital for Bertram and Ernest in 2011?

A) $224,000 and $245,000

B) $203,333 and $221,167

C) $221,333 and $239,167

D) $256,000 and $220,000

3) Under the Uniform Probate Code, the term “personal representative” refers to which

of the following?

A) An executor, but not an administrator

B) An administrator, but not an executor

C) Neither an executor nor an administrator

D) Either an executor or an administrator

4) In a liquidation under Chapter 7, the trustee

A) may not be appointed, but may only be elected

B) may not be elected, but may only be appointed

C) is responsible for converting assets to cash and distributing payments to claimants

D) is responsible for appointing a creditors’ committee

5) On January 1, 2011, Bigg Corporation sold equipment with a book value of $20,000

and a 10-year remaining useful life to its wholly-owned subsidiary, Little Corporation,

for $30,000. Both Bigg and Little use the straight-line depreciation method, assuming

no salvage value. On December 31, 2011, the separate company financial statements

held the following balances associated with the equipment:

Bigg Little

Gain on sale of equipment$10,000

Depreciation expense$3,000

Equipment30,000

Accumulated depreciation3,000

A working paper entry to consolidate the financial statements of Bigg and Little on

December 31, 2011 included a

A) debit to equipment for $10,000

B) credit to gain on sale of equipment for $10,000

C) debit to accumulated depreciation for $1,000

D) credit to depreciation expense for $3,000

6) In reference to accounting for trusts or estates, which of the following statements is

correct?

A) Estates are subject to taxation, but trusts are not

B) Estates are subject to probate laws that vary widely across the fifty states

C) Estates are subject to income taxes at the federal level, but not at the state level

D) Estates and trusts are taxed regardless of size

7) Pental Corporation bought 90% of Sedacor Company’s common stock at its book

value of $400,000 on January 1, 2011 . During 2011, Sedacor reported net income of

$130,000 and paid dividends of $40,000. At what amount should Pental’s Investment in

Sedacor account be reported on December 31, 2011?

A) $400,000

B) $481,000

C) $490,000

D) $530,000

8) If estate assets are insufficient to pay all claims in full, under the Uniform Probate

Code which of the following would be paid first?

A) Reasonable funeral expenses

B) Necessary medical and hospital expenses of the last illness of the decedent

C) Unsecured debts

D) The costs and expenses of administration of the estate

9) Ulysses Company purchases goods from China amounting to 372,372 Yuan (the

transaction is denominated in the Chinese Yuan). Assume the Yuan is trading at $0.154

at the date the goods are ordered, and the Yuan is trading at $0.155 at the date the goods

are received, and when the invoice is paid a month later, the Yuan is trading at $.156.

Assume all three dates are in the same fiscal year. Which of the following is true?

A) The entry to record the payment will include a gain of $744.74

B) The entry to record the payment will include a gain of $372.37

C) The entry to record the purchase will include a credit to Accounts Payable of

$57,345.29

D) The entry to record the purchase will include a credit to Accounts Payable of

$57,717.66

10) Swamp Co., a 55%-owned subsidiary of Pond Inc., made the following entry to

record a sale of merchandise to Pond:

Accounts Receivable40,000

Sales Revenue40,000

All Swamp sales are at 125% of cost. One-fourth of this merchandise remained in the

Pond’s inventory at year-end. A working paper entry to eliminate unrealized profits

from consolidated inventory would include a credit to Inventory in the amount of

A) $2,000

B) $2,500

C) $8,000

D) $10,000

11) Match each of the following descriptions with the correct category for a private,

not-for-profit hospital. Each term may be used more than once.

Categories:

A. Revenue

B. Deduction from Revenue

C. Expense

D. Gains / Losses

_____1> Courtesy allowances provided to hospital patients

_____2> Premium fees

_____3> Fees paid to the doctors

_____4> Charges to patients for patient services

_____5> Wages paid to nursing staff

_____6> Contractual allowances arranged with third-party payors

_____7> Cafeteria sales

_____8> Wages paid to hospital janitors

_____9> Depreciation expense on hospital equipment

_____10>Other operating revenueunrestricted

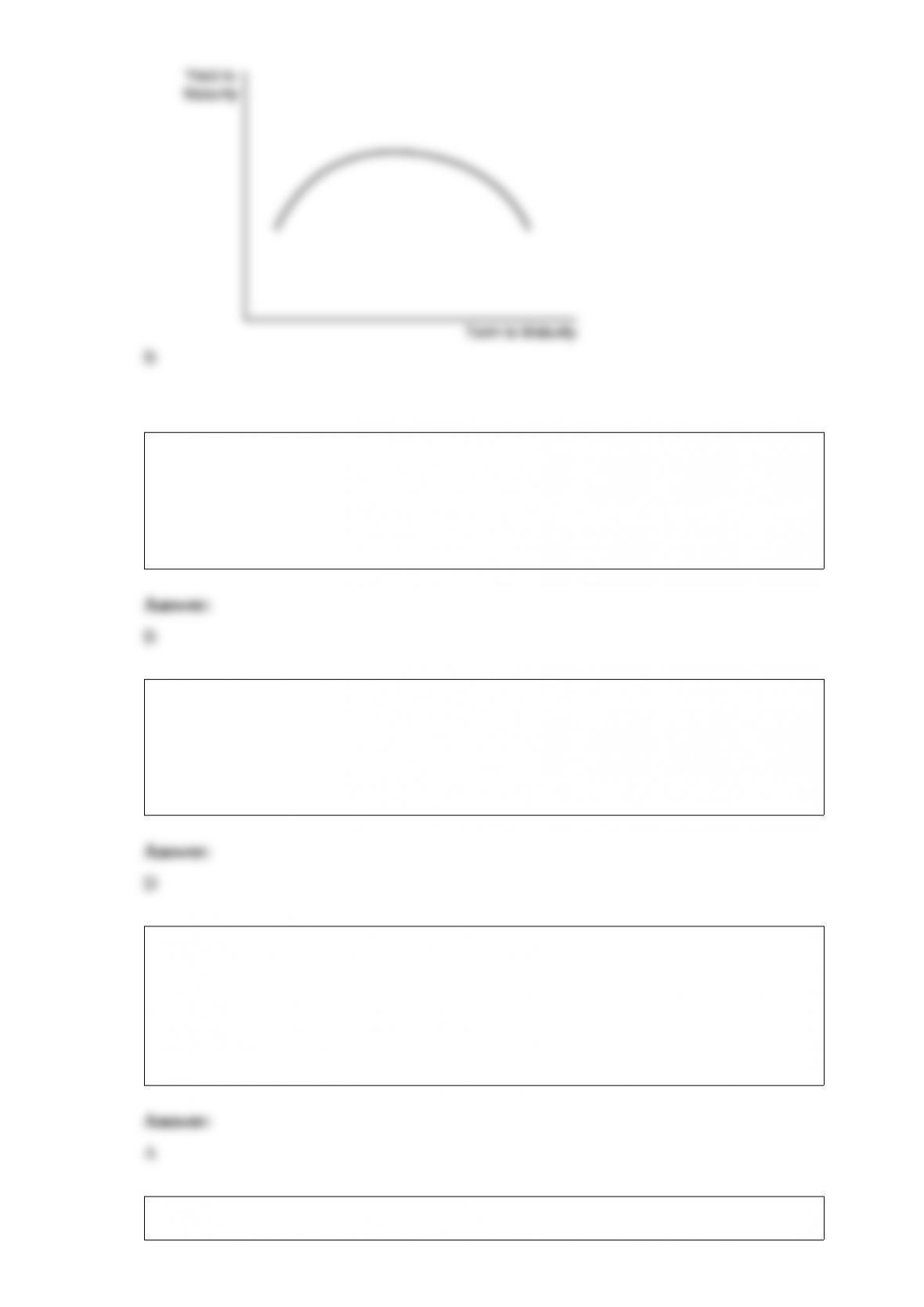

12) The U-shaped yield curve in the figure above indicates that the inflation rate is

expected to

A) remain constant in the near-term and fall later on

B) fall sharply in the near-term and rise later on

C) rise moderately in the near-term and fall later on

D) remain constant in the near-term and rise later on

13) Government-wide financial statements exclude the

A) general fund

B) fiduciary funds

C) proprietary funds

D) special revenue funds

14) Voluntary health and welfare organizations

A) may not have paid executives or staff

B) are governed by separate GASB statements

C) use fund accounting, following the rules for proprietary fund reporting

D) are supported by, and provide voluntary services to, the public

15) A forward contract used as a cash flow hedge will be recorded as an asset if

A) the holder is expecting to receive a payment as a result of the contract

B) the holder is accounting for the hedged instrument as a fair value hedge

C) the holder is hedging the net investment in a foreign entity

D) the holder is using the alternate accounting method and deferring all gains or losses

from the hedge

16) Palmer Company owns a 25% interest in Sad, Incorporated, a domestic company.

Sad had net income of $60,000 and paid dividends of $20,000. Palmer’s tax rate is 35%.

For simplicity, assume that Sad’s undistributed earnings are Palmer’s only temporary

timing difference. Assume Sad qualifies for the 80% dividend received deduction.

Which of the following statements is correct?

A) The current tax liability is $700

B) The current tax liability is $1,050

C) Under GAAP, Palmer provides for income taxes on Sad’s undistributed earnings with

a credit to deferred tax liability of $700

D) Under GAAP, Palmer provides for income taxes on Sad’s undistributed earnings

with a credit to deferred tax liability of $1,050

17) Gains and losses incurred at liquidation are distributed to the partners using the

residual profit and loss sharing ratios because

A) using ownership percentages would permit solvent partners to not share profits with

insolvent partners

B) the residual profit and loss ratios represent the ownership percentages

C) these amounts represent profits and losses from prior periods that would have been

shared using the residual profit and loss ratios

D) using the established profit and loss sharing ratios is not permitted

18) The partners of the Minion, Nocti and Overly partnership share profits and losses in

the ratio of 6:3:1, respectively. The partners have decided to liquidate and terminate the

partnership. Prior to liquidation, the partnership balance sheet was as follows:

Cash$20,000Liabilities$120,000

Inventory100,000Minion, capital60,000

Fixed assets – net160,000Nocti, capital80,000

Overly, capital20,000

Total assets$280,000Total equity$280,000

Required:

Prepare a schedule of liquidation, given that the partnership sold the inventory for

$40,000 and the fixed assets for $120,000.

19) On November 1, 2011, Ross Corporation, a calendar-year U.S. corporation,

invested in a purely speculative contract to purchase 1 million euros on January 30,

2012, from Trattoria Company, an Italian brokerage firm. Ross agreed to purchase

1,000,000 euros from Trattoria at a fixed price of $1.420 per euro. Trattoria agreed to

transmit 1,000,000 euros to Ross on January 30, 2012 . Net settlement is not permitted.

The spot rates for euros are:

Nov 01, 2011 1 euro = $1.415

Dec 31, 2011 1 euro = $1.395

Jan 30, 2012 1 euro = $1.410

The 30-day futures rate for euros on December 31, 2011 was $1.405.

Required:

Prepare the General Journal entries that Ross would record on November 1, December

31, and January 30 .

20) The profit and loss sharing agreement for the Tuttle, Upman, and Veer partnership

provides for residual profits and losses to be allocated 2:3:6 to Tuttle, Upman, and Veer,

respectively. In 2011, the partnership recorded $11,000 of net income that was properly

allocated to the partners’ capital accounts. On January 18, 2012, after the books were

closed for 2011, Tuttle discovered that the $16,500 payment for the partnership’s

liability and workers compensation insurance for 2012 was recorded as insurance

expense when it was paid on December 28, 2011 .

Required:

Prepare the necessary correcting entry(s) for the partnership.

21) On June 30, 2011, Stampol Company ceased operations and all of their assets and

liabilities were purchased by Postoli Incorporated. Postoli paid $40,000 in cash to the

owner of Stampol, and signed a five-year note payable to the owners of Stampol in the

amount of $200,000. Their closing balance sheets as of June 30, 2011 are shown below.

In the purchase agreement, both parties noted that Inventory was undervalued on the

books by $10,000, and Pistoli would also take possession of a customer list with a fair

value of $18,000. Pistoli paid all legal costs of the acquisition, which amounted to

$7,000.

Postoli Stampol

Cash$150,000$17,000

Inventory260,000120,000

Other current assets420,00060,000

Land60,0000

Plant assets-net 590,000 190,000

Total Assets$1,480,000$387,000

Accounts payable$440,000$127,000

Notes payable160,00080,000

Capital stock, $5 par20,00050,000

Additional paid-in capital60,0000

Retained Earnings 800,000 130,000

Total Liabilities & Equities$1,480,000$387,000

Required:

1> Prepare the journal entry Postoli would record at the date of acquisition.

2> Prepare the journal entry Stampol would record at the date of acquisition.

22) Passo Corporation acquired a 70% interest in Saun Corporation in 2007 at a time

when Saun’s book values and fair values were equal. In 2010, Saun sold land to Passo

for $82,000 that cost $72,000. The land remained in Passo’s possession until 2012 when

Passo sold it outside the combined entity for $102,000.

After the books were closed in 2012, it was discovered that Passo had not considered

the unrealized gain from its intercompany purchase of land in preparing the

consolidated financial statements. The only entry on Passo’s books was a debit to Land

and a credit to Cash in 2010 for $82,000, and in 2012, a debit to Cash for $102,000 and

credits to Land for $82,000 and Gain on sale of land for $20,000.

Before the discovery of the error, the consolidated financial statements disclosed the

following amounts:

201020112012

Controlling interest share$750,000$600,000$910,000

Land200,000240,000300,000

Required:

1>Prepare elimination/adjusting entries relating to the land on the consolidated working

papers for December 31, 2010, December 31, 2011 and December 31, 2012 .

2>Determine the correct amounts for Land in 2010, 2011, and 2012 .

3>Calculate the amount at which the gain on the sale of land should have been reported

in 2012

23) The City of Sill established an Internal Service Fund to provide cleaning services to

all city offices and departments. The following transactions took place with respect to

this event.

1>The General Fund contributed cash of $49,000 to the Internal Service Fund. The

General Fund provided a $10,000 loan to the Internal Service Fund.

2>On January 1, 2011, the Internal Service Fund acquired a floor waxing machine for

cash of $5,000. It has a 5 year life with no salvage value, and the city uses straight-line

depreciation on their assets.

3>The cleaning services department billed other government agencies and departments

$226,000 and collected $187,000.

4>The cleaning services department incurred and paid the following expenses: cleaning

personnel wages, $65,000; payroll taxes, $10,000; cleaning supplies, $13,000; and

office rental and utilities, $77,000. The cleaning services department also repaid the

general fund for the loan.

5>The cleaning services department prepared the journal entry to depreciate their assets

for the year ending December 31, 2011 .

Required:

Prepare the necessary journal entries for each of the above transactions for the Internal

Service Fund.

24) Pancake Corporation saw the potential for vertical integration and purchases a 15%

interest in Syrup Corp. on January 1, 2010, for $150,000. At that date, Syrup’s

stockholders’ equity included $200,000 of $10 par value common stock, $300,000 of

additional paid in capital, and $500,000 retained earnings. The companies began to

work together and realized improved sales by both parties. On December 31, 2011,

Pancake paid $250,000 for an additional 20% interest in Syrup Corp. Both of Pancake’s

investments were made when Syrup’s book values equaled their fair values. Syrup’s net

income and dividends for 2010 and 2011 were as follows:

2010 2011

Net income$220,000$330,000

Dividends$20,000$30,000

Required:

1>Prepare journal entries for Pancake Corporation to account for its investment in

Syrup Corporation for 2010 and 2011 .

2>Calculate the balance of Pancake’s investment in Syrup at December 31, 2011

25) General Hospital is a private, not-for-profit hospital. The following information is

available about the operations.

1>Gross patient services charges totaled $3,700,000.

2>Included in the above revenues are: charity services, $360,000; contractual

adjustments, $1,200,000; courtesy allowances, $20,000; and estimated uncollectible

amounts, $250,000.

3>Premium fees receipts were $110,000.

4>Purchased $75,000 of hospital supplies on account, with payments on that account,

$36,000.

5>Received cash donations for a new hospital wing of $2,500,000.

6>Paid contractor $275,000 for billed costs toward the new hospital wing.

Required:

Prepare journal entries for the aforementioned transactions.

26) Paka Corporation owns an 80% interest in Sandra Company. Paka acquired Sandra’s

bonds on January 2, 2011 . The following information is from the adjusted trial

balances at December 31, 2011, at which time the bonds have three years to maturity.

The bonds have interest payment dates of January 1 and July 1 . Straight-line

amortization is used by both companies.

Paka Sandra

Investment in Sandra Bonds, $100,000 par98,500

7% Bonds payable, $200,000200,000

Bond premium6,000

Interest expense12,000

Interest receivable7,000

Interest income7,500

Interest payable7,000

Required:

Prepare the necessary consolidation working paper entries on December 31, 2011 with

respect to the intercompany bonds.