Cash receipts from sales on account have been misappropriated. Which of the following

acts would conceal this defalcation and be least likely to be detected by an auditor?

A) postponing recording of cash receipt entries

B) overstating the accounts receivable control account

C) overstating the accounts receivable subsidiary ledger

D) recording cash receipt entries early

The auditor would like to design a test of control to test the following key control:

‘shipping documents are issued in numerical order by the computer and are accounted

for weekly.” Which of the following typical tests of controls would be suitable?

A) trace sales documents issued to the sales journal and trace the daily total to the

general ledger

B) ask the shipping department about the process that they use to issue shipping

documents, paying particular attention to continuity of numerical sequence

C) use computer assisted audit testing to determine whether there are any numbers in

the sequence missing (gap detection)

D) match shipments to the associated sales invoice

Jane works for Middle Co. She is responsible for opening the mail, and preparing the

bank deposit for cheques received, which she then gives to the owner. After the owner

has deposited the cash, he gives Jane the stamped bank deposit slip, which she uses to

record the cash received in the accounts receivable records. How does this allocation of

responsibilities affect the audit process? The auditor should

A) increase control testing with respect to the accuracy assertion.

B) do substantive tests (compare the deposit slip to the accounts receivable records).

C) consider the possibility of material fraud.

D) increase control testing with respect to the completeness assertion.

The auditor has set materiality at XYZ Company of $50,000 based upon a percentage of

net assets. The company currently has a small profit (only $3,500). Which of the

following items would the auditor most likely consider to be material and request an

account balance adjustment?

A) a misclassification between accounts receivable and accounts payable of $10,000

B) incorrect allocation of a note payable to current rather than long term

C) poor wording in a note to the financial statements, making it a bit difficult to

understand

D) an understatement of depreciation expense, which would increase depreciation by

$5,000

A misstatement in the financial statements can be considered material if

A) it overshadows the financial statements as a whole.

B) knowledge of the misstatement would affect the decision of a reasonable user of the

statements.

C) it affects more than one account on the statements.

D) it affects only one account on the statements.

Which of the following internal controls over notes payable address risks associated

with the accuracy, allocation and completeness audit assertions?

A) renewals or new notes should be approved by the Board of Directors (as evidenced

in the minutes) or by senior management

B) authorized employees should perform independent recalculations of interest and

reconciliation of the notes payable balance to the general ledger

C) subsidiary records should be maintained for each note, and there should be control

over blank and paid notes

D) paid notes should be cancelled and retained under the custody of an authorized

official

Generally, all of the rules of professional conduct for CAs apply to

A) students in public practice.

B) students and members.

C) all members.

D) members in public practice.

What rights do secondary investors (i.e. those who purchase shares after an initial

offering) have to sue an auditor?

A) since they are third-party claimants, they would be part of a limited class of known

users

B) they could claim contributory negligence, since they had prior information of

company results

C) they can sue under provincial legislation without the need to prove reliance

D) since there is absence of causal connection, they would not be able to sue the

auditors

The highest cost audit will be incurred when the auditor expects that the internal control

system would

A) be effective, but the auditor found extensive control test deviations.

B) have few effective controls, but client’s personnel were well-trained and

knowledgeable.

C) be very sophisticated, and the tests of controls confirmed this.

D) have few effective controls, and tests of balances found many errors.

It is important that sales be billed and recorded in the journal as soon as possible after

A) the order is received.

B) the order is received and credit is approved.

C) credit is approved and it is verified that there is enough inventory to fill the order.

D) shipment takes place.

Which of the following services provides no assurance about the client’s financial

statements?

A) compilation

B) review

C) audit

D) SysTrust

Which one of the following audit procedures is a dual-purpose test?

A) Conduct analytical review to determine the reasonableness of the bad debt

allowance.

B) Examine credit limit changes for authorization.

C) Calculate the accuracy of the accounts receivable aging.

D) Observe error message when incorrect customer number is entered.

An example of vouching would be to trace from

A) receiving reports to the acquisitions journal.

B) the acquisitions journal to supporting vendors’ invoices.

C) duplicate bank deposit slips to the cash receipts journal.

D) cancelled cheques to the cash disbursement journal.

Where an independence threat occurs, it may be that only the person affected needs to

be removed from the engagement. In this case, other members of the firm can complete

the engagement. An example of a situation where only the student or member would be

excluded from the engagement is where PA

A) has a significant financial interest in the client, such that influence could be exerted.

B) used to be a controller at the client, but now works for the PA firm.

C) owns ten percent of the shares of the client.

D) is a board member of the client with signing authority for cheques.

At every audit engagement, the auditor is required to consider that there could be

significant risks of misstatement for revenue recognition. At ABC Ltd., the auditor has

concluded that, yes, there are material risks of misstatement associated with revenue

recognition. How does this affect the extent of testing for accounts receivable?

A) audit risk will be increased

B) inherent risks will be decreased

C) decreased control testing is required

D) increased substantive testing is required

In the sales and collection cycle, the results of the tests of controls determine

A) the extent to which planned detection risk is satisfied for each accounts receivable

objective.

B) whether assessed control risk for sales and cash receipts needs to be revised.

C) if tests of details of balances need to be performed.

D) whether positive or negative confirmations should be used for this engagement.

The ASPE (Accounting Standards for Private Enterprises) financial reporting

framework normally requires the auditor to report using the corresponding figures

approach. This means that the auditor reports on

A) the current year’s financial statements.

B) both periods under audit, the current and prior year.

C) three years, the current and prior year, and the effects of the prior year.

D) only the ending balances of the general ledger accounts.

To test for recorded sales for which there were no actual shipments, the auditor traces

from the

A) bill of lading to the sales journal.

B) sales journal to the shipping documents.

C) sales journal to the accounts receivable subsidiary ledger.

D) bill of lading to the supporting customer order and sales order.

Ethical dilemmas occur when

A) you know what you want to do but the rules say otherwise.

B) businesses disregard the laws and engage in illegal behaviour.

C) a person chooses to act in his/her own interest.

D) a choice must be taken about appropriate behaviour.

The audit objective which requires the auditor to determine that notes payable on the

notes payable schedule are properly classified can be tested with the following

procedure.

A) Review the notes to determine whether any are with related parties.

B) Confirm notes payable.

C) Examine corporate minutes for loan approval.

D) Examine notes, minutes, and bank confirmations for restrictions.

Three conditions for fraud are referred to as the “fraud triangle.” One of the sides of this

triangle is incentives or pressures. The other two sides are

A) opportunities, a desire to meet debt repayment obligations.

B) opportunities, attitudes or rationalizations.

C) attitudes or rationalizations, the need to maintain stock prices.

D) the need to maintain stock prices and meet debt repayment obligations.

Which of the following items includes criteria for accepting a compilation engagement?

A) evaluation of whether the financial statements are in accordance with ASPE

B) no reason to believe that the financial statements are false or misleading

C) completion of an independence threat analysis, ensuring that there are no threats to

independence

D) completion of a client risk analysis, with the conclusion that risks are low

A) Discuss what is meant by the term “control environment” and identify four control

environment subcomponents that the auditor should consider.

B) List the steps that management follows in assessing risks relevant to the preparation

of financial statements in conformity with an applicable financial reporting framework.

C) How does the auditor obtain knowledge about management’s risk assessment

process?

D) Explain how management’s risk assessment process differs from the auditor’s risk

assessment process.

E) What is the relationship between management’s risk assessment process and audit

evidence?

Certain types of misstatements that affect cash may be detected in the audit of tests of

controls. Which of the following misstatements would be detected in the audit of the

acquisition and payment cycle?

A) Failure to bill a customer for goods shipped

B) Billing a customer at the incorrect price

C) Improper reimbursement of an officers’ personal expenses

D) Paying an employee at the incorrect wage rate

Which of the following illustrates the definition of auditing with respect to the evidence

analysis process?

A) accumulation and evaluation of evidence about balance sheet accounts

B) learning about different types of computing technology, such as mainframes

C) writing an operational audit report that is tailored to the client’s situation

D) making sure that the auditor is competent and understands evidence gathering

Anna performed a trend analysis of accounts receivable (AR) balances and computed

the days to collect AR ratio. When she compared the results of her analysis with the

industry averages, she found the results were unusually low compared to the industry

norm. Anna can conclude that

A) the accounts receivable balance is wrong.

B) the accounts receivable has an increased risk of misstatement.

C) the integrity of the company’s management is questionable.

D) she will not be able to rely on internal controls for accounts receivable for audit

purposes.

An underlying feature of the random-based selection of items is that each

A) stratum of the population be given equal representation in the sample.

B) each item in the population must be randomly ordered.

C) each item in the population should have an equal opportunity to be selected.

D) each item must be systematically selected using replacement.

From which of the following evidence-gathering audit procedures would an auditor

obtain most assurance concerning the existence of inventories?

A) observation of physical inventory counts

B) written inventory representations from management

C) confirmation of inventories in a public warehouse

D) auditor’s recomputation of inventory extensions

Since the audit of accounts payable generally takes a considerable amount of audit time,

effective internal controls, properly tested, can significantly reduce audit costs by

reducing

A) tests of controls.

B) confirmations.

C) tests of details of balances.

D) analytical procedures.

Which of the following internal control procedures will most likely prevent the

concealment of a cash shortage resulting from the improper write-off of a trade account

receivable? Write-offs must be

A) approved by a responsible officer after review of credit department

recommendations and supporting evidence.

B) supported by an aging schedule showing that only receivables overdue several

months have been written off.

C) approved by the cashier who is in a position to know if the accounts receivable have,

in fact, been collected.

D) authorized by company field sales employees who are in a position to determine the

financial standing of the customers.

Bigland and Betton, PAs, is being sued by a bank for potential negligence during an

audit engagement which was completed over five years ago. Which one of the

following actions during that audit engagement will help ensure that the suit is fairly

assessed?

A) good quality documentation

B) honest management at the client

C) low employee turnover

D) good employee memory of events

Jenny is the information technology support manager at CMH. Jenny is considered to

be a super-user at CMH since she can circumvent normal controls. In order to address

the risk of super-users, management should

A) remove the super-user.

B) establish effective compensating controls.

C) update the background check on the super-user on a yearly basis.

D) ensure that the super-user is familiar with the code of conduct of the company.

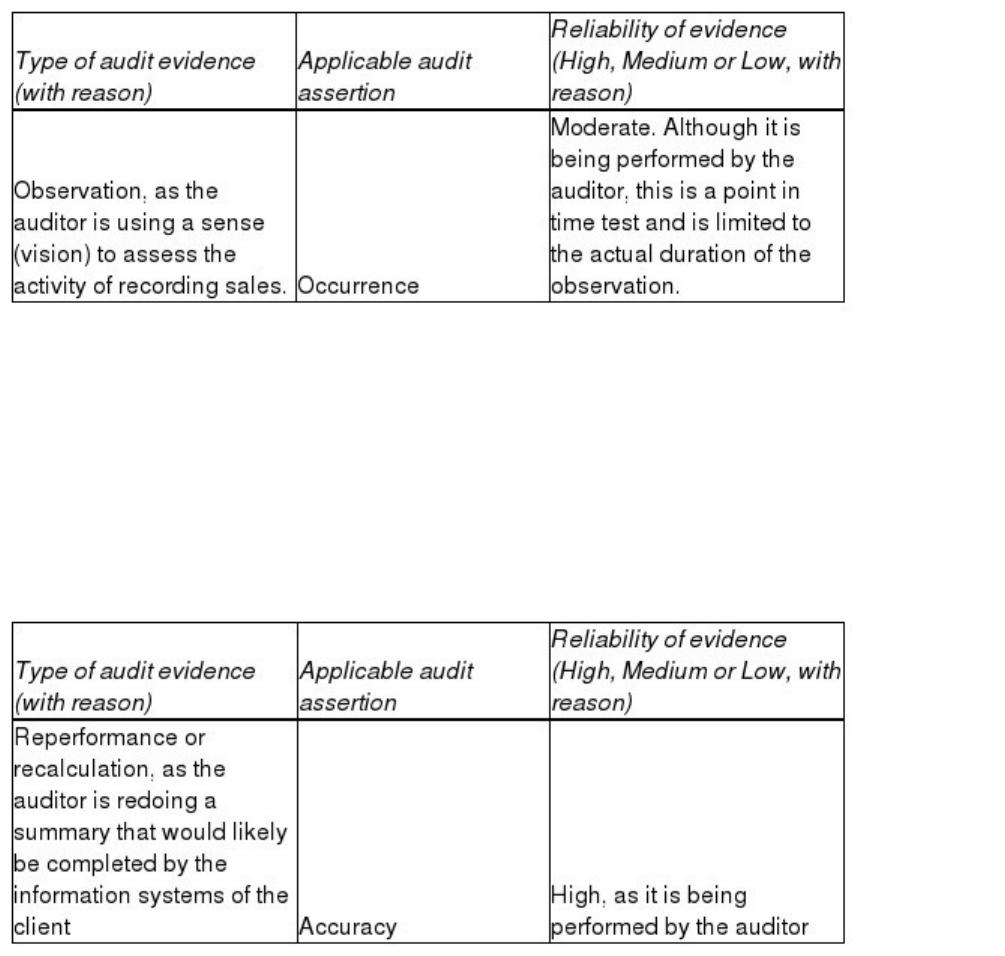

For each of the following audit procedures, state and describe the type of audit

evidence, state the audit assertion that it applies to, and describe the reliability of the

evidence (with reasons).

A) Watch staff scan products and enter cash received.

B) Reconcile daily cash drawer receipts (cash, debit card sales, credit card sales) with

daily sales for one week.

C) Calculate daily gross profit and gross profit by product line.

D) Account for a sequence of sales documents.

Once an understanding of internal controls is obtained that is sufficient for audit

planning, then the auditor must first assess

A) whether a lower level of control risk could be supported.

B) whether the financial statements are auditable.

C) the level of control risk supported by the understanding obtained.

D) the level of control risk to use.