Debits increase asset accounts and decrease liability accounts.

Revenue always is recognized once the buyer has physical possession of goods.

The expected postretirement benefit obligation (EPBO) is the discounted present value

of the total benefits expected to be paid by the employer to the plan participants.

A change from LIFO to any other inventory method is accounted for retrospectively.

Under federal securities laws, the SEC has the authority to set accounting standards in

the United States.

A change in reporting entity and a material error correction are both reported

prospectively.

The amount of the vested benefit obligation is less than the projected benefit obligation

and more than the accumulated benefit obligation.

If a seller makes payments to a customer to purchase goods and services, and those

payments are equal to the stand-alone selling prices of those goods and services, part of

those payments are a refund to the customer.

Activity-based methods of depreciation are appropriate for assets whose service life is a

function of use rather than time.

A company overstated its liability for warranties by $200,000. Its tax rate is 30%. As a

result of this error, income tax expense is:

a. Unaffected.

b. Overstated by $60,000.

c. Understated by $60,000.

d. Understated by $140,000.

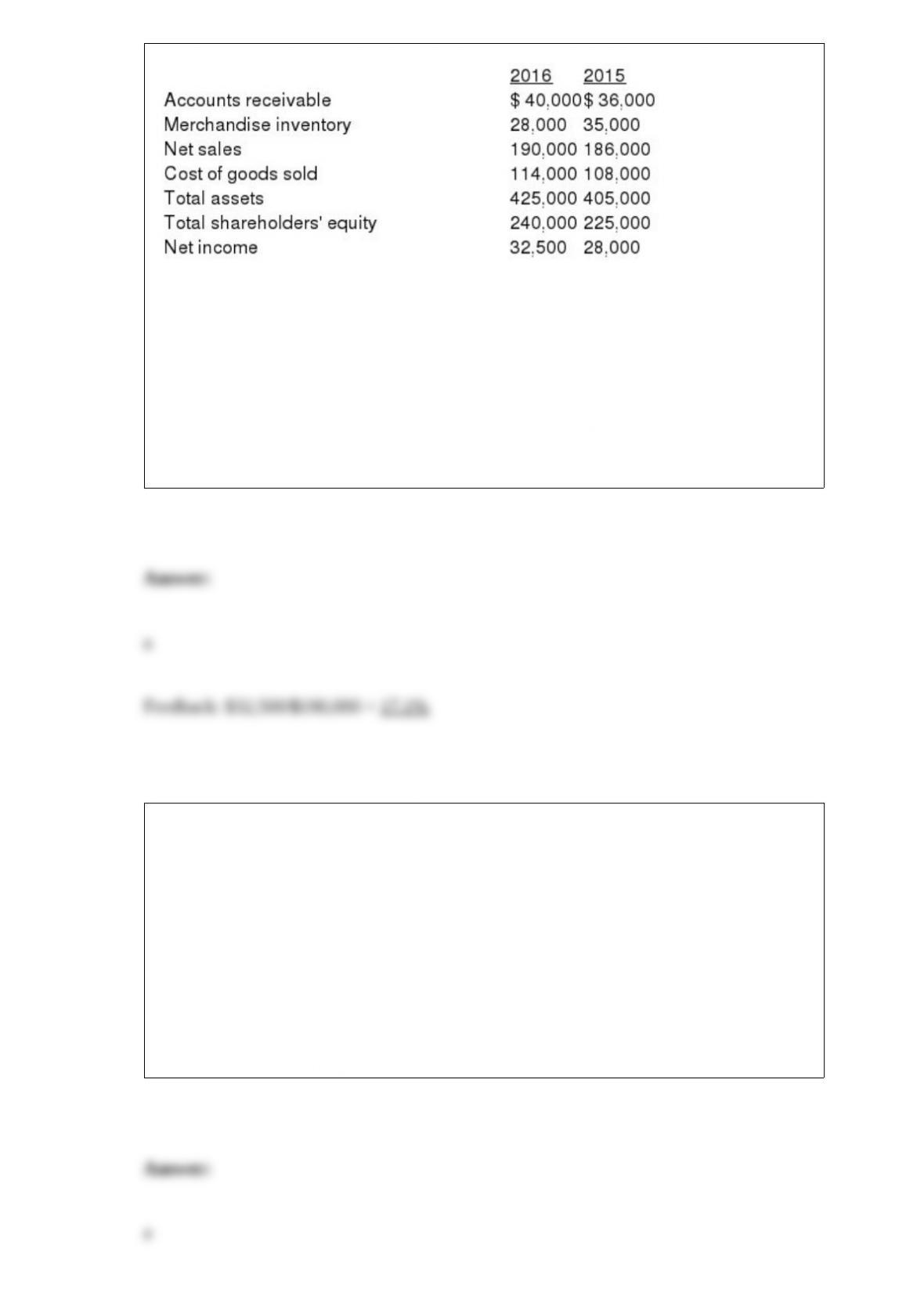

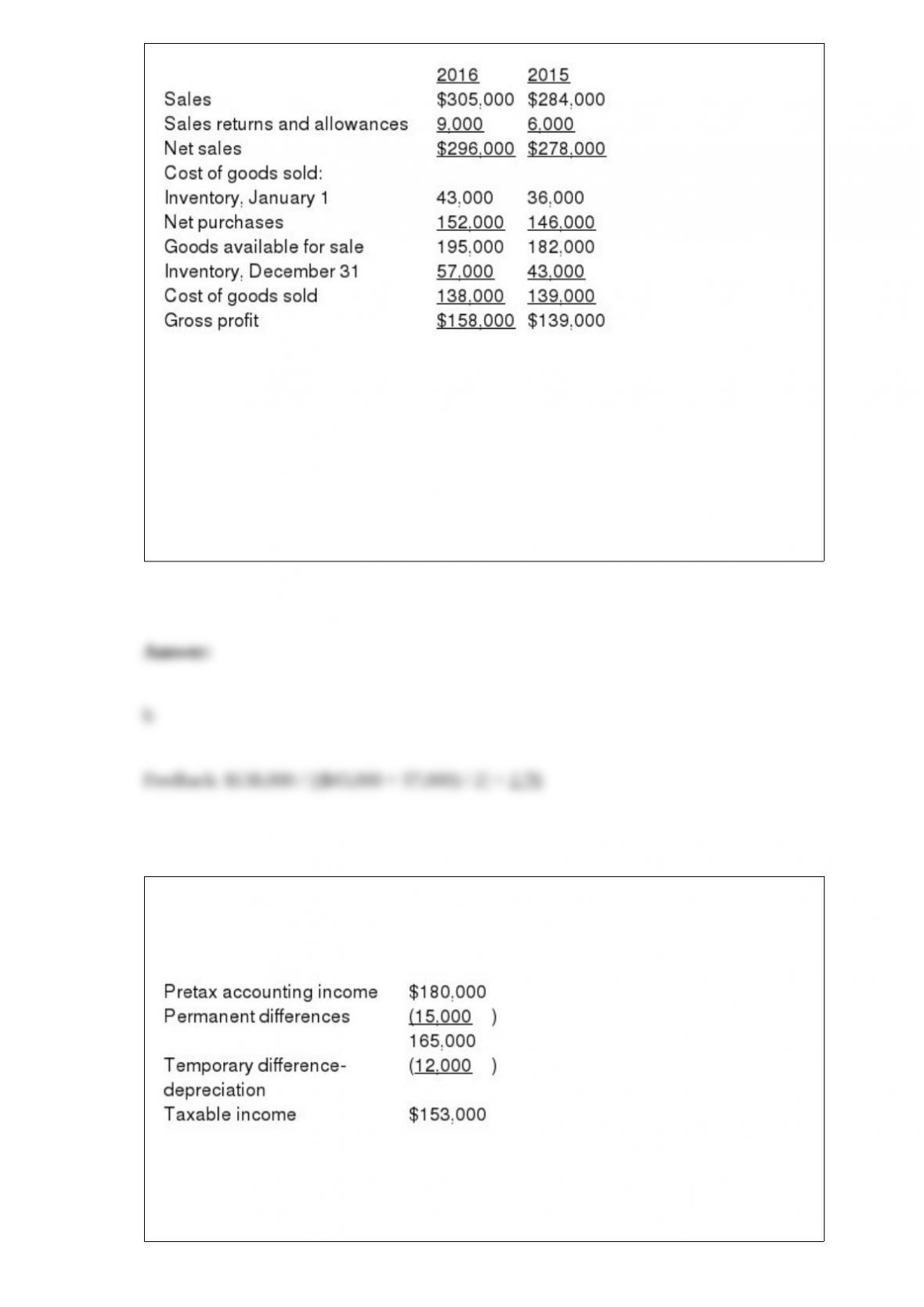

Excerpts from Hulkster Company’s December 31, 2016 and 2015, financial statements

are presented below:

Hulkster’s 2016 profit margin is (rounded):

a. 17.1%.

b. 13.5%.

c. 7.6%.

d. 4.5%.

The key accounting considerations relating to accounts payable are:

a. Determining their existence and ensuring that they are recorded in the appropriate

accounting period.

b. Determining their present value and ensuring that they are recorded in the

appropriate accounting period.

c. Determining their existence and determining the correct amount.

d. Determining the present value of the principal and the amount of the interest.

If Dizbert Company concluded that an investment originally classified as available for

sale would now more appropriately be classified as held to maturity, Dizbert would:

a. Not reclassify the investment, as original classifications are irrevocable.

b. Reclassify the investment as held to maturity and immediately recognize in net

income any unrealized gain or loss on the reclassification date.

c. Reclassify the investment as held to maturity and treat the fair value as of the date of

reclassification as the investment’s amortized cost basis for future amortization.

d. Need to restate earnings, as the original classification was in error.

Gershwin Wallcovering Inc. shipped the wrong shade of paint to a customer. The

customer agreed to keep the paint upon being offered a 15% price reduction. Gershwin

would record this reduction by crediting accounts receivable and debiting:

a. Sales.

b. Sales discounts.

c. Sales returns.

d. Sales allowances.

The lessee’s option to purchase a leased asset at a price that is sufficiently lower than

the asset’s expected fair value so that the exercise of the option appears reasonably

assured is called a:

a. Bargain purchase option.

b. Lessee buy-out option.

c. Lessor sell-out option.

d. Guaranteed purchase option.

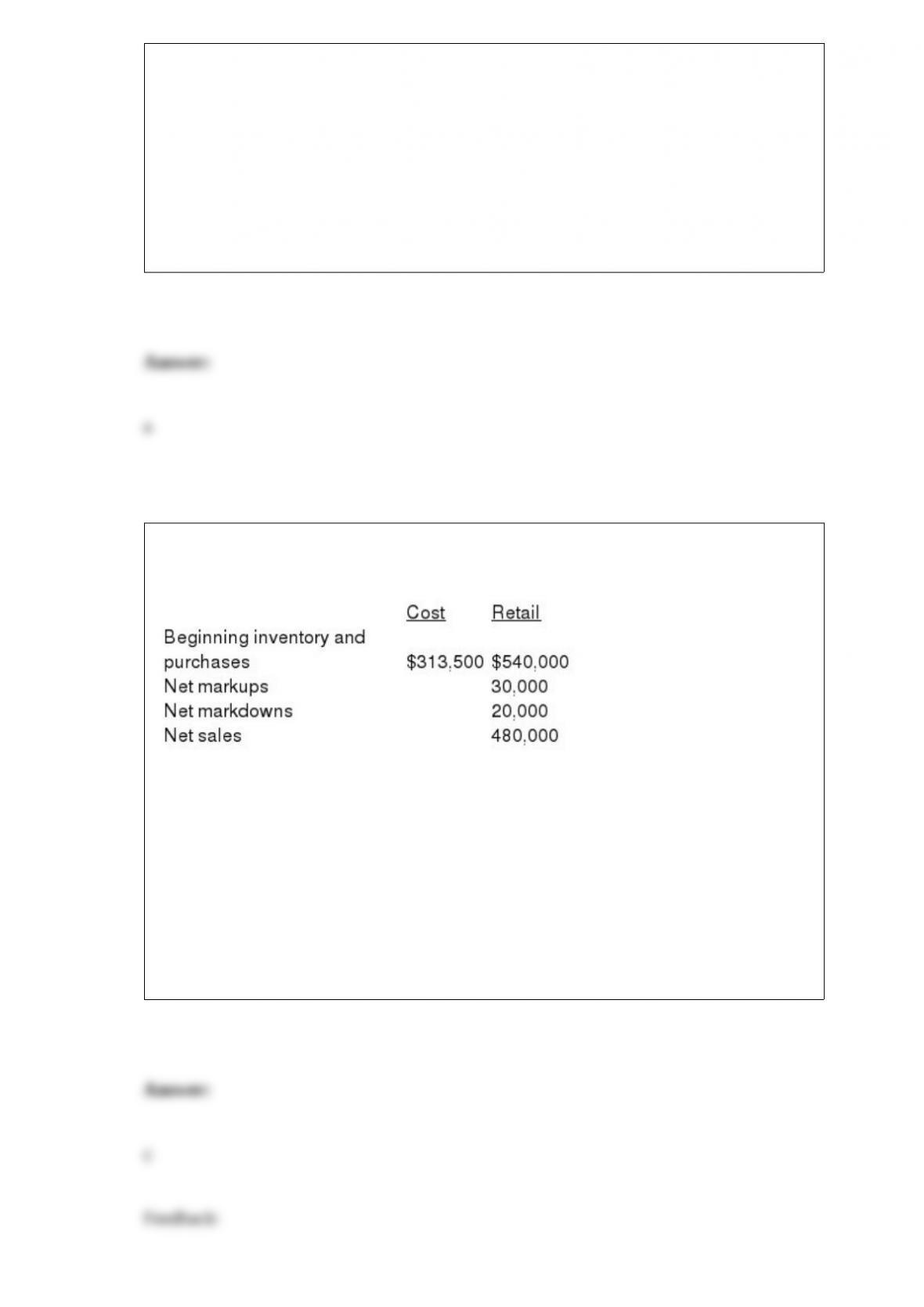

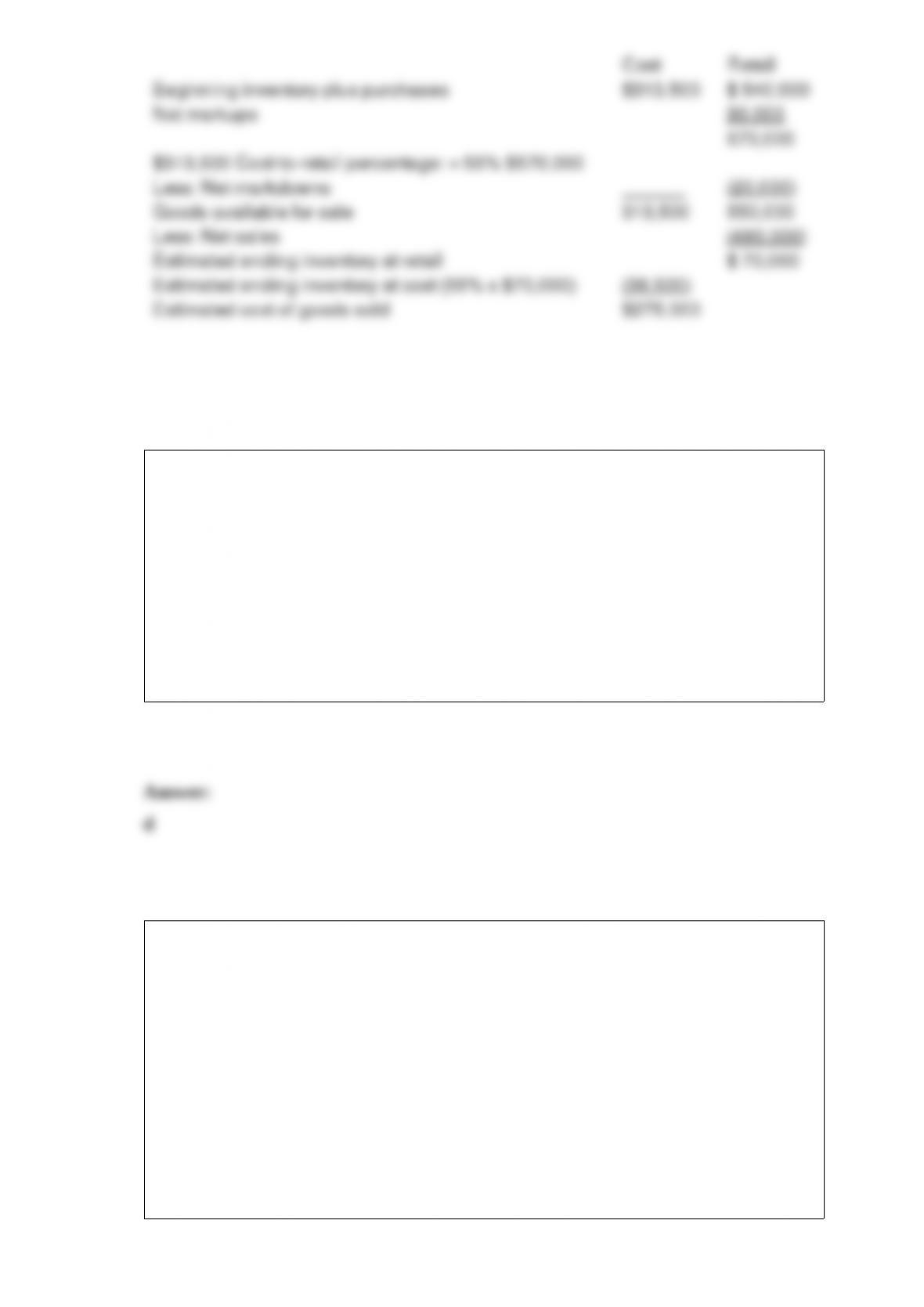

Cloverdale, Inc., uses the conventional retail inventory method to account for inventory.

The following information relates to current year’s operations:

What amount should be reported as cost of goods sold for the year?

a. $273,600.

b. $272,861.

c. $275,000.

d. None of these answer choices are correct.

Revenue and expense items and components of other comprehensive income can be

reported in the statement of shareholders’ equity using:

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

The compensation associated with a share of restricted stock under a stock award plan

is:

a. The market price of a share of similar fixed income securities.

b. The market price of an unrestricted share of the same stock.

c. The book value of an unrestricted share of the same stock.

d. The book value of a share of similar stock.

The conventional retail inventory method is based on:

a. Average cost.

b. LIFO cost.

c. Average, lower of cost and net realizable value.

d. LIFO, lower of cost and net realizable value.

When a tenant makes an end-of-period adjusting entry credit to the ‘œPrepaid rent’

account:

a. (S)he usually debits cash.

b. (S)he usually debits an expense account.

c. (S)he debits a liability account.

d. (S)he) credits an owners’ equity account.

Schneider Inc. had salaries payable of $60,000 and $90,000 at the end of 2015 and

2016, respectively. During 2016, Schneider recorded $620,000 in salaries expense in its

income statement. Cash outflows for salaries in 2016 were:

a. $590,000.

b. $620,000.

c. $650,000.

d. $530,000.

The preemptive right refers to the shareholder’s right to:

a. Maintain a proportional ownership interest in the corporation.

b. Vote for members of the board of directors.

c. Receive a share of dividends.

d. Share in profits proportionally with all other stockholders.

Anthony Thomas Candies (ATC) reported the following financial data for 2016 and

2015:

ATC’s inventory turnover ratio for 2016 is:

a. 2.42.

b. 2.76.

c. 3.21.

d. None of the above is correct.

Information for Kent Corp. for the year 2016:

Reconciliation of pretax accounting income and taxable income:

Cumulative future taxable amounts all from depreciation temporary differences:

As of December 31, 2015 $13,000

As of December 31, 2016 $25,000

The enacted tax rate was 30% for 2015 and thereafter.

What should be the balance in Kent’s deferred tax liability account as of December 31,

2016?

a. $5,200.

b. $7,500.

c. $25,000.

d. None of these answer choices are correct.

Common shareholders usually have all of the following rights except:

a. To share in the profits.

b. To share in assets upon liquidation.

c. To elect a board of directors.

d. To participate in the day-to-day operations.

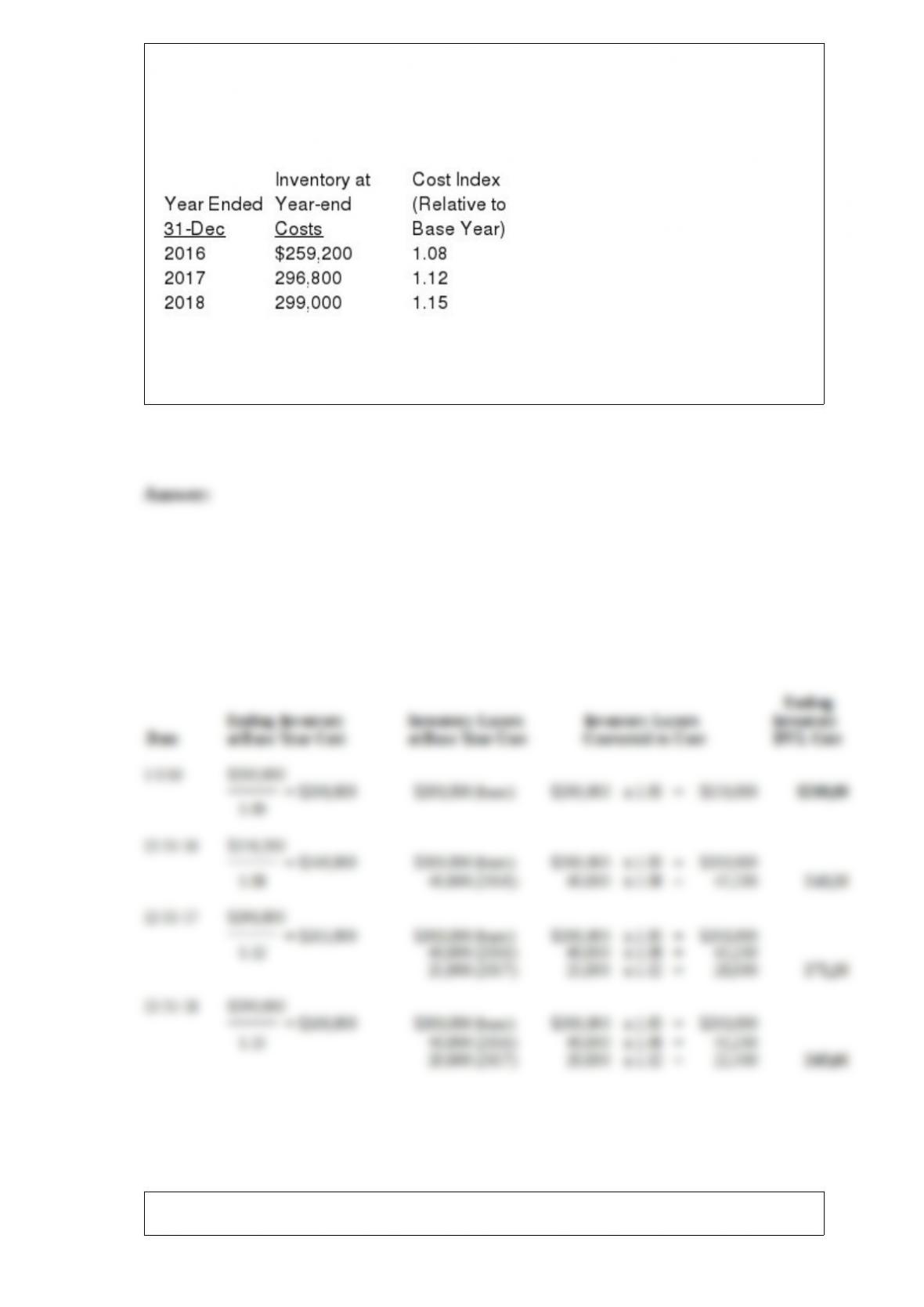

On January 1, 2016, the National Furniture Company adopted the dollar-value LIFO

method of computing inventory. An internal cost index is used to convert ending

inventory to base year. Inventory on January 1 was $200,000. Year-end inventories at

year-end costs and cost indexes for its one inventory pool were as follows:

Required:

Compute inventory amounts at the end of each year.

What activities are included in the statement of cash flows under the section titled

“Cash flows from financing activities”?

Prepare journal entries to record the following transactions of Daisy King Ice Cream

Company. If an entry is not required, state “No Entry.”

1> Started business by issuing 10,000 shares of capital stock for $20,000.

2> Signed a franchise agreement to pay royalties of 5% of sales.

3> Leased a building for three years at $500 per month and paid six months’ rent in

advance.

4> Purchased equipment for $5,400, paying $1,000 down and signing a two-year, 10%

note for the balance.

5> Purchased $1,800 of supplies on account.

6> Recorded cash sales of $800 for the first week.

7> Paid weekly salaries and wages, $320.

8> Paid for supplies purchased in item (5).

9> Paid royalties due on first week’s sales.

10> Recorded depreciation on equipment, $50.