1) Expulsion from the

A) True

B) False

2) Which of the following is the most effective control procedure to detect vouchers

that were prepared for the payment of goods that were not received?

A) Count goods upon receipt in storeroom

B) Match purchase order, receiving report, and vendor’s invoice for each voucher in

accounts payable department

C) Compare goods received with goods requisitioned in receiving department

D) Verify vouchers for accuracy and approval in internal audit department

3) The Independence Standards Board was formed to provide a conceptual framework

for independence issues related to audits of public companies.

A) True

B) False

4) Which of the following auditing procedures is ordinarily performed last?

A) reading minutes of the board of directors’ meetings

B) confirming accounts payable

C) obtaining a client representation letter

D) testing the purchasing function

5) Which of the following expenses is not typically evaluated as part of the audit of the

acquisition and payment cycle?

A) Depreciation expense

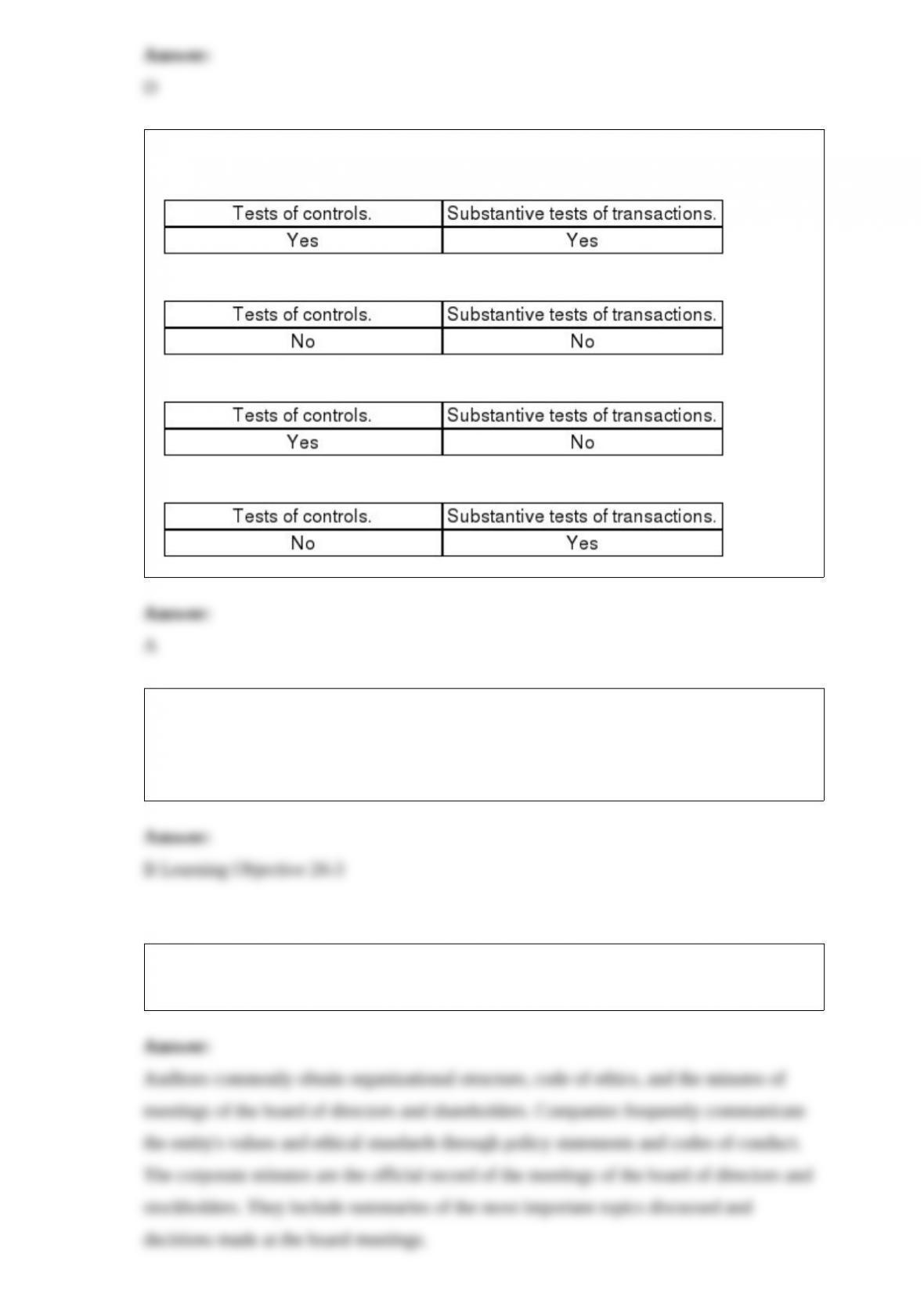

B) Insurance expense

C) Estimated Liability for Warranties

D) Property tax expense

6) For good internal control, the payroll function should be independent of the human

resources department.

A) True

B) False

7) Which of the following best defines fraud in a financial statement auditing context?

A) Fraud is an unintentional misstatement of the financial statements

B) Fraud is an intentional misstatement of the financial statements

C) Fraud is either an intentional or unintentional misstatement of the financial

statements, depending on materiality

D) Fraud is either an intentional or unintentional misstatement of the financial

statements, depending on consistency

8) The audit and accounting concern addressed in a monthly proof of cash is with:

A) adjusting account balances

B) reconciling the amounts per books and bank

C) determining the month-end balance

D) identifying cash transfers

9) The Credit Alliance approach to the concept of foreseen users states that to be liable

to third parties, an auditor (1) must know and intend that the work product would be

used by the third-party for a specific purpose, and (2) the knowledge and intent must be

evidenced by the auditor’s conduct.

A) True

B) False

10) When an auditor believes that an illegal act may have occurred, the first step he or

she should take is to gather additional evidence to determine the extent of the illegality.

A) True

B) False

11) The balance in the property tax expense account is most similar to:

A) depreciation expense

B) insurance expense

C) compensation expense

D) utilities expense

12) Prospective financial statements are for general use or for limited use. General use

refers to use by any third party, whereas limited use refers to use by third parties with

which the responsible party is negotiating directly. Which of the following statements is

not correct?

A) Forecasts can be provided for general use

B) Forecasts can be provided for limited use

C) Projections can be provided for general use

D) Projections can be provided for limited use

13) A proof of cash includes a reconciliation of cash receipts deposited in the bank with

the cash disbursements records for a given period.

A) True

B) False

14) Typically, analytical procedures are the primary means of verifying income

statement accounts resulting from allocations.

A) True

B) False

15) The auditor is concerned with the audited value rather than the error amount of each

item in the sample when using:

A) difference estimation

B) mean-per-unit estimation

C) ratio estimation

D) monetary-unit sampling

16) A common inventory observation procedure is to be alert for items that are

damaged, rust- or dust-covered, or located in inappropriate places. The balance-related

audit objective being achieved by this procedure is:

A) classification

B) cutoff

C) realizable value

D) rights

17) A vendor invoice is normally prepared at the time tangible goods are received and

indicates the description of goods, the quantity received, the date received, and other

relevant data.

A) True

B) False

18) For a private company audit, tests of controls are normally performed only on those

internal controls the auditor believes have not been operating effectively during the

period under audit.

A) True

B) False

19) To determine that sales are accurately recorded, the unit prices on the duplicate

sales invoices are normally compared with:

A) the original invoices

B) an approved master price list

C) the amounts recorded in the sales journal for that transaction

D) the amounts posted to the customer’s account in the accounts receivable master file

20) An important characteristic of IT is uniformity of processing. Therefore, a risk

exists that:

A) auditors will not be able to access data quickly

B) auditors will not be able to determine if data is processed consistently

C) erroneous processing can result in the accumulation of a great number of

misstatements in a short period of time

D) all of the above

21) Which of the following best expresses the requirement to establish with the client

an understanding of the responsibilities the auditor and company is taking for the audit

engagement?

A) Management asserts there are no material misstatements in the financials

B) Auditors assert that the primary audit goal is audit efficiency

C) Auditors assert that their primary responsibility is to plan and perform the audit in

order to provide reasonable assurance as to the detection of material misstatement due

to error or fraud

D) Management’s assertion that they will provide the auditor with a risk assessment as

to material misstatements due to errors or fraud in the company’s financial statements

22) The most important means of verifying account balances in the payroll and

personnel cycle are:

A) tests of controls and substantive tests of transactions

B) analytical procedures and tests of controls

C) analytical procedures and substantive tests of transactions

D) tests of controls and tests of details of balances

23) Which of the following statements is not correct?

A) There are many ways an auditor can accumulate evidence to meet overall audit

objectives

B) Sufficient appropriate evidence must be accumulated to meet the auditor’s

professional responsibility

C) It is appropriate to minimize the cost of accumulating evidence

D) Gathering evidence and minimizing costs are equally important considerations that

affect the approach the auditor selects

24) Both sampling and nonsampling risks are associated with:

A)

B)

C)

D)

25) The “Red Book” specifies all auditing standards issued by the U.S. General

Accounting Office.

A) True

B) False

26) What documents do auditors routinely obtain to aid in their understanding of a

client’s governance system? Briefly discuss each of these documents.

27) List and briefly describe the three conditions for fraud arising from fraudulent

financial reporting and misappropriation of assets as described in SAS No. 99.

28) Identify each of the seven factors that influence sample size for nonstatistical tests

of details of balances, and state whether each factor is directly or inversely related to

sample size.

29) Internal controls over year-end cash balances in the general account can be divided

into two categories. List the two below.

30) Two types of attestation services provided by CPA firms are audits and reviews.

Discuss the similarities and differences between these two types of attestation services.

Which type provides the least assurance?

31) Discuss the internal controls related to owners’ equity that are of concern to the

auditor.

32) Describe how the auditor tests the accuracy objective for accounts receivable.

33) Describe the audit procedures used to verify the accuracy and detail tie-in

objectives for prepaid insurance.

34) The most common fraud in the acquisition and payment cycle is for the fraudster to

issue payments to fictitious vendors and deposit the cash in fictitious accounts. What

procedures could the company take to prevent this type of fraud?

35) The following is a portion of an adverse audit report issued for a public company.

(Note: A separate report was issued on the effectiveness of internal control over

financial reporting.)

Independent Auditor’s Report

To the shareholders of Wallace Corporation

We have audited the accompanying balance sheet of Wallace Corporation as of

December 31, 2012, and the related statements of income, retained earnings, and cash

flows for the year then ended. These financial statements are the responsibility of the

company’s management. Our responsibility is to express an opinion on these financial

statements based on our audit.

We conducted our audit in accordance with the standards of the Public Company

Accounting Oversight Board (United States). Those standards require that we plan and

perform the audit to obtain reasonable assurance about whether the financial statements

are free of material misstatement. An audit includes examining, on a test basis, evidence

supporting the amounts and disclosures in the financial statements. An audit also

includes assessing the accounting principles used and significant estimates made by

management, as well as evaluating the overall financial statement presentation. We

believe that our audit provides a reasonable basis for our opinion.

The company has excluded from property and debt in the accompanying balance sheet

certain lease obligations that, in our opinion, should be capitalized in order to conform

with generally accepted accounting principles. If these lease obligations were

capitalized, property would be increased by $14,500,000, long-term debt by

$13,200,000, and retained earnings by $1,300,000 as of December 31, 2012, and net

income and earnings per share would be increased by $1,300,000 and $2.25,

respectively, for the year then ended.

Required:

Complete the above adverse audit report by preparing the opinion paragraph. Do not

date or sign the report.