1) The overall objective in the audit of the acquisition and payment cycle is:

A) to ensure the reliability of the affected accounts

B) to ensure the accuracy of the affected accounts

C) to evaluate whether the affected accounts are fairly stated in accordance with

accounting standards

D) to evaluate whether fraudulent payments were made

2) When an outside specialist has assumed full responsibility for taking the client’s

physical inventory, reliance on the specialist’s report is acceptable if:

A) the auditor’s report contains a reference to the assumption of full responsibility

B) the auditor is satisfied through application of appropriate procedures as to the

reputation and competence of the specialist

C) the auditor conducted the same audit tests and procedures as would have been

applicable if the client’s employees took the physical inventory

D) circumstances made it impracticable or impossible for the auditor either to do the

work personally or observe the work done by the inventory firm

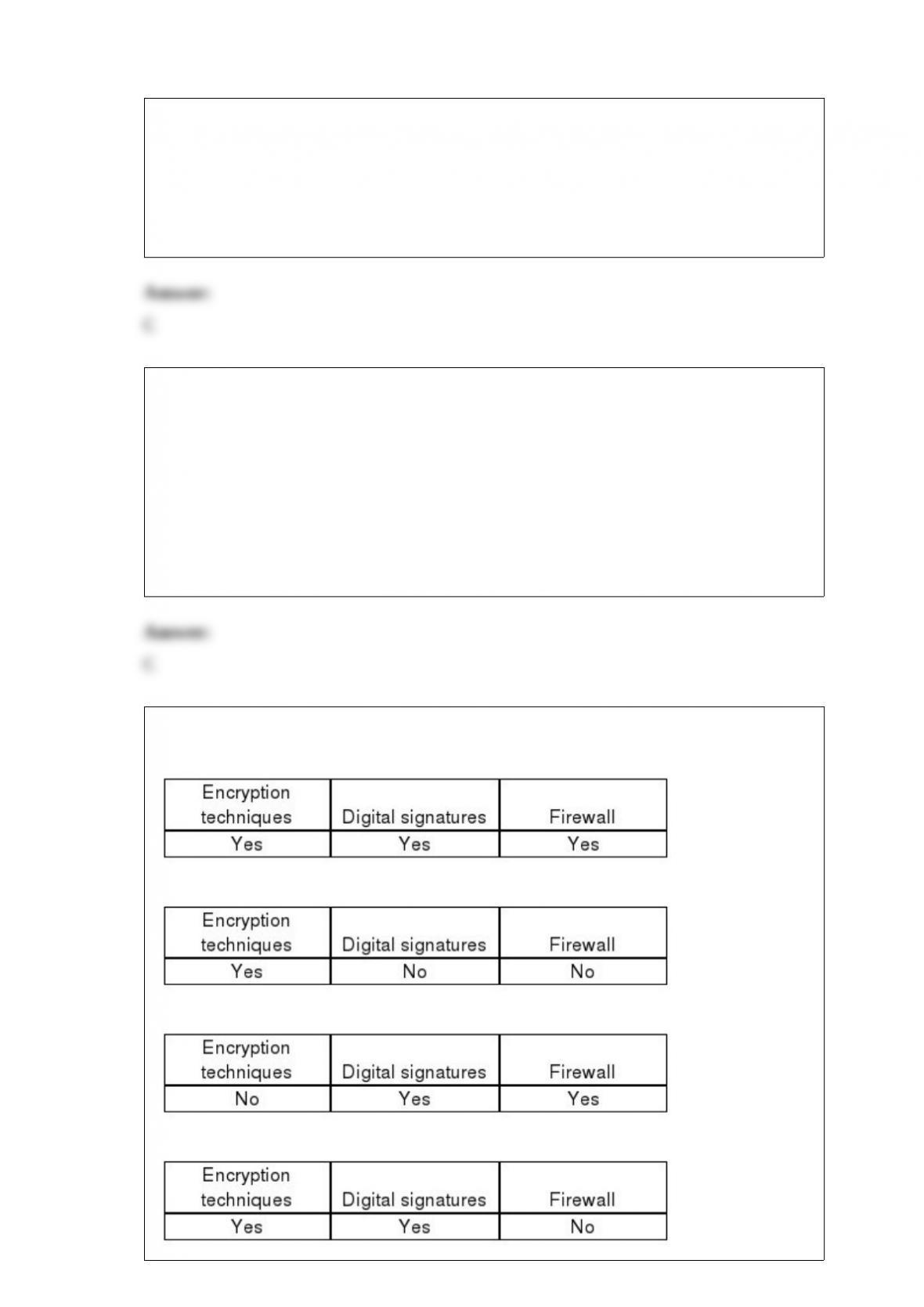

3) What tools do companies use to limit access to sensitive company data?

A)

B)

C)

D)

4) The shareholders’ capital stock master file is used as the basis for the payment of

dividends and also acts as a check on the accuracy of the common stock balance in the

general ledger.

A) True

B) False

5) Auditing standards recommend that auditors observe physical inventory counts by

the client.

A) True

B) False

6) When auditing a private company, the auditor should obtain an understanding of

internal control sufficient to:

A) provide reasonable protection against client fraud and defalcations by client

employees

B) assess control risk

C) provide a basis for suggestions to the client for improving the accounting system

D) provide a method for safeguarding assets, checking the accuracy and reliability of

accounting data, promoting operational efficiency, and encouraging adherence to

prescribed managerial policies

7) Section 404 requires auditors to perform walkthroughs to assist in understanding

internal control.

A) True

B) False

8) Which of the following statements is correct regarding non-audit services that are not

prohibited by Sarbanes-Oxley or SEC?

A) They must be approved by management of the client

B) They must be approved by staff of the PCAOB

C) They must be approved by staff of the PCAOB and the SEC

D) They must be approved by the company’s audit committee

9) SAS No. 99 requires auditors to document which of the following matters related to

the auditor’s consideration of material misstatements due to fraud?

A) Reasons supporting a conclusion that there is not a significant risk of material

improper expense recognition

B) Procedures performed to obtain information necessary to identify and assess the

risks of material fraud

C) Results of the internal auditor’s procedures performed to address the risk of

management override of controls

D) Discussions with management regarding separation of duties

10) You are determining the significance of the following: you set a 5% risk of

assessing control risk to low and your computation of the upper deviation risk is 7%.

What could you conclude?

A) There is a 95% chance the deviation rate is the population is less than 5%

B) There is a 5% chance the deviation rate in the population is less than 7%

C) There is a 95% chance the deviation rate in the population exceeds 95%

D) There is a 5% chance the deviation rate in the population exceeds 7%

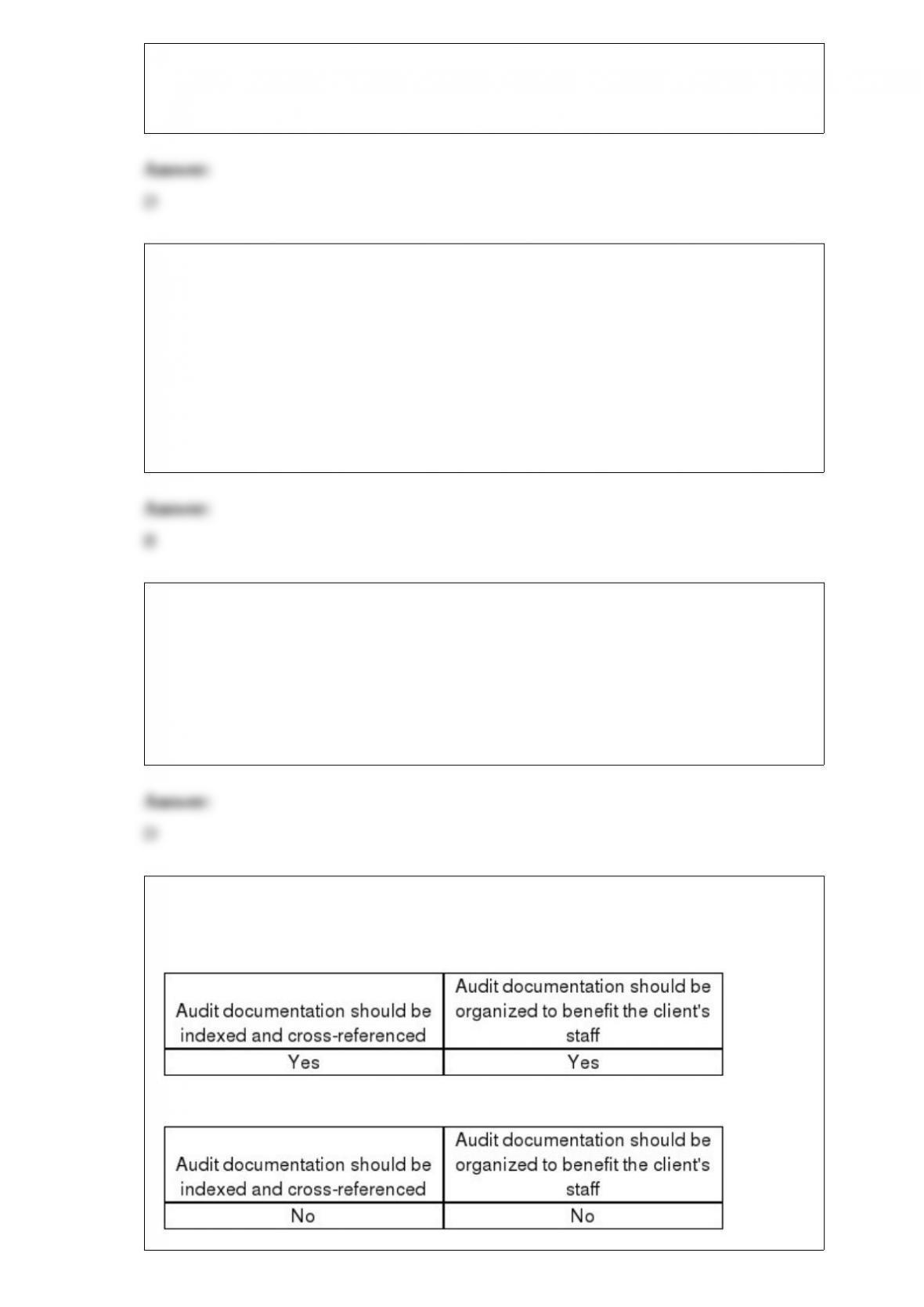

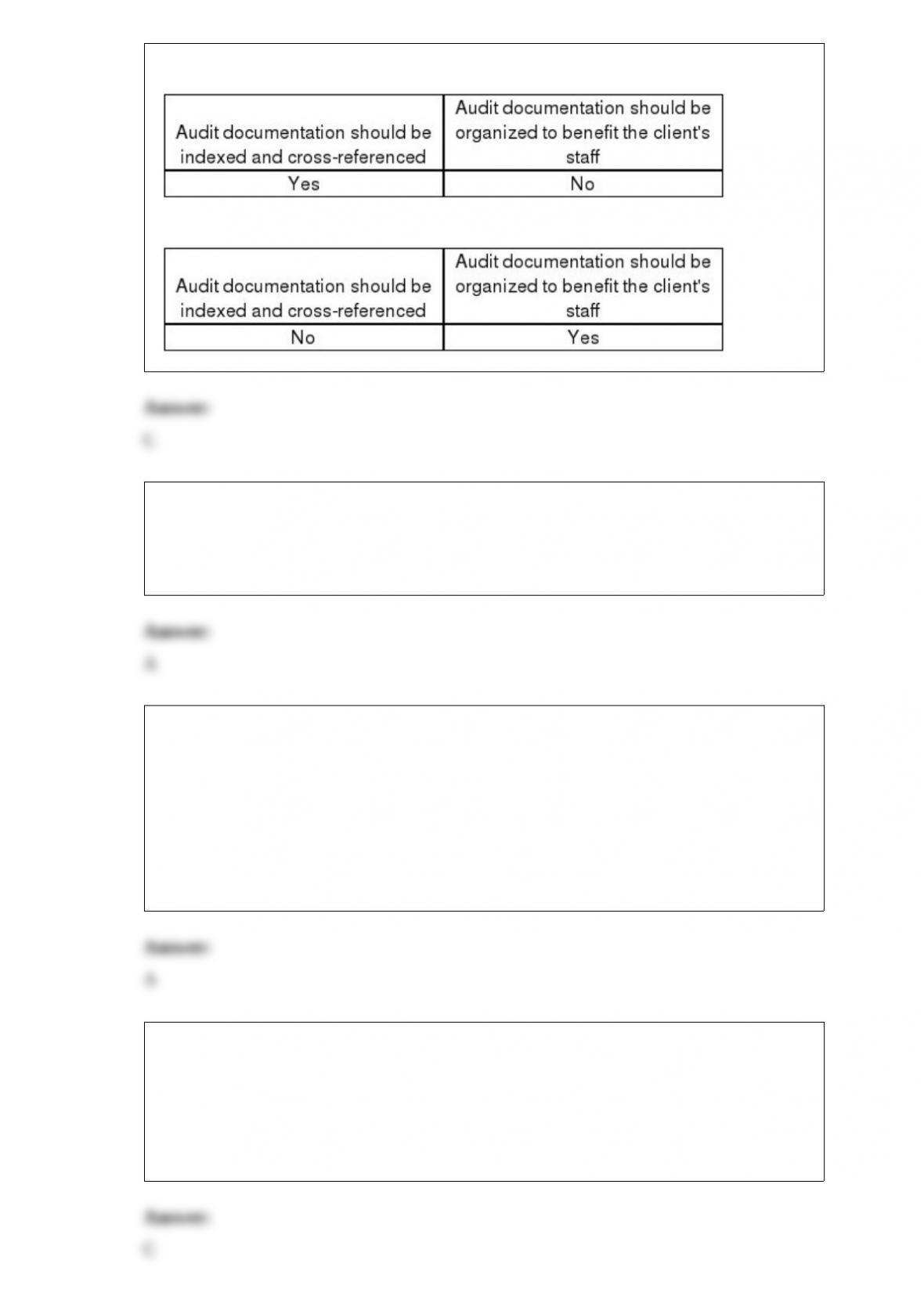

11) Audit documentation should possess certain characteristics. Which of the following

is true regarding those characteristics?

A)

B)

C)

D)

12) All of the Big Four and many of the smaller CPA firms now operate as Limited

Liability Partnerships.

A) True

B) False

13) Which of the following is not an essential component of quality control?

A) Policies and procedures to ensure that firm personnel are actively engaged in

marketing strategies

B) Policies and procedures to ensure that the work performed by firm personnel meet

applicable professional standards

C) Policies to ensure that personnel maintain their independence in fact and in

appearance

D) Policies that ensure that monitoring activities are effectively applied

14) The auditor’s starting point for verifying disposals of property, plant, and equipment

is the:

A) equipment account in the general ledger

B) file of shipping documents

C) client’s schedule of recorded disposals

D) equipment subsidiary ledger

15) Companies may intentionally understate earnings when income is high to create a

reserve of “earnings” that may be used in future years to increase earnings. This practice

is known as:

A) performance-based management

B) earnings management

C) asset management

D) expense management

16) Auditors involved in planning, performing, or reporting on audits under GAGAS

must complete ________ hours of continuing professional education in each two-year

period.

A) 20

B) 40

C) 60

D) 80

17) “Physical control over assets” is not a type of control that is applicable to the

payroll cycle.

A) True

B) False

18) When performing planning analytical procedures for a client the auditor detected

that the gross profit percentage had declined by 50% from the previous year to the year

currently under audit. The auditor should:

A) investgate the possibility the client may have made an error in their cost of goods

sold computation

B) assist management in developing greater cost efficiencies in their product line

C) prepare a going concern opinion for the client

D) advise the client to have extensive disclosure to alleviate investor concerns

19) In estimating the population misstatement, the first step in projecting from the

sample to the population is to:

A) make a point estimate

B) revise the upper error bound

C) calculate the precision interval

D) determine the population mean

20) When a disclaimer is issued because the auditor lacks independence:

A) no report title is included on the report

B) a one-paragraph audit report is issued

C) the only reason cited for issuing the disclaimer is the lack of independence

D) all of the above are correct

21) Generally, auditors assess inherent risk as moderate for related party transactions

because they expect clients to be aware of their scrutiny of such transactions.

A) True

B) False

22) The audit procedure “Examine notes payable, minutes, and bank confirmations for

restrictions” is performed when verifying the classification objective for notes payable.

A) True

B) False

23) The introductory paragraph of the standard audit report performs which functions?

I.State the CPA has performed an audit.

II.Lists the financials being audited.

III.States the financials are the responsibility of the auditor.

A) I and II

B) I and III

C) II and III

D) I, II and III

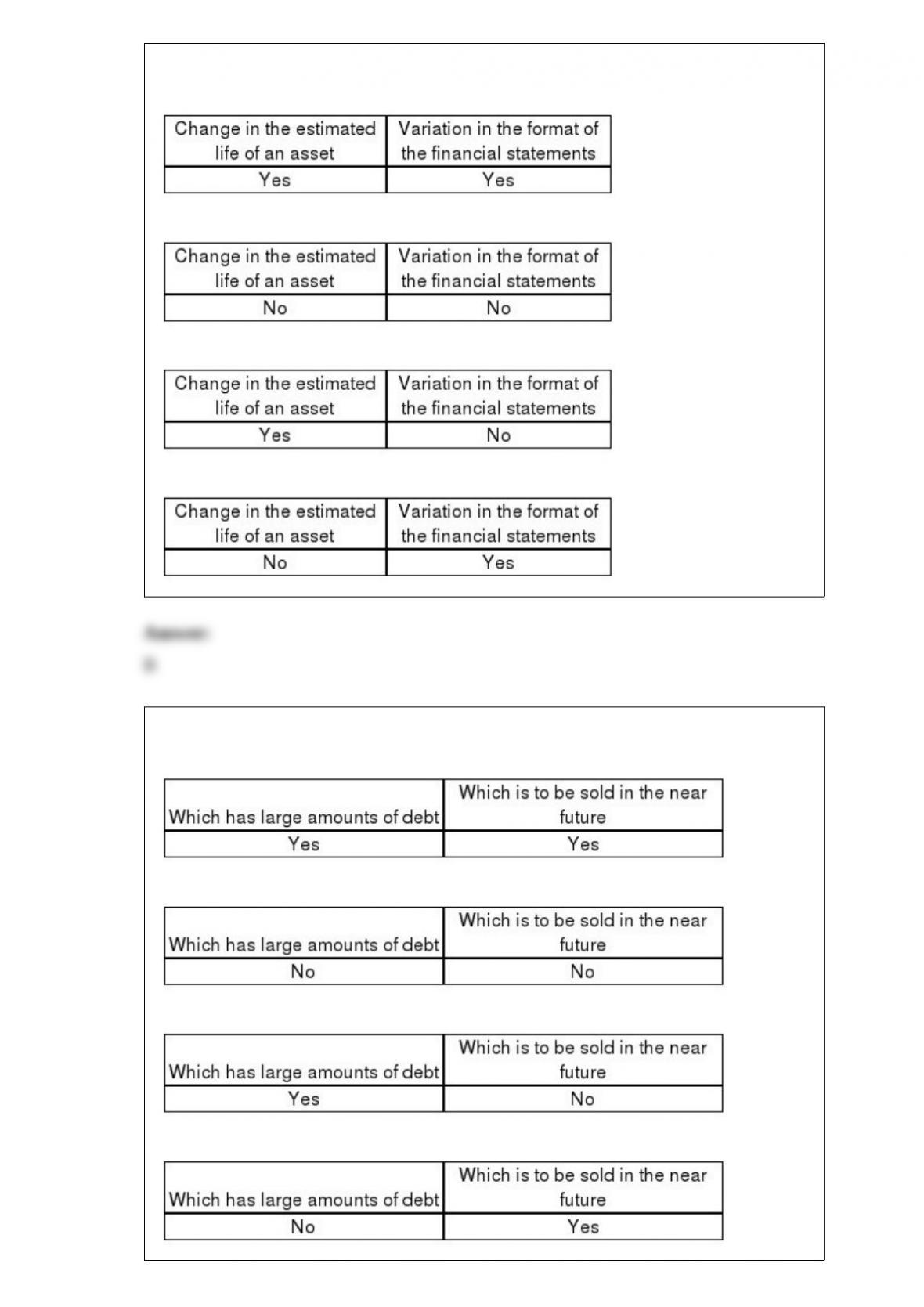

24) Indicate which changes would require an explanatory paragraph in the audit report.

A)

B)

C)

D)

25) The auditor is likely to accumulate more evidence when the audit is for a company:

A)

B)

C)

D)

26) Which of the following is the most objective type of evidence?

A) A letter written by the client’s attorney discussing the likely outcome of outstanding

lawsuits

B) The physical count of securities and cash

C) Inquiries of the credit manager about the collectability of noncurrent accounts

receivable

D) Observation of cobwebs on some inventory bins

27) Auditing standards indicate that reasonable assurance is a moderate, but not

absolute, level of assurance that the financial statements are free of material

misstatement.

A) True

B) True

28) Debt compliance letters are ordinarily addressed to:

A) underwriters of securities

B) the client’s audit committee

C) creditor financial institutions

D) the Securities and Exchange Commission

29) The test of transactions which requires one to “reconcile recorded cash

disbursements with the cash disbursements on the bank statement” satisfies the

objective of:

A) occurrence

B) completeness

C) accuracy

D) posting and summarization

30) A CPA has received an attorney’s letter in which no significant disagreements with

the client’s assessments of contingent liabilities were noted. The resignation of the

client’s lawyer shortly after receipt of the letter should alert the auditor that:

A) an adverse opinion will be necessary

B) undisclosed unasserted claims may have arisen

C) the auditor must begin a completely new examination of contingent liabilities

D) the attorney was unable to form a conclusion with respect to the significance of

litigation, claims, and assessments

31) Written communication that the auditor will provide reasonable assurance for the

detection of fraud is found in:

A) engagement letter

B) representation letter

C) responsibility letter

D) client letter

32) A procedure designed to test for monetary misstatements directly affecting the

correctness of financial statement balances is a:

A) test of controls

B) substantive test

C) test of attributes

D) monetary-unit sampling test

33) Which of the following occurrences would be least likely to warrant further audit

attention for the auditor?

A) Deviations from client’s established control procedures

B) Deviations from client’s budgeted values

C) Monetary misstatements in populations of transaction data

D) Monetary misstatements in populations of account balance details

34) If the client’s internal control for recording sales returns and allowances is evaluated

as ineffective:

A) a larger sample may be needed to verify cutoff

B) sampling is not appropriate

C) all sales returns must be traced to supporting documentation

D) all sales returns must be confirmed with the customer

35) Imprest accounts usually carry a significant balance.

A) True

B) False

36) Match seven of the terms for documents and records (a-k) used in the payroll and

personnel cycle with the descriptions provided below (1-7):

a.Human resource records

b.Deduction authorization form

c.Rate authorization form

d.Time card

e.Job time ticket

f.Summary payroll report

g.Payroll check

h.W-2 form

i.Payroll tax returns

j.Payroll journal

k.Payroll master file

________ 1> A file used for recording payroll transactions for each employee and

maintaining total employee wages paid for the year to date.

________ 2> A document indicating the time the hourly employee started and stopped

working.

________ 3> A document written in exchange for services received from an employee.

________ 4> Forms submitted to local, state, and federal units of government for the

payment of withheld taxes and the employer’s tax.

________ 5> A form authorizing payroll deductions, including the number of

exemptions for withholding of income taxes, U.S. savings bonds, and union dues.

________ 6> A form used to authorize the amount of pay.

________ 7> Records including date of employment, personnel investigations, rates of

pay, etc.

37) Although systematic sample selection is easy to use, its primary disadvantage is that

it is not a probabilistic sampling method.

A) True

B) False