1) At December 31, 2011, an Enterprise Fund has the following adjusted accounts

outstanding:

Insurance Expense$2,000

Depreciation Expense3,000

Supplies Expense10,000

Salaries Expense100,000

Service Revenues123,000

When preparing the closing entry for the temporary accounts at December 31, 2011, the

Enterprise Fund’s accountant will

A) credit Retained Earnings $8,000

B) credit Net Cash, $8,000

C) credit Net Assets, Unrestricted $8,000

D) credit Invested Capital Assets, Net of Related Debt, $8,000

2) Percy Inc. acquired 80% of the outstanding stock of Sillson Company in a business

combination. The book values of Sillson’s net assets are equal to the fair values except

for the building, whose net book value and fair value are $500,000 and $800,000,

respectively. At what amount is the building reported on the consolidated balance sheet?

A) $400,000

B) $500,000

C) $640,000

D) $800,000

3) Pyming Corporation accounts for its 40% investment in Sillabog Company using the

equity method. On the date of the original investment, fair values were equal to the

book values except for a patent, which cost Pyming an additional $40,000. The patent

had an estimated life of 10 years. Sillabog has a steady net income of $20,000 per year

and consistently pays out 40% of its net income as dividends to its shareholders. Which

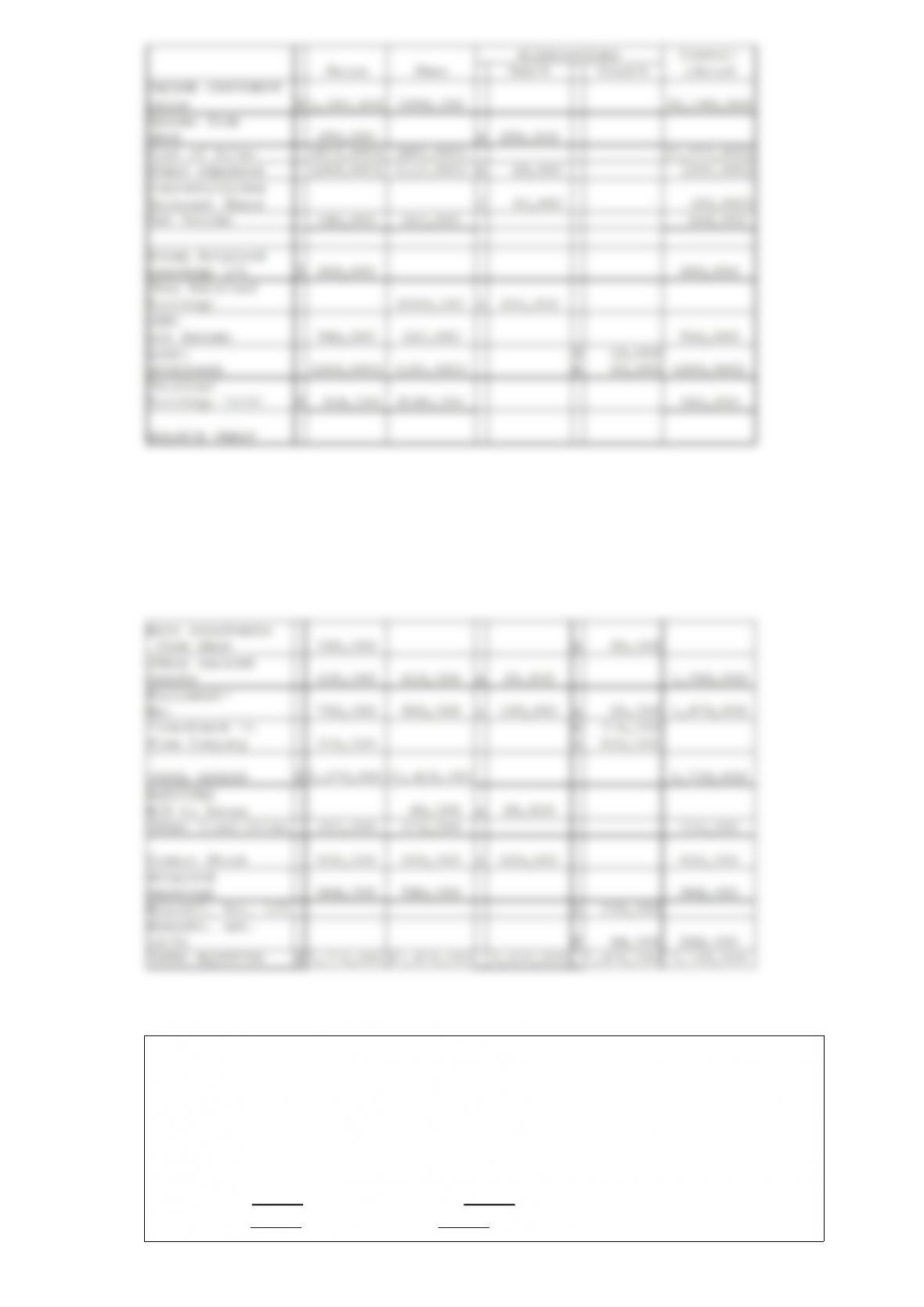

one of the following statements is correct?

A) The net change in the investment account for each full year will be a debit of $8,000

B) The net change in the investment account for each full year will be a debit of $4,800

C) The net change in the investment account for each full year will be a debit of $800

D) The net change in the investment account for each full year will be a credit of $800

4) Which of the following securities has the lowest interest rate?

A) Junk bonds

B) US Treasury bonds

C) Investment-grade bonds

D) Corporate Baa bonds

5) Jacana Corporation paid $200,000 for a 25% interest in Lilypad Corporation’s

common stock on January 1, 2010, but was not able to exercise significant influence

over Lilypad. During 2011, Jacana reported income of $120,000, excluding its income

from Lilypad, and paid dividends of $50,000. Lilypad reported net income of $40,000

during 2011 and paid dividends of $20,000. Jacana should report net income for 2011 in

the amount of

A) $115,000

B) $120,000

C) $125,000

D) $130,000

6) Which of the following statements is true regarding forward contracts, futures

contracts, options and swaps?

A) A forward contract can be purchased on the open market and is recorded at its

historical cost, then adjusted for changes in the market

B) A futures contract is negotiated between two parties who are betting in the opposite

direction on the movement of the underlying price

C) An option is a contract requiring the holder to either “put” or “call” an underlying

asset at a specified point in time

D) A swap is a contract between two parties to exchange an ongoing stream of cash

flows

7) On January 1, 2012, Pauline Company acquired 90% of Stephen Company at a cost

of $90,000. On January 1, 2012, Stephen Company acquired 10% of Pauline Company

at a cost of $10,000.

On January 1, 2012, the following data is available:

Stephen CompanyPauline Company

Common Stock$50,000Common Stock$50,000

Retained Earnings$50,000Retained Earnings$50,000

Assets fair value$100,000Assets fair value$100,000

Assets book value$100,000Assets book value$100,000

Liabilities$0Liabilities$0

At December 31, 2012, the following data is available:

January 1, 2012December 31, 2012

On Pauline Books:

Investment in Stephen$90,000$105,000

On Stephen Books:

Investment in Pauline$10,000$10,000

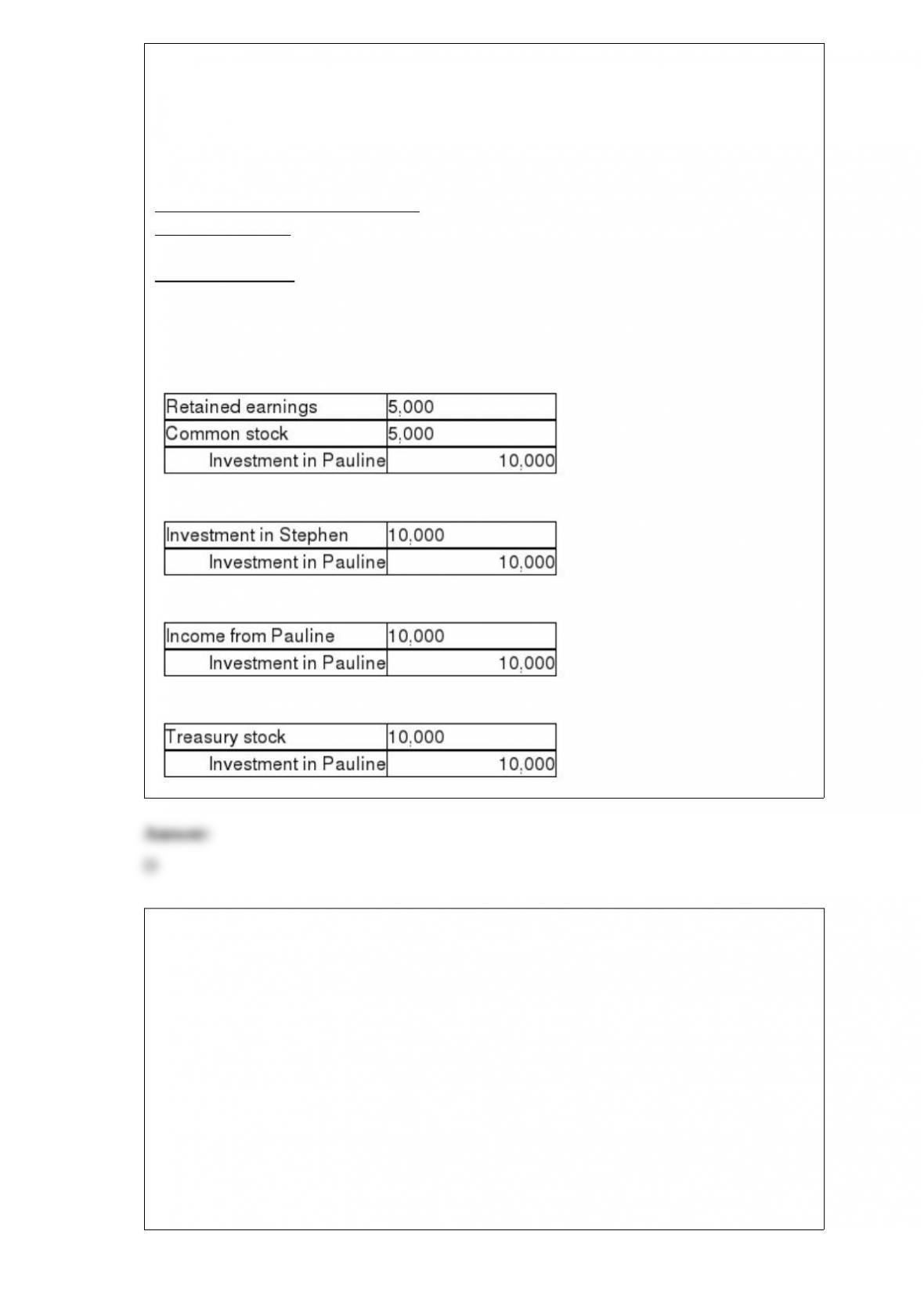

Assuming the treasury stock method is used, what elimination entry is needed for the

Investment in Pauline at December 31, 2012?

A)

B)

C)

D)

8) Pahm Corporation owns 80% of the outstanding voting common stock of Abussi

Corporation, which was purchased for $60,000 over Abussi’s book value. The excess

purchase price was attributable to goodwill. Abussi Corporation owns 60% of the

outstanding common stock of Badock Corporation, which was purchased at book value.

The separate net incomes of Pahm, Abussi, and Badock (excluding investment income)

for the year are $200,000, $240,000, and $260,000, respectively. There were no fair

value/book value differences in the assets and liabilities of Pahm, Abussi and Badock.

The amount of income for the current year assigned to the noncontrolling shareholders

of Badock Corporation is

A) $100,000

B) $104,000

C) $120,000

D) $140,000

9) On January 1, 2011, Plastam Industries acquired an 80% interest in Sparta Company

to assure a steady supply of Sparta’s inventory that Plastam uses in its own

manufacturing businesses. Sparta sold 100% of its output to Plastam during 2011 and

2012 at a markup of 125% of Sparta’s cost. Plastam had $12,000 of these items

remaining in its inventory at December 31, 2012 . If Plastam neglected to eliminate

unrealized profits from all intercompany sales from Sparta, the inventory on the

consolidated balance sheet at December 31, 2012 was

A) overstated by $1,920

B) understated by $1,920

C) overstated by $2,400

D) understated by $2,400

10) Pouch Corporation acquired an 80% interest in Shenley Corporation on January 1,

2012, when the book values of Shenley’s assets and liabilities were equal to their fair

values. The cost of the 80% interest was equal to 80% of the book value of Shenley’s

net assets. During 2012, Pouch sold merchandise that cost $70,000 to Shenley for

$86,000. On December 31, 2012, three-fourths of the merchandise acquired from Pouch

remained in Shenley’s inventory. Separate incomes (investment income not included) of

the two companies are as follows:

PouchShenley

Sales Revenue $180,000 $160,000

Cost of Goods Sold 120,00090,000

Operating Expenses 17,000 21,000

Separate incomes$ 43,000$ 49,000

The consolidated income statement for Pouch Corporation and subsidiary for the year

ended December 31, 2012 will show consolidated cost of sales of

A) $120,000

B) $136,000

C) $148,000

D) $210,000

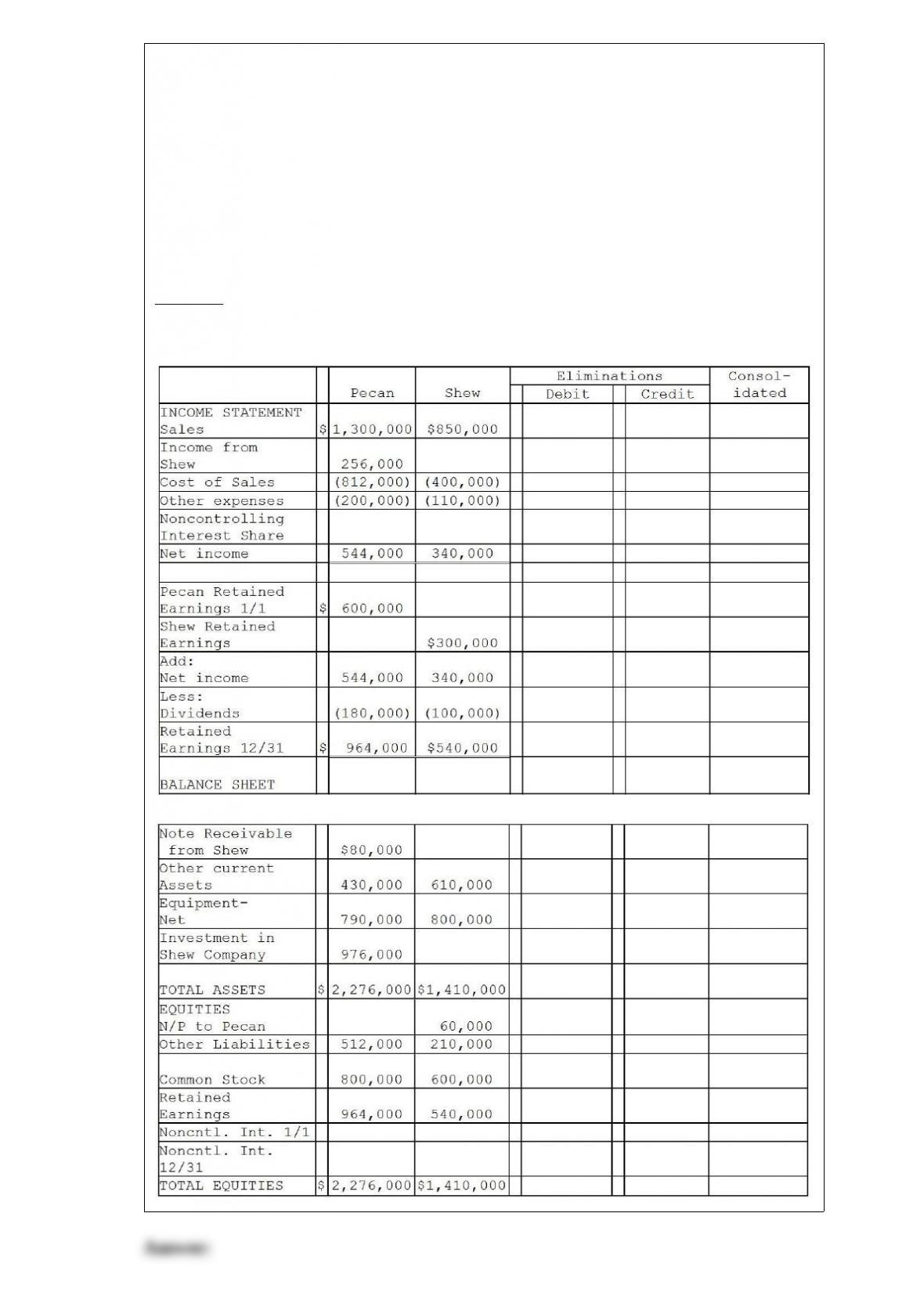

11) Pecan Incorporated acquired 80% of the voting stock of Shew Manufacturing for

$800,000 on January 2, 2011 when Shew had outstanding common stock of $600,000

and Retained Earnings of $300,000. The book value and fair value of Shew’s assets and

liabilities were equal except for equipment. The entire fair value/book value differential

is allocated to equipment and is fully depreciated on a straight-line basis over a 5-year

period.

During 2011, Shew borrowed $80,000 on a short-term non-interest-bearing note from

Pecan, and on December 31, 2011, Shew mailed a check for $20,000 to Pecan in partial

payment of the note. Pecan deposited the check on January 4, 2012, and recorded the

entry to reduce the note balance at that time.

Required:

Complete the consolidation working papers for the year ended December 31, 2011 .

12) On June 30, 2011, the Able, Baker, and Charlie partnership had the following fiscal

year-end balance sheet:

Cash$8,000Accounts payable$14,000

Accounts receivable12,000Loan from Charlie10,000

Inventory28,000Able, capital (20%)28,000

Plant assets-net24,000Baker, capital (20%)20,000

Loan to Able12,000Charlie,capital (60%)12,000

Total assets$84,000Total liab./equity$84,000

The percentages shown are the residual profit and loss sharing ratios. The partners

dissolved the partnership on July 1, 2011, and began the liquidation process. During

July the following events occurred:

*Receivables of $6,000 were collected.

*All inventory was sold for $8,000.

*All available cash was distributed on July 31, except for

$4,000 that was set aside for contingent expenses.

How much cash would Baker receive from the cash that is available for distribution on

July 31? (Assume a safe payments schedule is used.)

A) $ 0

B) $ 800

C) $2,400

D) $4,000

13) The Deferred Revenue account in government accounting is frequently used for

A) taxes billed that are not expected to be collected within 60 days of the fiscal year end

B) taxes billed that are not expected to be collected based on a bad debt percentage

history

C) taxes that are to be remitted from another government agency in the second month

before the fiscal year end

D) taxes that are to be remitted from another government agency in the first month after

the fiscal year end

14) If bonds with different maturities are perfect substitutes, then the ________ on these

bonds must be equal

A) expected return

B) surprise return

C) surplus return

D) excess return

15) If a corporation begins to suffer large losses, then the default risk on the corporate

bond will

A) increase and the bond’s return will become more uncertain, meaning the expected

return on the corporate bond will fall

B) increase and the bond’s return will become less uncertain, meaning the expected

return on the corporate bond will fall

C) decrease and the bond’s return will become less uncertain, meaning the expected

return on the corporate bond will fall

D) decrease and the bond’s return will become less uncertain, meaning the expected

return on the corporate bond will rise

16) What basis of accounting is used by proprietary funds?

A) Modified accrual accounting

B) Accrual accounting

C) Cash basis accounting

D) Fair value accounting

17) Parrot Company owns all the outstanding voting stock of Southern Manufacturing.

On January 1, 2012, Parrot sold machinery to Southern at its book value of $24,000.

Parrot had the machinery three years before selling it and used an eight-year

straight-line depreciation method, with zero salvage value. Southern will use the

straight-line depreciation method, and assumes the machine has five years remaining

and no salvage value. In the 2012 consolidating working papers, the depreciation

expense

A) required no adjustment

B) decreased by $4,800

C) increased by $4,800

D) increased by $8,000

18) Paris Corporation purchased 80% of the outstanding voting common stock of

Sanders Corporation on January 1, 2011, at a cost of $400,000. The stockholders’ equity

of Sanders Corporation on this date consisted of $200,000 of Capital Stock and

$100,000 of Retained Earnings. Book values were equal to fair values except for land

and inventory. The book value of Sanders’ land was $10,000, and fair value was

$22,000. The book value of Sanders’ inventory was $30,000, and fair value was

$25,000.

Under the entity theory, what amount of goodwill was reported on the consolidated

balance sheet at December 31, 2011?

A) $185,000

B) $191,250

C) $193,000

D) $200,000

19) Plateau Incorporated bought 60% of the common stock of Sachet Company several

years ago. At the time of purchase, the fair value and book value of Sachet’s net assets

were equal. The cost of the 60% investment was equal to 60% of the book value of

Sachet’s net assets. Plateau sells merchandise to Sachet at 125% above Plateau’s cost.

Intercompany sales from Plateau to Sachet for 2012 were $60,000. Unrealized profits in

Sachet’s December 31, 2011 inventory and December 31, 2012 inventory were $6,000

and $4,500, respectively. Sachet reported net income of $120,000 for 2012 .

Required: In General Journal format, prepare consolidation working paper entries at

December 31, 2012 to eliminate the effects of the intercompany inventory sales.

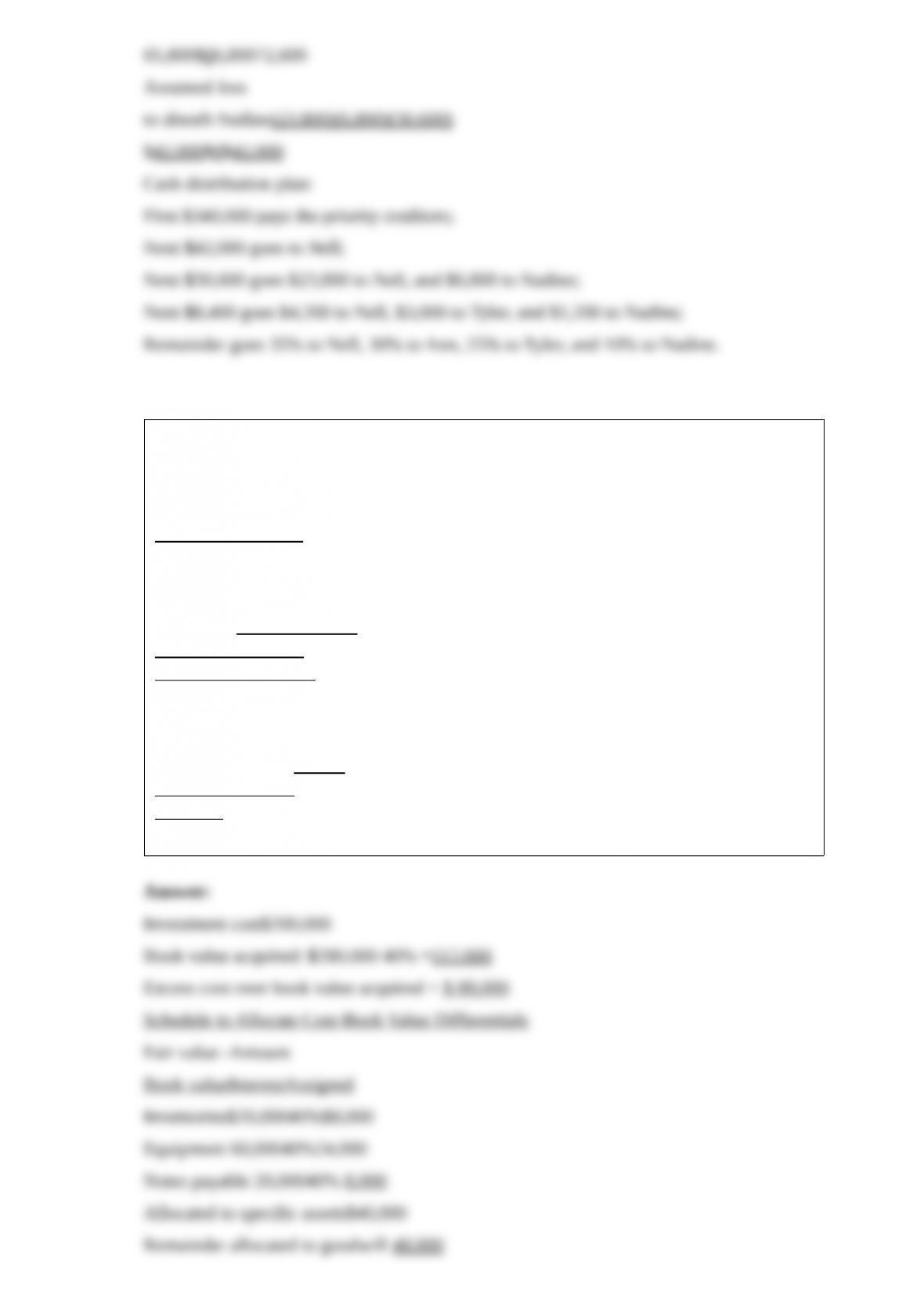

20) The partners of Nelatyna Manufacturing have decided to dissolve their partnership

as of the end of 2010 . The partnership is going to liquidate during the first several

months of 2011 . The four partners of Nell, Ann, Tyler and Nadine, share profits and

losses 35%, 30%, 25%, and 10%, respectively. The partnership trial balance at

December 31, 2010 is as follows:

DebitsCredits

Cash$60,000

Accounts receivable150,000

Inventory115,000

Loan to Tyler20,000

Furniture86,000

Equipment147,000

Goodwill63,000

Accounts payable$140,000

Note payable200,000

Loan from Nell30,000

Nell, capital (35%)110,000

Ann, capital (30%)60,000

Tyler, capital (25%)73,000

Nadine, capital (10%)28,000

Totals$641,000$641,000

Required:

Prepare a cash distribution plan for January 1, 2011, showing how cash installments

will be distributed among the partners as it becomes available. Prepare vulnerability

rankings for the partners and a schedule of assumed loss absorption.

21) Dotterel Corporation paid $200,000 cash for 40% of the voting common stock of

Swamp Land Inc. on January 1, 2011 . Book value and fair value information for

Swamp on this date is as follows:

BookFair

AssetsValuesValues

Cash$60,000$60,000

Accounts receivable120,000120,000

Inventories80,000100,000

Equipment340,000400,000

$ 600,000$ 680,000

Liabilities & Equities

Accounts payable$200,000$200,000

Note payable120,000100,000

Capital stock200,000

Retained earnings 80,000

$600,000$300,000

Required:

Prepare an allocation schedule for Dotterel’s investment in Swamp Land.

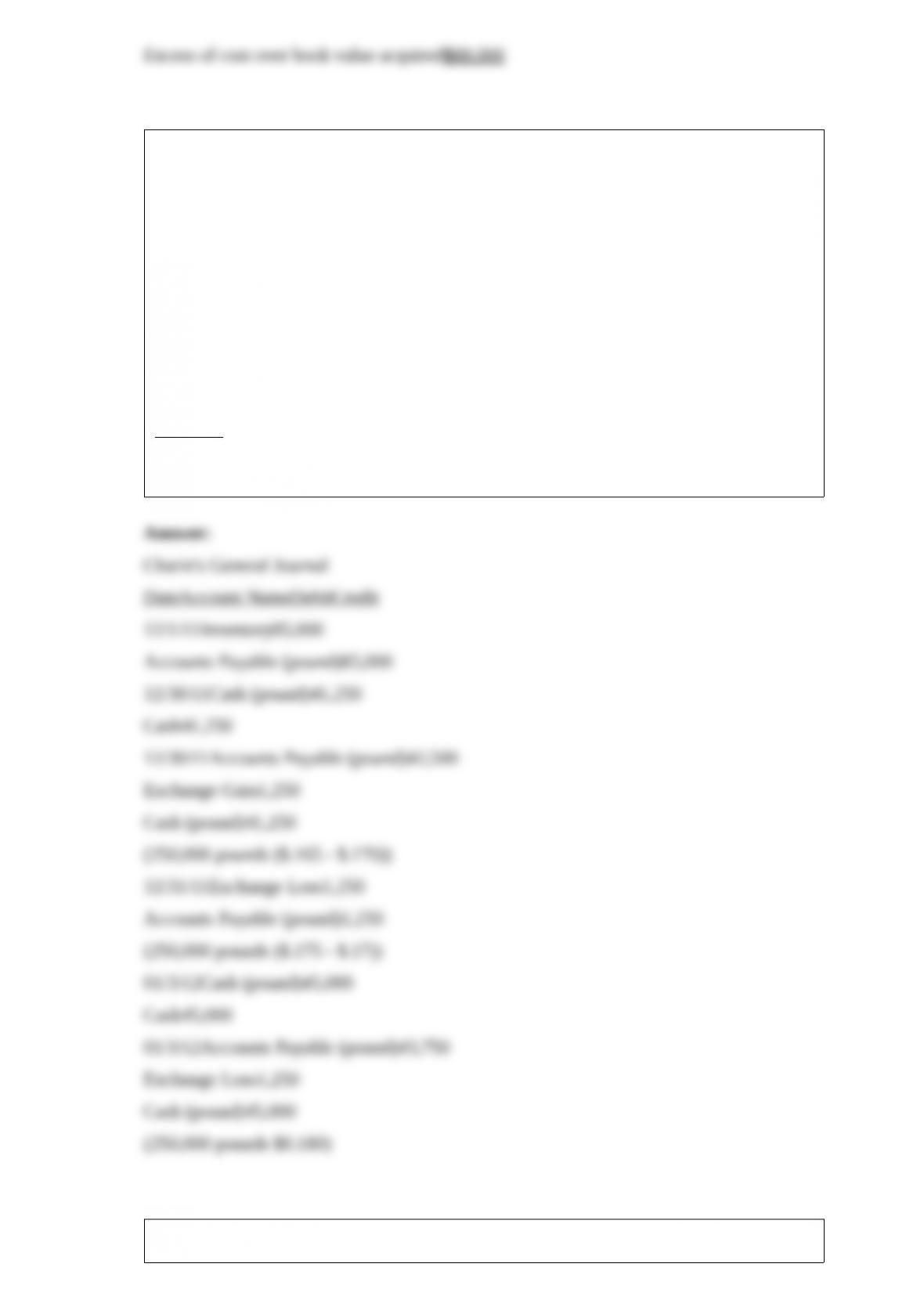

22) Charin Corporation, a U.S. corporation, imports and exports small electronics. On

December 1, 2011, Charin purchased components from an Egyptian manufacturer

amounting to 500,000 Egyptian pounds. The purchase is payable in Egyptian pounds.

At December 30, Charin wanted to take advantage of favorable exchange rates, but did

not have the full amount required to pay off the entire amount. Charin wired the funds

to pay off half of the balance owed, and expected to pay the remaining balance on

January 3, 2012 . Charin paid the remaining balance on January 3, 2012 .

The respective exchange rates were as follows:

December 1, 20111 pound = $.170

December 30, 20111 pound = $.165

December 31, 20111 pound = $.175

January 3, 20121 pound = $.180

Required:

Document the journal entries related to these transactions for the four dates shown. If

no entry is required, record “no entry.”

23) Platt Corporation paid $87,500 for a 70% interest in Suve Corporation on January

1, 2011, when Suve’s Capital Stock was $70,000 and its Retained Earnings $30,000.

The fair values of Suve’s identifiable assets and liabilities were the same as the recorded

book values on the acquisition date. Trial balances at the end of the year on December

31, 2011 are given below:

PlattSuve

Cash$4,500$20,000

Accounts Receivable26,00030,000

Inventory100,00080,000

Investment in Suve87,500

Cost of Goods Sold60,00040,000

Operating Expenses22,00037,000

Dividends15,00010,000

$315,000$217,000

Liabilities$47,000$27,000

Capital stock, $10 par value100,00070,000

Additional Paid-in Capital10,000

Retained Earnings31,00030,000

Sales Revenue120,00090,000

Dividend Income7,0000

$315,000$217,000

During 2011, Platt made only two journal entries with respect to its investment in Suve.

On January 1, 2011, it debited the Investment in Suve account for $87,500 and on

November 1, 2011, it credited Dividend Income for $7,000.

Required:

1>Prepare a consolidated income statement and a statement of retained earnings for

Platt and Subsidiary for the year ended December 31, 2011 .

2>Prepare a consolidated balance sheet for Platt and Subsidiary as of December 31,

2011 .

24) Willborough County had the following transactions in 2012 .

1>A central motor pool was established with a $200,000 nonreciprocal transfer from the

General Fund.

2>The water and sewer authority, which provides services to residents for a fee, issued

a bond offering at $750,000 par. Bonds proceeds are restricted to renovating the

treatment facility.

3>Willborough received a grant from the state to be used for renovation of the

courthouse amounting to $800,000. The General Fund will temporarily provide

$100,000 cash, because the grant is set up on a reimbursement basis and will not be

distributed until proper expenditures are documented.

4>Willborough’s central motor pool bills out automobile usage to various government

agencies amounting to $42,000.

5>The General Fund transfers $67,000 out of the operating budget to fund the county

employees’ pension plan.

Required:

Prepare the necessary journal entries for each of the above transactions for all funds

affected. Be sure to identify the fund type for each entry.

25) Suzanne Quincy passed away on October 25, 2011 . Suzanne left behind a limited

estate, so there are no tax issues to address, however, she owned a dog, Buddy, and

Suzanne provided for Buddy in the will. Suzanne left $100,000 for Buddy’s care, and

the remainder of her estate was left to her neighbor, Agnes. Suzanne’s estate had the

following events and transactions in the month following her death.

1>Her assets were converted to cash at their fair value as inventoried: Mutual funds,

$270,000; and Residence, $209,000. There were no other reportable assets.

2>Transferred $100,000 to a trust account at Second National Bank to provide care for

Buddy, and delivered Buddy to Paws and Claws Pet Farm, his new home.

3>Wrote check to pay for funeral expenses for $9,600.

4>Wrote check to pay for executor fees as designated in the will of $1,000.

5>Wrote check to pay balance of estate to Agnes.

Required:

Prepare the journal entries for the listed transactions. Disregard the impact of estate and

income taxes.

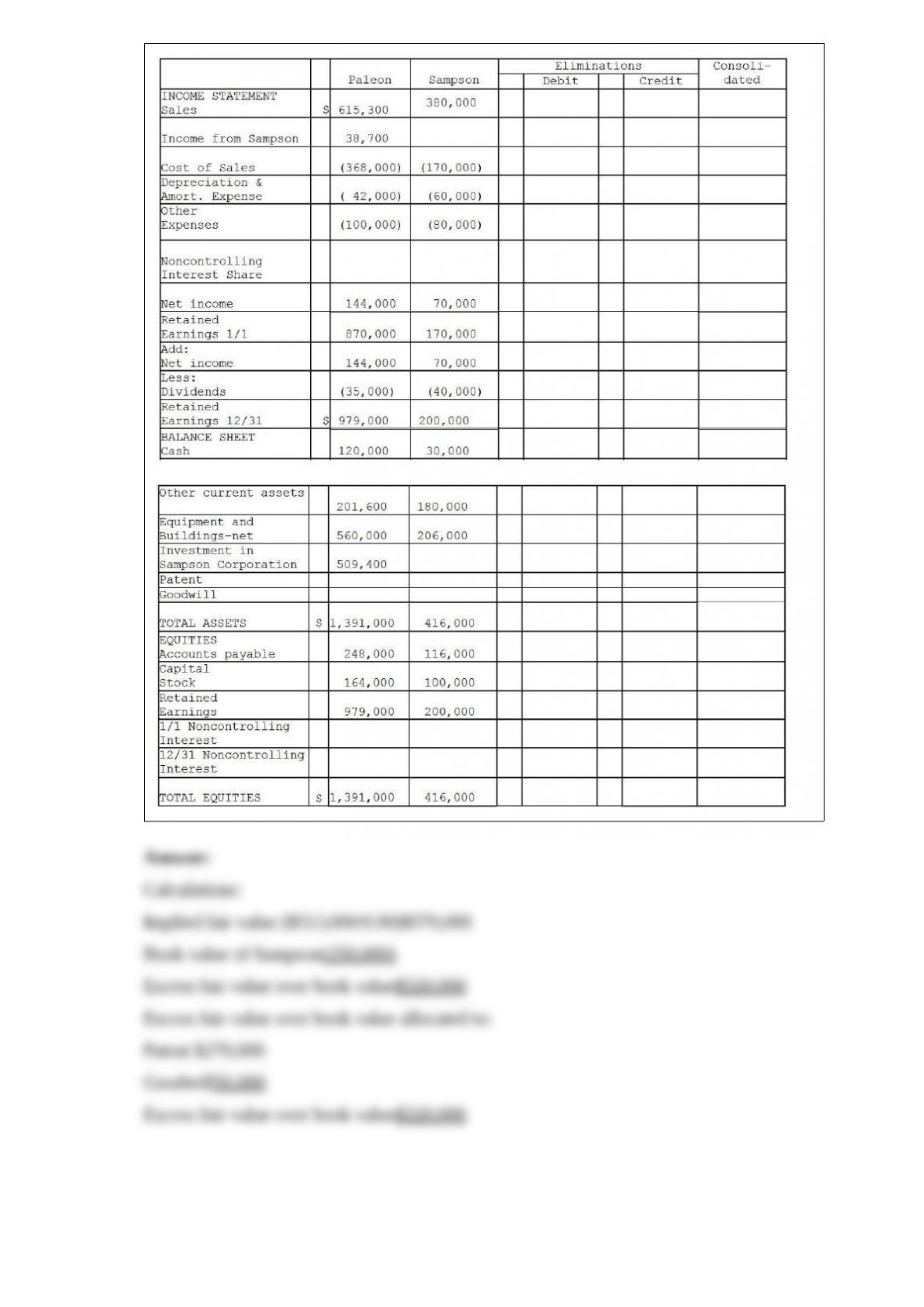

26) On January 2, 2011, Paleon Packaging purchased 90% of the outstanding common

stock of Sampson Shipping and Supplies for $513,000. Sampson’s book values

represented the fair values of all recorded assets and liabilities at that date, however

Sampson had rights to a patent that was not recorded on their books, with an

approximate fair value of $270,000, and a 10-year remaining useful life. Sampson’s

shareholders’ equity reported on that date consisted of $100,000 in capital stock and

$150,000 in retained earnings. Any remaining fair value/book value differential is

assumed to be goodwill. The December 31, 2012 financial statements for each of the

companies are provided in the worksheet below.

Required: Complete the consolidation worksheet provided below to determine

consolidated balances to be reported at December 31, 2012 .

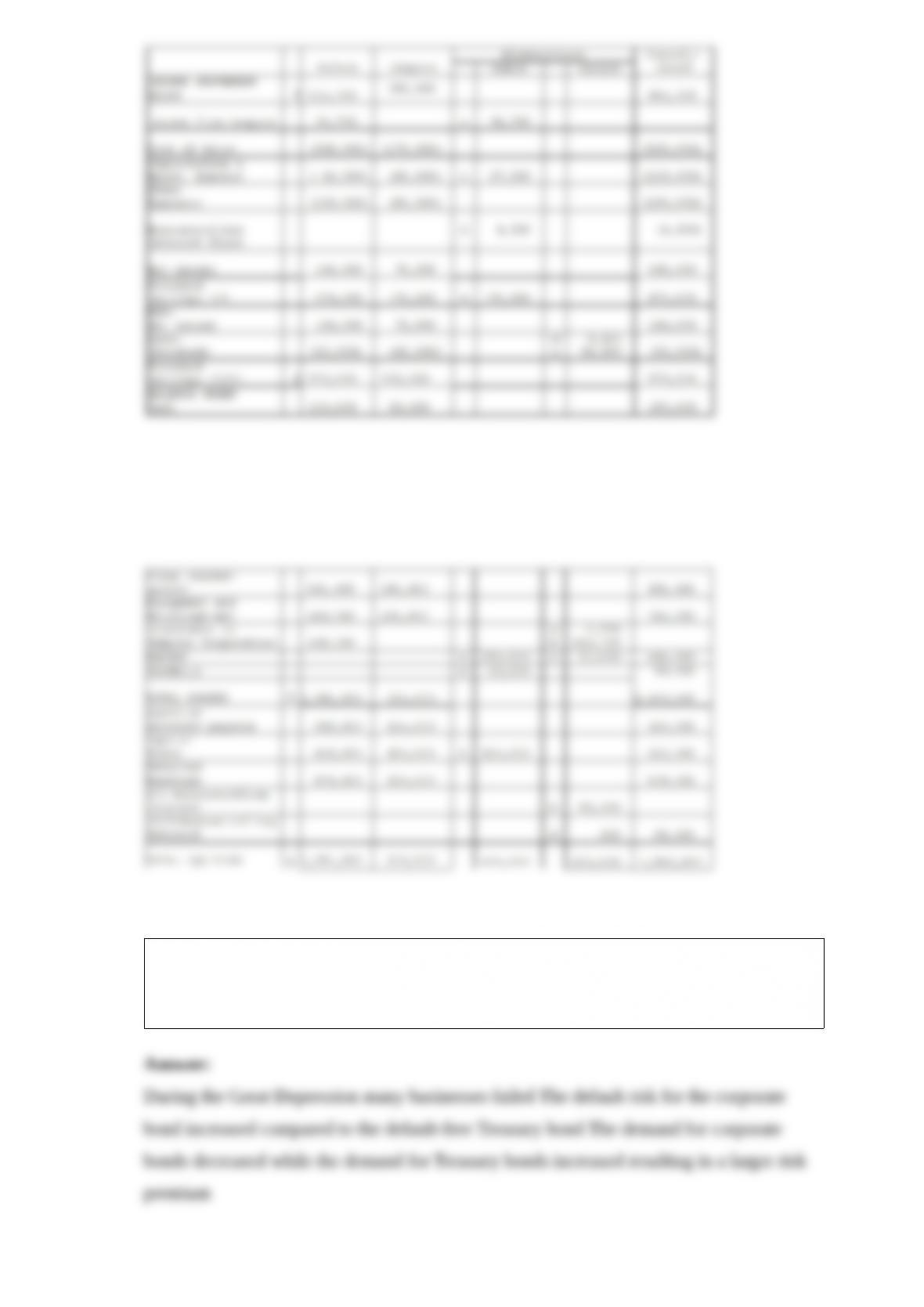

27) The spread between the interest rates on Baa corporate bonds and US government

bonds is very large during the Great Depression years 1930-1933 Explain this

difference using the bond supply and demand analysis

28) On June 1, 2011, Dapple Industries purchases an option contract for $5,000 on

10,000 gallons of aviation gas to minimize its purchasing cost price exposure. At the

time, the market price is $2.50 per gallon and the option price of $2 per gallon will

expire 6 months later. Dapple can exercise the option at its discretion. When Dapple

prepares quarterly reports on June 30, Dapple is still holding the option. On June 30, the

market price of aviation gas is $4.50 per gallon. The option is to be settled net.

On August 1, Dapple exercises the option when the gas market price is $5.00 per gallon

and purchases 40,000 gallons of gas. On August 15, Dapple uses all of the gas on a

charter flight.

Required:

What are Dapple’s journal entries with regard to the aviation gas option? Assume this is

a cash flow hedge. Ignore the time value of money.