1) In the gross method, sales discounts are reported as a deduction from sales.

2) In order to make adequate disclosure of related party transactions, companies should

report the legal form, rather than the economic substance, of these transactions.

3) Trade loading is a practice through which manufacturers try to show sales, profits,

and market share they don’t actually have.

4) The primary purpose of a statement of cash flows is to report the cash effects of

operations during a period.

5) If a company plans to retire long-term debt from a bond retirement fund, it should

report the debt as current.

6) Companies should always offset interest revenue against interest cost when

determining the amount of interest to be capitalized as part of the construction cost of

assets.

7) Which of the following is not a basic element of financial statements?

a.Assets

b.Balance sheet

c.Losses

d.Revenue

8) When a portion of inventories has been pledged as security on a loan,

a.the value of the portion pledged should be subtracted from the debt

b.an equal amount of retained earnings should be appropriated

c.the fact should be disclosed but the amount of current assets should not be affected

d.the cost of the pledged inventories should be transferred from current assets to

noncurrent assets

9) A statement of cash flows typically would not disclose the effects of

a.capital stock issued at an amount greater than par value

b.stock dividends declared

c.cash dividends paid

d.a purchase and immediate retirement of treasury stock

10) A markup of 20% on cost is equivalent to what markup on selling price?

a.17%

b.20%

c.80%

d.83%

11) Which of the following is false regarding the accounting for pensions under IFRS

and U.S. GAAP?

a.Prior service cost is recognized on the balance sheet under U.S. GAAP only

b.Under U.S. GAAP companies must amortize actuarial gains and losses over the

expected service lives of employees

c.Prior service cost is amortized into income over the expected service lives of

employees under U.S. GAAP only

d.Under IFRS companies may recognize actuarial gains and losses in income

immediately

12) At the beginning of 2014, Wallace Corporation issued 10% bonds with a face value

of $3,000,000. These bonds mature in the five years, and interest is paid semiannually

on June 30 and December 31 . The bonds were sold for $2,779,200 to yield 12%.

Wallace uses a calendar-year reporting period. Using the effective-interest method of

amortization, what amount of interest expense should be reported for 2014? (Round

your answer to the nearest dollar.)

a.$344,160

b.$334,510

c.$333,500

d.$332,500

13) Dunston Company will receive $300,000 in a future year. If the future receipt is

discounted at an interest rate of 10%, its present value is $153,948. In how many years

is the $300,000 received?

a.5 years

b.6 years

c.7 years

d.8 years

14) Agler Corporation’s balance sheet reported the following:

Capital stock outstanding, 5,000 shares, par $30 per share$150,000

Paid-in capital in excess of par80,000

Retained earnings100,000

The following transactions occurred this year:

(a)Purchased 200 shares of capital stock to be held as treasury stock, paying $60 per

share.

(b)Sold 150 of the shares of treasury stock at $65 per share.

(c)Sold the remaining shares of treasury stock at $50 per share.

Instructions

Prepare the journal entry for these transactions under the cost method of accounting for

treasury stock.

15) Transactions for the month of June were:

PurchasesSales

June 1(balance) 1,600 @ $3.20June 21,200 @ $5.50

34,400 @ 3.1063,200 @ 5.50

72,400 @ 3.3092,000 @ 5.50

153,600 @ 3.4010800 @ 6.00

221,000 @ 3.50182,800 @ 6.00

25400 @ 6.00

Assuming that perpetual inventory records are kept in units only, the ending inventory

on an average-cost basis, rounded to the nearest dollar, is

a.$8,192

b.$8,476

c.$8,580

d.$8,644

16) When inventory declines in value below original (historical) cost, and this decline is

considered other than temporary, what is the maximum amount that the inventory can

be valued at?

a.Sales price

b.Net realizable value

c.Historical cost

d.Net realizable value reduced by a normal profit margin

17) Financial statements for Kiner Company are given below:

Kiner Company

Balance Sheet

January 1, 2015

AssetsEquities

Cash$ 640,000Accounts payable$ 304,000

Accounts receivable576,000

Buildings and equipment2,400,000

Accumulated depreciation

buildings and equipment(800,000)Common stock1,840,000

Patents 288,000Retained earnings 960,000

$3,104,000$3,104,000

Kiner Company

Statement of Cash Flows

For the Year Ended December 31, 2015

Increase (Decrease) in Cash

Cash flows from operating activities

Net income$800,000

Adjustments to reconcile net income to net cash

provided by operating activities:

Increase in accounts receivable$(256,000)

Increase in accounts payable128,000

Depreciationbuildings and equipment240,000

Gain on sale of equipment(96,000)

Amortization of patents 32,000 48,000

Net cash provided by operating activities848,000

Cash flows from investing activities

Sale of equipment192,000

Purchase of land(400,000)

Purchase of buildings and equipment (768,000)

Net cash used by investing activities(976,000)

Cash flows from financing activities

Payment of cash dividend(240,000)

Sale of common stock 640,000

Net cash provided by financing activities 400,000

Net increase in cash272,000

Cash, January 1, 2015 640,000

Cash, December 31, 2015$912,000

Total assets on the balance sheet at December 31, 2015 are $4,432,000. Accumulated

deprecia-tion on the equipment sold was $224,000.

The balance in the Retained Earnings account at December 31, 2015 was

a.$720,000

b.$1,760,000

c.$1,520,000

d.$2,000,000

18) At December 31, 2014, the following information was available from Kohl Co.’s

accounting records:

Cost Retail

Inventory, 1/1/14$147,000$ 203,000

Purchases833,0001,155,000

Additional markups 42,000

Available for sale$980,000$1,400,000

Sales for the year totaled $1,200,000. Markdowns amounted to $10,000. Under the

lower-of-cost-or-market method, Kohl’s inventory at December 31, 2014 was

a.$294,000

b.$147,000

c.$140,000

d.$133,000

19) Presented below is information related to Hale Corporation:

Common Stock, $1 par$4,500,000

Paid-in Capital in Excess of ParCommon Stock550,000

Preferred 8 1/2% Stock, $50 par2,000,000

Paid-in Capital in Excess of ParPreferred Stock400,000

Retained Earnings1,500,000

Treasury Common Stock (at cost)150,000

The total paid-in capital (cash collected) related to the common stock is

a.$4,500,000

b.$5,050,000

c.$5,450,000

d.$4,900,000

20) When a company has a policy of making sales for which credit is extended, it is

reasonable to expect a portion of those sales to be uncollectible. As a result of this, a

company must recognize bad debt expense. There are basically two methods of

recognizing bad debt expense: (1) direct write-off method, and (2) allowance method.

Instructions

(a)Describe fully both the direct write-off method and the allowance method of

recognizing bad debt expense.

(b)Discuss the reasons why one of the above methods is preferable to the other and the

reasons why the other method is not usually in accordance with generally accepted

accounting principles.

21) The following data are provided:

December 31

2015 2014

Cash$ 750,000$ 500,000

Accounts receivable (net)800,000600,000

Inventories1,300,0001,100,000

Plant assets (net)3,500,0003,250,000

Accounts payable550,000400,000

Income taxes payable100,00050,000

Bonds payable700,000700,000

10% Preferred stock, $50 par1,000,0001,000,000

Common stock, $10 par1,200,000900,000

Paid-in capital in excess of par800,000650,000

Retained earnings2,000,0001,750,000

Net credit sales6,400,000

Cost of goods sold4,200,000

Operating expenses1,450,000

Net income750,000

Additional information:

Depreciation included in cost of goods sold and operating expenses is $610,000. On

May 1, 2015, 30,000 shares of common stock were issued. The preferred stock is

cumulative. The preferred dividends were not declared during 2015 .

The accounts receivable turnover for 2015 is

a.6,400 / 800

b.4,200 / 800

c.6,400 / 700

d.4,200 / 700

22) Equity securities acquired by a corporation which are accounted for by recognizing

unrealized holding gains or losses as other comprehensive income and as a separate

component of stockholders’ equity are

a.available-for-sale securities where a company has holdings of less than 20%

b.trading securities where a company has holdings of less than 20%

csecurities where a company has holdings of between 20% and 50%

d.securities where a company has holdings of more than 50%

23) Kern Company purchased bonds with a face amount of $800,000 between interest

payment dates. Kern purchased the bonds at 102, paid brokerage costs of $12,000, and

paid accrued interest for three months of $20,000. The amount to record as the cost of

this long-term investment in bonds is

a.$848,000

b.$828,000

c.$816,000

d.$800,000

24) Inventory may be recorded at net realizable value if

a.there is a controlled market with a quoted price

b.there are no significant costs of disposal

c.the inventory consists of precious metals or agricultural products

d.All of these answers are correct

25) What is disclosed in an income statement? Be specific.

26) Selected financial statement information and additional data for Johnston

Enterprises is presented below. Prepare a statement of cash flows for the year ending

December 31, 2014

Johnston Enterprises

Balance Sheet and Income Statement Data

December 31,December 31,

2014 2013___

Current Assets:

Cash$143,000$119,000

Accounts Receivable228,000306,000

Inventory 391,000 340,000

Total Current Assets762,000765,000

Property, Plant, and Equipment1,261,0001,122,000

Less: Accumulated Depreciation (476,000) (442,000)

Total Assets$1,547,000$1,445,000

Current Liabilities:

Accounts Payable$187,000$102,000

Notes Payable51,00068,000

Income Taxes Payable 85,000 76,500

Total Current Liabilities323,000246,500

Bonds Payable350,000391,000

Total Liabilities673,000637,500

Stockholders’ Equity:

Common Stock510,000467,500

Retained Earnings364,000340,000

Total Stockholders’ Equity 874,000 807,500

Total Liabilities & Stockholders’ Equity$1,547,000$1,445,000

Sales Revenue1,615,000$1,513,000

Less Cost of Goods Sold781,000731,000

Gross Profit834,000782,000

Expenses:

Depreciation Expense153,000136,000

Salaries and Wages Expense391,000357,000

Interest Expense34,00034,000

Loss on Sale of Equipment 12,000 0

Income Before Taxes244,000255,000

Less Income Tax Expense 98,000 102,000

Net Income$146,000$153,000

Additional Information:

During the year, Johnston sold equipment with an original cost of $133,000 and

accumulated depreciation of $119,000 and purchased new equipment for $272,000.

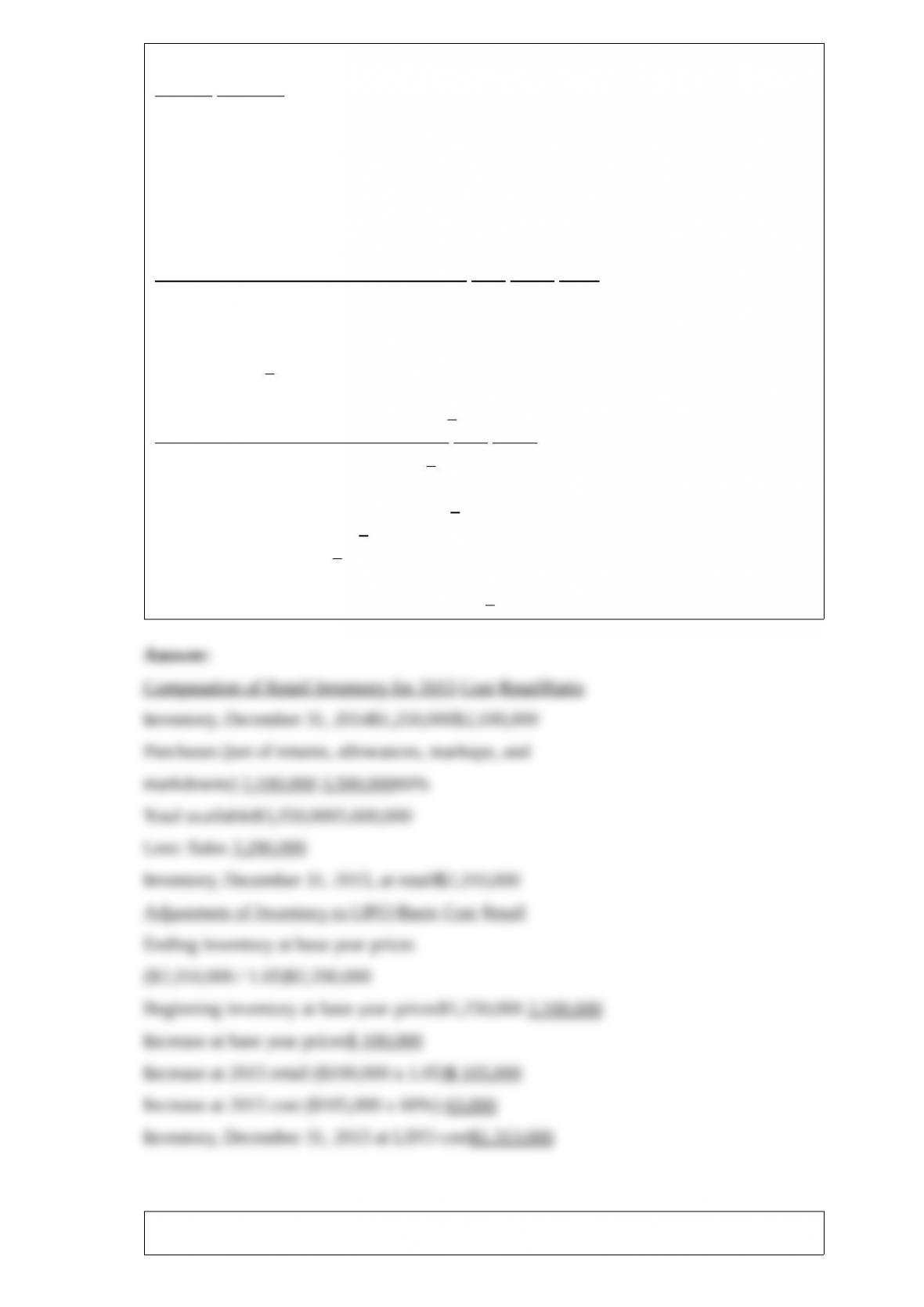

27) Flint Department Store wishes to use the retail LIFO method of valuing inventories

for 2015 . The appropriate data are as follows:

At Cost At Retail

December 31, 2014 inventory (base layer)$1,250,000$2,100,000

Purchases (net of returns, allowances, markups, and markdowns)2,100,0003,500,000

Sales revenue3,290,000

Price index for 2015105

Instructions

Complete the following schedule (fill in all blanks and show calculations in the

parentheses):

Computation of Retail Inventory for 2015 Cost Retail Ratio

Inventory, December 31, 2014$1,250,000$2,100,000

Purchases (net of returns, allowances,

markups, and markdowns)%

Total available$

____________________________________

Inventory, December 31, 2015, at retail$

Adjustment of Inventory to LIFO Basis Cost Retail

Ending inventory at base year prices$

()

Beginning inventory at base year prices$

Increase at base year prices$

Increase at 2015 retail()$

Increase at 2015 cost()

Inventory, December 31, 2015, at LIFO cost$

28) Alice, Inc. has the following deferred tax assets at December 31, 2014:

What amount would Alice, Inc. report as a current deferred tax asset under IFRS and

under U.S. GAAP?

_IFRS_U.S. GAAP

a$510,000$510,000

b.$0$255,000

c.$255,000 $510,000

d.$510,000$255,000

29) During periods of rising prices, the use of FIFO (as compared with LIFO) will

result in what effect on the financial statements?

30) The stockholders’ equity section of Benton Corporation’s balance sheet as of

December 31, 2014 is as follows:

Stockholders’ Equity

Common stock, $5 par value; authorized, 2,000,000 shares;

issued, 400,000 shares$2,000,000

Paid-in capital in excess of par850,000

Retained earnings 3,000,000

$5,850,000

The following events occurred during 2015:

1>Jan. 530,000 shares of authorized and unissued common stock were sold for $8 per

share.

2>Jan. 16Declared a cash dividend of 20 cents per share, payable February 15 to

stock-holders of record on February 5 .

3>Feb. 1040,000 shares of authorized and unissued common stock were sold for $12

per share.

4>March 1A 30% stock dividend was declared and issued. Fair value per share is

currently $15.

5>April 1A two-for-one split was carried out. The par value of the stock was to be

reduced to $2.50 per share. Fair value on March 31 was $18 per share.

6>July 1A 15% stock dividend was declared and issued. Fair value is currently $10 per

share.

7>Aug. 1A cash dividend of 20 cents per share was declared, payable September 1 to

stockholders of record on August 21 .

Instructions

Enter the above events into the following work sheet showing how each event affects

the column. Event No. 1 will serve as an example.

Common Stock

No. ofTotalPaid-in Capital In

ItemShares Issued Par Value Excess of ParRetained Earnings

Beginning Balance1/1/13400,000$2,000,000$850,000$3,000,000

Event #1Jan. 5 30,000 150,000 90,000 -0-

Balance430,000$2,150,000$940,000$3,000,000

Event # 2Jan. 16 (and events 3 through 7)