The basis for recording direct and indirect labor costs incurred is a summary of the

period’s

a. job order cost sheets

b. time tickets

c. employees’ earnings records

d. clock cards

In an effort to simplify the multiple production department factory overhead rate

method, the same rate can be used for all departments.

a. True

b. False

the percentage analysis of the relationship of each component in a financial statement to

a total within the statement

Match each definition that follows with the term (a’“h) it defines.

a. discontinued operations

b. extraordinary items

c. change from one generally accepted accounting principle to another

d. horizontal analysis

e. vertical analysis

f. common-sized financial statements

g. current position analysis

h. profitability analysis

During the period, labor costs incurred on account amounted to $175,000, including

$150,000 for production orders and $25,000 for general factory use. Factory overhead

applied to production was $23,000. The entry to record the factory overhead applied to

production is

a. Work in Process Factory Overhead 25,000

25,000

b. Factory Overhead Work in Process 23,000

23,000

c. Work in Process Factory Overhead 23,000

23,000

d. Factory Overhead Accounts Payable 25,000

25,000

Understanding how costs behave is useful to management for all the following reasons

except

a. predicting customer demand

b. predicting profits as sales and production volumes change

c. estimating costs

d. changing an existing product production

After the sales budget is prepared, the capital expenditures budget is normally prepared

next.

a. True

b. False

If the unit selling price is $40, the volume of sales is $3,000,000, sales at the break-even

point amount to $2,500,000, and the maximum possible sales are $3,300,000, the

margin of safety is 14,500 units.

a. True

b. False

When you are interpreting financial ratios, it is useful to compare a company’s ratios to

some form of standard.

a. True

b. False

Custom-made goods would be accounted for using a process costing system.

a. True

b. False

Challenger Factory produces two similar products’”regular widgets and deluxe widgets.

The total plant overhead budget is $675,000 with 300,000 estimated direct labor hours.

It is further estimated that deluxe widget production will need 3 direct labor hours for

each unit and regular widget production will require 2 direct labor hours for each unit.

Using the single plantwide factory overhead rate with an allocation base of direct labor

hours, how much factory overhead will Challenger Factory allocate to deluxe widget

production if budgeted production for the period is 50,000 units and actual production

for the period is 58,000 units?

a. $391,500

b. $225,000

c. $261,000

d. $337,500

Processing returned materials

Identify the following quality control activities as either value-added or

non-value-added.

a. Value-added

b. Non-value-added

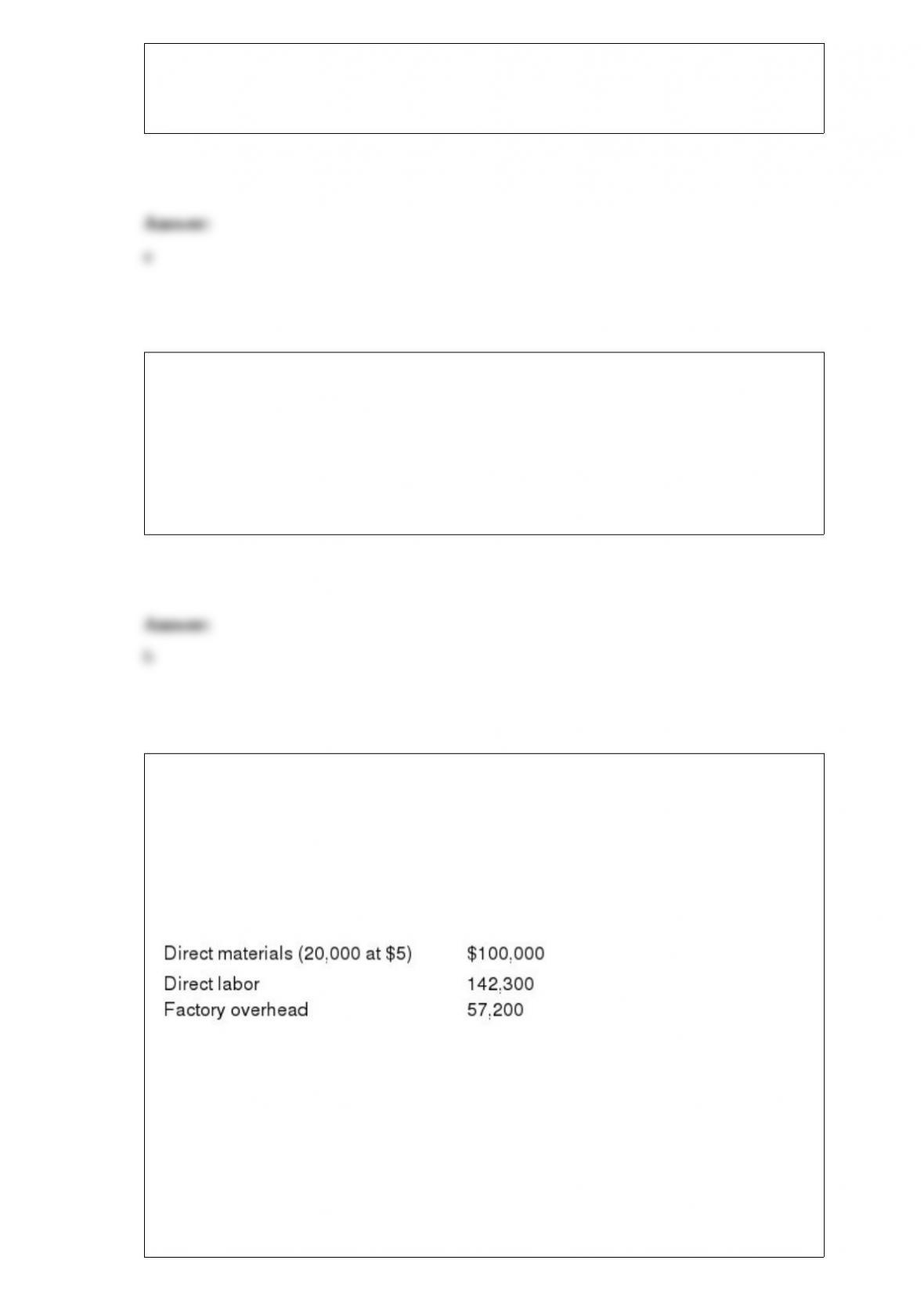

Department J had no work in process at the beginning of the period; 18,000 units were

completed during the period; and 2,000 units were 30% completed at the end of the

period. The following manufacturing costs were debited to the departmental work in

process account during the period (Assume the company uses FIFO and rounds cost per

unit to two decimal places):

Assuming that all direct materials are placed in process at the beginning of production,

what is the total cost of the departmental work in process inventory at the end of the

period?

a. $90,000

b. $283,140

c. $199,500

d. $16,438

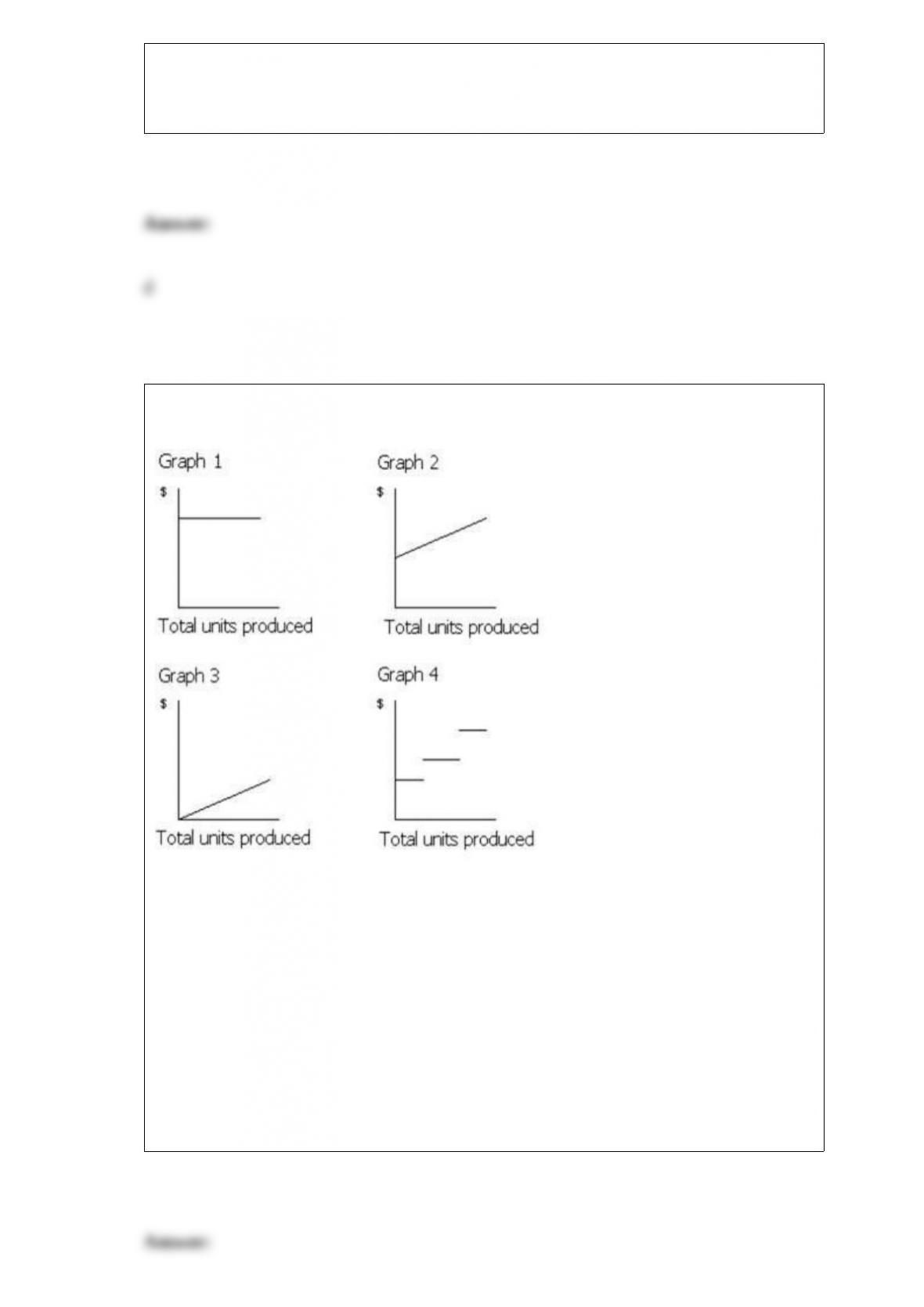

Figure 21-1

Which of the graphs in Figure 21-1 illustrates the behavior of a total variable cost?

a. Graph 2

b. Graph 3

c. Graph 4

d. Graph 1

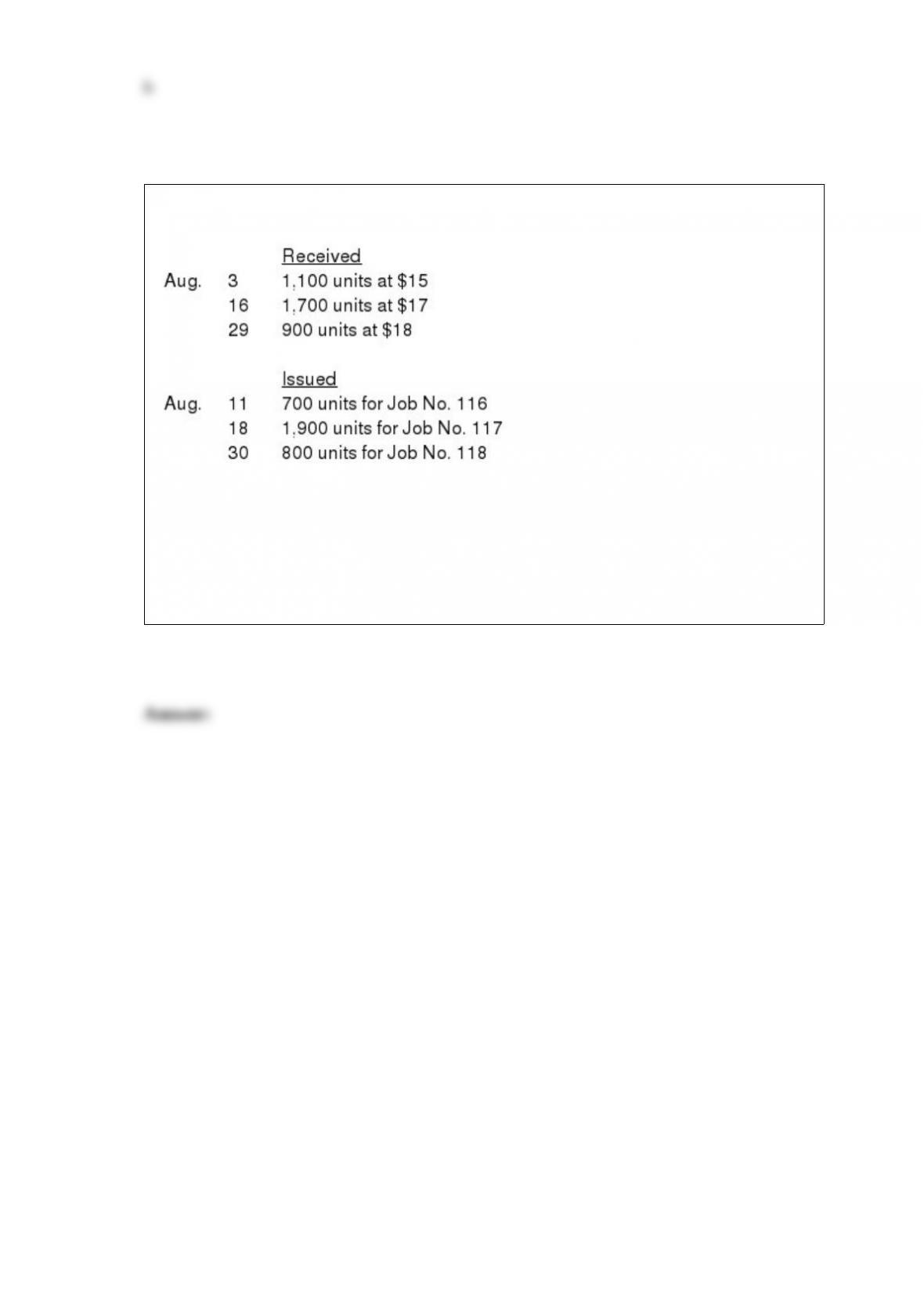

During August, the receipts and distributions of Material No. B4G9 are as follows:

(a) Determine the cost of each of the three issues under a perpetual system, using the

first-in, first-out method.

(b) Present the journal entry to record the issuance of the materials for the month,

assuming that the cost of issuances is determined by the first-in, first-out method.

The first budget to be prepared is usually the production budget.

a. True

b. False

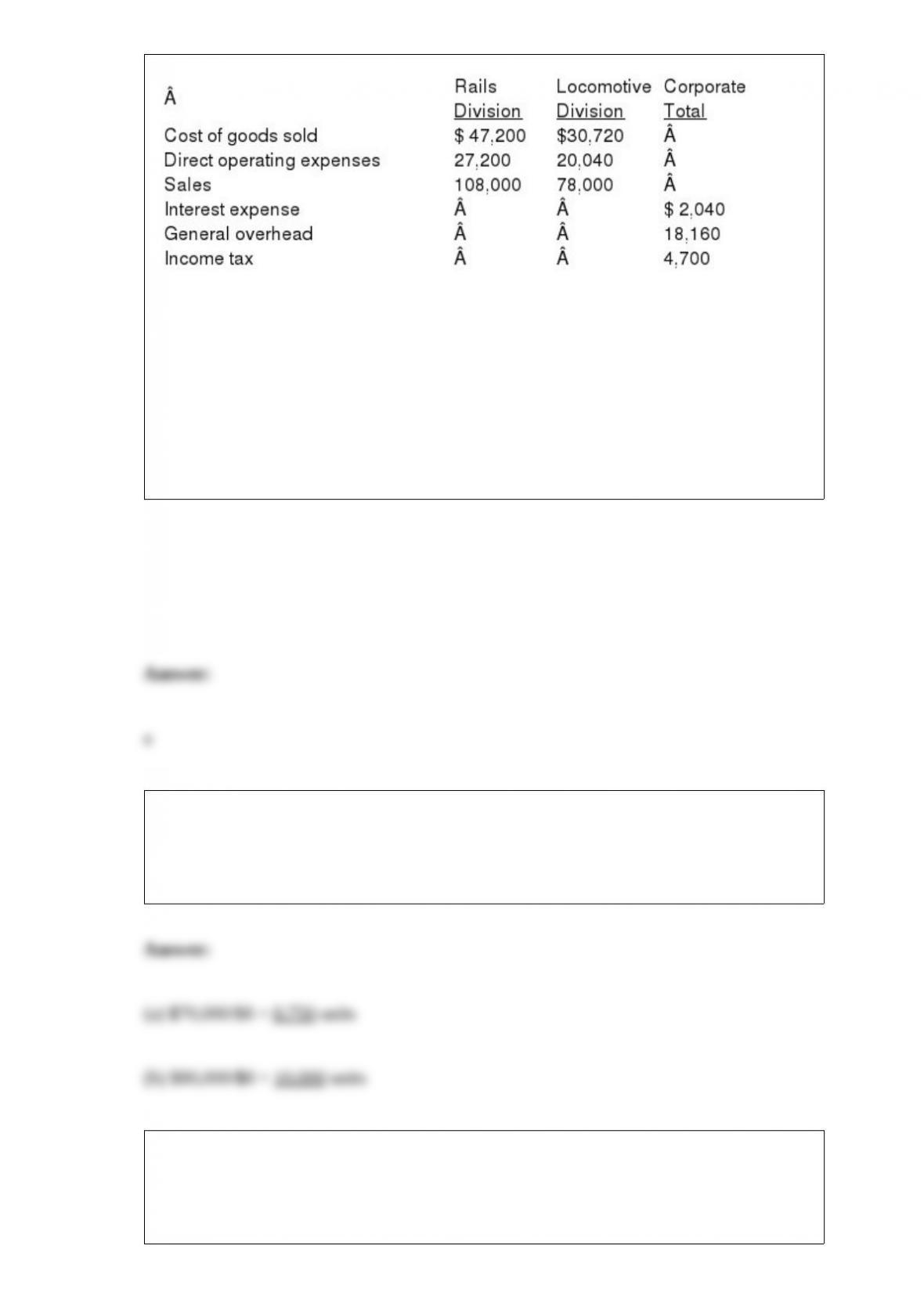

The following financial information was summarized from the accounting records of

Train Corporation for the current year ended December 31:

The gross profit for the Rails Division is

a. $60,800

b. $33,600

c. $8,700

d. $21,150

For the past year, Pedi Company had fixed costs of $70,000, unit variable costs of $32,

and a unit selling price of $40. For the coming year, no changes are expected in

revenues and costs, except that property taxes are expected to increase by $10,000.

Determine the break-even sales (units) for (a) the past year and (b) the coming year.

Division A of Chacha Company has sales of $140,000, cost of goods sold of $83,000,

operating expenses of $43,000, and invested assets of $150,000.

What is the investment turnover for Division A?

a. 0.93

b. 9.3

c. 1.07

d. 10.7

A qualitative characteristic that may impact upon capital investment analysis is

manufacturing flexibility.

a. True

b. False

The entry to record the flow of direct labor costs into production in a job order cost

accounting system is

a. debit Factory Overhead, credit Work in Process

b. debit Finished Goods, credit Wages Payable

c. debit Work in Process, credit Wages Payable

d. debit Factory Overhead, credit Wages Payable

A process cost system be appropriate for a

a. natural gas refinery

b. jet airplane builder

c. catering business

d. custom cabinet builder