In its 2016 annual report to shareholders, the Goodday Chemical Company included the

following disclosure note excerpts on CONTINGENCIES in its annual report to

shareholders: At December 31, 2016, Goodday had recorded liabilities aggregating

$66.5 million for anticipated costs related to various environmental matters, primarily

the remediation of numerous waste disposal sites and certain properties sold by

Goodday. These costs include legal and consulting fees, site studies, the design and

implementation of remediation plans, post-remediation monitoring and related activities

and will be paid over several years. The amount of Goodday’s ultimate liability in

respect of these matters may be affected by several uncertainties, primarily the ultimate

cost of required remediation and the extent to which other responsible parties

contribute. At December 31, 2016, Goodday had recorded liabilities aggregating $218.7

million for potential product liability and other tort claims, including related legal fees

expected to be incurred, presently asserted against Goodday. The amount recorded was

determined on the basis of an assessment of potential liability using an analysis of

available information with respect to pending claims, historical experience, and, where

available, current trends. Goodday is a defendant in numerous lawsuits involving at

December 31, 2016, approximately 63,000 claimants alleging various asbestos-related

personal injuries purported to result from exposure to asbestos in certain rubber-coated

products manufactured by Goodday in the past or in certain Goodday facilities.

Typically, these lawsuits have been brought against multiple defendants in state and

federal courts. In the past, Goodday has disposed of approximately 22,000 cases by

defending and obtaining the dismissal thereof or by entering into a settlement. Goodday

has policies and coverage-in-place agreements with certain of its insurance carriers that

cover a substantial portion of estimated indemnity payments and legal fees in respect of

the pending claims. At December 31, 2016, Goodday has recorded an asset in the

amount it expects to collect under the policies and coverage-in-place agreements with

certain carriers related to its estimated asbestos liability. Goodday has also commenced

discussions with certain of its excess coverage insurance carriers to establish

arrangements in respect of their policies. Subject to the uncertainties referred to above,

Goodday has concluded that in respect of any of the above described liabilities, it is not

reasonably possible that it would incur a loss exceeding the amount recognized at

December 31, 2016, with respect thereto which would be material relative to the

consolidated financial position, results of operations, or liquidity of Goodday. Briefly

explain the GAAP requirement from which the costs/obligations for environmental

cleanup and product liability/tort claim matters were accrued in the financial

statements.

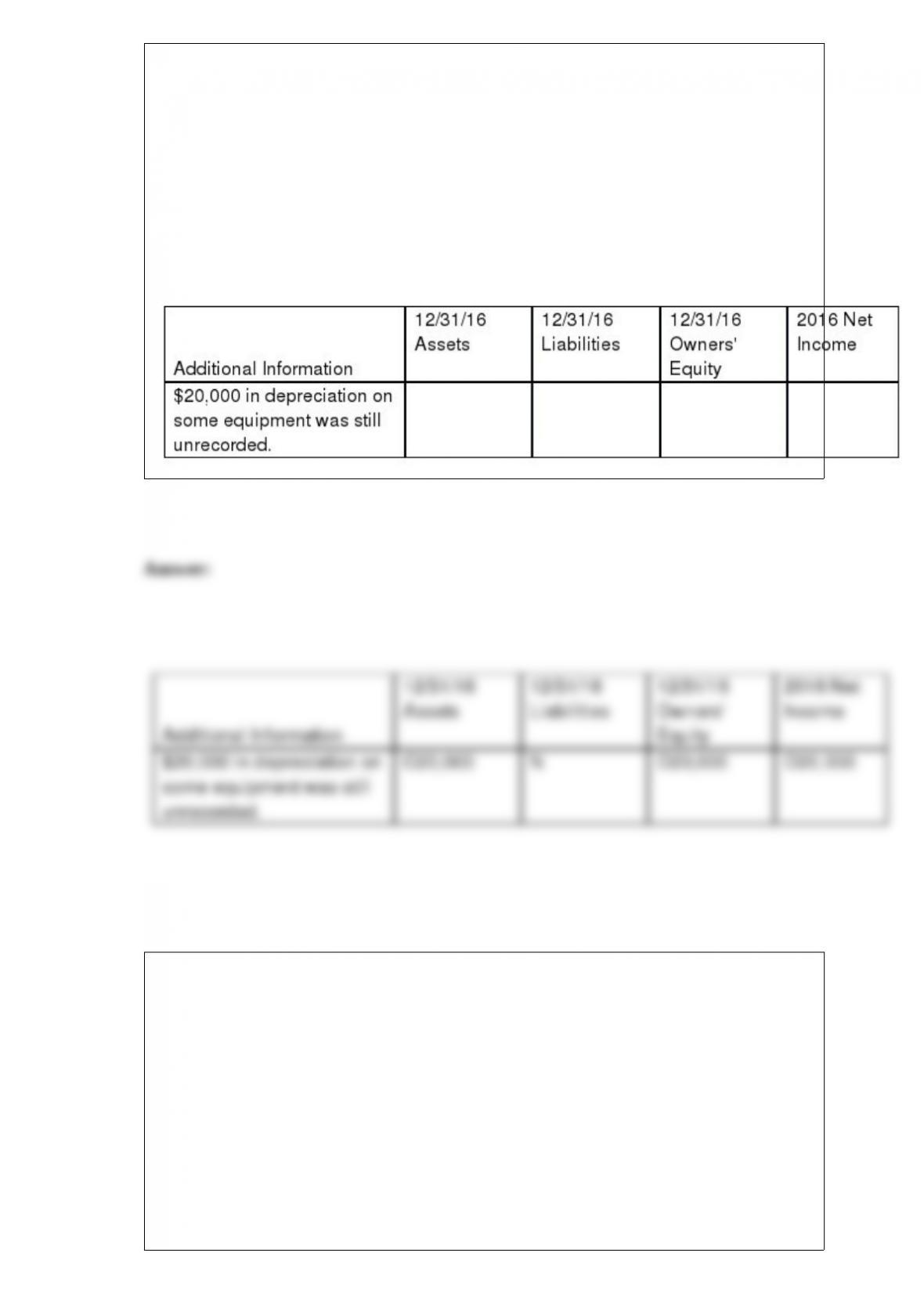

Suppose that Laramie Company’s adjusted trial balance ignored the following

information. For each item of information, indicate what effects, if any, these omissions

would have on the stated components of Laramie Company’s 2016 Income Statement

and 12/31/16 Balance Sheet. Assume no income taxes. Use the following code for your

answers and be sure to include the dollar amounts of the effects next to the letter O or

U: N = No Effect

O = Overstated

U = Understated

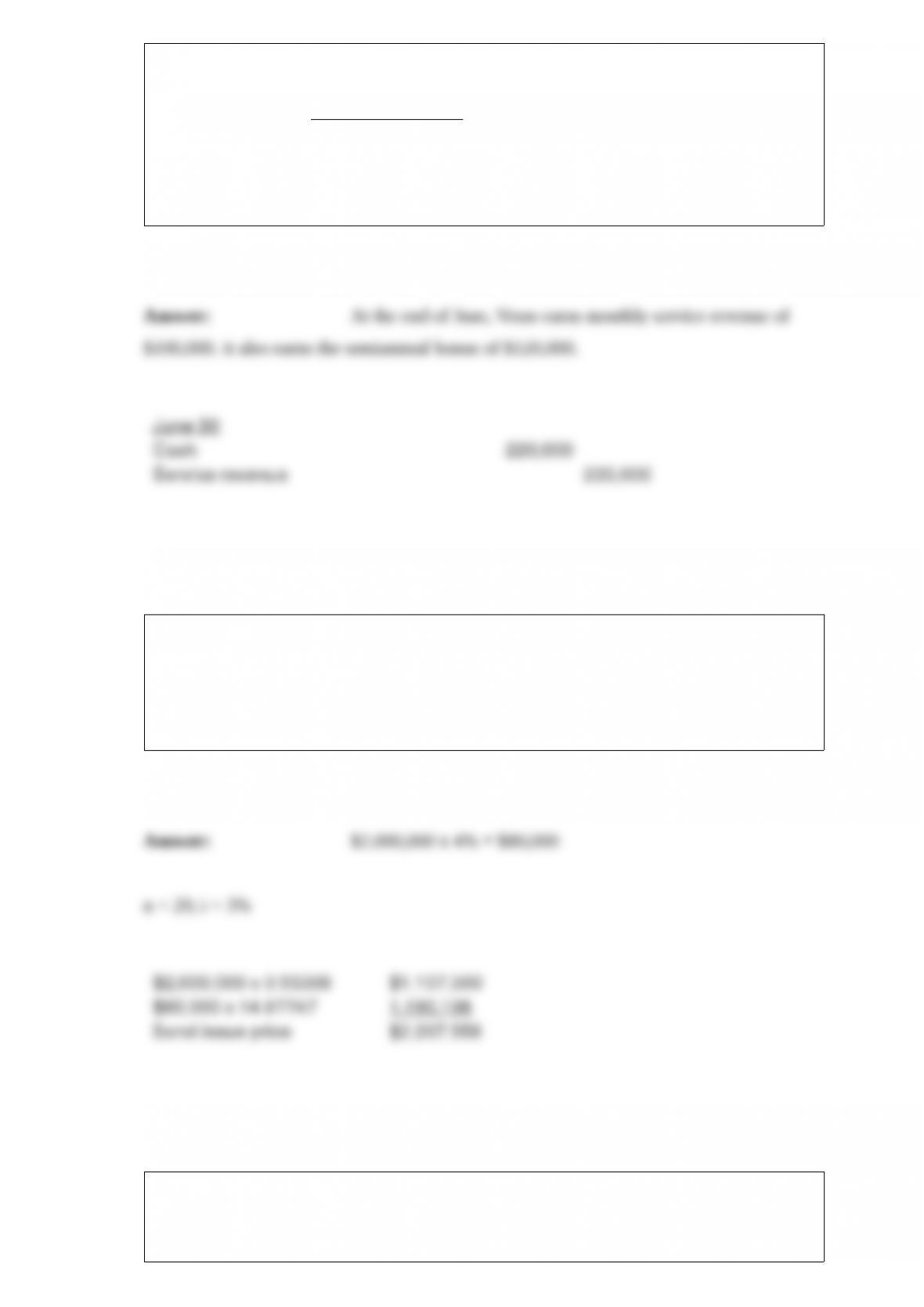

Veras Bus Transportation provides on-campus bus services for universities. On January

1, it enters into a one-year contract with Moose University to operate five bus lines

traveling throughout the campus. Under the contract, Veras will be paid $100,000 on the

last day of each month. In addition, Veras will receive an additional $120,000 at the end

of each six-month period, provided it remains free of accidents. – On January 1, based

on historical experience, Veras estimated that there is a 75% chance that it will remain

free of accidents for the entire year.

– On March 20, three of the most senior drivers at Veras abruptly left. As a result, Veras

had to hire inexperienced drivers to fill the vacant positions. Consequently, Veras

revised its estimate to a 30% chance that it would earn the semiannual bonus.

– On June 30, Moose confirmed that there was no accident between January and June,

so Veras would be entitled to the semiannual bonus. Veras bases estimates of variable

consideration on the most likely amount it expects to receive.

Prepare Veras’ June 30 journal entry to account for the revenue earned from June 1 –

June 30, as well as any necessary adjustments to revenue presumed to have been

previously recorded.

GHI Company will issue $2,000,000 in 8%, 10-year bonds when the market rate of

interest is 6%. Interest is paid semiannually.

Required: Determine how much cash GHI Company should realize from the bond

issue.

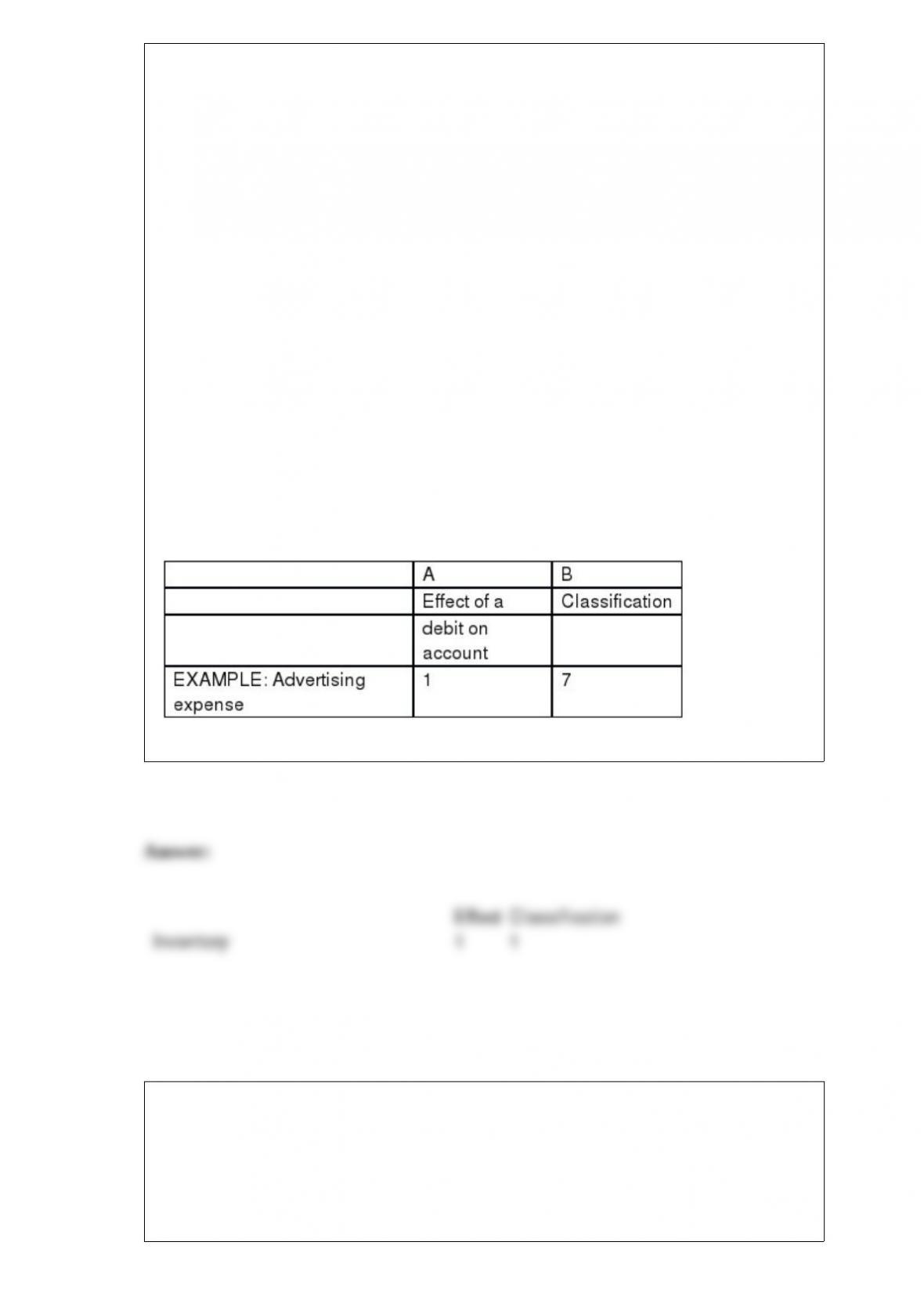

Below is a list of accounts in no particular order. Assume that all accounts have normal

balances. Required: In column A, indicate whether a debit will:

1> Increase the account balance, or

2> Decrease the account balance. In column B, classify each account according to the

following scheme. For contra accounts, indicate the classification of the account to

which it relates.

1>A current asset in the balance sheet.

2>A noncurrent asset in the balance sheet.

3>A current liability in the balance sheet.

4>A long-term liability in the balance sheet.

5>A permanent equity account in the balance sheet.

6>A revenue account in the income statement.

7>An expense account shown in the income statement.

8> Account does not appear in either the balance sheet or the income statement.

Inventory

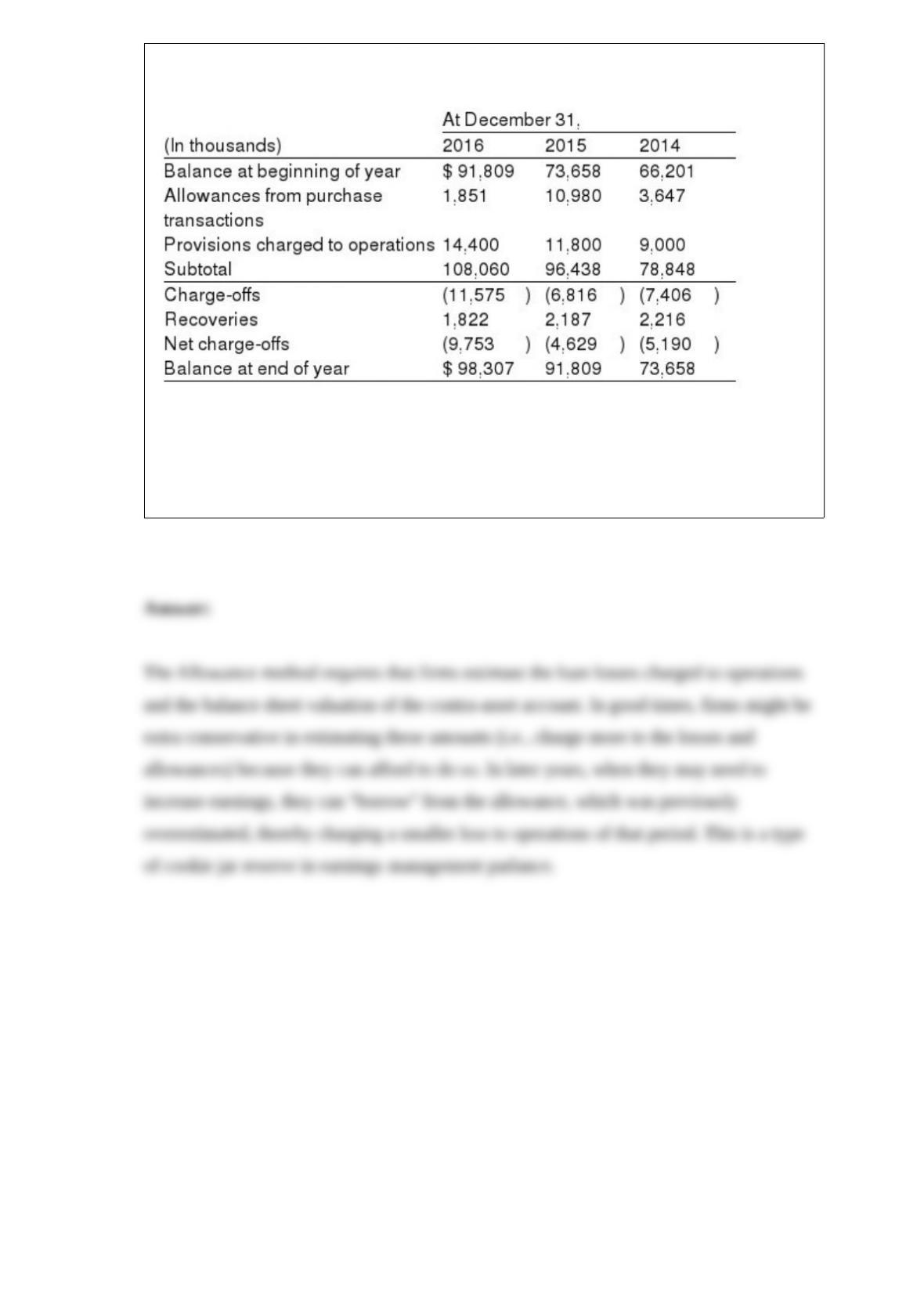

The following note disclosure is taken from the 2016 annual report to shareholders of

Winchester International Corporation. NOTE 5: ALLOWANCE FOR LOAN LOSSES

The allowance for loan loss is maintained at a level to absorb probable losses inherent

in the loan portfolio. This allowance is increased by provisions charged to operating

expense and by recoveries on loans previously charged off, and reduced by charge-offs

on loans. The following is a summary of the changes in the allowances for loan losses

for three years:

Winchester also reported (in thousands) in its comparative balance sheet that it held

Loans receivable, net, of $6,869,911 and $6,819,209 at December 31, 2016, and

December 31, 2015, respectively. How might a company with loan receivables like

Winchester be able to manage earnings in applying generally accepted accounting

principles?