Which of the following presents key aspects of the process of accounting in the correct

chronological order?

a. Totaling, auditing, and budgeting

b. Budgeting, recording, and communicating

c. Recording, totaling, and auditing

d. Identifying, recording, and communicating

Answer:

A company which uses special journals should record a transaction involving the

purchase of merchandise for cash in a

a. single-column purchases journal.

b. multiple-column purchases journal.

c. cash payments journal.

d. general journal.

Answer:

Live Wire Hot Rod Shop follows the revenue recognition principle. Live Wire services

a car on July 31. The customer picks up the vehicle on August 1 and mails the payment

to Live Wire on August 5. Live Wire receives the check in the mail on August 6. When

should Live Wire show that the revenue was recognized?

a. July 31

b. August 1

c. August 5

d. August 6

Answer:

Marin Company sells 9,000 units of its product in 2015 for $500 each. The selling price

includes a one-year warranty on parts. It is expected that 3% of the units will be

defective and that repair costs will average $50 per unit. In the year of sale, warranty

contracts are honored on 180 units for a total cost of $9,000.

What amount should Marin Company report as Warranty Expense in its 2015 income

statement?

a. $13,500.

b. $9,000.

c. $4,500.

d. $67,500.

Answer:

Selection of an inventory costing method by management does not usually depend on

a. the fiscal year end.

b. income statement effects.

c. balance sheet effects.

d. tax effects.

Answer:

A daily cash count of register receipts made by a cashier department supervisor

demonstrates an application of which of the following internal control principles?

a. Documentation procedures

b. Segregation of duties

c. Establishment of responsibility

d. Independent internal verification

Answer:

All bonds will always fall into which one of the following pairs of categories?

a. Secured or unsecured

b. Mortgage or sinking fund

c. Debenture or unsecured

d. Callable or convertible

Answer:

Aaron, Inc. paid $120,000 to buy back 10,000 shares of its $1 par value common stock.

This stock was sold later at a selling price of $8 per share. The entry to record the sale

includes a

a. debit to Retained Earnings for $40,000.

b. credit to Retained Earnings for $10,000.

c. debit to Paid-in Capital from Treasury Stock for $120,000.

d. credit to Paid-in Capital from Treasury Stock for $10,000.

Answer:

If an adjustment is needed for unearned revenues, the

a. liability and related revenue are overstated before adjustment.

b. liability and related revenue are understated before adjustment.

c. liability is overstated and the related revenue is understated before adjustment.

d. liability is understated and the related revenue is overstated before adjustment.

Answer:

The depreciation method that applies a constant percentage to depreciable cost in

calculating depreciation is

a. straight-line.

b. units-of-activity.

c. declining-balance.

d. None of these answers are correct.

Answer:

Beginning inventory plus the cost of goods purchased equals

a. cost of goods sold.

b. cost of goods available for sale.

c. net purchases.

d. total goods purchased.

Answer:

On February 2, Jerry’s Printing Service received a payment of $9,000 for contracted

printing work that will be completed over the next 3 months. As of the end of February,

the company had completed 1/3 of the work. The adjusting journal entry at the end of

February for unearned revenue will include

a. a debit to Unearned Service Revenue for $9,000

b. a credit to Unearned Service Revenue for $6,000

c. a credit to Service Revenue for $3,000

d. a debit to Cash for $3,000

Answer:

If an adjusting entry is not made for an accrued revenue,

a. assets will be overstated.

b. expenses will be understated.

c. stockholders’ equity will be understated.

d. revenues will be overstated.

Answer:

Silk Company issued $500,000 of 7%, 10-year bonds on one of its interest dates for

$431,850 to yield an effective annual rate of 9%. The effective-interest method of

amortization is to be used. Interest is paid annually.

The journal entry on the first interest payment date, to record the payment of interest

and amortization of discount will include a

a. debit to Interest Expense for $35,000.

b. credit to Cash for $38,867.

c. credit to Discount on Bonds Payable for $3,867.

d. debit to Interest Expense for $45,000.

Answer:

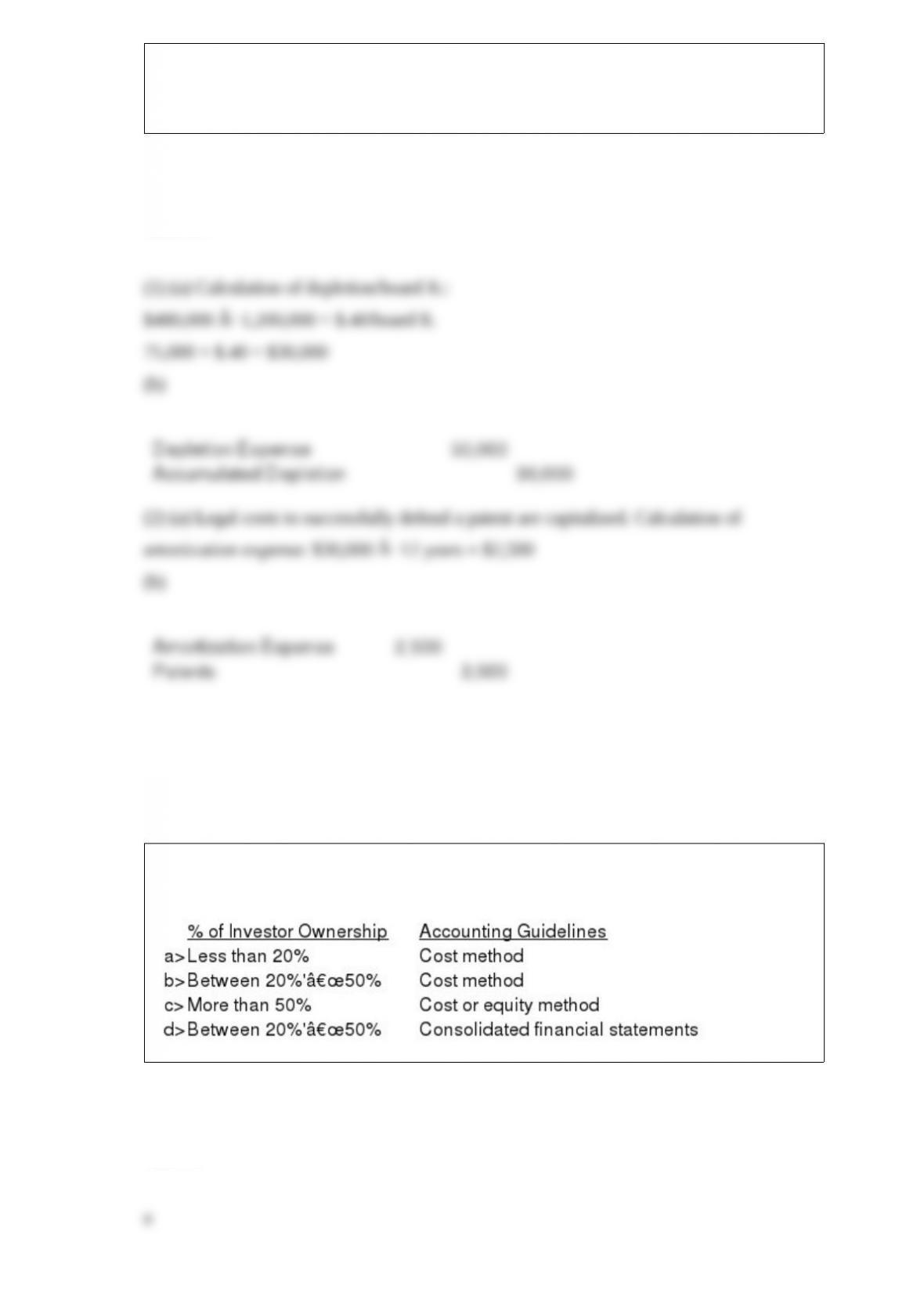

For each of the following unrelated transactions, (a) determine the amount of the

amortization or depletion expense for the current year, and (b) present the adjusting

entries required to record each expense at year end.

(1) Timber rights were purchased on a tract of land for $480,000. The timber is

estimated at 1,200,000 board feet. During the current year, 75,000 board feet of timber

were cut and sold.

(2) Costs of $8,000 were incurred on January 1 to obtain a patent. Shortly thereafter,

$22,000 was spent in legal costs to successfully defend the patent against competitors.

The patent has an estimated legal life of 12 years.

Answer:

Which of the following is the correct matching concerning the appropriate accounting

for long-term stock investments?

Answer:

A dividend based on paid-in capital is termed a liquidating dividend.

Answer:

On February 1, Results Income Tax Service received a $3,000 cash retainer for tax

preparation services to be rendered equally over the next 4 months. The full amount

was credited to the liability account Unearned Service Revenue. Assuming that the

revenue is recognized equally over the 4-month period, what balance would be reported

on the February 28 balance sheet for Unearned Service Revenue?

Answer:

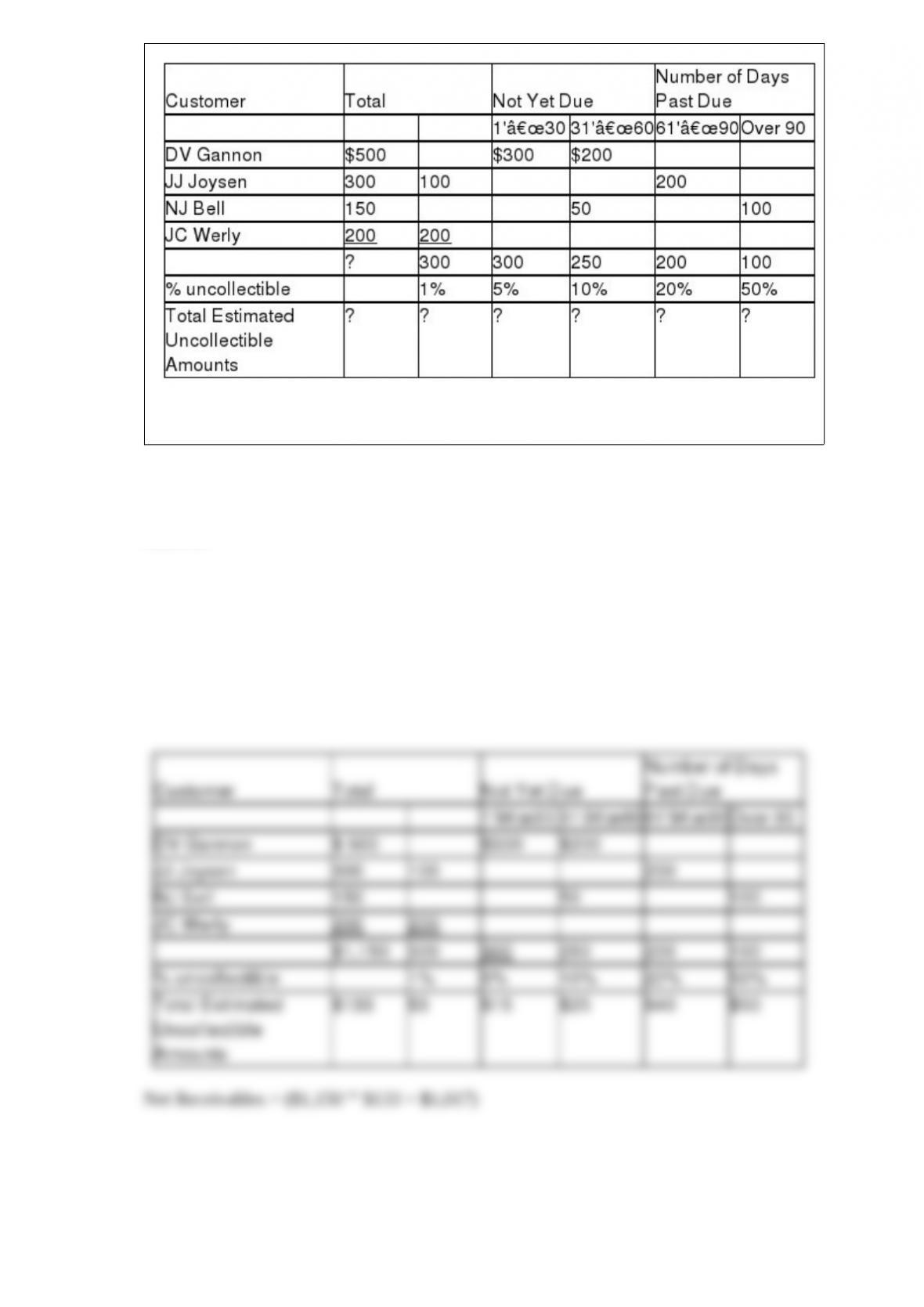

Stine Co. sells Christmas angels. Patel determines that at the end of December, it has

the following aging schedule of Accounts Receivable:

Compute the net receivables based on the above information at the end of December.

(There was no beginning balance in the Allowance for Doubtful Accounts).

Answer:

Instructions: Journalize the following transactions for Fortier Company.

1> Issued 7,000 shares of no-par common stock. The market price of the stock is $12

per share.

2> Issued 3,000 shares of 5%, $100 par, cumulative preferred stock for $122 per share.

3> Declared dividends on preferred dividend of 5% per share.

4> Purchased 500 shares of common stock at $14 for treasury.

5> Paid preferred dividend declared in #3.

Answer:

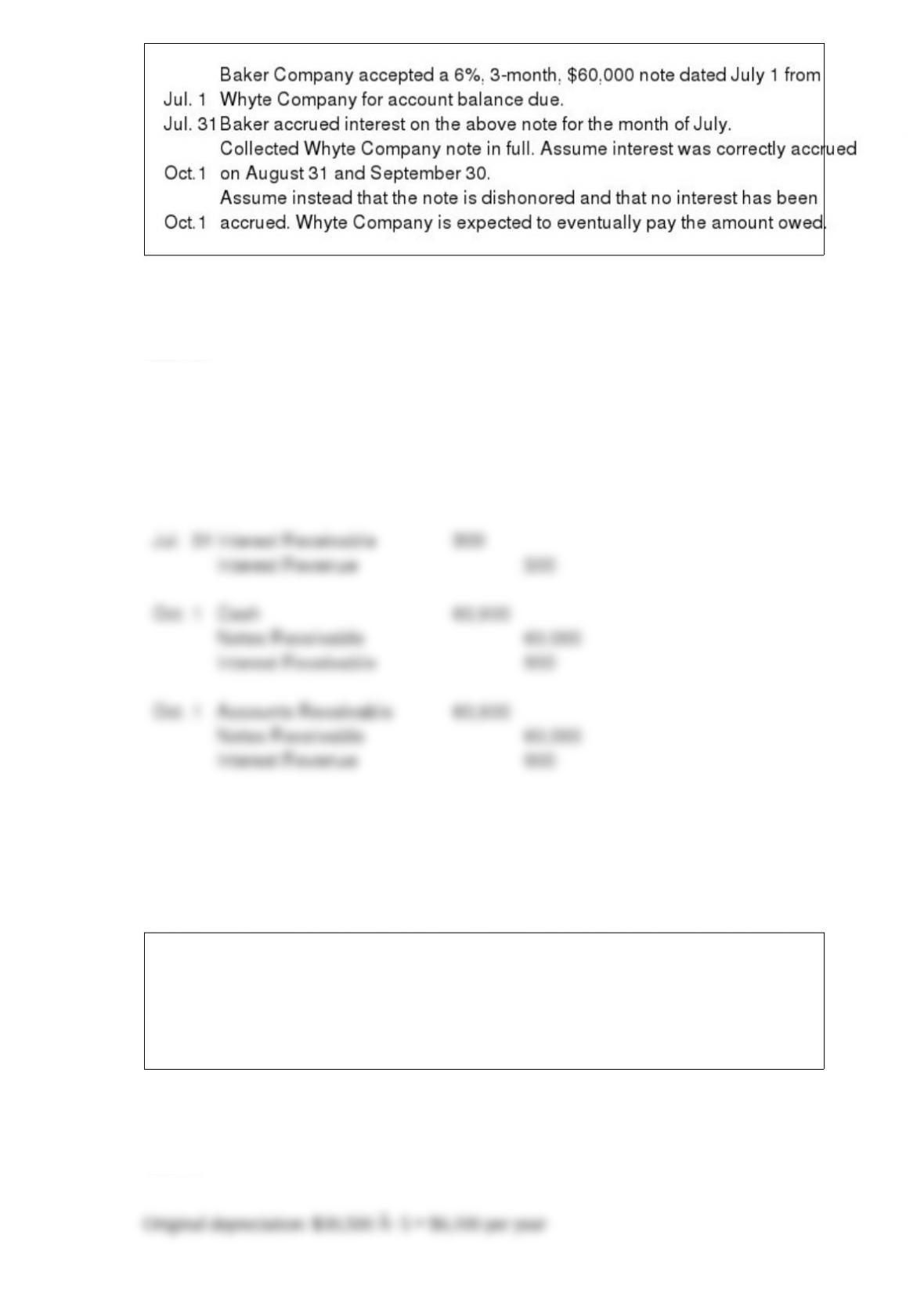

Instructions

Prepare journal entries to record the following events:

Answer:

On January 1, 2013, Santo Company purchased a computer system for $30,500. The

system had an estimated useful life of 5 years and no salvage value. At January 1, 2015,

the company revised the remaining useful life to two years. What amount of

depreciation will be recorded for 2015 and 2016?

Answer:

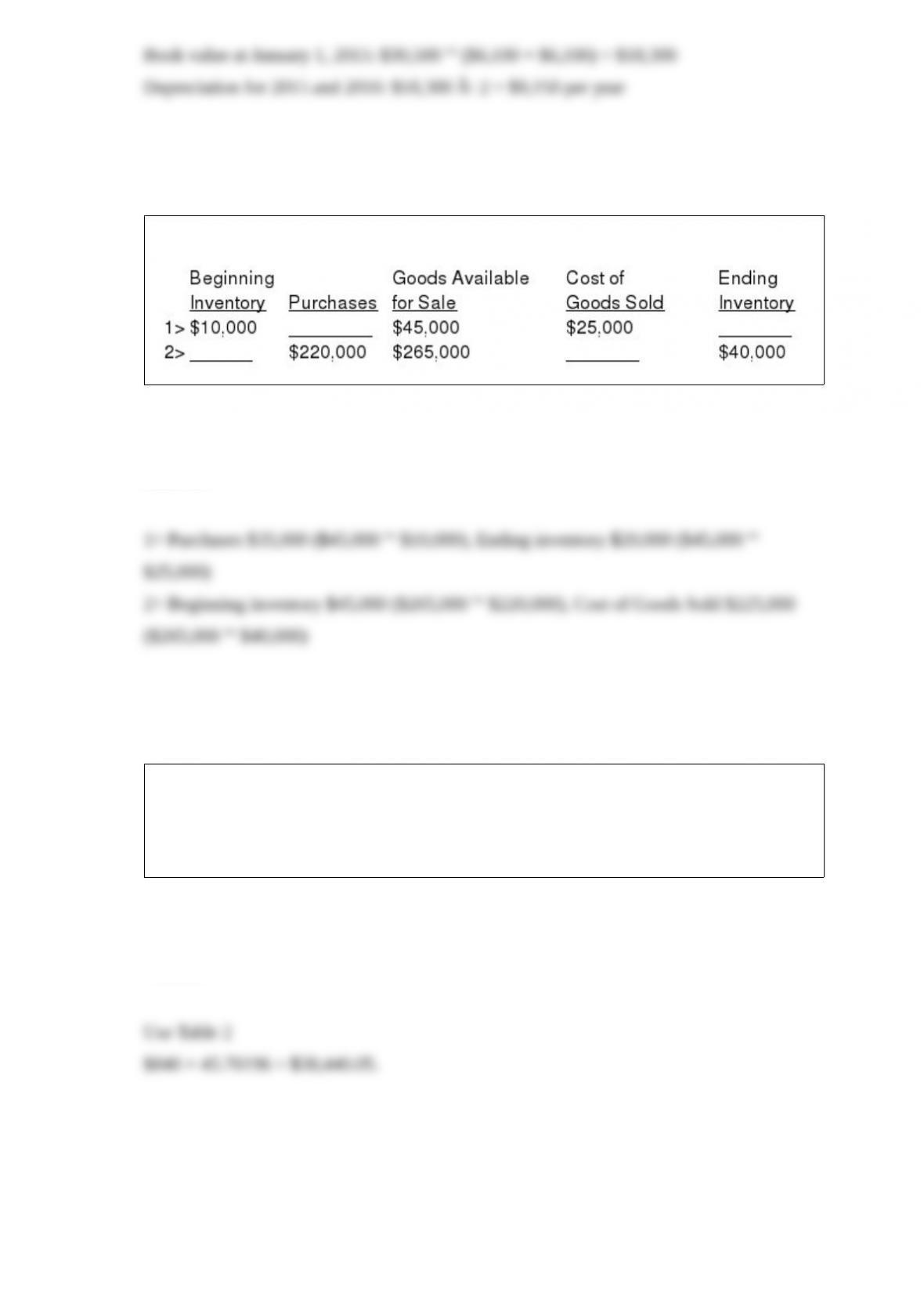

For each of the following, determine the missing amounts.

Answer:

Bill Cigarettes acquired a bad habit of smoking in high school. Bill spends

approximately $70 a month or $840 a year on cigarettes. He is not concerned with

health issues, but he is keenly aware of financial issues. Show Bill how much he would

have at retirement in 20 years if he invested $840 a year at 8% instead of smoking.

Answer: