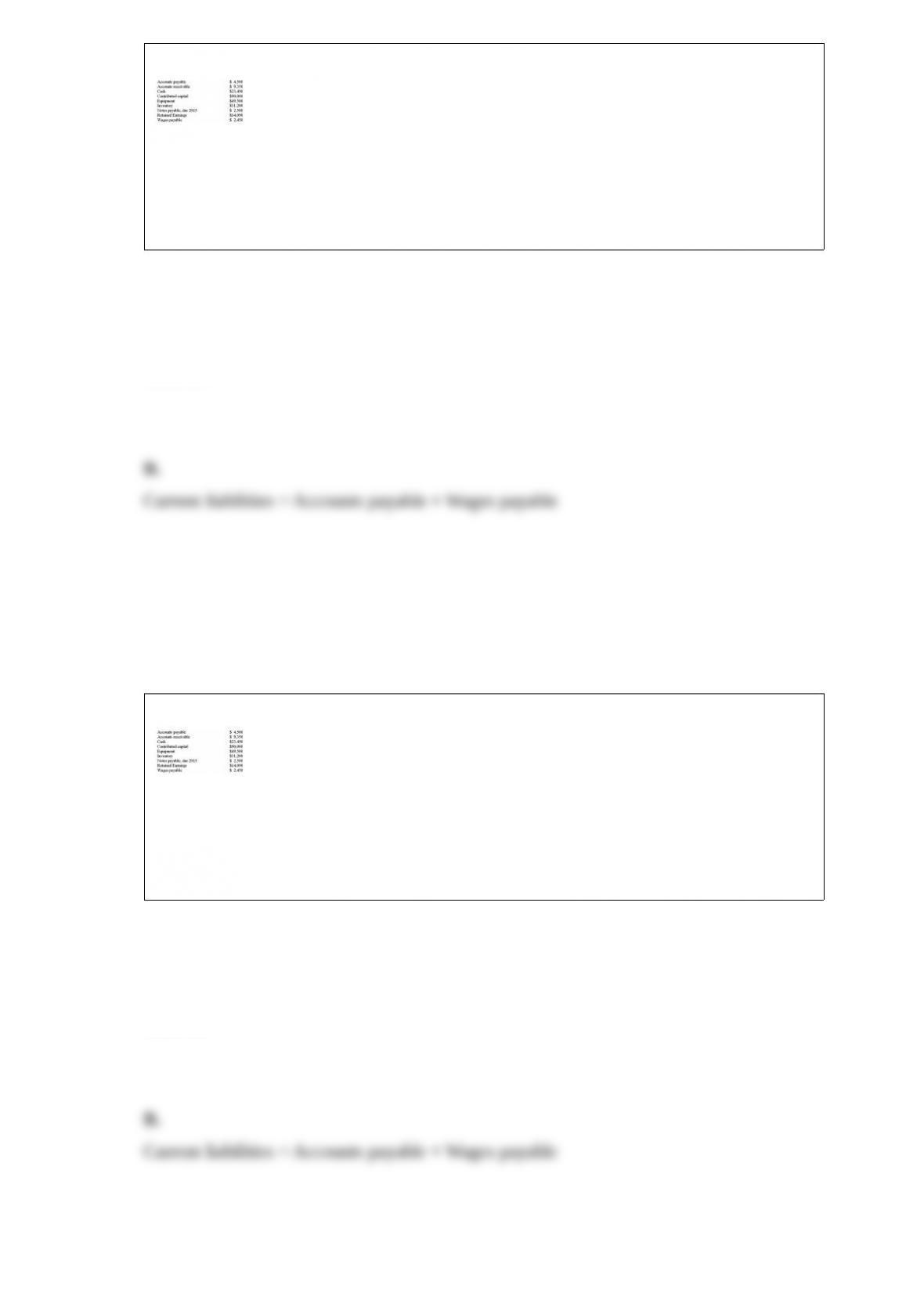

A company reported the following information at December 31, 2013:

What is the amount of current liabilities on the classified balance sheet?

A. $9,450

B. $6,950

C. $113,540

D. $4,500

Answer:

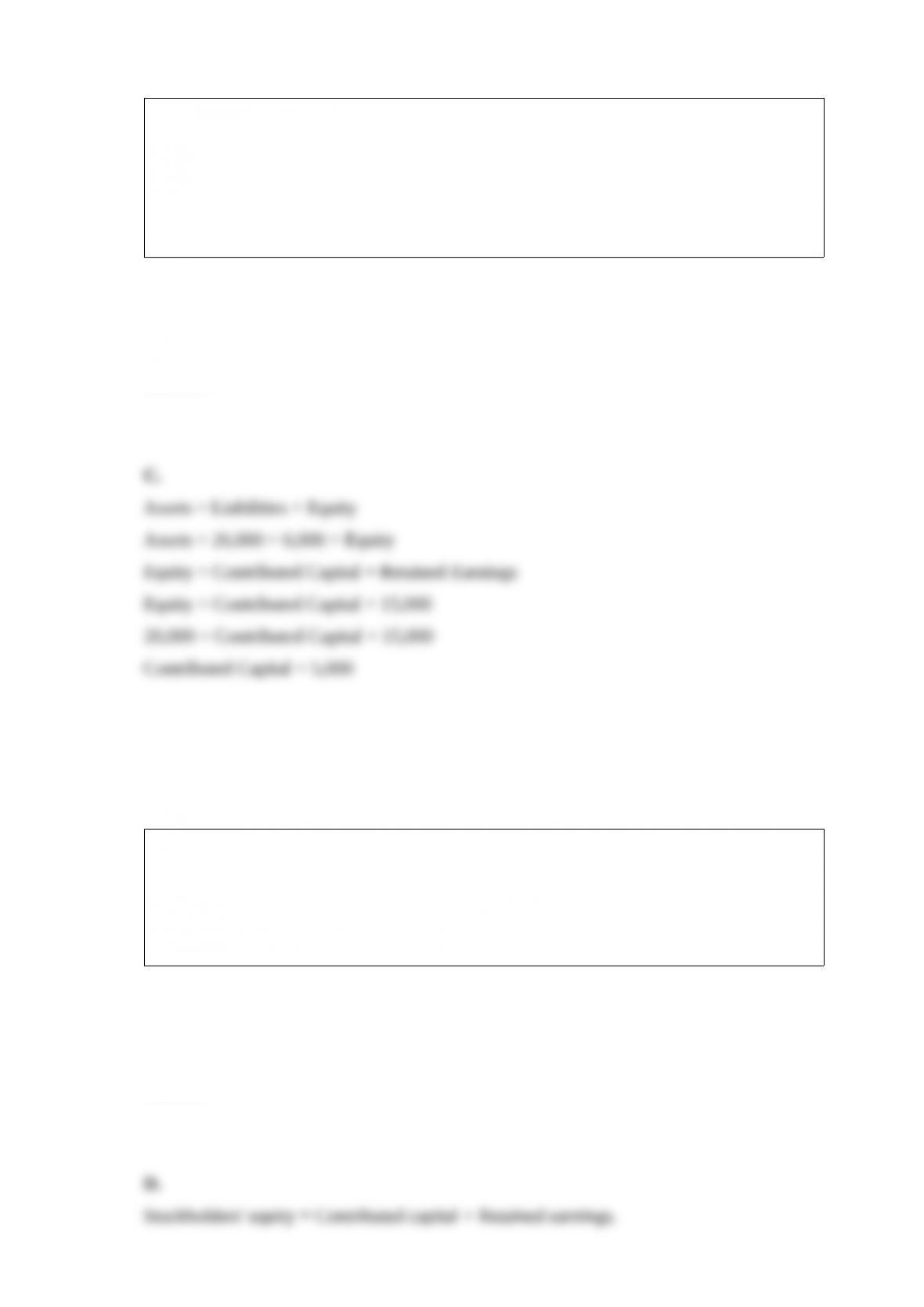

A company reported the following information at December 31, 2013:

What is the amount of current liabilities on the classified balance sheet?

A. $9,450

B. $6,950

C. $113,540

D. $4,500

Answer:

A company reported the following information at December 31, 2013:

What is the total of the CREDIT balance accounts?

A. $111,040

B. $104,090

C. $113,540

D. $108,590

Answer:

Which of the following is a ANSWER: TRUE statement?

A. Conservatism requires accountants to intentionally understate assets.

B. Separate entity assumption in accounting requires that the financial activities of the

owners of a company be reported on the company’s balance sheet.

C. The cost principle states that recording activities at cost will result in the balance

sheet representing the ANSWER: TRUE value of the company.

D. A transaction is recorded in accounting if it has a measurable financial effect on the

assets, liabilities or stockholders’ equity of a business.

Answer:

Which of the following is a ANSWER: TRUE statement?

A. Conservatism requires accountants to intentionally understate assets.

B. Separate entity assumption in accounting requires that the financial activities of the

owners of a company be reported on the company’s balance sheet.

C. The cost principle states that recording activities at cost will result in the balance

sheet representing the ANSWER: TRUE value of the company.

D. A transaction is recorded in accounting if it has a measurable financial effect on the

assets, liabilities or stockholders’ equity of a business.

Answer:

Which account would be increased by a debit?

A. Retained earnings

B. Accounts receivable

C. Contributed capital

D. Notes payable

Answer:

Which account would be decreased by a credit?

A. Cash

B. Accounts payable

C. Contributed capital

D. Retained earnings

Answer:

The classified balance sheet for a company reported current assets of $1,623,850, total

liabilities of $799,540, contributed capital of $1,000,000 and retained earnings of

$130,260. The current ratio was 2.5.

What is the total amount of noncurrent assets?

A. $493,590

B. $824,310

C. $649,540

D. $305,950

Answer:

The classified balance sheet for a company reported current assets of $1,623,850, total

liabilities of $799,540, contributed capital of $1,000,000 and retained earnings of

$130,260. The current ratio was 2.5.

What is the total amount of current liabilities?

A. $649,540

B. $4,059,625

C. $771,920

D. $799,540

Answer:

Which of the following is a FALSE statement?

A. Total Assets are $1,929,800.

B. Total Stockholders’ equity is $1,130,260.

C. Long-term liabilities are $130,260.

D. The amount of current assets is 2.5 times the amount of current liabilities.

Answer:

Which of the following is a FALSE statement?

A. Total Assets are $1,929,800.

B. Total Stockholders’ equity is $1,130,260.

C. Long-term liabilities are $130,260.

D. The amount of current assets is 2.5 times the amount of current liabilities.

Answer:

A company purchased land costing $27,000 by making a 25 percent cash down

payment and signing a 90-day note for the balance. The entry to record this transaction

would

A. Increase total assets.

B. Decrease total liabilities.

C. Decrease contributed capital.

D. Increase retained earnings.

Answer:

Each account is assigned a number and this listing of all accounts is called a

A. trial balance.

B. journal.

C. ledger.

D. chart of accounts.

Answer:

Which of the following would decrease stockholders’ equity?

A. Stock issued for cash.

B. Repayment of notes payable.

C. Land purchased for cash.

D. Dividends paid to owners.

Answer:

A Company has $15,000 of retained earnings, $26,000 of assets, and $6,000 of

liabilities. How much is contributed capital?

A. $17,000

B. $15,000

C. $5,000

D. $35,000

Answer:

Stockholders’ equity in a corporation consists of:

A. long-term assets.

B. current assets plus long-term assets.

C. assets plus liabilities.

D. contributed capital plus retained earnings.

Answer:

Typical cash flows from investing activities include:

A. payments to purchase property and equipment.

B. repayment of loans.

C. proceeds from issuing notes payable.

D. receipts from cash sales.

Answer:

On January 1, Kirk Corporation had total assets of $850,000. During the month the

following activities occurred:

– Kirk Corporation acquired equipment costing $6,000, promising to pay cash for it in

60 days.

– Kirk Corporation purchased $3,500 of supplies for cash.

– Kirk Corporation sold land which it had acquired 2 years ago. The land had cost

$15,000 and it was sold for $15,000 cash.

– Kirk Corporation signed an agreement to rent additional storage space next month at a

charge of $1,000 per month.

– The financial vice president of Kirk Corporation purchased a new vehicle for cash of

$35,000.

What is the amount of total assets of Kirk Corporation at the end of the month?

A. $859,500

B. $856,000

C. $821,000

D. $806,000

Answer:

Which of the following statements is ANSWER: TRUE?

A. Asset and liability accounts have a normal debit balance.

B. To debit an account means to increase it.

C. Contributed capital and retained earnings have a normal credit balance.

D. To credit an account means to decrease it.

Answer:

Which of the following statements is ANSWER: TRUE?

A. Asset and liability accounts have a normal debit balance.

B. To debit an account means to increase it.

C. Contributed capital and retained earnings have a normal credit balance.

D. To credit an account means to decrease it.

Answer:

Which of the following statements is ANSWER: TRUE?

A. Asset and liability accounts have a normal debit balance.

B. To debit an account means to increase it.

C. Contributed capital and retained earnings have a normal credit balance.

D. To credit an account means to decrease it.

Answer:

Which of the following would cause a trial balance to be out of balance?

A. A transaction was recorded twice.

B. A transaction was not recorded.

C. A transaction was posted to the wrong accounts.

D. Only the credit of a transaction was recorded.

Answer:

When accounts receivable are collected:

A. Stockholders’ equity increases.

B. Total assets increase.

C. Total assets decrease.

D. The amount of total assets is unchanged.

Answer:

The requirement that transactions be recorded at their exchange price at the transaction

date is called the

A. conservatism exception.

B. separate entity assumption.

C. cost principle.

D. monetary unit assumption.

Answer:

The following changes occurred in the year 2013: Assets decreased by $3,500 and

liabilities increased by $2,800.

What is the amount of the change in stockholders’ equity in the year 2013?

A. $5,750 increase.

B. $700 decrease.

C. $6,300 decrease.

D. $550 increase.

Answer:

What is the amount of stockholders’ equity at January 1, 2014?

A. $9,450

B. $15,750

C. $15,050

D. $14,450

Answer:

Which of the following would not be classified as a current asset?

A. Cash

B. Accounts payable

C. Supplies

D. Inventory

Answer:

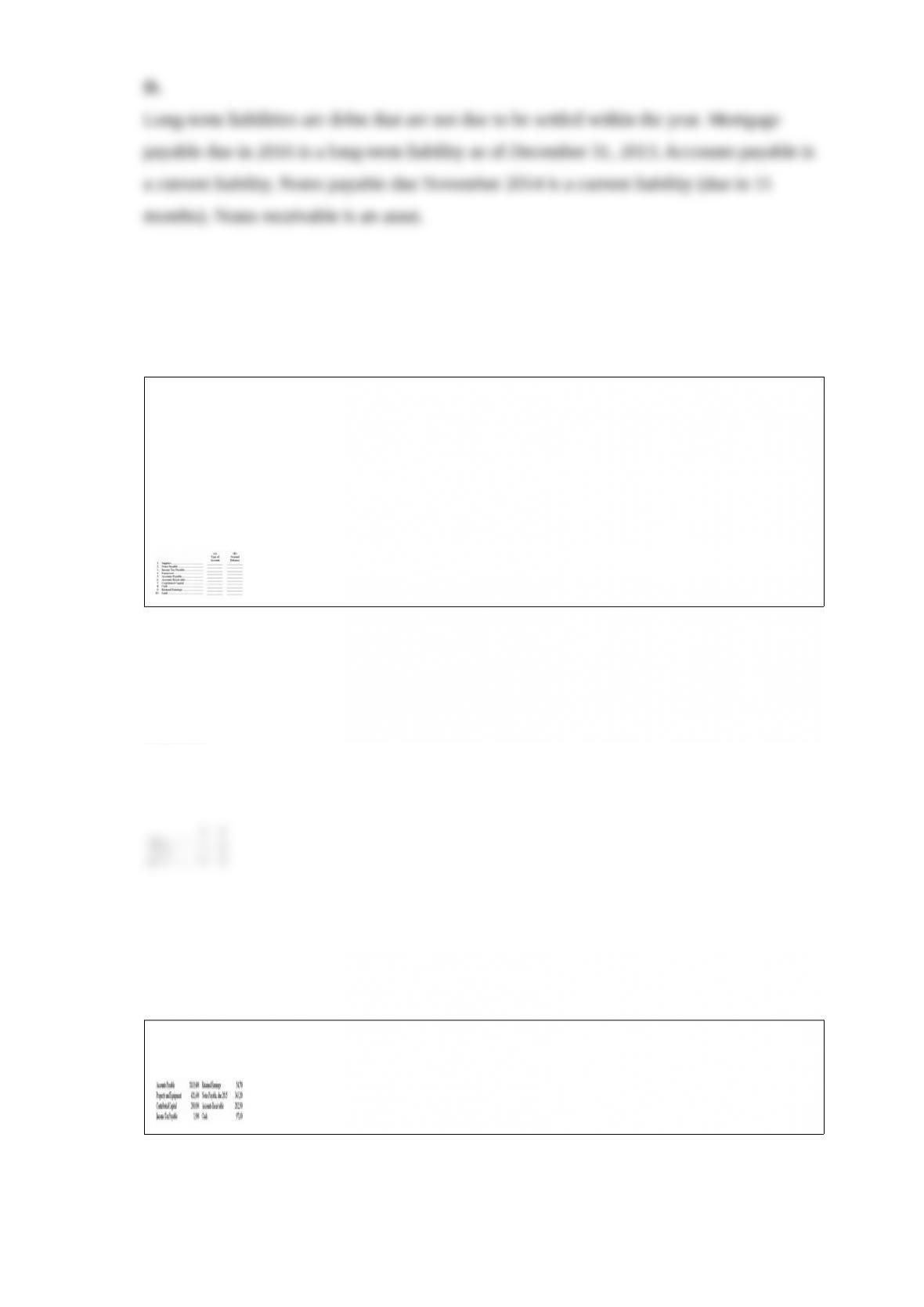

Which of the following would be classified as a long-term liability on the balance sheet

at December 31, 2013?

A. Accounts payable, 30-day account.

B. Notes payable, due November 2014.

C. Notes receivable, matures April 2015.

D. Mortgage payable, due January 2016.

Answer:

Which of the following would be classified as a long-term liability on the balance sheet

at December 31, 2013?

A. Accounts payable, 30-day account.

B. Notes payable, due November 2014.

C. Notes receivable, matures April 2015.

D. Mortgage payable, due January 2016.

Answer:

Selected accounts for Moonbills Corporation appear below.

Instructions: For each account, indicate the following:

(A) In the first column at the right, indicate the nature of each account, using the

following abbreviations:

Asset A, Liability L, Stockholders’ Equity SE.

(B) In the second column, indicate the normal balance by inserting dr (for debit) or cr

(for credit).

Answer:

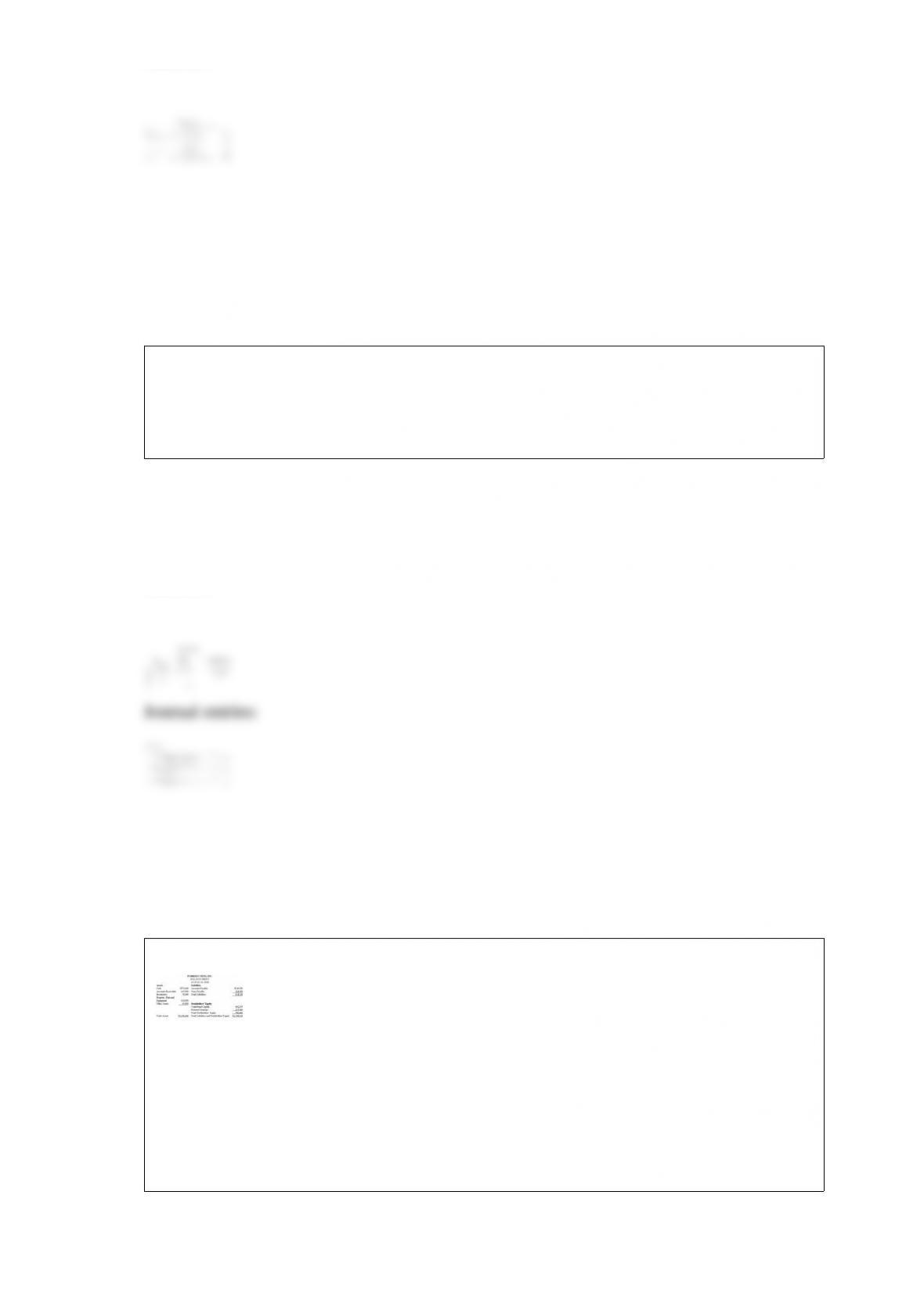

Prepare a classified balance sheet for Purrfect Pets, Inc., using the following data for

June 30, 2013.

Answer:

Stockholders contribute $10,000 cash to a company. The company uses $5,000 to buy

new equipment and $3,000 to pay off accounts payable. Show the effect of these

transactions on the basic accounting equation. Then, show the journal entries that would

be used to record the transactions.

Answer:

The balance sheet for Purrfect Pets, Inc., as of June 30, 2013, is shown below.

During July 2013, stockholders contribute $300,000 cash for additional ownership

shares. The company pays $550,000 in cash and borrows $150,000 from a bank to buy

some new stores.

a) Show the effects of these transactions on the basic accounting equation.

b) Journalize these transactions.

c) Show the new balance sheet as of July 31, 2013, after these transactions have

occurred, assuming there was no other July activity.

Answer:

During the month, a company enters into the following transactions:

– Buys $4,000 of supplies on account.

– Pays $5,000 cash for new equipment.

– Pays off $3,000 of accounts payable.

– Pays off $1,500 of notes payable.

a) Analyze the effect of these transactions on the basic accounting equation.

b) Journalize these transactions.

Answer:

CheapBooks Incorporated (CI) had the following business activities, for which you are

to prepare journal entries. Reference each journal entry to the transaction number,

shown below.

1) Stockholders invest $25,000 cash in the corporation.

2) CI purchased $400 of office supplies on credit.

3) CI purchased office equipment for $7,000, paying $2,500 in cash and signing a

30-day note payable for the remainder.

4) CI paid $200 cash on account for office supplies purchased in transaction 2.

5) CI purchased two acres of land for $10,000, signing a 2-year note payable.

6) CI sold one acre of land at one-half of the total cost of the two acres, receiving the

full amount or $5,000 in cash.

7) CI made a payment of $5,000 on its 2-year note.

Answer:

If a purchase of supplies for $400 was mistakenly recorded as a credit to Supplies, but

the cash paid for the supplies was correctly recorded, what would be the effect on the

accounting equation?

Answer:

On January 1, 2013, NWK, Inc.’s assets were $300,000 and its stockholders’ equity was

$140,000. During the year, assets increased $15,000 and liabilities decreased $10,000.

What was the stockholders’ equity on December 31, 2010?

Answer:

On March 3, 2013, your company pays $4,000 to acquire supplies. Should this be a

recognized accounting transaction? If so, what accounts are affected and by how much

each?

Answer:

Use the following information as of December 31, 2013, to calculate the amounts of

cash and retained earnings. The company’s total assets are $36,000. This company

doesn’t have any other accounts.

Answer:

For each of the following, indicate how the line item would be categorized on a

classified balance sheet.

CA (current asset)

LTA (long-term asset)

CL (current liability)

LTL (long-term liability)

SE (stockholders’ equity)

____ 1/ Property and Equipment

____ 2/ Contributed Capital

____ 3/ Supplies

____ 4/ Retained Earnings

____ 5/ Accounts Receivable

____ 6/ Accounts Payable

Answer:

Match the term and the explanation. There are more explanations than terms.

_____ 1/dr

_____ 2/cr

_____ 3/Classified balance sheet

_____ 4/Contributed capital

_____ 5/Accounting equation

_____ 6/Transaction

_____ 7/Accounts payable

_____ 8/Journal entry

A. The account credited when cash is received in exchange for stock issued.

B. Another name for stockholders’ equity or shareholders’ equity.

C. An exchange or event that has a direct impact on a company’s balance sheet.

D. A balance sheet that has not yet been publicly released.

E. When a company becomes included in the Fortune 500.

F. A method of recording a transaction in debit/credit format.

G. A transaction that is triggered automatically merely by the passage of time.

H. The abbreviation for an item posted on the left side of a T-account.

I. The expression that assets must equal liabilities plus stockholders’ equity.

J. The value of a company’s public relations campaign.

K. Amounts owed to suppliers for goods or services bought on credit.

L. An event that has no effect on the balance sheet and is not recorded in the financial

statements.

M. Liabilities divided by assets.

N. A balance sheet that has assets and liabilities categorized as current vs. long-term.

O. The abbreviation for an item posted on the right side of a T-account.

Answer:

For each of the following, indicate how the event would most likely be categorized.

EE (external exchange)

IE (internal event)

NT (no transaction)

____ 1/A company sells $2 million in goods for immediate payment.

____ 2/The company uses up office supplies.

____ 3/The stock market rises 10% and the value of a company’s stock increases.

____ 4/A company pays cash to an inventor for the legal rights to produce a new

product.

____ 5/Management promises to pay workers an overtime bonus as required by their

union contract.

____ 6/A company uses up supplies to manufacture a product.

____ 7/A company receives $1 million in orders but no down payments.

Answer:

Listed below are components of several transactions. In the blank to the left indicate

whether a debit (dr) or credit (cr) would be required to record the component of the

transaction.

_____1/ Increase in Cash.

_____2/ Increase in Accounts Payable.

_____ 3/ Decrease in Notes Payable.

_____4/ Increase in Inventory.

_____ 5/Increase in Contributed Capital.

_____ 6/ Decrease in Property and Equipment.

Answer:

Match the term and the explanation. There are more explanations than terms.

_____ 1/Duality of effects

_____ 2/Journal entry

_____ 3/Posting

_____ 4/Conservatism

_____ 5/Debit

_____ 6/Chart of accounts

_____ 7/T-account

_____ 8/Credit

_____ 9/Cost principle

A. A journal entry that lowers the balance of the account.

B. When journal entries are copied to the appropriate T-account.

C. The concept that a company must keep separate accounts by time period.

D. A simplified version of an account in the General Ledger.

E. The mechanism used to record each transaction in the General Journal.

F. When a company’s balance sheet has been verified by an outside auditor.

G. The concept that any transaction must have at least two effects on the accounting

equation.

H. When a dollar value is assigned to an item recorded in the accounting system.

I. Compares balance sheet items from two different time periods.

J. An amount that is posted on the left side of a T-account or ledger.

K. The principle that a company should use the least optimistic measure, when

uncertainty exists.

L. Assets are initially recorded at the amount paid to acquire them.

M. A journal entry that raises the balance of the account.

N. A balance sheet where assets appear on the top, liabilities in the middle and

stockholders’ equity appears on the bottom.

O. An amount that is posted on the right side of a T-account.

P. A summary of account names and numbers.

Answer:

Match the term and the explanation. There are more explanations than terms.

_____ 1/Duality of effects

_____ 2/Journal entry

_____ 3/Posting

_____ 4/Conservatism

_____ 5/Debit

_____ 6/Chart of accounts

_____ 7/T-account

_____ 8/Credit

_____ 9/Cost principle

A. A journal entry that lowers the balance of the account.

B. When journal entries are copied to the appropriate T-account.

C. The concept that a company must keep separate accounts by time period.

D. A simplified version of an account in the General Ledger.

E. The mechanism used to record each transaction in the General Journal.

F. When a company’s balance sheet has been verified by an outside auditor.

G. The concept that any transaction must have at least two effects on the accounting

equation.

H. When a dollar value is assigned to an item recorded in the accounting system.

I. Compares balance sheet items from two different time periods.

J. An amount that is posted on the left side of a T-account or ledger.

K. The principle that a company should use the least optimistic measure, when

uncertainty exists.

L. Assets are initially recorded at the amount paid to acquire them.

M. A journal entry that raises the balance of the account.

N. A balance sheet where assets appear on the top, liabilities in the middle and

stockholders’ equity appears on the bottom.

O. An amount that is posted on the right side of a T-account.

P. A summary of account names and numbers.

Answer:

On June 30, a company purchased 1 year of insurance coverage which started

immediately, paying cash of $2,400. Choose theTRUE statement.

A. On June 30, cash would be debited for $2,400.

B. On the Income Statement for the year, insurance expense will be $1,200.

C. On the Balance Sheet at the end of the year, prepaid insurance will be $2,400.

D. On the Balance Sheet at the end of the year, prepaid insurance will be a non-current

asset.

Answer:

The allowance method for uncollectible accounts is used for accounts receivable but not

for notes receivable.

Answer:

If a company uses $100 million in cash to pay off debt, its stockholders’ equity will rise

$100 million.

Answer:

Which of the following is notTRUE of the Income Statement of a company that was

formed 10 years ago?

A. Reports a Net Loss for the year if expenses are more than revenues.

B. Reports the financial effects of activities that have occurred since the company’s

inception.

C. Reports the amount of the increase in stockholders’ equity this year as a result of the

company’s operations.

D. Reports Net Income which is not an account in the ledger.

Answer:

A company has net income of $148,000 and a net profit margin ratio of .087.

Which of the following is not aTRUE statement?

A. A net profit margin ratio of .087 means that 8.7 cents of profit or net income is made

for each dollar of sales.

B. The amount of sales revenue for this period is $1,700,000 (rounded to the nearest

hundred thousand).

C. A higher net profit margin ratio this year than last year indicates an improvement in

controlling expenses.

D. If income from operations is less than net income, this means that the company had

no non-operating revenue.

Answer:

Which of the following isTRUE about terms 2/10, n/30?

A. A 2% discount is given if the invoice is paid in 10 days; the full amount is due in 30

days.

B. A 10% discount is given if the invoice is paid in 2 days; the full amount is due in 30

days.

C. The discount period is 30 days.

D. The credit period is 10 days.

Answer:

Which one of the following statements regarding the accrual and cash basis of

accounting isTRUE?

A. Using the accrual basis of accounting, if payment is received before delivery of a

good or service, a revenue is recorded at the time the payment is received.

B. Using the accrual basis of accounting, if payment is received after delivery of a good

or service, an asset is recorded at the time the good or service was delivered.

C. Using the cash basis of accounting, if payment is received before delivery of a good

or service, net income is affected when goods or services are delivered.

D. Using the cash basis, if payment is received after delivery of a good or service,

unearned revenue is recorded.

Answer:

Income tax expense would be found on the income statement of a corporation, but not

on the income statement of a sole proprietorship.

Answer:

If inventory is sold with terms of FOB destination, goods in transit belong to the seller.

Answer:

Which of the following is notTRUE regarding the quick ratio?

A. If a company has more current assets than liquid assets, the current ratio will be

larger than the quick ratio.

B. A high quick ratio suggests a high ability to pay current liabilities.

C. Liquid assets include cash and cash equivalents, short-term investments, and net

accounts receivable.

D. A quick ratio greater than 1 implies a company could not pay all of its current

liabilities.

Answer:

A company incurred $5,000 in wages for employees for the year. $4,500 of these wages

were paid by the end of the year. Choose theTRUE statement.

A. Wages payable on the income statement will be $4,500.

B. Wages expense on the income statement will be $500.

C. Wages expense on the balance sheet will be $5,000.

D. Wages payable on the balance sheet will be $500.

Answer:

Which of the following statements regarding periodic versus perpetual inventory

systems isTRUE?

A. Perpetual inventory systems are inferior for determining optimal times to reorder

merchandise.

B. Periodic inventory systems require a greater investment in technology to implement

them.

C. Perpetual inventory systems may assist in determining inventory lost due to

shrinkage.

D. Periodic inventory systems allow sales personnel to provide more immediate

information regarding availability of inventory.

Answer:

The retained earnings account has a beginning balance of $321,975 and an ending

balance of $356,413. Net income is $40,251. Which of the following statements

isTRUE?

A. $5,813 would be subtracted when determining cash flows from financing activities.

B. $40,251 would be added when determining cash flows from financing activities.

C. $34,438 would be added when determining cash flows from financing activities.

D. $321,975 would be added when determining cash flows from operating activities.

Answer:

The closing process includes a transfer of the Dividends Declared account balance to

the Retained Earnings account.

Answer:

Which of the following statements isTRUE of a multiple-step income statement?

A. It groups all revenues together.

B. It reports a different amount of net income than a single-step income statement.

C. It includes expenses that would not appear on a single-step income statement.

D. Net income is probably not the number that investors and creditors care most about.

Answer:

A company has outstanding 10 million shares of $2 par common stock and 1 million

shares of $4 par preferred stock. The preferred stock has an 8% dividend rate. The

company declares $300,000 in total dividends for the year. Which of the following

isTRUE if the preferred stockholders only have a current dividend preference?

A. Preferred stockholders will receive the entire $300,000, and they must also be paid

$20,000 before the end of the current accounting period. Common stockholders will

receive nothing.

B. Preferred stockholders will receive $24,000 or 8% of the total dividends. Common

stockholders will receive the remaining $276,000.

C. Preferred stockholders will receive the entire $300,000, and they must also be paid

$20,000 sometime in the future before common stockholders will receive anything.

D. Preferred stockholders will receive the entire $300,000, but will receive nothing

more relating to this dividend declaration. Common stockholders will receive nothing.

Answer:

Companies within the same industry do not always use the same depreciation method,

but will use the same expected useful life for the same piece of equipment.

Answer:

Liquidity measures the ability of a company to meet its current financial obligations.

Answer:

The asset turnover ratio is directly affected by operating and financing decisions.

Answer:

External audits are conducted by Certified Public Accountants (CPAs) who are not

independent of the company.

Answer:

The adjusted trial balance is completed to check that debits still equal credits after the

income statement is prepared.

Answer:

Which of the following statements regarding the asset turnover ratio isTRUE?

A. The asset turnover ratio compares the amount of sales revenue for the period to the

book value of assets at the end of the period.

B. An asset turnover ratio must be less than 1.

C. The higher the ratio, the less efficiently the company is using its assets.

D. This ratio is not expressed as a percentage.

Answer:

Tax accounting and financial accounting use the same depreciation calculations and

there are no differences in the results between the two accounting systems.

Answer:

Which of the following statements regarding the calculation of cash flows from

operating activities under the direct method isTRUE?

A. When the direct method is used, each revenue and expense account on the income

statement is individually examined to calculate the cash flows from operating activities.

B. Noncash revenues and expenses must be included in cash flows from operating

activities when preparing a statement of cash flows using the direct method.

C. Depreciation is reported as a cash inflow in the cash flows from operating activities

when the direct method is used.

D. A loss on the sale of a long-term asset is subtracted in the cash flows from operating

activities when the direct method is used.

Answer:

A company has an asset account, Prepaid Insurance, with a balance of $3,750 at the

beginning of the month. The company used $980 of insurance during the month. Which

of the following statements isTRUE?

A. The company should credit Insurance Expense for $980 and debit Prepaid Insurance

for $980.

B. Retained earnings should decrease and stockholders’ equity should increase because

of this event.

C. The company should debit Insurance Expense for $980 and credit Prepaid Insurance

for $980.

D. Retained earnings and stockholders’ equity should increase because of this event.

Answer:

Issuing stock to obtain financing is called equity financing.

Answer:

Which of the following statements regarding repurchased stock isTRUE?

A. It is generally less costly for a company to give employees repurchased shares than

to issue new shares.

B. When a company records a stock repurchase, it is tracking a stockholder’s sale of

stock to another investor.

C. Treasury stock is reported on the balance sheet as an asset.

D. Treasury stock is repurchased stock that has been authorized but is not issued.

Answer:

You are pleasantly surprised to discover that a popular actress appears on The Tonight

Show wearing your company’s jeans. Later, your company’s sales increase by $500,000

as a result. When the actress appeared on TV, you would have recorded an asset because

the TV appearance was expected to bring future economic benefits to your company.

Answer:

Which of the following statements is notTRUE of a corporation?

A. A corporation is taxed as a separate legal entity.

B. A corporation has easy transferability of ownership.

C. A corporation may have the ability to raise large amounts of capital.

D. A corporation’s owners have unlimited liability.

Answer:

Your company issued bonds at a premium. Which of the following statements is

notTRUE?

A. The contra account, premium on bonds payable, is amortized each year by shifting

part of its balance to interest expense.

B. On the date of issuance, the stated interest rate was greater than the market interest

rate.

C. As the current date approaches the maturity date, the carrying value of the bond

approaches the face value of the bond.

D. The account used to record the premium has a normal debit balance.

Answer:

Which of the following isTRUE?

A. Credits increase both revenues and expenses.

B. Credits increase expenses and decrease revenues.

C. Credits increase revenues and decrease expenses.

D. Credits decrease both revenues and expenses.

Answer:

Refer to the summary financial information for Momentum Clothing Distributors.

Which of the following statements isTRUE?

A. The company’s level of financing risk was greater in 2014 than it was in 2013.

B. In comparison to 2013, the company became less efficient in 2014 in generating

revenues from its investment in assets.

C. Despite the increase in sales in 2014, the company controlled its expenses just as

well as it had in 2012.

D. The company’s level of financing risk was less in 2013 than it was in 2012.

Answer:

Interest and dividends from investments held by a company are reported as cash inflows

from investing activities on the statement of cash flows.

Answer:

On April 30, 2014, a three-year insurance policy was purchased with a cash payment of

$18,000. Coverage began immediately.

If Salaries payable were recorded on December 31, and these salaries were paid on the

following January 5, the entry on January 5 would be:

A. Debit to Salaries Expense and Credit to Cash.

B. Debit to Salaries payable and Credit to Cash.

C. Debit to Cash and Credit to Salaries Payable.

D. Debit to Cash and Credit to Salaries Expense.

Answer:

The intangible asset most frequently reported by U.S. businesses is:

A. goodwill.

B. trademarks.

C. patents.

D. licensing rights.

Answer:

Carrying insufficient quantities of inventory on hand:

A. would not affect the company’s profitability.

B. may result in lost sales.

C. has little effect on customer satisfaction.

D. will increase the costs of carrying inventory.

Answer:

A contingent liability:

A. is always a specific amount.

B. is an obligation arising from the purchase of goods or services on credit.

C. is an obligation not requiring a future payment.

D. is a potential obligation that depends on a future event.

Answer:

External audits are performed by:

A. Certified Management Accountants (CMAs).

B. Certified Financial Analysts (CFAs).

C. Certified Public Accountants (CPAs).

D. Certified Internal Auditors (CIAs).

Answer:

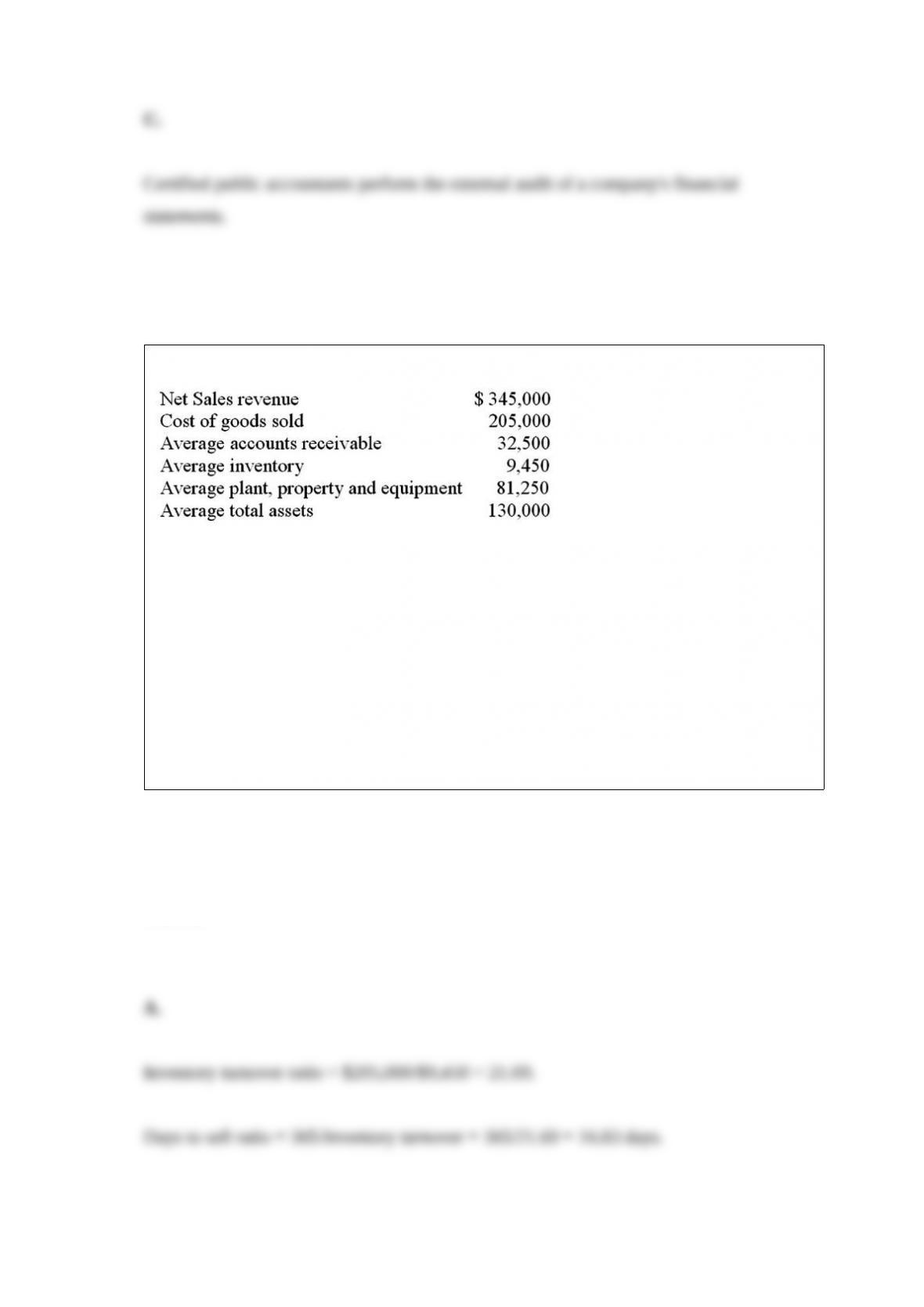

The following information is available for a company for the current year:

Which of the following is closest to the company’s days to sell ratio for the current

year?

A. 16.83

B. 79.18

C. 26.53

D. 34.37

Answer:

Which of the following is an activity in the operations of a manufacturer, but not in the

operations of a merchandising or service company?

A. Selling the good to consumers.

B. Receiving cash.

C. Selling the good to other firms.

D. Buying raw materials.

Answer:

The amount of retained earnings at the end of the year is

A. $15,000.

B. $11,000.

C. $12,000.

D. $1,000.

Answer:

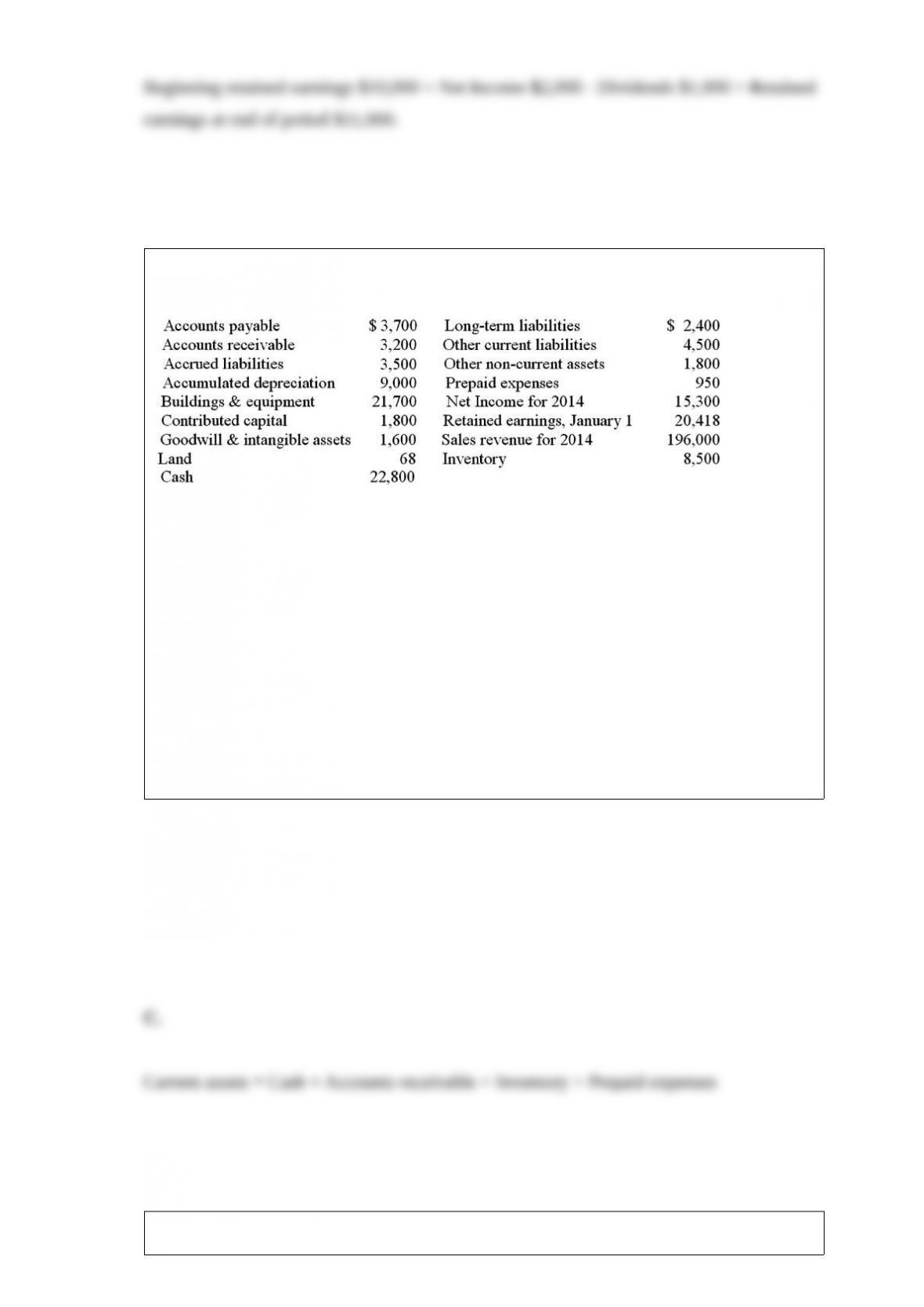

A retail clothing company began operations in 2014 with assets of $42,000. The

following additional data have been taken from the records as of December 31, 2014:

All accounts have normal balances.

What is the amount of current assets to be reported on the balance sheet at the end of

2014?

A. $26,950.

B. $34,500.

C. $35,450.

D. $51,618.

Answer:

An example of an accrued expense is

A. Services performed, but not yet billed.

B. Accumulated interest on a note payable.

C. Prepaid insurance.

D. Depreciation.

Answer:

When interest is calculated for periods shorter than a year, the formula to calculate

interest is:

A. I = P x R x T, where I = interest calculated, P = principal, R = annual interest rate,

and T = number of months.

B. I = P x R x T, where I = interest calculated, P = principal, R = annual interest rate,

and T = (number of months ÷ 12)

C. I = P x R x T, where I = interest calculated, P = principal, R = monthly interest rate,

and T = (number of months ÷ 12).

D. I = (MV – P)/T, where I = interest calculated, MV = maturity value, P = principal and

T = number of months.

Answer:

Flynn Company’s monthly bank statement showed the ending balance of cash of

$18,500. The bank reconciliation for the period showed an adjustment for a deposit in

transit of $1,500, outstanding checks of $2,000, a NSF check of $700, bank service

charges of $30 and the EFT from a customer in payment of the customer’s account of

$1,500.

Use the information above to answer the following question. What journal entry should

be recorded by Flynn Company for the EFT?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

Which of the following actions would be considered unethical?

A. A company does not distribute any of its profits to stockholders.

B. A company rounds the revenues and expenses that it reports on the income

statement.

C. An unintentional mistake made by a new accountant.

D. The cousin of one of the business owners is hired to perform the annual audit.

Answer:

A company’s comparative balance sheet show total assets for 2015 and 2014 as

$990,000 and $900,000, respectively. What is the percentage change to be reported in

the horizontal analysis?

A. Increase of 10%

B. Increase of 9%

C. Increase of 5%

D. Increase of 4%

Answer:

The following transactions occurred during July:

1. Received $800 cash for services rendered during July.

2. Received $5,000 from issuance of stock to investors.

3. Received $400 from a customer in payment of accounts receivable from the prior

month.

4. Billed customers for services performed in July, $3,500.

5. Borrowed $2,500 from the bank, giving a promissory note in exchange.

6. Received $1,000 from a customer for services to be performed next year.

What is the amount of Revenue for July?

A. $5,300

B. $5,700

C. $4,300

D. $7,200

Answer:

A high accounts receivable turnover ratio indicates:

A. the company’s sales are increasing.

B. a large proportion of the company’s sales are on credit.

C. customers are making payments very quickly.

D. the company is taking longer to sell inventory.

Answer:

In a common size balance sheet, each item on the balance sheet is expressed as a

percentage of:

A. Total assets.

B. Total liabilities.

C. Net income.

D. Total stockholders’ equity.

Answer:

A piece of equipment was acquired on January 1, 2013, at a cost of $22,000, with an

estimated residual value of $2,000 and an estimated useful life of four years. The

company uses the double-declining-balance method. What is its book value at

December 31, 2014?

A. $5,500.

B. $10,000.

C. $11,000.

D. $12,000.

Answer:

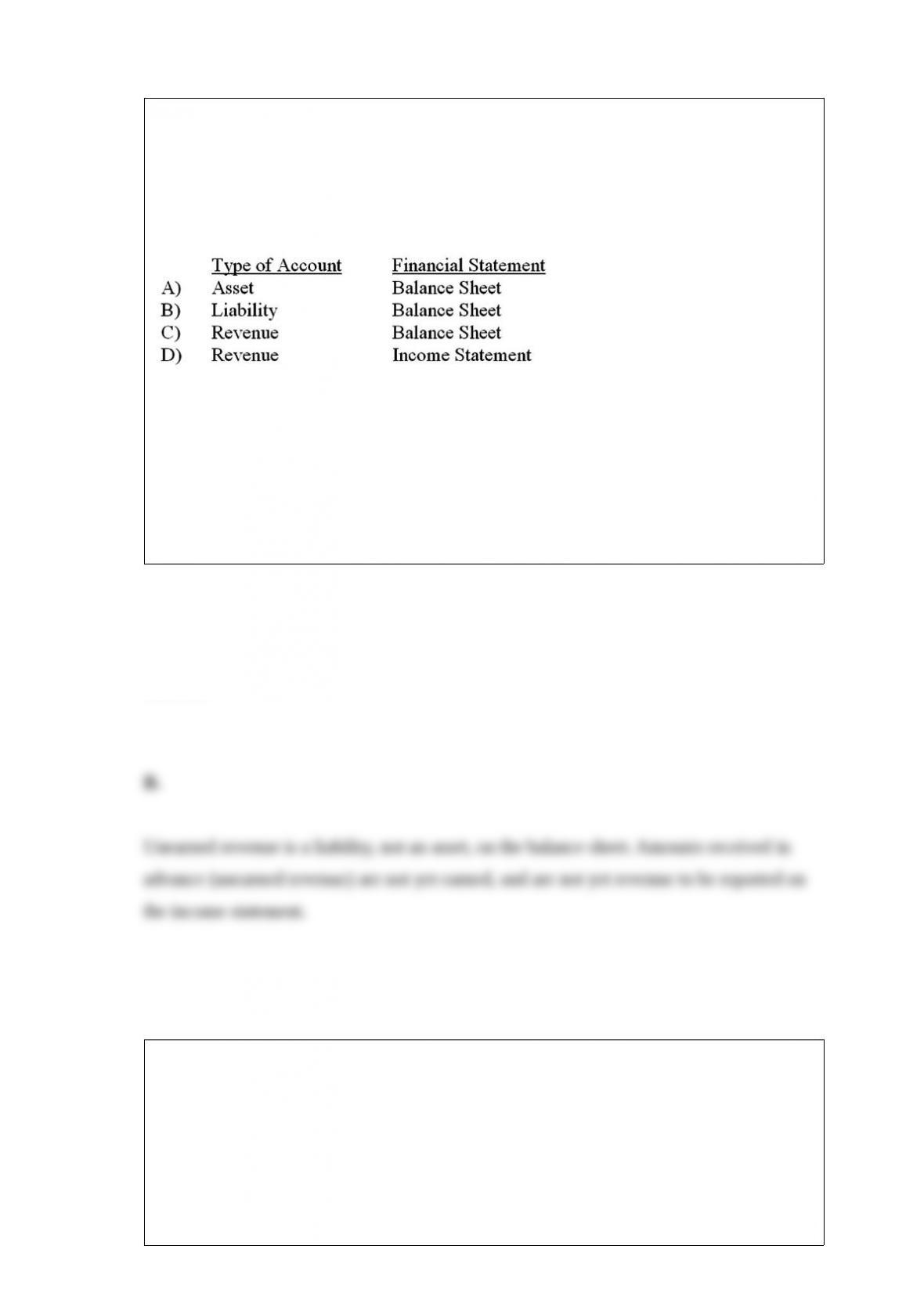

Time Warner is a publishing and communications company, specializing in magazines,

cable television operation, television program development, and other

telecommunication services. Its financial statements show $37,666 in an account called

“Unearned Subscriber Revenue,” which represents amounts that customers have paid in

advance of receiving magazines, cable television, and internet services. What type of

account is this and on what statement is it reported?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

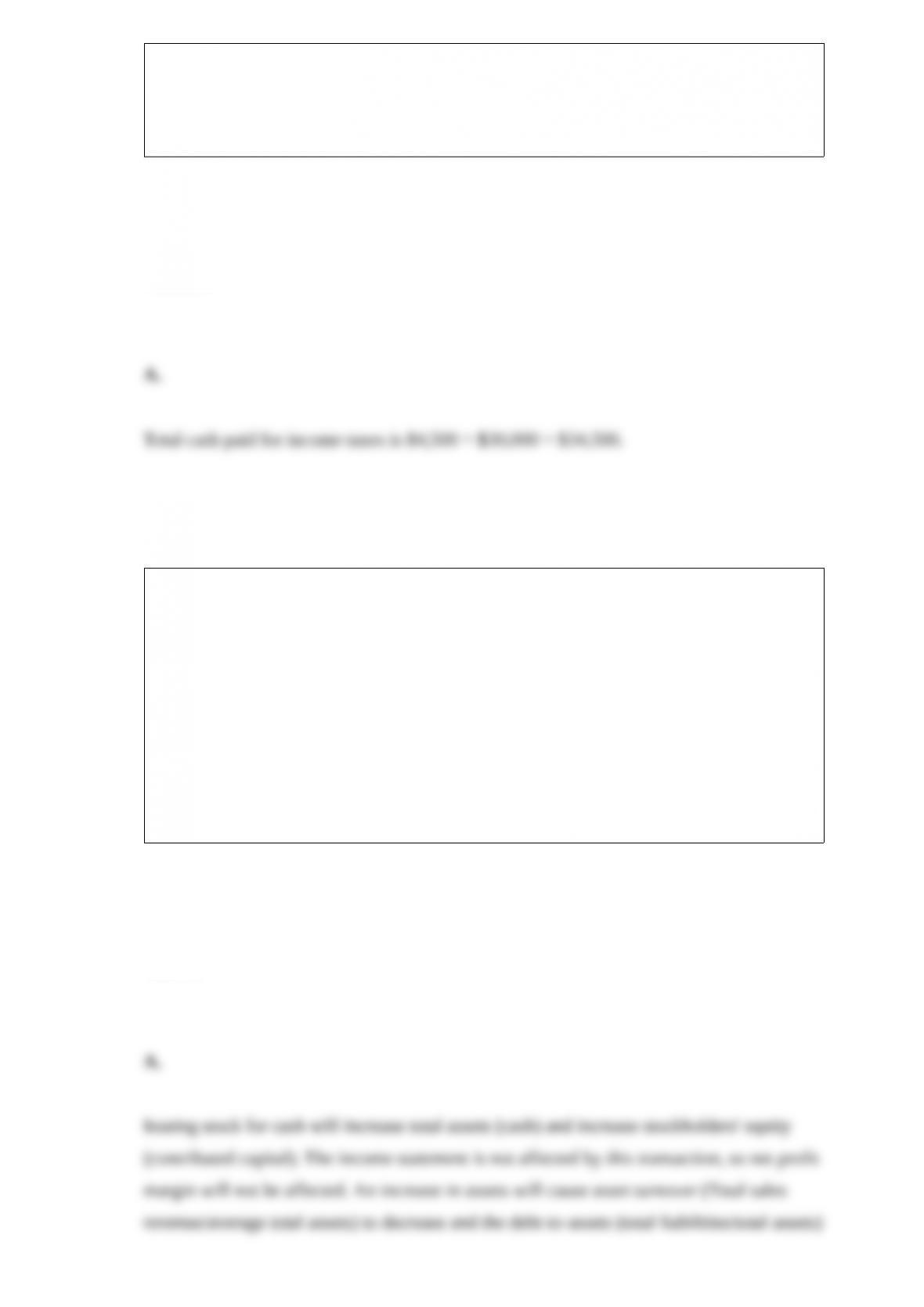

In 2014, a company paid $4,500 which it owed from its 2013 income tax liability and

$30,000 for its 2014 tax liability. The company still owes $6,000 at year-end. How

much should the company report as cash paid for income taxes on its 2014 statement of

cash flows, using the direct method?

A. $34,500

B. $40,500

C. $30,000

D. $3,500

Answer:

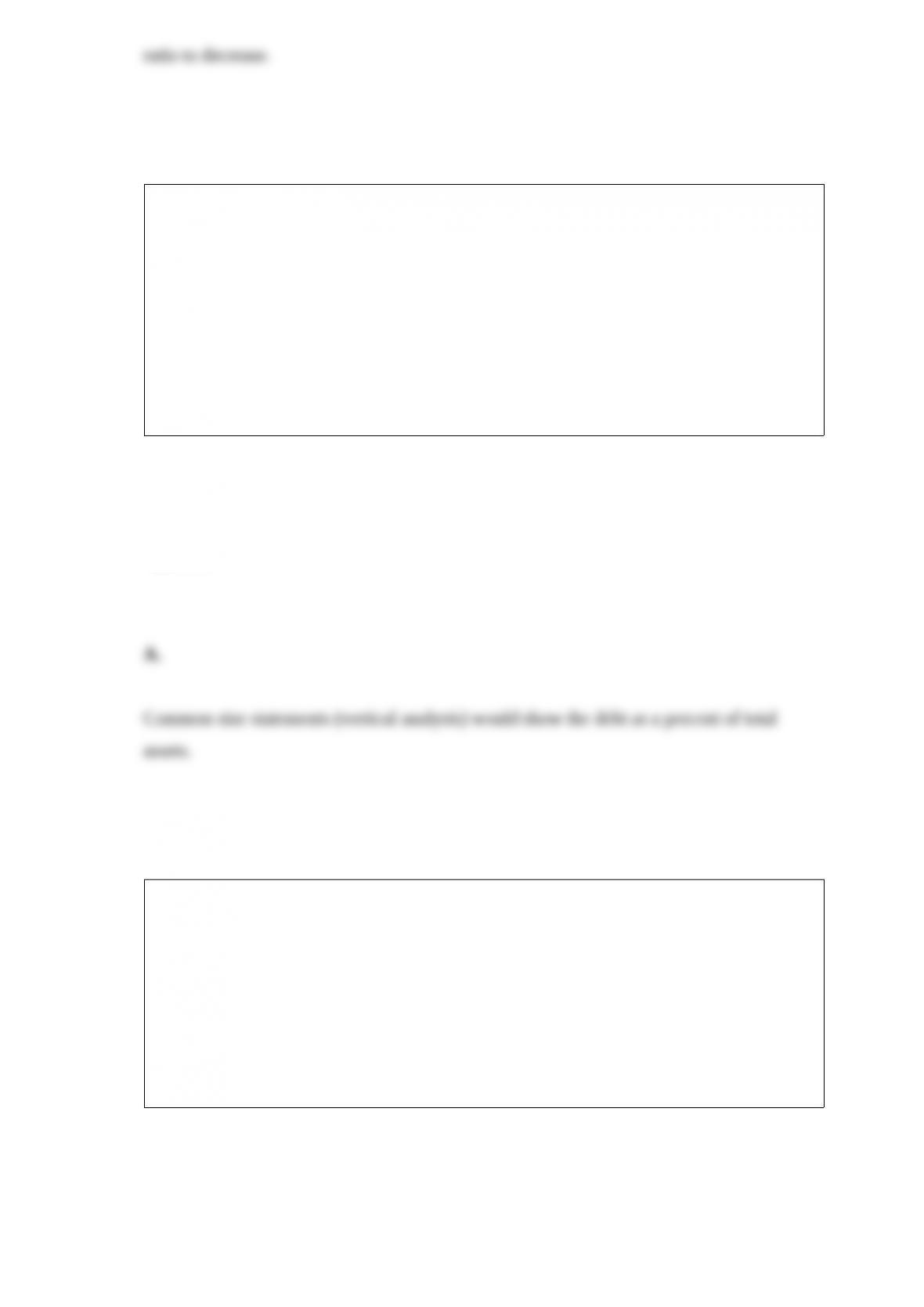

At the end of last year, Cessa Company had total assets in the amount of $4,000,000

and total liabilities in the amount of $3,000,000. The company sold stock to new

stockholders for $1,000,000. As a direct result of this transaction, the:

A. the debt-to-assets ratio will decrease.

B. asset turnover will increase.

C. net profit margin will increase.

D. net profit margin will decrease.

Answer:

Which type of analysis could reveal that a company is relying heavily on debt

financing?

A. Common size statements.

B. Horizontal analysis.

C. The asset turnover ratio.

D. Trend analysis.

Answer:

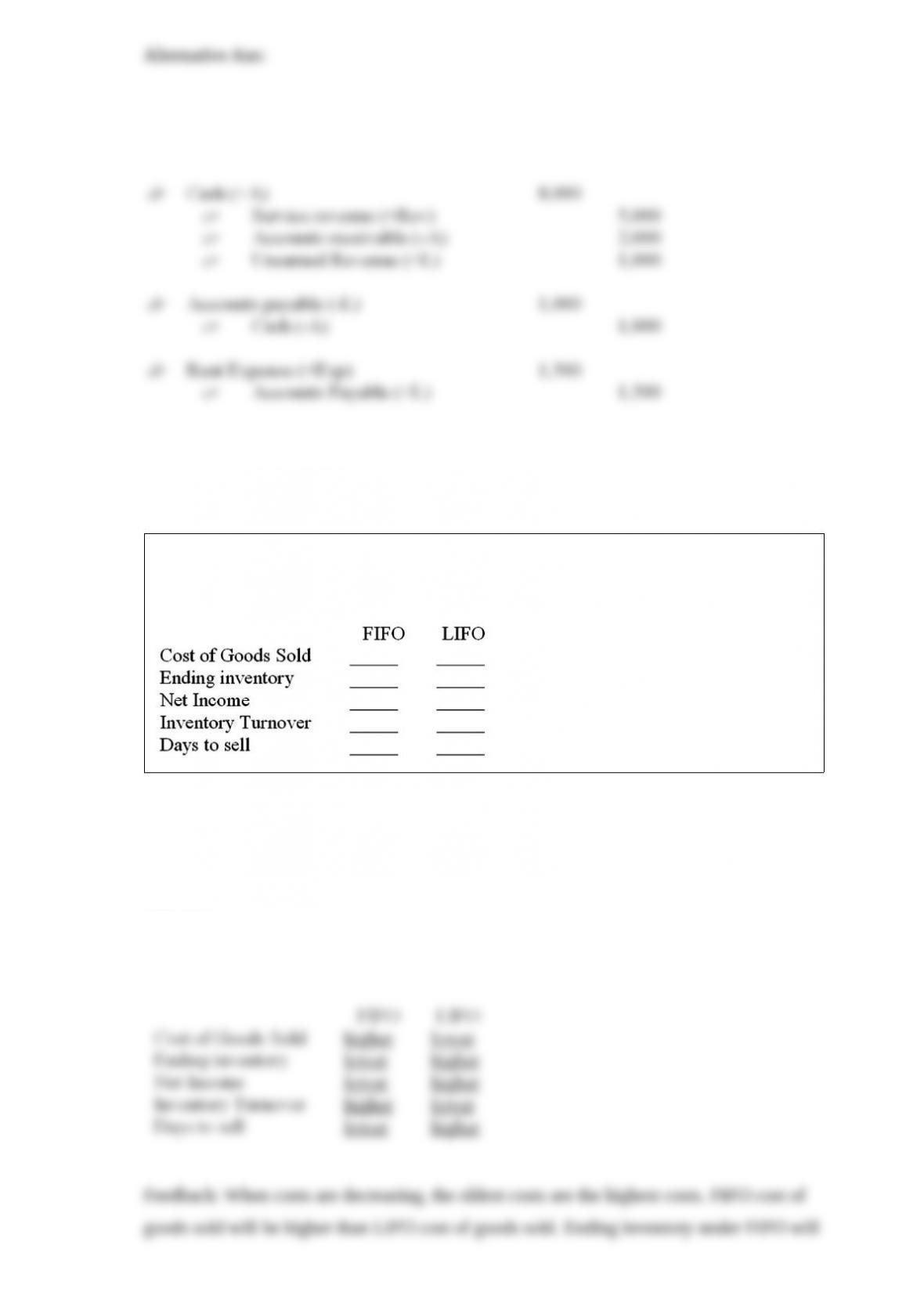

Given the following information for Maynor Company in 2014, calculate the company’s

ending inventory and cost of goods sold using the following inventory costing methods,

assuming the company uses a perpetual inventory system:

a) Weighted Average

b) FIFO

c) LIFO

Answer:

On April 30, 2014, a three-year insurance policy was purchased with a cash payment of

$18,000. Coverage began immediately.

What is the amount to be reported on the balance sheet as Prepaid Insurance at

December 31, 2014?

A. $0

B. $14,000

C. $12,000

D. $16,000

Answer:

When a company records depletion on natural resources, it will have which of the

following effects?

A. Expenses increase.

B. Net income decreases.

C. Inventory increases.

D. Cash flow decreases.

Answer:

Park & Company was recently formed with a $5,000 investment in the company by

stockholders. The company then borrowed $2,000 from a local bank, purchased $1,000

of supplies on account, and also purchased $5,000 of equipment by paying $2,000 in

cash and signing a promissory note for the balance. Based on these transactions, the

company’s total assets are:

A. $7,000.

B. $9,000.

C. $10,000.

D. $11,000.

Answer:

Match the term and the explanation. There are more definitions than terms.

_____ 1/ cash basis

_____ 2/ net profit margin

_____ 3/ unadjusted trial balance

_____ 4/ prepaid expense

_____ 5/ unearned revenue

_____ 6/ revenue recognition policy

_____ 7/ Expense Recognition (Matching) principle

A. Reported when a company sells goods or services in the ordinary course of business

for more than it costs to produce.

B. Reporting expenses and revenue according to the time the underlying activities

occur.

C. A list of account balances when the accounts do not yet include all revenues and

expenses.

D. The concept that expenses should be reported at the same time as the related

revenue.

E. The principle that changes in assets must be matched by changes in liabilities and

equity.

F. Also known as net assets, this is the value of assets minus liabilities.

G. An asset account indicating a company has already paid a cost not yet incurred.

H. A company’s policy on when to report revenue in the financial statements.

I. Reporting expenses and revenues according to the time the money is paid or received.

J. A liability account indicating customers have already paid for services not yet

rendered.

K. A ratio that indicates the percent of each revenue dollar that is left over after

covering costs and expenses.

Answer:

A company uses the direct write-off method and discovers a customer’s account in the

amount of $3,000 will not be paid because the customer has declared bankruptcy. What

is the journal entry that would be made to record this write-off?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

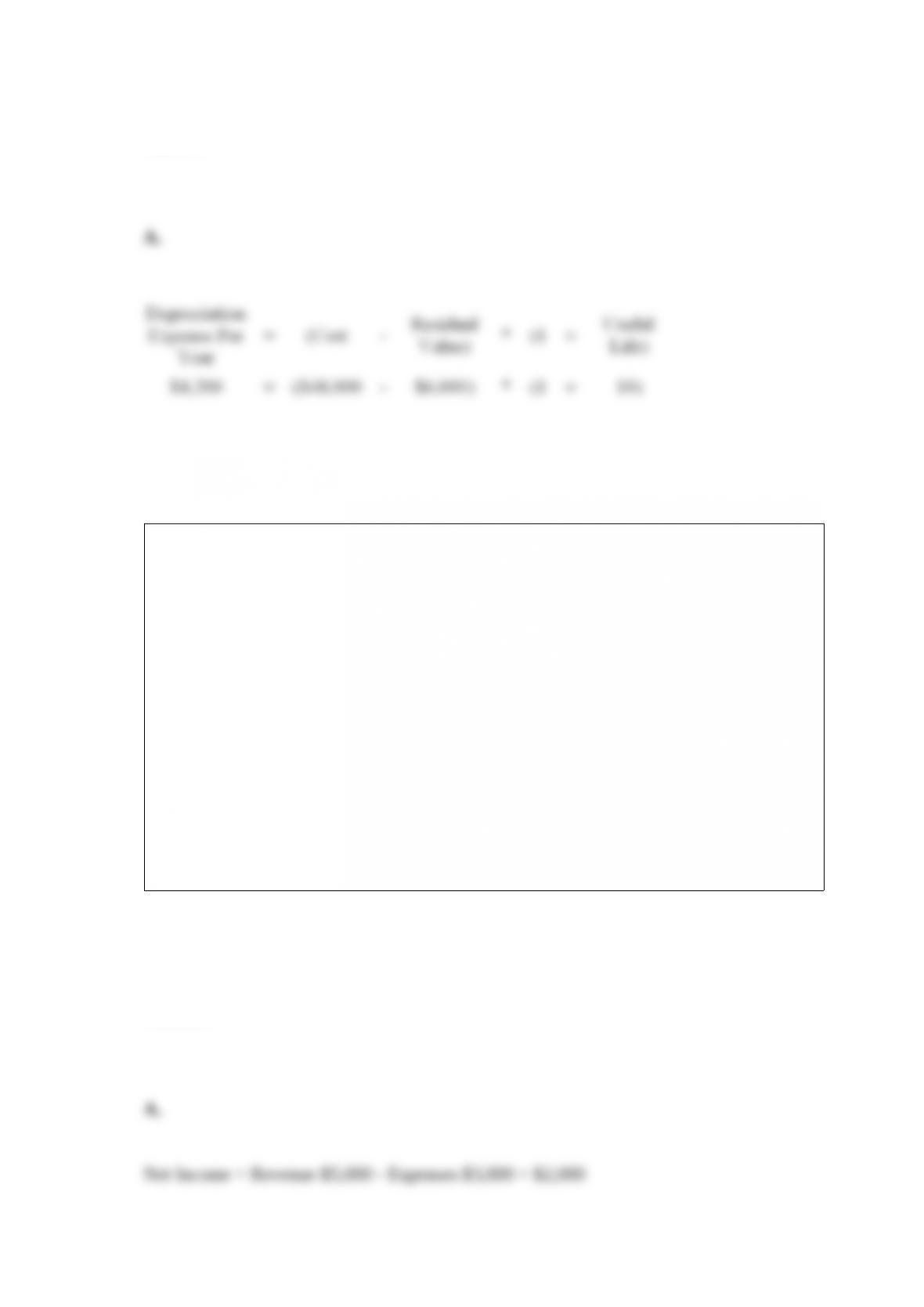

A company buys equipment for $48,000 and expects to use it for ten years and then sell

it for $6,000. Using the straight-line method, the company should report depreciation

for the equipment of:

A. $4,200 per year.

B. $8,400 per year.

C. $4,800 per year.

D. $9,600 per year.

Answer:

A company started the year with the following: Assets $100,000; Liabilities $30,000;

Contributed Capital $60,000; Retained Earnings $10,000. During the year the company

earned revenue of $5,000, all of which was received in cash, and incurred expenses of

$3,000, all of which was unpaid as of the end of the year. In addition, the company paid

dividends of $1,000 to owners. Assume no other activities occurred during the year.

What was the amount of net income for the year?

A. $2,000

B. $1,000

C. $3,000

D. $5,000

Answer:

Which of the following ratios is used to evaluate a company’s efficiency in using its

assets?

A. Current ratio.

B. Debt to assets ratio.

C. Return on assets ratio.

D. Asset turnover ratio.

Answer:

Which of the following would not be considered a contingent liability?

A. Products sold with a warranty.

B. Pending lawsuits.

C. Frequent flyer miles earned by passengers.

D. Advance ticket sales.

Answer:

Brief Respite, Inc., sold underwear made from a fabric that gave many of its customers

a serious rash. The customers are suing the company in a class action suit and Brief

Respite’s attorneys think it is probable that the case will cost the company $2 million,

although the verdict is not yet in. The company should:

A. not include this information in its annual report.

B. record a liability and a gain for $2 million.

C. only explain the situation in the notes to the financial statements.

D. record a liability and a loss for $2 million.

Answer:

Jim’s Gymnastics Training’s operations for the month of October are summarized as

follows:

– Provided $5,000 of training to students.

– Received $8,000 cash from studentsof which $4,000 is for training provided in

October (as billed above), $1,000 is for training to be provided in November, and

$3,000 is for training provided in September.

– Paid September’s gym rental bill of $1,000. Received October’s bill of $1,500 but did

not pay.

Prepare appropriate journal entries using the accrual basis of accounting.

Answer:

Fill in the blanks below with the words “higher” and “lower” to indicate which

inventory costing method causes the value to be higher and which causes it to be lower.

Assume that the cost of merchandise is decreasing.

Answer:

Answer:

Answer:

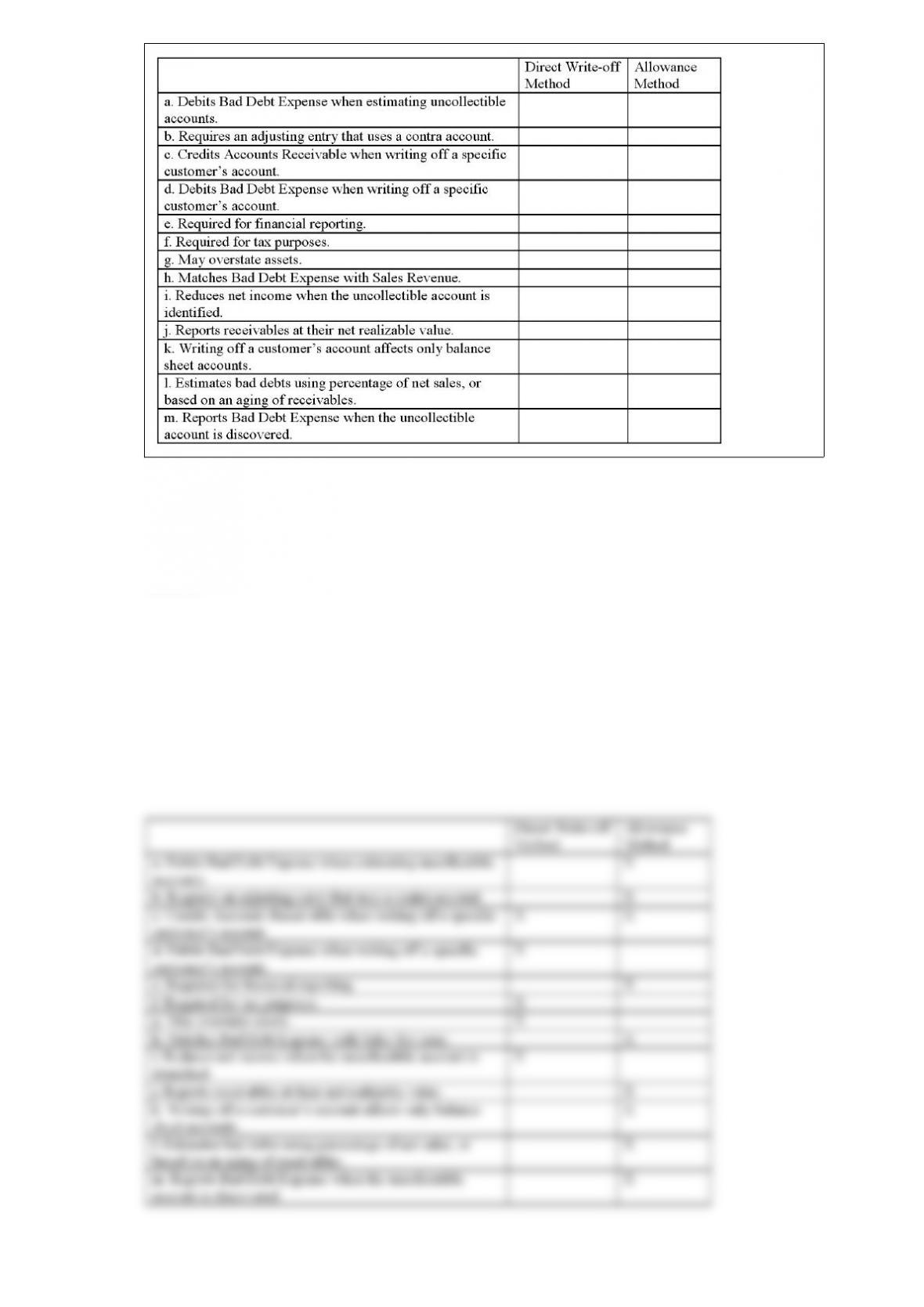

Indicate whether each of the following items is a characteristic of the Direct Write-off

Method or the Allowance Method by placing an “X” in the appropriate column. If an

item is a characteristic of both methods, place an “X” in both columns.

Answer:

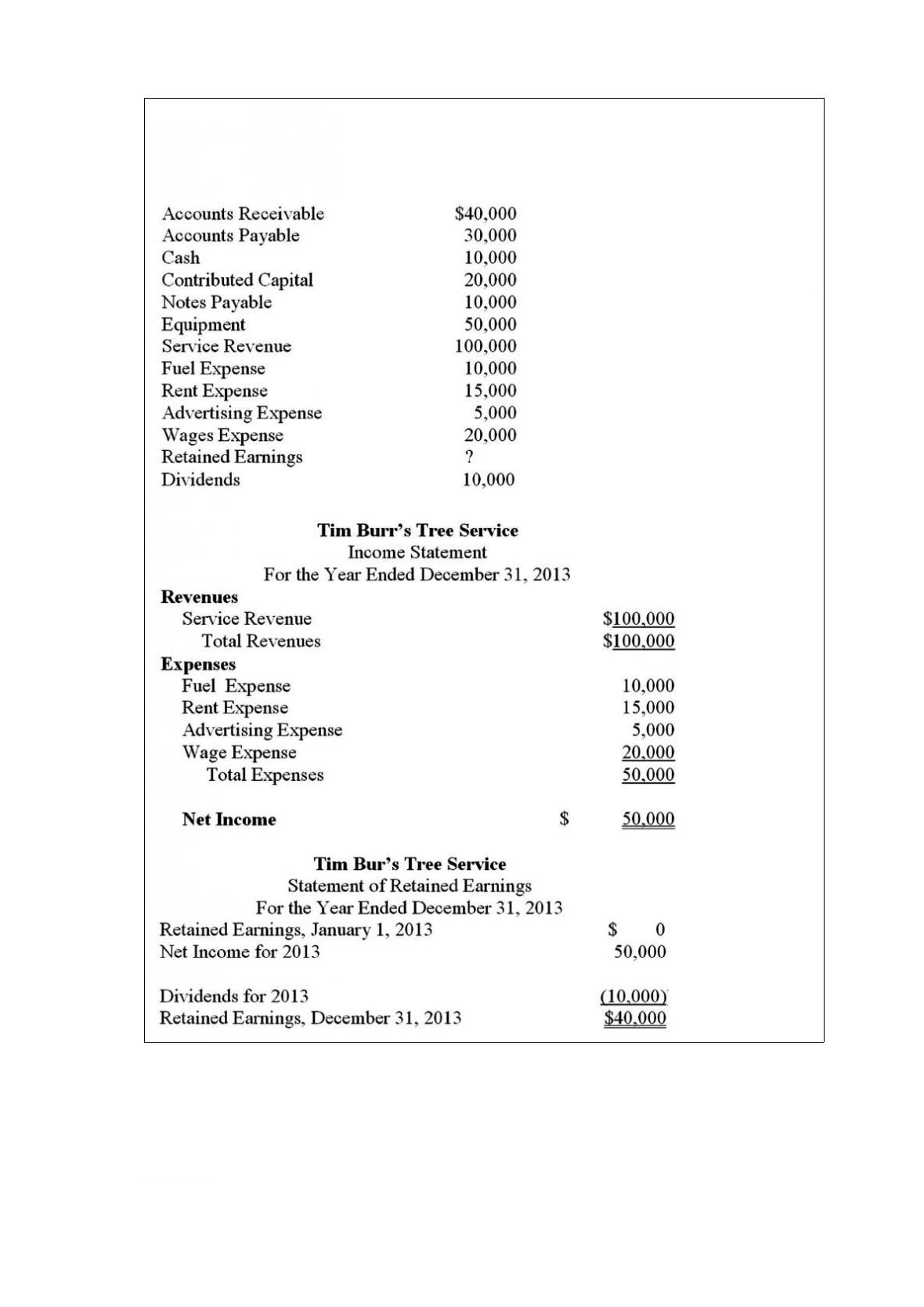

Following is a list of financial statement items and amounts for Tim Burr’s Tree Service

as of 12/31/13, the end of its first year in operation. Use this information to prepare the

Income Statement, Statement of Retained Earnings, and Balance Sheet.

Answer:

Answer:

The following merchandise transactions occurred during December for two different

companies: Rippen and Burnen. Both companies use a perpetual inventory system.

On December 3, Rippen Corporation sold merchandise on account to Burnen Corp. for

$480,000, terms 2/10, n/30. This merchandise originally cost Rippen $320,000.

On December 8, Burnen Corp. returned merchandise to Rippen Corporation for a credit

of $30,000. Rippen returned this merchandise to inventory at its original cost of

$20,000.

December 12, Burnen Corp. paid Rippen Corporation for the amount owed.

A) Prepare the journal entries to record these transactions on the books of Rippen

Corporation.

B) What is the amount of net sales to be reported on Rippen Corporation’s income

statement?

C) What is the Rippen Corporation’s gross profit percentage?

Answer:

You have received the bank statement for your company’s account and need to reconcile

it with your general ledger cash account. Your records show an ending balance for the

month of $12,722.40 while the bank’s records show an ending balance of $12,367.16.

The bank charged $8 in service fees and paid $26.05 in interest. All but three checks

written during the month were processed by the bank without incident during the

month. The three exceptions were:

1) Check #841 was correctly processed by the bank as $981.27 but was mistakenly

recorded by you as $781.27.

2) Check #853 for $64.57 had not yet been processed by the bank.

3) Check #855 for $683.46 had not yet been processed by the bank.

All but two of the deposits made during the month were processed by the bank without

incident. The two exceptions were:

1) A customer check for $307.95, which had been deposited during the month, was

returned NSF.

2) A deposit totaling $613.37 had not yet been processed by the bank.

Using the information provided above, prepare a bank reconciliation.

Answer:

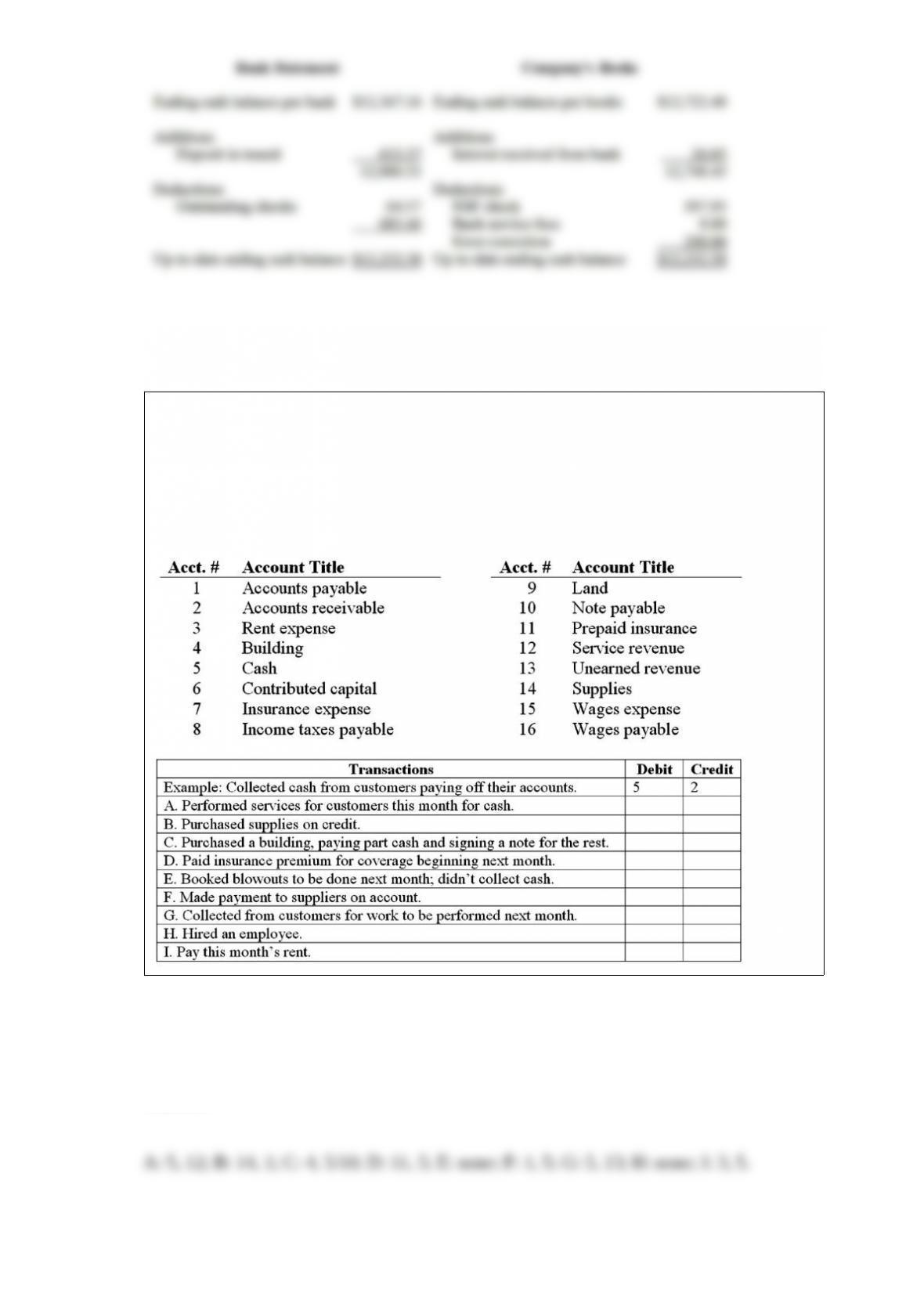

The following is a series of accounts for the Sprinkler Blowout Company, listed

alphabetically and numbered for identification. Following the accounts is a series of

transactions. For each transaction, indicate the account(s) that should be debited and

credited by entering the appropriate account number(s) to the right of each transaction.

If no journal entry is needed, write none after the transaction. The first transaction is

given as an example.

Answer:

On December 31, 2014, Purrfect Pets had retained earnings of $267,800 before making

its closing entries. During 2014, the company had service revenue of $168,100 and

other revenue of $81,300. The company used supplies (mainly cat food and litter)

during the year which cost $87,900. Administrative expenses were $16,400 and wages

(paid in cash) were $18,300. Taxes were $13,700 and dividends declared and paid

totaled $6,000.

Prepare T-accounts for the income statement accounts, dividends declared, and retained

earnings at the end of the year before closing. Then, enter the closing journal entries in

the T-accounts and compute the ending balances of the T-accounts.

Answer:

Answer:

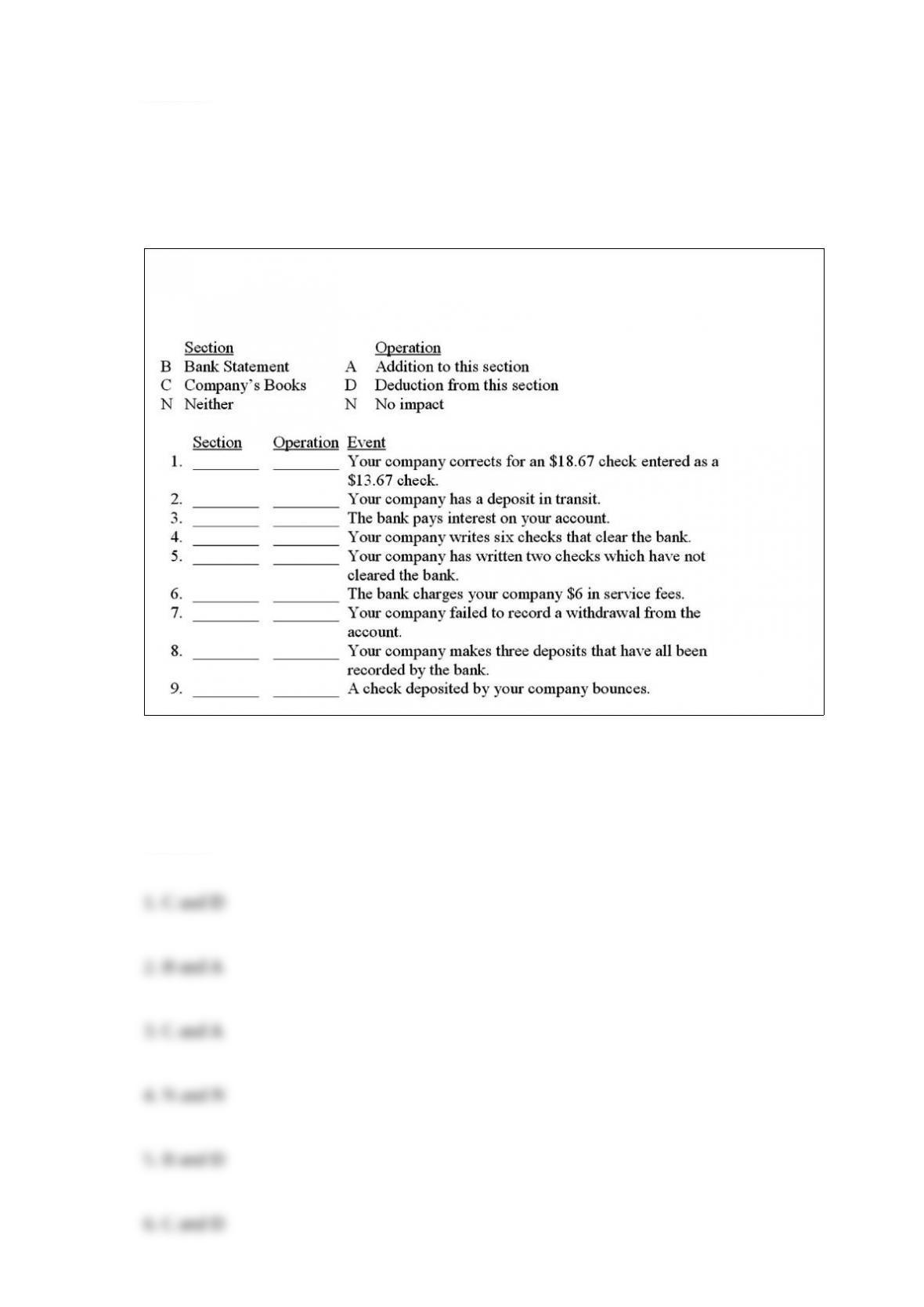

For each of the following events, match the event with the section of the bank

reconciliation in which it is listed, if at all, and indicate the operation performed.

Answer:

Answer:

Insert the appropriate letter A, D, or C into the correct blank to describe the type of

adjustment required at the end of April.

Entry Type

A Accrual adjusting entry

D Deferral adjusting entry

C Closing entry

6/ The Grass is Greener transfers revenues of $50,000 and expenses of $32,000 to

retained earnings.

7/ The Grass is Greener makes an entry to reflect use of equipment.

8/ The Grass is Greener transfers dividends of $1,200 to retained earnings.

9/ The Grass is Greener records income taxes.

10/ The weekly payroll of $5,000 to be paid next week is recorded.

Answer: