1) The auditor’s primary concern about authorization centers on shipment of goods to

customers.

A) True

B) False

2) Independent registrars commonly disburse cash dividends to shareholders.

A) True

B) False

3) When labor is a material factor in inventory valuation, the auditor should place

special emphasis on testing the internal controls concerning:

A) fictitious employees

B) authorization of wage rates

C) proper valuation and allocation of balances

D) completeness of recorded transactions

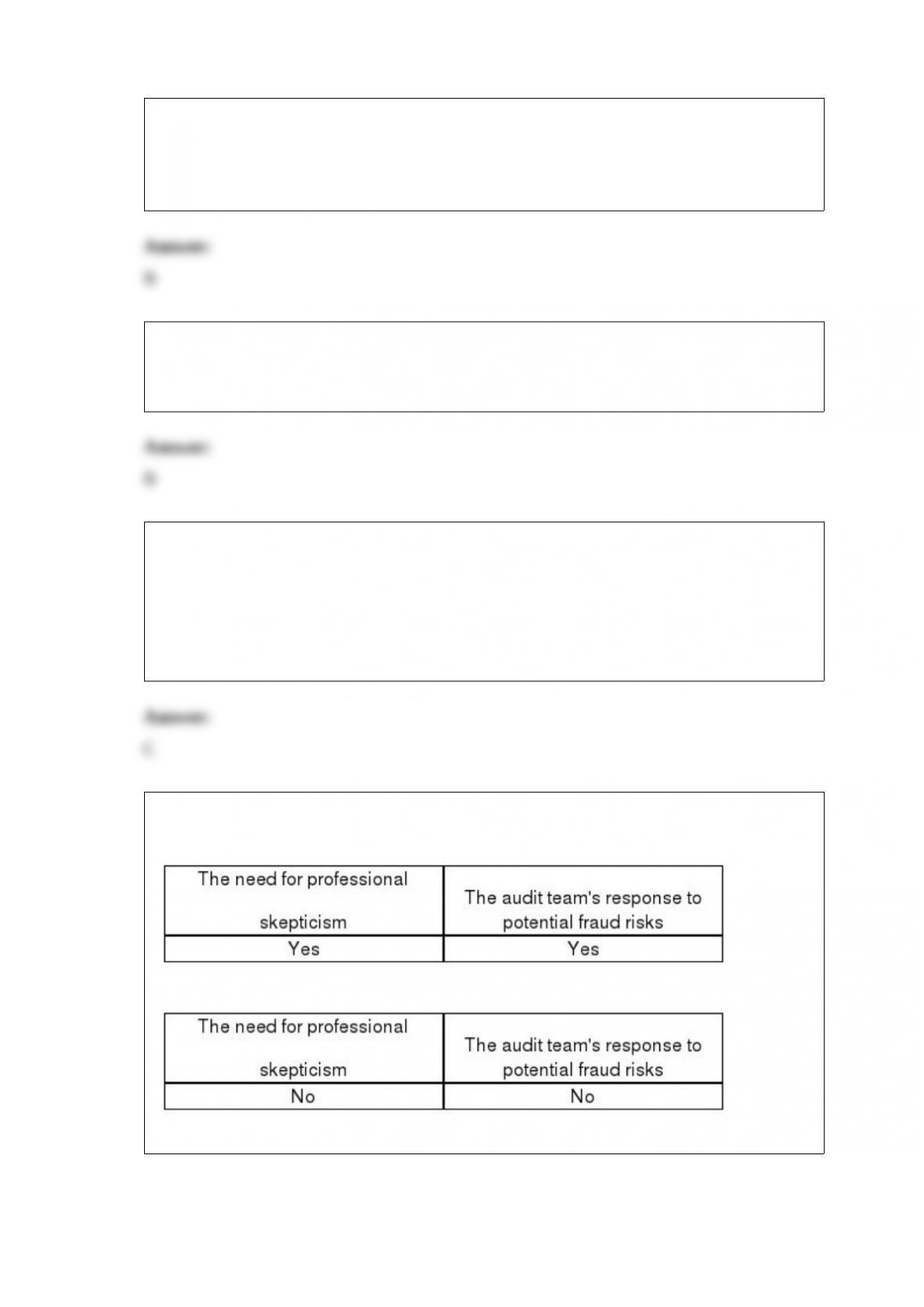

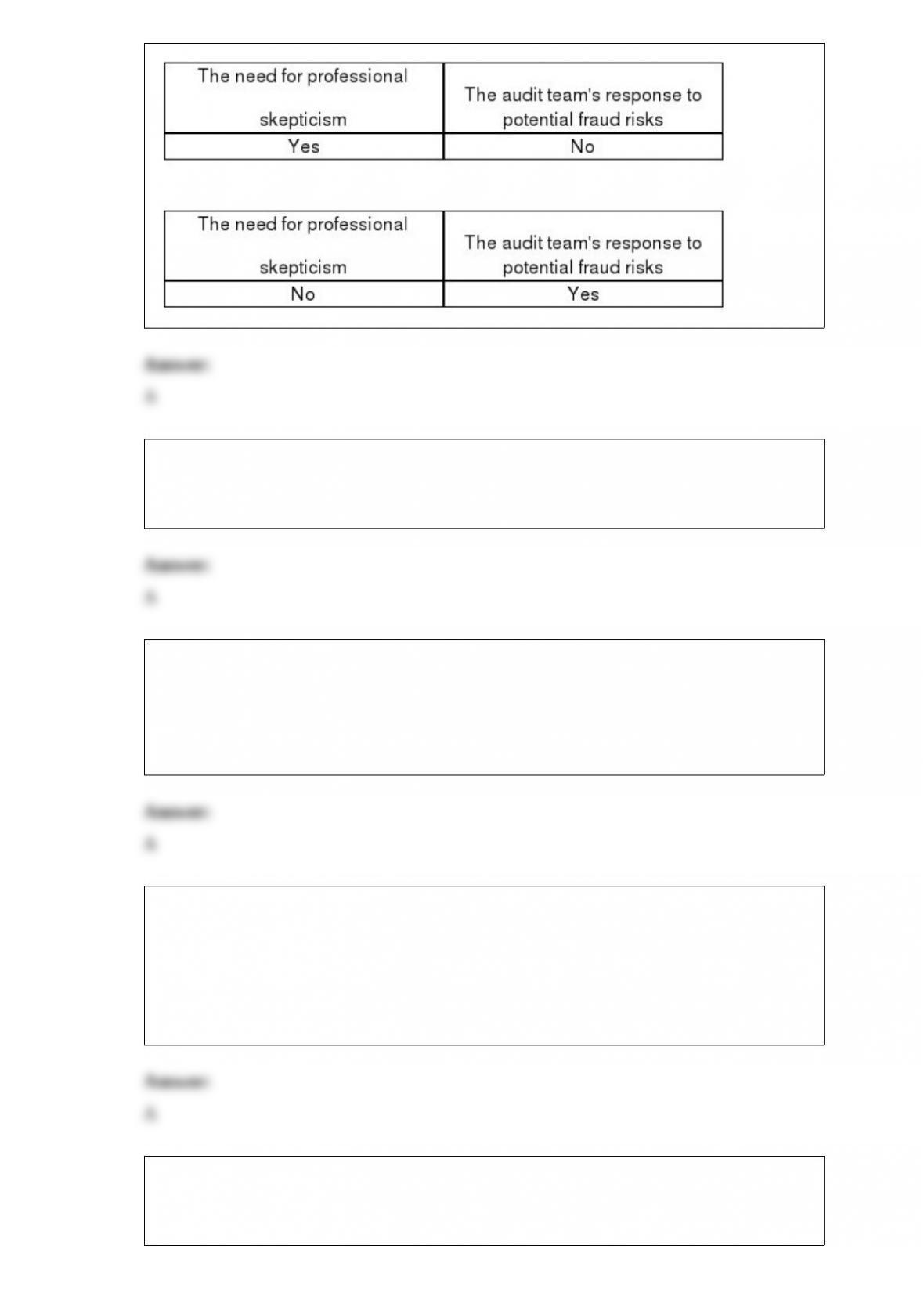

4) As part of the brainstorming sessions, auditors are directed to emphasize:

A)

B)

C)

D)

5) Analytical procedures are the least costly type of audit test.

A) True

B) False

6) Auditors are likely to prepare a proof of cash when the client has:

A) material control weaknesses in cash receipts and cash disbursements

B) material control weaknesses in accounts receivable and revenue

C) material control weaknesses in accounts payable and inventory

D) material control weaknesses in payroll

7) Which of the following is least likely to cause uncertainty about the ability of an

entity to continue as a going concern?

A) A potential lawasuit against the entity for a patent infringement

B) Loss of major customers

C) Significant recurring operating losses

D) Working capital deficiencies

8) If internal controls over cash-related transactions are adequate, the auditor is justified

in reducing the audit tests for the year-end bank reconciliation.

A) True

B) False

9) Which of the following statements is true of a public company’s financial statements?

A) Sarbanes-Oxley requires the CEO only to certify the financial statements

B) Sarbanes-Oxley requires the CFO only to certify the financial statements

C) Sarbanes-Oxley requires the CEO and CFO to certify the financial statements

D) Sarbanes-Oxley neither requires the CEO nor the CFO to certify the financial

statements

10) Which of the following statements is correct?

A) Bank personnel are responsible for providing reasonable assurance that a response to

a bank confirmation is accurate

B) Bank personnel are responsible for providing complete assurance that a bank

confirmation is complete

C) Bank personnel are not responsible for searching their records for bank balances or

loans beyond those included on the bank confirmation

D) Bank personnel are not responsible for providing information related to interest on

the bank confirmation

11) Which of the following best describes the purpose of control activities?

A) the actions, policies and procedures that reflect the overall attitudes of management

B) the identification and analysis of risks relevant to the preparation of financial

statements

C) the policies and procedures that help ensure that necessary actions are taken to

address risks to the achievement of the entity’s objectives

D) activities that deal with the ongoing assessment of the quality of internal control by

management

12) A database management system:

A) allows clients to create databases that include information that can be shared across

multiple applications

B) stores data on different files for different purposes, but always knows where they are

and how to retrieve them

C) allows quick retrieval of data, but at a cost of inefficient use of file space

D) allows quick retrieval of data, but it needs to update files continually

13) When the auditor uses tracing as an audit procedure for tests of transactions she is

primarily concerned with which audit objective?

A) Occurrence

B) Completeness

C) Cutoff

D) Classification

14) Cutoff procedures for inventory purchased should be designed by companies to

assure the company that:

A) inventory owned by the company has been received

B) inventory included in the year end inventory count has been paid

C) inventory received before year end was recorded before year end

D) inventory was correctly valued at year end

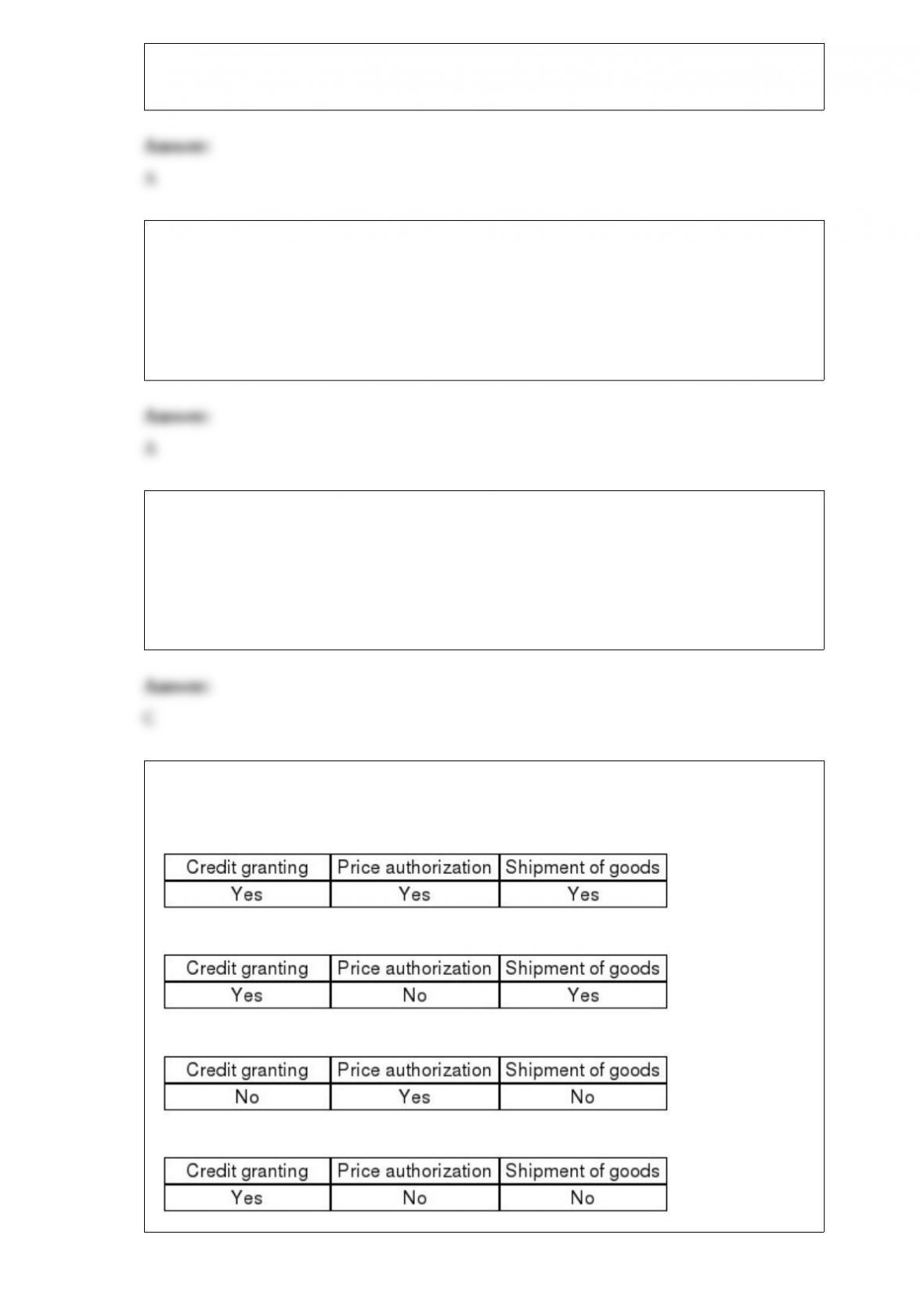

15) Which of the following is the appropriate point at which the auditor deems

authorization to be critical?

A)

B)

C)

D)

16) A CPA sole practitioner purchased stock in a client corporation and placed it in a

trust as an educational fund for the CPA’s minor child. The trust securities were not

material to the CPA but were material to the child’s personal net worth. Would the

independence of the CPA be considered to be impaired with respect to the client?

A) Yes, because the stock is a direct financial interest

B) Yes, because the stock is an indirect financial interest that is material to the CPA’s

child

C) No, because the CPA does not have a direct financial interest in the client

D) No, because the CPA does not have a material indirect financial interest in the client

17) An adverse opinion is issued when the auditor believes:

A) some parts of the financial statements are materially misstated or misleading. The

financial statements would be found to be materially misstated if an investigation were

performed

B) the financial statements would be found to be materially misstated if an investigation

were performed

C) the auditor is not independent

D) the overall financial statements are so materially misstated that they do not present

fairly the financial position or results of operations and cash flows in conformity with

GAAP

18) Which of the following includes all payroll transactions processed by the

accounting system for a given period of time?

A) payroll journal

B) payroll transaction file

C) time report

D) payroll summary

19) An auditor is gathering evidence on the completeness assertion. To do so she

performs a test to verify that all goods received by the company have been recorded

properly. The document population for this test would consist of all:

A) Vendor Invoices

B) Purchase Orders

C) Receiving Reports

D) Cash Disbursements for Accounts Payables

20) Significant deficiencies and material weaknesses in internal control of a public

company must be reported in writing to which of the following?

A) the Public Company Accounting Oversight Board

B) members of management who are responsible for the related area of the company

C) audit committee of the company’s board of directors

D) the

21) The test of details of balance procedure which requires the auditor to account for

unused inventory tag numbers to make sure none have been deleted is associated with

the audit objective of:

A) accuracy

B) existence

C) detail tie-in

D) completeness

22) Which of the following documents is best for verifying the correct balance in

accounts payable?

A) Bills of lading

B) Confirmations

C) Vendors’ invoices

D) Vendors’ statements

23) Which of the following is not a category of inquiry used by auditors?

A) Assessment inquiry

B) Declarative inquiry

C) Interrogative inquiry

D) Informational inquiry

24) “Auditing around the computer” is acceptable only if the auditor has access to the

client’s data in a machine-readable language.

A) True

B) False

25) Which of the following statements best expresses the impact that the performance

of audit procedures has on statistical vs. nonstatistical sampling?

A) Audit procedures on the sample item will vary as a result of using either statistical or

nonstatistical sampling

B) The audit procedures will be the same for either statistical or nonstatistical sampling

but they must be performed differently for each

C) Statistical sampling requires quantitative audit procedures, whereas nonstatistical

sampling requires judgmental audit procedures

D) Audit procedures on the sample item will not vary as a result of using either

statistical or nonstatistical sampling

26) Logic tests and completeness tests are examples of application controls.

A) True

B) False

27) Sales should be recorded, at the earliest, when:

A) the order is received

B) the order is received and credit is approved

C) credit is approved and it is verified that there is enough inventory to fill the order

D) the shipment takes place

28) The introductory paragraph of the auditor’s report states that the auditor is

responsible for the preparation, presentation and opinion on financial statements.

A) True

B) False

29) Match seven of the terms (a-p) with the description/definitions provided below

(1-7):

a.Commitments

b.Completing the engagement checklist

c.Contingent liability

d.Dual-dated audit report

e.Financial statement disclosure checklist

f.Independent review

g.Inquiry of client’s attorneys

h.Letter of representation

i.Other information in annual reports

j.Review for subsequent events

k.Subsequent events

l.Unadjusted misstatement worksheet

m.Management letter

n.Pending claim

o.Unasserted claim

p.Audit documentation review

________ 1> A review of the financial statements and the entire set of audit files by an

independent reviewer to whom the audit team must justify the evidence accumulated

and the conclusions reached.

________ 2> A potential future obligation to an outside party for an unknown amount

resulting from activities that have already taken place.

________ 3> A written communication from the client to the auditor formalizing

statements that the client has made about matters pertinent to the audit.

________ 4> A potential legal claim against a client where the condition for a claim

exists but no claim has been filed.

________ 5> Transactions that occurred after the balance sheet date, which affect the

fair presentation or disclosure of the statements being audited.

________ 6> Agreements that the entity will hold to a fixed set of conditions, such as

the purchase or sale of merchandise at a stated price.

________ 7> The use of one audit report date for normal subsequent events and a later

date for one or more subsequent events.

30) The objectives of internal auditors are considerably broader than the objectives of

external auditors.

A) True

B) False

31) As control risk increases, the amount of substantive evidence the auditor plans to

accumulate should increase.

A) True

B) False

32) Assurance provided by a review is substantially less than an audit. Which of the

following statements is true regarding these services?

A) A review requires more substantive evidence than an audit

B) An audit requires less evidence related to internal control than a review

C) A review requires less evidence than an audit

D) None of the above statements is true

33) The balance-related audit objective realizable value is not applicable when auditing

notes payable.

A) True

B) False

34) Confirmation of accounts receivable provide evidence related to the existence,

accuracy and cutoff objectives.

A) True

B) False

35) The auditor has a responsibility to review transactions and activities occurring after

the year-end to determine whether anything occurred that might affect the statements

being audited. The procedures required to verify these transactions are commonly

referred to as the review for:

A) contingent liabilities

B) subsequent year’s transactions

C) late unusual occurrences

D) subsequent events

36) The Sarbanes-Oxley Act of 2002 makes it felony to destroy or create documents to

impede or obstruct a federal investigation. Those provisions were adopted following

which of the following legal cases?

A) United States v. Natelli

B) United States v. Andersen

C) ESM Government Securities v. Alexander Grant & Co

D) United States v. Simon

37) On the last day of the fiscal year, the cash disbursements clerk drew a company

check on bank A and deposited the check in the company account in bank B to cover a

previous theft of cash. The disbursement has not been recorded. The auditor will best

detect this form of kiting by:

A) examining the composition of deposits in both bank A and bank B subsequent to

year-end

B) examining paid checks returned with the bank statement of the next account period

after year-end

C) preparing, from the cash disbursements records, a summary of bank transfers for one

week prior to and subsequent to year-end

D) comparing the detail of cash receipts as shown by the client’s cash receipts records

with the detail on the confirmed duplicate deposit tickets for three days prior to and

subsequent to year-end

38) Which one of the following is more difficult to evaluate objectively?

A) Presentation of financial statements in accordance with generally accepted

accounting principles

B) Compliance with government regulations

C) Efficiency and effectiveness of operations

D) All three of the above are equally difficult

39) Which of the following is a significant risk to the auditor regarding an audit in a

highly automated information environment?

A) does not place enough reliance on the processed information

B) places too much reliance on the processed information

C) processed information may not reveal the sources of the information

D) does not understand the processed information produced by the automated

environment

40) IT has several significant effects on an organization. Which of the following would

not be important from an auditing perspective?

A) organizational changes

B) the visibility of information

C) the potential for material misstatement

D) None of the above; i.e., they are all important

41) Describe the auditor’s responsibilities related to required communications between

the auditor and those charged with governance (remove auditor committee) regarding

internal control.

42) Bank reconciliation audit tests are designed to detect misstatements other than

through the improper payment of cash or failure to receive cash normally would not be

detected as part of the tests of the bank reconciliation. List below at least THREE

misstatements that are designed to be detected by bank reconciliation.

43) One category of general controls is physical and online security. Describe the

control and give at least three examples of implementation of the control.

44) CPAs can be held liable for criminal activity under both state and federal laws.

Infamous cases have involved United States vs. Natelli and ESM Government

Securities v. Alexander Grant and Co. Discuss what occurred and prepare a summary of

the court findings.

45) What are three specific risks to IT systems?

46) Discuss the advantages and benefits of using generalized audit software.

47) Briefly describe a SysTrust engagement.