The calculation of future value requires the removal of interest.

Expenditures currently deducted in the tax return but not included with expenses in the

income statement until subsequent years create deferred tax liabilities.

The primary motivation behind the lower of cost and net realizable value rule is

consistency.

Revenues are inflows or other enhancements of assets or settlements of liabilities from

activities that constitute the entity’s ongoing operations.

International Financial Reporting Standards require a company to classify expenses in

an income statement by function.

Assume that the scales, software and calibration service are viewed as one performance

obligation. How much revenue will Ortiz recognize in 2016 for this contract?

On July 15, 2016, Ortiz & Co. signed a contract to provide EverFresh Bakery with an

ingredient-weighing system for a price of $90,000. The system included finely tuned

scales that fit into EverFresh’s automated assembly line, Ortiz’s proprietary software

modified to allow the weighing sytem to function in EverFresh’s automated system, and

a one-year contract to calibrate the equipment and software on an as-needed basis.

(Ortiz competes with other vendors who offer ongoing calibration contracts for Ortiz’s

systems.) If Ortiz was to provide these goods and services separately, it would charge

$60,000 for the scales, $10,000 for the software, and $30,000 for the calibration

contract. Ortiz delivered and installed the equipment and software on August 1, 2016,

and the calibration service commenced on that date. a. $0

b. $37,500

c. $63,000

d. $90,000

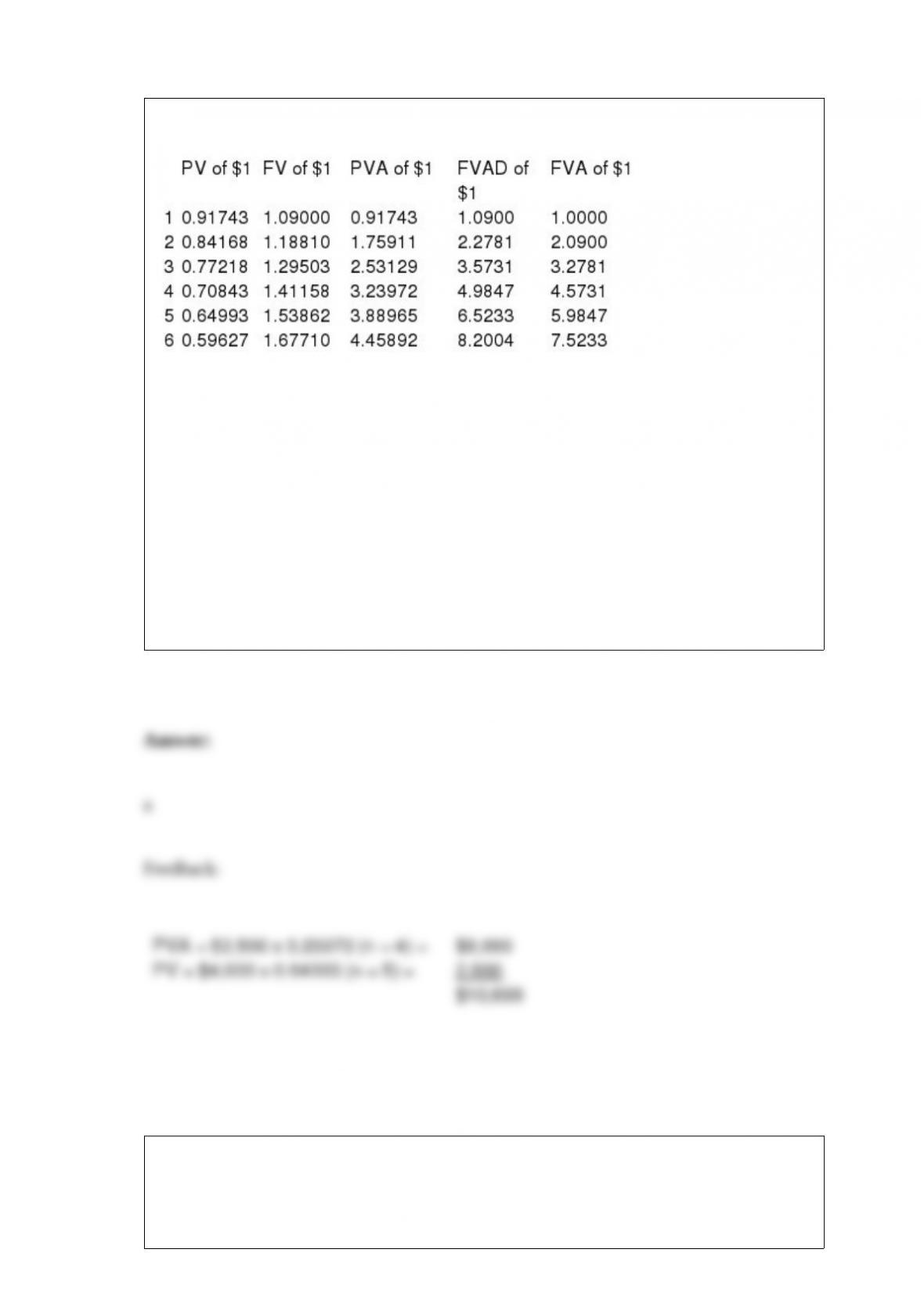

Present and future value tables of 1 at 9% are presented below.

Mustard’s Inc. sold the rights to use one of its patented processes that will result in cash

receipts of $2,500 at the end of each of the next four years and a lump sum receipt of

$4,000 at the end of the fifth year. The total present value of these payments if interest

is at 9% is:

a. $10,699.

b. $11,468.

c. $12,100.

d. $14,000.

Which of the following is true about reporting cash under IFRS?

a. Cash accounts include loans made to customers, but not to related parties.

b. Overdrafts typically cannot be offset against positive balance in other cash accounts

on the balance sheet.

c. Cash overdrafts are not allowed.

d. Overdrafts typically are not shown as current liabilities on the balance sheet.

Flapper Jack’s Pancake Restaurants Inc. sells franchises for an initial fee of $36,000

plus operating fees of $500 per month. The initial fee covers site selection, training,

computer and accounting software, and on-site consulting and troubleshooting, as

needed, over the first five years. On March 15, 2015, Tim Cruise signed a franchise

contract, paying the standard $6,000 down with the balance due over five years with

interest.

Assume at March 15, 2015, the time of signing the contract, collection of the receivable

was reasonably assured and there were no significant continuing obligations. The

journal entry at signing would include a:

a. Credit to franchise fee revenue for $36,000.

b. Credit to franchise fee revenue for $9,000.

c. Credit to unearned franchise fee revenue for $36,000.

d. Credit to unearned franchise fee revenue for $27,000.

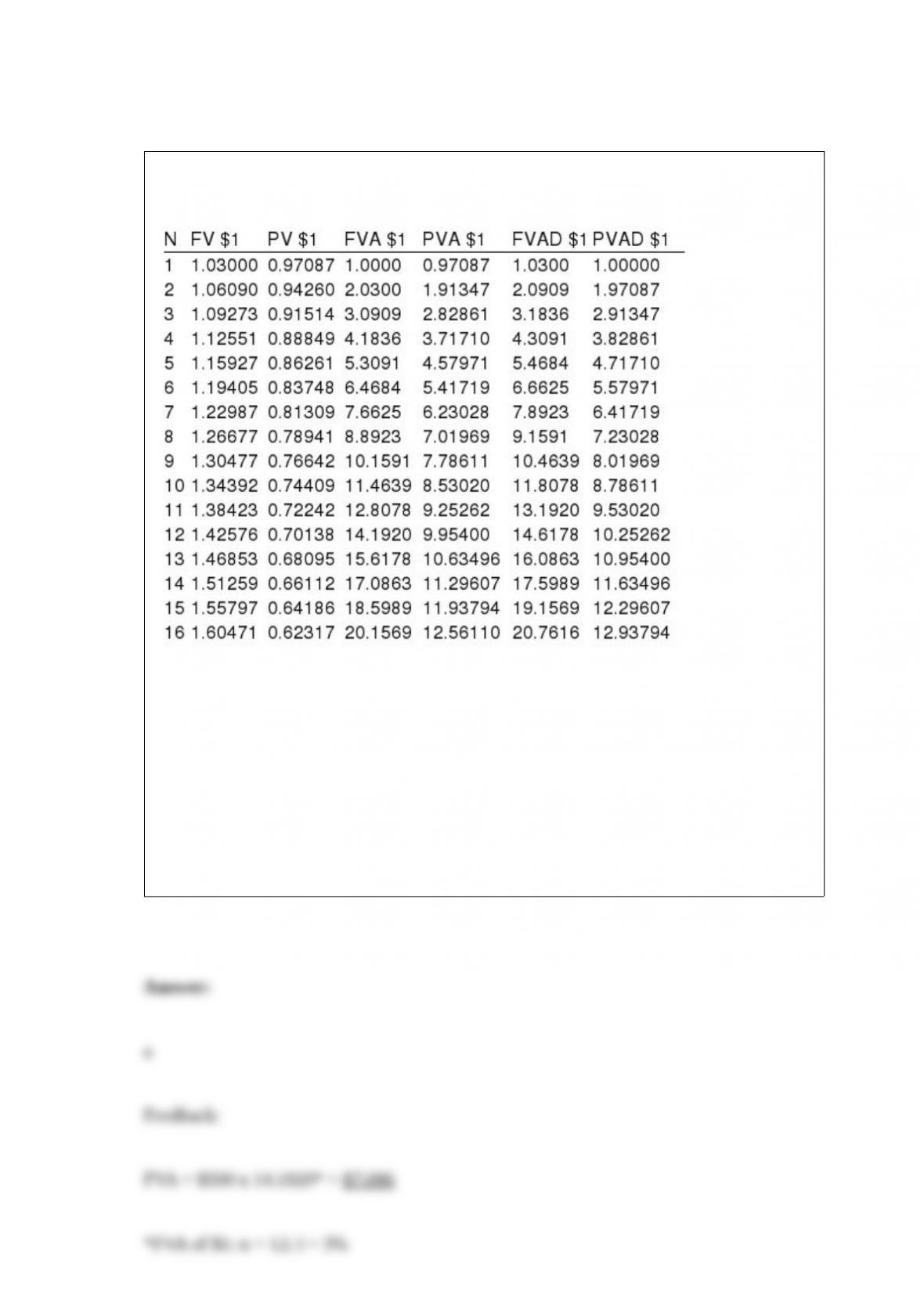

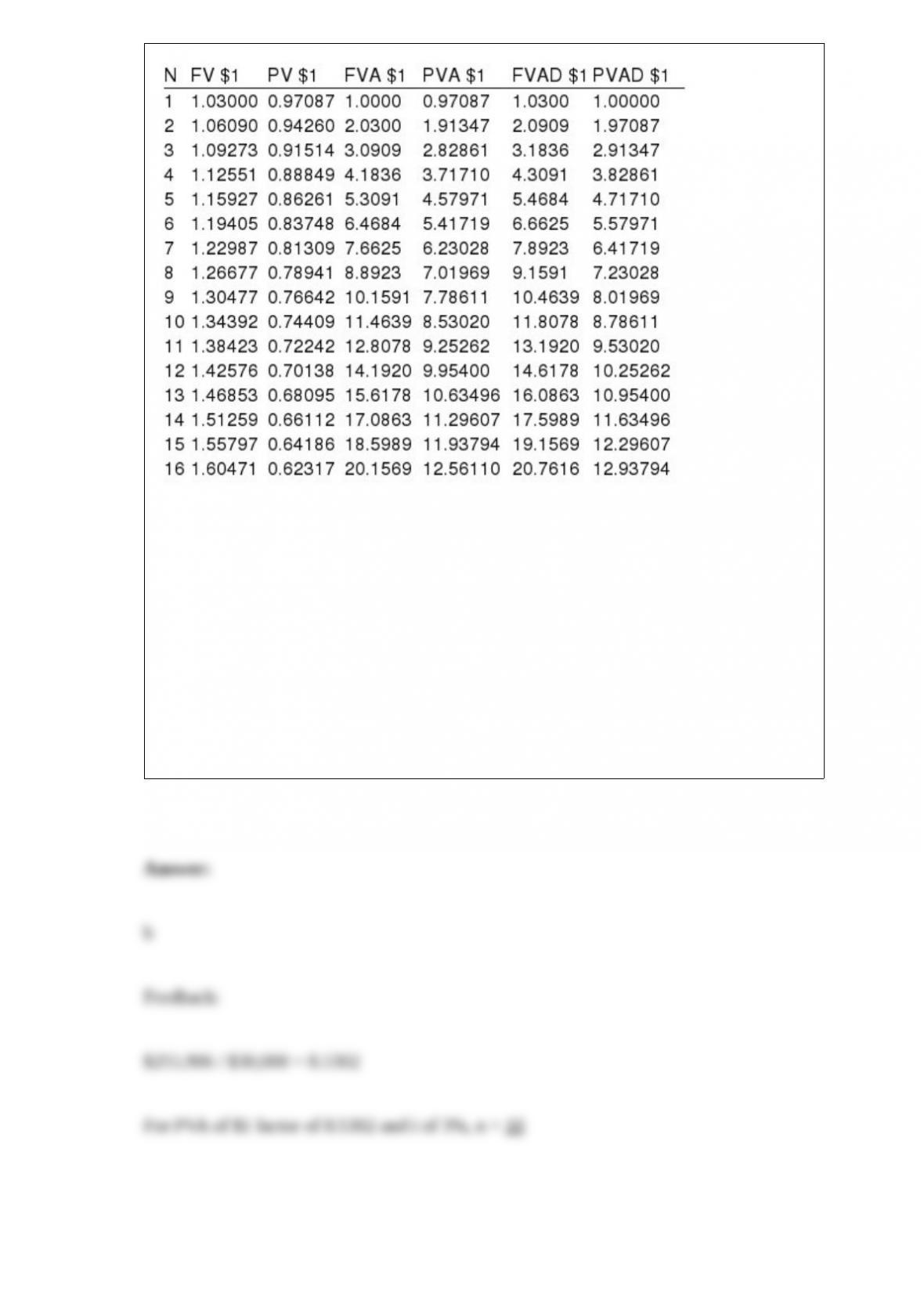

Present and future value tables of $1 at 3% are presented below:

At the end of each quarter, Patti deposits $500 into an account that pays 12% interest

compounded quarterly. How much will Patti have in the account in three years?

a. $7,096.

b. $7,213.

c. $7,129.

d. $8,880.

External decision makers would not look primarily to financial accounting information

to assist them in making decisions on:

a. Granting credit.

b. Capital budgeting.

c. Selecting stocks.

d. Mergers and acquisitions.

The Maytag Corporation’s income statement includes income from continuing

operations and a loss on discontinued operations. Earnings per share information would

be provided for:

a. Net income only.

b. Income from continuing operations and net income only.

c. Income from continuing operations, loss on discontinued operations, and net income

only.

d. None of the other answers is correct.

The replacement of a major component increased the productive capacity of production

equipment from 10 units per hour to 18 units per hour. The expenditure should be

debited to:

a. Repairs.

b. Equipment.

c. Maintenance.

d. Gain from repairs.

Under IFRS No. 9, which is not a category for accounting for investments?

a. Fair value through profit and loss.

b. Fair value through other comprehensive income.

c. Held-to-maturity.

d. Amortized cost.

When a capital lease is first recorded at the inception of the lease, the lessee typically

debits:

a. Leased asset.

b. Rent expense.

c. Lease expense.

d. Lease receivable.

Amortizing a net loss for pensions will:

a. Increase retained earnings and increase accumulated other comprehensive income.

b. Decrease retained earnings and decrease accumulated other comprehensive income.

c. Increase retained earnings and decrease accumulated other comprehensive income.

d. Decrease retained earnings and increase accumulated other comprehensive income.

On April 31, 2016, Elkhorn Associates borrowed $10 million cash from Colonial Bank

and issued a 5-month, noninterest-bearing note, priced to yield an effective interest rate

of 10%. The stated discount rate on this loan is:

a. More than the effective interest rate.

b. Less than the effective interest rate.

c. Equal to the effective interest rate.

d. Unrelated to the effective interest rate.

If the lessee expects to obtain title to leased property due to a bargain purchase option

or passage of title at the end of the lease term:

a. The lessee ignores any residual value for the leased property.

b. The lessor ignores any residual value for the leased property.

c. The lessee adds the present value of the residual value to the amount recorded for the

lease.

d. The lessor will always charge a higher annual lease rate.

Present and future value tables of $1 at 3% are presented below:

Jimmy has $255,906 accumulated in a 401K plan. The fund is earning a low, but safe,

3% per year. The withdrawals will take place at the end of each year starting a year

from now. How soon will the fund be exhausted if Jimmy withdraws $30,000 each

year?

a. 11 years.

b. 10 years.

c. 8.5 years.

d. 8.8 years.

A simple capital structure might include:

a. Stock rights.

b. Convertible bonds.

c. Nonconvertible preferred stock.

d. Stock purchase warrants.

Preferred dividends would not be subtracted from earnings when computing basic

earnings per share in a year when the dividends are not declared if the preferred stock

is:

a. Noncumulative.

b. Convertible.

c. Participating.

d. Cumulative.

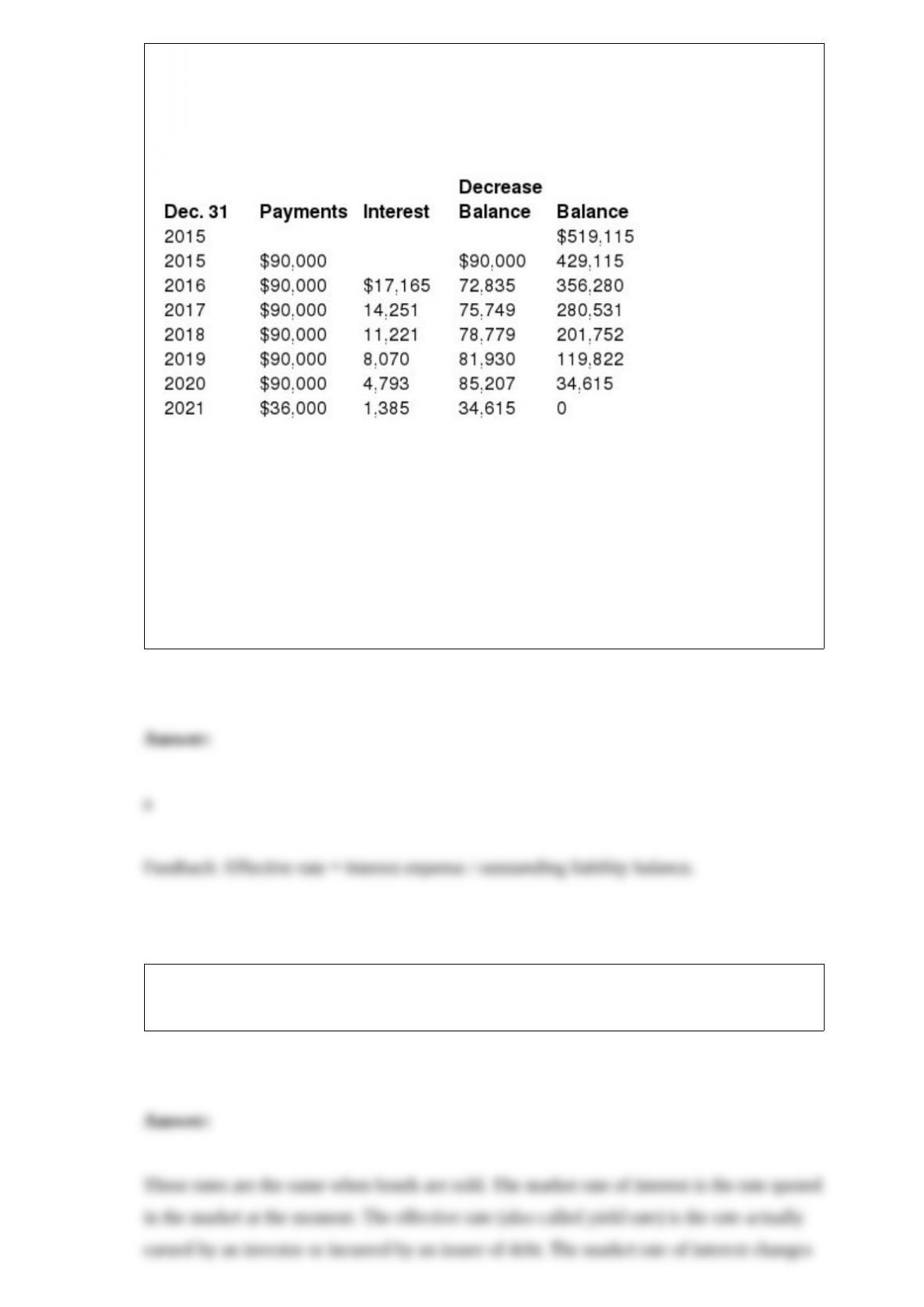

On December 31, 2015, Reagan Inc. signed a lease for some equipment having a

nine-year useful life with Silver Leasing Co. The lease payments are made by Reagan

annually, beginning at signing date. Title does not transfer to the lessee, so the

equipment will be returned to the lessor on December 31, 2021. There is no bargain

purchase option, and Reagan guarantees a residual value to the lessor on termination of

the lease.

Reagan’s lease amortization schedule appears below:

What is the effective annual interest rate charged to Reagan on this lease?

a. 4%.

b. 6%.

c. 8%.

d. 17%.

What is meant by the “market rate” of interest, the “effective rate” of interest, and the

“yield rate” of interest?

CompuValue Center sells a full assortment of computer parts, including motherboards,

video cards, and cables, and also offers complementary computer assembly services.

CompuValue estimates that it incurs $50 in labor and materials on average to complete

one assembly order, with an average of 75% profit based on cost. Required: Assuming

that computer parts and assembly service are separate performance obligations, estimate

the stand-alone selling price of the assembly service based on the expected cost plus

margin approach.

What activities are included in the statement of cash flows under the section titled

“Cash flows from investing activities”?

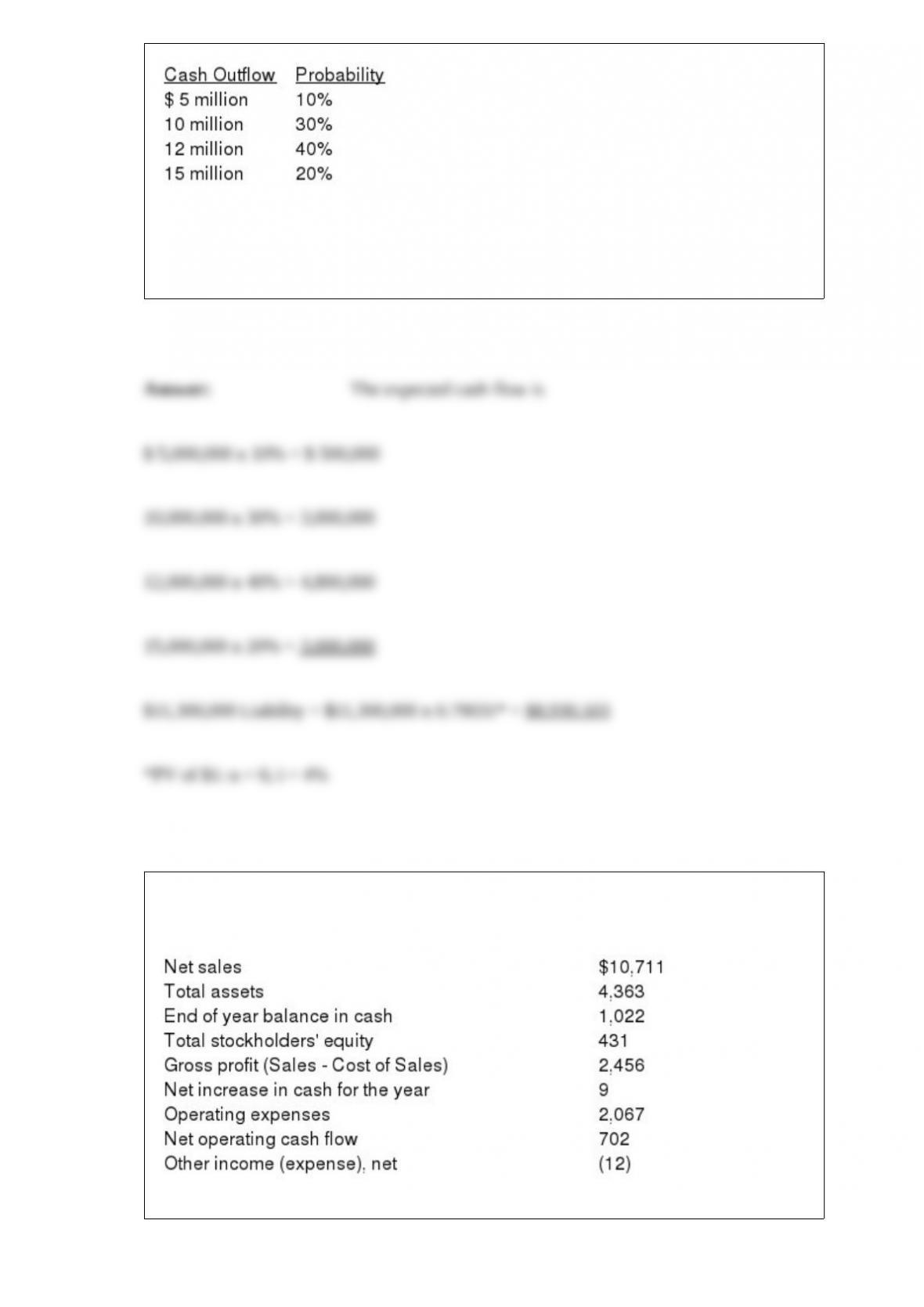

Jackpot Mining is obligated to the State of California to restore leased land to its

original condition after its mining activities are over in six years. The cash flow

possibilities and probabilities for the restoration costs in six years are as follows:

The company’s credit-adjusted risk-free interest rate is 4%. Required:

Calculate the liability that Jackpot must record at the beginning of the project for the

restoration costs.

The following information ($ in millions) comes from a recent annual report of

Amazon.com, Inc.:

Compute Amazon’s cost of goods sold for the year.

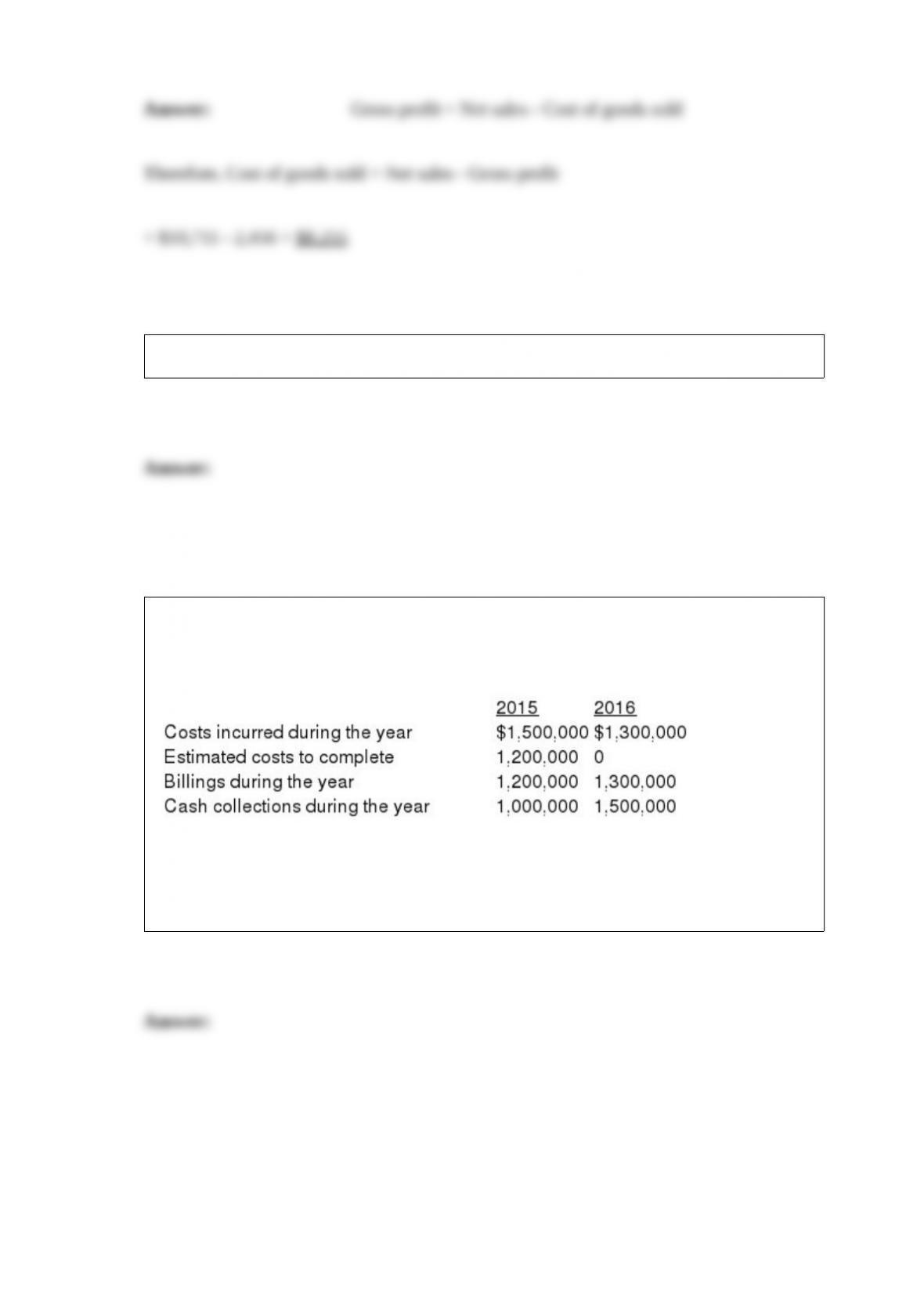

McCombs Contractors received a contract to construct a mental health facility for

$2,500,000. Construction was begun in 2015 and completed in 2016. Cost and other

data are presented below:

Assume that McCombs recognizes revenue upon project completion.

Required: Compute the amount of gross profit recognized by McCombs during 2015

and 2016.

Fredo, Inc., purchased 10% of Sonny Enterprises for $1,000,000 on January 1, 2016.

Sonny recognized a total of $400,000 net income during 2016, paid $30,000 of

dividends to Fredo during 2016, and at December 31, 2016, the market value of the

Sonny investment increased to $1,040,000.

Required: Prepare the journal entries necessary to account for the Sonny investment,

assuming that Fredo accounts for that investment as (1) an available-for-sale

investment, and (2) elects the fair-value option.

On June 30, 2014, Mobley Corporation acquired a patent for $4 million. The patent was

estimated to have an eight-year life and no residual value. Mobley uses the straight-line

method of amortization for intangible assets. At the beginning of January 2016, Mobley

successfully defended its patent against infringement. Litigation costs totaled $650,000.

Required:

1> Calculate patent amortization for 2014 and 2015.

2> Prepare the journal entry to record the 2016 litigation costs.

3> Calculate amortization for 2016.

4> Repeat requirements 2 and 3 assuming that Mobley prepares its financial statements

according to International Financial Reporting Standards (IFRS).

Casper Chemical recently acquired a building located on two acres of land for a

lump-sum price of $3.2 million. In your job as assistant controller, you determined the

allocation of the price using the relative fair values to be $1 million and $2.2 million for

the land and building, respectively. When you reported these initial values to Jake

Reese, the company’s controller, he told you to change the allocation to $1.5 million for

the land and $1.7 million for the building. When you asked him why the change, he

explained that the company is having a difficult time meeting profitability goals and

that his proposed allocation will help the bottom line for future years.Required:

1> How will the controller’s proposed allocation help the bottom line in future years?

2> Discuss the ethical dilemma faced by the assistant controller.