Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term

1> _____ Time-Series Analysis

2> _____ Common-Size Financial Statements

3> _____ Management Discussion and Analysis

4> _____ Price/Earnings Ratio

5> _____ Earnings Per Share

6> _____ Comprehensive Income

7> _____ Discontinued Operations

8> _____ Net Income

Definition

A) The practice of reporting accounting data in the national monetary unit.

B) A nonrecurring item associated with abandoning or selling an operation.

C) The earnings of a company after taxes.

D) An increase in an asset or a decrease in a liability that results from peripheral

activities.

E) After-tax earnings adjusted for gains and losses that may disappear before they are

realized.

F) A section of the annual report that can be used in interpreting the results of financial

statement analysis.

G) The ratio calculated by dividing the net income by the number of common shares

outstanding.

H) The ratio calculated by dividing the price of a share of stock by the earnings per

share.

I) Also known as ratio analysis.

J) A nonrecurring item on the income statement that reflects gains and losses associated

with extraordinary events.

K) Another name for a trend analysis.

L) The practice of reporting information in percentages rather than monetary amounts.

When the petty cash fund is replenished:A) Cash is debited.B) Petty Cash is credited.C)

Petty Cash is debited.D) Appropriate expense accounts are debited.

A company uses a weighted-average perpetual inventory system. The following

transactions took place during the month of August:

What is the per-unit value of ending inventory on August 31?(Round each per unit cost

to two decimal points.)

A) $12.00

B) $13.80

C) $15.42

D) $16.00

E) $17.74

If no errors have been made, when a company prepares its adjusted trial balance:

A) assets will equal liabilities plus Retained Earnings.

B) stockholders’ equity will include the current period’s net income.

C) the debit column and the credit column will be equal.

D) income statement accounts will have been closed.

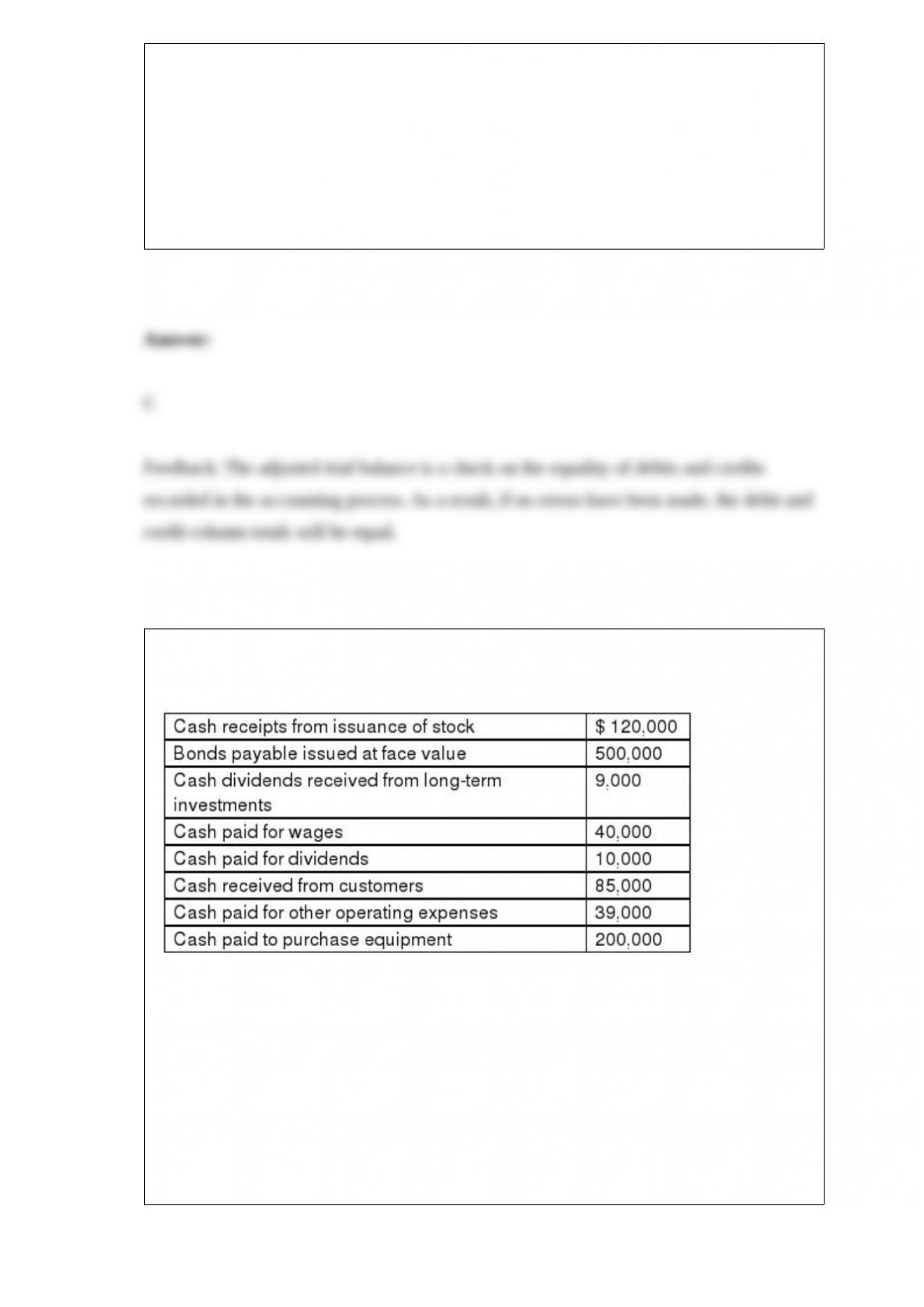

Flynn Corporation had the following cash flows for the current year. The company uses

the direct method in preparing the statement of cash flows.

Use the information above to answer the following question. What is the net cash

provided by (used in) investing activities?

A) ($200,000)

B) $420,000

C) $410,000

D) ($190,000)

Which of the following is a correct statement about the nature of equipment?

A) While equipment is an asset, its use is recorded as an expense.

B) While equipment is an asset, its use is recorded as a liability.

C) While equipment is an asset; its use is recorded as affects Common Stock.

D) Equipment and its use both affect liabilities.

Using the indirect method, which of the following would be added to net income?

A) A decrease in Supplies

B) An increase in Prepaid Insurance

C) A decrease in Salaries and Wages Payable

D) An increase in Equipment

Oklahoma Company has a fiscal year ending on December 31, 2015. The following

information has been gathered so that the company could prepare adjustments:

A) The company had $4,000 of office supplies on hand on January 1, 2015, purchased

$6,300 of supplies during the year, and had $1,200 of supplies were on hand on

December 31, 2015.

B) On October 1, 2015, a three-year insurance premium of $27,000 was paid for

coverage beginning on that date. The payment was recorded in the Prepaid Insurance

account.

C) A delivery vehicle was purchased for $30,000 on April 1, 2015. The vehicle has a

5-year useful life and no salvage value. Depreciation is estimated to be $6,000 per year

or $500 per month.

D) The company rents some of its unused factory space to a small manufacturer. The

lease required an advance payment of $18,000 for six months’ rent on November 1,

2015, and the lease term began that day. The advance payment received from the tenant

was recorded as Unearned Revenue when it was received.

E) Employees work five days per week and are paid $75,000 every other Friday; each

pay period includes ten week days. The last payday during the company’s fiscal year

was properly recorded on Friday, December 26, 2015. The employees worked on

December 29, 30, and 31, 2015; they will not be paid for that work until Friday, January

9, 2016.

F) The Accounting Department sends bills to customers every Friday and records the

revenue earned at that time. Customers were billed and the related revenue was

properly recorded on Friday, December 26, 2015. Since then, services were performed

on December 29, 30, and 31, 2015; those services totaled $29,000. This amount has not

been recorded.

Required:

Prepare the adjusting entry that is required for each of the situations described above.

Assume that you are adjusting the related accounts as of the end of the year and that no

adjustments have been made since the dates provided above.

What of the following statements about Accumulated Other Comprehensive Income

(Loss) is not correct?

A) Accumulated Other Comprehensive Income (Loss) reports unrealized gains and

losses, which are temporary changes in the value of certain assets and liabilities the

company holds.

B) Accumulated Other Comprehensive Income (Loss) can relate to pensions, foreign

currencies, and financial investments.

C) Accumulated Other Comprehensive Income (Loss) is a component of stockholders’

equity.

D) Accumulated Other Comprehensive Income (Loss) is reported on the income

statement.

Which of the following statements concerning electronic funds transfers is not correct?

A) Businesses sometimes receive payments from customers via EFT.

B) An EFT occurs when a customer electronically transfers funds from his or her bank

account to the company ‘s bank account.

C) Because electronic funds transfers are deposited directly into the company ‘s bank

account, they require additional internal control procedures.

D) To process an EFT, the accounting department merely records journal entries to

debit Cash and credit Account Receivable from each customer.

Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term

1> _____ Accrued liability

2> _____ Loan covenant

3> _____ Issue price

4> _____ Face value

5> _____ Line of credit

6> _____ Public debt offering

7> _____ Security

8> _____ Contingent liability

9> _____ Debt-to-assets ratio

Definition

A. Bond features that allow the issuer to repay the loan early.

B. A prearranged agreement that allows a company to borrow at will up to a limit.

C. This item is reported as a contra asset account.

D. The amount that the lender actually pays for a bond.

E. The cost of issuing a bond.

F. Debt features that, if violated, allow the lender to revise loan terms.

G. The total amount of money that a company owes in debt.

H. The amount a company must repay creditors when a bond matures.

I. These are liabilities that have been incurred during the period but not yet paid.

J. When a company borrows money by issuing bonds in the financial markets.

K. A bond feature that allows a creditor to seize assets if debt is not properly repaid.

L. This type of liability is uncertain; it exists only if some other condition occurs.

M. Total liabilities divided by total assets.

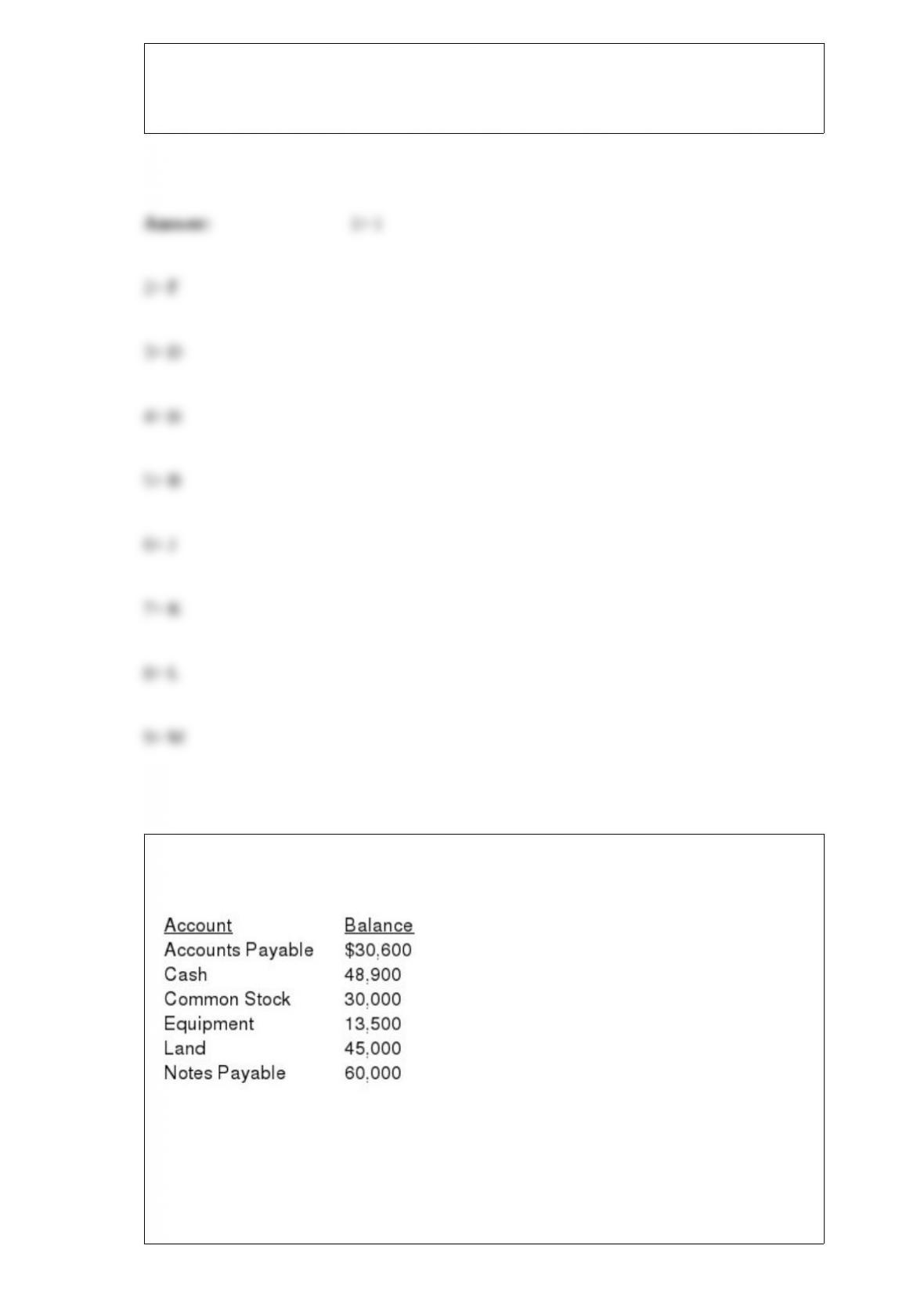

The following account balances were listed on the trial balance of Edgar Company at

the end of the period:

The company ‘s trial balance is not in balance and the company ‘s accountant has

determined that the error is in the cash account. What is the correct balance in the cash

account?

A) $57,900.

B) $31,500.

C) $2,100.

D) $62,100.

The Accounts Payable account:

A) has a normal credit balance.

B) is increased by a debit.

C) is an asset.

D) is increased when a company receives cash from customers.

If Insurance Expense is $7,000 and the beginning and ending balances of Prepaid

Insurance are $1,500 and $2,000, respectively, the cash paid for insurance is:

A) $7,000.

B) $6,500.

C) $5,000.

D) $7,500.

When the indirect method is used, if accounts receivable increases during the

accounting period, the change in accounts receivable is:

A) added to the change in the cash account.

B) subtracted from net income.

C) added to net income.

D) subtracted from the change in the cash account.

Beginning inventory plus purchases minus ending inventory equals:

A) net sales.

B) cost of goods sold.

C) goods available for sale.

D) net purchases.

In this period, a company recorded Sales Revenue of $50,000 from sales of goods to

customers who agreed to pay later. In the next period, the company received payment

from customers of $45,000. Which of the following statements is correct?.

A) Revenue for this period is $45,000.

B) Accounts Receivable at the end of this period is $50,000.

C) Accounts Payable at the end of this period is $5,000 (or $50,000 – $45,000).

D) Expenses for next period will increase by $5,000 (or $50,000 – $45,000).

A company purchased equipment by issuing a $200,000, one-year, 8% note payable.

The transaction would be recorded in the accounting records with a credit to Notes

Payable for:

A) $200,000.

B) $216,000.

C) $184,000.

D) $208,000.

The income statement would report the amount of:

A) cash at the end of the year.

B) supplies used up during the current year.

C) dividends distributed to owners during the current year.

D) unpaid employee wages at the end of the year.