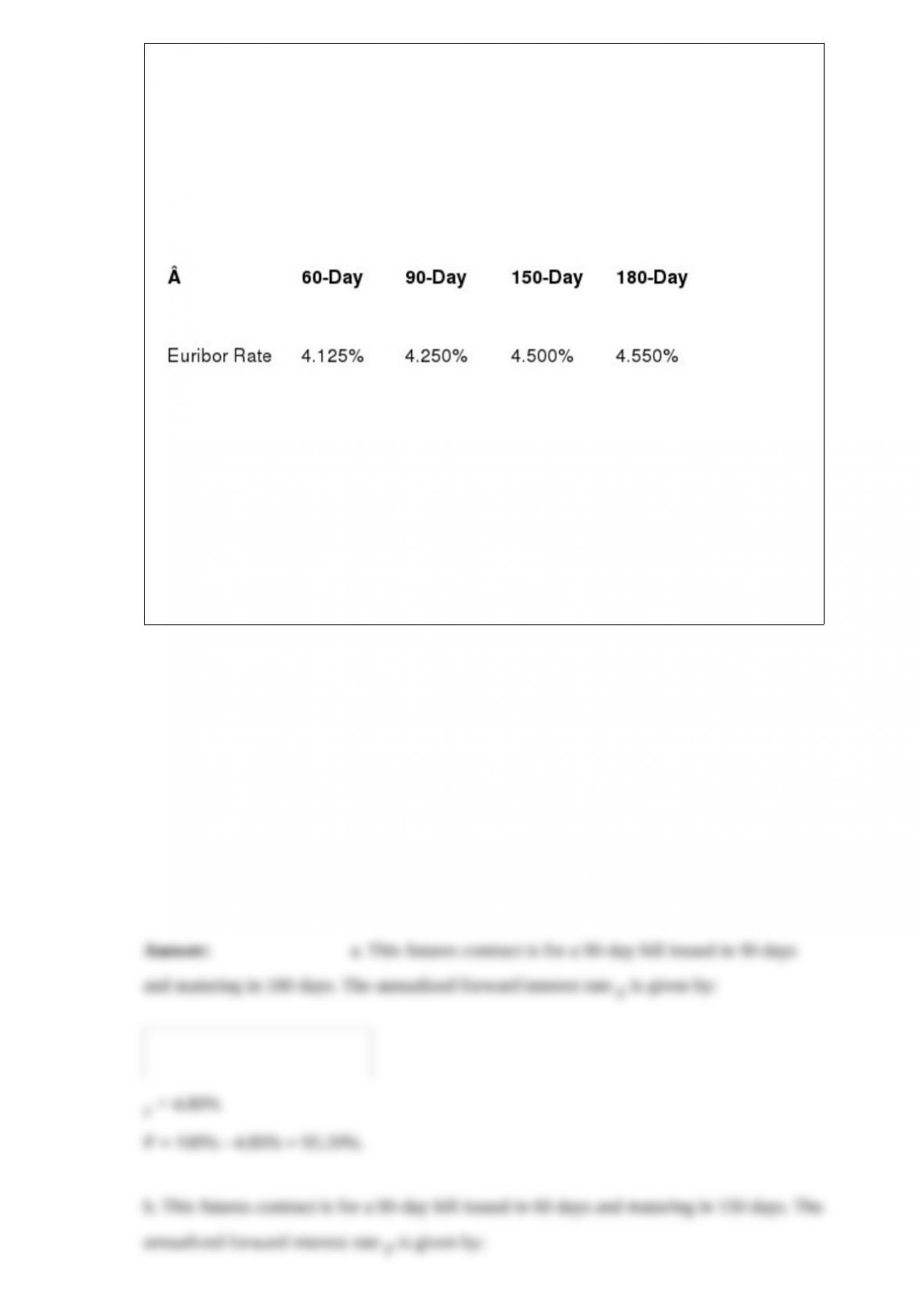

You wish to establish the theoretical futures price on a Euribor contract quoted on the

London International Financial Futures Exchange (LIFFE) in London. The futures

contract is for a 90-day Euribor rate at expiration of the futures contract. You look at the

current term structure of Euribor interest rates. Following the standard conventions for

short-term rates, all interest rates are quoted as annualized linear rates. In other words,

the interest paid for a maturity of T days is equal to the annualized rate quoted, divided

by 360 and multiplied by T. The observed rates are as follows:

a. What should be the Euribor futures price quoted today with an expiration date in

exactly

90 days?

b. What should be the Euribor futures price quoted today with an expiration date in

exactly

60 days?

Grupo Televisa S.A. is a Mexican firm listed in Mexico, with an American Depository

Receipt (ADR) traded on the NYSE. The stock prices are 300 pesos in Mexico, and 30

dollars in New York; the exchange rate is 10 pesos per dollar. Suddenly, a political

problem in Mexico leads to a depreciation of the peso and a drop of the Mexican stock

market. The new exchange rate is 11 pesos per dollar, and the new stock price of Grupo

Televisa is 275 pesos.

a. What should the price quoted in New York be?

b. Actually the stock price in New York is 20 dollars. Should you buy or sell the stock,

and why?

UBS AG is listed as an ADR on the New York Stock Exchange (NYSE) in dollars

(USD). It is also listed in Zurich in Swiss francs (CHF). Here are some quotes:

NYSE (in )

Zurich (in CHF) 187-188

CHF/$ (Swiss francs per dollar) 1.7360-1.7380

In addition, you have to pay a commission of 0.3% in New York or 0.5% in Zurich.

a. Where should you buy UBS shares if you are an American investor?

b. Where should you sell UBS shares if you are an American investor?

c. If all commissions were waived for a large transaction, would yourbe the same?

d. the same questions for a Swiss investor.

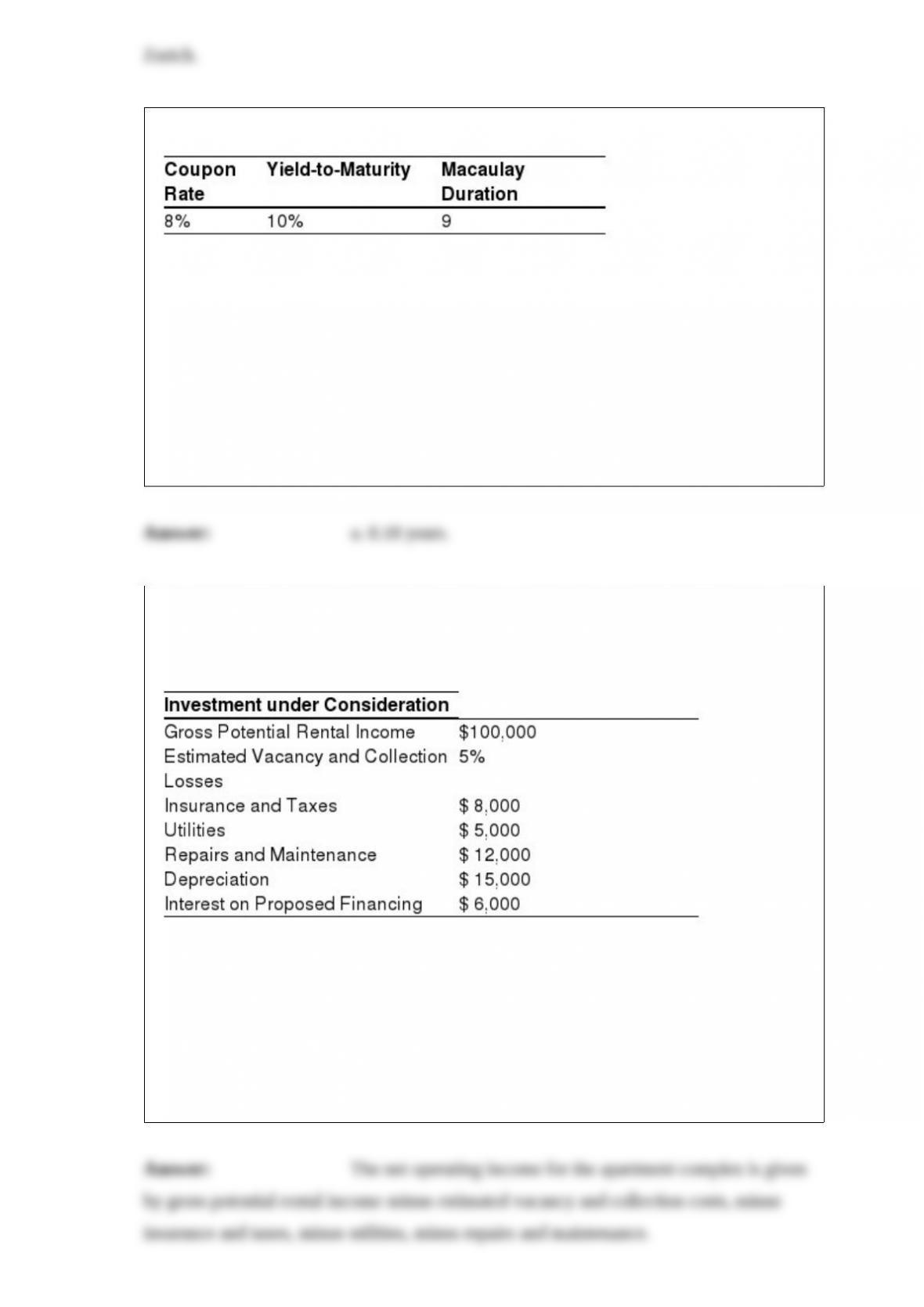

A bond with annual coupon payments has the following characteristics:

The bond’s modified duration (in years) is:

a. 8.18 years.

b. 8.33 years.

c. 9.78 years.

d. 10.00 years.

An investor estimates that investing ¬5 million in a particular venture capital project

can return

$40 million at the end of five years if it succeeds; however, she realizes that the project

may fail at any time between now and the end of the fifth year. The investor is

considering an equity investment in the project and her cost of equity for a project with

this level of risk is 15%. In the table below are the investor’s estimates of certain

probabilities of failure for the project. First, 0.30 is the probability of failure in year

one. The probability that project fails in the second year, given that it has survived

through year one, is 0.25; and so forth:

a. Determine the expected net present value of the project.

b. Recommend whether the project should be undertaken.

You hold some shares of BMW listed in Frankfurt. The share price is 750, and a gross

dividend

of 30 is paid. The current exchange rate is 1.15 . The German government

imposes a 15% withholding tax on dividends paid to U.S. investors. Your marginal tax

rate is 30%.

a. What dividend per share will you receive in U.S. dollars?

b. What tax will you have to pay to the U.S. government on the dividend received?

In 1994, the United States was experiencing a fairly strong economic recovery, ahead of

other nations. Fears of an overheating economy led to sudden inflationary fears for the

next few years.

a. Would you expect U.S. interest rates to rise or drop?

b. Would you expect the dollar to depreciate or appreciate?

c. Would you expect a foreign bond portfolio to be a good investment compared to a

U.S. dollar portfolio under this scenario?

Assume that the domestic volatility (standard deviation in yen) of the Japanese bond

market is 8%. The volatility of the yen against the U.S. dollar is 6%.

a. What would the dollar volatility of the Japanese bond market be for a U.S. investor if

the correlation between the Japanese stock market returns and exchange rate

movements were zero?

b. Suppose the dollar volatility of the Japanese stock market is 11.35%, what can you

conclude about the correlation between the Japanese bond market movements and

exchange rate movements?

Bank PAPOUF decides to issue two bonds and wonders what should be the fair interest

rate on these bonds:

– Bond A: A two-year dual-currency bond with interest in and principal in $. The

bond is issued for 100 and pays an interest rate of i , each year for two years. The

principal is reimbursed at $50.

– Bond B: A two-year currency option bond. The bond is issued in $ with a face value of

$ 100. The bondholder can choose to have the coupons and principal paid in dollars or

in , at a specified exchange rate of = 2, that is, receive either $100 or 200 as

principal repayment, or receive either $C or 2C as interest if C is the coupon set in

dollars.

Current market conditions are as follows:

Spot exchange rate: S = = 2.

a. What should be the coupon i set on Bond A consistent with current market

conditions?

b. What should be the coupon C set on Bond B consistent with current market

conditions?

On April 1, an Australian investor decides to hedge a U.S. portfolio worth $10 million

against exchange risk using AUD call options. The spot exchange rate is AUD/$ = 2.5

or $/AUD = 0.40.

The Australian investor can buy November calls AUD with a strike price of 0.40 U.S.

cents per

AUD at a premium of 0.8 U.S. cent per AUD. The size of one contract is AUD 125,000.

The delta

of the option is estimated at 0.5.

a. How many AUD calls should our investor buy to hedge the U.S. portfolio against the

AUD/$ currency risk?

b. A few days later the U.S. dollar has dropped to AUD/$ = 2.463 ($/AUD = 0.406) and

the dollar value of the portfolio has remained unchanged at $10 million. The November

40 AUD call is now worth 1.2 cents per AUD and has a delta estimated at 0.7. What is

the result of the hedge?

c. How should the hedge be adjusted?

Consider two European firms listed on Euronext:

– Company I: Its stock return shows a consistent positive correlation with the value of

the euro.

The stock price of Company I (in euros) tends to go up when the euro appreciates

relative to the U.S. dollar.

– Company II: Its stock return shows a consistent negative correlation with the value of

the euro. The stock price of Company II (in euros) tends to go down when the euro

appreciates relative to the U.S. dollar.

An American investor wishes to buy European stocks but is unsure about whether to

invest in Company I or Company II. She is afraid of a depreciation of the euro relative

to the U.S. dollar. Which of the two investments would offer some protection against a

weakening U.S. dollar?

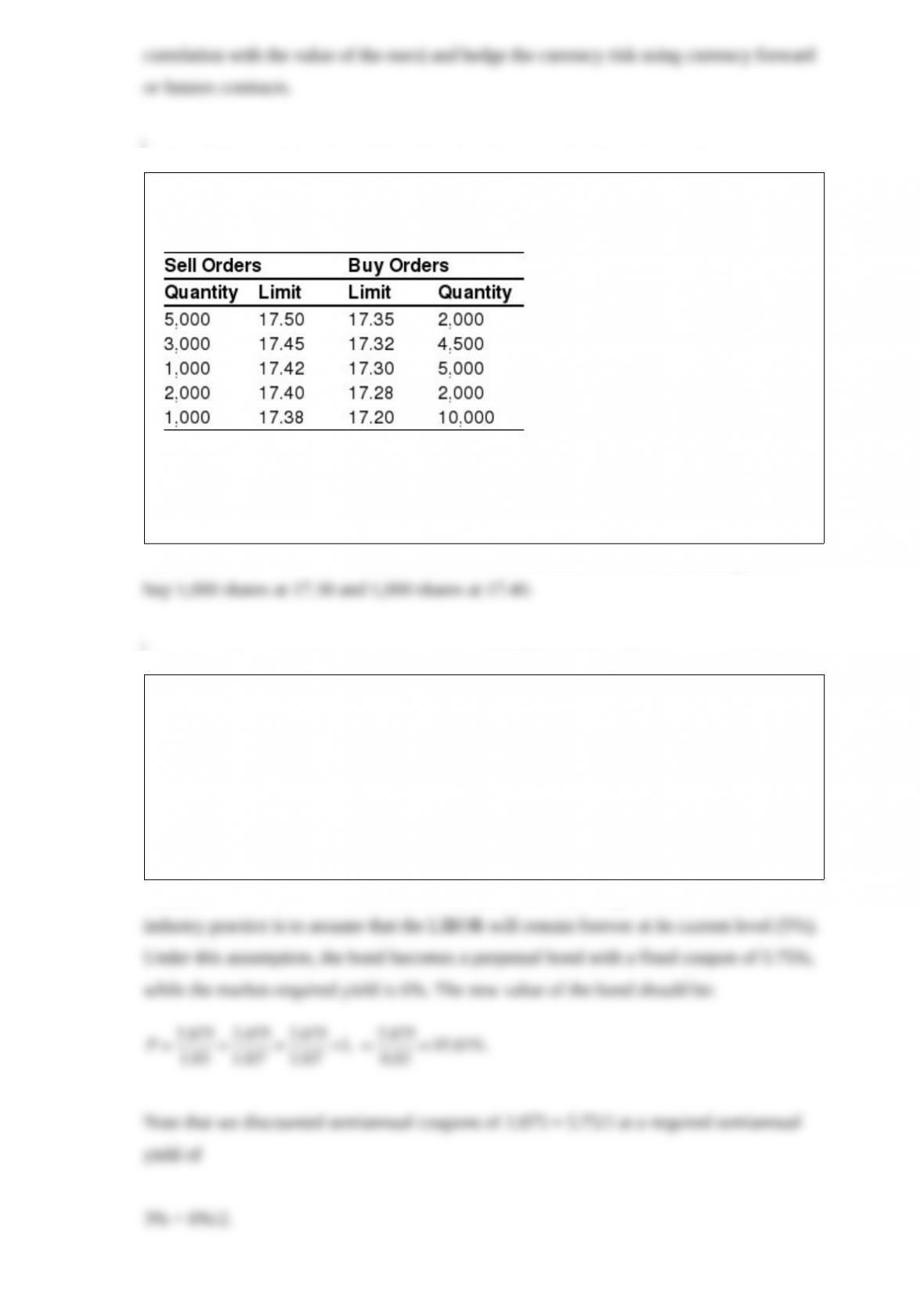

Vivendi Universal is a French firm listed on Euronext, the Paris Bourse. You can access

the central limit order book directly on the Internet and find the following information:

You wish to buy 2,000 shares and enter a market order to buy those shares. A market

order has no limit, so, it will be executed against the best matching order. At what price

will you buy the shares?

A corporation rated A has issued a semiannual FRN in dollars. This is a perpetual bond,

which will pay coupons indefinitely if the corporation does not default. The coupon is

set at six-month LIBOR plus a spread of ¾%. The six-month dollar LIBOR is equal to

5%.

Six months later, the six-month dollar LIBOR has remained at 5%, but the

market-required spread for A-rated corporations on long-term FRNs has moved to 1%.

Give some estimation of the new value of the FRN on the reset date.

Guaranteed note.

You are a young banker offering a client to issue a guaranteed note. The yield curve is

flat at 9% for each maturity. Options on the stock index are offered by banks. An

at-the-money call with a two-year maturity trades at 12% of the index value, whereas a

three-year call is worth 15% of the index.

You wonder about the characteristics of the bond. If you offer a high coupon, the

indexation will be low. Therefore, you decide to compute the indexation levels in

accordance to the current market conditions for maturities of two and three years and

coupon levels of 0%, 2%, and 5%.

The euro is quoted as = 1.1420-1.1425, and the Canadian dollar is quoted as

= 1.3540-1.354 What is the implicit quotation?

The average premium on currency calls has decreased, whereas the premium on

currency puts has increased. What explanations can you provide?

What is the difference between a foreign bond and a Eurobond?