You hold a bond with a duration of 17. Its yield is 6% while the cash (one-year) rate is

4%. You expect yields to move down by 10 basis points over the year.

a. Give a rough estimate of your expected return.

b. What is the risk premium on this bond?

In studying the impact of consolidation on Price/Earnings (P/E) ratios, there are four

basic methods of consolidating the account of a subsidiary into the parent company:

· Full consolidation. Assets, liabilities, and earnings of the subsidiaries are fully

incorporated,

line-by-line, into the parent’s accounts, with special care to avoid double counting.

· Proportional consolidation. Assets, liabilities, and earnings are consolidated

line-by-line, proportionate to the percentage of ownership in the subsidiary.

· Equity consolidation. A share of the subsidiary profits is consolidated on a one-line

basis, proportionate to the share of equity owned by the parent. The value of the

investment in the subsidiary is adjusted to reflect the change in the subsidiary’s equity.

· No consolidation. This is sometimes referred to as the cost method, whereby only

dividends received from the subsidiary affect earnings of the parent. The value of the

investment in the subsidiary is carried at cost in the parent’s book and is not revalued.

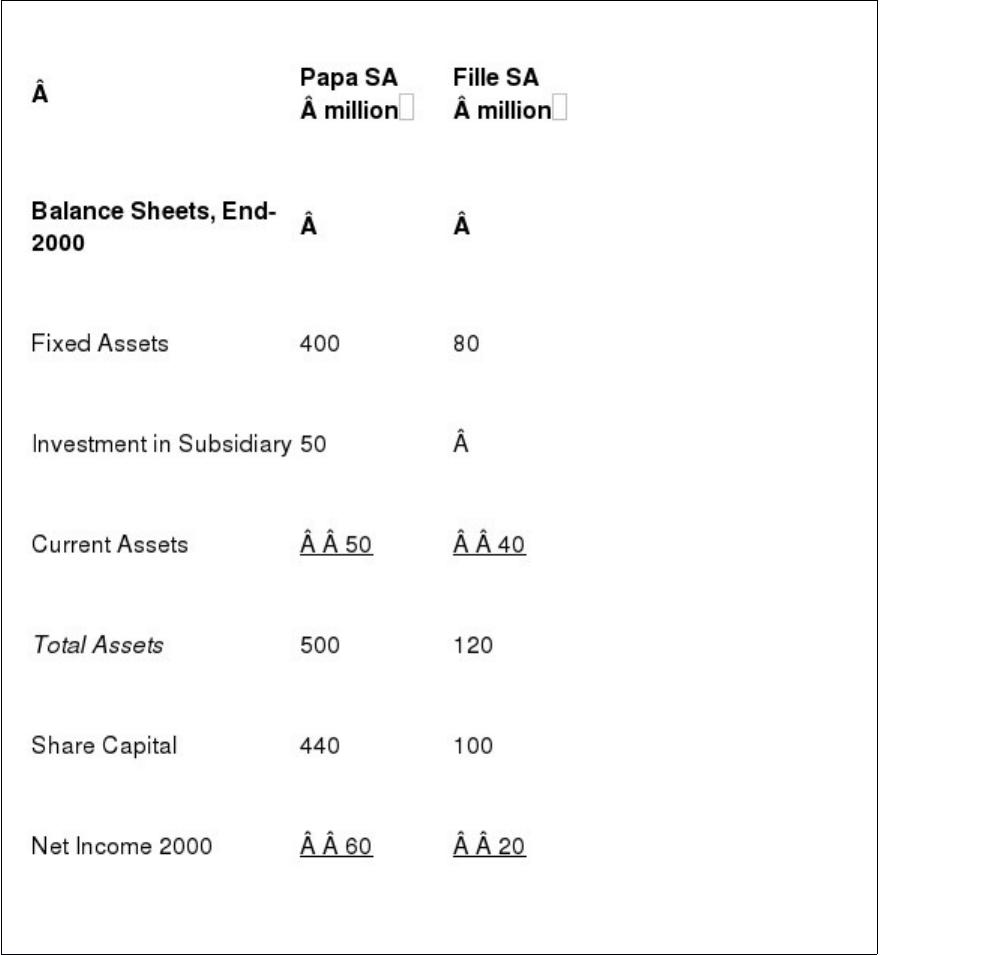

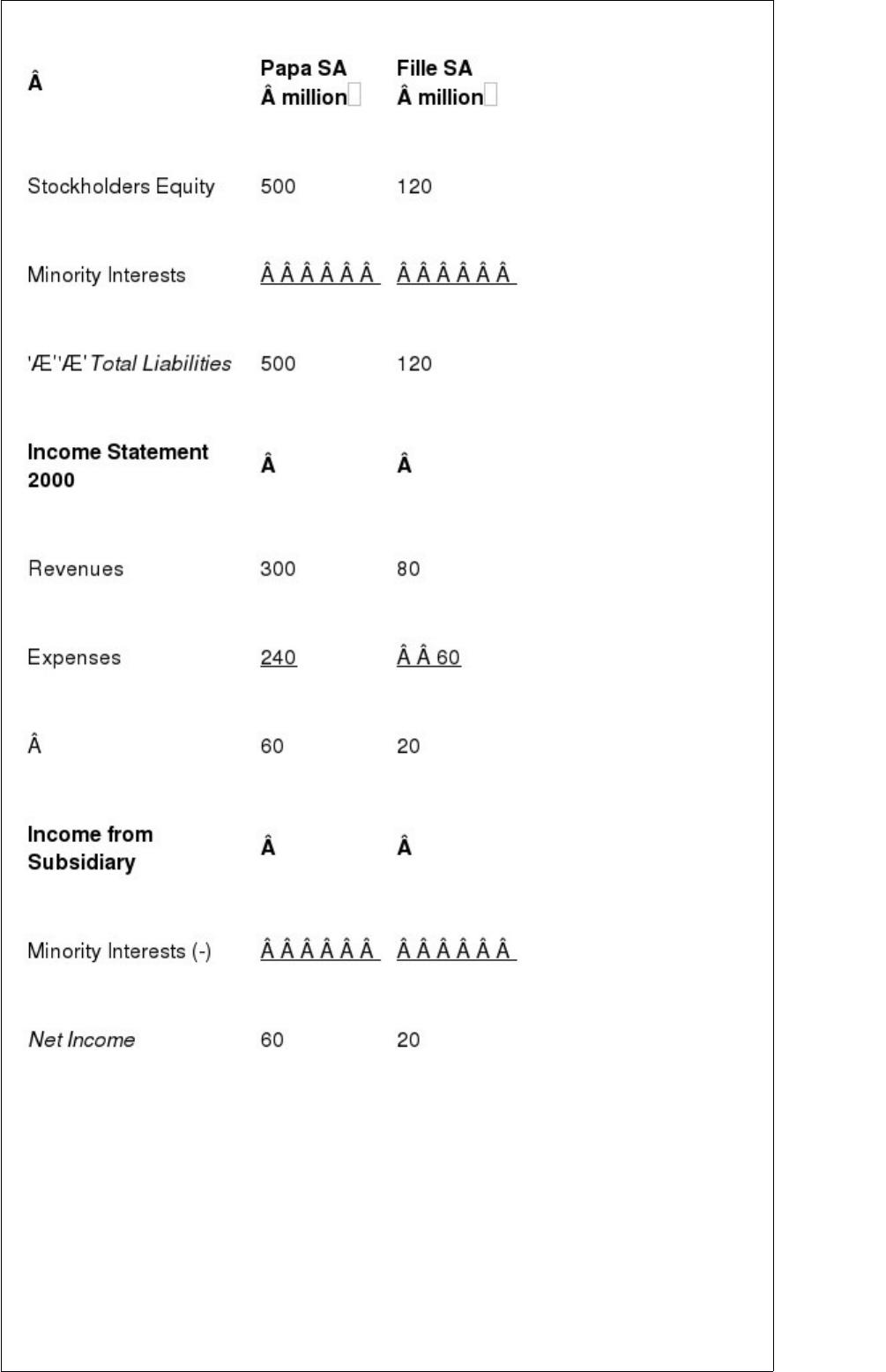

Here are the simplified 2000 accounts of Papa SA and Fille SA, two French firms. Papa

SA owns 50% of Fille SA, a company created the previous year. Fille SA has not paid

any dividend. The nonconsolidated accounts follow:

Continued

The nonconsolidated accounts for Papa SA use the cost method, whereby the

investment in the subsidiary is carried at historical cost in the balance sheet of the

parent.

a. Establish the consolidated accounts, using the other three methods outlined above.

b. Which method provides the highest reported net income for Papa SA?

c. Which method provides the highest P/E ratio, based on book value, for Papa SA?

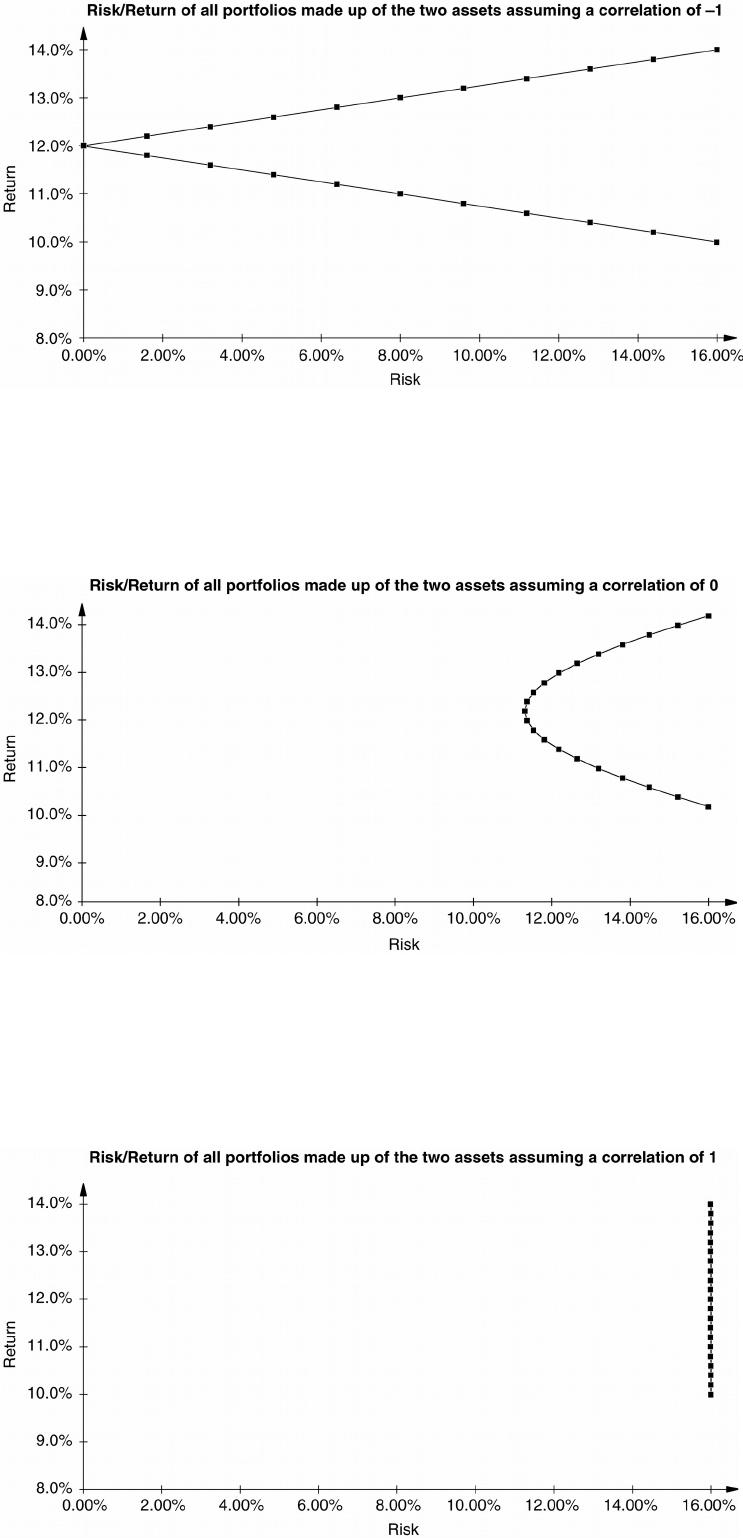

Here are the expected returns and risks of two assets:

E(R1) = 10% 1= 16%

E(R2) = 14% 2= 16%

a. Assume a correlation of 0.5 and draw all the portfolios made up of the two assets in

an Expected Return/Risk graph.

b. Same question assuming successively a correlation of -1, 0, and +1.

c. Looking at the four graphs, what do you conclude about the importance of correlation

in

risk-reduction?

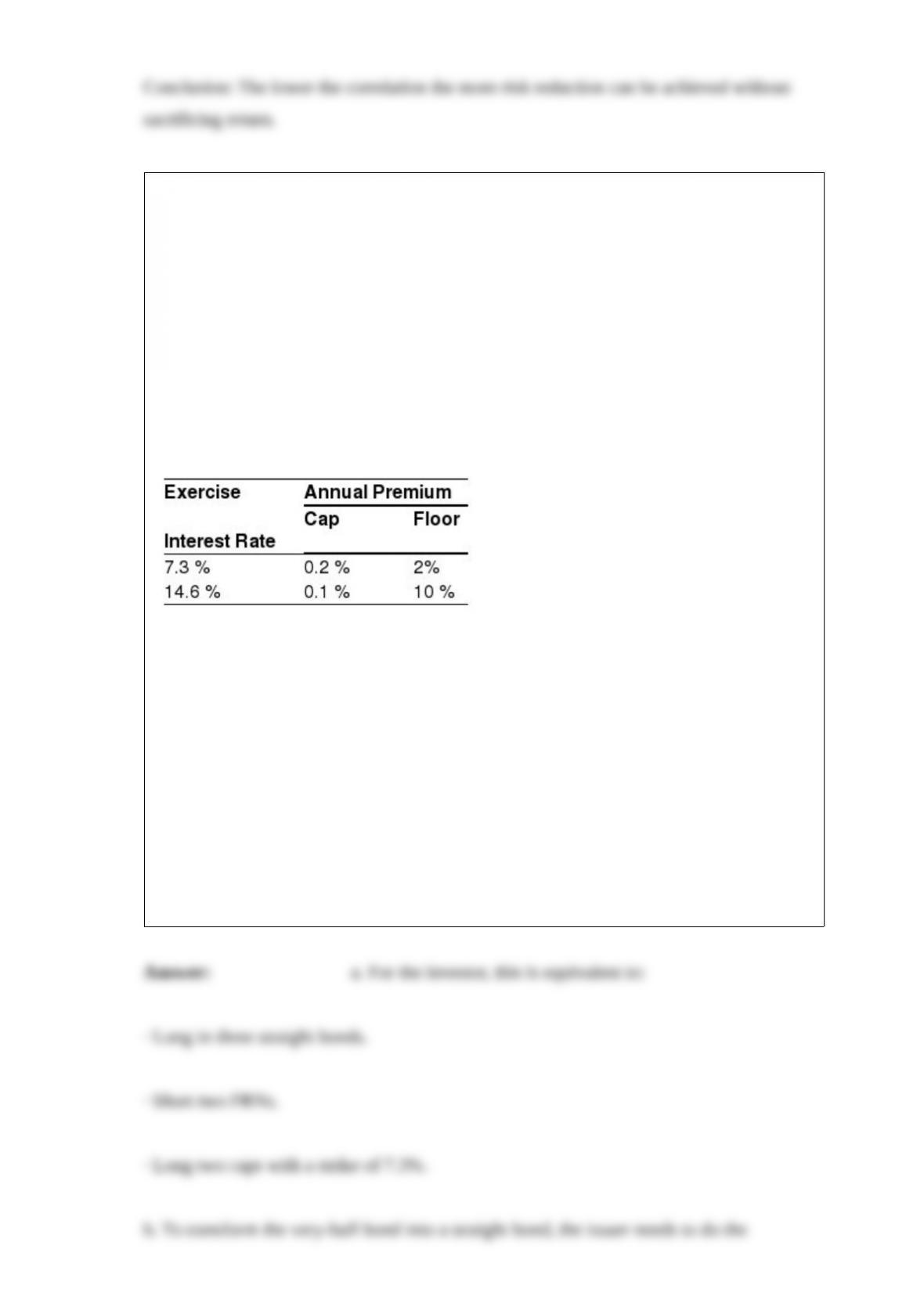

The Kingdom of Papou issues a very-bull bond with a coupon equal to:

14.6 – 2 x LIBOR.

Of course, the coupon cannot be negative.

The Kingdom could have issued a FRN at LIBOR + ¼ %, or a straight bond at 5.30%.

The current market conditions for swaps are 5% against LIBOR.

You could also trade in caps and floors with different exercise prices (these are levels of

interest rates). The premium are paid annually.

a. You are a buyer of this very-bull bond. Tell us what it is equivalent to, in terms of

buying/selling: FRN, straight bonds, caps or floors.

b. Assume that the Kingdom actually wanted to issue a straight bond (fixed coupon).

The bank will put in place a “de-mining” portfolio with swaps and options so that this

very-bull bond plus the “de-mining” portfolio is equivalent to a straight bond. What is

exactly the “de-mining” portfolio? (Be very precise and tell us if the Kingdom must pay

fixed, receive LIBOR or vice versa, etc.)

c. What is the cost advantage for the Kingdom compared to issuing bonds at 5.30%?

d. Same question assuming that the Kingdom wanted to issue an FRN at LIBOR + ¼%?

Which of the following bonds has the longest duration?

a. 8-year maturity; 6% coupon.

b. 8-year maturity; 11% coupon.

c. 15-year maturity; 6% coupon.

d. 15-year maturity; 11% coupon.

An asset manager has conducted an extensive econometric study and proposes a

forecasting model. He has found that a currency with a high interest rate tends to

appreciate relative to a currency with

a low interest rate. The simple forecasting model for the one-year exchange rate is that a

currency should appreciate over the year by the amount of the interest rate differential

quoted today. For example, if the Australian dollar exchange rate is = 2 and the

one-year interest rates in AUD and are 4% and 7%, respectively, the U.S dollar

should move up by 3% relative to the Australian dollar, and your forecast for the

exchange rate at the end of the year is = 2.06.

a. What is the current forward exchange rate?

b. What type of forward transaction would you conduct to capitalize on your forecast?

c. If everyone were using your model and following your strategy, what would happen

to the exchange and interest rates?

A straight bond with an annual coupon of 9% will be reimbursed 100% in three years.

The previous coupon has just been paid and this bond currently trades at 105.25%. Its

European yield-to-maturity is 7%.

a. What is its modified duration?

b. What is its semiannual yield-to-maturity?

c. What is its simple yield?

A one-year bond is issued by a corporation with a 5% probability of default by

year-end. In case of default, the investor will recover nothing. The one-year yield for

default-free bonds is 10%.

a. What yield should be required by investors on these corporate bonds if they are risk

neutral?

b. What should the credit spread be?

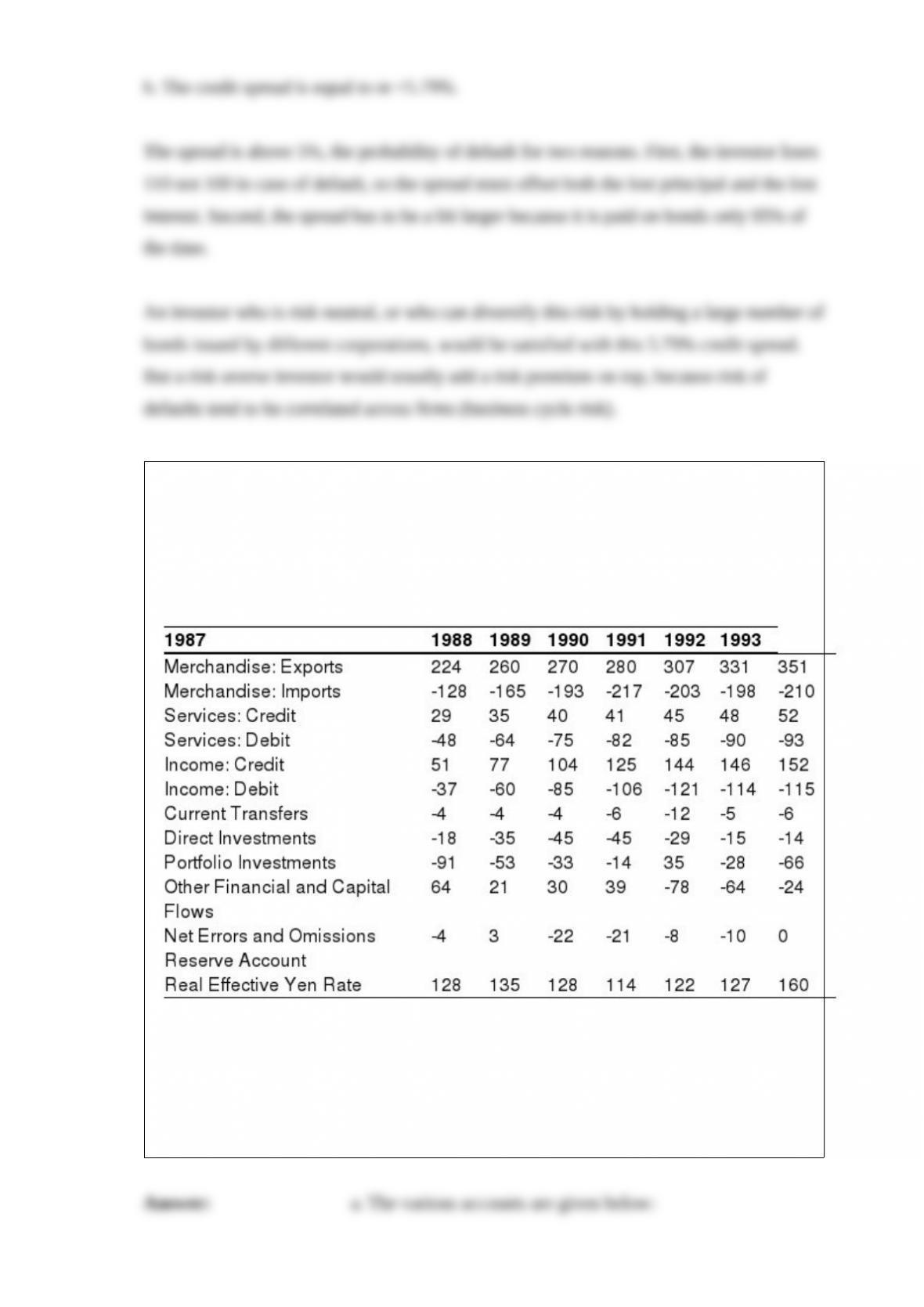

The Japanese balance of payments from 1987 to 1993 is as follows. All numbers are

reported in billions of U.S. dollars. The last line gives the real effective exchange rate

index of the yen relative

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and

official reserve account for each year.

b. Use these numbers to describe what has happened in terms of Japanese financial

transactions with the rest of the world.

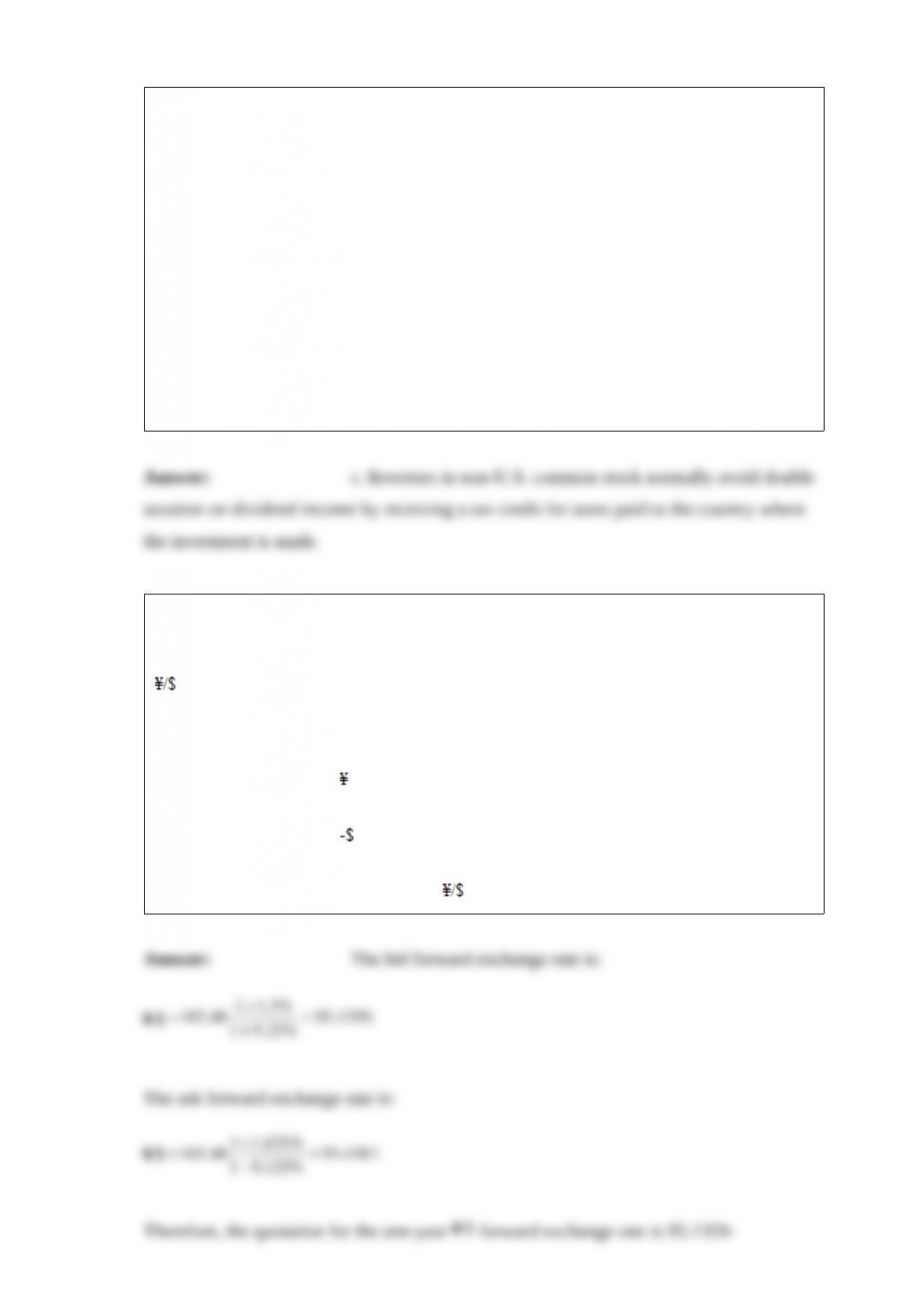

Which of the following statements best characterizes the taxation of returns on

international investments in an investor’s country and/or the country where the

investment is made?

a. Capital gains normally are taxed only by the country where the investment is made.

b. Tax-exempt investors normally must pay taxes to the country where the investment is

made.

c. Investors in non-U.S. common stock normally avoid double taxation on dividend

income by receiving a tax credit for taxes withheld by the country where the investment

is made.

d. The investor’s country normally withholds taxes on dividend payments.

The bid-ask rates are as follows:

Spot exchange rate:

102.40-48

Interest rates:

One-year interest rate in 11/2 – 5/8

One-year interest rate in 91/8 – 1/4

What is the quotation for the one-year forward exchange rate?

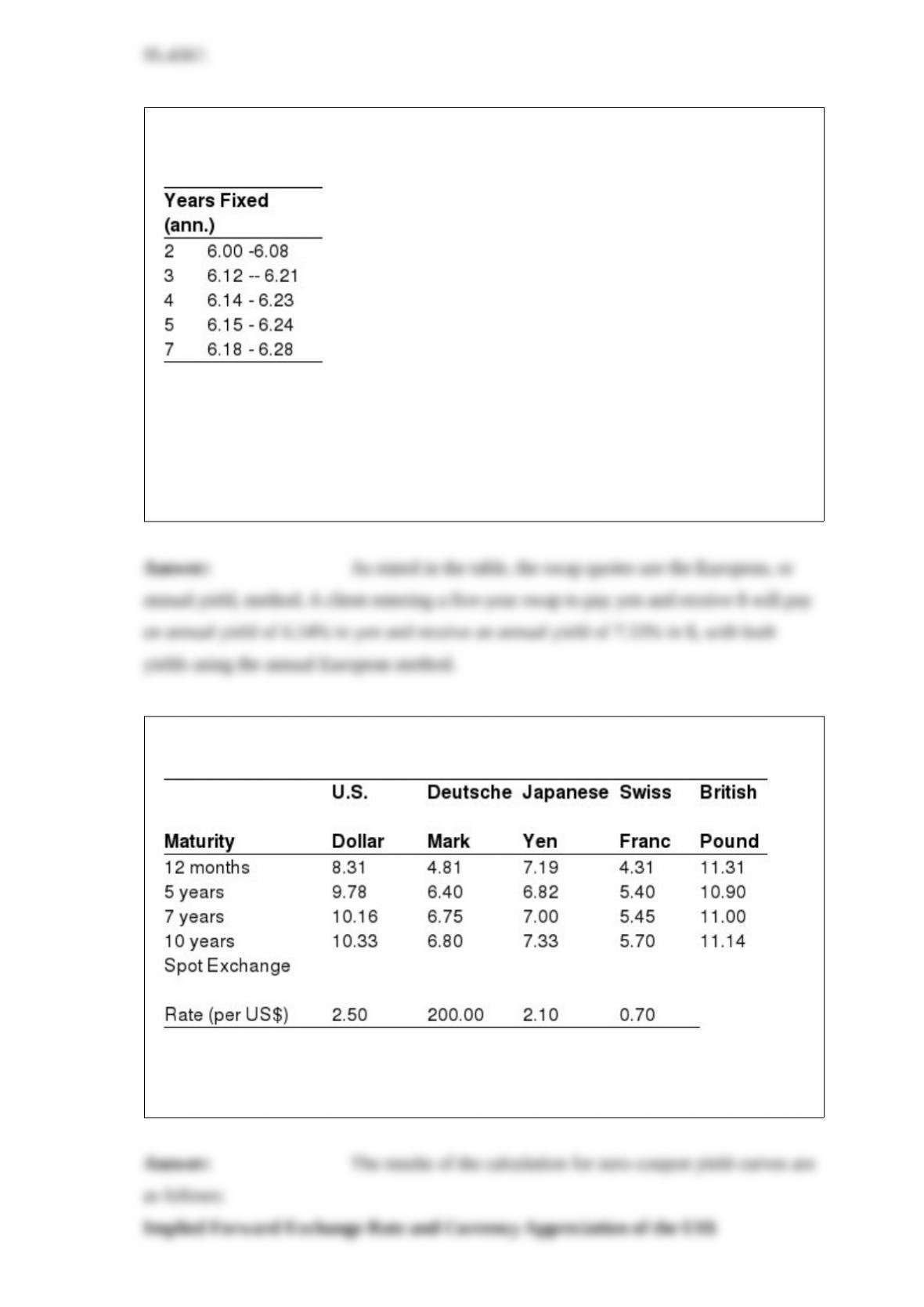

A swap dealer provides the following quotations for a yen/$ currency swap. The quotes

are for a yen fixed rate against the U.S. Treasury yield flat, with annual payments.

A client wishes to enter a five-year swap, paying yen and receiving $. The current yield

on five-year U.S. Treasury bonds is 7.20%, using the semiannual method, which

amounts to 7.33%, using the annual European method.

What will the exact terms of the swap be if the client accepts these quotations?

Back in 1985, when the Deutsche mark still existed, the yield curves were as follows:

Calculate the implied forward exchange rates, assuming that yields on zero-coupon

bonds (European convention) for maturities of more than one year.

The current Swiss franc/euro rate is 1.5 francs per euro. Inflation rates are

approximately 1% in Switzerland and between 1.8% and 2.2% in the various countries

of the euro zone. One-year interest rates are 2% in Swiss francs and 3% in euros. What

would be a natural forecast for the Swiss franc/euro exchange rate next year?

Why did U.S. commercial banks have an interest in the development of the Eurobond

market?