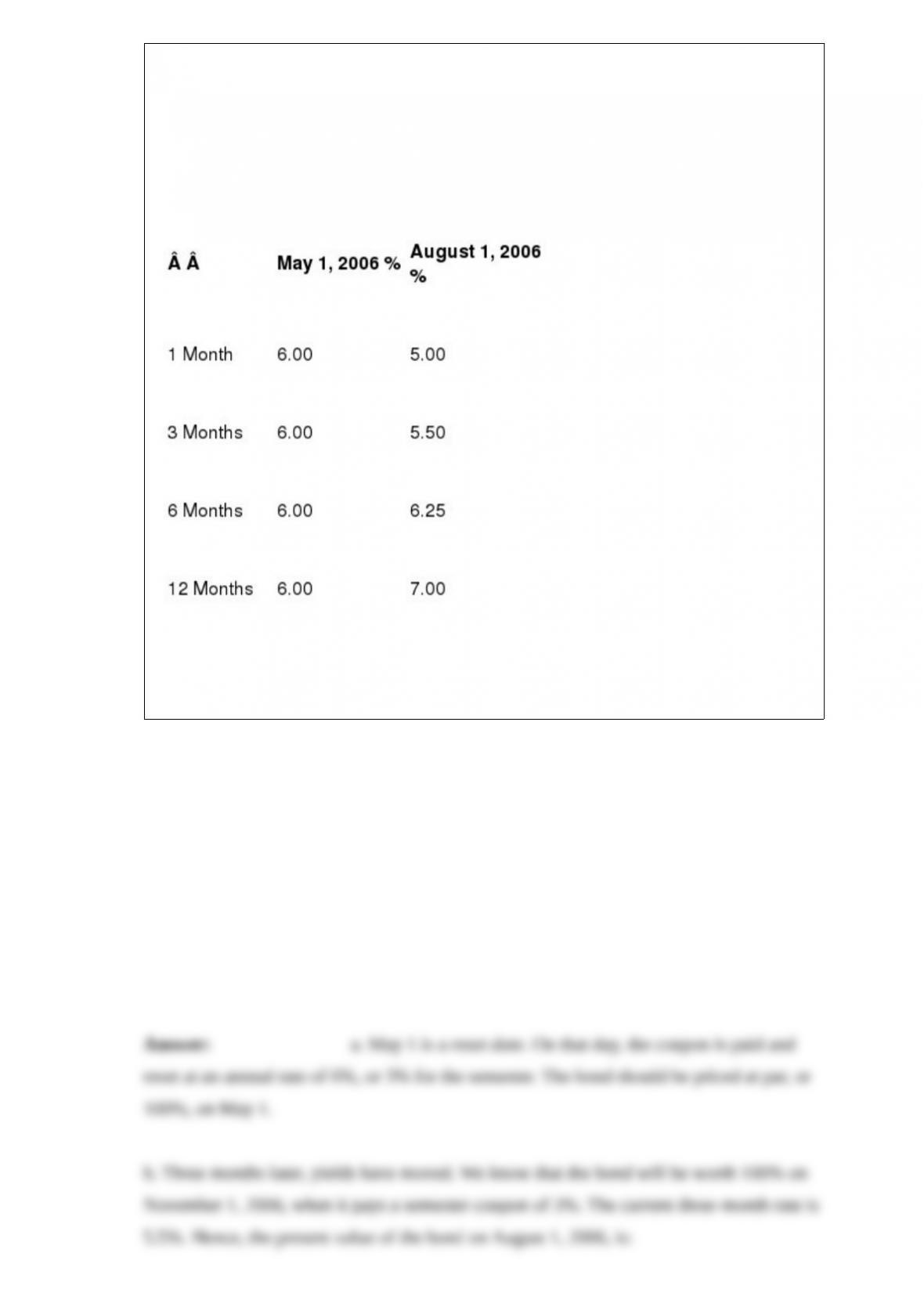

A company without default risk can issue a five-year dollar FRN at LIBOR. The

coupon is paid and reset semiannually. It is certain that the issuer will never have

default risk and will always be able to borrow at LIBOR. The FRN is issued on

November 1, 2005, when the six-month LIBOR is at 5%. Here are the dollar yield

curves on two different dates:

a. What should the value of the FRN be on May 1?

b. What should the value and the clean price of the FRN be August 1, 2006?

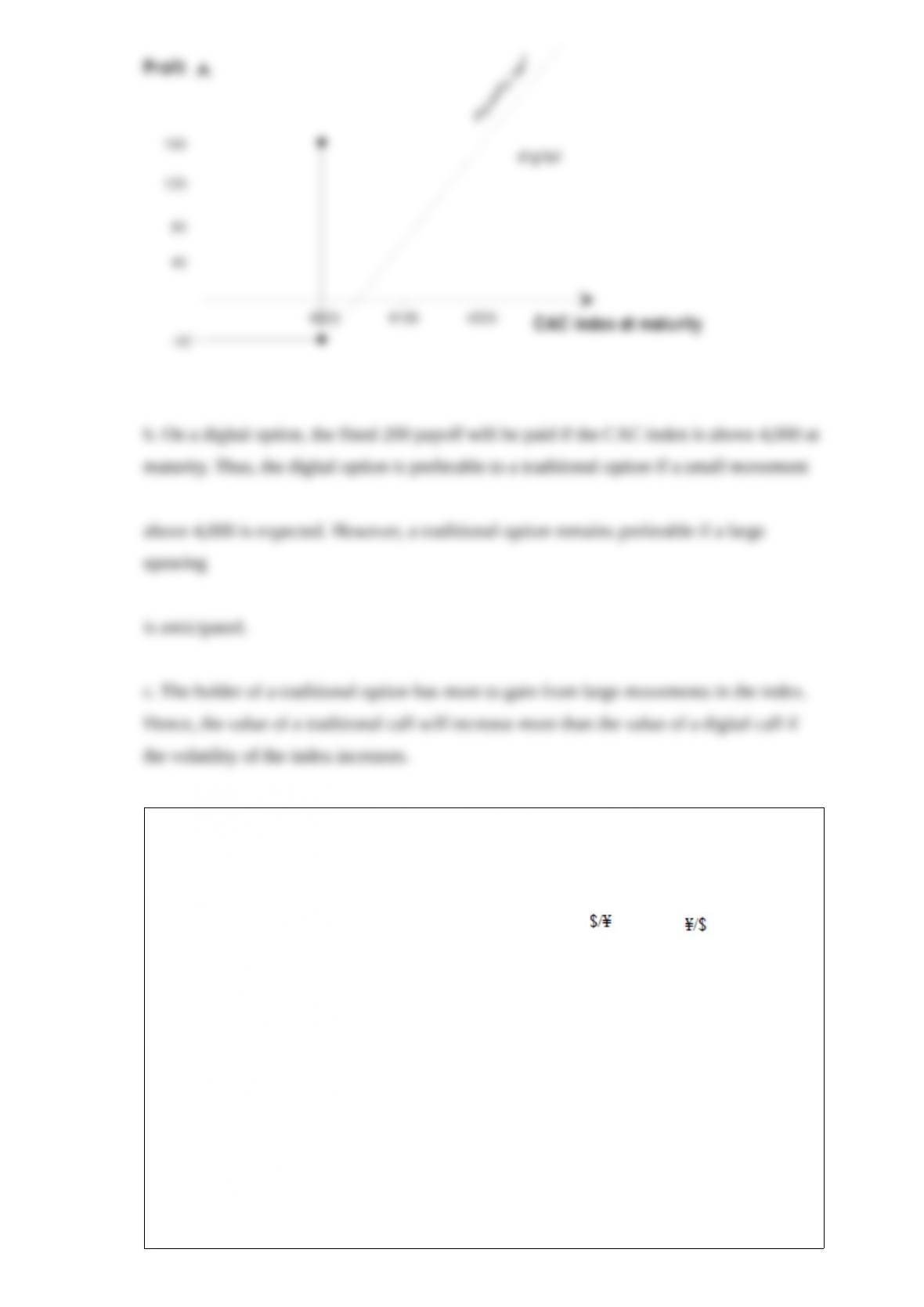

Digital options: Digital (or binary) options can only have two payoffs at maturity. If the

strike condition set in the option is met, the buyer will receive the full prespecified

payoff. If not, the buyer receives no payoff. This is different from a traditional option

where there exists an infinite number of payoffs. For example, we could have a digital

option on the French CAC index, stating that the option buyer will get ¬200 if the CAC

index is above 4,000 at expiration and zero otherwise. On this digital option, the buyer

will get exactly 200 as soon as the CAC index is above the 4,000 level at expiration,

whether it be 4,001, 4,100, or 5,000.

a. Draw the profit and loss curve at expiration as a function of the CAC index for these

two options:

· Traditional call on the CAC index: Exercise price: 4,000; premium: 40.

· Digital call on the CAC index: Exercise price: 4,000; payoff if exercised: 200;

premium: 40.

b. What are the relative advantages of the two options?

c. Assume that the volatility of the French stock market increases suddenly. Should the

premium on the digital call increase more (or less) than the premium on the traditional

call?

Titi, a Japanese company, issued a six-year international bond in dollars convertible into

shares of the company. At time of issue, the long-term bond yield on straight dollar

bonds was 10% for such an issuer. Instead, Titi issued bonds at 8%. Each $1,000 par

bond is convertible into 100 shares of Titi. At time of issue, the stock price of Titi is

1,600 yen, and the exchange rate is 100 yen = 0.5 dollars ( = 0.005, = 200).

a. Why can the bond be issued with a yield of only 8%, below the market rate for

straight dollar bonds?

b. What would happen if:

· The stock price of Titi increases?

· The yen appreciates?

· The market interest rate of dollar bonds drops?

A year later, the new market conditions are as follows:

· The yield on straight dollar bonds of similar quality has risen from 10% to 11%.

· Titi stock price has moved up to 2,000.

· The exchange rate is 0.006.

c. What would be a minimum price for the Titi convertible bond?

d. Could you try to assess the theoretical value of this convertible bond as a package of

other securities, such as straight bonds issued by Titi, options or warrants on the yen

value of Titi stock, and futures and options on the dollar/yen exchange rate?

A small German bank has the following portfolio of loans in U.S. dollars, valued at

market value:

The German bank fears a long-term depreciation of the U.S. dollar relative to the euro

and believes in stable U.S. interest rates.

a. What is its currency exposure?

b. What type of swap arrangements should it contract?

c. What should the principal of the swaps be?

In the 1970s, France had a dual exchange rate system in place for its residents. All

business trade transactions took place at the official, or “commercial,” exchange rate

(say, 5 francs per U.S. dollar). All foreign investments by French industrial corporations

were subject to prior government authorization. The regulation was even stricter for

French financial institutions or private residents. They were not allowed to transfer

currency abroad. French tourists could not take abroad more than FF 5,000 (or its

equivalent in foreign currency) per year. French residents could buy foreign securities,

but had to use a special “financial” rate to purchase these foreign currencies. Basically,

the supply of foreign currency assigned to “financial” francs was fixed. To buy foreign

securities, residents had to use the proceeds of the sales of foreign securities by other

French residents. This led to a separate market for the “financial” franc with a different

exchange rate. Foreign income and dividends paid were repatriated at the “commercial”

franc rate and did not increase the supply of “financial” currency available. By contrast,

foreigners were free to buy and sell French securities at the “commercial” rate, but they

were not allowed to borrow francs.

a. Explain why this type of control imposed on French residents helps defend the

French franc, which was periodically under devaluation pressure.

b. Would you expect the financial exchange rate to be higher or lower than the

commercial rate?

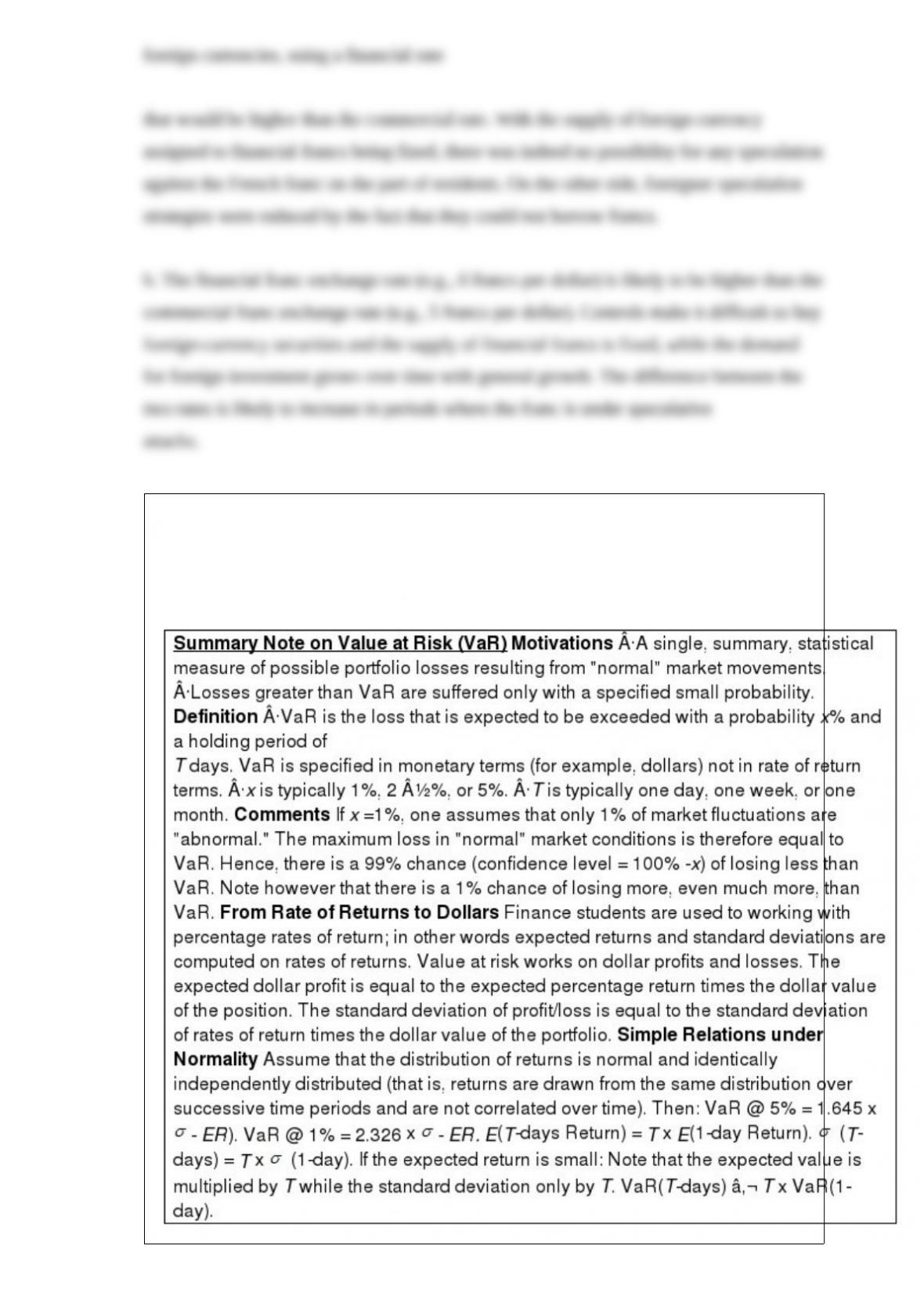

The next problem deals with Value at Risk, which is not detailed in this textbook. A

brief summary note on Value at Risk is given below.

You have to compute the VaR (Value at Risk) of a portfolio with a probability of 5%

(confidence level of 95%). Your portfolio is worth $100 million evenly invested in two

assets (50 million in asset 1 and 50 million in asset 2). Here are some statistics for

monthly returns of the two assets:

E(R1) = E(R2) = 0%

(R1) = 5%

(R2) = 7%

Correlation = 0.5.

You make the hypothesis that the distributions are normal.

You know that in a normal distribution 5% of the observations lie below -1.645 x ³.

a. What is the monthly VaR of the portfolio with a 5% probability?

b. What is the one-year VaR of the portfolio with a 5% probability?

An asset manager follows an active international asset allocation strategy. The average

execution cost for a buy or a sell order is forecasted at 0.6%. On average, the manager

turns over the portfolio once a year. Various administrative costs include a custodial

cost amount of 0.5% per year of assets under management. The annual management fee

is 1% of assets under management. The annual expected return before costs is 14%

compared to an expected return of 10% on a passive global benchmark (some global

index).

a. What is the annual expected return net of execution costs?

b. What is the net annual expected return for the client?

c. Should the client expect the portfolio to outperform the global index used as a

benchmark?

Inflation indexed bonds.

Many countries, among which the United Kingdom, the United States, and France, have

issued inflation indexed bonds. Coupons and reimbursement value depend on the price

index at the time of payment. Let’s assume that a bond has been issued for 100 at time

0, with a maturity and a real coupon equal to . Let It be the price index at time t. The

coupon paid at t will be:

Ct = x It/I0.

And the reimbursement value at maturity n will be:

R = 100 x I/I0.

Since the reimbursement is also indexed on the price index, we can easily check that the

actual yield is equal to the real coupon accrued by the inflation rate.

However, the real interest rate required by the market fluctuates with time. Knowing the

market price of an inflation indexed bond and its real coupon, we can easily compute

(using a discounting method) its real yield at any time t.

If the indexed bond still has years to maturity, we just have to use the discounting

method for a real cash-flow bond:

Knowing the real interest rate , we can compare it with the nominal interest rate on

classic bonds.

a. In terms of risk, what is the interest of such bonds? What kind of investors is it aimed

at?

b. In terms of return, assume that yield curves and are flat and that we expect the

inflation level to remain constant for the coming years. You expect an annual inflation

rate of . In what case do you prefer an inflation-indexed bond to a straight bond? [Find

the relation between r, and ]

You are a U.S. investor and wish to buy 10,000 shares of Club Mediterranee (“Club

Med”). You can buy them on the Paris Bourse or on SEAQ International in London.

You ask the brokers to quote you net prices (no commissions paid). There are no taxes

on foreign shares listed in London. Here are the quotes:

London (in )

Paris (in )

(dollars per pound) 1.5000-1.5040

(euros per dollar) 0.91100-0.91200

a. What is your total dollar cost if you buy the Club Med shares at the cheaper place?

b. Are there arbitrage opportunities between London and Paris?

Assume that the domestic and foreign assets have standard deviations of = 16% and

= 19%, respectively, with a correlation of = 0.6. The risk-free rate is equal to 5%

in both countries.

a. The expected returns of the domestic and foreign assets are both equal to 10%, E(Rd)

= E(Rf) = 10%. Calculate the Sharpe ratios for the domestic asset, the foreign asset, and

an internationally- diversified portfolio equally invested in the domestic and foreign

assets. What do you conclude?

b. Assume now that the expected return on the foreign asset is higher than on the

domestic asset, E(Rd) = 10% but E(Rf) =12%. Calculate the Sharpe ratio for an

internationally diversified portfolio equally invested in the domestic and foreign assets,

and compare your findings to those in Question (a).

A hedge fund has a capital of ¬100 million and invests in a market neutral long/short

strategy on the European equity market. Shares can be borrowed from a primary broker.

The arrangement with the primary broker is that the hedge fund deposits as guarantee

securities with an equivalent market value at time of lending, plus an additional cash

margin deposit equal to 10% of the value of the shares. The primary broker keeps any

interest earned on the margin and charges a fee equal to an annual rate of 0.5% of the

value of the shares borrowed. The hedge fund believes that European value stocks will

outperform European growth stocks. The hedge fund expects that value stocks will

outperform growth stocks by 5% over the year. The hedge fund wishes to retain a cash

cushion of ¬10 million

for unforeseen events. The short-term euro interest rate is 3%.

a. What market-neutral strategy would you suggest that would take full advantage of

this scenario?

b. What is the expected return according to the funds’ expectations?

c. Assume now that the European stock index appreciates by 20% over the year, but that

value stocks underperform growth stocks by 10%. Compute a likely market value of the

fund at year’s end.

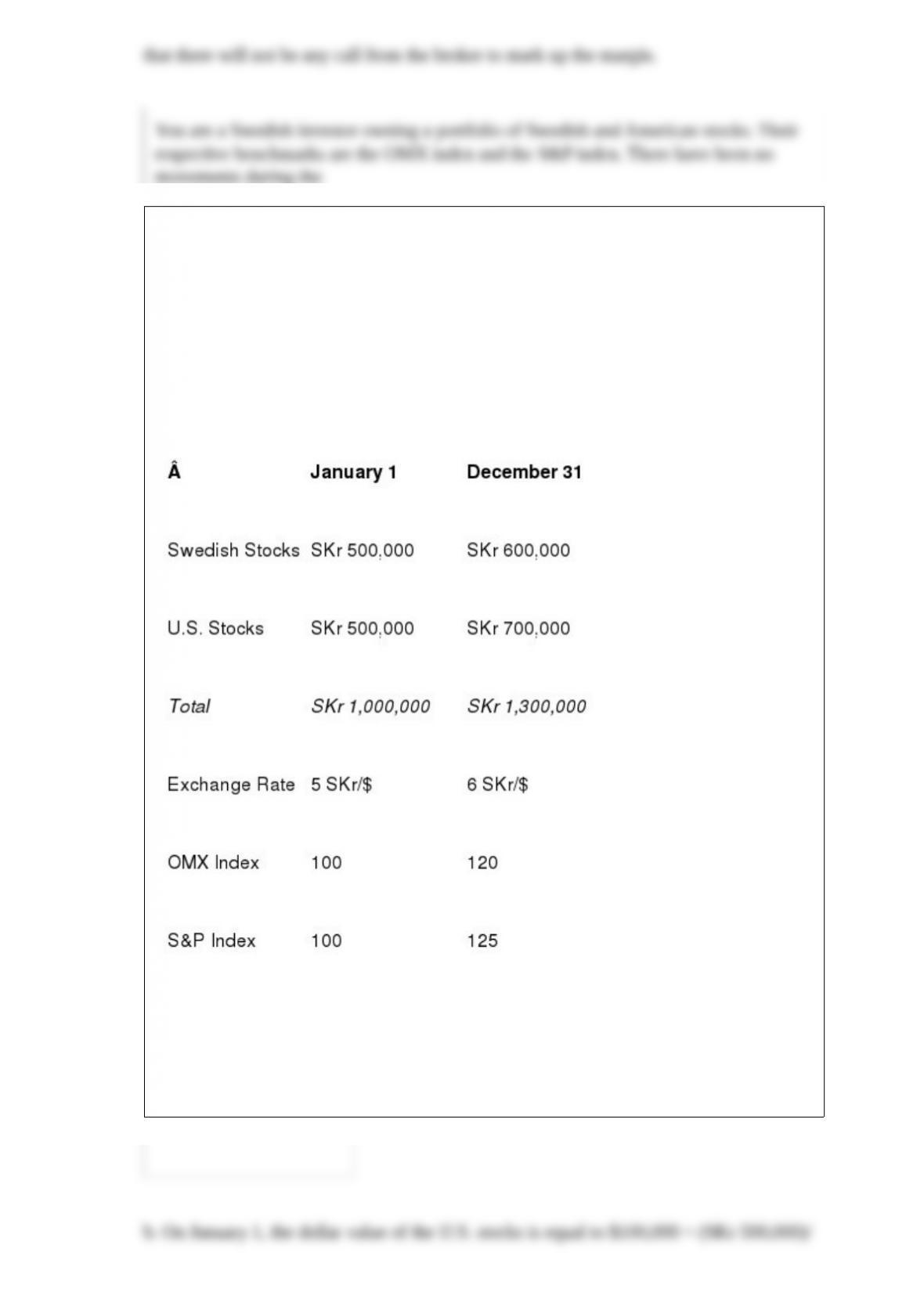

You are a Swedish investor owning a portfolio of Swedish and American stocks. Their

respective benchmarks are the OMX index and the S&P index. There have been no

movements during the

year (cash flows, sales, or purchases, dividends paid). Valuation and performance

analysis is done in Swedish krona (SKr). Here are the valuations at the start and the end

of the year:

a. What is the total return on the portfolio?

b. Decompose this return into capital gain, yield, and currency contribution.

c. What is the contribution of security selection?

You specialize in arbitrage between the futures and the cash market on the Paris Bourse.

The CAC stock index is made up of 40 leading stocks. The futures price of the CAC

contract with delivery in a month is 2,120. The size of the contract is 10 times the

index. The spot value of the index is given as 2,000. Actually, there are transaction costs

in the cash market; the bid-ask spread is around 40 points. You can buy a basket of

stocks representing the index for 2,020 and sell the same basket for 1,980. Transaction

costs on the futures contracts are assumed to be negligible. During the next month, the

stocks in the index will pay dividends amounting to 5 per index. These dividends have

already been announced, so there is no uncertainty about this cash flow. The current

one-month interest rate in euros is 61/2 – 5/8%.

a. Do you detect any arbitrage opportunity?

b. What profit could you make per contract?

c. What is the theoretical value of the futures bid and ask prices?

The market price of a two-year bond is 105% of its nominal value. The annual coupon

to be paid in exactly one year is 7%. Its yield-to-maturity (European method) is

4.336%.

a. Calculate its duration.

b. Calculate its simple yield.

c. Calculate its semiannual yield (U.S. method).

Fuji Bank issued convertible Eurobonds in January 1989. Convertible bonds were a

popular way for Japanese banks to raise funds while the Tokyo stock market was

booming in the 1980s. The lure of capital gains from converting the bonds to equity

allowed the banks to issue the securities with a very low interest rate.

Fuji Bank Eurobond was a 500-million Swiss franc zero-coupon bond, issued at par

with a maturity of five years. A bond with a face value of 100 Swiss francs could be

converted into two shares of Fuji Bank at any time starting in 1991. At time of issue,

Fuji’s stock was worth 3,590 yen, and a Swiss franc was worth 80 yen. The bond also

had a put option that could be exercised at the start of 1991 (and only at that time).

Bondholders had the option of redeeming the bond at a premium of 2.625% over its

face value. In other words, bondholders could obtain 102.625 francs for each bond. On

January 14, 1991, the Tokyo stock market and the yen dropped. A stock of Fuji Bank

was worth

2,400 yen, and a Swiss franc was worth 95 yen. Yields on Swiss franc bonds were

around 4%. Most bonds were presented for early redemption.

a. Why was it advantageous for a bondholder to exercise the put option?

b. What was the total yen loss for Fuji Bank?

Strumpf Ltd. decides to issue a convertible bond with a maturity of two years. Each

bond is issued with a nominal value of 100 and an annual coupon C; of course, C has

to be determined. Each bond can be redeemed for 100 or converted into one share of

Strumpf at the option of the bondholder.

The current stock price of Strumpf is 90. The yield curve for an issuer like Strumpf is

flat at 6%. Barings is ready to issue long-term options on Strumpf shares. The

premiums on calls with one-year and two-year expirations are given below:

a. American-type calls are more expensive than European-type calls. Is it reasonable?

b. Assume that the bond can only be converted at maturity, after payment of the second

coupon. What should be the fair coupon rate C, consistent with the above market

conditions?

c. Assume that the bond is issued with the coupon rate determined above. The yield

curve suddenly moves from 6% to 6.1% and the option premiums stay the same. What

should be the new market price of the convertible bond?

d. Assume now that the bond can be converted on two dates (rather than one as above).

These dates are the first year (right after the first coupon payment) and the second year

as above. It is not possible to convert the two-year bond at any other date. Is it possible

to construct an arbitrage portfolio allowing to price the fair coupon C with the above

data? Be precise in your explanation and state what type of options you would need to

price the bond.

You are an American investor holding some German stocks. Over the month, the value

of your

stock portfolio goes from 5 million to 5.2 million. The exchange rates move from $1

per euro

to $0.98 per euro.

a. What is your rate of return in euros?

b. What is your rate of return in dollars?

c. Is the difference between the dollar return and the euro return exactly equal to the

percentage movement in the exchange rate? If not, why?

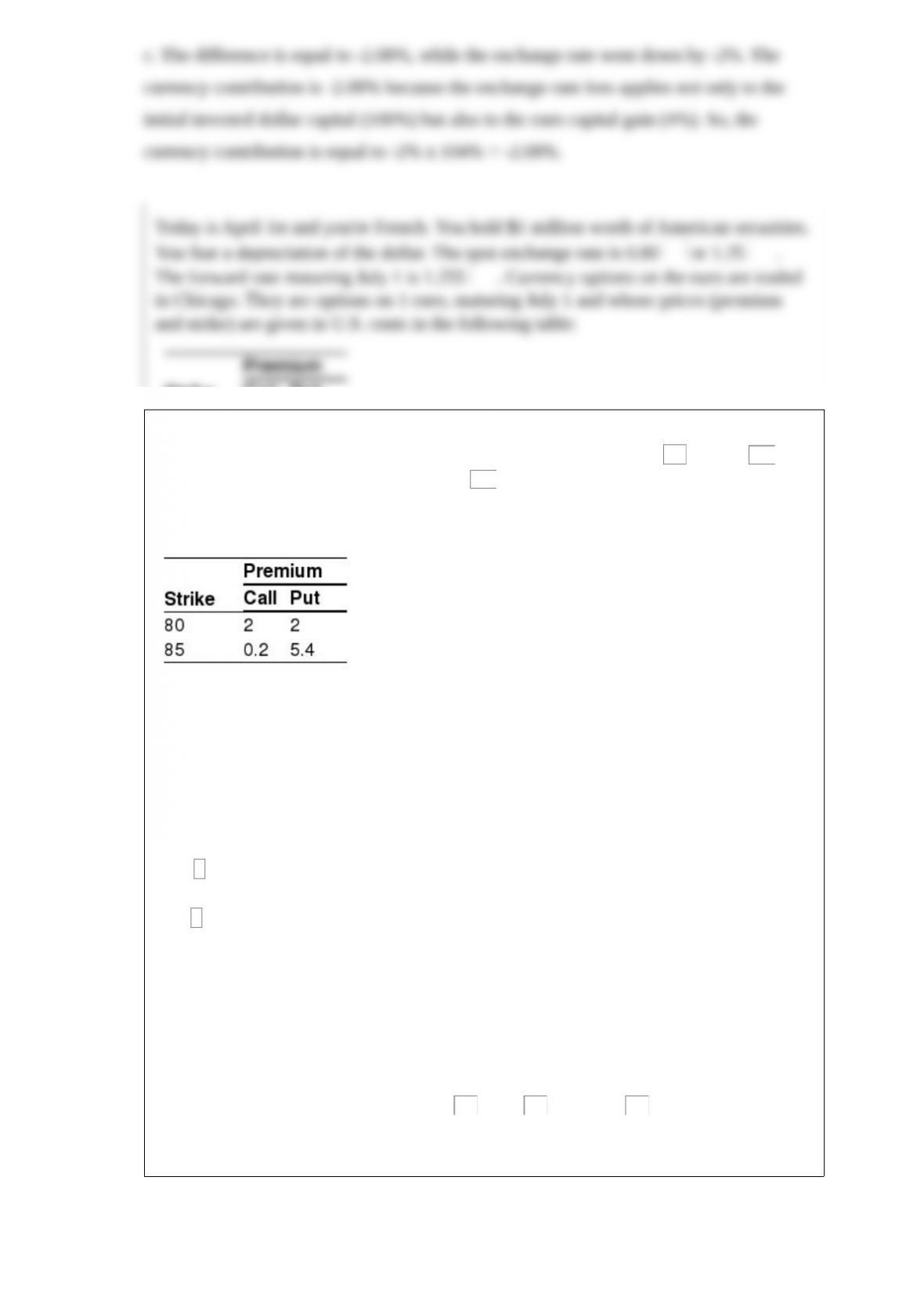

Today is April 1st and you’re French. You hold $1 million worth of American securities.

You fear a depreciation of the dollar. The spot exchange rate is 0.80 or 1.25 .

The forward rate maturing July 1 is 1.255 . Currency options on the euro are traded

in Chicago. They are options on 1 euro, maturing July 1 and whose prices (premium

and strike) are given in U.S. cents in the following table:

If you hedge using a forward contract, the bank requires no deposit. If you buy options,

you must sell some of your U.S. securities in order to buy these options. You assume

that your securities will keep exactly the same value on July 1.

a. You decide to hedge. What will be the euro value of your portfolio on July 1?

b. You decide to insure your portfolio using currency options. Do you need to buy/sell

calls /

puts ?

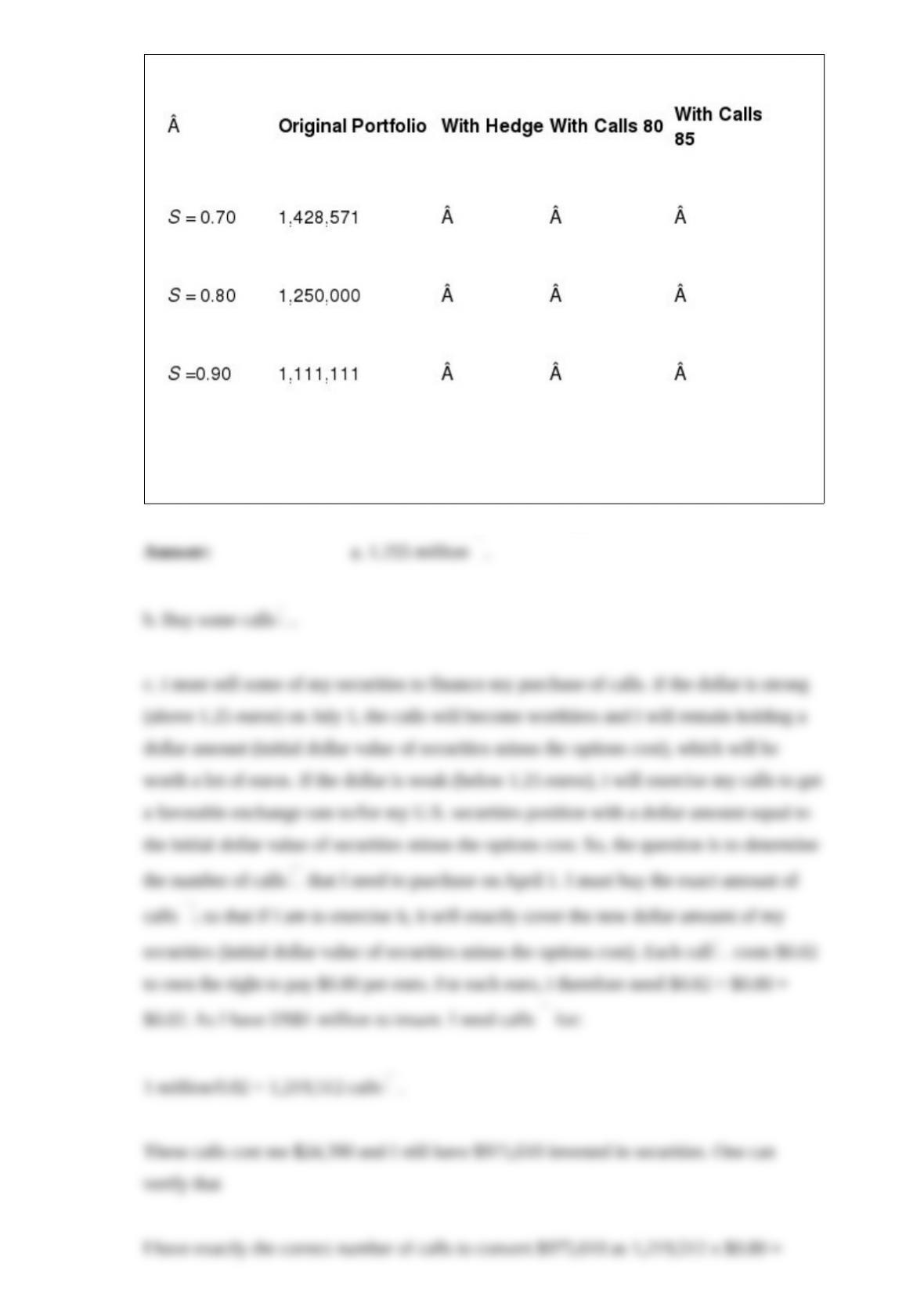

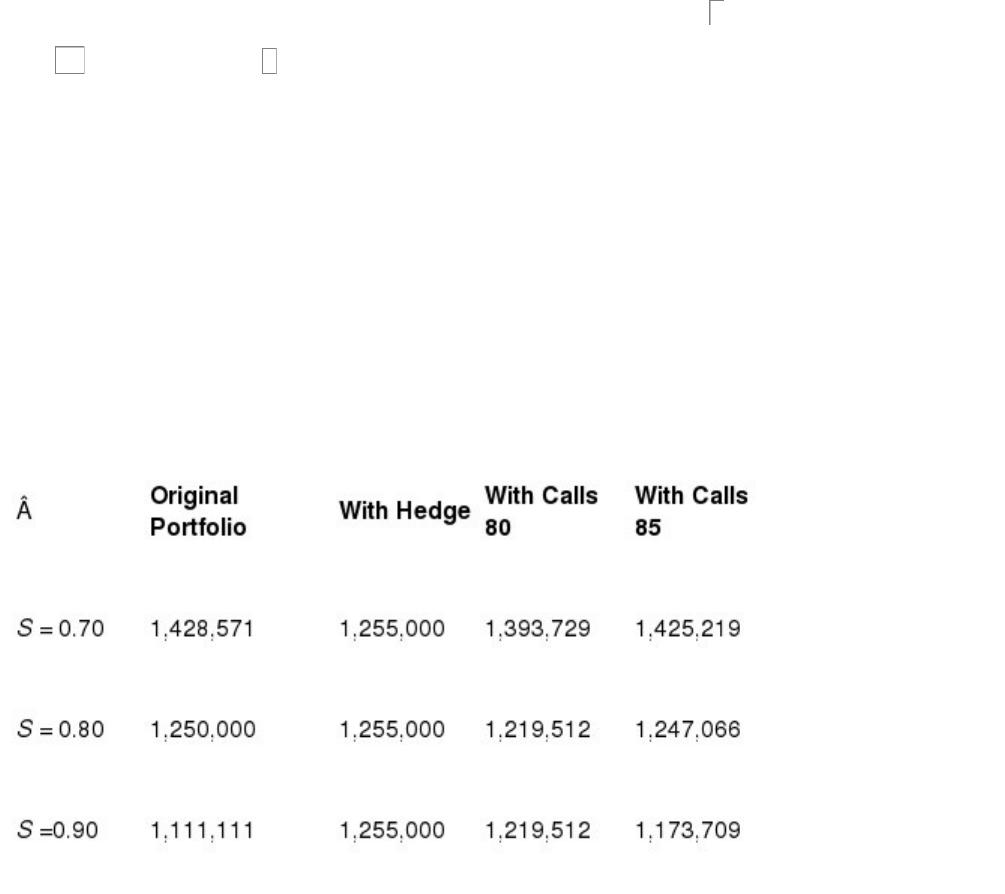

c. Assume that you use options with a strike of 80 U.S. cents. How many options do

you need to insure perfectly your portfolio?

d. Same question with options with a strike of 85?

e. Simulate the results of your hedge and insurance with the two options if the spot

exchange rate on July 1 is equal to 0.70 , 0.80 , and 0.90 . Fill the following

table with the value of the portfolio in euros:

Portfolio Value in Euros on July 1:

f. What is the best choice if you think that the chances of the depreciation of the $ are

very weak but still exist.

An American investor wants to invest in a diversified portfolio of Japanese stocks but

can invest only a rather small sum. The investor also worries about fiscal and

transaction cost considerations. Why would futures contracts on the Nikkei index be an

attractive alternative?

A manager holds a diversified portfolio of British stocks worth £5 million. He has

short-term fears about the market but feels that it is a sound long-term investment. He is

a firm believer in betas, and his portfolio’s ¢ is equal to 0.8. What are the alternatives

open to temporarily reduce the risk on his British portfolio?

Pouf is a rapidly growing and pleasant country in the Austral hemisphere. Its

inhabitants are called Poufans, and its currency is the pof. The bond market is fairly

active with many issues by Poufan companies, but there are no foreign investors or

issuers. The current yield on pof bonds is 10%. Poufan investors have to pay a 15% tax

on interest income received. The newly elected Poufan government wishes to

internationalize its bond market and attract foreign issuers. To do so, it decides to

remove any taxation of income on bonds issued by foreign corporations in Pouf.

Several changes take place after the enactment of this tax provision:

·Several well-known foreign corporations issue pof-denominated bonds in the Poufan

bond market.

·Several well-known Poufan corporations issue international bonds denominated in U.S.

dollars.

·Several dollar/pof swaps are arranged.

Try to provide a sensible explanation for this phenomenon.

Suppose that you overheard the following statements at a conference for institutional

investors:

(A German national): “My money manager knows the German firms very well; why

should I bother to invest in French and American shares? I am not familiar with their

names or their operations, and I will have to pay much higher costs to buy them.”

(A French national): “Why should I buy German and American shares? The foreign

brokers will give preferential treatment to their domestic clients, and I am going to get a

lousy deal in terms of prices and costs. Furthermore, I can’t read the financial

statements of these companies, as they are written in German or English, and with

different accounting methods.”

(An American national): “I can’t even pronounce the names of these foreign companies;

how could I defend investing abroad in front of my board of trustees? By the way, what

is the capital of Switzerland: Geneva or Zurich?”

How would you try to convince these people to diversify their portfolios if you were the

marketing representative of a big international money manager?

You purchase a Eurobond in euros, at a quoted price of 101.5%. The annual coupon on

the bond is 6%, and we are exactly one month after the past coupon date. You buy

¬100,000 of nominal value of this bond. What is your total expense?

Assume that you are a British investor who is considering investments in the German

(Stocks A and B) and Swiss (Stocks C and D) stock markets. The world market risk

premium is 4.5%. The currency risk premium on the Swiss franc is 0.5%, and the

currency risk premium on the euro is 1%. The interest rate on one-year risk-free bonds

is 4% in the United Kingdom. In addition, you are provided with the following

information:

Calculate the expected return for each of the stocks. The British pound is the base

currency.

In late 1994, it was announced that Japan’s monthly current account was shrinking and

that this effect could be permanent. Is this news good or bad for the Japanese yen?

Why?

To provide full protection against unexpected tax imposition, all Eurobond contracts

have a covenant stating that the issuer will increase the interest payments to make up

for any tax imposed. Assume that Paf Inc. has issued a Eurobond with a coupon of $10

per $100 bond. For some reason, Paf Inc. is forced by its government to transfer 15% of

the coupon as withholding tax, so that the net coupon paid to the bondholder is only

$8.50. What should Paf Inc. do, according to the bond covenant?