A German corporation finalized a sale to a Thai client on April 15. The German

corporation will deliver some gardening equipment on May 31 and will be paid 345

million baht on June 30. The current spot exchange rate is 40 baht/euro. The German

corporation is worried about a depreciation

of the baht in the coming two months and wishes to sell those baht forward against

euros.

a. Give some reasons why the German corporation should use forward rather than

futures currency contracts.

b. Exactly what contract should the German corporation arrange with its bank?

A bond has been issued in euros with an annual coupon rate of 10%. The previous

coupon has just been paid. This bond has a sinking fund provision: Half of the issue is

reimbursed in two years and half in three years. You hold 10 million of nominal value

of this bond.

a. Write the three future annual cash flows in euros, assuming that the previous coupon

has just been paid.

b. The yield curve is currently flat at 9%. What is the value of the bond, its

yield-to-maturity, its duration, and its modified duration?

c. How much do you stand to lose if the yield curve moves uniformly from 9% to 9.1%

within

one day?

A client invested $100 at the start of the month. Assume that the manager tracks an

assigned benchmark index. The benchmark is at 100 at the start of the period. After 10

days the portfolio gained 10% (value = $110), just like the index, and the client added

an extra $20 (total portfolio value = $130). From day 10 to 30, the portfolio, and the

index, lost 9.09% [final portfolio value of $130 x

(1-0.0909) = $118.18].

a. What are the rates of returns using the various methods outlined in the text?

b. Which rate should you use to evaluate the performance of the manager relative to its

benchmark?

Here are some quotes for spot exchange rates and three-month interest rates:

Spot exchange rates:

1.1865-1.1870

108.10-108.20

Interest rates:

Three-month euro 5-51/4

Three-month euro 31/4-31/2

Three-month euro 11/4-11/2

What should the quotes be for:

a. The spot exchange rate?

b. The three-month forward exchange rate?

c. The three-month forward exchange rate?

Suppose that you are an investor based in Denmark, and you expect the U.S. dollar to

depreciate by 3% over the next year. The interest rate on one-year risk-free bonds is 5%

in the United States, and 3.75% in Denmark. The current exchange rate is DKr 6.35 per

U.S. dollar. You buy some U.S. stocks with an expected return of 7% in dollars.

a. Calculate the foreign currency risk premium from the Danish investor’s viewpoint.

b. Calculate the expected return on the U.S. stock from the Danish investor’s viewpoint,

that is, in Danish krone.

c. Calculate the risk premium on the U.S. stock from a U.S. viewpoint and from the

Danish investor’s viewpoint.

d. Calculate the expected return on the U.S. stock from the Danish investor’s viewpoint,

assuming that the Danish investor hedges the currency risk. Calculate the risk premium

on the hedged

U.S. stock from the Danish investor’s viewpoint.

You will receive $10 million at the end of June and will invest it for three months on the

Eurodollar market. The current three-month Eurodollar rate is 6%, and you are worried

that the rate will drop by the end of June. Here are some market quotes:

·Eurodollar LIBOR futures, June delivery: Price 94%.

·Call eurodollar, June expiration, strike price 94%: Premium 0.4%.

·Put Eurodollar, June expiration, strike price 94%: Premium 0.4%.

The contract sizes are $1 million.

a. Should you buy or sell futures to hedge your interest rate risk?

b. Should you buy (or sell) calls (or puts) to insure a minimum rate at the time you will

invest your money? What is this rate?

c. In June, the Eurodollar rate has moved to 4%. What is the result of your strategies

using futures and using options?

d. What if the rate is equal to 8% in June?

The spot is equal to 1.1795. The one-year interest rates on the Eurocurrency market

are 4% in euros and 5% in U.S. dollars. The one-month interest rates are 3% in euros

and 4% in U.S. dollars.

a. What is the one-year forward exchange rate?

b. What is the one-month forward exchange rate?

In 1994, the United States was experiencing a fairly strong economic recovery, ahead of

other nations. Fears of an overheating economy led to sudden inflationary fears for the

next few years.

a. Would you expect U.S. interest rates to rise or drop?

b. Would you expect the dollar to depreciate or appreciate?

c. Would you expect a foreign bond portfolio to be a good investment compared to a

U.S. dollar portfolio under this scenario?

A French company knows that it will have to pay 10 million Swiss francs in three

months. The current spot exchange rate is 0.6000 . The three-month forward rate

is 0.603 . The treasurer is worried that the euro will depreciate in the next few

weeks.

a. What action can be taken?

b. Three months later, the spot exchange rate turns out to be 0.620 ; was it a wise

decision?

There is a 0.5% probability of default by the year-end on a one-year bond issued at par

by a particular corporation. If the corporation defaults, the investor will not get

anything. Assuming that a default-free bond exists with identical cash flows and

liquidity, and the one-year yield on this bond is 4%.

a. What yield should be required by risk-neutral investors on the corporate bond?

b. What should the credit spread be?

Derive a theoretical price for each of the following futures contracts quoted in the

United States and indicate why and how the market price should deviate from this

theoretical value. In each case, consider one unit of underlying asset. The contract

expires in exactly three months, and the annualized interest rate on three-month dollar

London InterBank Offered Rate (LIBOR) is 12%.

All interest rates quoted are annualized.

Let’s consider the NKK dual-currency bond shown in Exhibit 7.3. It is a bond quoted in

yen at 101%. What would happen to the market price if the following scenarios took

place?

a. The market interest rate on (newly issued) yen bonds drops significantly.

b. The dollar drops in value relative to the yen.

c. The market interest rate on (newly issued) dollar bonds drops significantly.

d. Would you give the same answers if the same bonds were quoted in dollars?

You consider investing in some emerging country. Its recent economic growth rate is

around 7%, well above the average growth rate of developed countries estimated at 2%

by the OECD. Its annual inflation rate is around 10%, well above the average inflation

rate of developed countries estimated at 2% by the OECD. The currency of the

emerging country has been depreciating at an annual rate of around 8% against major

currencies. While the volatility of the World stock index (standard deviation of dollar

returns) is around 15%, the stock market of this emerging country has a volatility of

25%. The correlation of this emerging stock market with the World index is only 0.2.

a. Are the high inflation rate and weak currency sufficient reasons to avoid investing in

this emerging country?

b. Is the high volatility of the local market a sufficient reason to avoid investing in this

emerging country?

c. Suggest why you would consider investing in this emerging country.

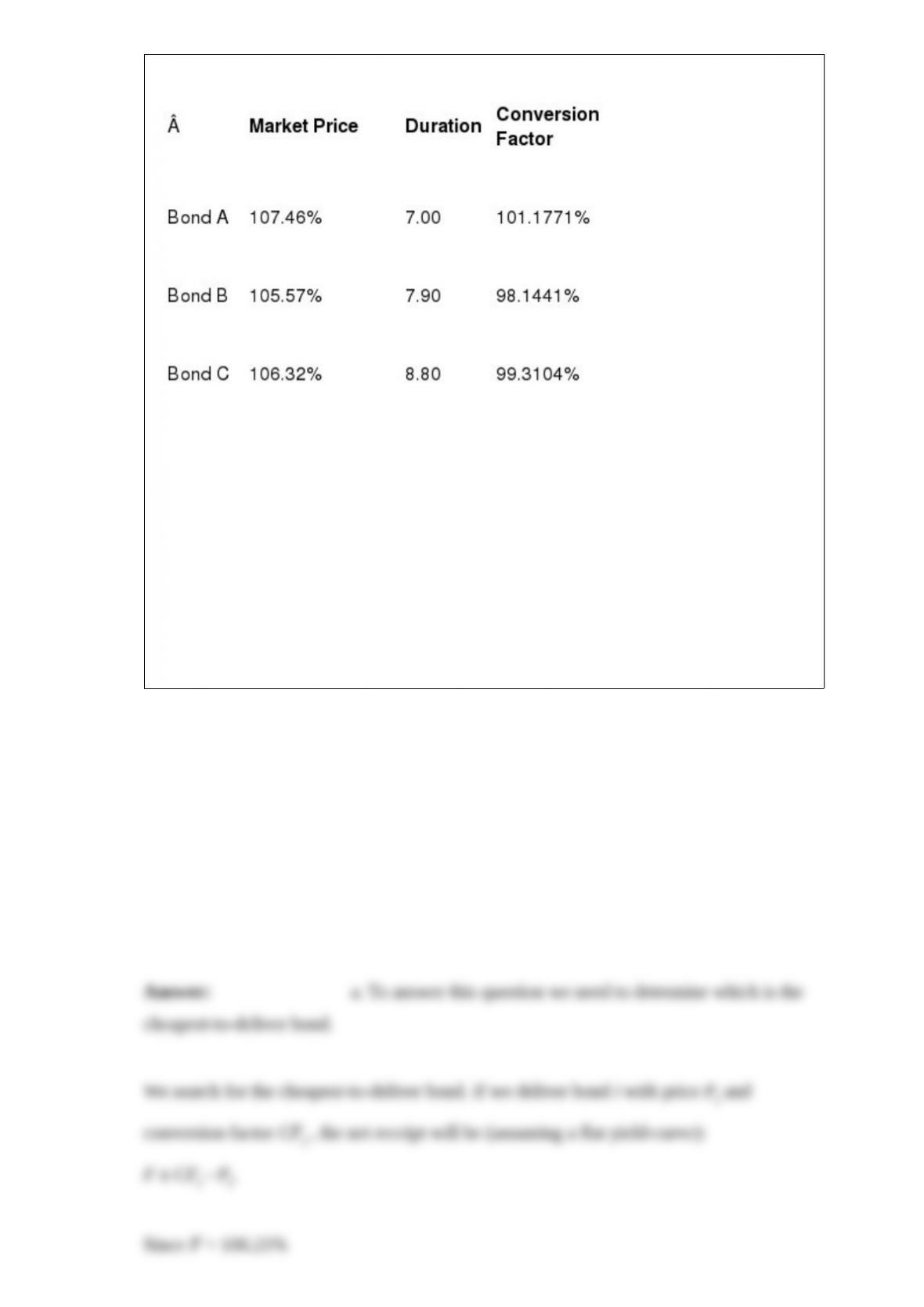

A few years ago when the French franc (FF) still existed, the MATIF futures exchange

in Paris had a very active market for the French government bond contract. The

underlying asset is a notional long-term government bond with a yield of 10%. The size

of the contract is FF 500,000 of nominal value. Futures prices are quoted in percentage

of the nominal value. On April 1, the French term structure of interest rate is flat. The

bond futures price for delivery in June is equal to 106.21%. The three French

government bonds that can be used for delivery have the following characteristics:

a. Is the futures price consistent with the spot bond prices? (Find the bond cheapest to

deliver.)

b. Estimate the interest rate sensitivity (duration) of the futures price.

c. You are an insurance company with a portfolio of French government bonds. The

portfolio has a nominal value of FF 100 million and a market value of FF 110 million.

Its average duration is 3.5. You are worried that social unrest in France could lead to an

increase in French interest rates. Rather than selling the bonds, you wish to temporarily

hedge the French interest rate risk. How many futures contracts would you sell and

why?

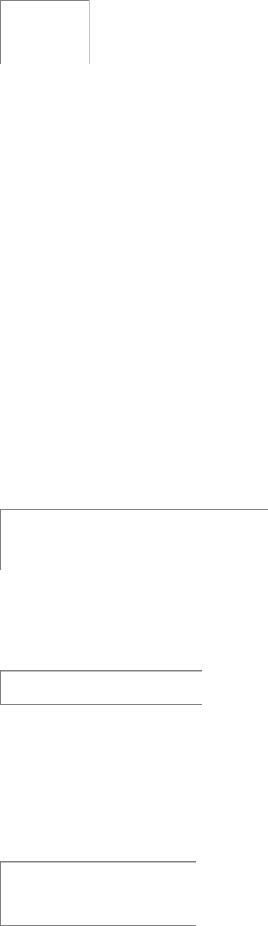

The SOL Group specializes in hedge funds invested on the Paf stock market. Over the

year 1999, the Paf stock market index went up by 20%. The SOL Group had three

hedge funds with very different investment strategies. As expected, the 1999 returns on

the three funds were quite different. Here are the performances of the three funds before

and after management fees set at 20% of gross profits:

The average gross performance of the three funds is exactly equal to the performance

on the Paf stock index. At year-end, most clients had left the third fund, and SOL C was

closed. At the start of 2000, the SOL group launched an aggressive publicity campaign

among portfolio managers, stressing the remarkable return on SOL A. If potential

clients asked whether the SOL Group had other hedge funds invested in Paf, the SOL

Group mentioned the only other fund, SOL B, and claimed that their average gross

performance during 1999 was 35%.

What do you think of this publicity campaign?

A German investor holds a portfolio of British stocks. The market value of the portfolio

is 20 million, with a of 1.5 relative to the FTSE index. In November, the spot value

of the FTSE index is 4,000. The dividend yield, euro interest rates, and pound interest

rates are all equal to 4% (flat yield curves).

a. The German investor fears a drop in the British stock market (but not in the British

pound).

The size of FTSE stock index contracts is 10 pounds times the FTSE index. There are

futures contracts quoted with December delivery. Calculate the futures price of the

index.

b. How many contracts should you buy or sell to hedge the British stock market risk?

c. You believe that the capital asset pricing model (CAPM) applies to British stocks.

The expected stock market return is 10%. What is the expected return on this portfolio

before and after hedging?

d. You now fear a depreciation of the British pound relative to the euro. Will the

strategies above protect you against this depreciation? (Assume that the margin on the

futures contract is deposited in euros.)

e. The forward exchange rate is equal to 1.4 per . How many pounds should you sell

forward?

You would like to protect your portfolio of British equity against a downward

movement of the British stock market.

a. What are the relative advantages of stock index futures and options?

b. Should you prefer in-the-money or out-of-the-money options?

You are a U.S. investor considering purchase of one of the following securities. Assume

that the currency risk of the German government bond will be hedged, and the

six-month discount on Deutsche mark forward contracts is -0.75% versus the U.S.

dollar.

You do not expect any price change in U.S. bond prices in the next six months.

Calculate the expected price change required in the German government bond, which

would result in the two bonds having equal total returns in U.S. dollars over a

six-month horizon.

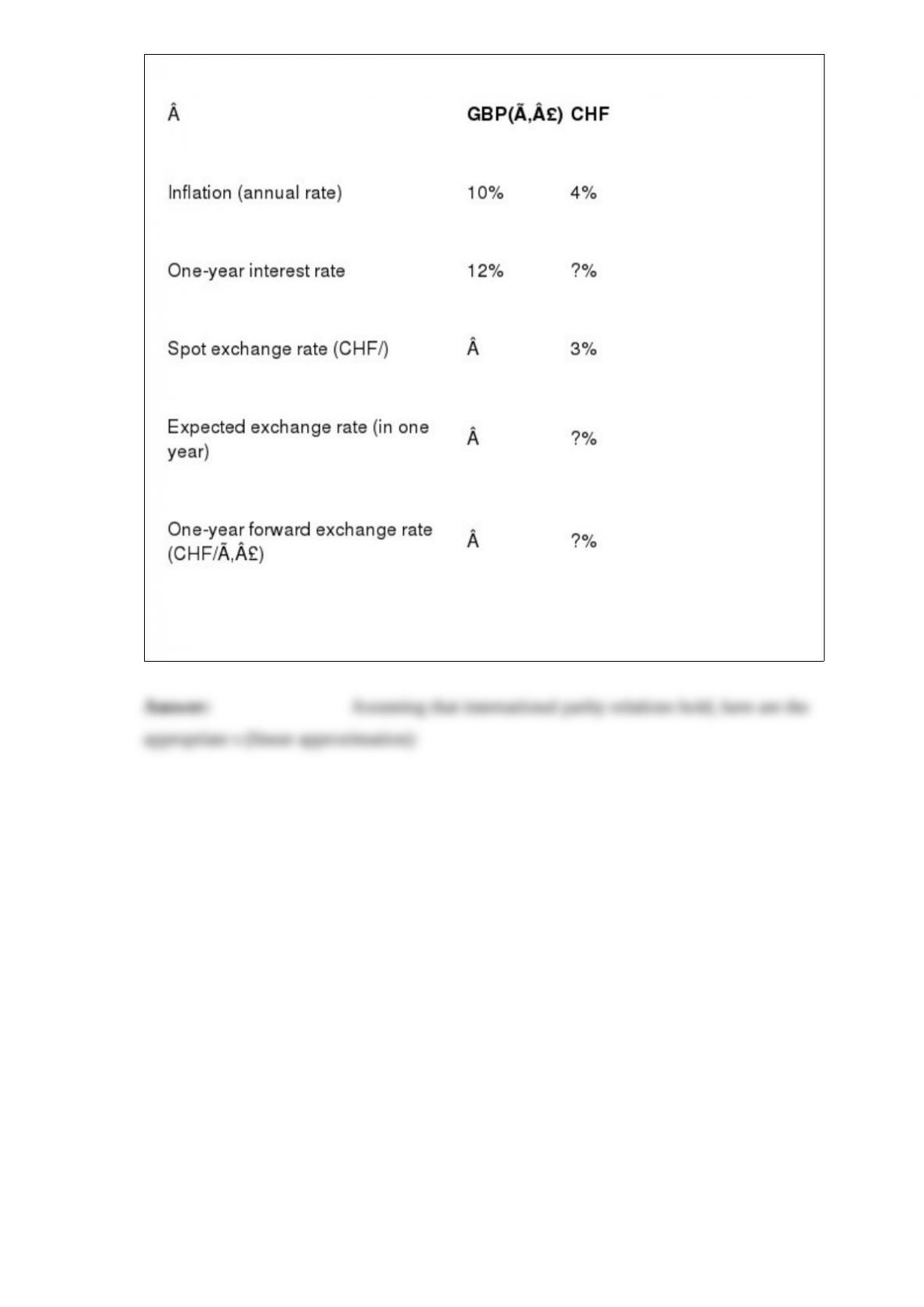

Here are some statistics:

Based on the linear approximation of international parity relations, replace the question

marks with the appropriate

The spot exchange rate is 130 yen per euro. Inflation rates in Japan and Germany are

similar. Over the past year the rate moved from 110 to 130. Is this good news or bad

news for Japanese firms competing with German firms in the automobile market?

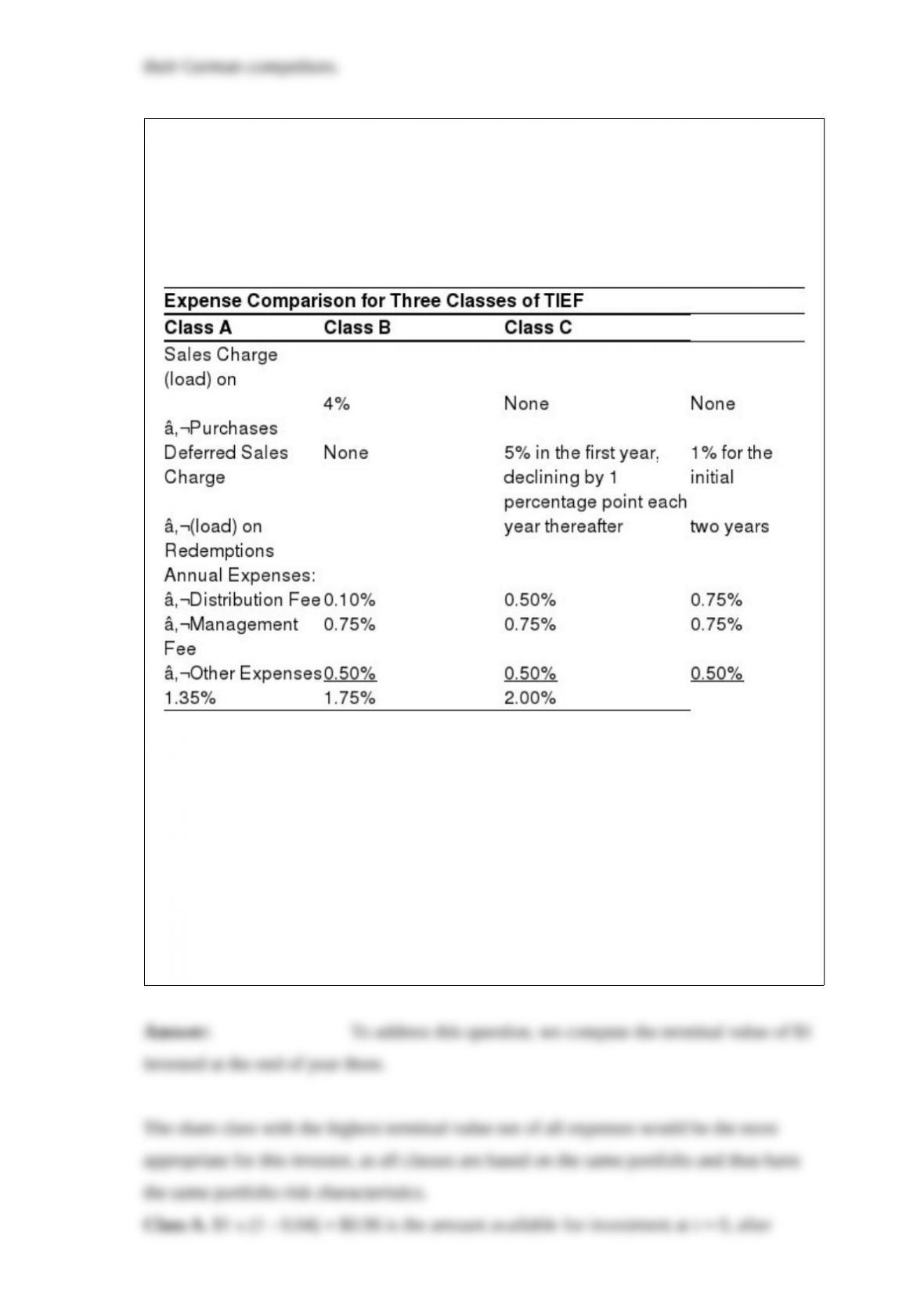

An investor is considering the purchase of Tata International Equity Fund (TIEF) for his

portfolio. Like many U.S.-based mutual funds today, TIEF has more than one class of

shares. Although all classes hold the same portfolio of securities, each class has a

different expense structure. This particular mutual fund has three classes of shares: A,

B, and C. The expenses of these classes are summarized in the following table:

The time horizon associated with the investor’s objective in purchasing TIEF is three

years; he decides to specify it as just over three years. He expects equity investments

with risk characteristics similar to TIEF to earn 10% per year, and he decides to make

his selection of fund share class based on an assumed 10% return each year, gross of

any of the expenses given in the table above.

Based on only the above information, determine the class of shares that is most

appropriate for this investor. Assume that expense percentages given will be constant at

the given values. Assume that the deferred sales charges are computed on the basis of

net asset value (NAV).

If the average premium on gold call options declines, does this mean that they are

becoming undervalued and, therefore, should be bought? Using valuation models, give

at least two possible reasons for this decline.

A Japanese investor holds a portfolio of British stocks worth 10 million. The current

three-month dollar/pound forward exchange rate is = 1.65, and the current

three-month yen/dollar forward exchange rate is = 100. What position should the

Japanese investor take to hedge the pound/yen exchange risk?

You visit the foreign exchange trading room of a major bank. A trader asks for

quotations of the British pound from various correspondents and hears the following

quotes:

From Bank A: 1.6580-1.6585

From Bank B: 1.6582-1.6587

What do they mean?

Assume that you are an international bank that has lent money to some Latin American

countries. Because of the nonpayment of interest due, you have already taken

substantial reserves against these nonperforming loans. Why would you be willing to

exchange these loans for Brady bonds?

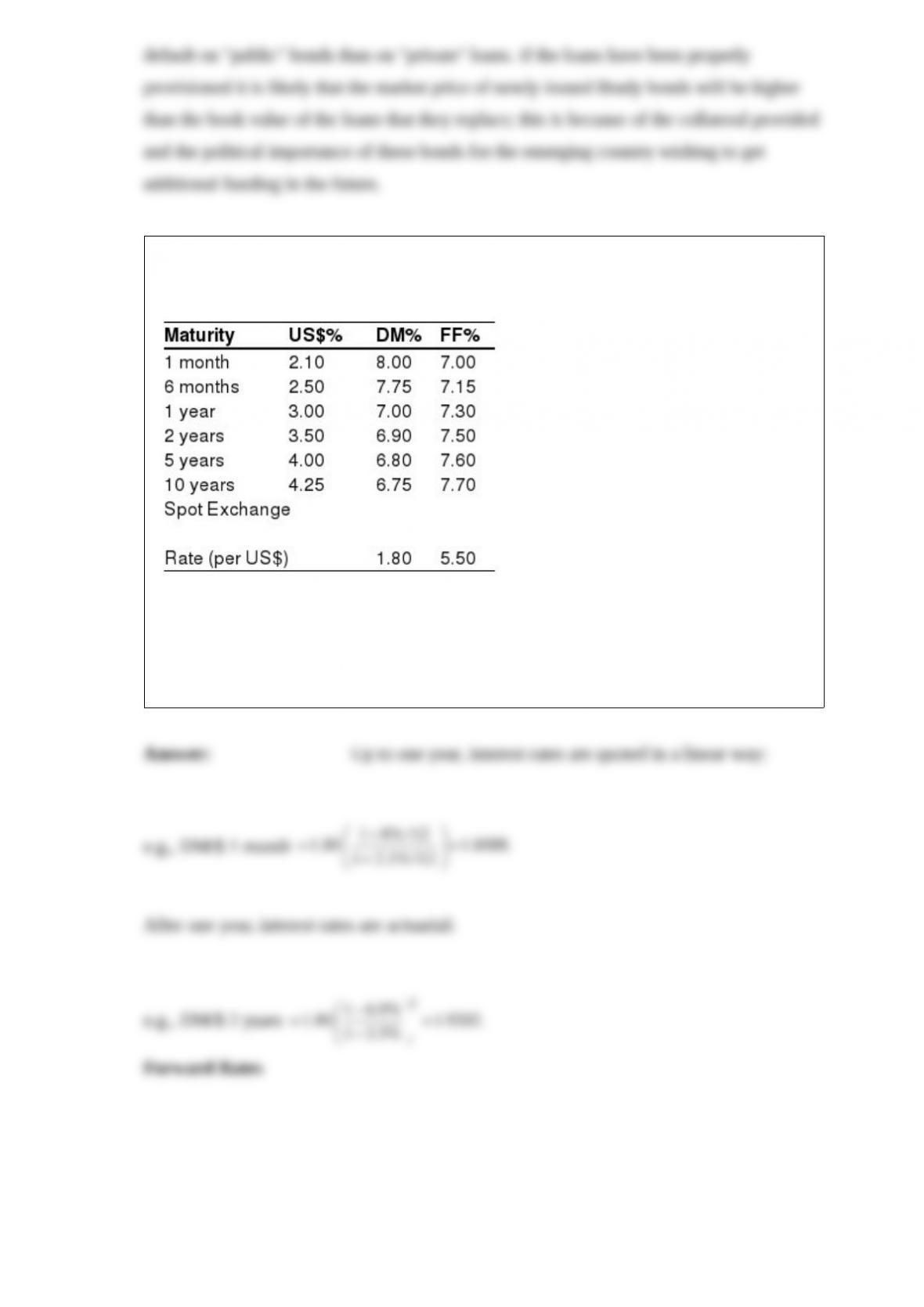

Several years ago, when the Deutsche mark and French franc still existed, the yield

curves were as follows:

Calculate the implied forward exchange rates, assuming that the interest rates are

international money rates (linear convention) for maturities of less than a year and

yields on zero-coupon bonds (European convention) for maturities of more than one

year.