The Japanese stock market has a sigma of 18%, when computed in yen. The U.S. stock

market has a sigma of 17% in US$ and the US exchange rate has a sigma of 6%. The

correlation between the Japanese stock market and currency movements is -0.1; in other

words, the Japanese stock market tends to go up when the yen goes down. The

correlation between the Japanese and U.S.

stock markets is equal to 0.4, measured either in local currency of in dollars.

a. What is the sigma of the Japanese market when expressed in dollars?

b. Using this number, calculate the sigma, in dollars, of a portfolio made up of 50% of

Japanese stocks and 50% of U.S. stocks.

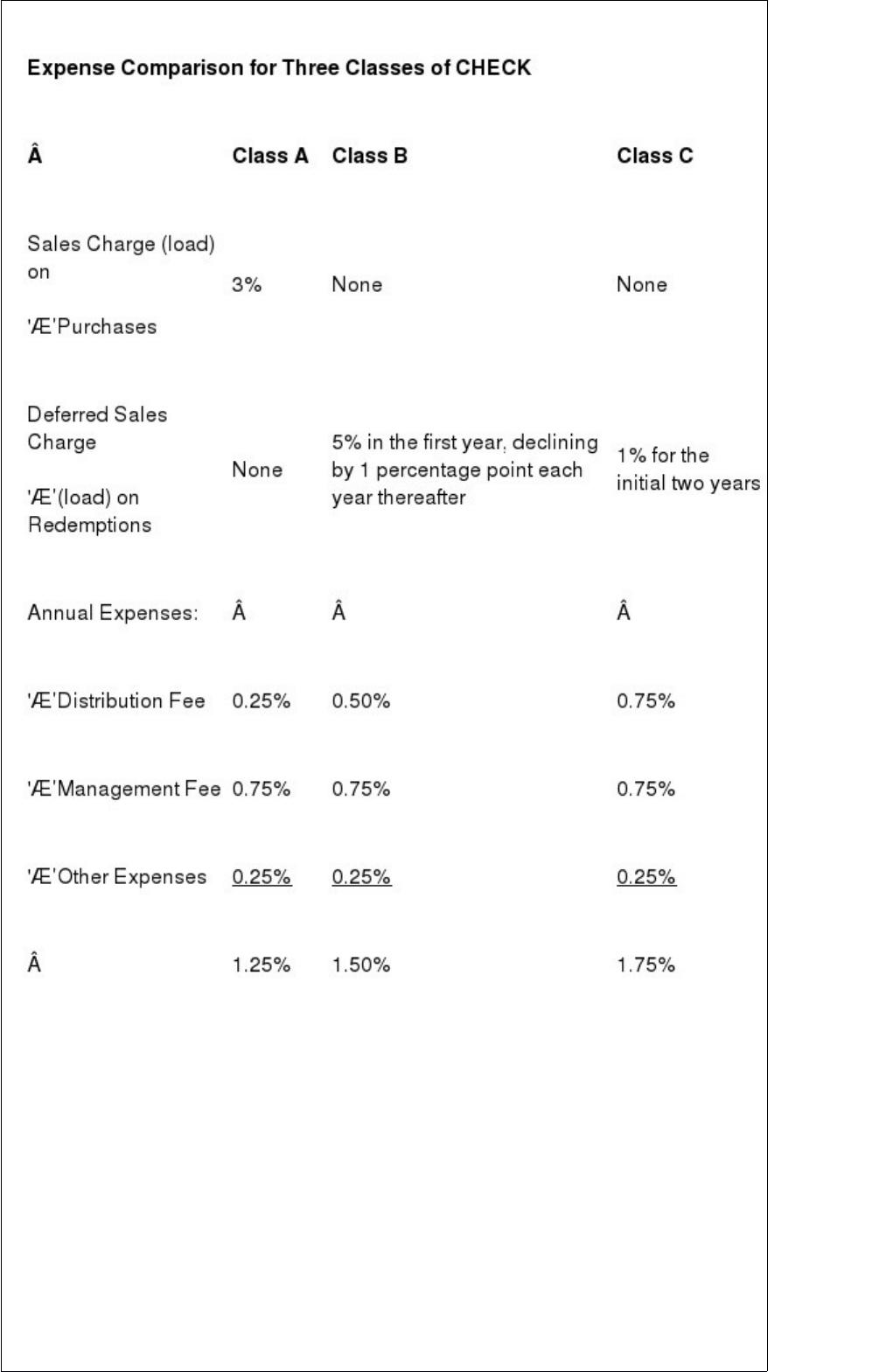

An investor is considering the purchase of CHECK Fund for his portfolio. Like many

U.S.-based mutual funds today, CHECK has more than one class of shares. Although all

classes hold the same portfolio of securities, each class has a different expense

structure. This particular mutual fund

has three classes of shares: A, B, and C. The expenses of these classes are summarized

in the following table:

The time horizon associated with the investor’s objective in purchasing CHECK is five

years. He expects equity investments with risk characteristics similar to CHECK to earn

8% per year, and he decides to make his selection of fund share class based on an

assumed 8% return each year, gross of any of the expenses given in the table above.

a. Based on only the above information, determine the class of shares that is most

appropriate for this investor. Assume that expense percentages given will be constant at

the given values. Assume that the deferred sales charges are computed on the basis of

NAV.

b. Suppose that, as a result of an unforeseen liquidity need, the investor needs to

liquidate his investment at the end of the first year. Assume an 8% rate of return has

been earned. Determine the relative performance of the three fund classes, and interpret

the results.

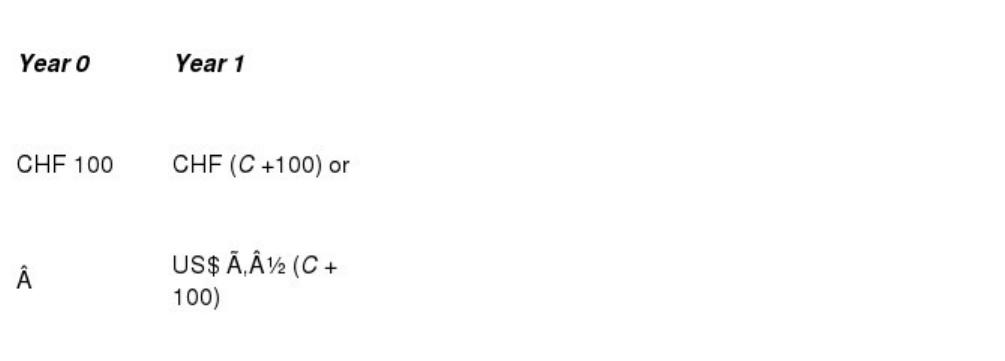

A company is deciding whether to issue a one-year dual-currency bond or a one-year

currency option bond.

·The dual-currency bond would be issued in CHF (Swiss francs) with a principal of

100 CHF per bond, with interest payable in CHF and principal repaid in U.S. dollars

($50). Denote x the interest at which this bond is issued.

·The currency option bond is issued in CHF (100 CHF), and the interest and principal

are repaid in CHF or $ at the option of the bondholder. The principal repaid is either

100 CHF or $50, and the interest rate is either y CHF or 1/2y dollars.

As you guessed, the current spot exchange rate is 2 CHF/$. The current one-year market

interest rates are 6% in CHF and 10% in $. One-year currency options are quoted in

Chicago. A put CHF is quoted at 1.2 U.S. cents per CHF; this option premium is for one

CHF, with a strike price of 50 U.S. cents.

a. What is the fair interest rate x on the dual-currency bond?

b. What is the fair interest rate y on the currency option bond?

An Italian investor owns a portfolio of South Korean stocks worth 1.25 billion won.

The current spot and one-month forward exchange rates are 1,250 won/ (one won =

0.0008 euro). Interest rates are equal in both countries. You are worried that some

rumor about the bankruptcy of a major local bank could lead to a strong depreciation of

the won. You have observed that Korean stocks tend to react negatively to a

depreciation of the local currency (won). A broker tells you that a regression of Korean

stock returns (measured in won) on the /won percentage exchange rate movements has

a slope of +0.50. In other words, Korean stocks tend to go down by 0.5% when the won

depreciates

by 1%.

a. Discuss what your currency hedge ratio should be.

b. A month later, your Korean stock portfolio has gone down to 1.1875 billion won and

the spot and forward exchange rates are now 0.00072 /won. Analyze the return on

your hedged portfolio.

Exchange traded funds (ETFs) are usually considered to have many interesting

properties. In the list below, indicate which statements DO NOT apply to ETFs:

a. ETFs allow to invest in a diversified portfolio.

b. ETFs are cost effective.

c. ETFs will never drop in value.

d. ETFs benefit from some attractive tax characteristics.

e. ETFs can be traded at any time during market opening.

f. ETFs are designed to take advantage of the manager’s stock picking ability.

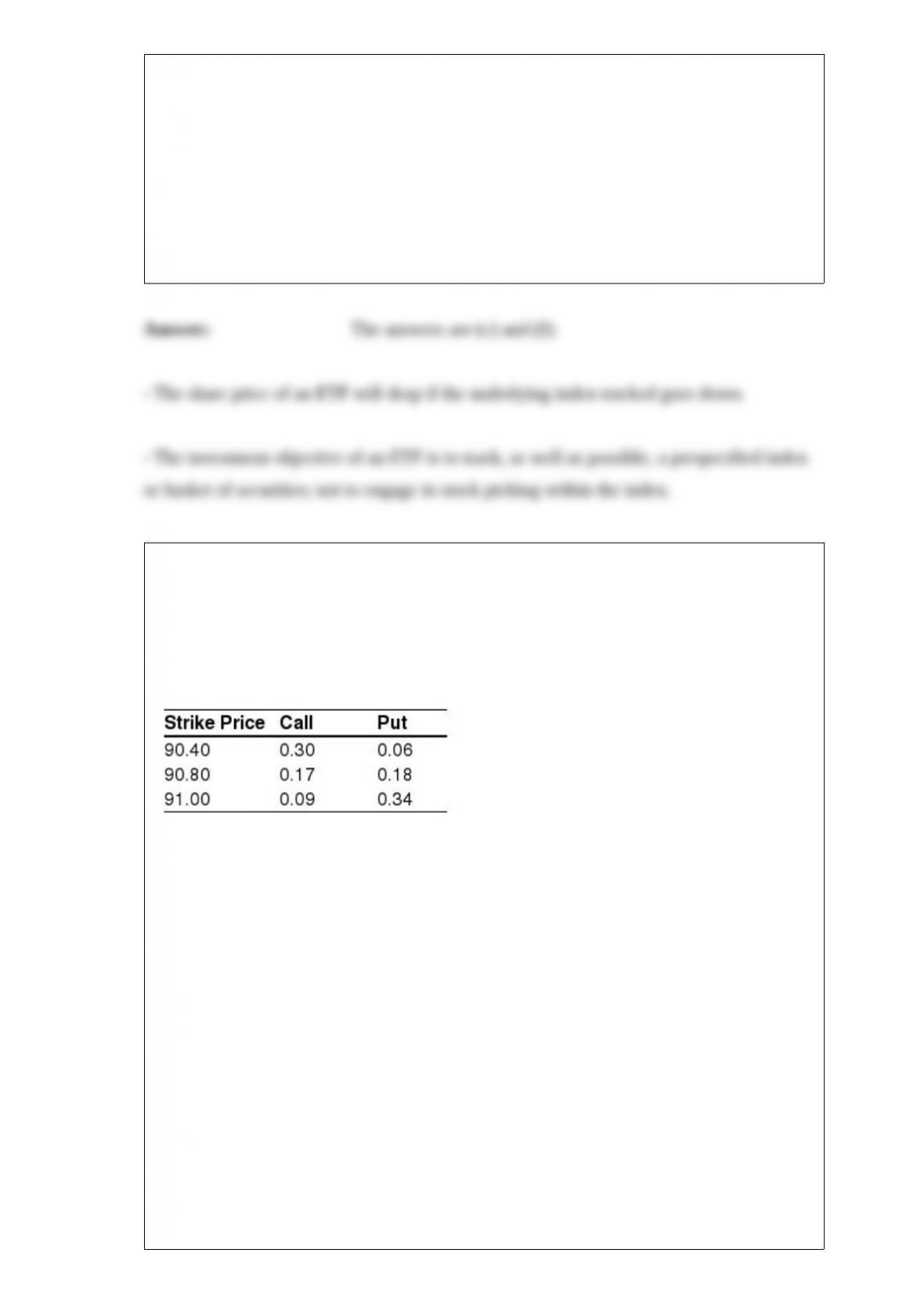

The French futures market, MATIF, trades Euribor contracts. The Euribor is the

three-month interbank interest rate on euros. The contract size is €1 million, and the

margin is €3,000. On

January 10, March futures trade at 90.74%. Options on the Euribor futures contract are

also listed. The premiums (in %) on March options are as follows:

A few days later (January 14), the futures price moves to 89.50.

a. What is the gain or loss, in euros, for someone who sold a futures contract on January

10?

b. What is the return, as a percentage of the initial investment (margin)?

c. Are all option premiums quoted on January 10 reasonable?

d. You know that you will have to borrow ¬10 million in March and fear a rise in

interest rates. What are the maximum borrowing rates that you can insure using the

various options?

e. To cap your borrowing rate, you decide to use options with a strike price of 90.80.

How many calls (or puts) should you buy (or sell)?

On January 14, the premium on the call March 90.80 moves to 0.02, and the premium

on the put March 90.80 moves to 1.33.

f. What is the ¬ profit (or loss) on your option position?

g. What is the rate of return on your option position?

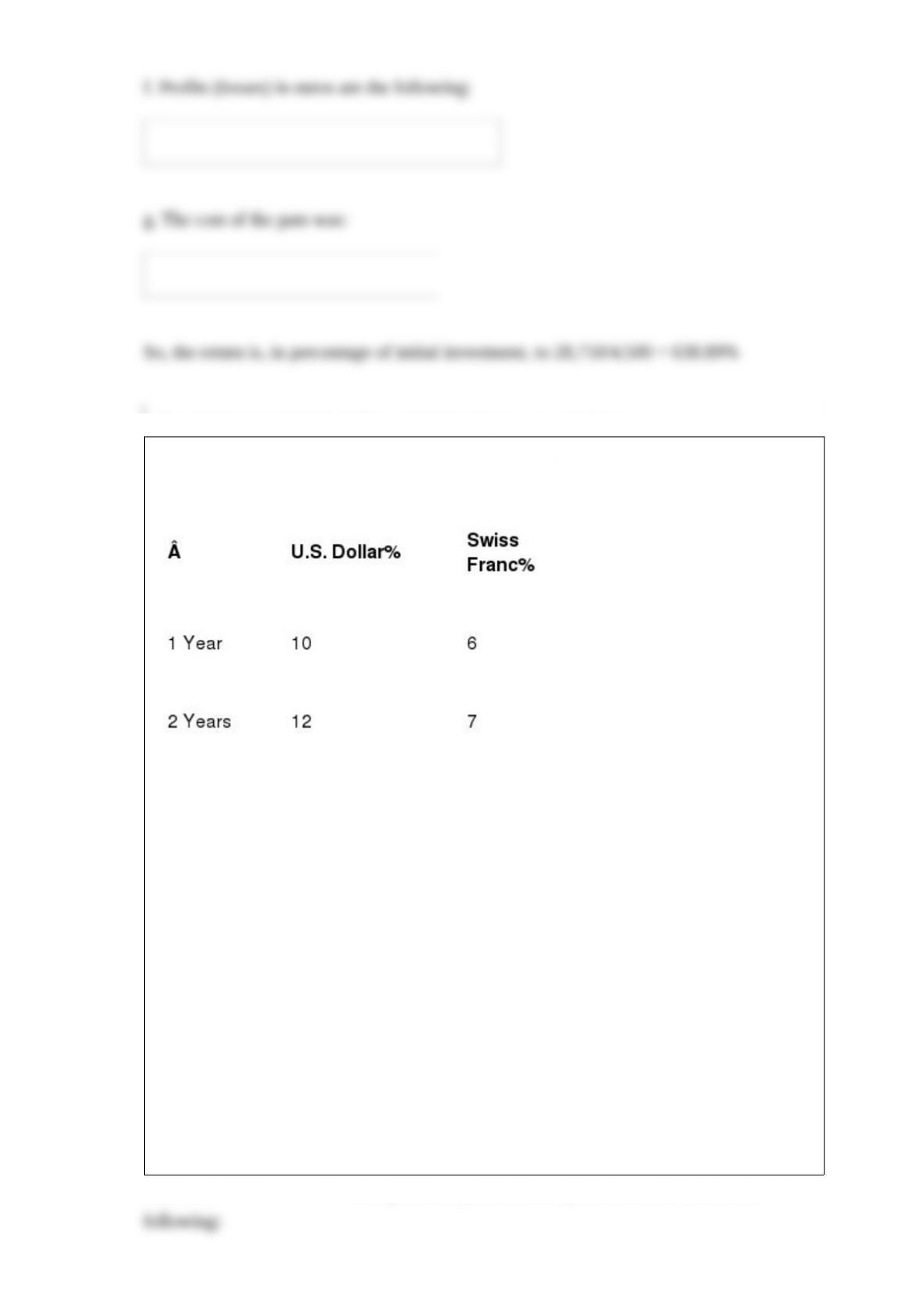

The yield curves in U.S. dollars and Swiss francs are as follows:

These are yields for zero-coupon bonds of one- and two-year maturities. The spot

exchange rate is SF/$ = 1.5.

a. What are the implied one-year and two-year forward exchange rates?

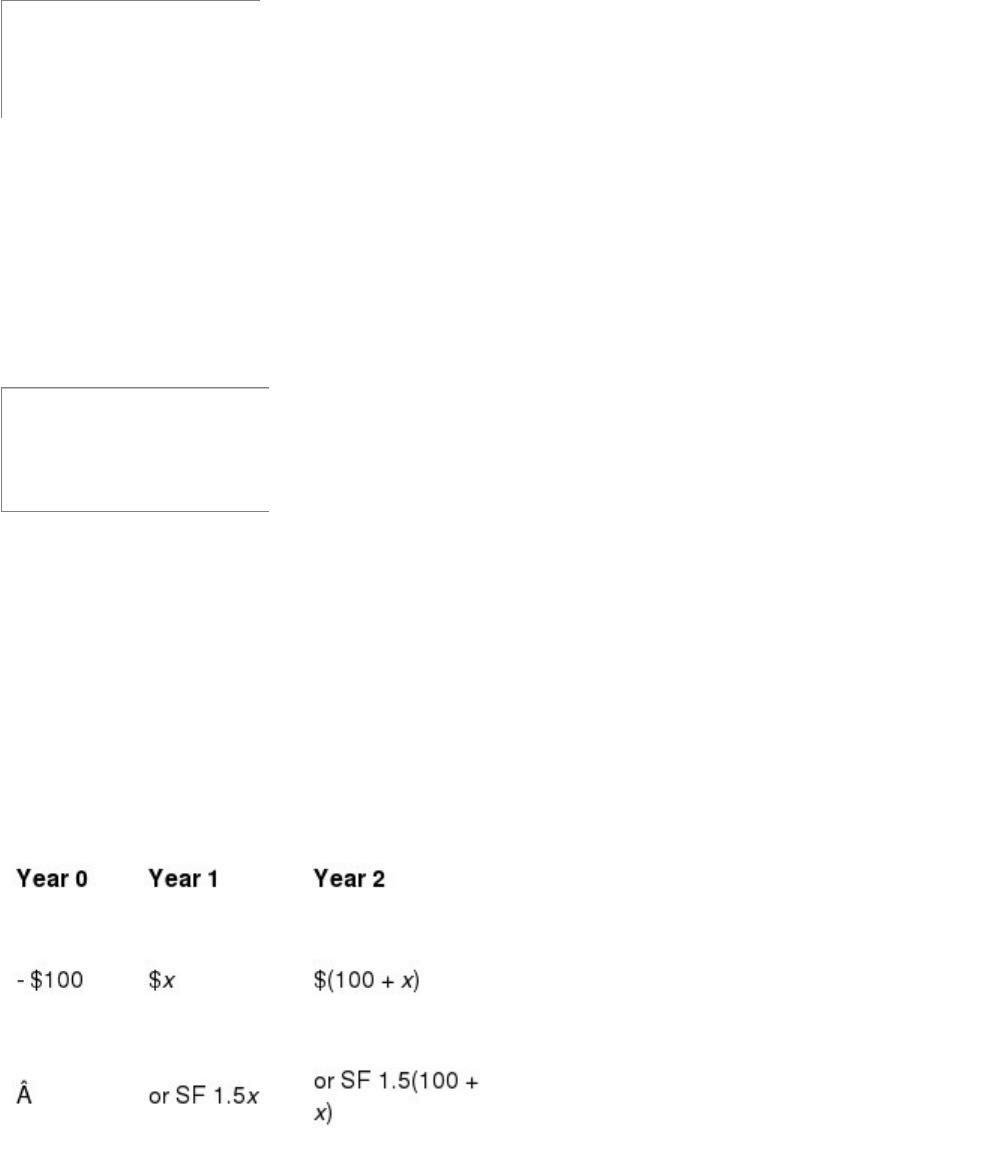

b. You contemplate issuing a dual-currency bond. You could issue zero-coupon bonds in

both currencies at the interest rates above. Instead, you wish to issue bonds of SF 150

with a coupon C in Swiss francs, paid each year for two years, and reimbursed for $100

at the end of two years. What is the interest rate c% (c = C/150) on the bond that would

be consistent with the yield curves above?

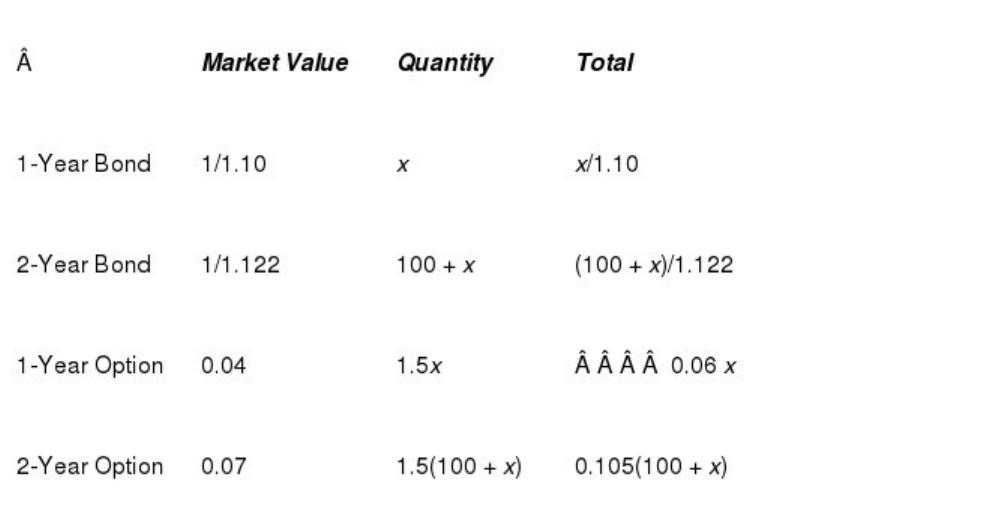

c. You contemplate issuing a two-year currency option bond. The bond is issued for

$100 and gives the option to receive the coupons and principal payment in either dollars

or Swiss francs at a fixed exchange rate of SF/$51.5. A bank gives you quotes on the

premiums for SF calls with a strike price of 1/1.5 = 0.66666 US$. The premium for a

one-year call is 4 U.S. cents (per Swiss franc) and for a two-year call is 7 U.S. cents.

What coupon rate should you set on your currency option bond?

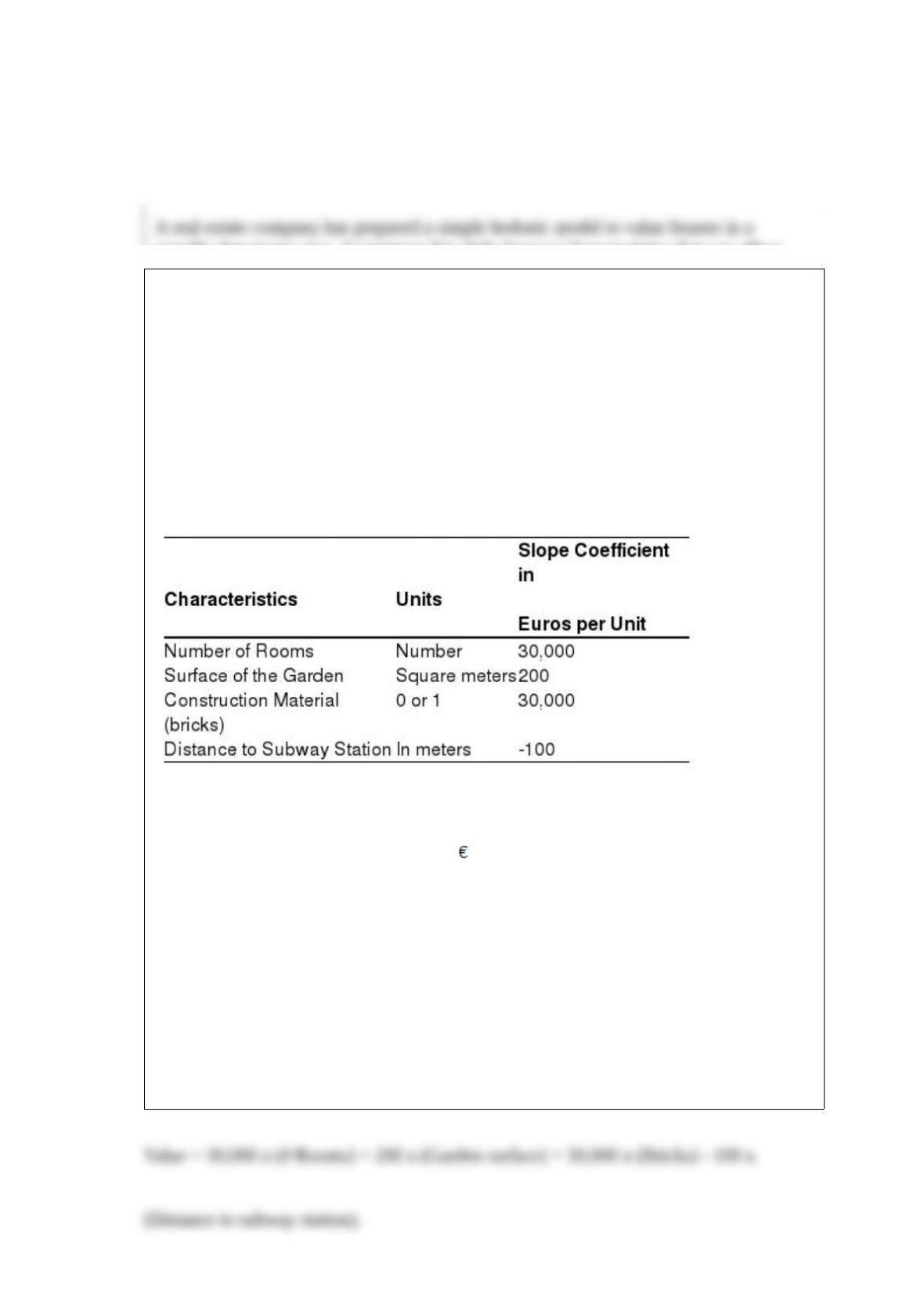

A real estate company has prepared a simple hedonic model to value houses in a

specific downtown area. A summary list of the houses’ characteristics that can affect

pricing are:

– The number of main rooms.

– The surface of the garden (if any).

– The construction material (wood or brick).

– The distance to a subway station.

A detailed statistical analysis of a large number of recent transactions in the area

allowed to derive the following slope coefficients:

A typical house in the area has 5 main rooms, a garden of 500 square meters,

constructed with bricks, and a distance of 300 meters to the nearest subway station. The

transaction price for a typical house was 250,000.

a. You wish to value a house that has 7 rooms, a small garden of 100 square meters,

constructed in wood, and a distance of 100 meters to the nearest subway station. What

is the appraisal value based on this sales comparison approach of hedonistic price

estimation?

b. You wish to value a house that has 7 rooms, a garden of 1,000 square meters,

constructed in brick, and a distance of 1 kilometer to the nearest subway station. What

is the appraisal value based on this sales comparison approach of hedonistic price

estimation?

In 1993 Daimler-Benz became the first German company to be listed on the New York

Stock Exchange (NYSE). This forced Daimler-Benz to file a reconciliation statement

with U.S. GAAP (Form 20-F). Because Daimler-Benz drew on hidden reserves during

the recession of 1993, its German-reported profit (in Deutsche mark or DM) was a

small, but positive, DM615 million. It translated into a DM1.84 billion loss according

to U.S. GAAP. Daimler’s 1993 net worth translates from DM18.15 billion under

German rules to DM26.28 billion under U.S. GAAP.

a. Explain what happened on earnings.

b. Explain what happened on book value (net worth).

c. In a profitable year, Daimler-Benz decides to increase its hidden reserves. How

would this decision affect earnings calculated according to U.S. and German GAAP?

d. Same question for book value.

A nine-year bond has a yield-to-maturity of 10% and a modified duration of 6.54 years.

If the market yield changes by 50 basis points, the bond’s expected price change is:

a. 3.27%

b. 3.66%

c. 5.00%

d. 6.54%

In Hong Kong, the size of a futures contract on the Hang Seng stock index is HK $50

times the index. The margin (initial and maintenance) is set at HK $32,500. You predict

a drop in the Hong Kong stock market following some economic problems in China

and decide to sell one June futures contract on April 1. The current futures price is

7,200. The contract expires on the second-to-last business day of the delivery month

(expiration date: June 27). Today is April 1, and the current spot value of the stock

market index is 7,140.

a. Why is the spot value of the index lower than the futures value of the index?

b. Indicate the cash flows that affect your position if the following prices are

subsequently observed:

What are the major determinants of the value of a currency option (call and put)?

a. Briefly justify each determinant and its direction.

b. What is the relation between a currency put and a currency call (put€call parity)?

c. In what circumstances would an American-type option be exercised before

expiration?

(You may provide an example to illustrate your answers.)

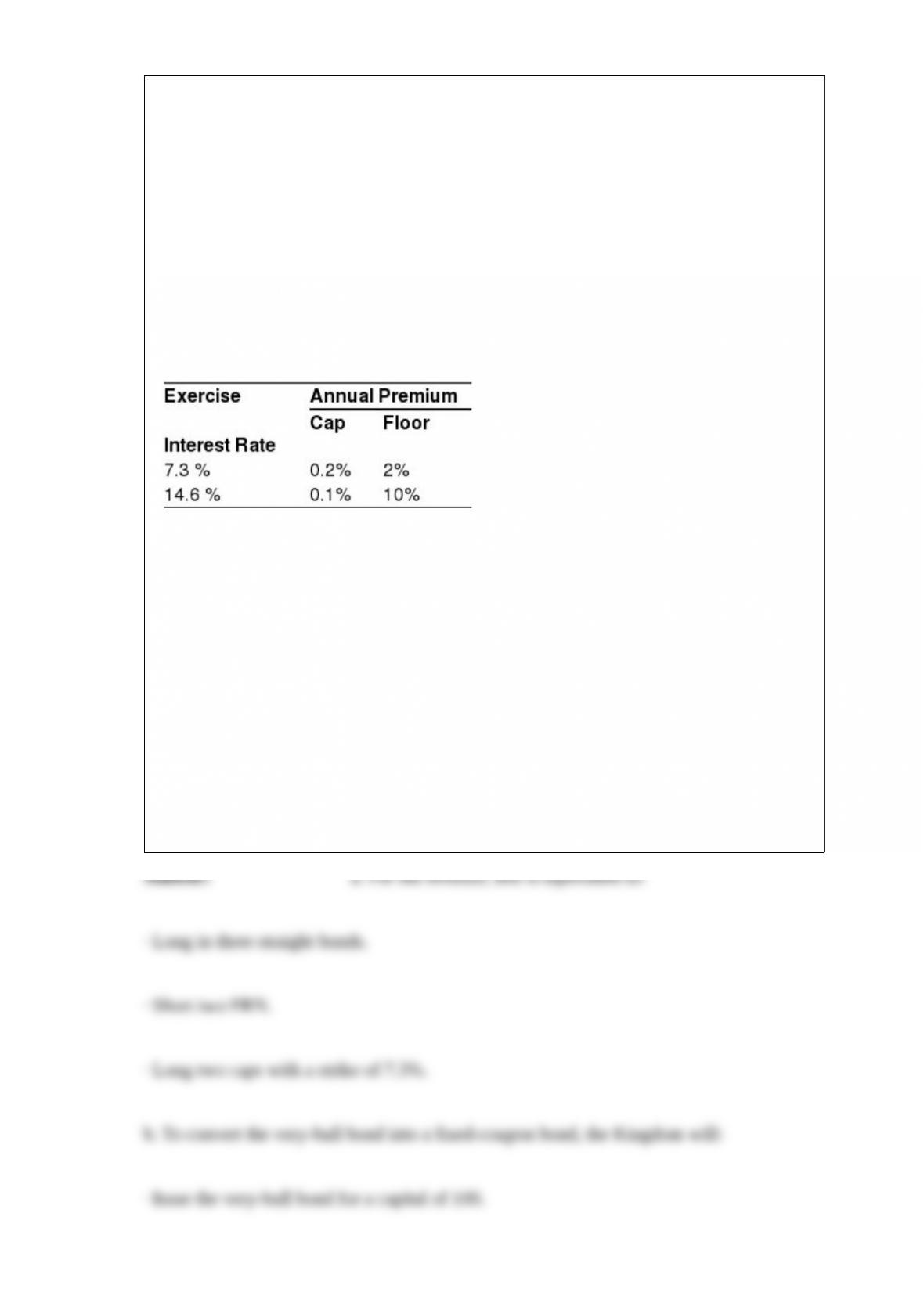

The Kingdom of Papou issues a very-bull bond with a coupon equal to:

14.6 – 2 x LIBOR.

Of course, the coupon cannot be negative.

The Kingdom could have issued a FRN at LIBOR + ¼%, or a straight bond at 5.30%.

The current market conditions for swaps are 5% against LIBOR.

You could also trade in CAPS and FLOORS with different exercise prices (these are

levels of interest rates). The premiums are paid annually.

a. You are a buyer of this very-bull bond. Tell us what it is equivalent to, in terms of

buying/selling: FRN, straight bonds, caps or floors?

b. Assume that the Kingdom actually wanted to issue a straight bond (fixed coupon).

The bank will put in place a “de-mining” portfolio with swaps and options so that this

very-bull bond plus the “de-mining” portfolio is equivalent to a straight bond. What is

exactly the “de-mining” portfolio? [Be very precise and tell us if the Kingdom must pay

fixed, receive LIBOR or vice versa, etc. …]

c. What is the cost advantage for the Kingdom compared to issuing bonds @ 5.30 %?

d. Same question assuming that the Kingdom wanted to issue an FRN @LIBOR + ¼

%?

The interest rate on one-year risk-free bonds is 5% in the United Kingdom, and 75% in

Switzerland. The current exchange rate is 0.5 per Swiss franc. Suppose that you are a

British investor and you expect the Swiss franc to appreciate by 2% over the next year.

a. Calculate the foreign currency risk premium.

b. Calculate the domestic currency return on the foreign bond, assuming that your

currency appreciation expectations are met.

A Turkish clothing company is buying material in Mexico. It needs to pay 1 million

Mexican pesos. The exchange rates published in a local newspaper are as follows:

· One U.S. dollar is worth 1356 Turkish liras.

· One U.S. dollar is worth 129.64 Mexican pesos.

The Turkish company calls its local banker, who advises that it needs to do two foreign

exchange transactions: One selling liras to buy dollars, and the other buying pesos with

these dollars. The company is surprised that its banker does not engage directly in a

single transaction from liras to pesos. Why would the bid-ask spread be much larger on

the lira/peso transaction than the sum of the bid-ask spread of the two lira/dollar and

peso/dollar transactions?

A company can generate an return on equity (ROE) of 12% and has an earnings

retention ratio of 0.80. Next year’s earnings are projected at 100 million. If the

required rate of return for the company is 10%, what is the company’s tangible P/E

value, franchise factor, growth factor, and franchise

P/E value?

There are several ETFs listed on the American Stock Exchange (AMEX). One of them

is iShares-Switzerland. This ETF tracks the Morgan Stanley Capital International (

The currencies of several emerging countries depreciate at a rapid pace. Does it imply

that you should not invest in their stock markets? For example, the Polish zloty went

from 15,767 to 21,444 zlotys per U.S. dollar in 1993. The Polish stock market went

from 1,040 to 12,439 during the same period. Guess why the zloty depreciated.

Let’s consider a Swiss franc futures contract traded in the United States. On February 18

(a Friday), the March contract closedat 0.7049 dollar per Swiss franc. The size of the

contract is 125,000 Swiss francs. The initial margin is $2,600 per contract and the

maintenance margin is $1,600. Assume that you buy one March contract on February

19 at 0.7049 $/SFr and you deposit, in cash, an initial margin of $2,600. Listed below

are the futures quotations (settlement prices) observed on three successive days:

What are the cash flows associated with the marking-to-market procedure?

Give at least two reasons why Eurobonds are issued in bearer form.

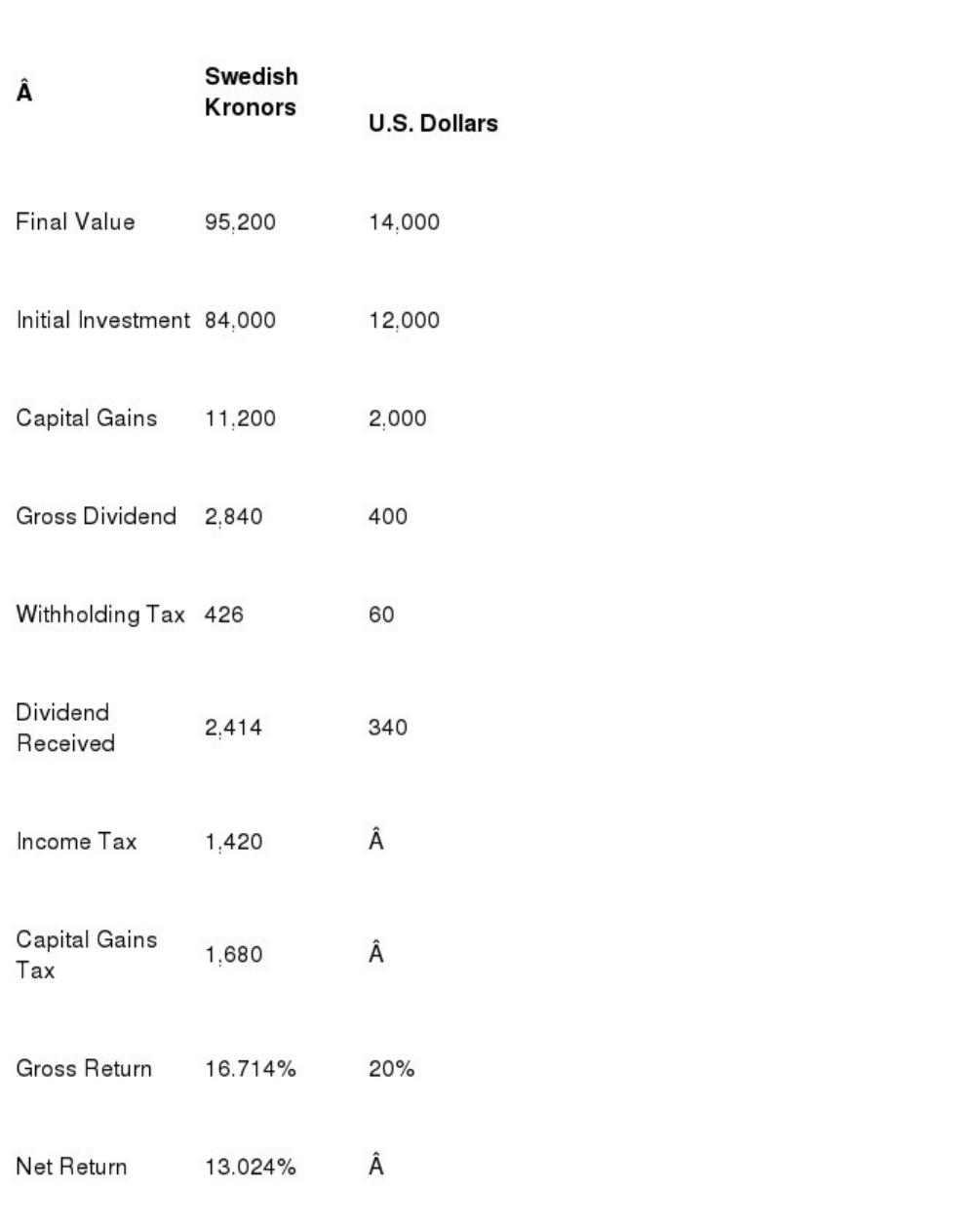

A Swedish investor bought 100 shares of IBM on January 1 on the New York Stock

Exchange at 120. The exchange rate was SEK/USD = 7.00. Over the year, the

investor has received a gross dividend of 4 per share; the net dividend received is

3.4 because of a 15% withholding tax levied by the United States. The exchange rate at

the time of dividend payment was SEK/USD = 7.1.

By December 31, the investor resells the IBM shares at 140, but the exchange rate has

dropped suddenly to SEK/USD = 6.8. Ignoring commissions, what is the rate of return

on the investment, in dollars and kronas, gross and net of taxes? The Swedish investor

is taxed at 50% on income and 15% on capital gains; the U.S. withholding tax can be

used as a tax credit in Sweden.

Consider an asset that has a beta of 20. If the risk-free rate is 3.5% and the market risk

premium

is 3%, calculate the expected return on the asset.