Which of the following is an example of an artificially scarce good?

A) diamonds, because their supply is artificially restricted by monopoly producers

B) music that is downloadable from the Internet for a fee

C) a daily newspaper

D) hot dogs in a sports stadium, because the number of suppliers is restricted

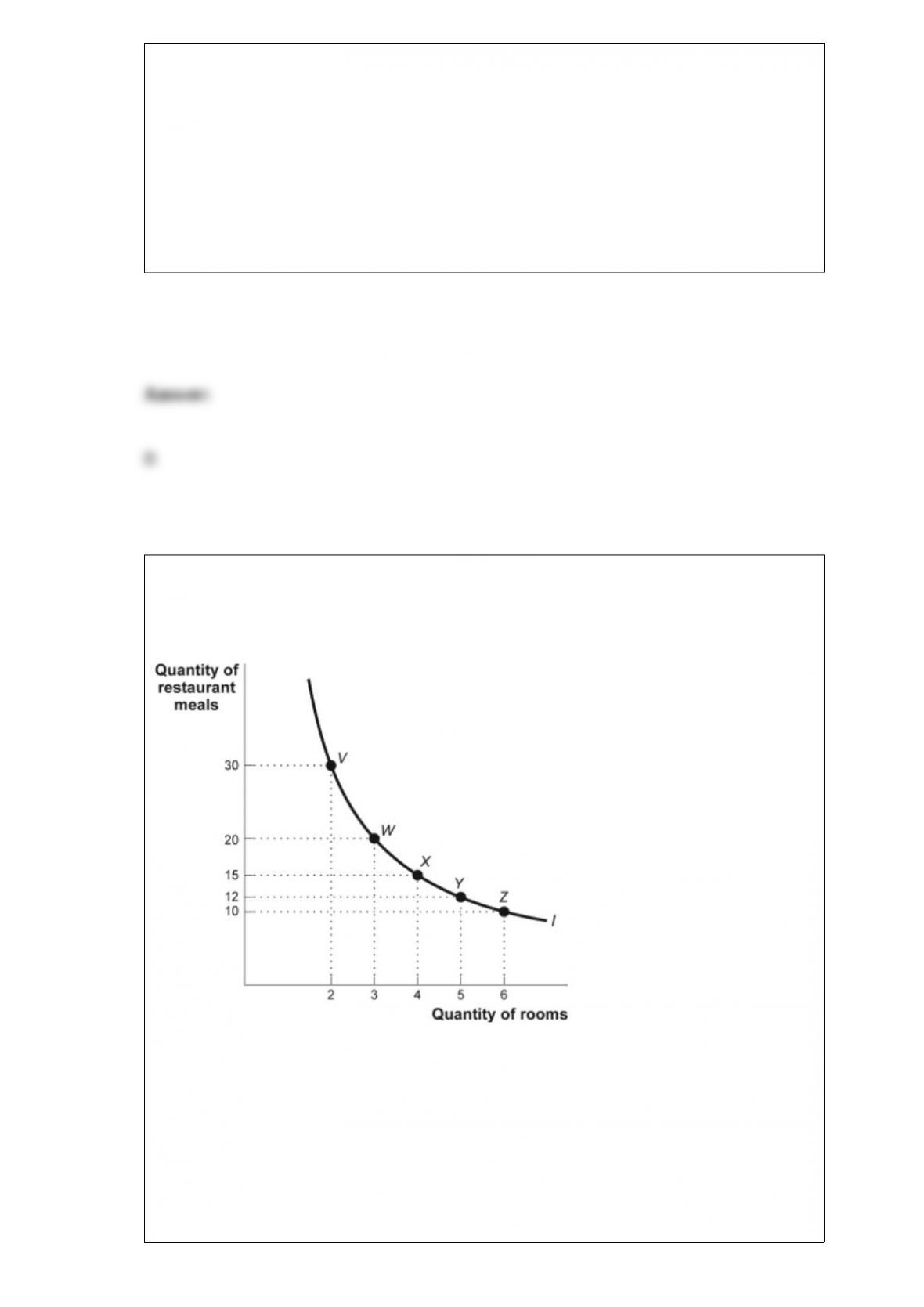

Figure and Table: The Changing Slope of an Indifference Curve

(Figure and Table: The Changing Slope of an Indifference Curve) Look at the figure

and table The Changing Slope of an Indifference Curve. The slope between points X

and Y is:

A) 3.

B) “5.

C) “0.33.

D) “3.

If the price of a cookie is $1 and the price of a brownie is $2, the price of cookies in

terms of brownies is:

A) 0.5.

B) 1.0.

C) 2.0.

D) undefined.

The total consumer surplus for good X can be calculated in all ways EXCEPT as:

A) the sum of the individual consumer surpluses for all buyers of X.

B) the area below the demand curve for X and above the price of X.

C) the area bounded by the demand curve for X and the two axes.

D) the sum, for all buyers of X, of the difference between what each buyer is willing to

pay for X and the amount actually paid.

In a perfectly competitive industry, the market demand curve is usually:

A) perfectly inelastic.

B) perfectly elastic.

C) downward-sloping.

D) relatively elastic.

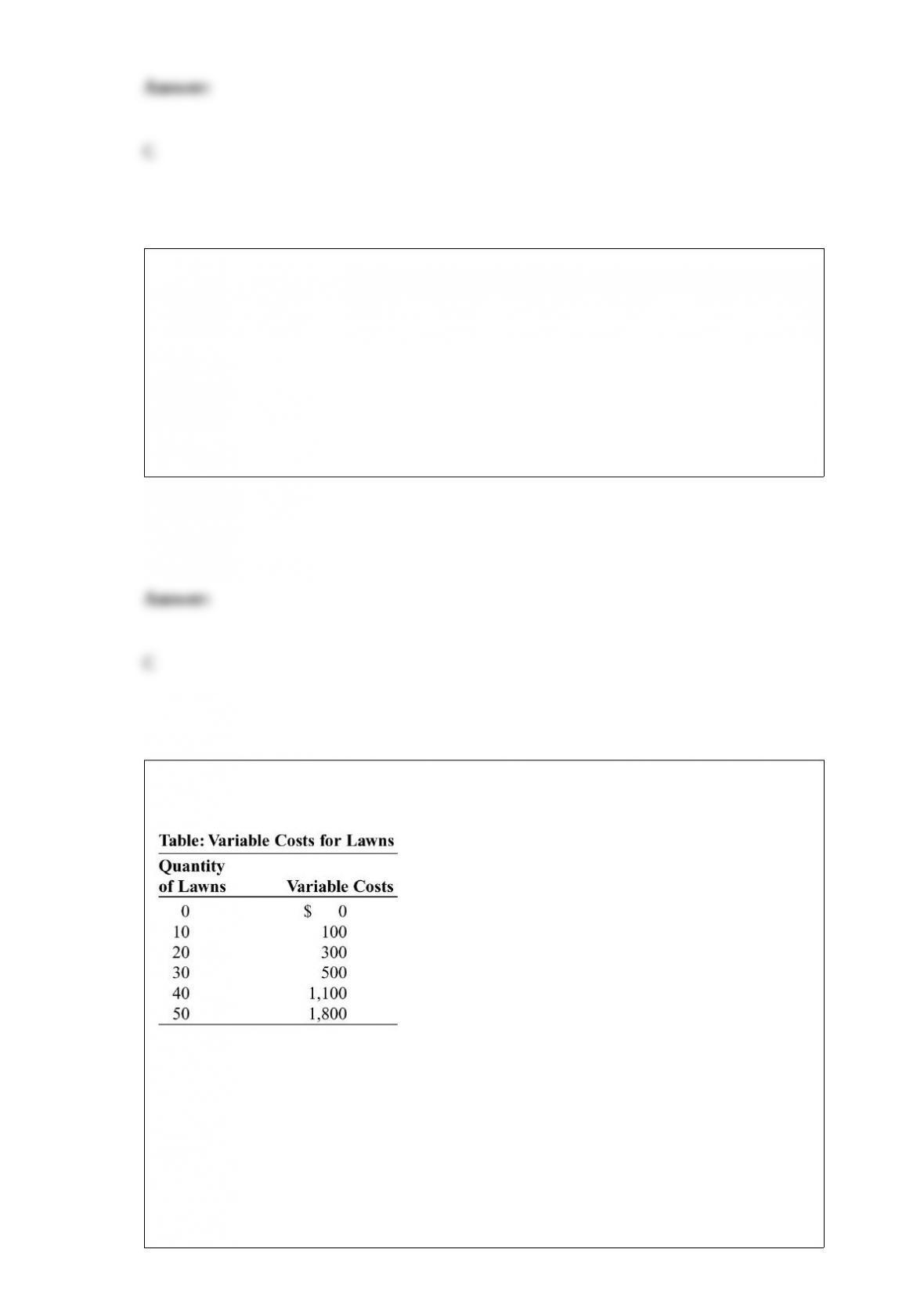

(Table: Variable Costs for Lawns) Look at the table Variable Costs for Lawns. During

the summer, Alex runs a lawn-mowing service, and lawn-mowing is a perfectly

competitive industry. Assume that costs are constant in each interval; that is, the

variable cost of mowing 1 through 10 lawns is $100. His only fixed cost is $1,000 for

the mower. His variable costs include fuel, his time, and mower parts. If the price for

mowing a lawn is $70, how much is Alex’s profit per unit at the profit-maximizing

output?

A) “$10

B) $10

C) $34

D) $14

If there is a 25% probability that Joseph will earn $10 per hour at his job today and a

75% probability that he will earn $20 per hour today, his expected pay per hour is:

A) $10.00.

B) $15.00.

C) $17.50.

D) $20.00.

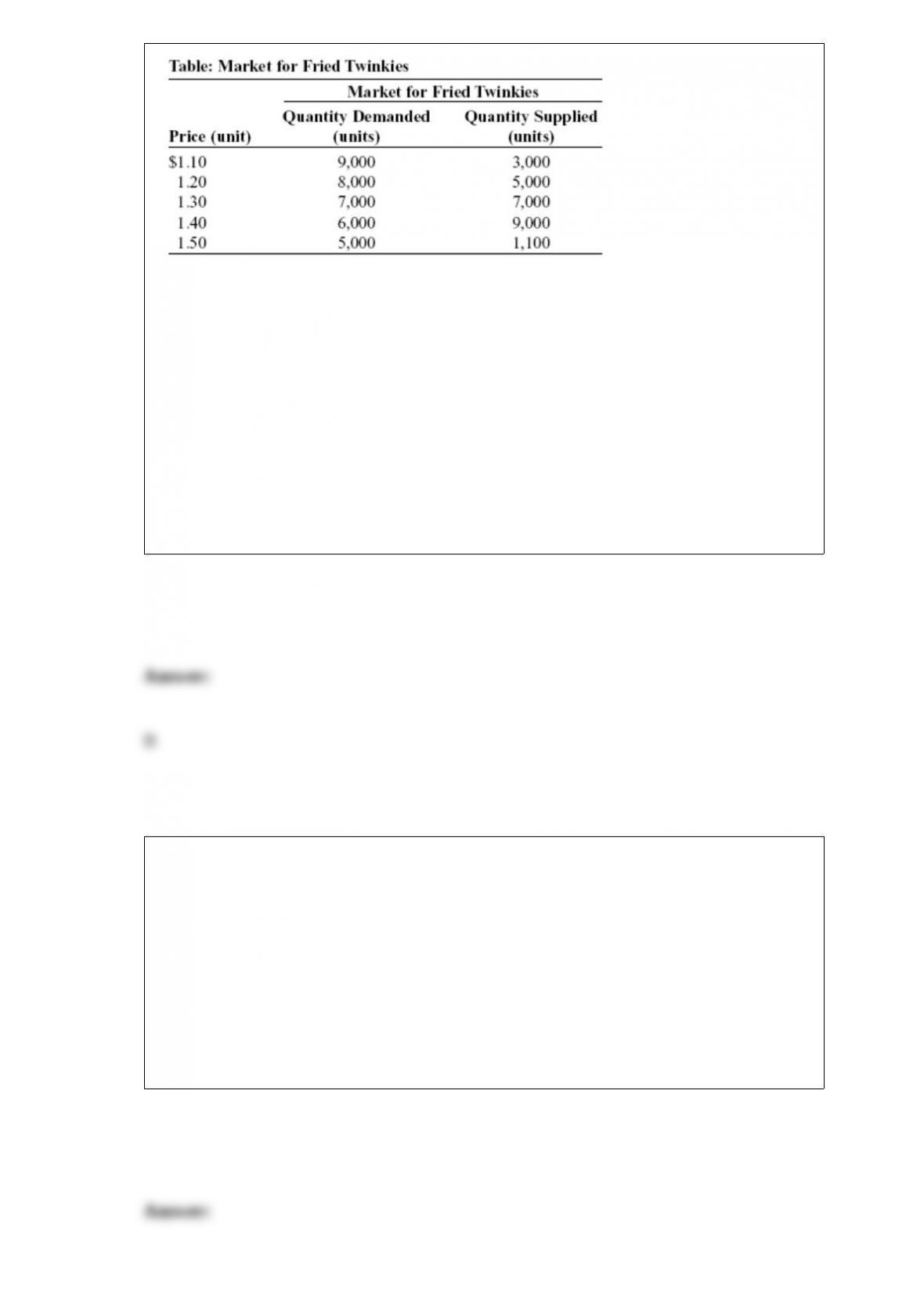

(Table: Market for Fried Twinkies) Look at the table Market for Fried Twinkies. If the

government imposes a quota of 5,000 on the fried Twinkie market, the quota rent per

fried Twinkie will be:

A) $1.20.

B) $0.30.

C) $1.50.

D) $1.00.

The pair of items that is likely to have the largest positive cross-price elasticity of

demand is:

A) coffee and tea.

B) skis and ski boots.

C) pizza and pepperoni.

D) milk and cookies.

The Orlando, Florida, theme park industry tends to follow a price leadership model.

This means that:

A) each theme park sets its own price and operating hours independent of what other

parks do.

B) Disney often sets a price and rival theme parks then follow with similar if not

identical prices.

C) Disney often sets prices only to be undercut by rival firms who prefer to engage in

price wars.

D) firms use explicit written agreements to charge identical prices.

Diminishing marginal returns occur when:

A) each additional unit of a variable factor adds more to total output than the previous

unit.

B) each additional unit of a variable factor adds less to total output than the previous

unit.

C) the marginal product of a variable factor is increasing at a decreasing rate.

D) total product decreases.

In 2012, health care expenditures in the United States were approximately _____ per

person.

A) $500

B) $1,000

C) $9,000

D) $12,000

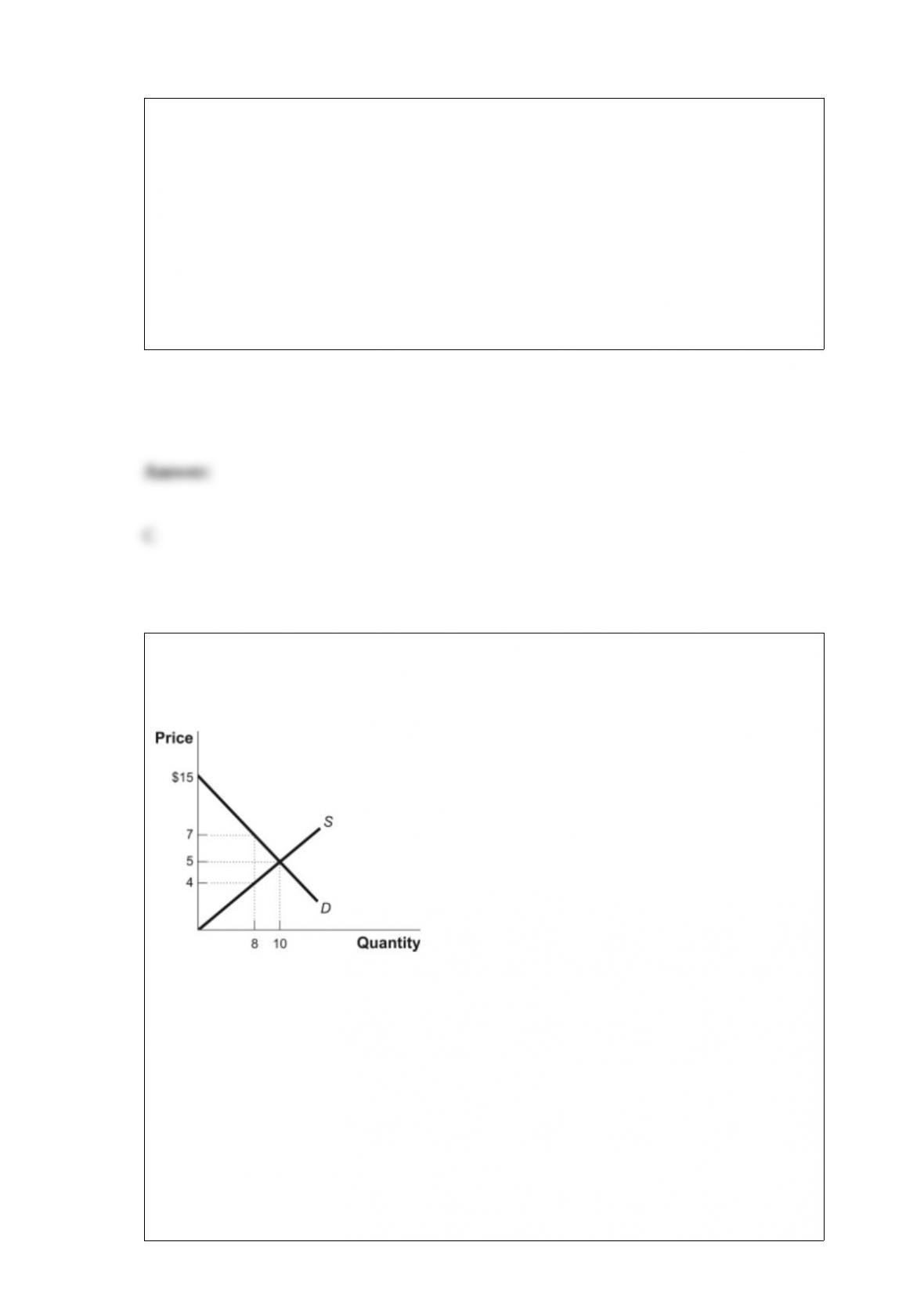

Figure: The Market for Sandwiches

(Figure: The Market for Sandwiches) Look at the figure The Market for Sandwiches. At

the competitive price of $5, 10 sandwiches are sold. At this competitive price, consumer

surplus equals _____ and producer surplus equals _____.

A) $50; $50

B) $100; $50

C) $50; $25

D) $100; $25

The profit-maximizing rule, expressed as _____, is adhered to by firms operating in a

market that is _____.

A) MC > MR; monopolistically competitive but not perfectly competitive

B) MC = MR; both monopolistically competitive and perfectly competitive

C) MC > MR; perfectly competitive but not monopolistically competitive

D) MC = MR; either monopolistically competitive or perfectly competitive, depending

on the costs of production

Scenario: Monopolistically Competitive Firm

For a monopolistically competitive firm, Q = 160 ” P; MC = 20 + 2Q; and TC = 20Q +

Q2 + 20.

(Scenario: Monopolistically Competitive Firm) Given the information in the scenario

Monopolistically Competitive Firm, what is the profit-maximizing level of output for

this firm in the short run?

A) 160 units

B) 20 units

C) 35 units

D) 180 units

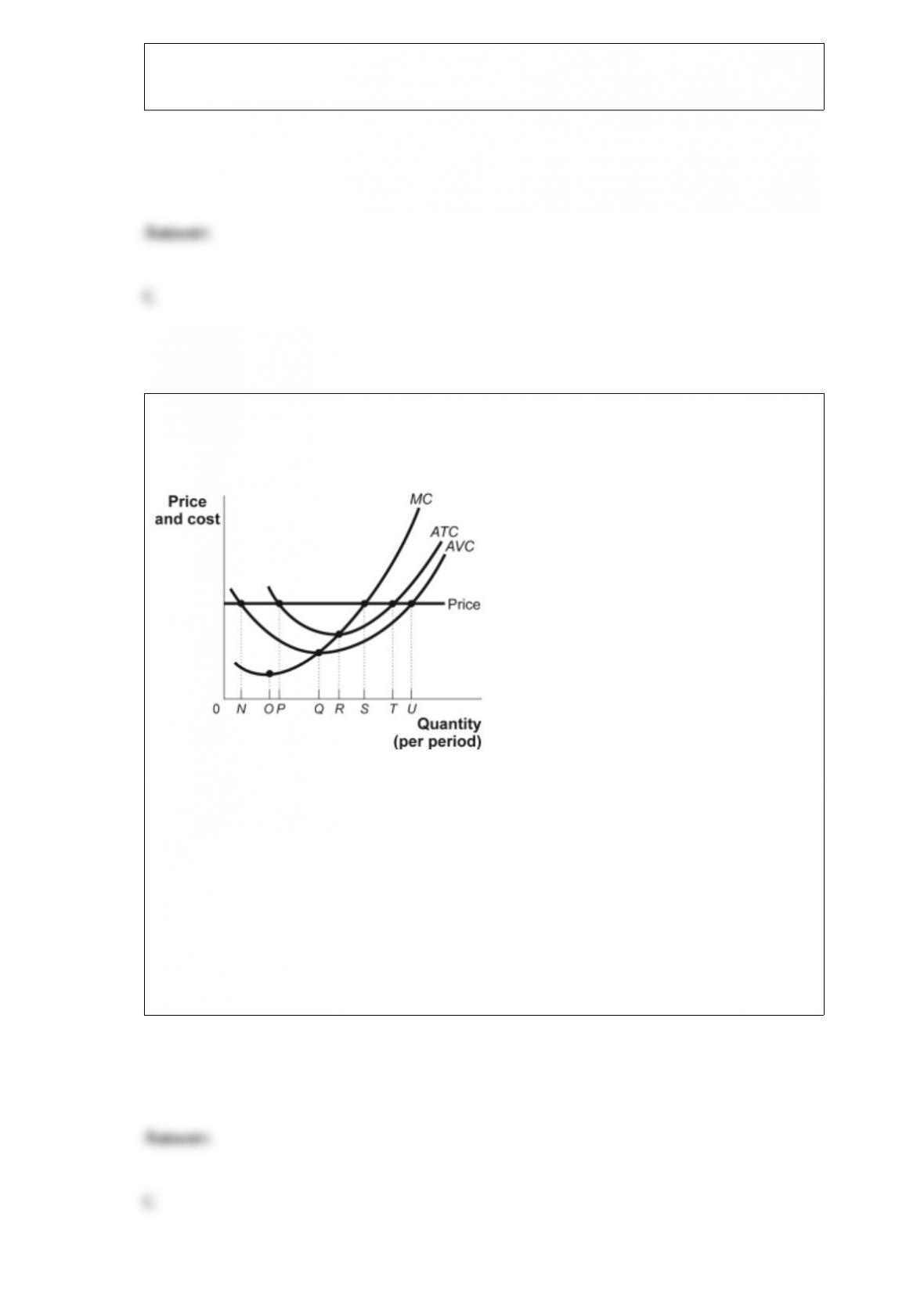

Figure: Short-Run Costs

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. At the given price, the

most profitable level of output occurs at quantity:

A) N.

B) P.

C) S.

D) T.

The strategy of reducing or eliminating risks by taking a small share in many

independent events or by taking advantage of the predictability associated with large

numbers of independent events is known as:

A) floating.

B) specializing.

C) pooling.

D) screening.

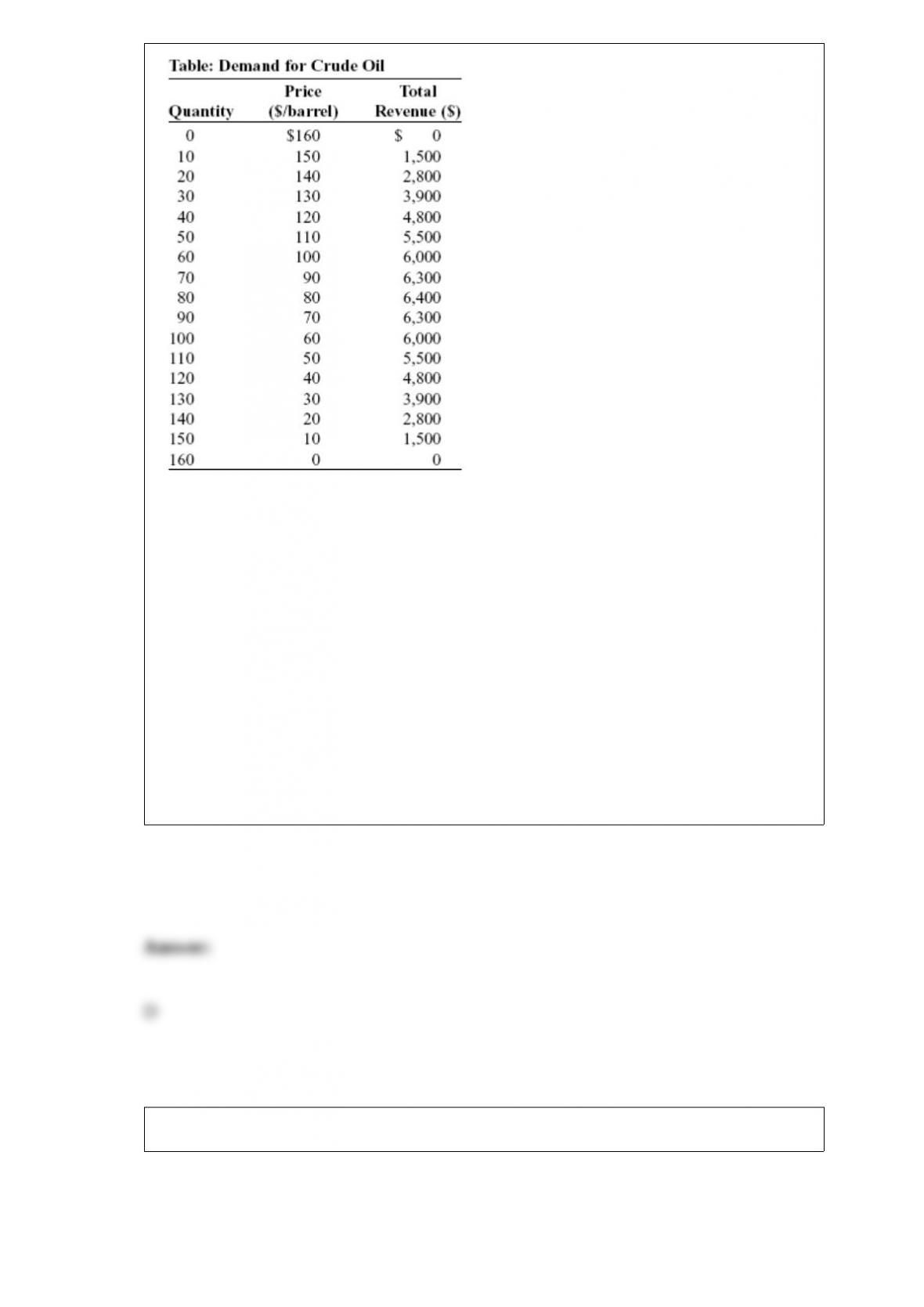

(Table: Demand for Crude Oil) Look at the table Demand for Crude Oil. Assume that

the crude oil industry is a duopoly and the marginal cost and fixed cost of producing

crude oil equals zero. Suppose that the two firms are maximizing industry profit and

splitting the profit evenly. If firm 1 decides to cheat and increase production by 10 more

barrels and firm 2 continues to produce 40 barrels, firm 2 will earn profits of:

A) $6,400.

B) $6,300.

C) $3,500.

D) $2,800.

The market for salmon is in equilibrium. A price ceiling, a price floor, and a quota limit

in this market would all cause:

A) deadweight loss arising from a quantity exchanged that is less than the equilibrium

quantity.

B) a supply price that exceeds a demand price.

C) revenue collected by the government on each unit of salmon harvested.

D) deadweight loss arising from a transfer of surplus from consumers to producers.

Unemployment insurance is a(n) _____ that is _____.

A) monetary transfer; means-tested

B) monetary transfer; not means-tested

C) in-kind benefit; means-tested

D) in-kind benefit; not means-tested

A choice made _____ is a choice whether to do a little more or a little less of

something.

A) at the fringe

B) in the beginning

C) at the margin

D) after the fact

Market equilibrium occurs when:

A) there is no incentive for prices to change in the market.

B) quantity demanded equals quantity supplied.

C) the market clears.

D) there is no incentive for prices to change in the market, quantity demanded equals

quantity supplied, and the market clears.

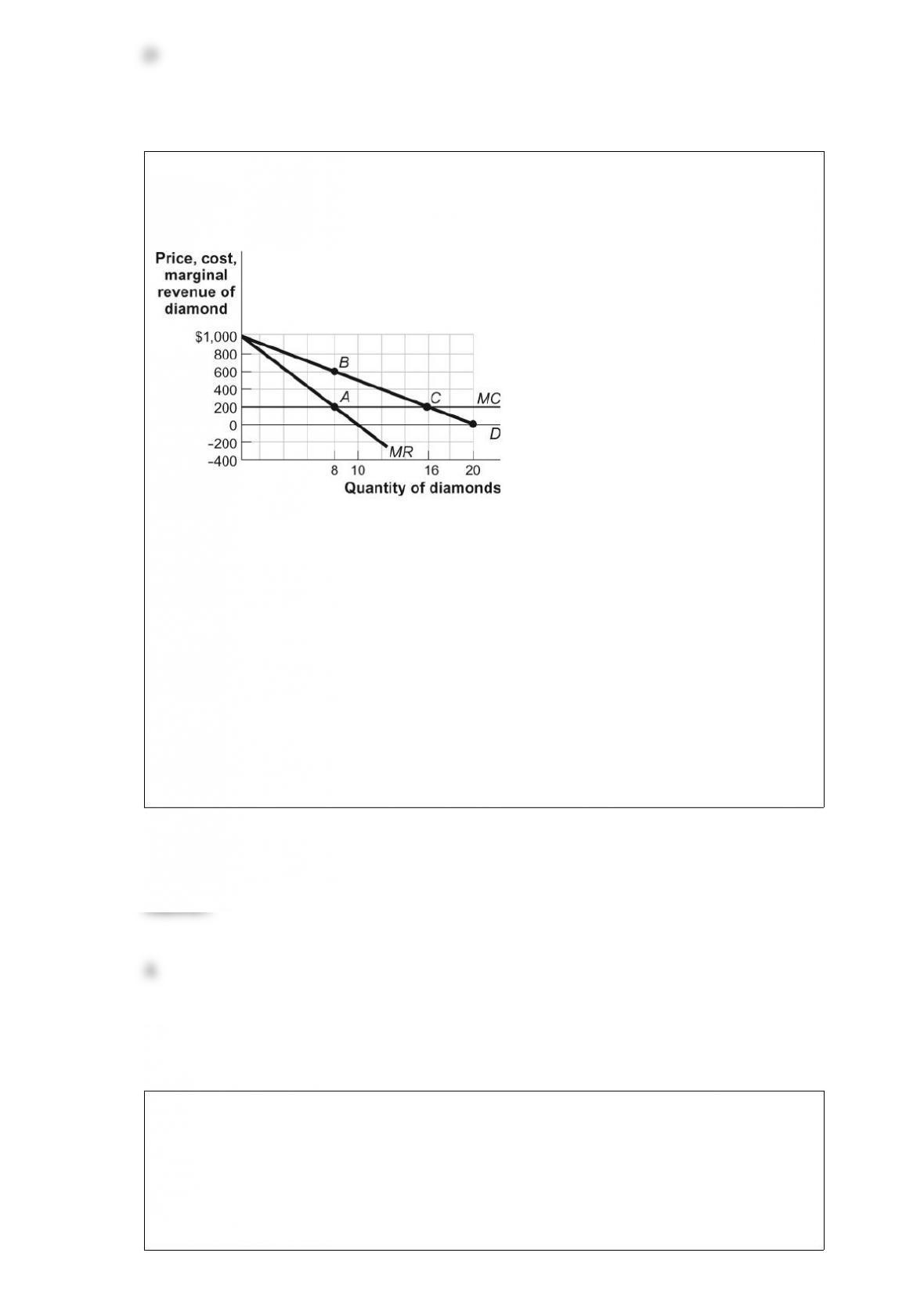

Figure: The Profit-Maximizing Output and Price

(Figure: The Profit-Maximizing Output and Price) Look at the figure The

Profit-Maximizing Output and Price. Assume that there are no fixed costs and AC =

MC = $200. At the profit-maximizing output and price for a monopolist, producer

surplus is:

A) $3,200.

B) $6,400.

C) $1,000.

D) $1,600.

An economy has achieved _____ if it _____ pass up any opportunities to make some

people better off without making others worse off.

A) efficiency; does not

B) equity; does

C) efficiency; does

D) equity; does not

Jill, a careful utility maximizer, consumes peanut butter and ice cream. Assume that

both peanut butter and ice cream are normal goods. She had just achieved the

utility-maximizing solution in her consumption of the two goods when the price of

peanut butter increased. As she adjusted to this event, the marginal utility of peanut

butter _____ and that of ice cream _____.

A) rose; rose

B) fell; fell

C) fell; rose

D) rose; fell

When the price of chocolate-covered peanuts decreases from $1.10 to $0.95, the

quantity demanded increases from 190 bags to 215 bags. In this price range, the

demand for chocolate covered peanuts is _____, and total revenue will _____ when

price decreases.

A) elastic; increase

B) elastic; decrease

C) inelastic; increase

D) inelastic; decrease

Payments from the government to assist individuals are called:

A) taxes.

B) transfers.

C) the welfare state.

D) SCHIP.

Yovanka has diabetes, and she will pay any amount of money for insulin. What is likely

the best characterization of Yovanka’s demand for insulin?

A) price-inelastic

B) price-elastic

C) perfectly price-inelastic

D) perfectly price-elastic