Which of the following are likely to occur when interest rates rise sharply?

a. Fixed-rate loans are pre-paid.

b. Bonds are called.

c. Deposits are withdrawn early.

d. All of the above occur when interest rates rise sharply.

e. a. and b.

Answer:

Which of the following would not be considered “hot money”?

a. Jumbo CDs

b. Fed funds purchased

c. Eurodollar time deposits

d. Retail demand deposits

e. Repurchase agreements

Answer:

A new charter to start a federal savings association is obtained from the:

a. Office of the Comptroller of the Currency.

b. National Credit Union Administration.

c. Office of Thrift Supervision.

d. State banking department.

e. Federal Reserve

Answer:

If a bank has a positive GAP, a decrease in interest rates will cause interest income to

__________, interest expense to__________, and net interest income to __________.

a. increase, increase, increase

b. increase, decrease, increase

c. increase, increase, decrease

d. decrease, decrease, decrease

e. decrease, increase, increase

Answer:

Which of the following is not an advantage of larger cash balances for a bank?

a. Larger cash balances reduce the need to borrow at the discount window.

b. Larger cash balances reduce the risk of bank runs.

c. Larger cash balances reduce the risk of paying penalties to the Federal Reserve.

d. Larger cash balances increase reserve balances.

e. Larger cash balances reduce a bank’s interest expense.

Answer:

A change in net interest income would occur when:

a. the composition of the assets of the bank change.

b. the average asset yield changes.

c. the volume of the assets of the bank change.

d. the average interest expense changes.

e. All of the above

Answer:

For a bank with deficient capital ratios, which of the following actions could be taken to

increase the capital ratios, holding everything else the same?

a. Cut the bank’s dividend payment.

b. Increase the bank’s burden.

c. Repurchase the bank’s common stock on the open market.

d. Increase the bank’s growth rate by making additional commercial loans.

e. Reduce the bank’s holdings of Treasury securities.

Answer:

The only quantitative measure of a consumer loan applicant’s character is their:

a. down payment.

b. home equity.

c. time on the job.

d. credit report.

e. credit card balance.

Answer:

Approximately what percentage of commercial banks were currently considered well

capitalized at the end of 2007?

a. 94%

b. 84%

c. 74%

d. 64%

e. 54%

Answer:

Two bonds with different coupon amounts are priced to yield the same yield to maturity.

For a given change in market rate:

a. the bond with the lower coupon will always change more in price than the bond with

the higher coupon.

b. the bond with the higher coupon will always change more in price than the bond with

the lower coupon.

c. the bond with the lower coupon rate will only change more in price than the bond

with the higher coupon rate if the market rate decreases.

d. The bond with the higher coupon rate will only change more in price than the bond

with the lower coupon rate if the market rate increases.

e. the price change will be the same for both bonds.

Answer:

Which act limited the activities a company could engage in if it owned a bank?

a. Federal Reserve Act

b. Bank Holding Company Act

c. McFadden Act

d. Glass-Steagall Act

e. Competitive Equality Banking Act

Answer:

A shift from core deposits to non-core deposits will:

a. always increase the amount of fixed rate assets.

b. always increase the amount of rate-sensitive assets.

c. generally increase the amount of non-earning assets.

d. generally reduce net interest income.

e. b. and d.

Answer:

A bank that deals primarily with commercial customers is called:

a. an Edge Act bank.

b. a retail bank.

c. a wholesale bank.

d. a uniform bank.

e. a liability bank.

Answer:

To the nearest dollar, what is the value today of an investment that pays $10,000 in five

years, assuming an annual opportunity cost of 6%?

a. $7,473

b. $11,592

c. $8,626

d. $7,130

e. None of the above

Answer:

Which of the following would be considered an unacceptable consumer loan?

a. A home improvement loan, secured by a first mortgage

b. A home improvement loan, secured by a second mortgage

c. A $10,000 loan on a new $30,000 boat, secured by the boat

d. A loan on for 80% of the value on a new automobile, secured by the automobile

e. A loan for 95% of the value of used skydiving equipment, secured by the equipment

Answer:

Which of the following is the most flexible of the Fed’s tools for implementing

monetary policy?

a. Changes in the fed funds rate

b. Changes in the required reserve ratio

c. Changes in the discount rate

d. Open market operations

e. Private placements

Answer:

Which of the following is not part of the CAMELS ratings?

a. Capital adequacy.

b. Asset quality.

c. Earnings quality.

d. Liabilities quality.

e. Sensitivity to market risk.

Answer:

A universal bank can engage in:

a. making commercial loans.

b. making consumer loans.

c. selling insurance.

d. all of the above

e. a. and b. only

Answer:

Preferred stock:

a. has characteristics of debt and common equity.

b. claims are subordinate to common stockholders.

c. dividends may not be deferred.

d. always pay fixed-rate dividends.

e. all of the above.

Answer:

The national average FICO score is:

a. 370

b. 470

c. 570

d. 670

e. 770

Answer:

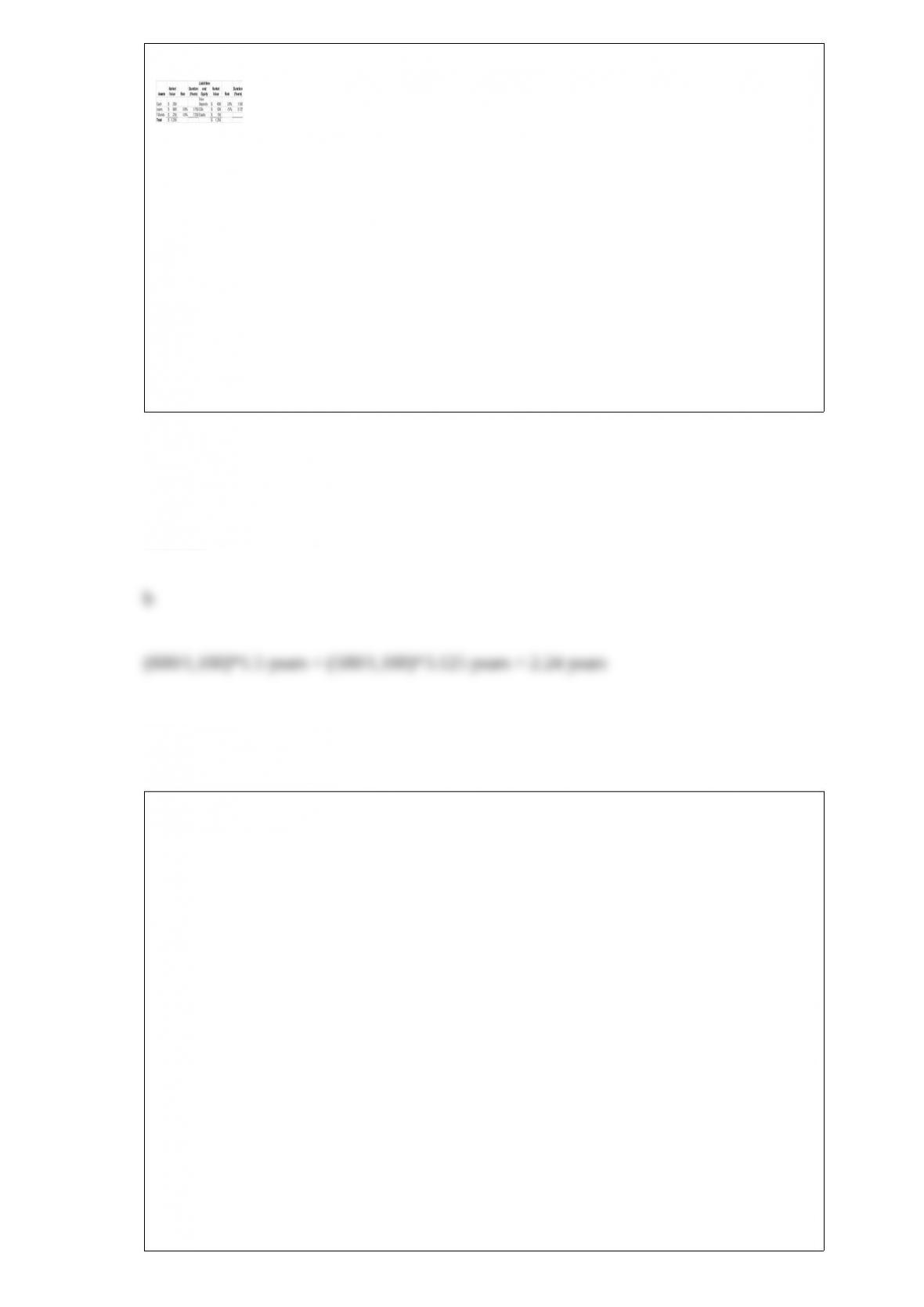

Use the following bank information.

What is the weighted average duration of liabilities?

a. 2.0 years

b. 2.24 years

c. 3.25 years

d. 4.5 years

e. 6.5 years

Answer:

Put the following steps of the creation of a banker’s acceptance in order.

I. Shipping documents delivered

II. Letter of credit delivered

III. Bankers’ acceptance presented at maturity

IV. Goods are shipped

a. I, IV, II, III

b. II, IV, III, I

c. II, IV, I, III

d. I, IV, III, II

e. I, II, III, IV

Answer:

A bank that does not meet the minimum levels for Tier 1 capital, total capital, and

leverage capital ratios is classified as:

a. well-capitalized.

b. adequately capitalized.

c. undercapitalized.

d. significantly undercapitalized.

e. critically undercapitalized.

Answer:

The most dominant type of Eurocurrency deposits are:

a. Euroyens.

b. Eurodollars.

c. Eurosterlings.

d. Eurofrancs.

e. Euromarks.

Answer:

The largest single loan category for all banks is:

a. real estate loans.

b. commercial loans.

c. credit card loans.

d. industrial loans.

e. agricultural loans.

Answer:

Which of the following is likely to have a negative effective duration?

a. A high coupon, interest only mortgage-backed security that is pre-paying at a high

rate.

b. A low coupon U.S. Treasury bond.

c. Fed Funds purchased.

d. Demand deposits

e. None of the above can have a negative effective duration.

Answer:

The Dodd-Frank Volker Rule:

a. allows commercial and investment banks to merge.

b. prohibits proprietary trading using FDIC insured funds.

c. encourages investing and sponsoring of hedge funds

d. both a. and b.

e. both b. and c.

Answer:

Which of the following is not part of Tier 1 or core capital?

a. minority interests in equity capital of consolidated subsidiaries.

b. common stockholders equity

c. cumulative perpetual preferred stock.

d. noncumulative perpetual preferred stock.

e. All of the above are part of Tier 1 or core capital..

Answer:

At the end of 2008, which of the following investment banks remained independent?

a. Bear Stearns

b. Goldman Sachs

c. Lehman Brothers

d. Merrill Lynch

e. a. and b.

Answer:

Which of the following is not a component of the Farm Credit System?

a. Farm Credit Banks

b. Agricultural Credit Associations

c. Federal Land Credit Associations

d. Farm Credit Administration

e. Agricultural Lending Office

Answer:

When is interest rate risk for a bank greatest?

a. When interest rates are volatile.

b. When interest rates are stable.

c. When inflation is high.

d. When inflation is low.

e. When loan defaults are high.

Answer: