A U.S. grocery store chain bought $800,000 worth of Kenyan currency from a bank in

Kenya. It then used these funds to buy $800,000 worth of coffee from Kenyan coffee

growers.

As a result of this exchange, by how much and in which direction did:

A. U.S. net exports change?

B. U.S. net capital outflow change?

The law of demand states that, other things equal, when the price of a good rises, the

quantity demanded of the good falls, and when the price falls, the quantity demanded

rises.

a. True

b. False

Pauline is offered a Job in Minneapolis that pays $80,000. She is offered a similar job in

Louisville that pays$71,200. Which pair of CPIs would ensure that the two salaries

have the same purchasing power?

a. 90 in Minneapolis and 83 in Louisville

b. 90 in Minneapolis and 72 in Louisville

c. 100 in Minneapolis and 89 in Louisville

d. 105 in Minneapolis and 90 in Louisville

Suppose that there are diminishing returns to capital. Suppose also that two countries

are the same except one has less capital and so less real GDP per person. Suppose that

both increase their saving rate from 3 percent to 4 percent. In the long run

a. both countries will have permanently higher growth rates of real GDP per person, and

the growth rate will be higher in the country with more capital.

b. both countries will have permanently higher growth rates of real GDP per person,

and the growth rate will be higher in the country with less capital.

c. both countries will have higher levels of real GDP per person, and the temporary

increase in growth in the level of real GDP per person will have been greater in the

country with more capital.

d. both countries will have higher levels of real GDP per person, and the temporary

increase in growth in the level of real GDP per person will have been greater in the

country with less capital.

A decrease in demand is represented by a

a. movement downward and to the right along a demand curve.

b. movement upward and to the left along a demand curve.

c. rightward shift of a demand curve.

d. leftward shift of a demand curve.

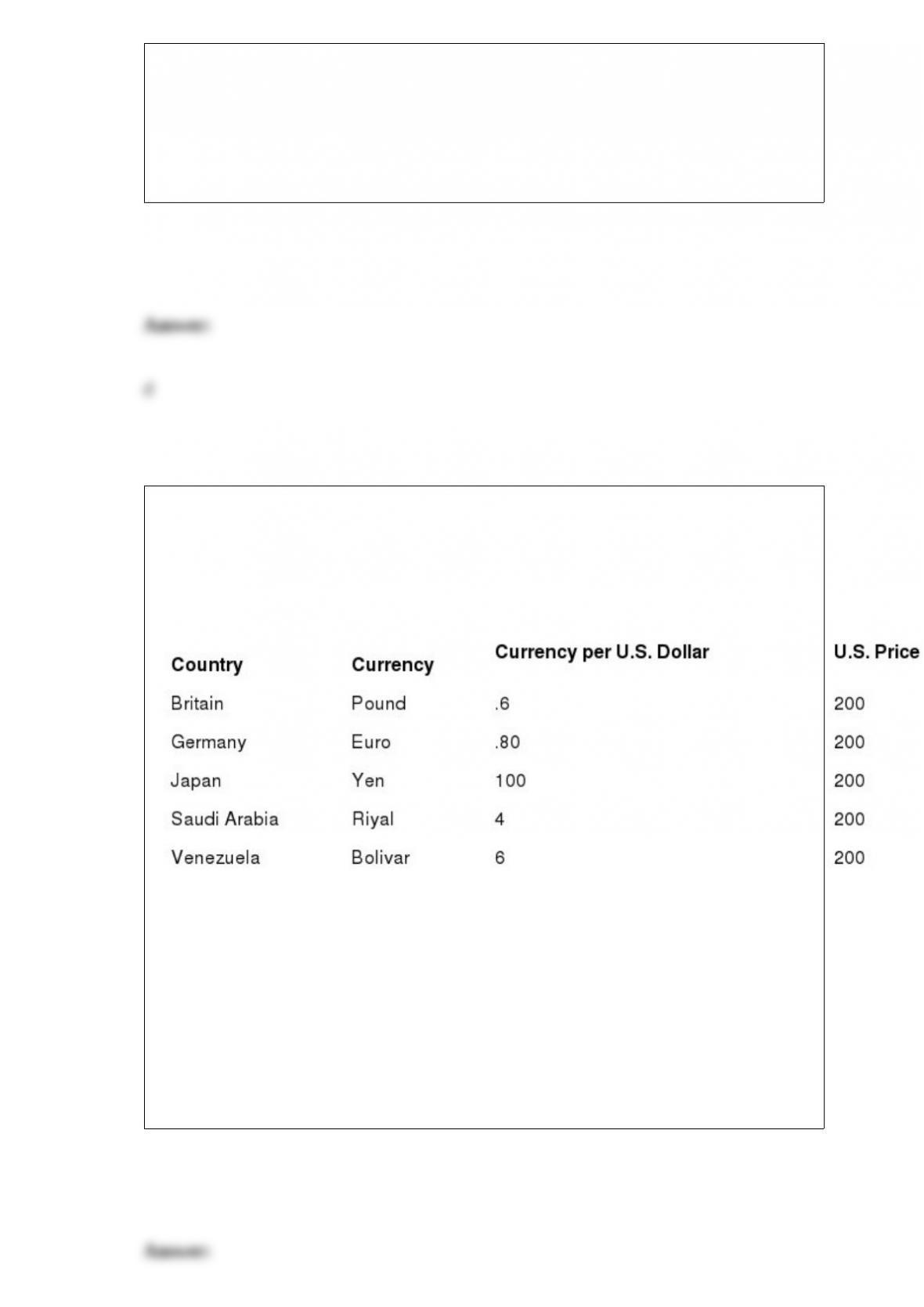

Table31-2

RefertoTable31-2. For which country(ies) in the table does purchasing-power parity

with the U.S. hold?

a. Germany and Japan

b. Japan and Saudi Arabia

c. Britain and Venezuela

d. Germany

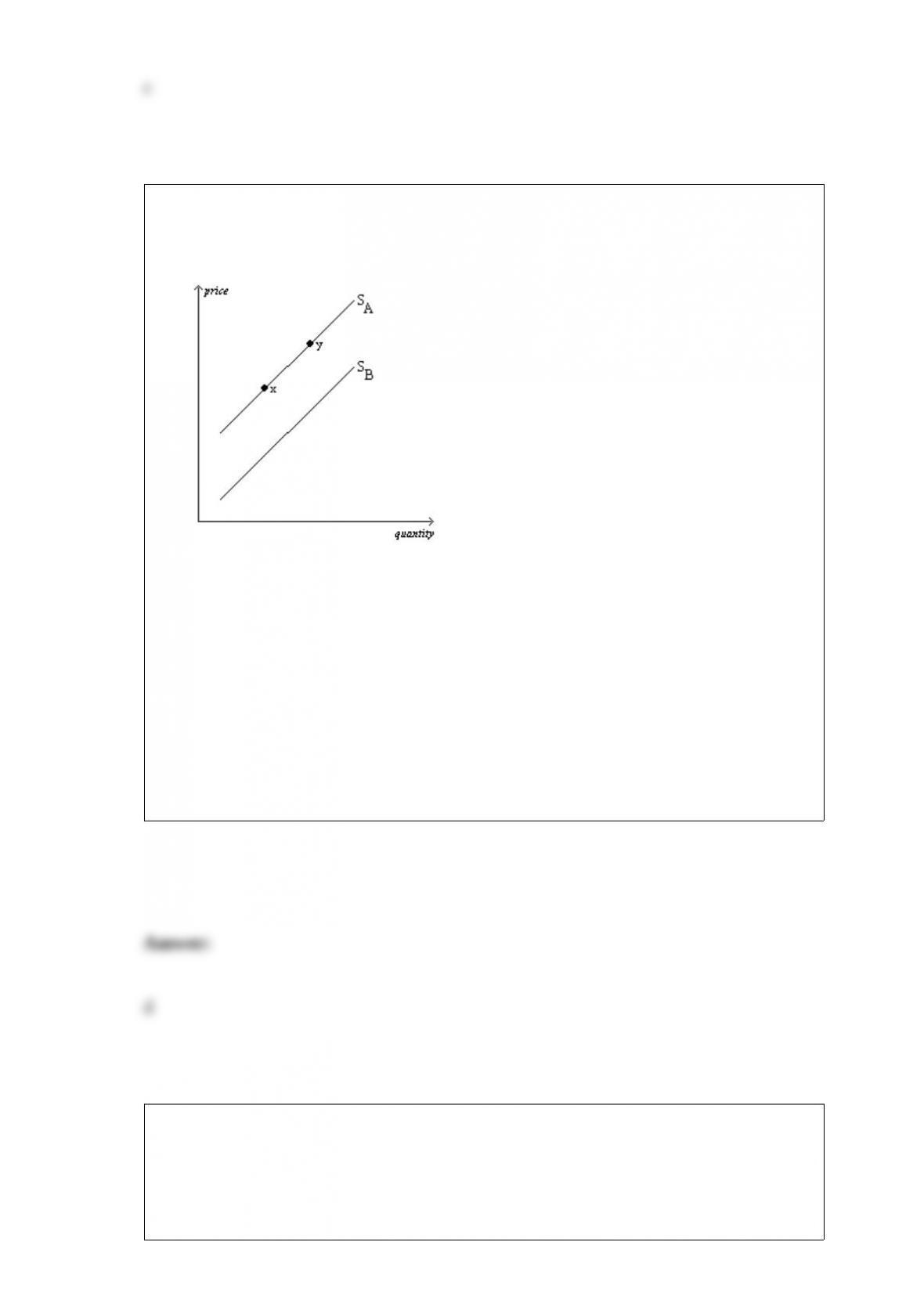

Figure 4-25

The graph below pertains to the supply of paper to colleges and universities.

RefertoFigure4-25.All else equal, an increase in the price of the pulp used in the paper

production process would cause a move from

a. x to y.

b. y to x.

c. SAto SB.

d. SBto SA.

If at a given real interest rate desired national saving is $140 billion, domestic

investment is $90 billion, and net capital outflow is $60 billion, then at that real interest

rate in the loanable funds market there is a

a. surplus. The real interest rate will rise.

b. surplus. The real interest rate will fall.

c. shortage. The real interest rate will rise.

d. shortage. The real interest rate will fall.

If citizens of a country are not saving much, it is better to

a. force citizens to save.

b. reduce investment.

c. have foreigners invest in the domestic economy than no one at all.

d. to prevent opportunities for citizens to buy capital assets abroad.

The consumer price index is used to

a. convert nominal GDP into real GDP.

b. turn dollar figures into meaningful measures of purchasing power.

c. characterize the types of goods and services that consumers purchase.

d. measure the quantity of goods and services that the economy produces.

Which of the following policy actions shifts the aggregate-demand curve?

a. an increase in the money supply

b. an increase in taxes

c. an increase in government spending

d. All of the above are correct.

Which of the following is a requirement for the Bureau of Labor Statistics to place

someone in the “unemployed” category?

a. The person must have worked no more than 10 hours during the past week.

b. The person must have tried to find employment during the previous four weeks.

c. The person may not have been laid off.

d. All of the above are correct.

Imagine the U.S. economy is in long-run equilibrium. Then suppose the value of the

U.S. dollar decreases. At the same time, people in the U.S. revise their expectations so

that the expected price level rises. We would expect that in the short-run

a. real GDP will rise and the price level might rise, fall, or stay the same.

b. real GDP will fall and the price level might rise, fall, or stay the same.

c. the price level will rise, and real GDP might rise, fall, or stay the same.

d. the price level will fall, and real GDP might rise, fall, or stay the same.

In constructing models, economists

a. leave out equations, since equations and models tend to contradict one another.

b. ignore the long run, since models are useful only for short-run analysis.

c. sometimes make assumptions that are contrary to features of the real world.

d. try to include every feature of the economy.

Your company discovers a better way to produce mousetraps, but your better methods

are not apparent from the mousetraps themselves. Your knowledge of how to more

efficiently produce mousetraps is

a. common technological knowledge.

b. common, but not technological, knowledge.

c. proprietary technological knowledge.

d. proprietary, but not technological, knowledge.

A decrease in quantity supplied

a. results in a movement downward and to the left along a fixed supply curve.

b. results in a movement upward and to the right along a fixed supply curve.

c. shifts the supply curve to the left.

d. shifts the supply curve to the right.

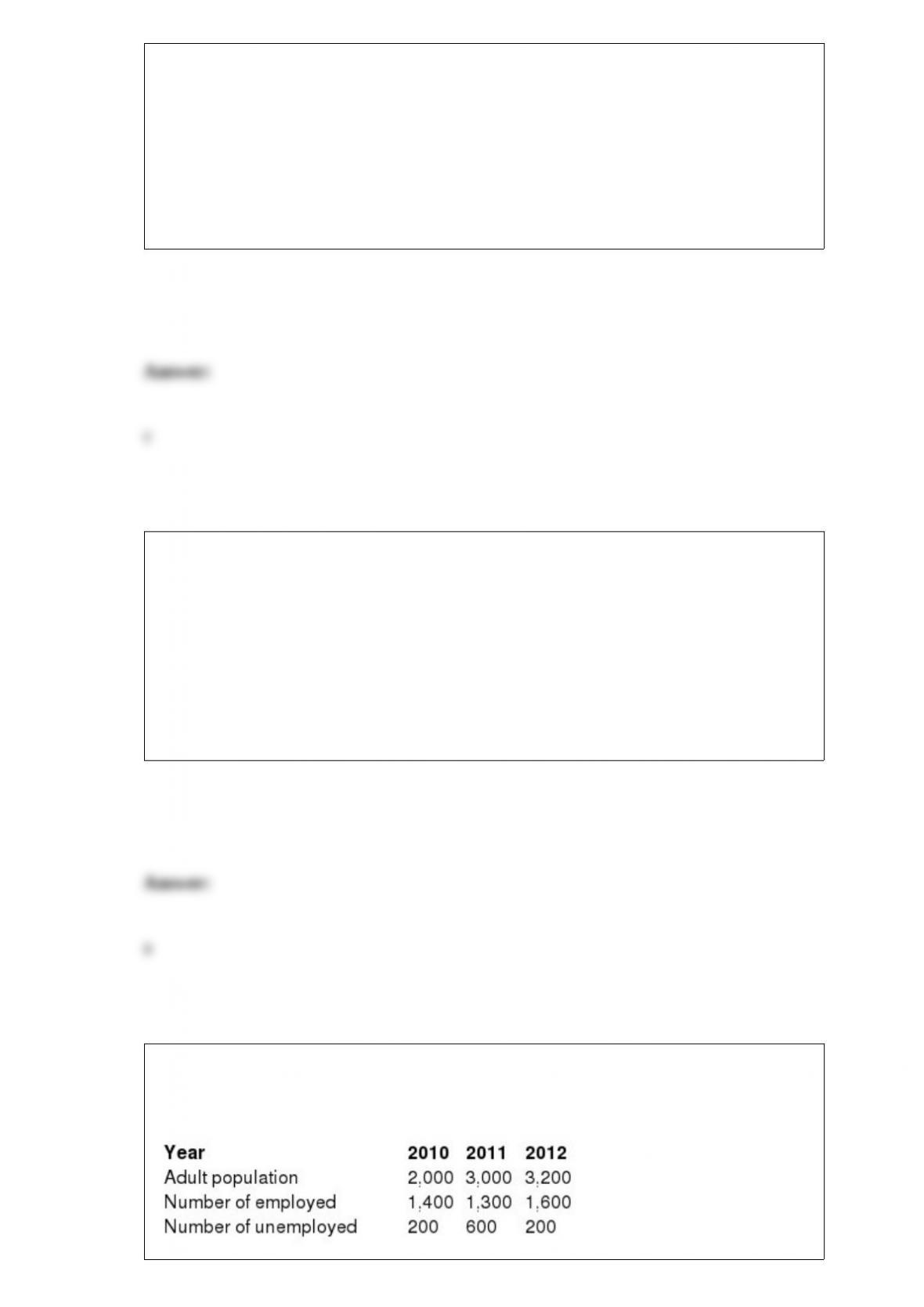

Table 28-2

Labor Data for Aridia

RefetoTable28-2.The unemployment rate of Aridia in 2012 was

a. 6.25%.

b. 11.1%.

c. 12.5%.

d. 56.25%.

Other things the same, if U.S. net capital outflow rises, so does U.S. saving.

a. True

b. False

A management professor discovers a way for corporate management to operate more

efficiently. He publishes his findings in a journal. His findings are

a. proprietary and common knowledge.

b. common, but not proprietary, knowledge.

c. proprietary, but not common, knowledge.

d. neither proprietary nor common knowledge.

In fiscal year 2011, the U.S. government ran a deficit of about $1,300 billion. In fiscal

year 2012, the government ran a deficit of about $1,087 billion. Other things the same,

this change would be expected to have

a. decreased interest rates and investment.

b. decreased interest rates and increased investment.

c. increased interest rates and investment.

d. increased interest rates and decreased investment.

Based on the quantity equation, if Y= 3,000, P= 3, and V= 4, then M=

a. $4,000.

b. $2,250.

c. $250.

d. $36,000.

Which country has had a higher growth rate than the U.S. over about the last 120 years?

a. India

b. Mexico

c. United Kingdom

d. Pakistan

The “invisible hand” refers to

a. how central planners made economic decisions.

b. how the decisions of households and firms lead to desirable market outcomes.

c. the control that large firms have over the economy.

d. government regulations without which the economy would be less efficient.

Suppose the price index was 110 in 2004, 120 in 2005, and 125 in 2006. Which of the

following statements is correct?

a. The economy experienced inflation between 2004 and 2005 and between 2005 and

2006.

b. The inflation rate was positive between 2004 and 2005, and it was negative between

2005 and 2006.

c. The inflation rate was higher between 2005 and 2006 than it was between 2004 and

2005.

d. All of the above are correct.

When Mexico suffered from capital flight in 1994, the U.S. real interest rate

a. rose and the real exchange rate of the dollar appreciated.

b. rose and the real exchange rate of the dollar depreciated.

c. fell and the real exchange rate of the dollar appreciated.

d. fell and the real exchange rate of the dollar depreciated.

In the ordered pair (3, 6), 3 is the

a. x-coordinate.

b. y-coordinate.

c. origin.

d. slope.

Kristine has a savings account at a bank. If the nominal interest rate she earns exceeds

the rate of inflation, then her purchasing power increases over time.

a. True

b. False

Given that Tamar is a risk-averse person, she might accept a bet with a 50 percent

chance of losing $100 today if she had a 50 percent

a. chance of winning $120 in two years and the interest rate was 11%.

b. chance of winning $114 in two years and the interest rate was 7%.

c. chance of winning $110 in two years and the interest rate was 3%.

d. None of the above are correct; a risk averse person would not accept any of the above

bets.

Unions

a. raise the wages of unionized workers and raise unemployment.

b. raise the wages of unionized workers and reduce unemployment.

c. reduce the wages of unionized workers and raise unemployment.

d. reduce the wages of unionized workers and reduce unemployment.

The quantity of money has no real impact on things people really care about like

whether or not they have a job. Most economists would agree that this statement is

appropriate concerning

a. both the short run and the long run.

b. the short run, but not the long run.

c. the long run, but not the short run.

d. neither the long run nor the short run.

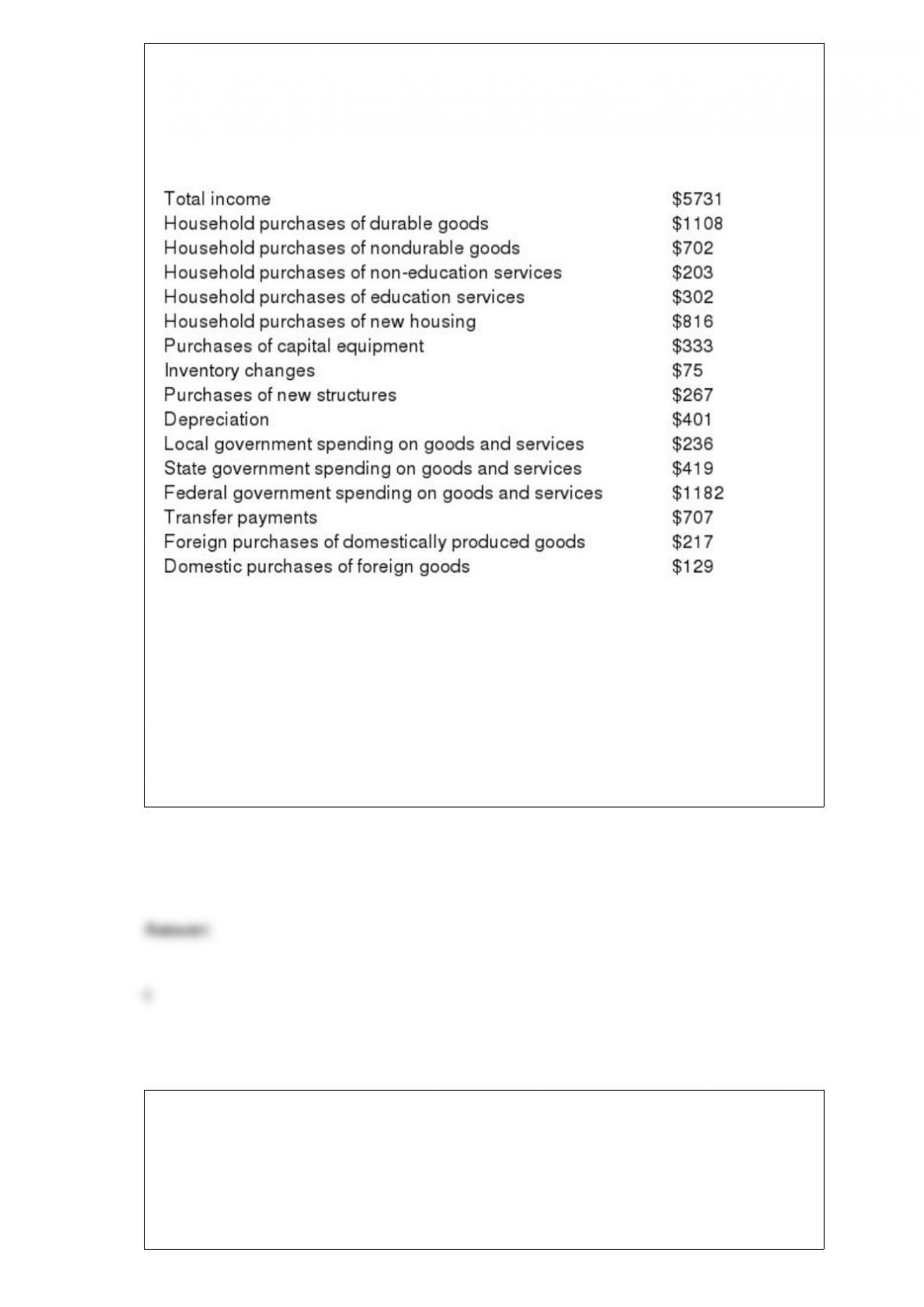

Table 23-3

The table below contains data for the country of Crete for the year 2010.

RefertoTable23-3.What was Crete’s investment in 2010?

a. $675

b. $1090

c. $1491

d. $1793

Bill is restoring a car and has already spent $4,000 on the restoration. He expects to be

able to sell the car for $6,200. Bill discovers that he needs to do an additional $2,400 of

work to make the car worth $6,200 to potential buyers. He could also sell the car now,

without completing the additional work, for $3,800. What should he do?

a. He should sell the car now for $3,800.

b. He should keep the car since it wouldn”t be rational to spend $6,400 restoring a car

and then sell it for only $6,200.

c. He should complete the additional work and sell the car for $6,200.

d. It does not matter if Bill sells the car now or completes the work and then sells it at

the higher price because the outcome will be the same either way.

The most common data for testing economic theories come from

a. carefully controlled and conducted laboratory experiments.

b. computer models of economies.

c. historical episodes of economic change.

d. centrally planned economies.

If the Federal Reserve increases the interest rate on bank deposits at the Fed, banks will

want to hold

a. fewer reserves, so the reserve ratio will fall.

b. fewer reserves, so the reserve ratio will rise.

c. more reserves, so the reserve ratio will fall.

d. more reserves, so the reserve ratio will rise.

If the number of dollars needed to buy a representative basket of goods falls, the price

level

a. falls, so the value of money falls.

b. falls, so the value of money rises.

c. rises, so the value of money falls.

d. rises, so the value of money rises.

In terms of duration, how does cyclical unemployment differ from structural

unemployment?

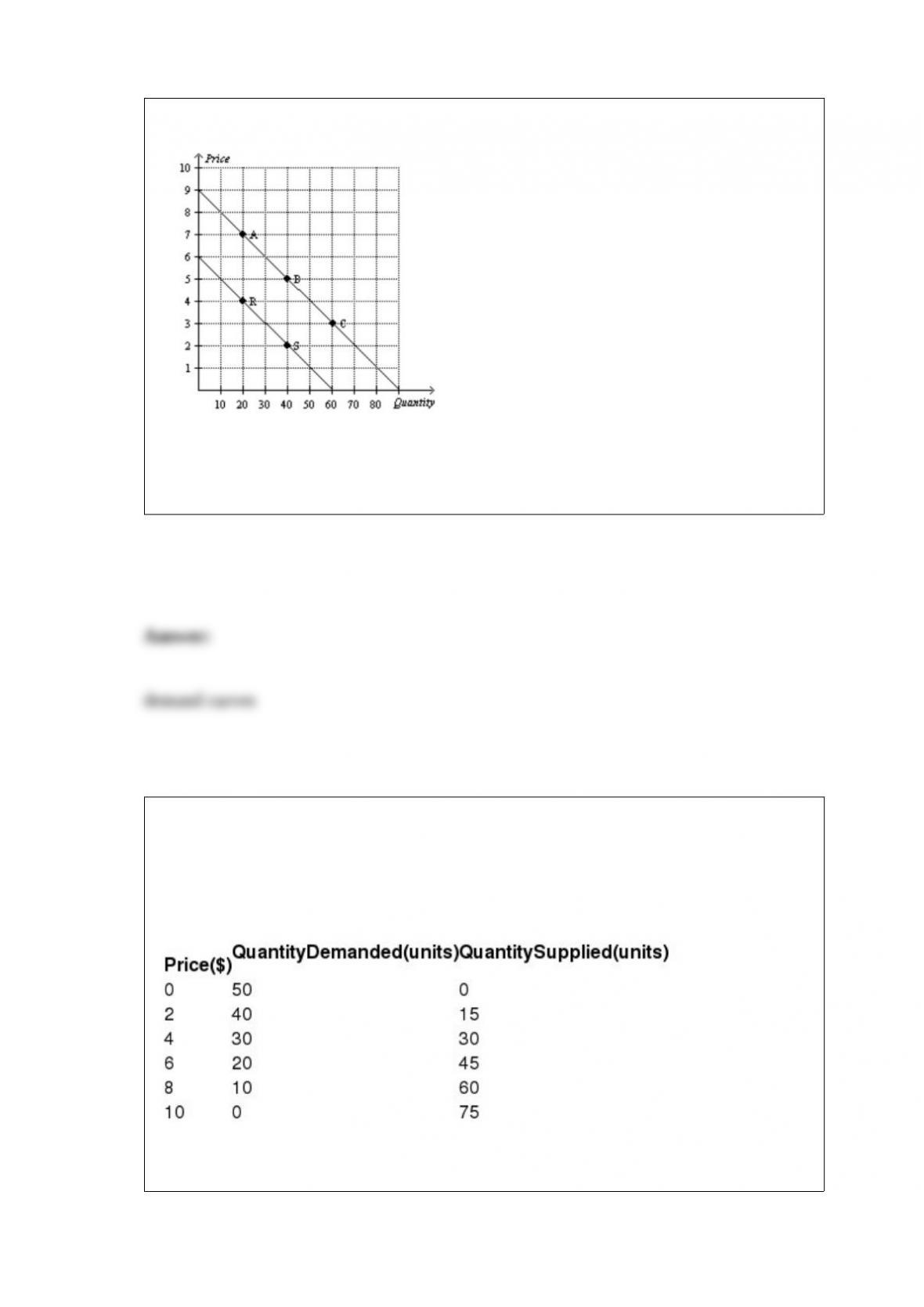

Figure 2-22

Refer to Figure2-22. Given that price is measured on the vertical axis, quantity is

measured on the horizontal axis, and that the curves are downward-sloping, what type

of curves are depicted here?

Table 4-16

The following table shows the supply and demand schedules in a market.

RefertoTable4-16. At a price of $2, will there be a surplus or shortage of units in this

market?

Using typical estimates of the sacrifice ratio, how much output would likely be

sacrificed to reduce inflation by 3 percent?

Describe the two things that limit the precision of the Fed’s control of the money supply

and explain how each limits that control.

What term do we use to refer to the understanding of the best ways to produce goods

and services?

Designers of the Federal Reserve System were concerned that the Fed might form

policy favorable to one part of the country or to a particular party. What are some ways

that the organization of the Fed reflects such concerns?

Last year residents of country A purchased $400 billion of foreign assets and $200 of

foreign goods. Foreigners purchased $300 billion dollars of country A’s assets. What

was the value of country A’s exports?

Explain why it is the case that the value of intermediate goods produced and sold during

the year is not included directly as part of GDP, but the value of intermediate goods

produced and not sold is included directly as part of GDP.

Suppose that changes in aggregate demand tended to be infrequent and that it takes a

long time for the economy to return to long-run output. How would this affect the

arguments of those who oppose using policy to stabilize output?

Are the effects of an increase in aggregate demand in the aggregate demand and

aggregate supply model consistent with the Phillips curve? Explain.

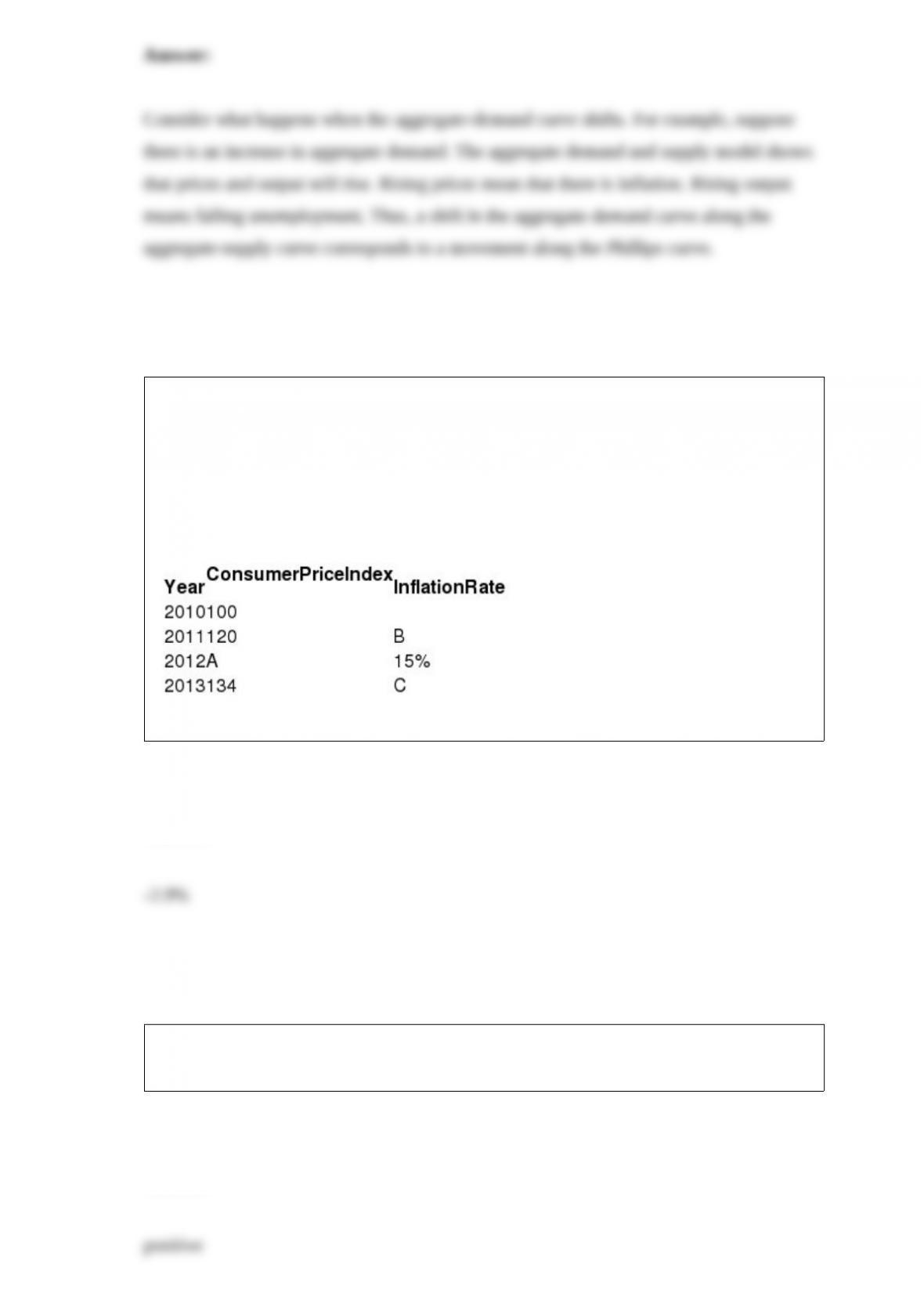

Table 24-16

The table below lists annual consumer price index and inflation rates for a country over

the period 2010-2013. Assume the year 2010 is used as the base year.

RefertoTable24-16. Calculate the missing value that belongs in space C.

Which type of statement – positive or negative – can be evaluated by analyzing data

alone?

There are three factors that help explain the slope of the aggregate demand curve.

Which two are less important? Why are they less important?

What is the change in the money supply when the Fed purchases $700 worth of bonds

and the required reserve ratio is 14 percent assuming banks hold no excess reserves?

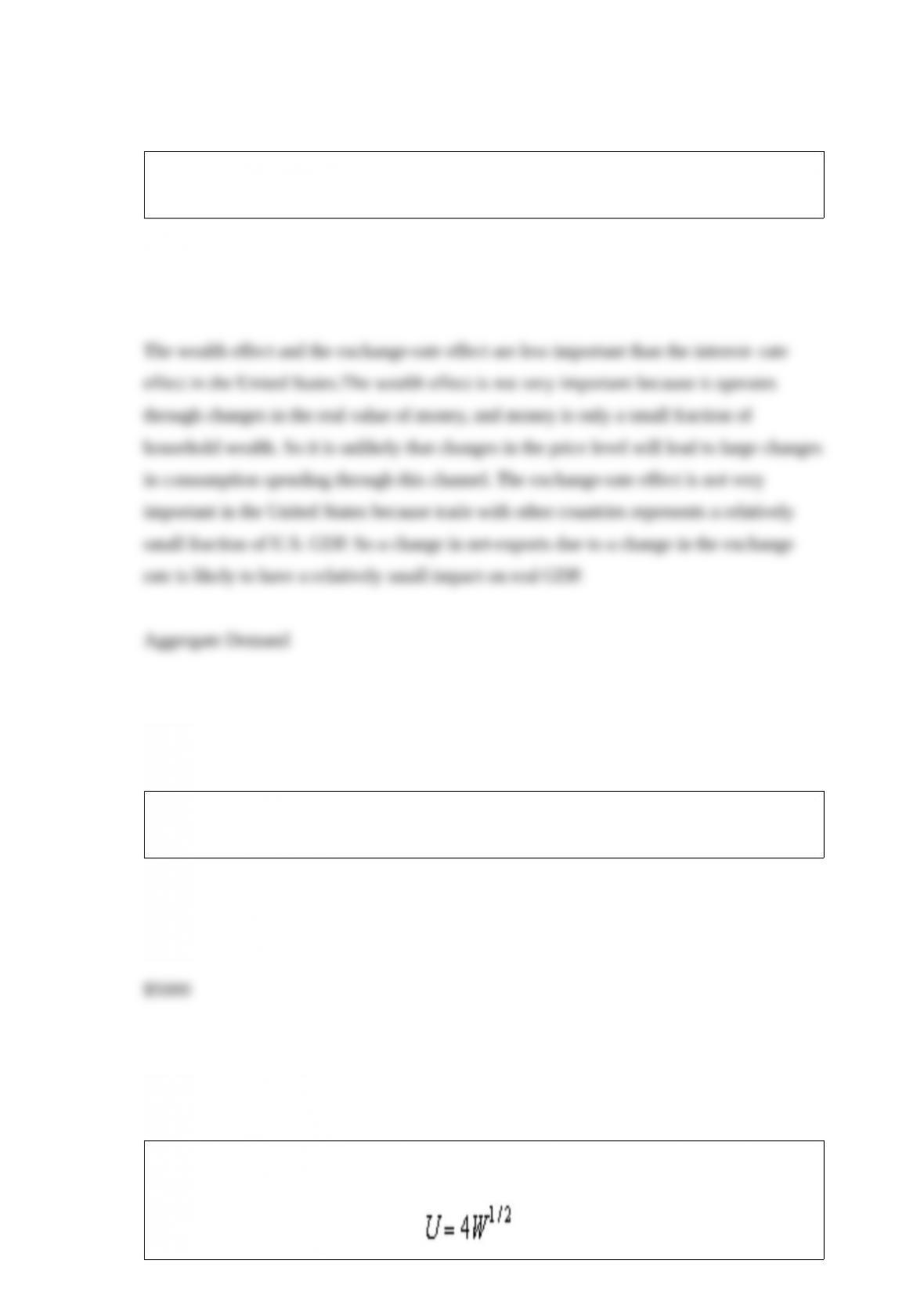

Scenario 27-2

Suppose Dave has a utility function where Wis his wealth in millions of

dollars and Uis the utility he obtains.

RefetoScenario27-2.Is Dave risk averse? Explain.