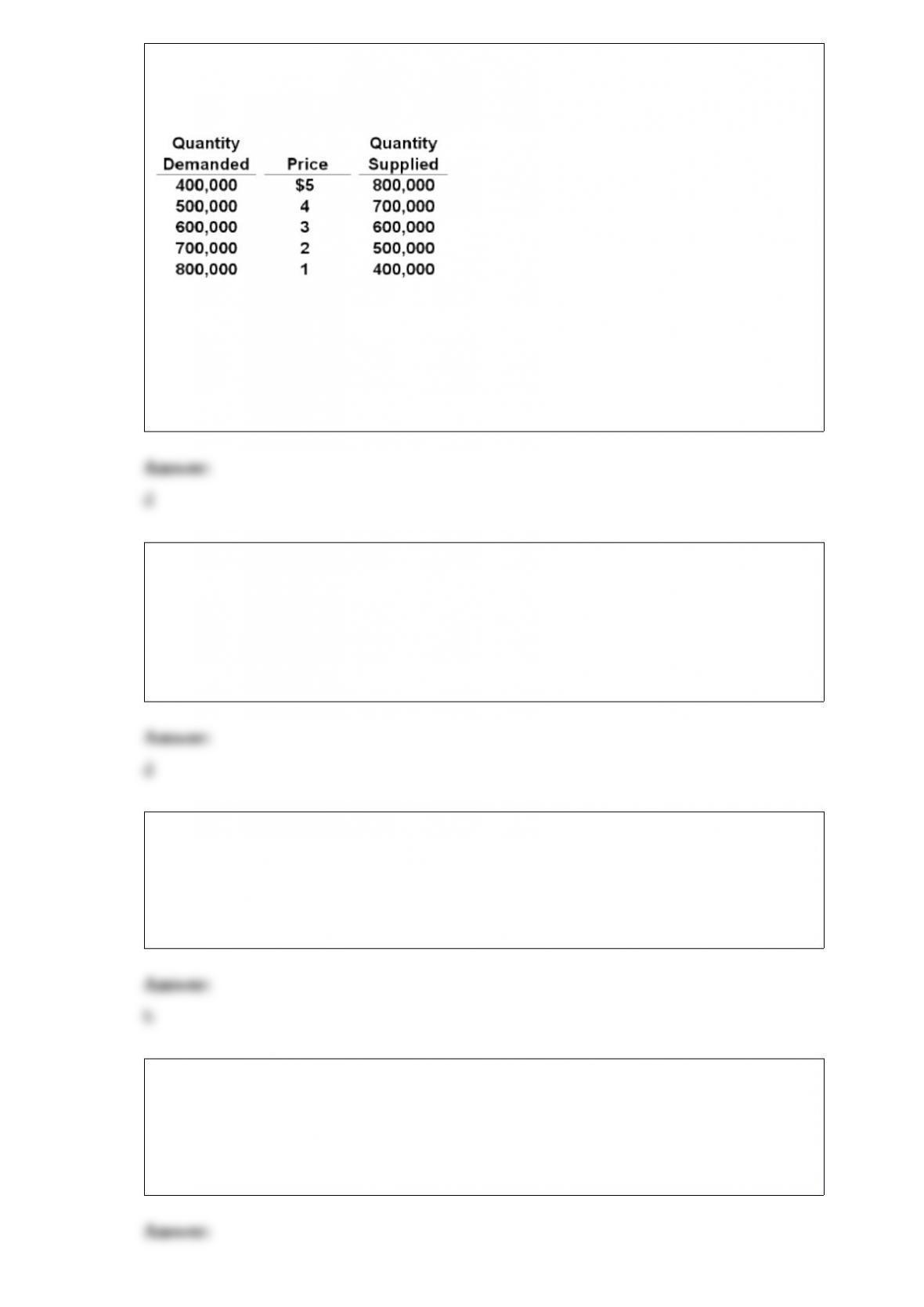

1) the following table applies to a purely competitive industry composed of 100

identical firms.

refer to the above table. for each of the 100 firms in this industry, marginal revenue and

total revenue will be:

a.$4 and $400, respectively.

b.$3 and $30,000, respectively.

c.$4 and $20,000, respectively.

d.$3 and $18,000, respectively.

2) the production possibilities curve tells us:

a.the specific combination of two products that is most desired by society.

b.that costs do not change as society varies its output.

c.costs are irrelevant in a society that has fixed resources.

d.the combinations of two goods that can be produced with society’s available

resources.

3) for a nation’s real gdp per capita to rise during a year:

a.consumption spending must increase.

b.real gdp must increase more rapidly than population.

c.population must increase more rapidly than real gdp.

d.investment spending must increase.

4) if a firm can sell 3,000 units of product a at $10 per unit and 5,000 at $8, then:

a.the price elasticity of demand is 0.44

b.a is a complementary good.

c.the price elasticity of demand is 2.25

d.a is an inferior good.

5) what percentage of the u.s. adult population has a college or postcollege education

(as of 2007)?

a.8 percent

b.29 percent

c.41 percent

d.75 percent

6) (consider this) over the past several decades, the percentage of women in the paid

u.s. workforce has:

a.increased in spite of declining wages for women.

b.decreased because relatively more women are staying home to raise their children.

c.increased due to higher wages, expanded job accessibility, changing preferences and

attitudes, and other factors.

d.increased for unmarried women, but decreased for married women.

7) The recessionary expenditure gap associated with the recession of 2001 resulted

from:

A.the government’s attempt to control hyperinflation.

B.a major increase in personal and corporate taxes.

C.a rapid decline in investment spending.

D.a rapid increase in imports resulting from large tariff reductions.

8) in a competitive market:

a.external benefits will always exceed external costs.

b.resources will be misallocated if government does not properly adjust demand and

supply for large external costs and benefits.

c.resources will be allocated efficiently only if external benefits equal external costs.

d.an efficient allocation of resources is realized even where there are large external

costs and benefits.

9) the following is cost information for the creamy crisp donut company:

entrepreneur’s potential earnings as a salaried worker = $50,000

annual lease on building = $22,000

annual revenue from operations = $380,000

payments to workers = $120,000

utilities (electricity, water, disposal) costs = $8,000

value of entrepreneur’s talent in the next best entrepreneurial activity = $80,000

entrepreneur’s forgone interest on personal funds used to finance the business = $6,000

refer to the above data. creamy crisp’s explicit costs are:

a.$286,000.

b.$150,000.

c.$94,000.

d.$156,000.

10) if the equation y = 5 + 6x was graphed, the:

a.slope would be -5

b.slope would be +5

c.slope would be +.6

d.vertical intercept would be +.6

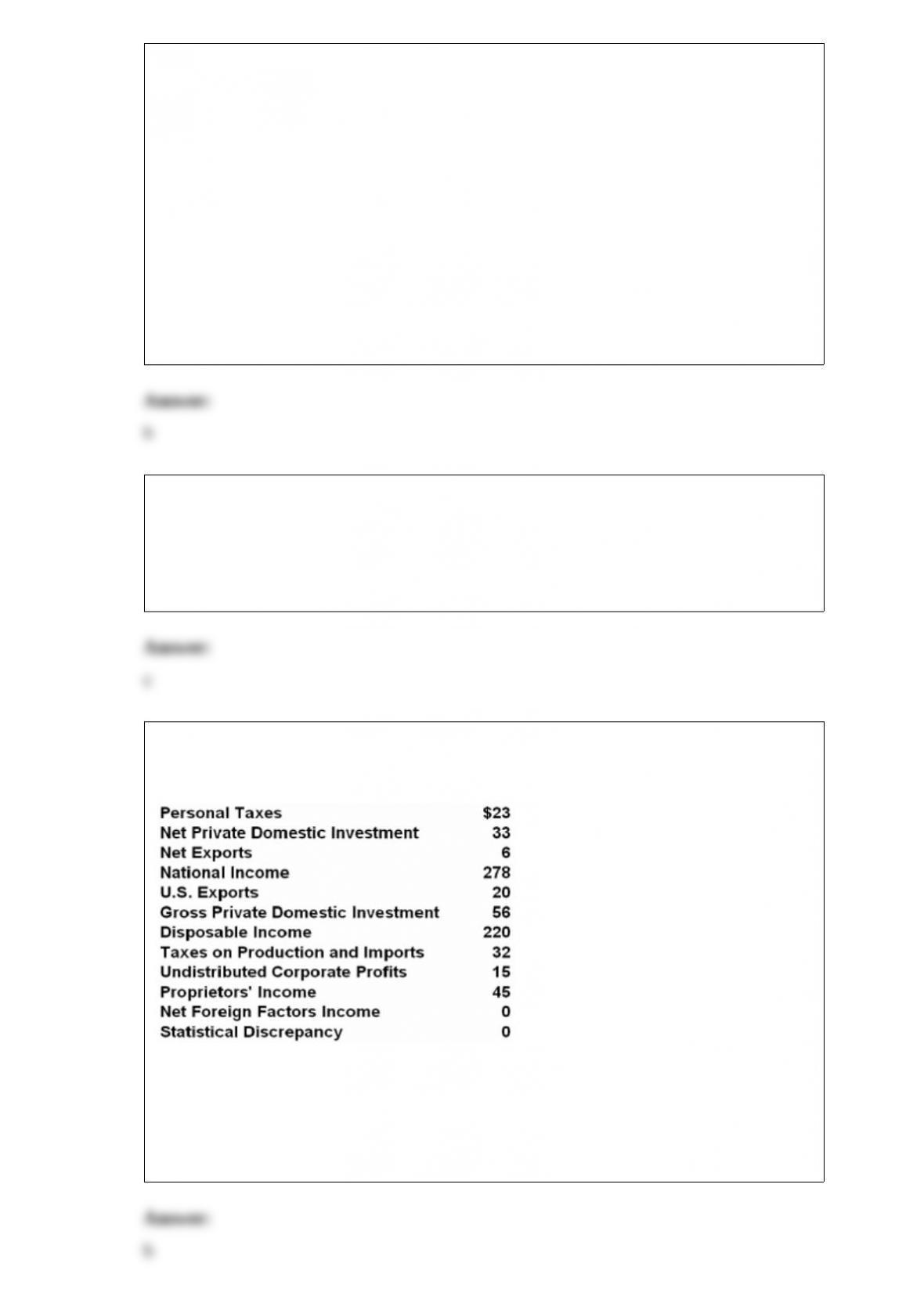

11) answer the next question(s) on the basis of the following national income data. all

figures are in billions of dollars.

refer to the above data. the gross domestic product is:

a.$328.

b.$301.

c.$382.

d.$333.

12) other things equal, which of the following might shift the demand curve for

gasoline to the left?

a.the discovery of vast new oil reserves in montana

b.the development of a low-cost electric automobile

c.an increase in the price of train and air transportation

d.a large decline in the price of automobiles

13) which of the following could be used to correct for a positive externality?

a.a subsidy to consumers of the good.

b.a subsidy to producers of the good.

c.provision of the good by government.

d.all of these are ways to correct for a positive externality.

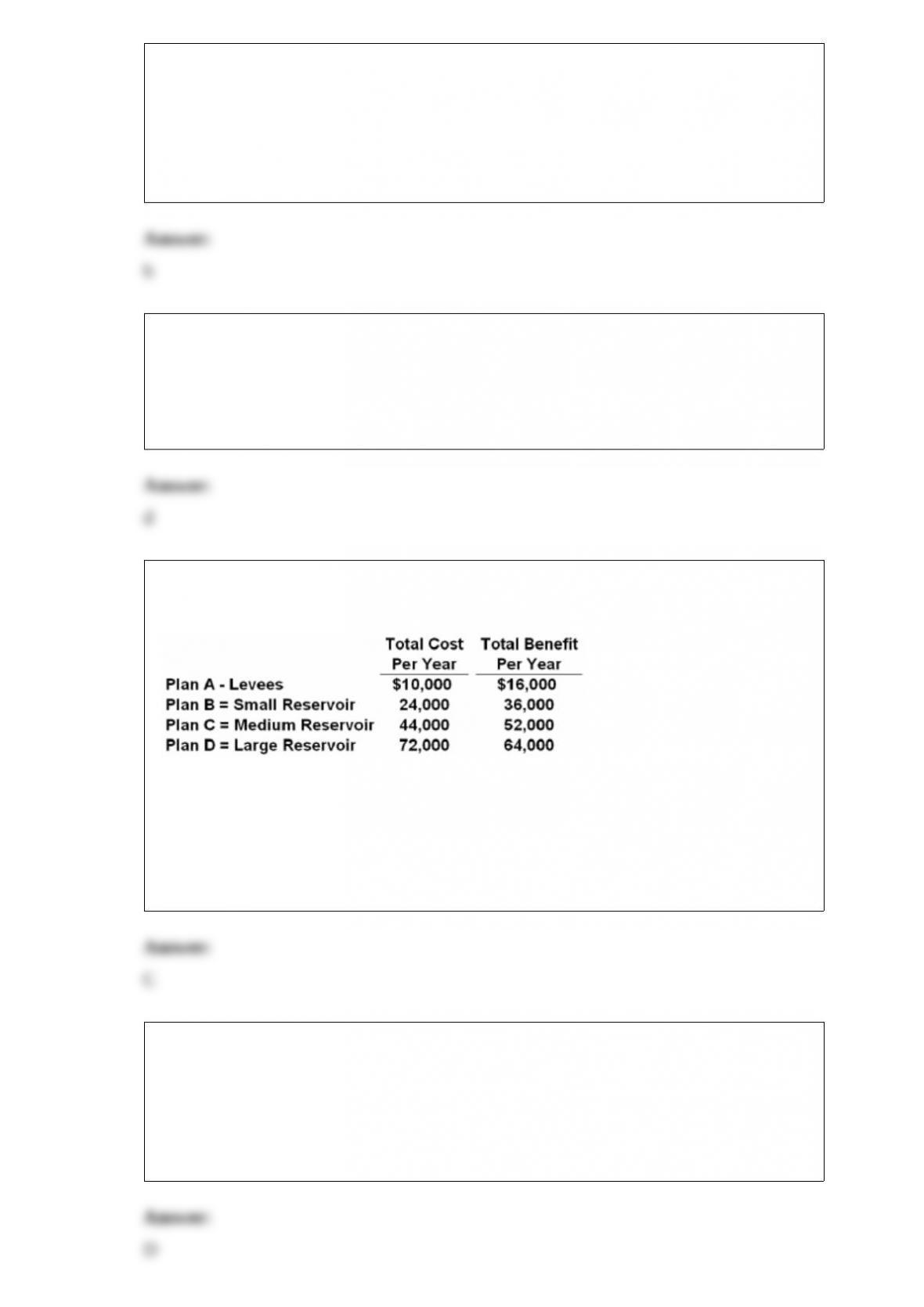

14) The following data are for a series of increasingly extensive flood control projects:

Refer to the above data. On the basis of cost-benefit analysis government should

undertake:

A.Plan D.

B.Plan C.

C.Plan B.

D.Plan A.

15) During periods of rapid inflation, money may cease to work as a medium of

exchange:

A.unless it has been designated legal tender.

B.unless it is backed by gold.

C.it is too scarce for everyone to have enough for transactions.

D.because people and businesses will not want to accept it in transactions.

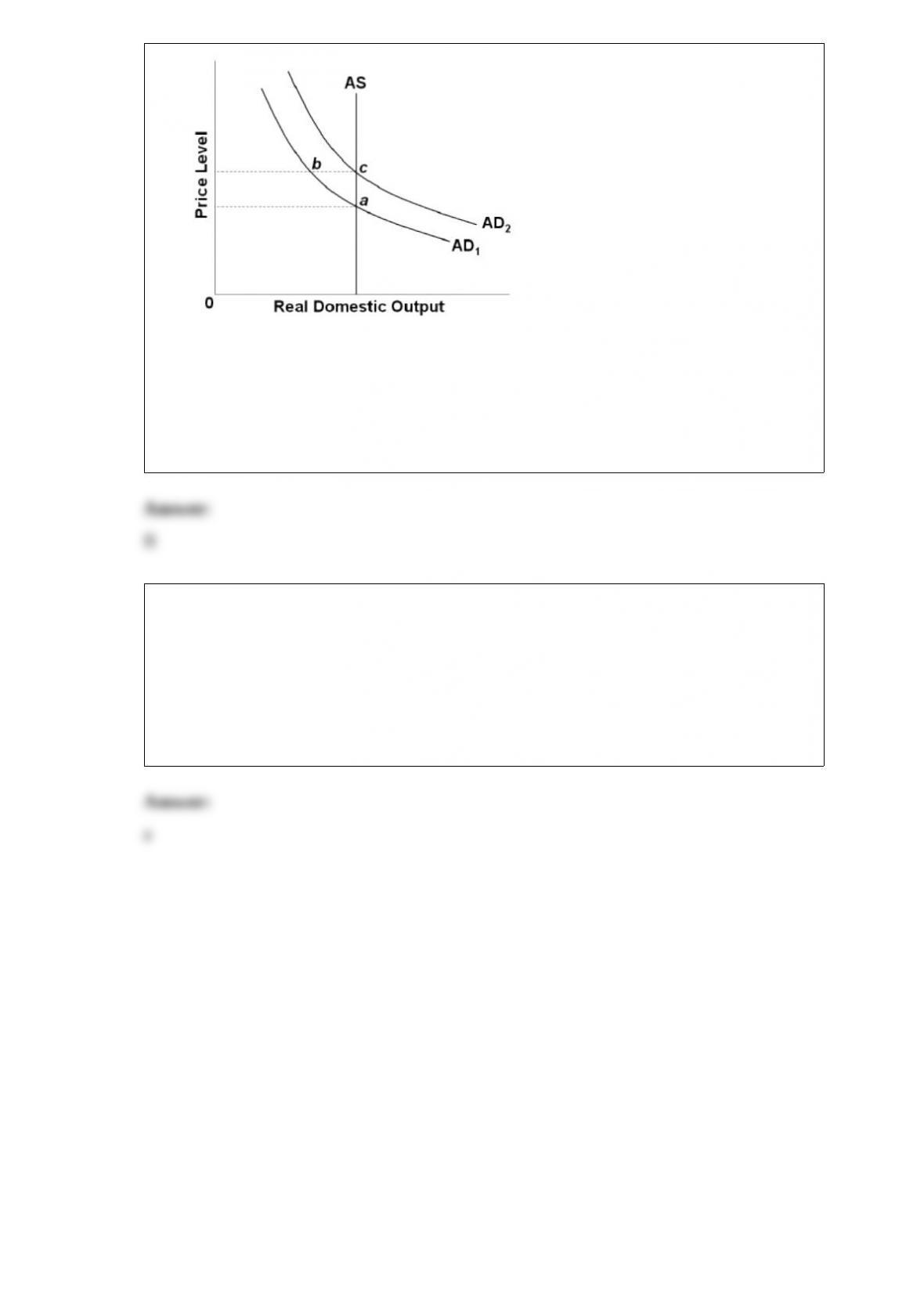

16)

Refer to the above diagram. Rational expectations theory says that a fully anticipated

shift in aggregate demand from AD1 to AD2 will:

A.move the economy from a to b to c.

B.move the economy directly from a to c.

C.move the economy from a to new equilibrium at b.

D.shift the AS curve to the right.

17) indy currently earns $50,000 in taxable income and pays $8000 in taxes. suppose

that indy faces a marginal tax rate of 25 percent and his boss offers him a raise of $2000

per year. indy should:

a.accept the raise because his after-tax income will rise by $1500.

b.reject the raise because his after-tax income will fall by $3000.

c.reject the raise because his after-tax income will fall by $4500.

d.reject the raise because his after-tax income will fall by $6000.