What is the null hypothesis when performing an F-test to test the strength of an

instrument?

a.) the instrument is weak, with no different from 0.

b.) it is a strong instrument with all significantly different from 0.

c.) the instrument is sufficiently strong with at least 1 significantly different from 0.

d.) the instrument is weak with all different from 0.

What type of model consists of a two stage process where the first stage is a binary

choice model of sample selection and the second stage is the linear model of interest?

a.) Tobit

b.) Heckit

c.) multinomial logit

d.) probit

When estimating a VEC model using a two step least squares process, what is the

second step?

a.) use least squares to estimate the cointegrating relationship

b.) use least squares to estimate first differences as a function of estimated residuals

c.) use least squares to estimated residuals as a function of first differences

d.) use least squares to estimate first differences as a function of lagged differences

In the multiple regression model which of the following does NOT lead to larger

variances of the least squares estimators b2 and var(b2)?

a.) larger error variances,

b.) larger correlation between x2 and x3

c.) smaller values of Æ©(xi2 – xÌ…2)2

d.) larger correlation between x2 and y

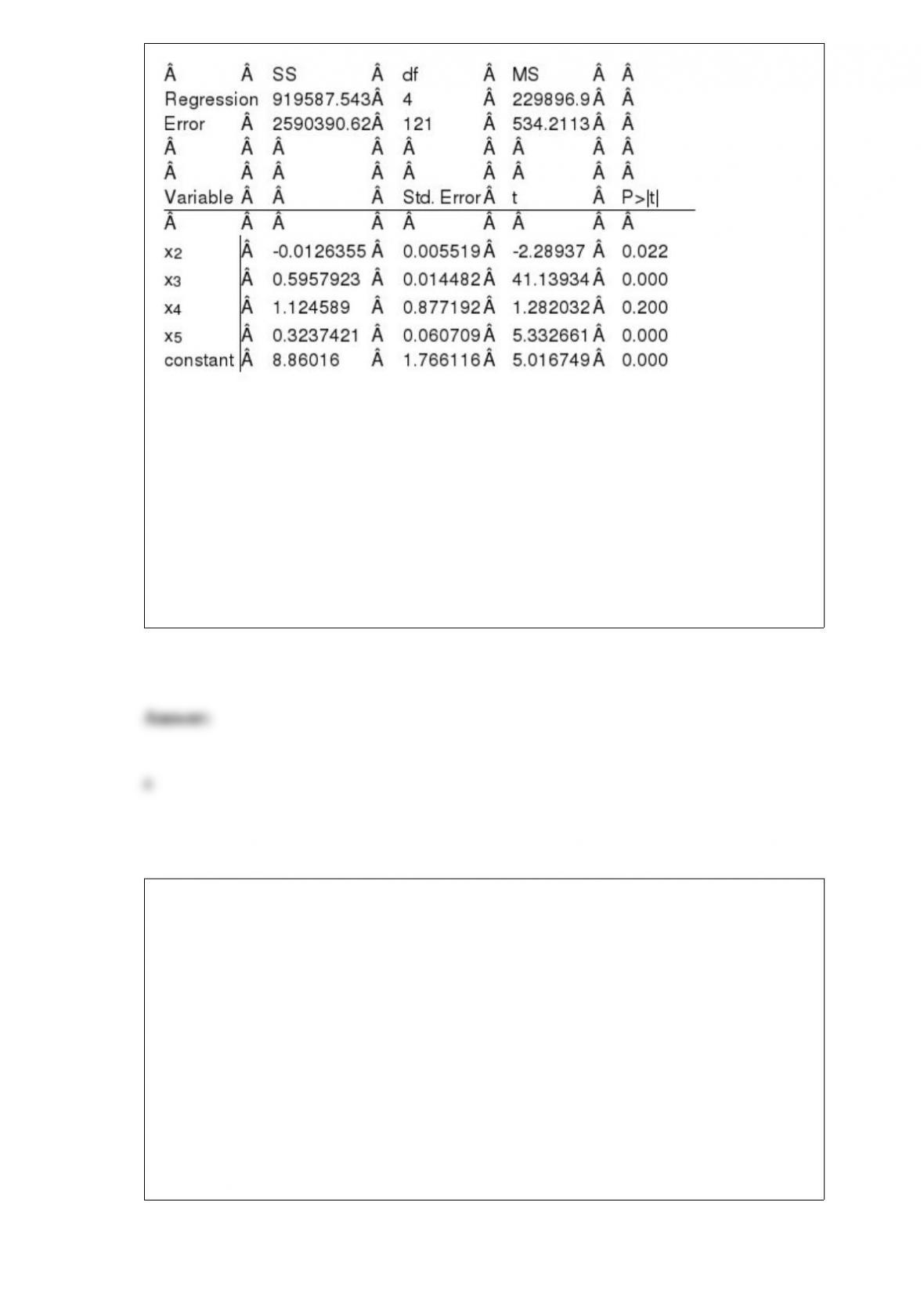

A model estimated using a dataset with 125 observations generates the following

results.

If you want to test the hypothesis = .47. What p-value does this test statistic generate

if you are performing a two-tailed test?

a.) 0.000

b.) ≃0.02

c.) ≃0.01

d.) 0.05

What does ARCH abbreviate?

a.) autoregressive conditional heteroskedastic

b.) alternative regression creating homoscedasticity

c.) all regression characteristic hierarchy

d.) abbreviated regular consistent hypothesis

Why is a random error term included in an econometric model?

a.) because many economic models have not been well developed yet and need to allow

for inaccuracies

b.) because some people are irrational

c.) because there is intrinsic uncertainty in any economic activity due to individual

decision making

d.) because most estimating techniques are not well suited to work with a deterministic

model.

Which model is also called an error components model?

a.) pooled model

b.) fixed effects

c.) random effects

d.) none of these

Treatment effects are best estimated using data from

a.) randomized, controlled experiments.

b.) subjects that have already undergone the risky treatment.

c.) people most in need of the treatments.

d.) natural or quasi-experiments.

Which assumption is most likely to be violated with times series data:

a.) E(et)=0

b.) var (et)= 2

c.) cov(et, e) =0, t s

d.) et N(0, 2)

In the OLS model, what happens to var(1) as the sample size (N) increases?

a.) it also increases

b.) it decreases

c.) it does not change

d.) cannot be determined without more information

What does it mean for a series to have a unit root?

a.) it has a constant mean equal to 1

b.) it has a constant variance equal to 1

c.) it is stationary

d.) it is integrated of order 1

You estimate a simple linear regression model using a sample of 62 observations and

obtain the following results (estimated standard errors in parentheses below coefficient

estimates):

y = 97.25 + 33.74* x

(3.86) (9.42)

You want to test the following hypothesis: H0: = 12, H1: 12. If you choose to

reject the null hypothesis based on these results, what is the probability you have

committed a Type I error?

a.) between .05 and .10

b.) between .01 and .025

c.) between .02 and .05

d.) It is impossible to determine without knowing the true value of

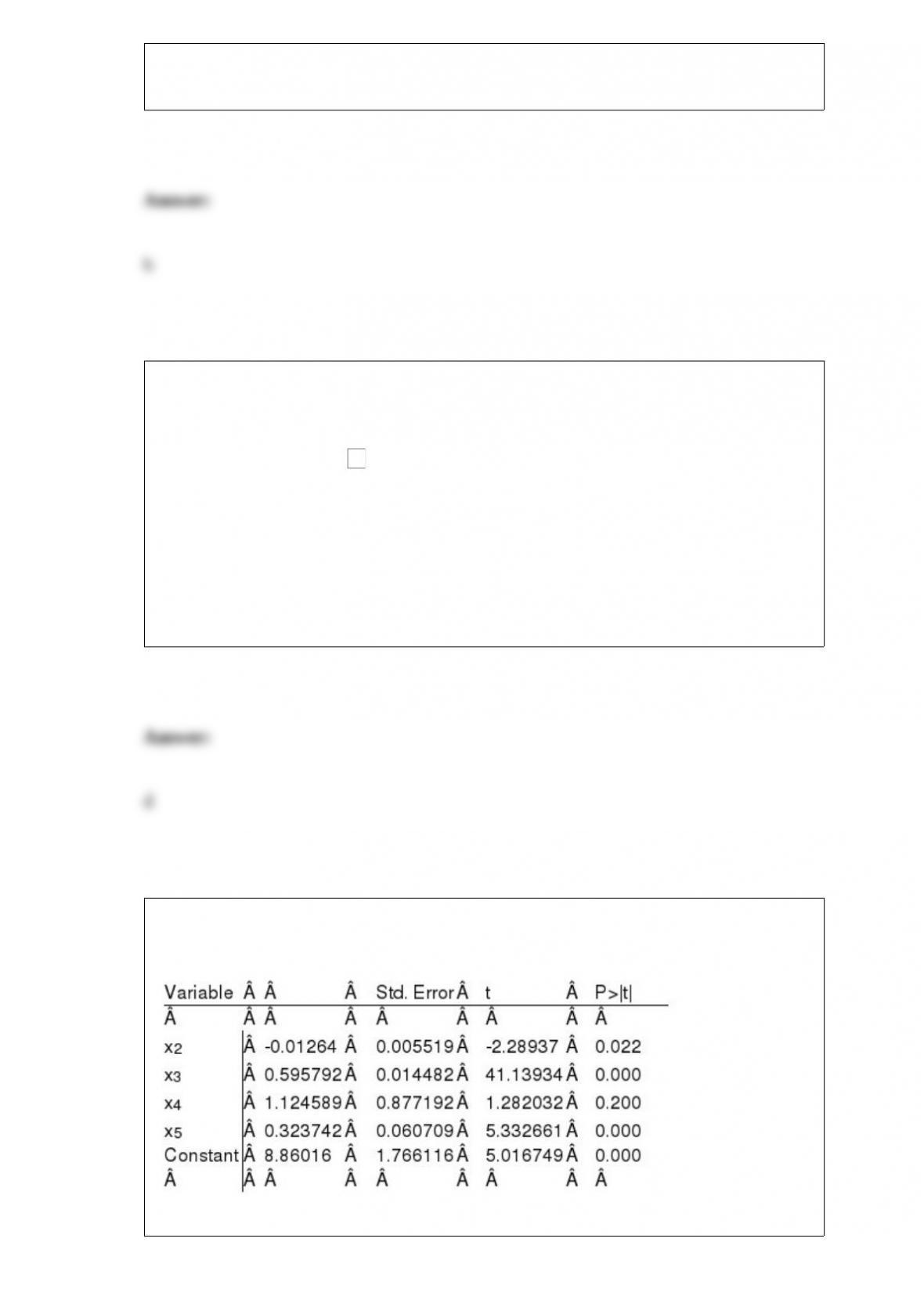

A model estimated using a dataset with 125 observations generates the following

results.

What is the R2 for this sample?

a.) .2620

b.) .3550

c.) .0888

d.) .2172

How do you test for endogenous regressors, or correlation between the error term and

any regressor in a random effects model?

a.) estimate coefficients with RE and FE, then perform a Hausman test of equality

b.) estimate the model capturing estimated residuals, then regress residuals on all

regressors and perform an F-test

c.) estimate RE model capturing estimated residuals, then estimate coefficients of

correlation with each regressor

d.) estimate RE and FE models and perform an F test on each model individually. If the

difference between the F statistics is significant, conclude endogeneity.

How do you find the first difference in yt?

a.) yt– yt-1

b.) dy/ dt

c.) yt –

d.) (yt ‘“ 2