The optimal number of units to produce is best expressed when:

a. marginal benefit exceeds marginal cost

b. marginal cost exceeds marginal benefit

c. marginal benefit and marginal cost are close to equal

d. both a and c

Land on both sides of the border of Brazil and Venezuela has long been occupied by the

Yanomamo people. These “fierce people” are the last Stone Age tribe left in South

America. Following discovery of gold, approximately 45,000 garimperios (gold miners)

invaded the Yanomamo territory. The mining process pollutes the rivers and scares

away game, so traditional Yanomamo sources of food, are almost impossible to find

now. The Yanomamo are starving. Economists call this problem

a. the cost disease.

b. an externality.

c. specialization.

d. rent seeking.

Along a supply curve,

a. supply changes as price changes.

b. quantity supplied changes as price changes.

c. supply changes as technology changes.

d. quantity supplied changes as technology changes.

Over the course of the twentieth century there has been no pronounced tendency for

concentration in the United States to increase.

a. True

b. False

Perfectly elastic demand curves are vertical.

a. True

b. False

“Equilibrium” is a situation in which there are no inherent forces to produce change.

a. True

b. False

The average fixed cost curve increases as output increases.

a. True

b. False

If the MPP of labor is 60 and the price of labor per period is $20, the MPP of machinery

is 75 and the price of the machinery per period is $25, in order to achieve optimal input

proportions the firm should use

a. more labor and less machinery.

b. more machinery and less labor.

c. more labor with the same amount of machinery.

d. the current combination.

Exhibit 4-1

The following are the equations for the supply and demand curves in the market for

weezils:

Demand: Qd = 20 − 2P

Supply: Qs = 5 + 3P

where Qd is the quantity demanded, Qs is the quantity supplied, and P is the price per

weezil in dollars

Refer to Exhibit 4-1. If the government imposes a price floor of $4 a weezil, how many

weezils will be sold?

a. 5

b. 10

c. 12

d. 14

During the Revolutionary War, the Pennsylvania legislature attempted to help the

Continental Army by enacting

a. wage floors for soldiers in the army.

b. bonuses for soldiers who re-enlisted.

c. laws to buy food for the soldiers stationed in Pennsylvania.

d. price controls on essential commodities.

e. All of the above are correct.

The short-run supply curve of a perfectly competitive firm

a. intersects the minimum point of its short-run average total cost curve but not its

short-run average variable cost curve.

b. intersects the minimum point of its short-run average variable cost curve but not its

short-run average total cost curve.

c. intersects the minimum point of both its short-run average variable cost and its

short-run average total cost curves.

d. intersects the minimum point of its short-run average total cost curve and may or

may not intersect the minimum point of its short-run average variable cost curve.

A firm can stay in business while taking a loss in the short run as long as it covers its

a. fixed costs.

b. variable costs.

c. fixed and variable costs.

d. A firm can never stay in business when it experiences losses.

A comprehensive income tax with few loopholes is efficient because labor

a. supply is very little affected by taxation.

b. demand is very little affected by taxation.

c. supply is highly responsive to taxation.

d. demand is highly responsive to taxation.

Which of the following is a direct tax?

a. excise tax

b. tax on corporate profits

c. property tax

d. sales tax

Governments can most effectively encourage a firm to produce the efficient level of

output of a good whose production causes a beneficial externality by

a. increasing the demand at every price for the good.

b. subsidizing the production of the good.

c. taxing the production of the good.

d. imposing a price ceiling on the good.

When price falls, demand rises.

a. True

b. False

National defense and coastal lighthouses are examples of

a. public goods.

b. private goods.

c. high marginal cost goods.

d. depletable goods.

Which of the following is not true for a public good?

a. Marginal cost of serving public good to one more person is zero.

b. Free rider problem arises in case of public goods.

c. Exclusion is not possible in most of the public goods.

d. Public goods include only material commodities.

An increase in wages in the public sector is always accompanied by an increase in labor

productivity.

a. True

b. False

An appropriate government policy toward negative externalities is to

a. subsidize the activity that creates the negative externality.

b. impose a tax or fine on the activity that creates the negative externality.

c. pay money to the party that creates the negative externality.

d. impose a tax on recipients of the negative externality.

If the government puts price controls on medical care, this will increase the supply of

affordable care in the United States.

a. True

b. False

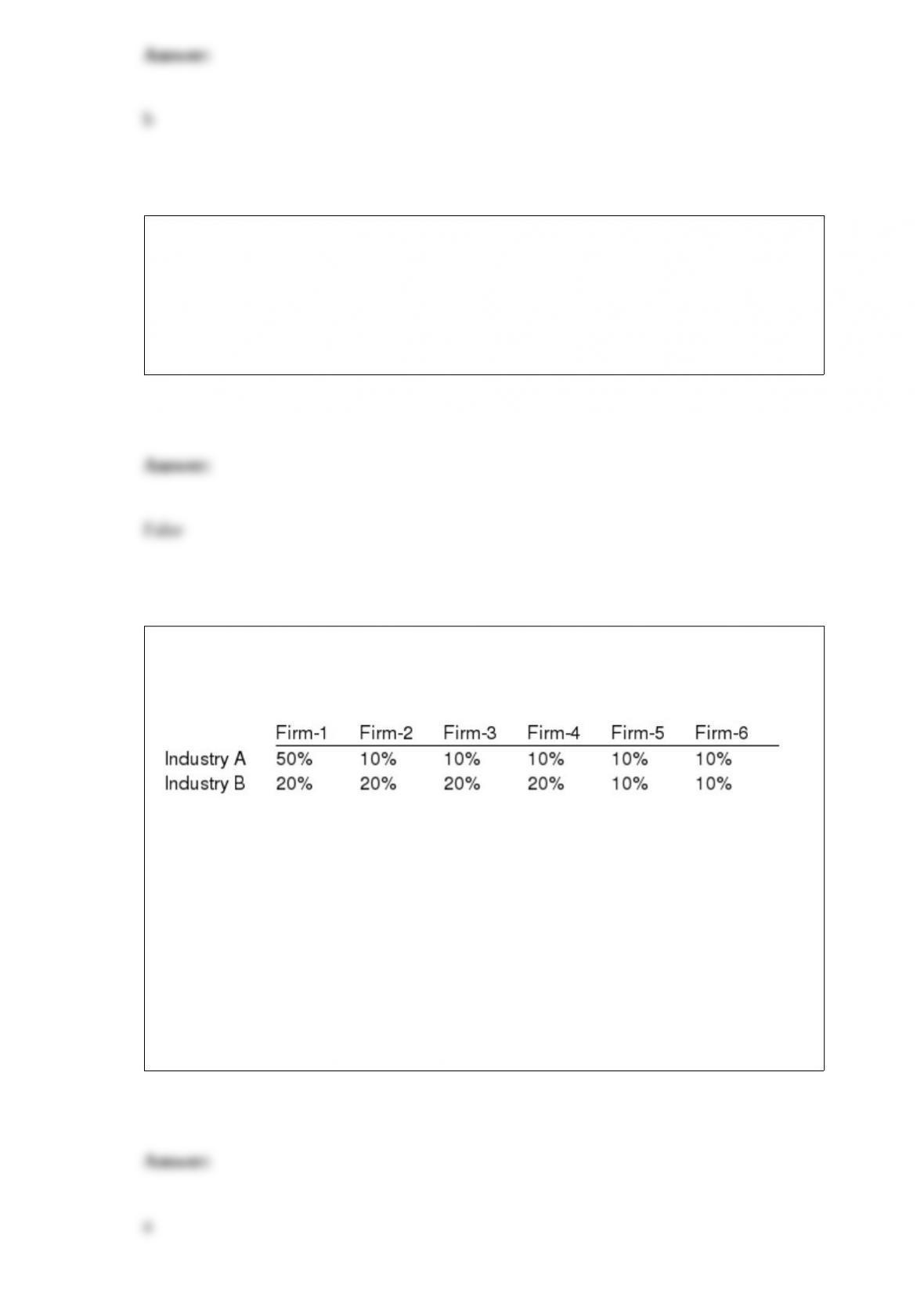

For the two industries with market shares listed below, which of the following would be

true?

Table 13-1

a. The concentration ratio would be the same for both industries but the HHI would be

higher for Industry A.

b. The concentration ratio would be the same for both industries but the HHI would be

higher for Industry B.

c. The HHI would be the same for both industries but the concentration ratio would be

higher for Industry B.

d. Both the concentration ratio and the HHI would be the same for both industries.

Which of the following would be classified as an externality?

a. Smoke from a chimney causes discolored and peeling paint on other houses in the

neighborhood.

b. Noise from an unmuffled car wakes a sleeping person.

c. A neighbor cleans up a yard and repaints a house.

d. All of the above are externalities.

If a firm shuts down in the short run, its losses are equal to

a. TC − TR.

b. TFC.

c. TVC.

d. MC.