The price for labor is the wage rate. What happens to the supply of labor if wages

increase?

a. It increases.

b. It decreases.

c. It does not change.

d. Uncertain-economic theory has no answer to this question.

According to the kinked demand curve model, an oligopolist may face

a. more elastic demand than a monopolistic competitor.

b. less elastic demand than a monopolistic competitor.

c. more elastic demand if she raises her price than if she lowers her price.

d. less elastic demand if she raises her price than if she lowers her price.

Because a monopolist must cut its price to increase its sales by one unit,

a. MR > P at every output level.

b. MC > MR at every output level.

c. P > MR at every output level.

d. MC > P at every output level.

The classic example of a detrimental externality is

a. education.

b. pollution.

c. discovery of an AIDS vaccine.

d. Mrs. Lewis’ prize-winning rose garden.

When comparing industries, a monopolistically competitive industry is less competitive

than an oligopoly.

a. True

b. False

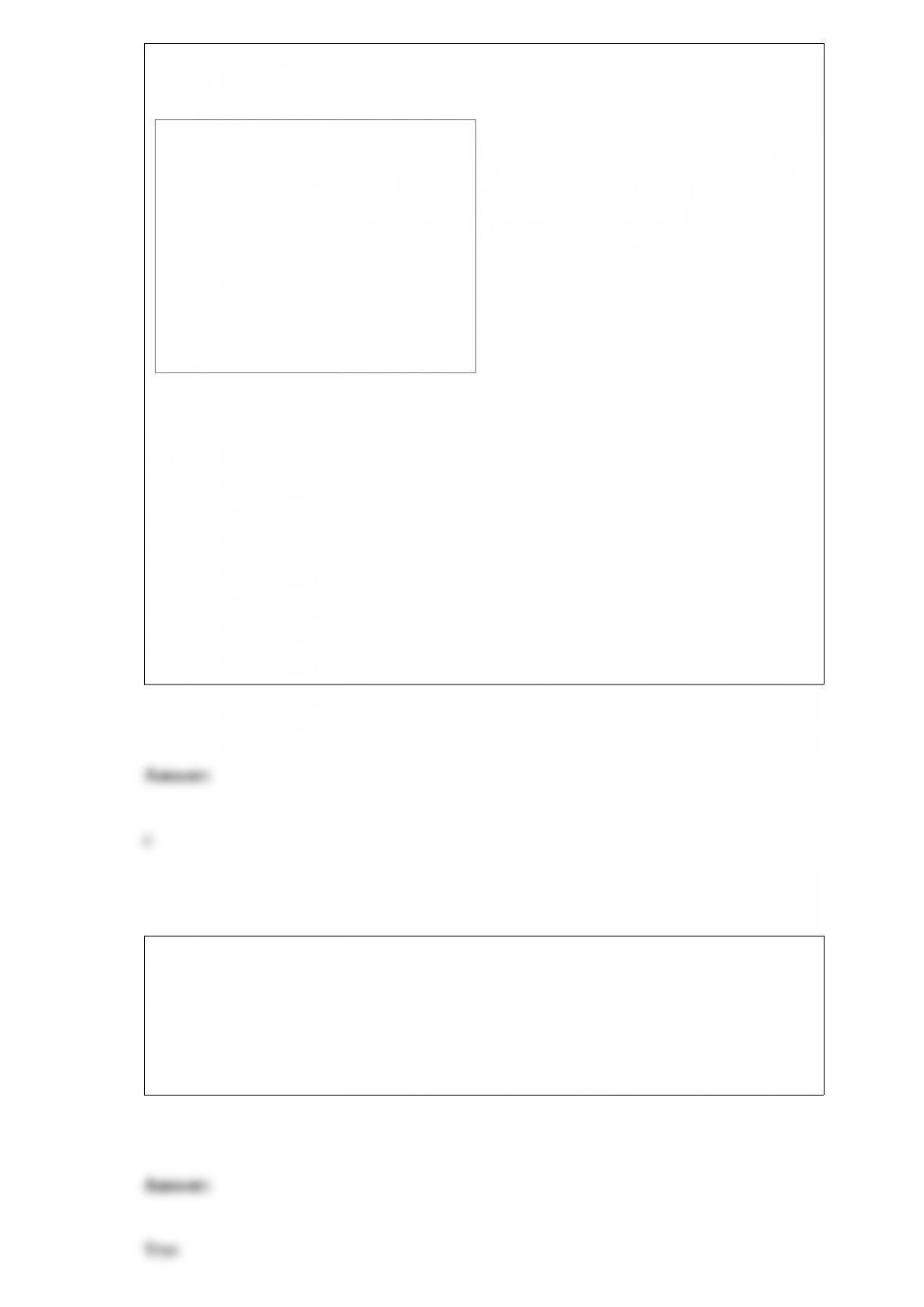

Figure 12-3

In Figure 12-3, demand curve CAD represents a market in which oligopolists will

match the price changes of rivals and demand curve EAB represents a market in which

oligopolists will ignore the price changes of rivals. According to the kinked demand

model, the relevant demand curve will be

a. demand curve CAB.

b. demand curve CAD.

c. demand curve EAD.

d. demand curve EAB.

Price elasticity of demand can be written as percentage change in Q divided by

percentage change in P.

a. True

b. False

Under laissez faire, the allocation of scarce resources among the different industries

a. is possible only with government tax and subsidy policies.

b. is accomplished by the price system.

c. requires a considerable amount of central planning.

d. is the result of consumer planning.

In a market system, the major coordination tasks are carried out

a. with the approval of central planners.

b. as part of the regular appropriation process of Congress.

c. irregularly by the major corporations.

d. automatically by the market mechanism.

Market economies have air and water pollution, but nonmarket economies

a. have much less pollution.

b. have pollution that is much worse than in market economies.

c. have about the same amount of pollution as market economies.

d. don’t generally suffer from external effects of any sort.

Which of the following is more likely be the price elasticity of demand for anti-venom?

a. highly inelastic

b. unit elastic

c. elastic

d. perfectly elastic

Market economies produce outcomes that

a. are virtually ideal in all respects.

b. are inferior to most other systems.

c. are, in some respects, far from ideal.

d. are virtually indistinguishable from command economies.

Usury laws typically regulate

a. interest rates paid on savings.

b. interest rates charged on loans.

c. rents charged on land.

d. economic rent earned in all factor markets.

Some nations that seek to produce all of their own needs face the problem that

a. people don’t want a wide variety of choices when buying.

b. some industries are too small to be efficient.

c. other countries may want to buy from them.

d. All of the above are true.

A market which firms can enter if they choose and exit without losing money invested

is

a. pure monopoly.

b. duopoly.

c. contestable.

d. a market where there are kinked demand curves.

With a monopoly, the consumer’s surplus is lower than it would be with a perfectly

competitive industry.

a. True

b. False

The four-firm concentration ratio for an industry is

a. the number of firms in the industry, divided by four.

b. the share of industry output sold by the four largest firms in the industry.

c. the percentage of total industry profits claimed by the four largest firms.

d. the share of industry output sold by the fourth largest firm in the industry.

The production possibilities frontier illustrates

a. the constant rate of technological progress.

b. the fundamental concept of scarcity.

c. the rapid growth of the U.S. economy.

d. that guns always trade for butter.

Identify the economist who first addressed the environmental problem in terms of

externalities.

a. Joseph Schumpeter

b. Maynard Keynes

c. A.C. Pigou

d. J.B. Say

A worker can always build a chair in four hours. If a chair sells for $40 in a perfectly

competitive market, then the equilibrium wage per hour in a perfectly competitive labor

market is

a. $4.

b. $10

c. $40

d. $160

In the long run, any firm may enter or leave a perfectly competitive market.

a. True

b. False

Rational choice requires that opportunity cost be

a. ignored in making a decision.

b. considered for individual choices, but not for societal choices.

c. computed, but not actually used in making a decision.

d. considered as part of making a decision.

e. used as the sole decision criterion.

Firms in perfect competition are often described as price

a. takers.

b. makers.

c. setters.

d. leaders.

Increased productivity of workers in manufacturing has

a. increased employment in manufacturing.

b. increased employment in agriculture.

c. decreased employment in agriculture.

d. decreased employment in services.

e. increased employment in services.