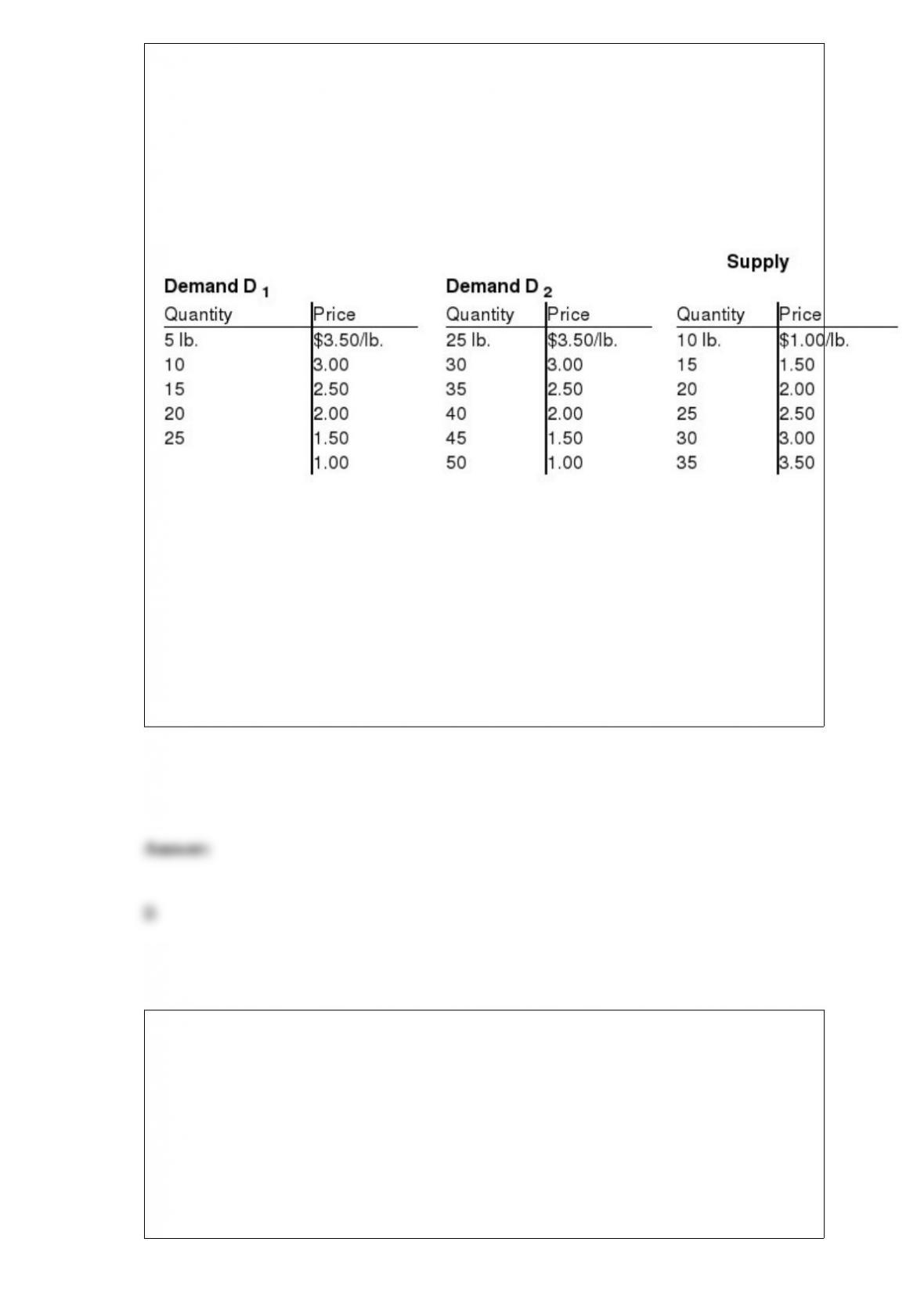

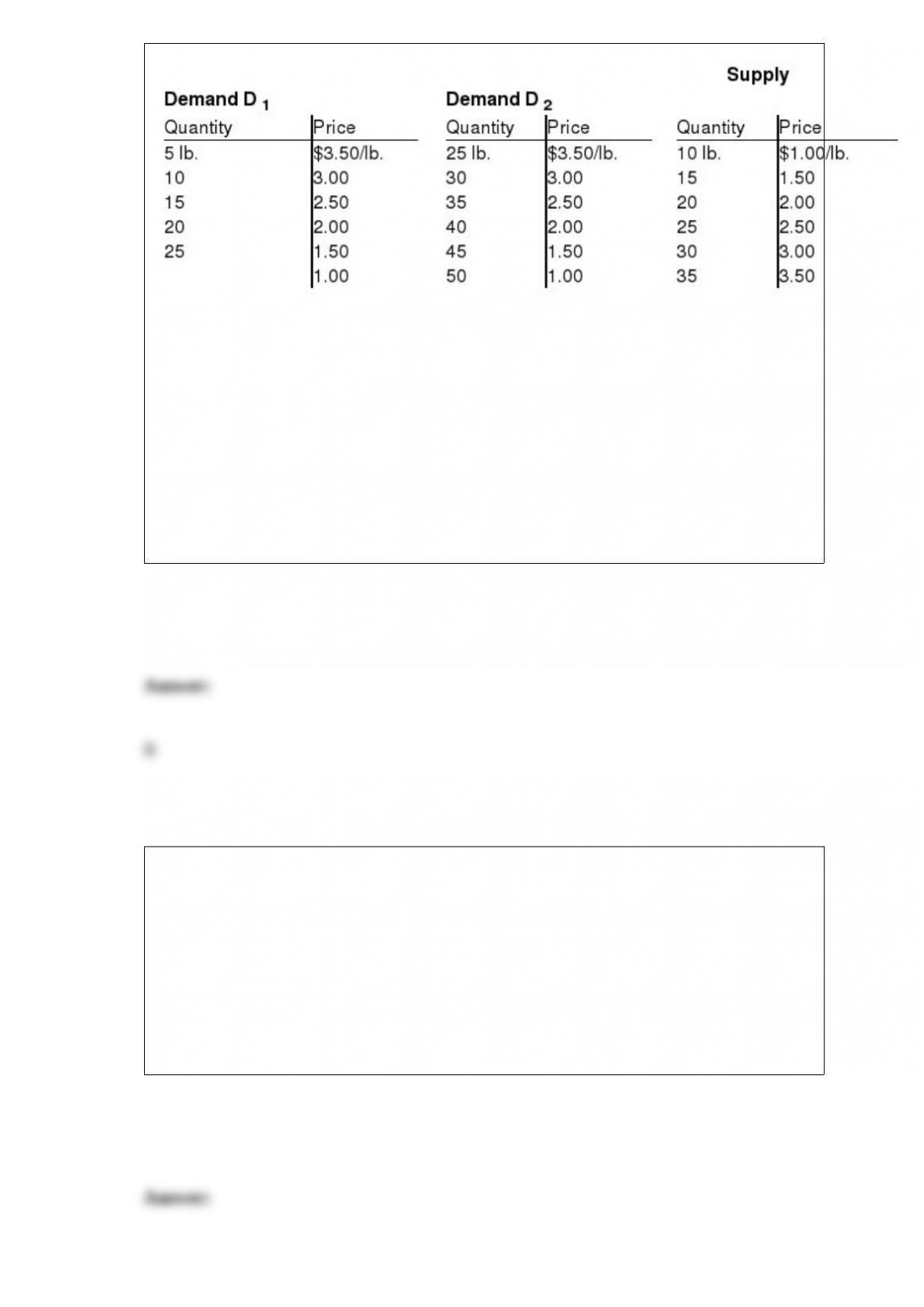

Demand and Supply for Grapes

The following tables show the demand and supply for grapes. Demand is uncertain,

with D1 and D2 each occurring 50% of the time. Suppliers must base their decisions on

the expected price and must sell all grapes they bring to the market at the going market

price.

If suppliers have rational expectations, what will be their expected price of grapes?

a. $2.00 per pound.

b. $2.50 per pound.

c. $3.00 per pound.

d. $3.50 per pound.

A Pigovian tax internalizes an external cost because

a. the cost then enters the decision-making process of the producer.

b. it would be collected by the Internal Revenue Service.

c. the revenue is used to compensate injured parties.

d. no transactions costs are created.

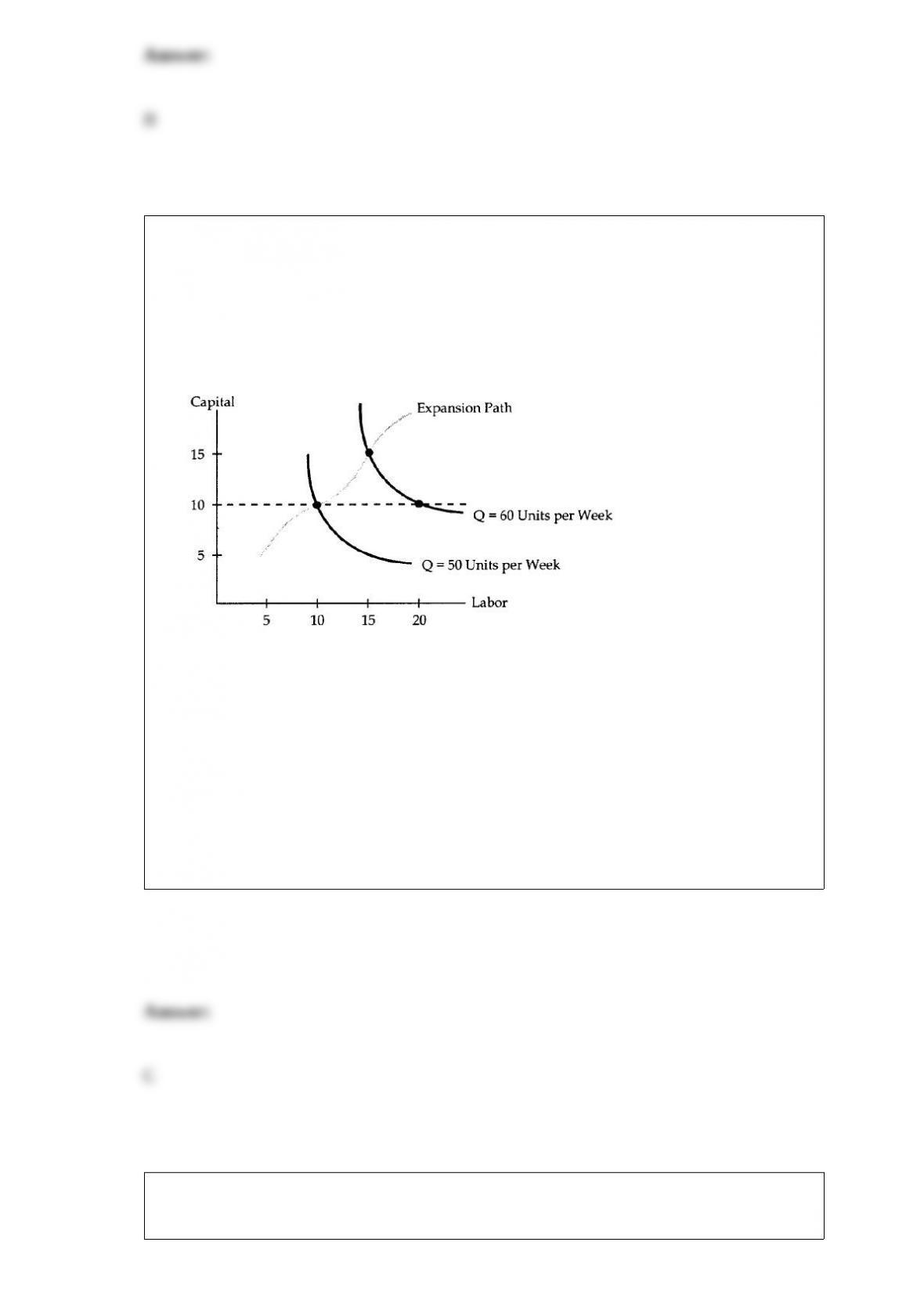

An isoquant shows the various combinations of labor and capital that

a. the firm will choose to employ in the long run.

b. yield the same total cost.

c. can produce some fixed level of output.

d. minimize the firm’s average cost of production.

Cournot Problem. Consider Cournot Duopolists that produce homogeneous goods.

These firms each have constant marginal costs of $10. The market for these firms’

product has demand Q = 100 – P.

In the Nash Equilibrium, each firm will produce.

a. 22.5 units

b. 30 units.

c. 45 units.

d. 90 units.

Cost of Production

The following questions refer to the diagram below. The wage rate is assumed to be $12

per hour, the rental rate is assumed to be $6 per hour, and capital is assumed to be fixed

in the short run at 10 hours.

The short-run average cost of producing 60 units of output per week is

a. $3 per unit.

b. $4.50 per unit.

c. $5 per unit.

d. $9 per unit.

The observation that consumer purchases of pecans decline as the price rises reflects:

a. a decrease in demand.

b. the law of demand.

c. an increase in demand.

d. the law of supply.

The nature preservation services supplied by The Nature Conservancy which buys up

ecologically important but endangered lands, is

a. nonrivalrous and nonexcludable.

b. nonrivalrous and excludable.

c. rival and nonexcludable.

d. a private service.

Caterpillar has spent $5 million to date on a new plant, and another $2 million is needed

to complete the plant. When construction was started, it was projected that production

at the new plant would add $12 million to Cat’s profit, but new projections show the

additional profit will be only $6 million. Assuming the incomplete plant is worthless,

should Cat complete the new plant or abandon it?

a. Cat should complete the plant because it would create a net profit of $4 million.

b. Cat should complete the plant because it would create a net profit of $1 million.

c. Cat should abandon the plant because a $5 million loss is better than a $6 million

loss.

d. Cat should abandon the plant because the plant costs $6 million more than the

expected profit.

If demand rises and supply falls, which of the following must be true?

a. The equilibrium quantity will rise.

b. The equilibrium quantity will fall.

c. The equilibrium quantity will not change.

d. The change in the equilibrium quantity is indeterminate.

When will setting a relatively high entry fee and a low competitive price be the best

strategy for a two-part tariff monopolist?

a. When the customers are nearly identical.

b. When the customers have inelastic demand for the product.

c. When the customers place a relatively low value on their time.

d. When the customers can be separated into a number of diverse groups.

A competitive firm will exit an industry in the long run when the market price falls

below its

a. marginal revenue.

b. marginal cost.

c. average cost.

d. average variable cost.

Demand and Supply for Grapes

The following tables show the demand and supply for grapes. Demand is uncertain,

with D1 and D2 each occurring 50% of the time. Suppliers must base their decisions on

the expected price and must sell all grapes they bring to the market at the going market

price.

If people have rational expectations, then they

a. are correct at least 50% of the time.

b. do not make systematic and correctable errors in prediction.

c. sometimes overestimate, but never underestimate, economic variables.

d. revise their expectations upward when their predictions are too low and downward

when they are too high.

In popular usage the term investor is used to refer to

a. a speculator in futures markets.

b. a buyer of risky assets.

c. an entrepreneur who purchases machinery and equipment to expand production.

d. individuals whose primary source of income is from returns on financial assets.

An equilibrium in which each individual optimizes, taking market prices as given, is

called

a. a Nash equilibrium.

b. a Walrasian equilibrium.

c. an Edgeworth equilibrium.

d. a robust equilibrium.

According to the law of one price,

a. there exists only one price that will clear a competitive market.

b. the long-run price of a commodity will equal the marginal cost of production.

c. identical goods will sell for identical prices.

d. the price of a good must equal the value of the labor used to produce it.

When a sales tax of 20¢ per soda is imposed on soda consumption, the supply curve for

soda shifts down by precisely 20¢ per soda.

Suppose that good X is on the horizontal axis and all other goods (measured in dollars)

are on the vertical axis in the consumer-choice diagram. If the consumer gains $10 in

income, then

a. the new budget line is parallel to and lies 10 units to the left of the old budget line.

b. the budget line shifts up by 10 dollars, with no change in the slope.

c. the vertical intercept of the budget line shifts up by $10, but the horizontal intercept

remains unchanged.

d. the slope of the budget line increases by 10 percent.

The marginal cost curve crosses

a. only the average variable cost curve at its bottom.

b. both the average cost curve and the average variable cost curve at their bottoms.

c. only the average cost curve at its bottom.

d. the marginal product curve at its maximum.

Suppose regulators impose a price ceiling on a monopoly. If the price ceiling is set

below the monopoly price but above the competitive price, then the monopoly will

a. reduce its output.

b. increase its production.

c. produce the same output at a lower price.

d. earn zero profit.

According to the law of large numbers, when a gamble is repeated many times,

a. the average outcome increases.

b. the average outcome is the expected value.

c. the probability of each outcome changes.

d. insurance becomes less profitable when many people buy it.

In the copycat game, there

a. is one Nash equilibrium.

b. are two Nash equilibria.

c. all the outcomes are Nash equilibria.

d. no matter what Ditto chooses, Dot would prefer the other activity.

Suppose that the average football player earns $1 million per year and that there are 500

players. The average school teacher earns $25,000 per year and there are 1 million

teachers. From this we can say that

a. football players are paid too much.

b. teachers are paid too little.

c. the group of football players must be more valuable than teachers as a group.

d. teachers as a group are more valuable than the group of football players.

New England Company plans to build a power plant on the Charles River. By using

river water to cool its plant, the river’s water temperature will rise enough that trout will

no longer survive, much to the dismay of local fishers. The loss of value to the fishers is

estimated as $100,000. The transactions costs of a side payment from either side to the

other are prohibitive of any agreement. Therefore, if the property right to the water is

worth

a. more than $100,000 to New England Company, who gets the right would not matter.

b. more than $100,000 to New England Company, efficiency dictates giving the right to

the fishers.

c. more that $100,000 to New England Company, efficiency dictates giving the right to

New England Company.

d. less than $100,000 to New England Company, efficiency dictates giving the right to

New England Company.

When is the law of demand violated for labor?

a. Never.

b. When the substitution and scale effects are in opposition, with the scale effect being

the larger.

c. When labor is a regressive factor.

d. When labor earns zero economic rent.

A compensated demand curve contains no

a. income effects.

b. substitution effects.

c. price elasticity.

d. income compensation.

Suppose that an indifference curve for Jack is drawn measuring quantities of pencils

along the horizontal axis and quantities of pens along the vertical axis. If the marginal

value of an additional pencil is 3 pens for Jack, the slope of his indifference curve in

this range is

a. 1/3.

b. 3.

c. 6.

d. dependent upon the prices of the two goods

According to most economists, when can government debt lead to higher interest rates?

a. Always.

b. Never.

c. When government spends money wastefully.

d. When misperceptions or default risks are significant.

Each additional unit of output produced by a unit of labor is valued at the price of the

firm’s output

a. always.

b. when the firm is selling in a competitive market.

c. when the firm has monopoly power in the market for its output.

d. when the firm has monopsony power in the market for labor.

When offered a bet at unfair odds, a risk-neutral individual will

a. not bet.

b. bet everything on the outcome favored by the unfair odds.

c. bet everything on the outcome not favored by the unfair odds.

d. be indifferent about the amount that he bets.

The market line must

When offered a bet at fair odds, a risk-neutral individual

a. accepts the bet if it is sufficiently small.

b. always wagers everything on one outcome or the other.

c. is indifferent about the amount that he bets.

d. chooses a risk-free basket of outcomes.

For which type of job would you expect to see a compensating differential?

a. An accountant.

b. A police officer.

c. A senator.

d. A tele-marketer.

This firm’s fixed costs are

a. zero.

b. $100.

c. $230.

d. cannot be determined without specifying the output level.

A simultaneous increase in both the demand for computers and the supply of computers

must increase

a. the number of computers bought and sold.

b. the price of computers.

c. both the equilibrium price and quantity of computers.

d. the shortage of computers in the market.

Demand in the apricot market can be expressed as P=100-Q. Further, the supply

function in the apricot industry is P=10+Q. If a social planner specifies that 20 units be

produced, is that level of production efficient? Can you propose a more efficient level

of production? Explain why your proposed level is better than that of the social planner.

At Olive’s Oranges customers may pick oranges from a 100-tree orchard at the price of

15¢ per orange. Olive’s orchard currently produces 8,000 oranges annually. Olive

estimates that installing a new irrigation system would increase her annual yield by 200

oranges, beginning next year. The irrigation system requires an immediate cost of $600.

In the Prisoners’ Dilemma game, the only outcome that is not Pareto optimal is also the

game’s only Nash equilibrium.

Normative criteria are used to analyze the desirability of economic outcomes.

Because the duopolists find it hard to act like a cartle in the Cournot setting, it follows

that there is deadweight loss in that market.

A nuclear disaster is an uninsurable risk because it would adversely affect a large

number of people simultaneously.

An indifference curve is a construct used by economists to show how tastes for an

individual change.

Contestable market conditions will cause a natural monopoly to produce the

competitive quantity.

For a competitive firm, marginal revenue is constant and equal to the market price.

Negligence is irrelevant when a strict liability standard is applied.

A businessman is confronted with the following opportunity. He can invest $10,000 in a

project that will either succeed wildly, fail miserably, or simply pay him back his

$10,000. If wildly successful, the project will earn the businessman $110,000, but if it

fails he will not get any money back.

If employers had to pay higher than equilibrium wages to their workers, then workers

would be better off but employers would be worse off.

A perpetuity is a bond with an established maturity date.

An industry’s demand curve for labor coincides with the horizontal sum of the

individual firms’ labor demand curves.

If the demand for a good is high, then there will be a shortage of that good.

A noncongested toll road is an example of a good that is excludable, but not rival in

consumption.

Stockholders can use high levels of compensation and substantial severance payments

to get their corporate executives to take on higher levels of risk.

If an Engel curve is downward sloping, then one of the two goods must be inferior.