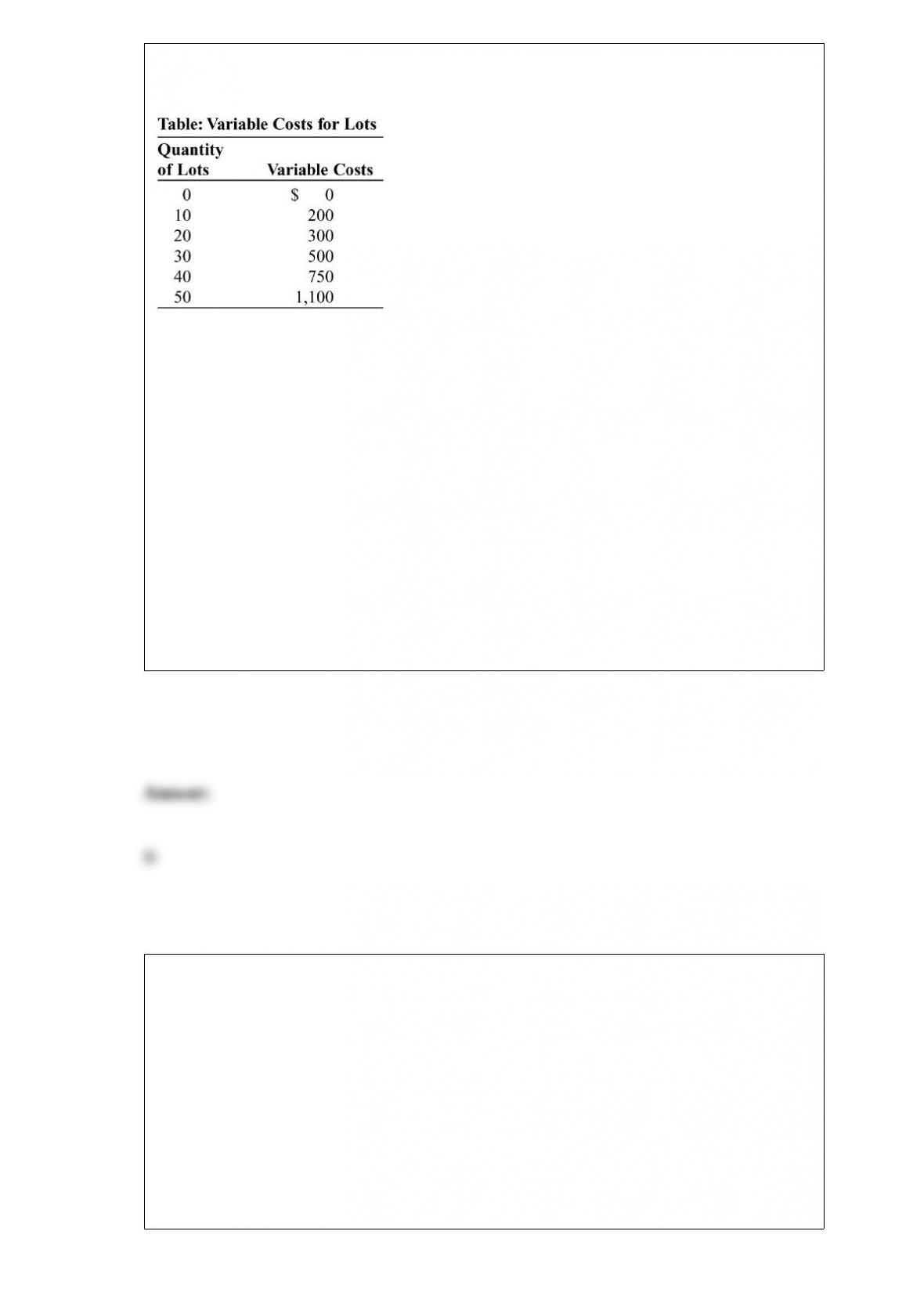

(Table: Variable Costs for Lots) Look at the table Variable Costs for Lots. During the

winter, Alexa runs a snow-clearing service in a perfectly competitive industry. Assume

that costs are constant in each interval; that is, the variable cost of clearing anywhere

from 1 through 10 lots is $200. Her only fixed cost is $1,000 for a snowplow. Her

variable costs include fuel, her time, and hot coffee. At what price does Alexa’ s

short-run supply curve start?

A) $200

B) $15

C) $50

D) $42

In a single year, the Netherlands can raise 100 tons of beef or produce 1,000 boxes of

tulips. In the same growing season, Belgium can raise 50 tons of beef or produce 750

boxes of tulips. In autarky, the opportunity cost of 1 ton of beef in the Netherlands is:

A) 100 tons of beef.

B) 1,000 boxes of tulips.

C) 10 boxes of tulips.

D) 0.1 box of tulips.

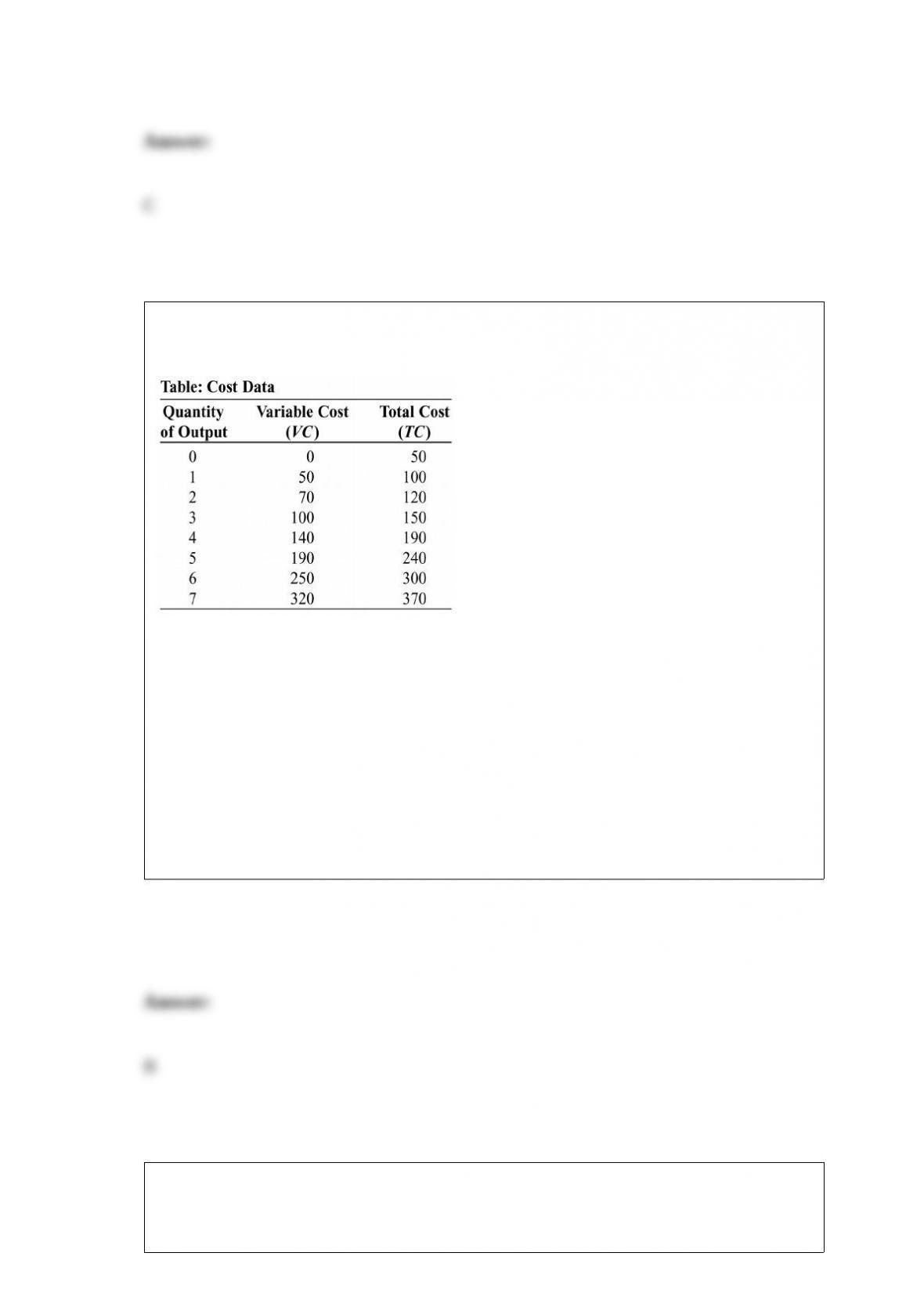

(Table: Cost Data) Look at the table Cost Data. The marginal cost of producing the fifth

purse is:

A) $60.

B) $50.

C) $35.

D) $20.

A firm’s marginal cost is:

A) the ratio of the change in fixed cost to the change in the quantity of output.

B) the slope of the total cost curve.

C) the slope of the average variable cost curve.

D) the ratio of the change in total output to the change in the quantity of labor.

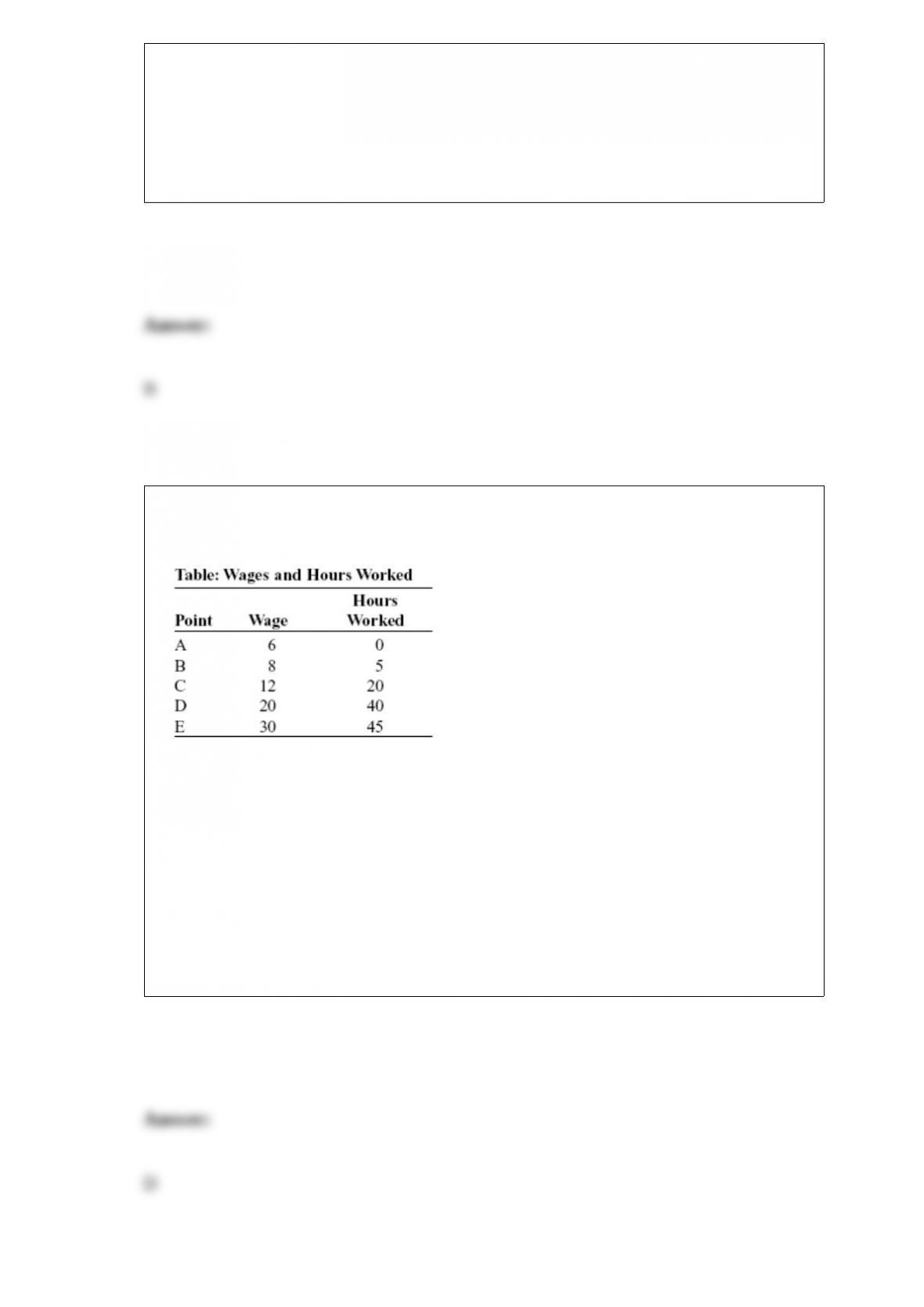

(Table: Wages and Hours Worked) Look at the

table Wages and Hours Worked. Graphing the relation with wages on the vertical axis

and hours worked on the horizontal axis, the slope between point A and point B is:

A) 2.5.

B) 5.

C) 2.

D) 2/5.

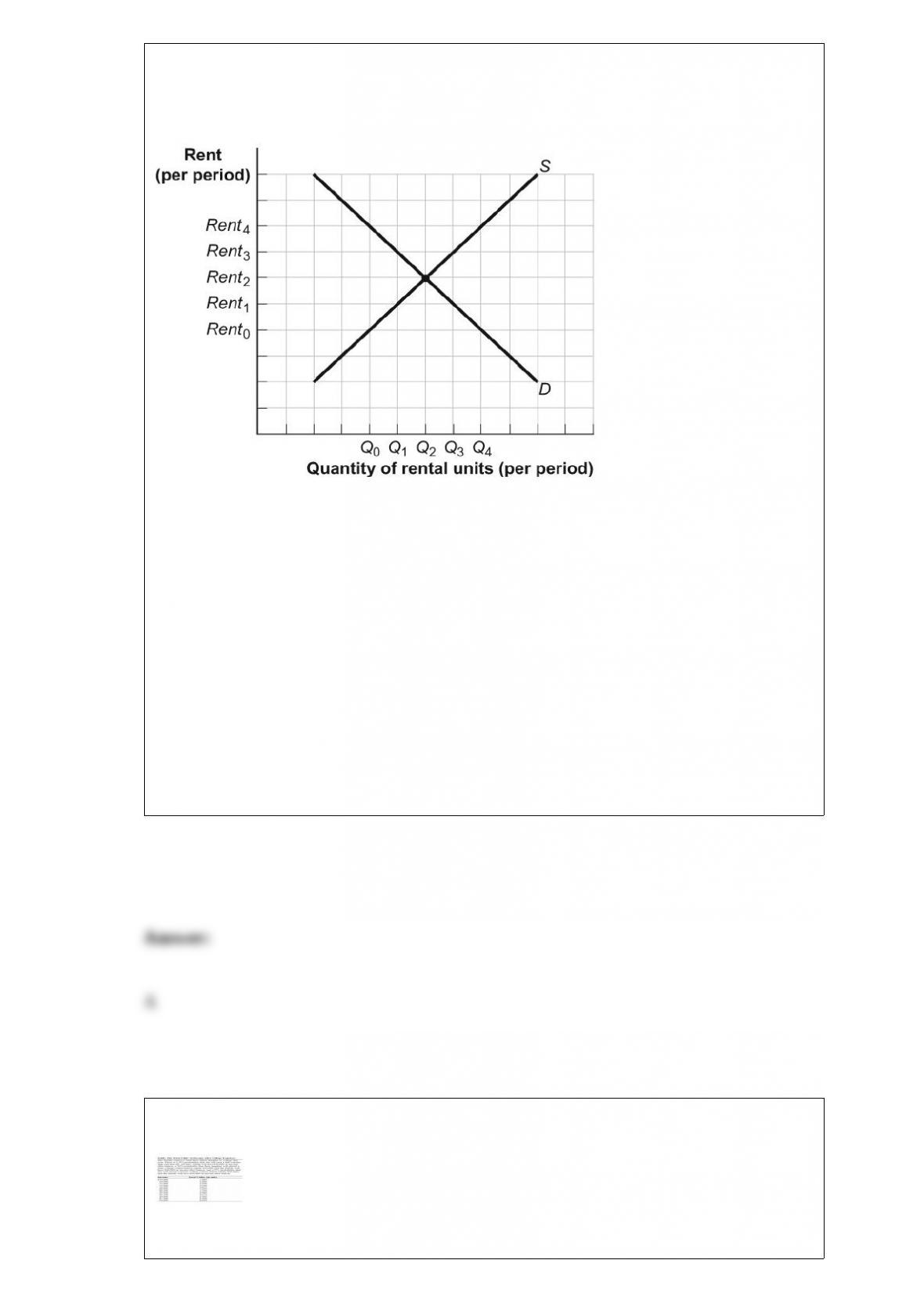

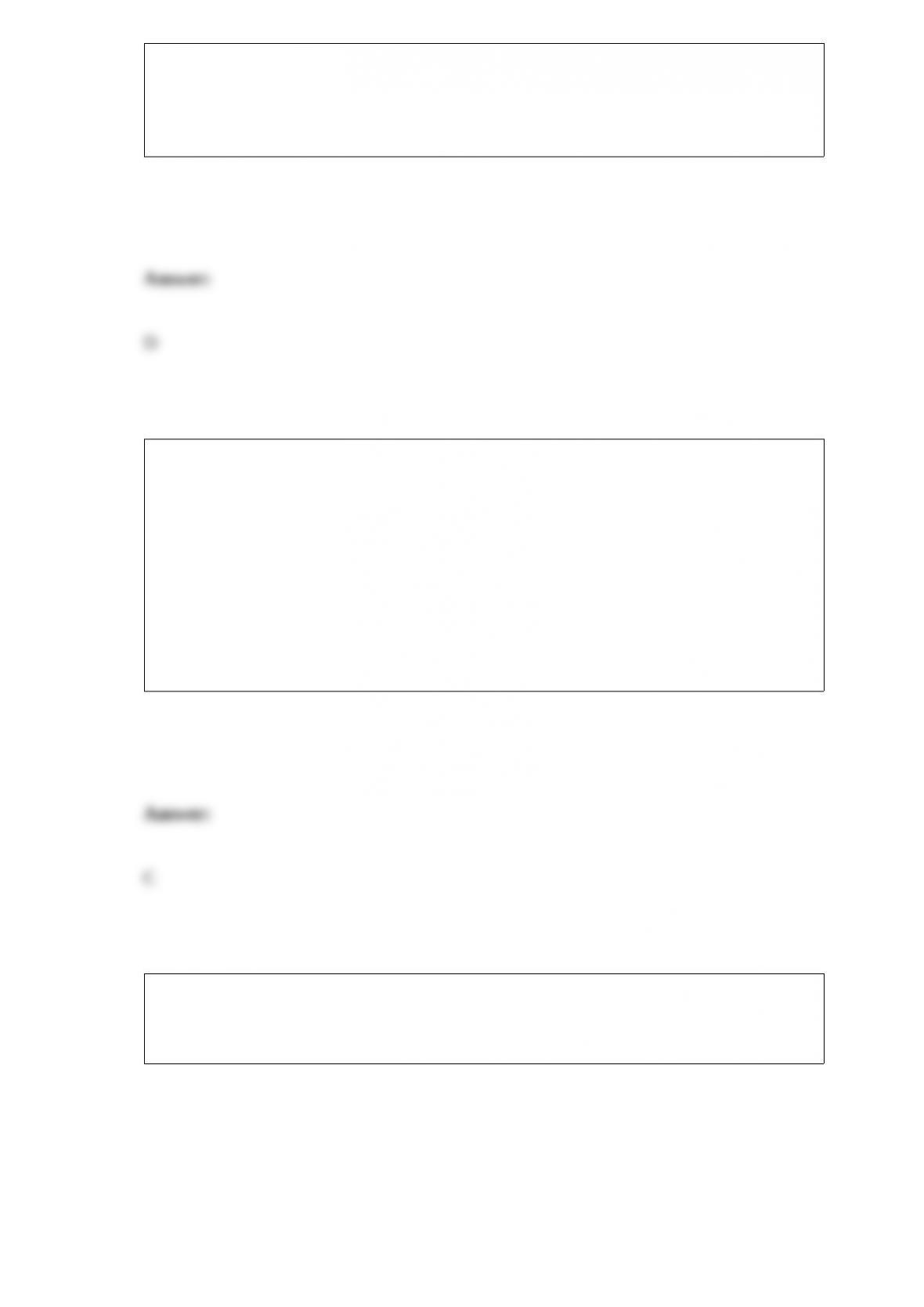

Figure: Rent Controls

(Figure: Rent Controls) Look at the figure Rent Controls. If rent controls are set at

Rent1:

A) the shortage of rental units is the distance Q3 ” Q1.

B) some renters will be willing to pay a price as high as Rent4 for Q1 units.

C) no one will have to pay a higher actual price than Rent0, nor will anyone be willing

to do so.

D) there will be a surplus of rental units, but it is impossible to tell how large the

surplus is based on the information provided.

(Table: Total Utility of Income After College Expenses) Look at the table Total Utility

of Income After College Expenses. Mr. and Mrs. Smith would be willing to pay as

much as _____ for insurance to pay their daughter’s tuition and eliminate the

uncertainty in the family’s income after tuition.

A) $12,000

B) $10,000

C) $8,000

D) $5,000

Ellen consumes goods X and Y. As she consumes less X, she must be compensated with

additional units of Y, and her marginal rate of substitution of X for Y decreases as she

consumes more Y. This means that goods X and Y are:

A) ordinary.

B) unique.

C) complements.

D) substitutes.

The short-run shut-down price is:

A) the price at which economic profit is zero.

B) the minimum of the AVC curve.

C) the intersection of the MC and ATC curves.

D) the minimum of the AFC curve.

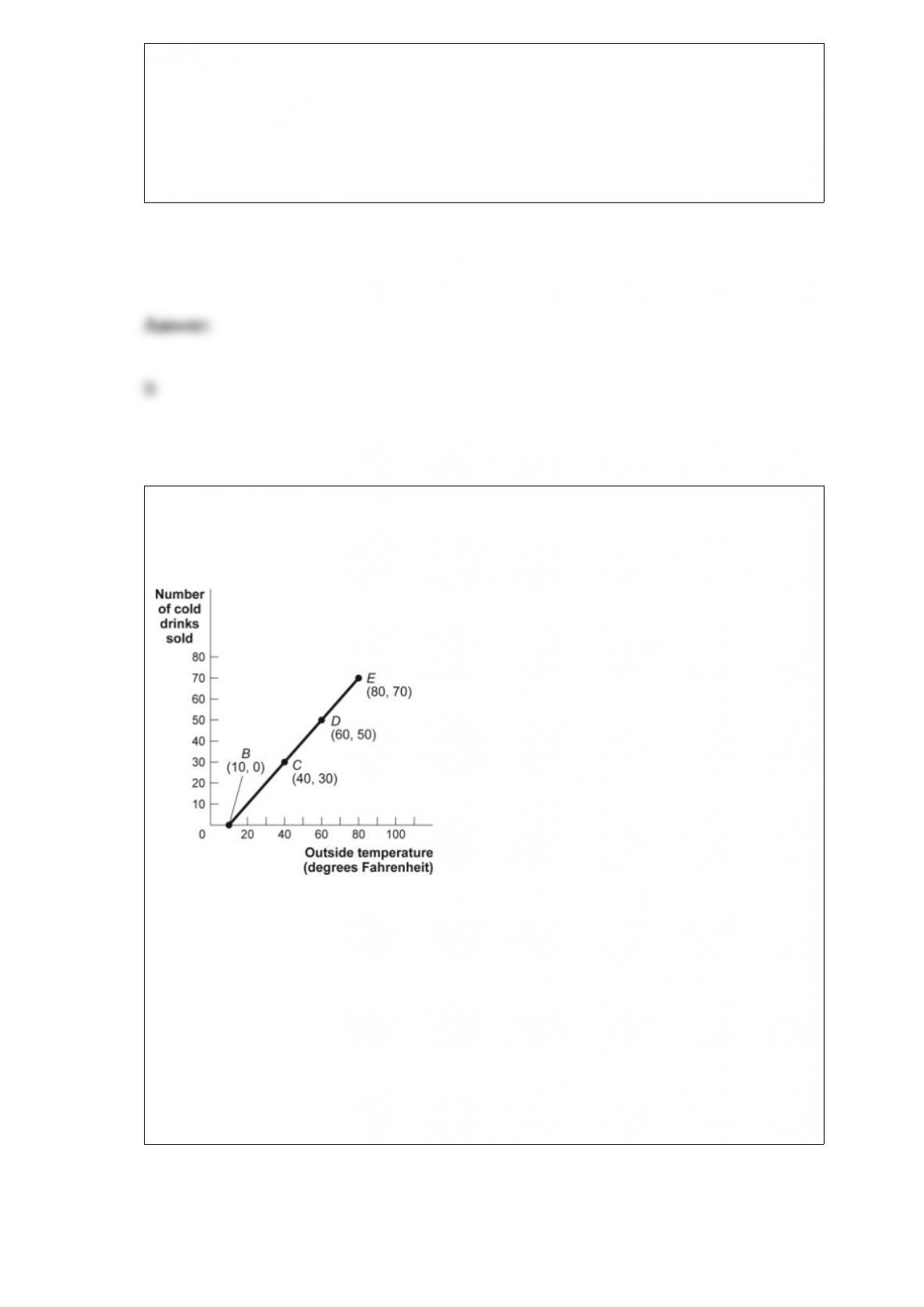

Figure: Cold Drinks Sold and Temperature

(Figure: Cold Drinks Sold and Temperature)

Look at the figure Cold Drinks Sold and Temperature. If we move from point B to point

C in the figure, the outside temperature has ______ degrees and the number of cold

drinks sold has ______.

A) decreased by 30; decreased by 30

B) increased by 20; increased by 20

C) increased by 30; increased by 30

D) increased by 40; increased by 40

Which of the following is a normative statement?

A) The rate of unemployment is 9%.

B) A high rate of economic growth creates jobs.

C) The federal government spends half of its budget on national defense.

D) Everyone in the United States deserves to be covered by national health insurance.

An ambiguous change in price and a decrease in quantity are most likely caused by:

A) no shift in supply and a shift to the left in demand.

B) a shift to the left in supply and a shift to the left in demand.

C) a shift to the right in supply and a shift to the left in demand.

D) a shift to the left in supply and a shift to the right in demand.

The production possibility frontier is bowed out because:

A) resources are not equally suited for the production of both goods.

B) resources are scarce.

C) economic growth leads to inefficiency.

D) resources are inefficiently used.

Figure: Unemployment Rate over Time

(Figure: Unemployment Rate over Time) Look

at the figure Unemployment Rate over Time. In the time-series graph, as we move from

the beginning of 2001 to the beginning of 2003, we see that the unemployment rate has

_____ from approximately _____ to approximately _____.

A) decreased; 5%; 4%

B) increased; 5.3%; 7.3%

C) decreased; 7.7%; 5.5%

D) increased; 4%; 6%

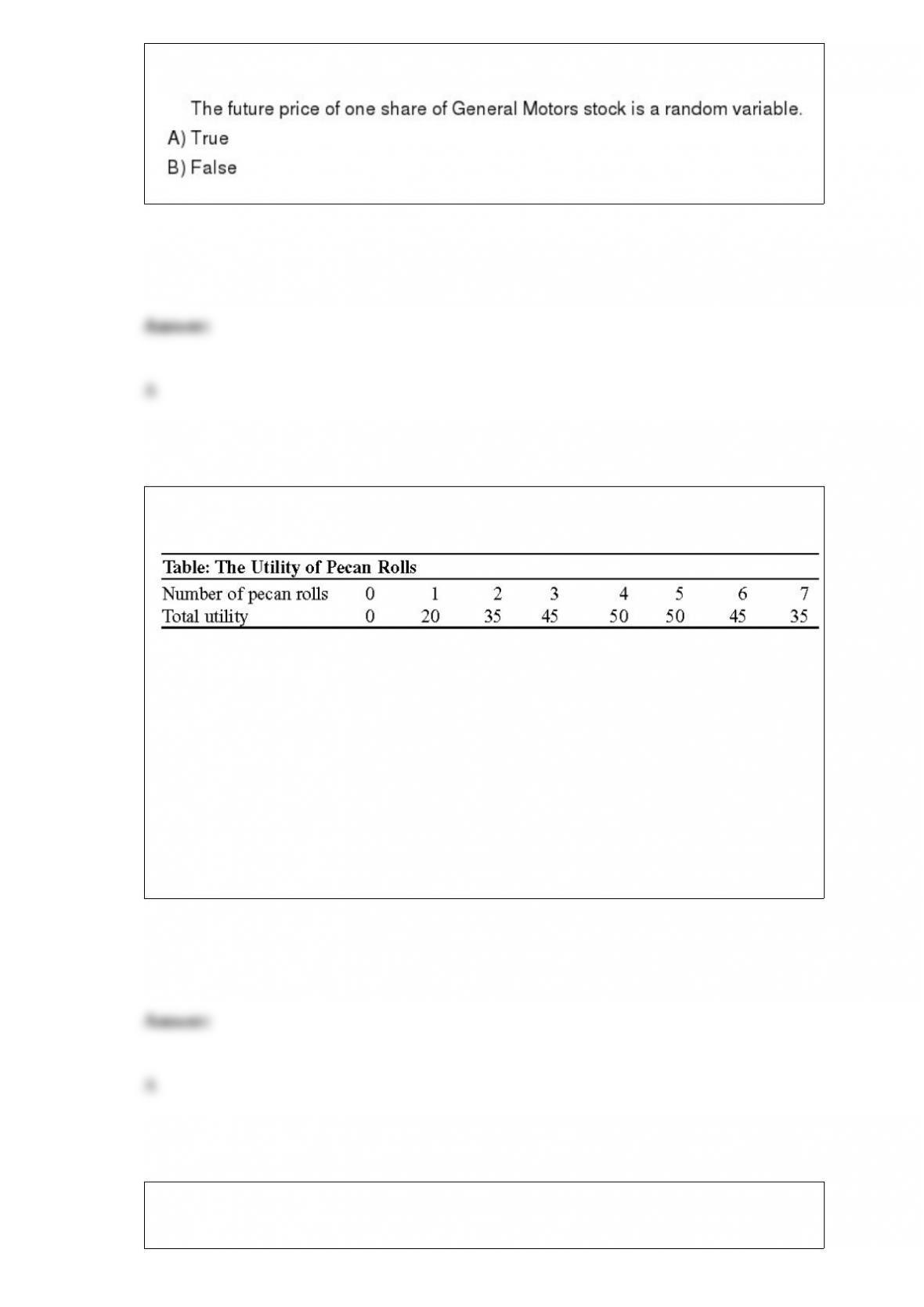

(Table: The Utility of Pecan Rolls) Look at the table The Utility of Pecan Rolls.

Marginal utility begins to diminish at the _____ roll.

A) second

B) third

C) fifth

D) sixth

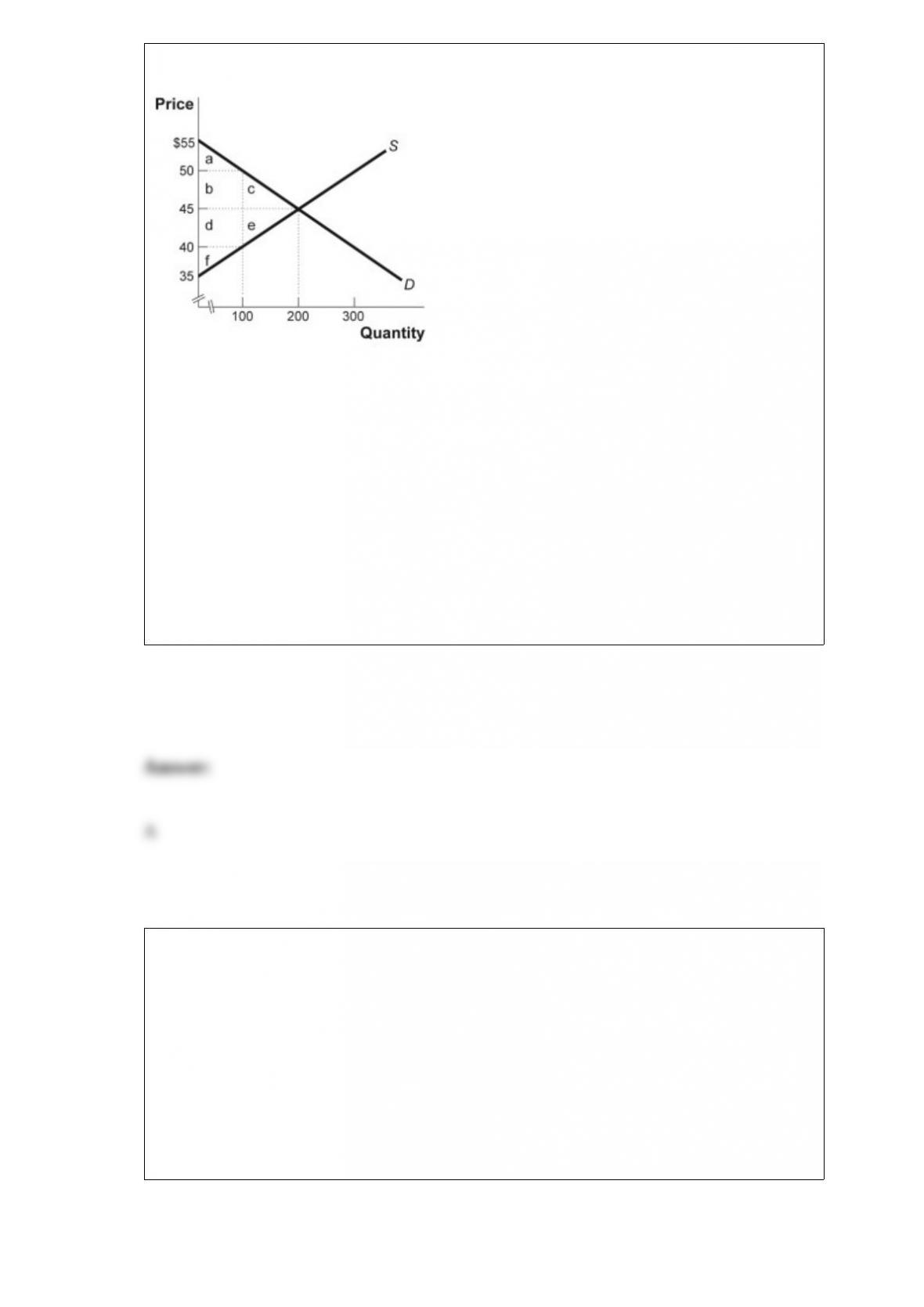

Figure: The Market for Blue Jeans

(Figure: The Market for Blue Jeans) Look at the figure The Market for Blue Jeans. The

government recently levied a $10 tax on the producers of blue jeans. What area or areas

in the graph identify the loss of producer surplus due to the tax?

A) d + e

B) e

C) d

D) d + e + f

Nara has gone to three movies this week. She has some extra money, so she decides to

go to another. This statement best represents this economic concept:

A) Resources are scarce.

B) The real cost of something is what you must give up to get it.

C) “How much” is a decision at the margin.

D) There are gains from trade.

No individual is willing to pay to provide the efficient level of a public good, since the:

A) marginal cost of production is zero.

B) good will be nonrival and thus underconsumed.

C) individual’s marginal benefit is less than the marginal social benefit.

D) marginal benefit of allowing one more individual to consume the good is zero.

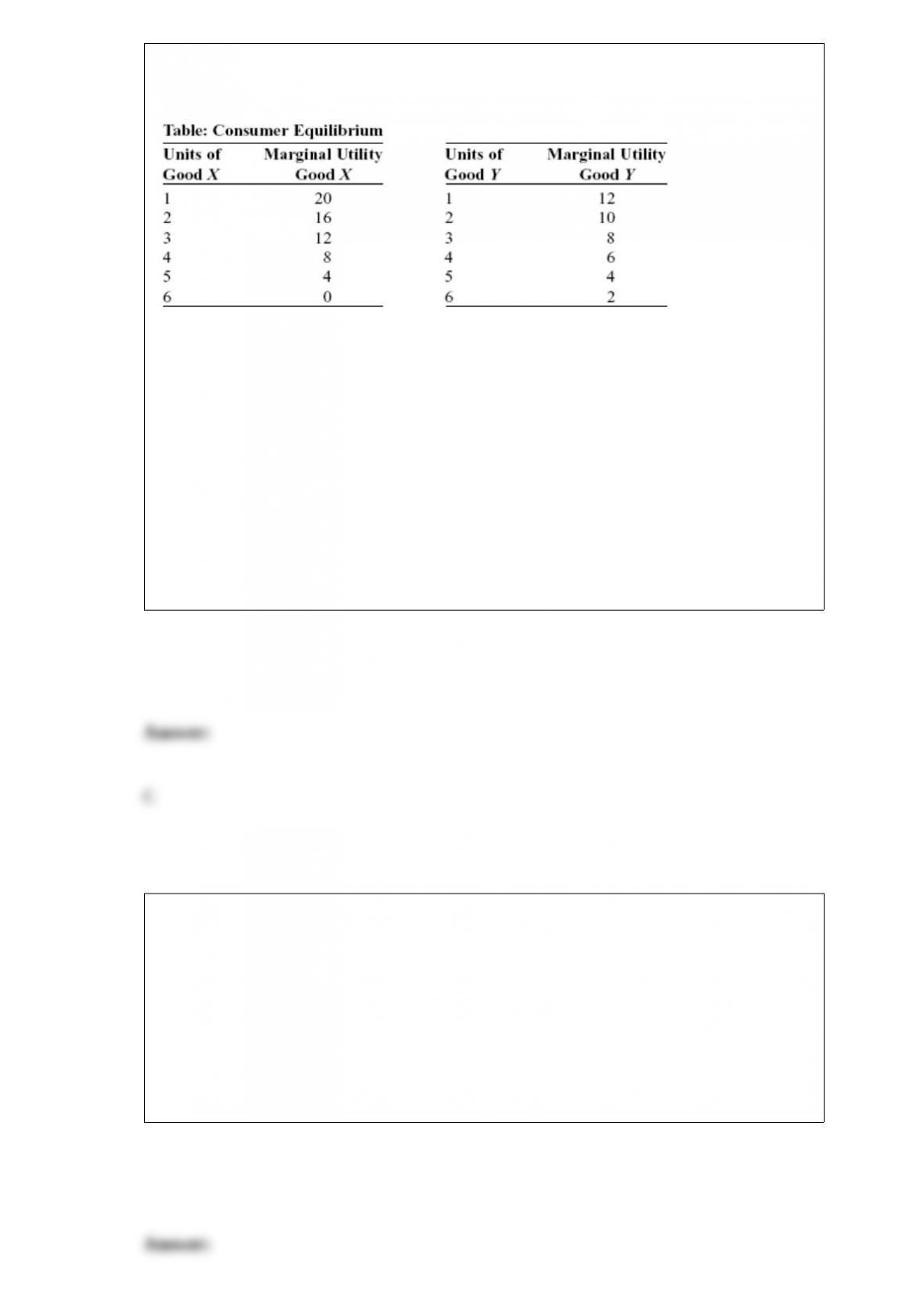

(Table: Consumer Equilibrium) Look at the table Consumer Equilibrium. Assume that

goods X and Y both cost $1 per unit and you have $7 to spend on both goods. To

maximize utility, you would consume _____ units of X and _____ units of Y.

A) 2; 5

B) 3; 4

C) 4; 3

D) 5; 2

The largest component of the factor distribution of income in the United States is:

A) interest and rents.

B) taxes.

C) corporate profits.

D) compensation of employees.

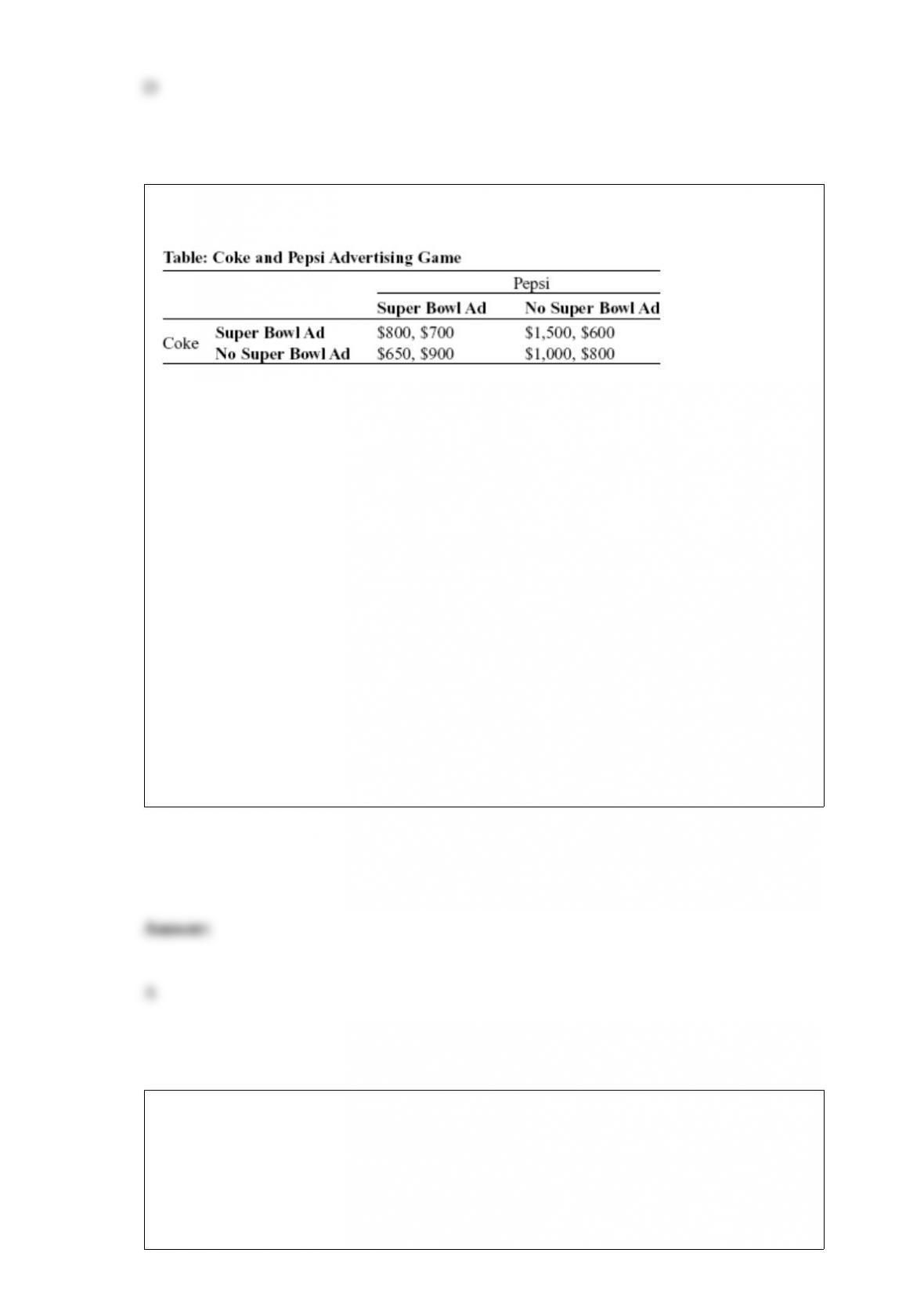

(Table: Coke and Pepsi Advertising Game) Look at the table Coke and Pepsi

Advertising Game. The soft-drink industry is dominated by Coke and Pepsi, and each

firm spends a lot of money on advertising. Suppose each firm is considering a costly

television commercial during halftime of the Super Bowl. The table shows the payoff

matrix of profits that each firm would receive from its advertising decision, given the

advertising decision of their rival. Profits in each cell of the payoff matrix are given as

(Coke, Pepsi). If each firm makes the decision whether to advertise on the Super Bowl

independently, the Nash equilibrium is for Coke _____ and Pepsi _____ during the

Super Bowl.

A) to advertise; to advertise

B) not to advertise; not to advertise

C) not to advertise; to advertise

D) to advertise; not to advertise

Industries that are made up of many competing producers, each selling a differentiated

product, and whose firms earn zero economic profits in the long run are:

A) perfectly competitive.

B) monopolies.

C) oligopolies.

D) monopolistically competitive.

The principal government agency in the United States responsible for enforcing

national environmental policies is the:

A) Department of Agriculture.

B) Department of the Interior.

C) Environmental Protection Agency.

D) Department of Justice.

Figure: Rent Controls

(Figure: Rent Controls) Look at the figure Rent Controls. Suppose that rent controls are

imposed. If the government wanted a rent control ceiling to be effective immediately,

what is one possible price to set?

A) Rent3

B) Rent4

C) Rent1

D) Rent2

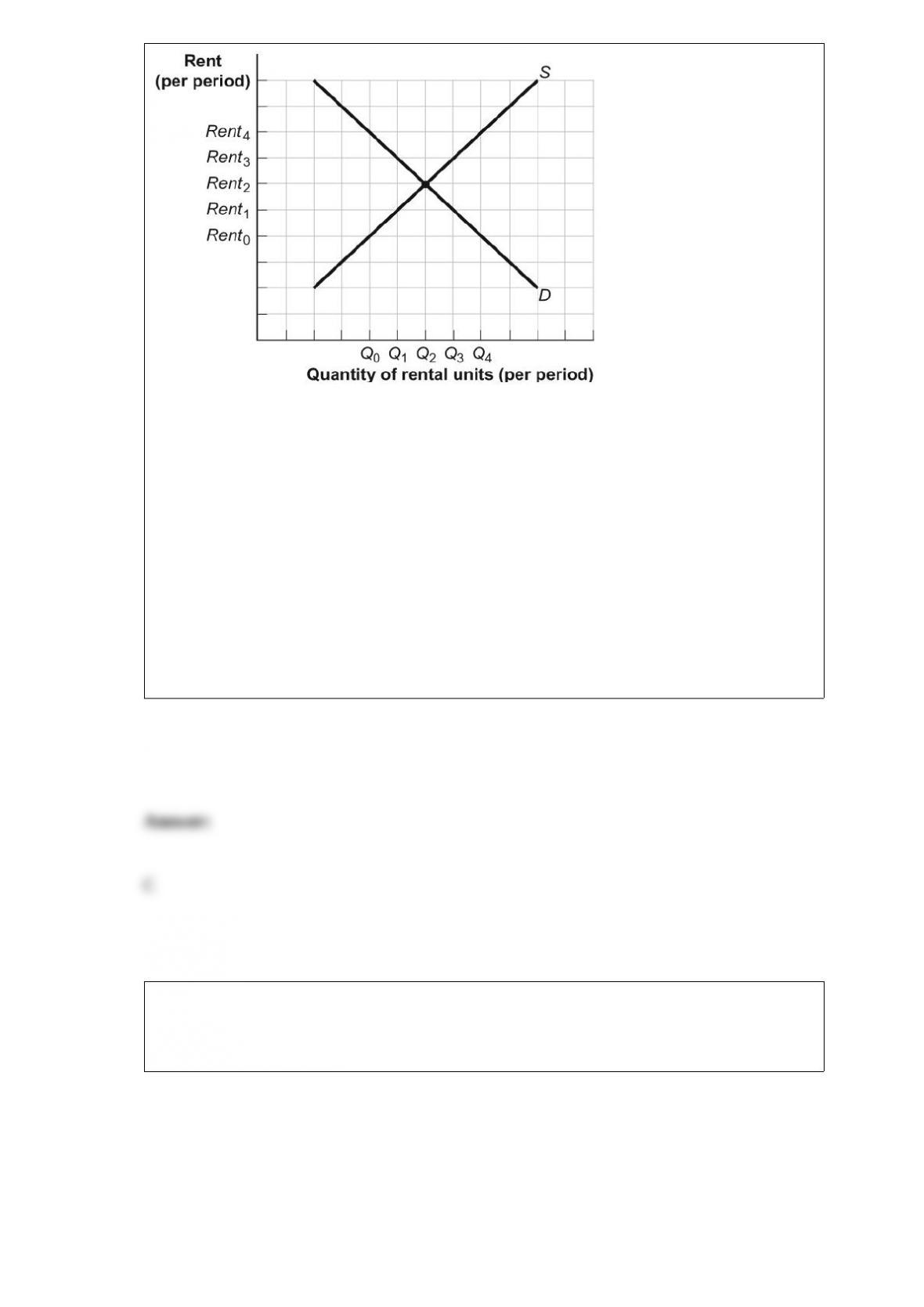

Figure: Supply and Demand

(Figure: Supply and Demand) Look at the figure Supply and Demand. A price ceiling of

P1 causes:

A) a shortage equal to the distance AB.

B) a surplus equal to the distance AB.

C) a shortage equal to the distance DE.

D) no change to the market.

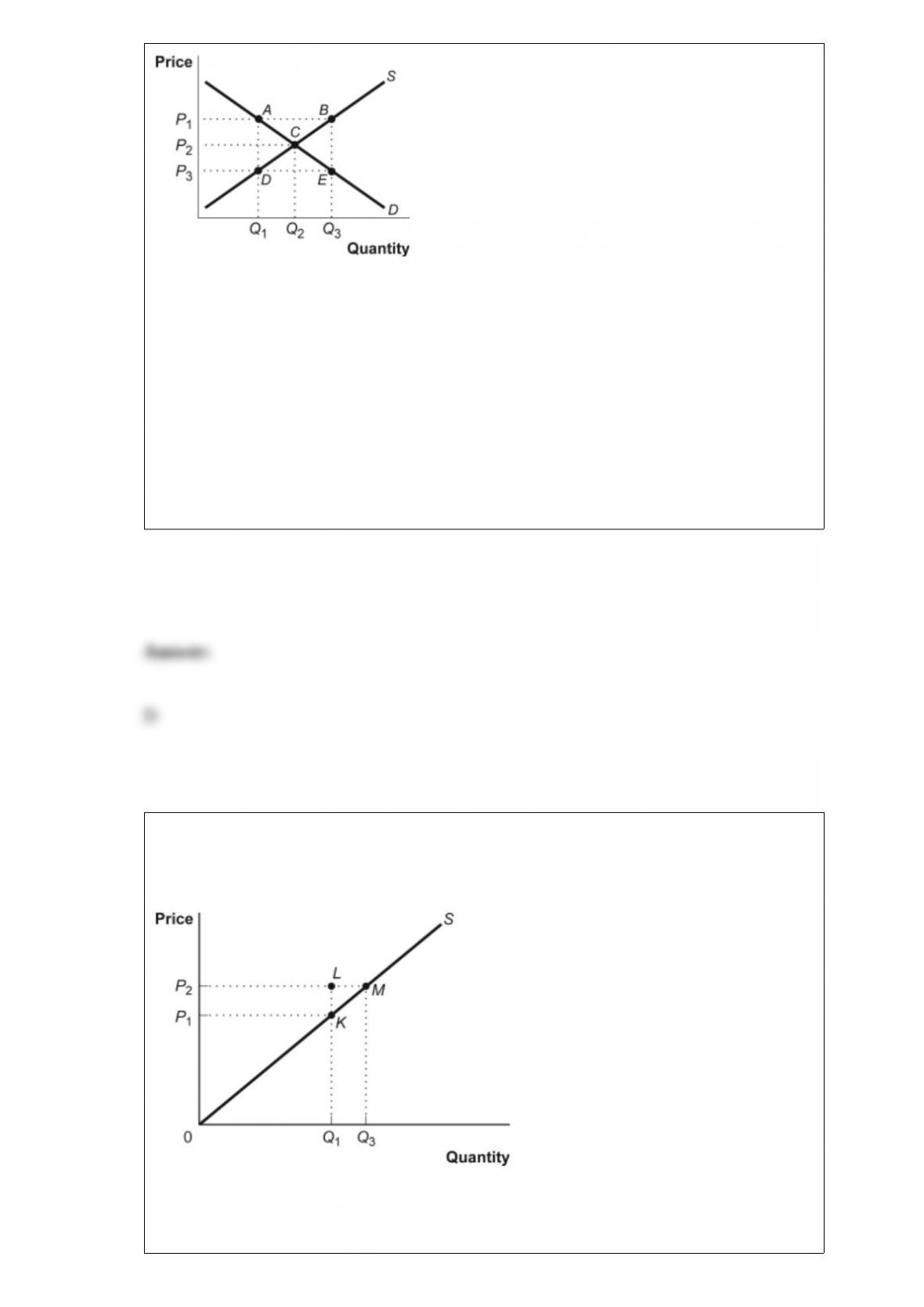

Figure: Producer Surplus II

(Figure: Producer Surplus II) Look at the figure Producer Surplus II. If the price rises

from P1 to P2, producer surplus increases by the area:

A) LMK.

B) P1K0.

C) P2M0.

D) P2P1KM.

In the long run:

A) the firm has time to change the level of all inputs.

B) inputs are neither variable nor fixed.

C) at least one input is free.

D) all inputs are more expensive.

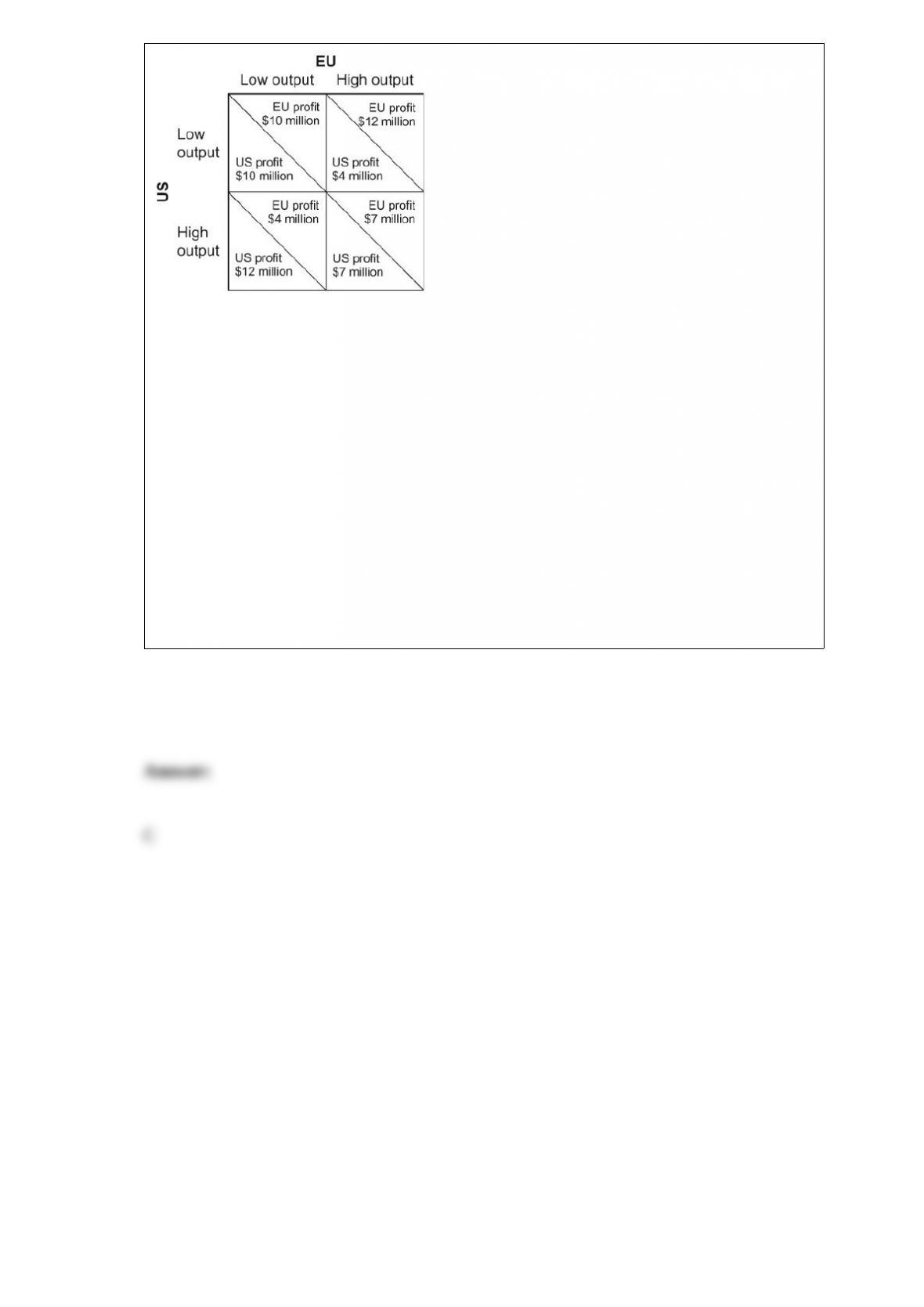

Figure: Payoff Matrix for the United States and the European Union

(Figure: Payoff Matrix for the United States and the European Union) Look at the

figure Payoff Matrix for the United States and the European Union. Suppose that the

United States and the European Union both produce corn, and each region can make

more profit if output is limited and the price of corn is high. The joint

profit-maximizing combination is for the United States to produce a _____ output and

the European Union to produce a _____ output.

A) high; high

B) high; low

C) low; low

D) low; high