BRICs is a term used in international finance to represent assets that are considered to

be inexpensive and sturdy, but fundamentally unsound and and incapable of coping

with the upheavals now apparent in international financial markets.

Currency risk is a concern for any international merger and acquisition activity. For

instance, once the bidder has successfully won the acquisition, the exposure evolves

from a transaction exposure to a contingent exposure.

When faced with additional risk from a foreign investment, firms typically account for

the additional risk by adjusting the discount rates or by adjusting cash flows.

In the U.S. and U.K. stock markets are characterized by ownership of firms

concentrated in the hands of a few controlling shareholders. In contrast, the rest of the

world tends to have more widespread ownership of shares.

The expected change in the option premium from a small change in the domestic

interest rate (home currency) is term rho.

In a typical naked corporate inversion transaction the corporation’s effective global tax

liability is reduced but the effective control does not change.

A hedge constructed using a put foreign currency option would protect you against

value losses, but allow, at the same time, the possibly reap value increases in the event

the exchange rate moved in your favor.

The liability of the aval is an “on balance sheet” obligation for the endorsing bank.

The goal of operating exposure analysis is to identify strategic operating techniques the

firm might adopt to enhance value in the face of unanticipated exchange rate changes.

To constitute a true letter of credit transaction, the bank’s L/C must contain a specified

expiration date or a definite maturity.

Indirect intervention for domestic currency valuation typically uses tools of monetary

policy as opposed to using tools of fiscal policy.

An unsponsored ADR may be initiated without the approval of the foreign firm with the

underlying stock.

A country experiencing a serious trade deficit is not as likely to expand imports as it

would be if running a surplus.

Like a forward market hedge, a money market hedge also involves a contract and a

source of funds to fulfill that contract. In this instance, the contract is a loan agreement.

The fundamental dilemma of foreign trade is being unwilling to trust a stranger in a

foreign land.

Empirical tests prove that PPP is an accurate predictor of future exchange rates.

The structure of a money market hedge is similar to a forward hedge. The difference is

the cost of the money market hedge is determined by the differential interest rates,

while the forward hedge is a function of the forward rates quotation.

The major advantage of a letter of credit to the exporter is that the exporter does not

receive any funds until the documents have arrived at a local port or airfield.

Multinational enterprises (MNEs) are firms, both for profit companies and

not-for-profit organizations, that have operations in more than one country, and conduct

their business through foreign subsidiaries, branches, or joint ventures with host country

firms.

Diversifying the financing base means diversifying sales, location of production

facilities, and raw material sources.

The major difference between currency futures and forward contracts is that futures

contracts are standardized for ease of trading on an exchange market whereas forward

contracts are specialized and tailored to meet the needs of clients.

Empirical studies indicate that MNEs have a lower debt/capital ratio than domestic

counterparts, indicating that MNEs have a lower cost of capital.

There are no important differences between domestic and international capital

budgeting methods.

The BOP should always balance.

The price of an option is always somewhat greater than its intrinsic value, since there is

always some chance that the intrinsic value will rise between the present and the

expiration date.

In determining why a firm becomes multinational there are many reasons. One reason is

that the firm is a knowledge seeker. They operate in foreign countries to exploit existing

technological expertise.

Depositary Receipts intra-market trades account for more than 90% of all DR trading

today.

One way a nation can improve its exports is by shortening the period for which credit

transactions can be insured.

International CAPM (ICAPM) assumes that there is a global market in which the firm’s

equity trades, and estimates of the firm’s beta, and the market risk premium, must then

reflect this global portfolio.

It is possible that efforts to decrease translation exposure may result in an increase in

transaction exposure.

The higher the price elasticity of demand, the higher the degree of pass-through.

Maximizing local profits in joint ventures overseas could be suboptimal from the

overall view of the MNE.

Because of the risks involved in international trade, most transactions follow

conventional methods and rarely require flexibility or creativity on the part of

management.

In the stakeholder capitalism model (SCM) the assumption of market efficiency is

absolutely critical.

Interest rate futures are relatively unpopular among financial managers because of their

relative illiquidity and their difficulty of use.

A draft is sometimes called a revocable letter of credit.

The time value is asymmetric in value as you move away from the strike price (i.e., the

time value at two cents above the strike price is not necessarily the same as the time

value two cents below the strike price).

Moral hazard may occur when a firm or individual takes on more risk when it knows

that someone else will “pick up the tab.”

Dividend yield is the change in the share price of stock as traded in the public equity

markets.

The authors claim that theoretical and empirical studies appear to show that

fundamentals do apply to the long-term for foreign exchange.

Which of the following is NOT a delisting category?

A) forced delistings

B) mergers

C) acquisitions

D) all of the above are categories of delistings

A U.S. investor makes an investment in Britain and earns 14% on the investment while

the British pound appreciates against the U.S. dollar by 8%. What is the investor’s total

return?

A) 22.00%

B) 23.12%

C) 6.00%

D) 4.88%

An agreement to swap a fixed interest payment for a floating interest payment would be

considered a/an:

A) currency swap.

B) forward swap.

C) interest rate swap.

D) none of the above

The authors refer to companies that have access to a ________ as MNEs, and firms

without such access are identified as ________.

A) global cost and availability of capital; domestic firms.

B) large domestic capital market; geographically challenged.

C) world financial markets; antiquated.

D) none of the above

Anglo-American markets is a term used to describe business markets in:

A) North, Central, and South America.

B) the United States, Canada, and Western Europe.

C) the United States, United Kingdom, Canada, Australia and New Zealand.

D) the United States, France, Britain, and Germany.

The United States taxes the domestic and remitted foreign earnings of U.S. based

MNEs no matter where the earnings occurred. This is an example of a/an ________

approach to levying taxes.

A) worldwide

B) territorial

C) neutral

D) equitable

A/An ________ option can be exercised only on its expiration date, whereas a/an

________ option can be exercised anytime between the date of writing up to and

including the exercise date.

A) American; European

B) American; British

C) Asian; American

D) European; American

________ exposure is far more important for the long-run health of a business than

changes caused by ________ or ________ exposure.

A) Operating; translation; transaction

B) Transaction; operating; translation

C) Accounting; translation; transaction

D) Translation; operating; transaction

TropiKana Inc., a U.S firm, has just borrowed euro 1,000,000 to make improvements to

an Italian fruit plantation and processing plant. If the interest rate is 5.50% per year and

the Euro depreciates against the dollar from $1.40/€ at the time the loan was made to

$1.35/€ at the end of the first year, how much interest will TropiKana pay at the end of

the first year (rounded)?

A) $55,000

B) €74,250

C) $74,250

D) $77,000

Terrorism, cyber attacks, and the anti-globalization movement are each examples of

________ risks.

A) firm-specific

B) country-specific

C) institutional

D) global-specific

The ________ approach argues that exchange rates are determined by the supply and

demand for a wide variety of financial assets

A) balance of payments

B) monetary

C) asset market

D) law of one price

According to the terminology associated with changes in currency values, which of the

following choices is the case when a currency’s value relative to other currencies is

changed by a government?

A) depreciation and revaluation

B) devaluation and appreciation

C) devaluation and revaluation

D) depreciation and appreciation

Which of the following could be considered an example of forced reinvestment if the

blockage of funds was expected to be temporary?

A) vertical reinvestment by an automobile manufacturer to buy parts suppliers and

showrooms

B) a lumber cutting company subsequently builds a paper mill with blocked funds

C) purchase of local money market instruments and short-term loans

D) all of the above

The difference between the expected (or required) return for the market portfolio and

the risk-free rate of return is referred to as:

A) beta.

B) the geometric mean.

C) the market risk premium.

D) the arithmetic mean.

Your authors note several empirical studies that have found:

A) no share price effect for foreign firms that cross-list on major U.S. exchanges.

B) a positive share price effect for foreign firms that cross-list on major U.S. exchanges.

C) a negative share price effect for foreign firms that cross-list on major U.S.

exchanges.

D) none of the above

If share price rises from $12 to $15 per share, and pays a dividend of $1 per share, what

was the rate of return to shareholders?

A) 26.67%

B) -13.33%

C) 33.33%

D) 16.67%

An ________ option can be exercised only on its expiration date, whereas a/an

________ option can be exercised anytime between the date of writing up to and

including the exercise date.

A) American; European

B) American; British

C) Asian; American

D) European; American

Instruction 8.1:

For the following problem(s), consider these debt strategies being considered by a

corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year

period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to

be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit

annually. The current one-year rate is 5%.

Refer to Instruction 8.1. Choosing strategy #3 will:

A) guarantee the lowest average annual rate over the next three years.

B) eliminate credit risk but retain repricing risk.

C) maintain the possibility of lower interest costs, but maximizes the combined credit

and repricing risks.

D) preclude the possibility of sharing in lower interest rates over the three-year period.

If a company fails to accurately predict it’s cost of equity, then:

A) the firm’s wacc will also be inaccurate.

B) the firm may not be using the proper interest rate to estimate NPV.

C) the firm may incorrectly accept or reject projects based on decisions made using the

cost of capital computed with an incorrect cost of equity.

D) All of the above are true.

In September 2009 a U.S. investor chooses to invest $500,000 in German equity

securities at a then current spot rate of $1.30/euro. At the end of one year the spot rate is

$1.35/euro.

Refer to Instruction 13.1. At the end of the year the investor sells his stock that now has

an average price per share of €57. What is the investor’s average rate of return before

converting the stock back into dollars?

A) 5.0%

B) -3.0%

C) -5.0%

D) 3.0%

The value of a European style call option is the sum of two components:

A) the present value plus the intrinsic value.

B) the time value plus the present value.

C) the intrinsic value plus the time value.

D) the intrinsic value plus the standard deviation.

Unsystematic risk:

A) is the remaining risk in a well-diversified portfolio.

B) is measured with beta.

C) can be diversified away.

D) all of the above

A ________ is a shared ownership in a foreign business.

A) licensing agreement

B) greenfield investment

C) joint venture

D) wholly-owned affiliate

Polaris Corporation has made an agreement to ship goods to a foreign firm with whom

they have not entered into a contract for three years. However, the firms have

communicated regularly since the last sale three years ago. This is an example of an:

A) unaffiliated known party transaction.

B) unaffiliated unknown party transaction.

C) affiliated party transaction.

D) none of the above

Another school of thought about the worldwide trend toward fuller and more

standardized disclosure rules is that the cost of U.S. level equity capital disclosure:

A) chases away potential listers of equity.

B) is an onerous costly burden.

C) leads to fewer foreign firms cross listing in U.S. equity markets.

D) all of the above

Instruction 8.1:

For the following problem(s), consider these debt strategies being considered by a

corporate borrower. Each is intended to provide $1,000,000 in financing for a three-year

period.

∙ Strategy #1: Borrow $1,000,000 for three years at a fixed rate of interest of 7%.

∙ Strategy #2: Borrow $1,000,000 for three years at a floating rate of LIBOR + 2%, to

be reset annually. The current LIBOR rate is 3.50%

∙ Strategy #3: Borrow $1,000,000 for one year at a fixed rate, and then renew the credit

annually. The current one-year rate is 5%.

Refer to Instruction 8.1. The risk of strategy #1 is that interest rates might go down or

that your credit rating might improve. The risk of strategy #3 is: (Assume your firm is

borrowing money.)

A) that interest rates might go down or that your credit rating might improve.

B) that interest rates might go up or that your credit rating might improve.

C) that interest rates might go up or that your credit rating might get worse.

D) none of the above

The ________ is the mechanism by which participants transfer purchasing power

between countries, obtain or provide credit for international trade transactions, and

minimize exposure to the risks of exchange rate changes.

A) futures market

B) federal open market

C) foreign exchange market

D) LIBOR

Which of the following is NOT an advantage to exporting goods to reach international

markets rather than entering into some form of FDI?

A) fewer political risks

B) greater agency costs

C) lower front-end investment

D) All of the above are advantages.

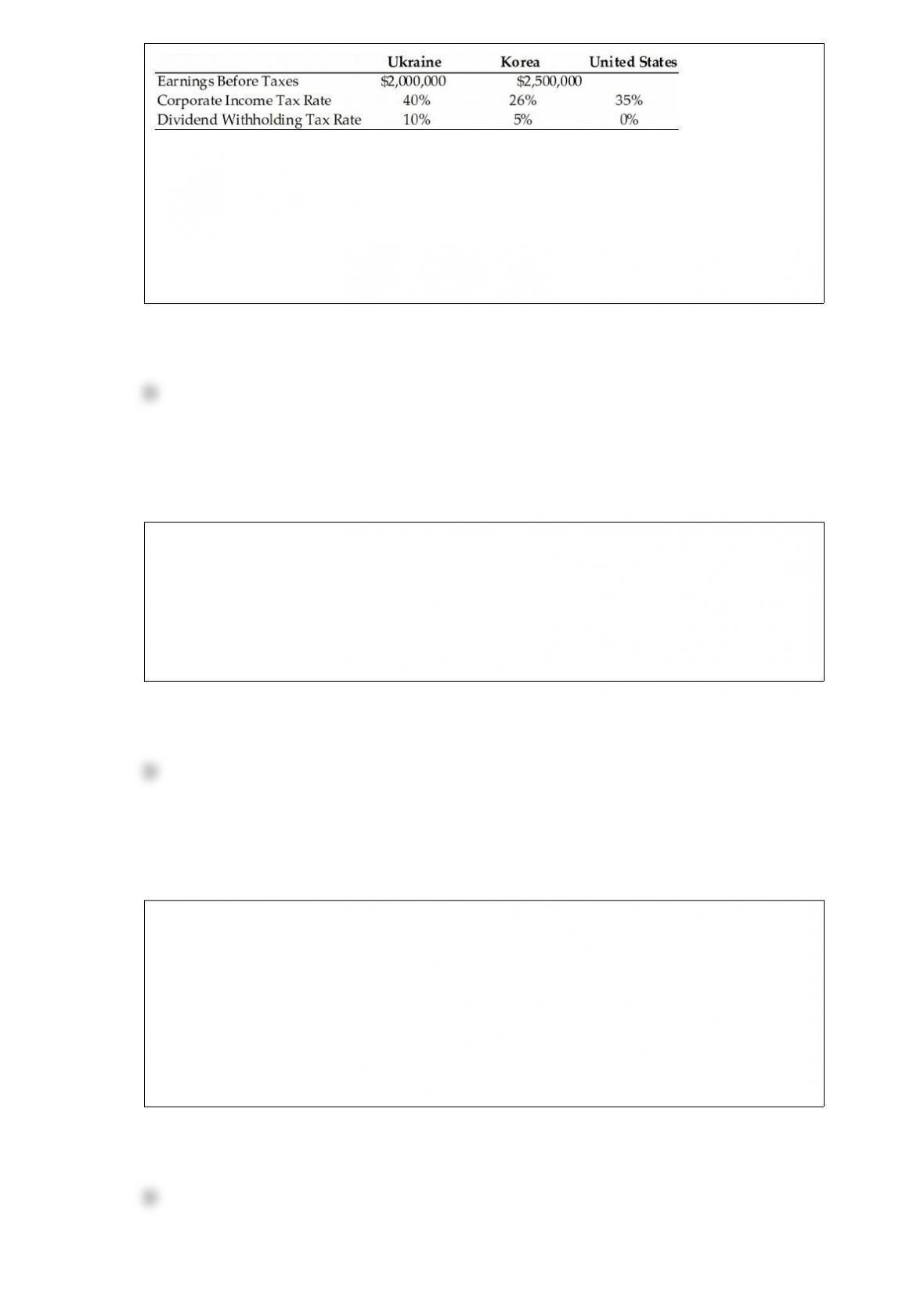

TABLE 15.1

Use the information to answer following question(s).

BayArea Designs Inc., located in Northern California, has two international

subsidiaries, one located in the Ukraine, the other in Korea. Consider the information

below to answer the next several questions.

Refer to Table 15.1. If BayArea pays out 50% of its earnings from each subsidiary, what

are the additional U.S. taxes due on the foreign sourced income from the Ukraine and

Korea respectively.

A) Ukraine = $0; Korea = ($30,000)

B) Ukraine = $100,000; Korea = $0

C) Ukraine = $0; Korea = $66,250

D) none of the above

________ is the cross-border purchase of assets that are then managed in a way that

hides the movement of money and its ownership.

A) Capital flight

B) Capital mobility

C) Irrational exuberance

D) Money laundering

A U.S. firm sells merchandise today to a British company for £150,000. The current

exchange rate is $1.55/£ , the account is payable in three months, and the firm chooses

to avoid any hedging techniques designed to reduce or eliminate the risk of changes in

the exchange rate. The U.S. firm is at risk today of a loss if:

A) the exchange rate changes to $1.52/£.

B) the exchange rate changes to $1.58/£.

C) the exchange rate doesn’t change.

D) all of the above

Eurobanks are:

A) banks where Eurocurrencies are deposited.

B) major world banks that conduct a Eurocurrency business in addition to normal

banking activities.

C) financial intermediaries that simultaneously bid for time deposits in and make loans

in a currency other than that of the currency of where it is located.

D) All of the above are descriptions of a Eurobank.

Which of the following is NOT an item to be considered in BOP calculations?

A) A foreign resident purchases a U.S. Treasury Bill.

B) A U.S.-based firm manages the development of an oil field in Kazakhstan.

C) A consumer buys a VCR made in Korea from a Florida Wal-Mart store.

D) A U.S. citizen living in Minnesota travels to Winnipeg, Canada, and buys a case of

LaBatt’s Canadian beer.

Which of the following is NOT an assumption of market efficiency?

A) Instruments denominated in other currencies are perfect substitutes for one another.

B) Transaction costs are low or nonexistent.

C) All relevant information is quickly reflected in both spot and forward exchange

markets.

D) All of the above are true.

When considering the phases of adjustment and response to operating exposure in the

LONG RUN, price changes tend to be ________ and volume changes tend to be

________.

A) fixed/contracted; contracted.

B) fixed/contracted; completely flexible.

C) completely flexible; completely flexible.

D) completely flexible; contracted.

A bid is the price in one currency at which a dealer will buy another currency. An ask is

the price at which a dealer will sell the other currency. Dealers bid (buy) at one price

and ask (sell) at a slightly higher price, making their profit from the spread between the

prices. List and explain three reasons/factors that could make the spread small.

What is a value-added tax? Where is this type of tax in wide usage? Why do you

suppose this form of taxation has NOT been widely accepted in the United States?

The decline of share listings in the United States has led to considerable debate over

whether these trends represent a fundamental global business shift away from the

publicly traded corporate form, or something that is more U.S.-centric combined with

the economic times. Develop an argument to why the decline happened.

What are the components of the weighted average cost of capital (WACC) and how do

they differ for an MNE compared to a purely domestic firm?

List and discuss three public pathway strategies for a MNE for raising equity capital

outside its home market.

Why do the U.S. tax authorities tax passive income generated offshore differently from

active income?

Your firm is faced with paying a variable rate debt obligation with the expectation that

interest rates are likely to go up. Identify two strategies using interest rate futures and

interest rate swaps that could reduce the risk to the firm.

Does foreign currency exchange hedging both reduce risk and increase expected value?

Explain, and list several arguments in favor of currency risk management and several

against.

Market imperfections do not necessarily imply that national securities markets are

inefficient. Develop an argument as to why this is possible.

The theme dominating global financial markets today is the complexity of risks

associated with financial globalization. List and explain examples of the complexity of

risks affecting the leading and managing of multinational firms in the rapidly moving

marketplace.

What are the traditional methods for countries to implement protectionism? What are

some typical non-tariff barriers to trade? How can MNEs overcome host country

protectionism?

The decision about where to invest abroad is influenced by behavioral factors. Explain

the behavioral approach to FDI.

What is a country’s balance of (merchandise) trade, and why is it so widely reported in

the financial and popular press?

Explain the logic behind the application of the PPP theory to explain changes in the

spot exchange rate.

What are the desired characteristics for a country if it expects to be used as a tax haven?

Define and explain the logic for the time value of an option. Explain the value of the

time value of an option for deep out-of-the money and deep in-the-money options.

Foreign exchange forecasting can be either long-term, or short-term in duration.

Compare and contrast the motivation for and the techniques a forecaster might use for

each of the time periods.