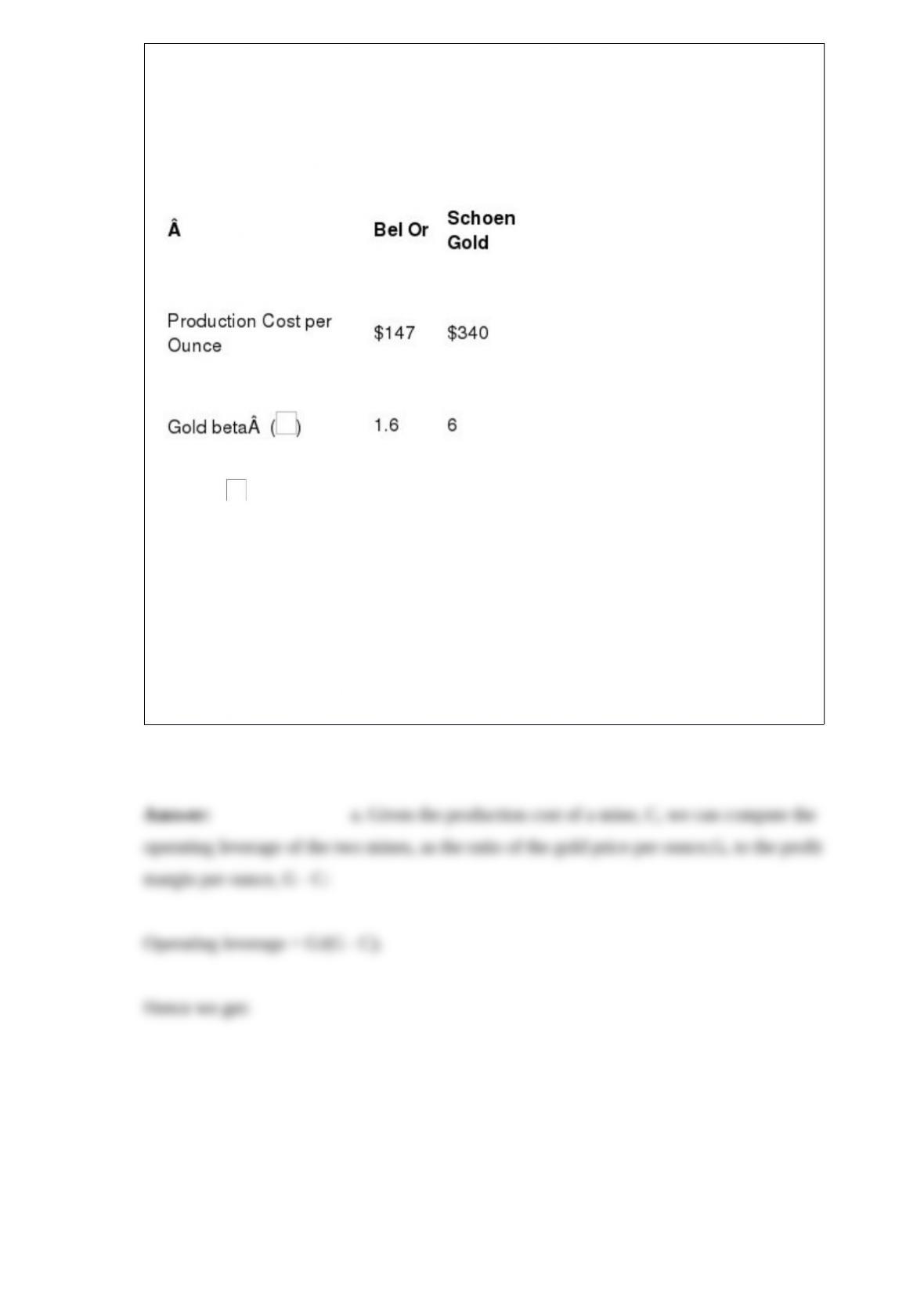

Let’s assume that you are a U.S. investor who wants to invest $10,000 in gold. The

current price of gold is $400, and you expect it to go up by 10% in the very short-term.

You consider buying shares of gold mines; you are debating whether to invest in Bel Or

or Schoen Gold. Your broker gives you the following information:

The gold is obtained by running a regression of the percentage price movements in

the gold mine stock on the percentage price movements in gold bullion. It indicates the

stock market price sensitivity to gold.

a. Explain why a gold mine with a high production cost should have a value that is

more sensitive to gold price movements than a gold mine with low production costs.

b. Which mine would you buy and why?

c. What is your expected return, given this scenario?

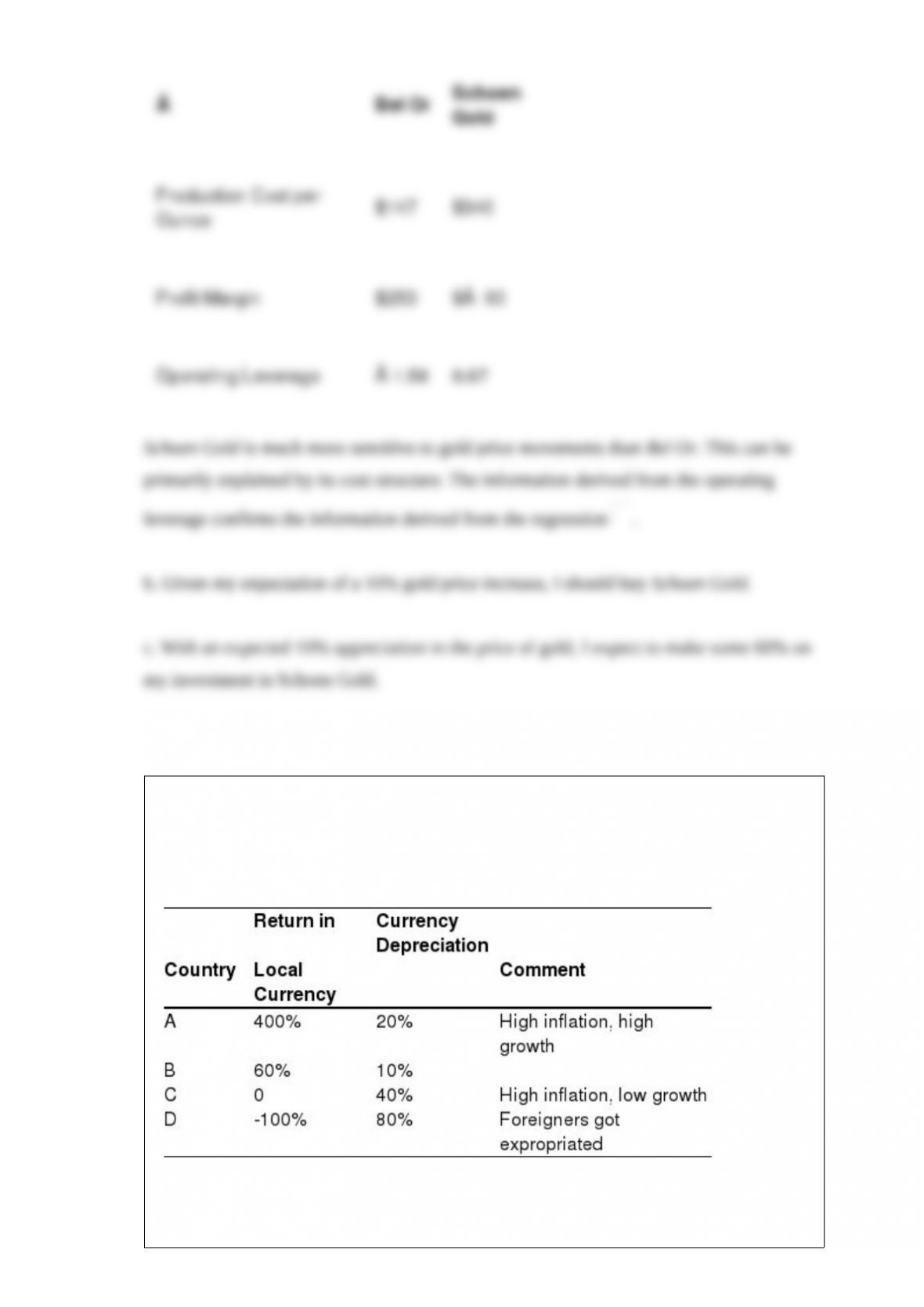

You consider investing in four very volatile emerging markets. These are small

countries just opening up to foreign investment. You spread your money equally across

them. After a year, the following observations are made on the performance of each

market:

a. Calculate the return, in dollars, on each market. The currency depreciation is equal to

the drop in the dollar value of one unit of local currency. For example, if the peso

moves from 1 dollar per peso to 0.8 dollar per peso, the depreciation of the peso is

measured as 20%.

b. What is the return on a portfolio equally invested in each market?

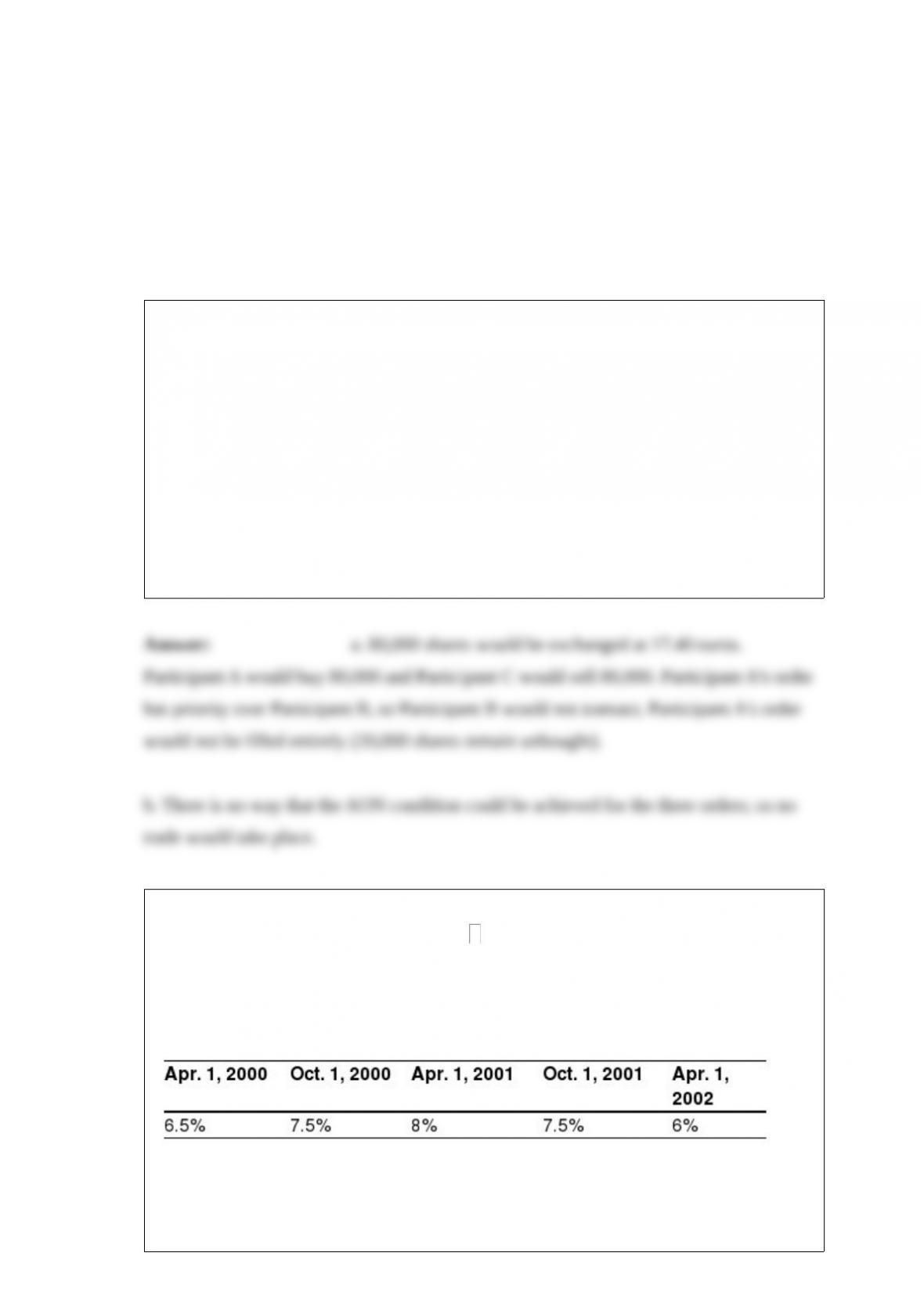

A five-year currency swap involves two AAA borrowers and has been set at current

market interest rates. The swap is for US$100 million against AUD 200 million at the

current spot exchange rate of AUD/$ 2.00. The interest rates are 4% in U.S. dollars and

7% in Australian dollars, or annual swaps of $4 million for AUD 14 million. A year

later, the interest rates have dropped to 3% in U.S. dollars and 6% in Australian dollars,

and the exchange rate is now AUD/$ 1.9.

a. What should the market value of the swap be in the secondary market?

Assume now that the swap is instead a currency-interest rate swap whereby the dollar

interest is set at LIBOR.

b. What would the market value of the currency-interest rate swap be if these conditions

prevailed a year later?

Assume that foreign exchange rates are totally unpredictable, as some theories and

empirical studies claim, so that the best prediction of the future spot rate is the current

spot rate.

a. Back in 1982, would you have suggested investing in U.S. dollar bills or in German

bills?

b. What about in 1992?

c. What about in 1997?

(Look at Exhibit 3.1 of the fifth edition, knowing that inflation rates were similar in the

two countries.)

Try to find some reasons why:

a. Stock and bond markets should be strongly correlated and,

b. Stock and bond markets should be weakly correlated.

Japanese companies tend to belong to groups (“keiretsu”) and to hold shares of one

another. Because these cross-holdings are minority interests, they tend not to be

consolidated in published financial statements. To study the impact of this tradition on

published earnings, take the following simplified example:

Company A owns 20% of Company B; the initial investment was 20 billion yen.

Company B owns 30% of Company A; the initial investment was 20 billion yen.

Both companies value their minority interests at historical cost. The year-end

nonconsolidated balance sheets of the two companies follow:

The annual net income of Company A was 15 billion yen. The annual net income of

Company B was 40 billion yen. Assume that the two companies do not pay any

dividends. The current stock market values are 250 billion yen for Company A and 550

billion yen for Company B.

a. Restate the earnings of the two companies, using the equity method of consolidation.

Remember that the share of the minority-interest profits is consolidated on a one-line

basis, proportionate to the share of the equity owned by the parent. The value of the

investment in the subsidiary is adjusted to reflect the change in the subsidiary’s equity.

b. Calculate the P/E ratios based on nonconsolidated and consolidated earnings. Are

they similar?

Orders for Vivendi Universal have been entered on a crossing network for European

shares. There is one order from Participant A to buy 100,000 shares, one order from

Participant B to buy 200,000 shares, and one order from Participant C to sell 80,000

shares. Assume that the orders were entered in that chronological order and that the

network gives priority to the oldest orders. At the time specified for the crossing

session, Vivendi Universal is transacted at 17.40 euros on Euronext in Paris, its primary

market.

a. What trades would take place on the crossing network?

b. Assume now that all the orders are AON (all or nothing), meaning that the whole

block has to be traded at the same price. What trades would take place?

An Italian corporation enters into a two-year interest rate swap in euros on April 1,

2000. The swap is based on a principal of 100 million, and the corporation will

receive 7% fixed and pay six-month Euribor. Swap payments are semiannual. The 7%

fixed rate is quoted as an annual rate using the European method, so the implied

semiannual coupon is 3.44% [since (1.0344)2 = 1.07]. Two years later, the swap is

finally settled, and the following Euribor rates have been observed:

a. What have the swap payments or receipts for the corporation been on each swap

payment date?

b. The same Italian corporation also entered another two-year interest rate swap in euros

on April 1, 2000. The swap is based on a principal of 100 million, and the corporation

contracted to receive 7% fixed and pay six-month Euribor. On this swap, the payments

are annual. Hence, the two successive six-month Euribor are compounded. Assuming

that the Euribor rates given in the previous problem have been observed, what have the

two annual swap payments been?

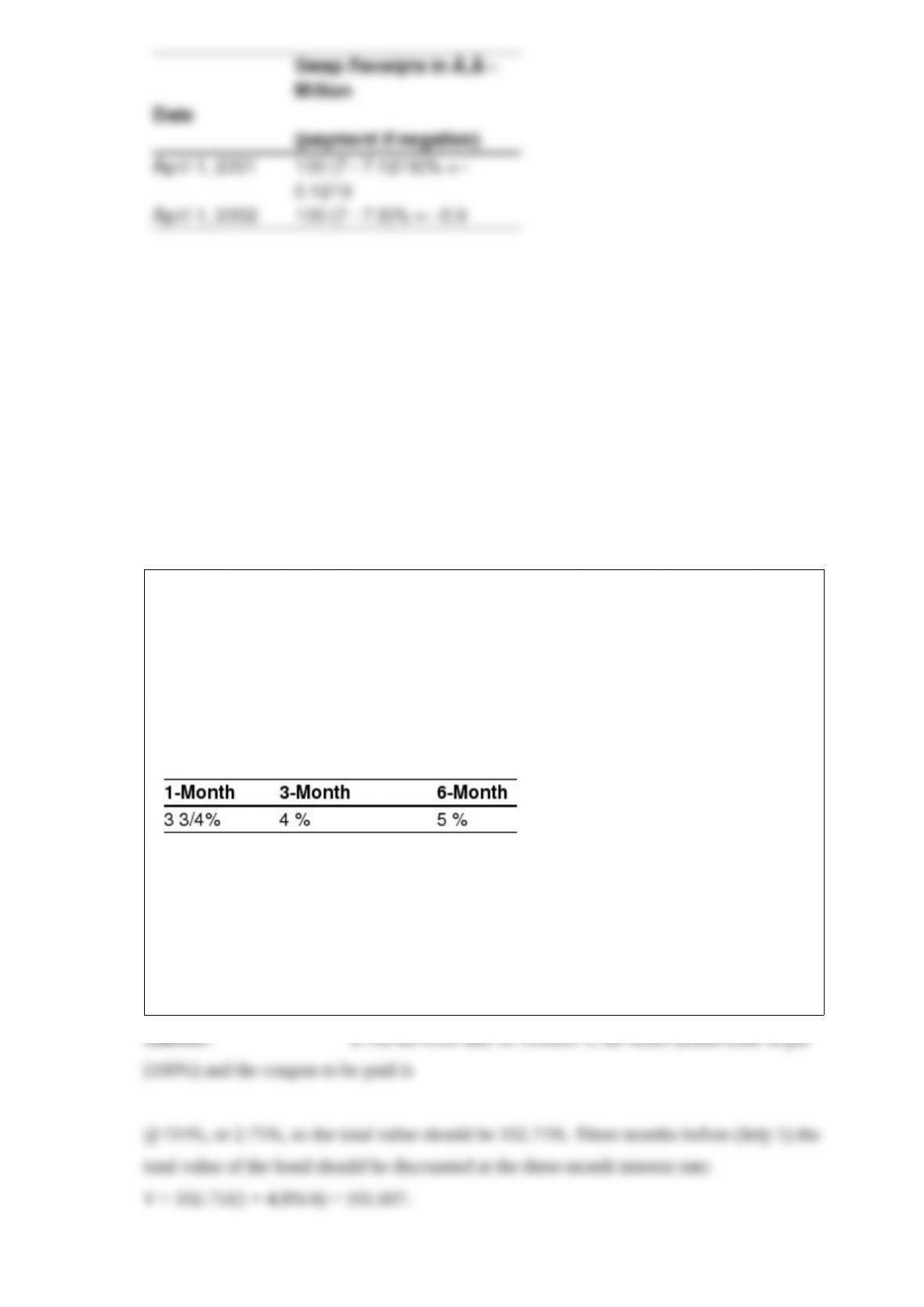

On April 1, 2000, a corporation rated AA has issued a semiannual FRN in dollars. This

is a perpetual bond, which will pay coupons indefinitely if the corporation does not

default. The coupon is set at six-month LIBOR plus a spread of ½ %. The six-month

dollar LIBOR is equal to 5%.

a. Three months later (July 1, 2000), the corporation is still rated AA and the

market-required credit spread for AA is still at ½%. We observe the following LIBOR

rates:

Give an estimation of the total value of the bond. What should be its quoted price?

b. Three months later (October 1, 2000), the coupon has just been paid. The six-month

dollar LIBOR is again at 5%, but the market-required spread for AA-rated corporations

on long-term FRNs has moved to 1%. Give some estimation of the new value of the

FRN on reset date.

In 1995, the Thai baht is pegged to a basket of currencies. Assume that the baht

exchange rate is set

at 25 baht per U.S. dollar. Thailand is experiencing rapid economic growth, with

extensive ongoing foreign investment. Consumer price index (CPI) inflation in

Thailand is somewhat higher than in the United States, and the current account in

Thailand is in deficit. Nevertheless, Thailand has no problem maintaining its fixed

exchange rate with the dollar.

a. Explain why the Thai baht does not depreciate as suggested by purchasing power

parity (PPP).

b. Two years later, prospects for economic growth are much lower and investors are

worried about the political and financial uncertainties in Thailand. Explain why the Thai

baht depreciates strongly against the U.S. dollar.

The euro is quoted as = 0.79610-0.79650, and the Australian dollar is quoted as

= 1.5675-1.5685. What is the implicit quotation?

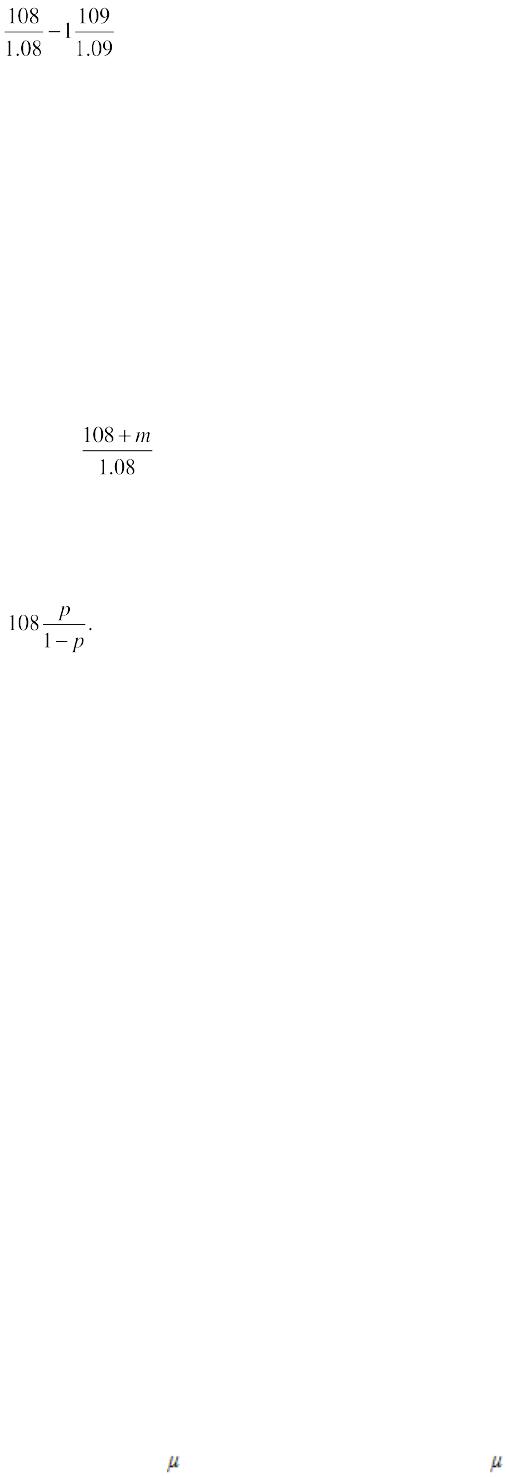

The current market conditions for an AAA client are 8% on a one-year dollar loan, and

8% fixed U.S. dollars for 9% fixed British pounds on a one-year dollar/pound currency

swap. Let’s consider a BBB client borrowing at (8 + m)% on a one-year dollar loan. The

same client can enter a dollar/pound currency swap, paying (8 + % fixed dollars and

receiving 9% fixed pounds. Assume that the customer has a probability of % to default

within a year. In case of default, the bank knows that it will recover nothing on either

transaction. The probability of default (e.g., 5%) is known and independent of

movements in interest and exchange rates. The spot exchange rate is S0 = 1 $/ .

Assuming that you can observe the prices of $/ currency options, suggest some

approach to determine the fair values of m and . (Assume that the bank has a large

number of clients whose probabilities of default are independent; therefore, the bank

can diversify away the uncertainty of default on this specific client.)

What are the potential biases of the simple yield calculation? Take the example of two

straight yen Eurobonds with the same maturity of five years. Bond A has a coupon of

12% and Bond B, a coupon of 8%. The current market yield on yen bonds is 10%.

These two bonds have the same yield-to-maturity of 10% and are correctly priced at

107.58% for Bond A and 92.42% for Bond B. What would be the yield-to-maturity

indicated by the simple yield calculation?

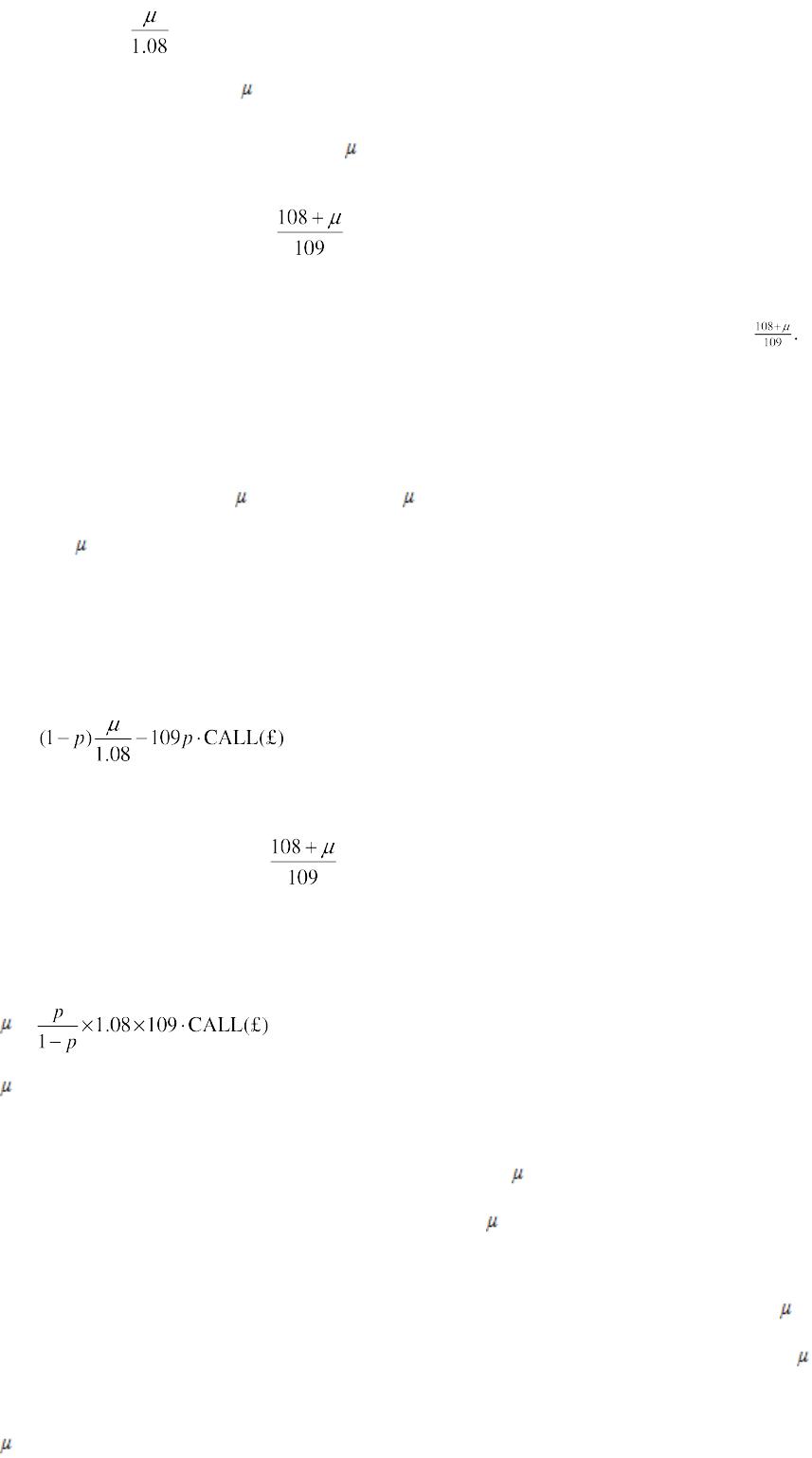

You are provided below with annual return, standard deviation of returns, and tracking

error to the relevant benchmark for three portfolios. Calculate the Sharpe ratio and

information ratio for the three portfolios and rank them according to each measure.

The yields on zero-coupon bonds are as follows:

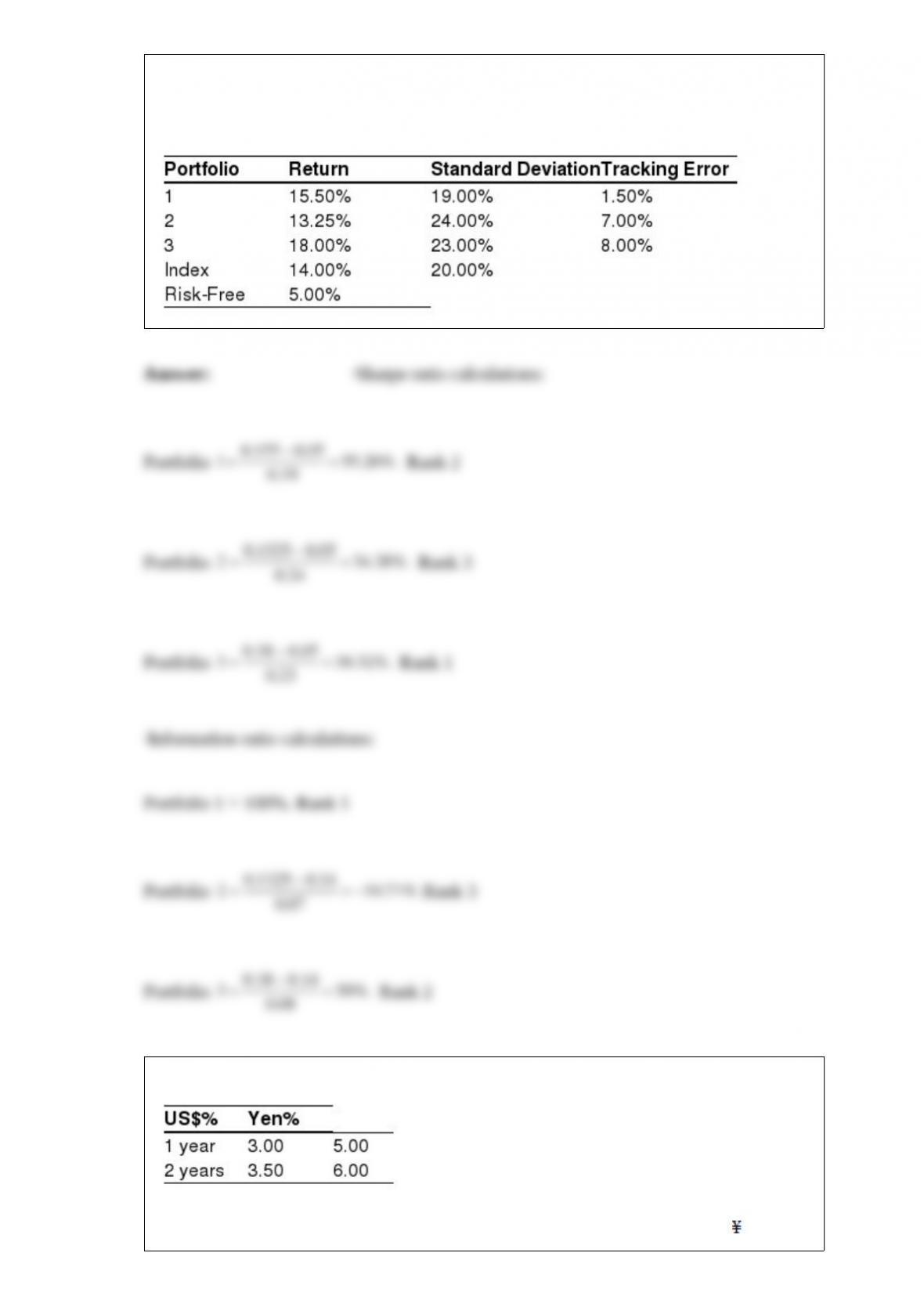

A young investment banker considers issuing a $/yen dual-currency bond for 100

million. It is a bond with interest paid in yen and principal repaid in dollars. The current

spot exchange rate is

$1 = 100. The bond will be reimbursed for $1 million in two years. The interest is paid

on year

one and year two. What should the interest paid in yen be?

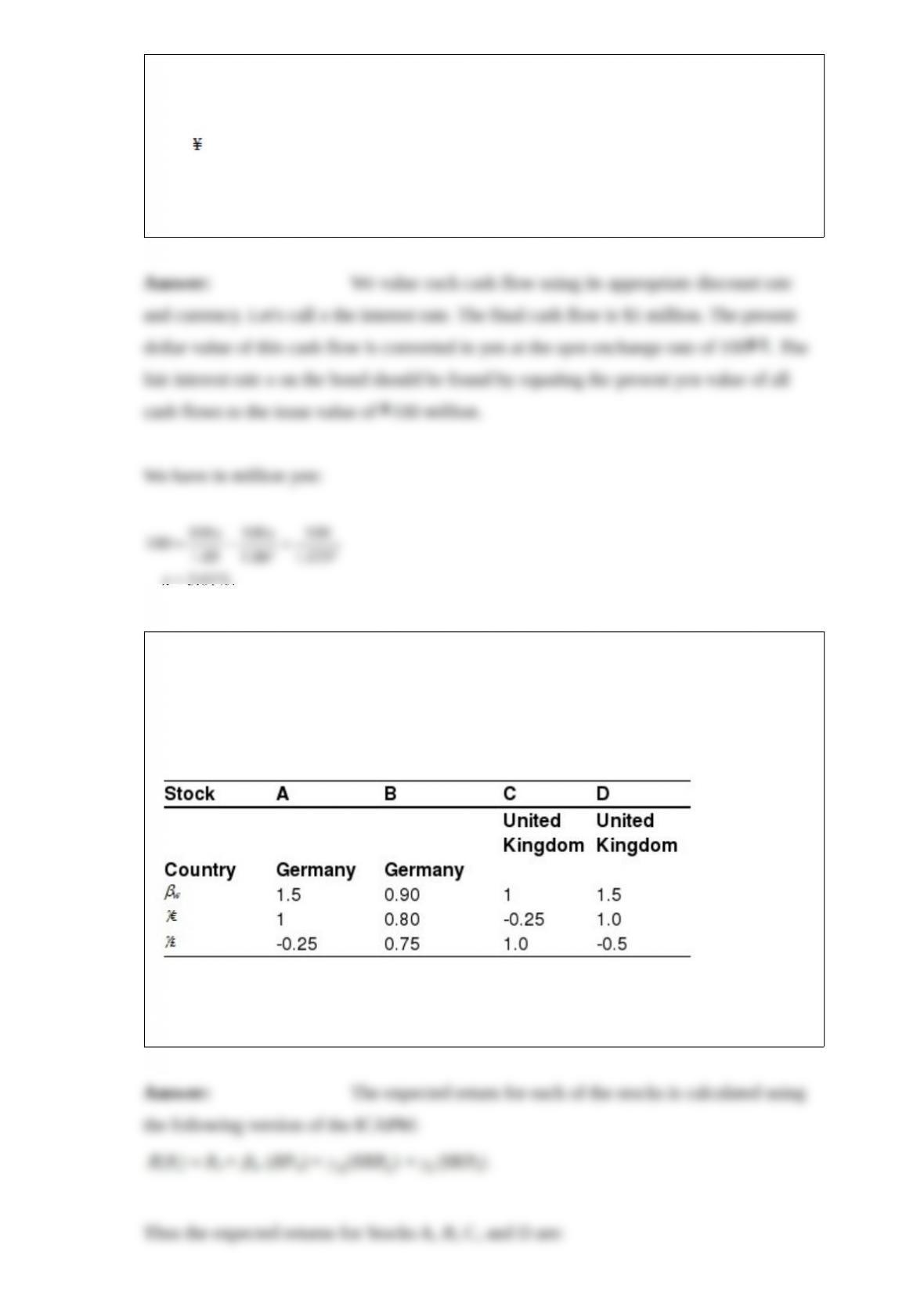

Assume that you are a U.S. investor who is considering investments in the German

(Stocks A and B) and British (Stocks C and D) stock markets. The world market risk

premium is 4.5%. The currency risk premium on the euro is 1%, and the currency risk

premium on the pound is -1%. In the United States, the interest rate on one-year

risk-free bonds is 4%. In addition, you are provided with the following information:

Calculate the expected return for each of the stocks. The U.S. dollar is the base

currency.

Here are some quotes of the Japanese yen/U.S. dollar spot exchange rate given

simultaneously on the phone by three banks:

Bank A: 121.15-121.30

Bank B: 121.22-121.35

Bank C: 121.20-121.25

Are these quotes reasonable? Do you have an arbitrage opportunity?

An American portfolio manager wishes to increases her exposure to Japanese stocks by

$10 million without taking much foreign exchange risk. The spot exchange rate is 100

per dollar. She considers several alternatives:

· Exchange Traded Funds (ETFs) are listed on the Tokyo stock exchange. The ETF is a

traded fund that tracks the TOPIX index. Each share has a value of 1,000.

· Futures contracts are available on the TOPIX index. Each contract is for 1,000 times

the index. The current futures price of the TOPIX index is 1,000. The margin deposit

per contract is 50,000.

· At-the-money call options on the TOPIX index are available. Each contract is for

1,000 times the index. The premium on the call is 60 per index or 60,000 per

contract.

What strategy could she adopt using those contracts?

You are an active British stock portfolio manager. Your performance is measured

against the FTSE index, a broadly based British stock index. It has been repeatedly

observed that small-capitalization stocks outperform large-capitalization stocks over

prolonged periods of time (‘small-firm effect”)

but that there have been periods when the reverse was true. It has also been repeatedly

observed that value stocks (firms with low price-to-book ratios) outperform growth

stocks over prolonged periods of time (“value/growth effect”) but that there have been

periods when the reverse was true.

How would an attribute factor model be useful in estimating the risks that your

performance deviates from that of the assigned benchmark?

A differential swap, or switch LIBOR swap, involves the LIBOR rates in two different

currencies but with both legs denominated in the same currency. A Japanese insurance

company engages in a differential swap whereby it receives the six-month Japanese yen

LIBOR and pays the six-month U.S. dollar LIBOR plus 50 but with both legs

denominated in yen. No principal is exchanged at the end. The current LIBOR for the

yen and the dollar are 6% and 4%, respectively, and the principal is 100 million yen.

Hence, the first swap payment will be based on a differential of 1.5% in yen [6% = (4%

– 0.5%)]. The current yield pick-up is 150 . There is no currency risk on this swap.

Provide some intuitive explanation for the pricing of such a swap, knowing that at the

time, the dollar yield curve was very steep (long-term rates are much higher than

short-term rates) and the yen yield curve was almost flat.

You are a young investment banker considering the issuance of a guaranteed note with

stock index participation for a client. The current yield curve is flat at 8% for all

maturities. Long-term at-the-money options on the stock market index are traded by

banks. Two-year at-the-money calls trade

at 17.84% of the index value; three-year at-the-money calls trade at 20% of the index

value. You

are hesitant about the terms to set in the structured note. You know that if you guarantee

a higher

coupon rate, the level of participation in the stock appreciation will be less. Your boss

asks you to compute the “fair” participation rate that would be feasible for various

guaranteed coupon rates and maturities. In other words, based on the current market

conditions (as described above), estimate the participation rates that are feasible with a

maturity of two or three years, and a coupon rate of: 0%, 1%, 2%, 3%, 5%, and 7%.