You are a foreign exchange dealer. You see the following quote on your Reuter’s screen:

a. The spot exchange rate of the Swedish krona is equal to 5.7 per U.S. dollar. The

three-month interest rates are 12% in and 8% in dollars. What is the three-month

forward exchange that you should quote?

b. In the language of currency traders would the Swedish krona be considered as

‘strong” or “weak” relative to the U.S. dollar?

c. Compute the annualized discount or premium on the dollar relative to the krona.

d. After a careful look at your screen, you discover that the spot exchange rate is really

5.7000-5.7015. The 12-month interest rates are 121/4 – 1/2% in and 81/4 – 1/2% in

U.S. dollars. What should be the bid-ask quote on the one-year forward rate?

e. A Swedish exporting firm expects to be paid $1 million in three months. Please

simulate the

value of this payment if in three months, the spot exchange rate is equal to =

5 and

= 6. What would be the value of this payment if the firm had hedged against

currency movements using the forward rate calculated in (a)?

An asset manager has a mandate to manage a European equity portfolio for a U.S.

pension client. The portfolio size is $100 million. The benchmark is some European

equity index with a 50% currency hedging target. But the currency management is

delegated to a currency overlay manager. The geographical breakdown of the portfolio

on January 1 is as indicated below:

a. Assume that the currency overlay manager is neutral on currencies (that is, does not

have specific forecasts on exchange rate). What would you expect the currency overlay

manager to do on this portfolio?

b. Assume now that the currency overlay manager is bullish on the euro and pound but

bearish on the Swiss franc (relative to the dollar). What kind of actions are you

expecting from the currency overlay manager?

The current dollar yield curve on the Eurobond market is flat at 7% for top-quality

borrowers. A French company of good standing can issue plain-vanilla straight and

floating-rate dollar Eurobonds at the following conditions:

·Bond A: Straight bond. Five-year straight dollar Eurobond with a coupon of 7.25%.

·Bond B: FRN. Five-year dollar FRN with a semiannual coupon set at LIBOR plus ¼%

and a cap of 14%. The cap means that the coupon rate is limited at 14% even if the

LIBOR passes 13.75%.

An investment banker proposes to the French company to issue bull and/or bear FRNs

at the following conditions:

·Bond C: Bull FRN. Five-year FRN with a semiannual coupon set at: 13.75% – LIBOR.

·Bond D: Bear FRN. Five-year FRN with a semiannual coupon set at: 2 x LIBOR – 7%.

The coupon on a bull FRN will increase when LIBOR drops. This is sometimes known

as a reverse floater. The coupon on the bull FRN cannot be negative, so it has a floor of

zero. The bear FRN will benefit from a rise in interest rates. The coupon on the bear

FRN is set with a cap of 20.50%.

a. Explain why a bull FRN could be attractive to some investors.

b. Explain why a bear FRN could be attractive to some investors.

c. Explain why it would be attractive to the French company to issue these FRNs

compared to current market conditions for plain-vanilla straight Eurobonds and FRNs.

The company assumes that LIBOR can never be below 3.5% or above 13.75%.

You hold a portfolio made of French stocks and worth 10 million. The beta ( ) of

this portfolio relative to the CAC index is 1. The interest rate for the euro is 4% for all

maturities and the annual dividend yield is 2%. The spot value of the CAC index on

January 1, 2000, is 5,000. A CAC contract has a size of 10 for each index point.

a. What should be the future price of the CAC contract with a three-month maturity?

b. You fear a fall in the French stock market. What should be your hedge ratio? How

many contracts do you buy/sell?

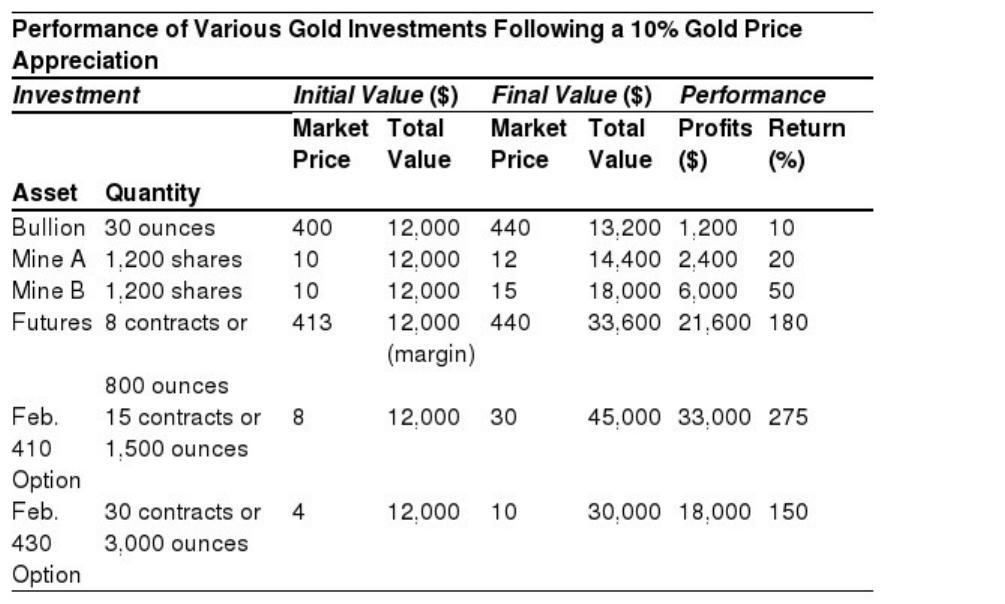

G.O. Bug wants to invest $12,000 in gold. In December, the spot price of gold is $400

per ounce. Bug is very confident that gold will appreciate by at least 10% before the

end of January and is willing to assume fairly risky positions to maximize the return on

this forecast. Bug is considering several alternatives:

– Gold bullion. Bug could buy 30 ounces, or roughly 1 kilogram.

– Gold futures. Bug could buy February futures. These contracts trade at $413 per

ounce, with an initial margin of $1,500 per contract of 100 ounces. Therefore, Bug

could buy eight contracts (12,000/1,500).

– Gold options. Bug considers two February call options with different strike prices.

Each option contract covers 100 ounces. The February 410 call quotes at $8 per ounce;

the February 430 call quotes at $4 per ounce. Therefore, Bug could buy fifteen contracts

of the first option or thirty contracts of the second option.

– Two gold mines. Mines A and B have the same stock price: $10 per share. A British

broker has estimated the gold of both mines using a discounted cash flow model as

well as historical regression analysis. Mine A is a rich mine with a gold equal to 2;

mine B has much higher production costs with a gold equal to 5. Bug could buy

1,200 shares of one of the gold mines.

Bug quickly rules out investing directly in bullion, which does not offer enough

leverage.

a. Assuming that Bug’s expectations are realized by the end of February, compute the

realized returns on the various alternative strategies considered. Simulate various values

of the spot price of gold in February (320, 360, 380, 400, 420, and 480).

b. Which investment strategy would you suggest to Bug?

The annualized performance, in U.S. dollars, of the United States and EAFE stock

indices are:

ReturnUS = 12% US = 15.5%

ReturnEAFE = 14.6% EAFE = 18.2%

Correlation = 0.47

a. What would be the return and risk of a portfolio invested half in the U.S. market and

half in the EAFE index?

b. What if the correlation increases to 0.6?

Consider two Thai firms listed on the Bangkok stock exchange:

– Thai A is a mining company that exports a large part of its minerals production. Much

larger competitors can be found in Latin and North America. The market price of its

production is largely determined in dollars on the world market.

– Thai B imports various engine parts from Europe and the United States. The demand

for its product is highly price elastic. A significant rise in baht prices lowers the

demand.

a. What will happen to the earnings and stock prices of the two companies if there is a

sudden and large devaluation of the Thai baht against major currencies?

b. What can you say about the currency exposures of the two companies ( )

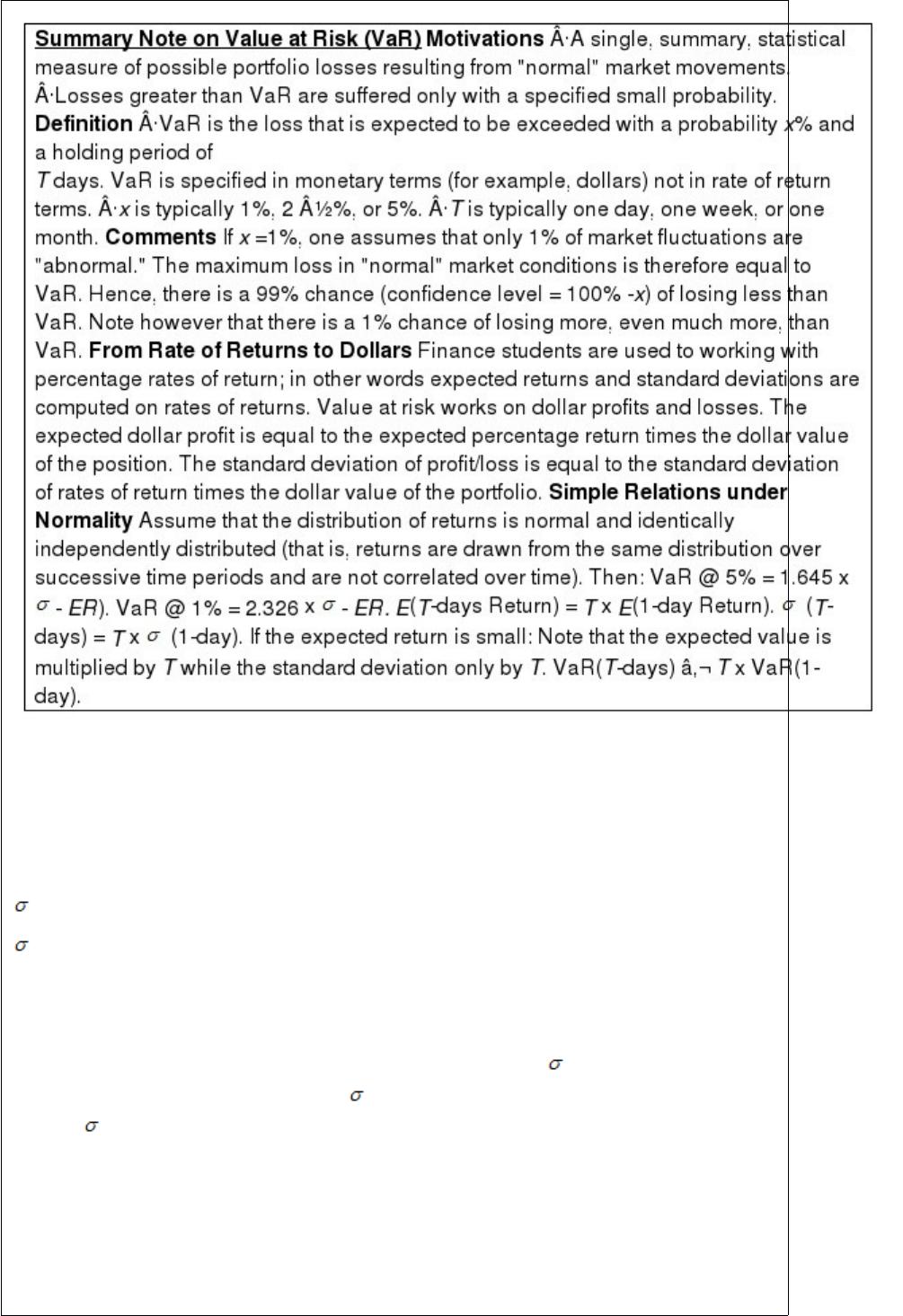

The next problem deals with Value at Risk, which is not detailed in this textbook. A

brief summary note on Value at Risk is given below.

You have to compute the VaR of a portfolio with a probability of 5% and 1%

(confidence level of 95% and 99%). Your portfolio is worth $100 million evenly

invested in two assets ($50 million in asset 1 and $50 million in asset 2). Here are some

statistics for monthly returns of the two assets:

ER1) = ER2) = 0.5%

R1= 8%

R2= 12%

Correlation = 0.4.

You make the hypothesis that the distributions are normal. We know that in a normal

distribution with expected return E(R) and standard deviation , 5% of the

observations lie below [E(R) – 1.645 x ] and 1% of the observations lie below [E(R) –

2.326 x ].

a. What is the one-month VaR of the portfolio with a 5% probability?

b. What is the one-month VaR of the portfolio with a 1% probability?

c. What is the one-year VaR of the portfolio with a 5% probability?

You are an investment banker working in Switzerland where yields are very low (1%

for all maturities). You are planning to offer a five-year Swiss franc/British pound bond

with the following characteristics:

· Issuer: Brit Ltd., a top-quality British company.

· Issue amount: SFr 100 million.

· Coupon in SFr: 5% (or SFr 5 million).

· Reimbursed value: 40 million.

This bond qualifies as a Swiss franc bond for the portfolio of a Swiss insurance

company.

The current spot exchange rate is 2.5 Swiss francs per British pound. The yield curve in

British pounds is flat at 7%. The pound/franc swap rates are 7% in pounds against 1%

in francs for all maturities.

a. Assume that Swiss insurance companies can account for their Swiss franc bond

holdings

at historical costs. Give a reason why it would be attractive to invest in this bond.

b. Is the coupon rate set at fair pricing (i.e., consistent with current market conditions)?

c. The British company desires to borrow in pounds and does not wish to carry any

currency risk on its debt. The investment banker needs to design a coupon swap that

would hedge the currency risk on that dual-currency bond for Brit Ltd. The designed

swap should have a zero value at time of contracting. Give one possible design for the

swap and calculate its associated swap rate.

d. What is the pound yield paid by the British company, once it has hedged its currency

risk on the dual-currency bond using the swap described above? What is the annual

cost-saving in British pounds compared to a straight pound bond?

The Japanese balance of payments from 1994 to 1997 is as follows. All numbers are

reported in billions of U.S. dollars. The last line gives the real effective exchange rate

index of the yen relative

to other currencies. An increase in the index means a real appreciation of the yen.

a. Calculate the trade balance, current account, capital and financial account, and

official reserve account for each year. b. Use these numbers to describe what has

happened in terms of Japanese financial transactions with the rest of the world.

The domestic economy seems to be overheating, with rapid economic growth and low

unemployment. News has just been released that the monthly activity level is even

higher than expected (as measured by new orders to factories and unemployment

figures). This news leads to renewed fears of inflationary pressures and likely action by

the monetary authorities to raise interest rates to slow the economy down. Why is this

news good or bad for the exchange rate?

Because of the relative rise in local production costs brought about by the appreciation

of the yen, many Japanese corporations have decided to transfer production abroad.

What should be the immediate and future impact on the Japanese balance of payments?

You are currently borrowing 10 million at three-month Euribor + 75 basis points. The

Euribor is

at 3%. You expect to borrow this amount for five years but are worried that Euribor will

rise in the future. You can buy a 4% cap on three-month Euribor over the next five years

with an annual cost of 0.75% (paid quarterly). Describe the evolution of your borrowing

costs under various interest rate scenarios (i.e., above and below 4%).

List three differences between dollar Eurobonds and Yankee bonds.

The bid-ask rates are as follows:

Spot exchange rate:

CHF/USD: 1.4100-1.4140

Interest rates:

One-month CHF 11/2 – 5/8

One-year CHF 11/4 – 1/2

One-month USD 51/8 – 1/4

One-year USD 51/2 – 3/4

What are the quotations for the one-month and one-year CHF/USD forward exchange

rates?

Foreign companies are complaining that they are prevented from exporting to Japan by

all kinds of official or unwritten impediments. Try to list some of these impediments.

What are the implications in terms of using PPP to forecast the yen exchange rate?

The spot exchange rate is =00. The one-year interest rate is equal to 4% in

Switzerland and 8% in the United States. What should the current value of the forward

exchange rate be?

In 1989, Jaguar Plc, an English company, was listed on the London SEAQ and on

NASDAQ. At the time, one-fourth of Jaguar common stock was held in the form of

American Deposit Receipts (ADRs) quoted on NASDAQ. Under U.K. accounting

principles, Jaguar reported a 1988 net income (before extraordinary items) of £61

million, a decrease of 27% from 1987 net income. Under U.S. generally accepted

accounting principles (GAAP), Jaguar reported a 1988 net income (before extraordinary

items) of £113 million, an increase of 89% over the comparable figure for 1987. What

would your reaction be as an investor?

Two bond indexes of the same market tend to give the similar total return indications

even if their composition is quite different. Why?