1) Direct costs are incurred for the benefit of more than one cost object.

2) An example of a controllable cost is equipment depreciation expense.

3) The responsibility for coordinating the preparation of a master budget should be

assigned to the Chief Executive Officer.

4) If the internal rate of return (IRR) of an investment is lower than the hurdle rate, the

project should be accepted.

5) Limited liability partnerships are designed to protect innocent partners from

malpractice or negligence claims resulting from the acts of another partner.

6) The Modified Accelerated Cost Recovery System (MACRS) is part of the U.S.

federal income tax laws and may be used for financial reporting.

7) Decentralization refers to companies that have multiple locations.

8) The FIFO method of computing equivalent units includes the beginning inventory

costs in computing the cost per equivalent unit for the current period.

9) The sales journals of companies using the perpetual and periodic inventory systems

differ in that under the perpetual system a column is used to record cost of goods sold

and inventory amounts for each sale but not the periodic system.

10) Direct materials and direct labor are examples of costs that are debited to the

Factory Overhead account in a job costing system.

11) The payment of cash dividends never changes the balance of retained earnings.

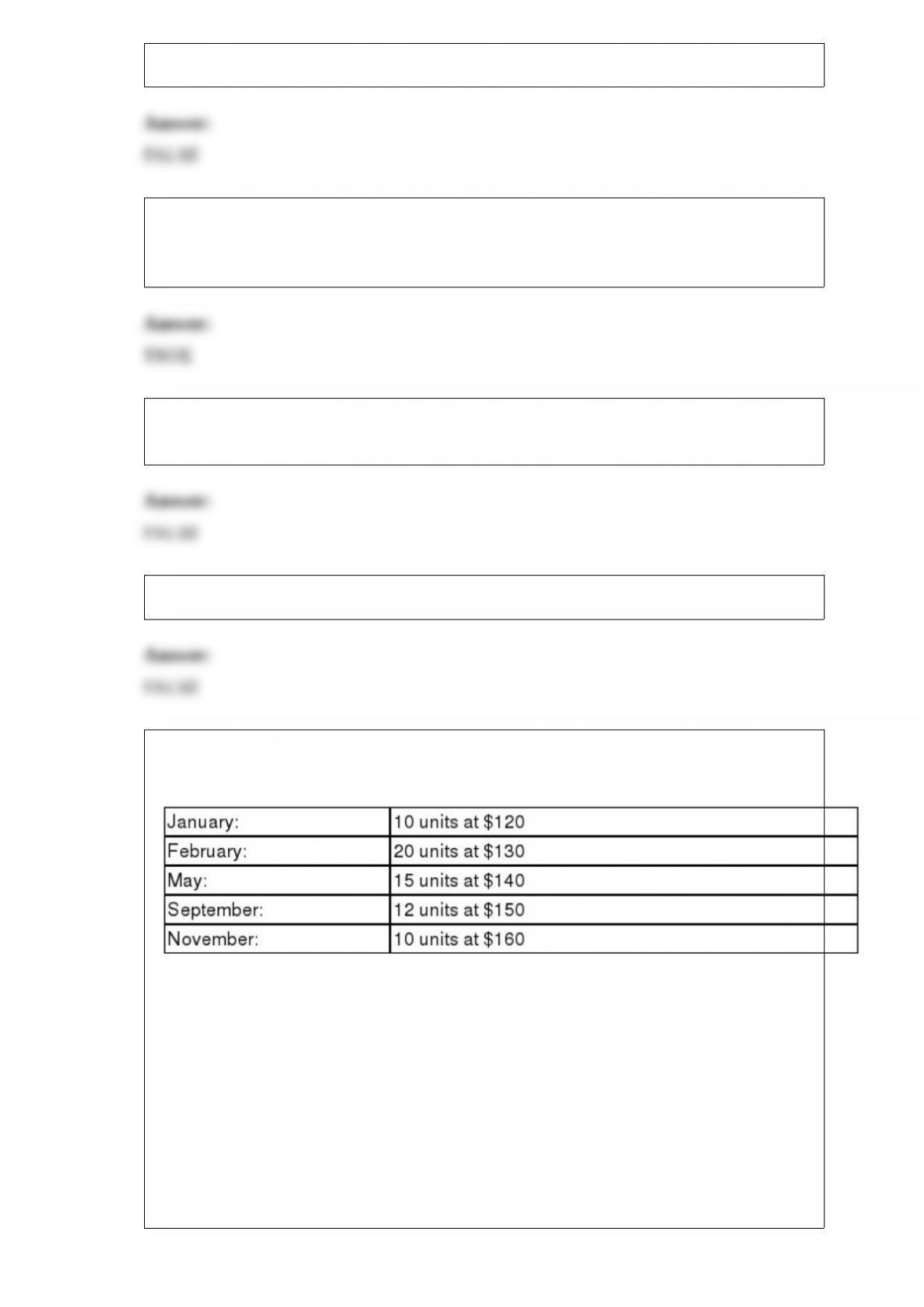

12) A company had the following purchases during the current year:

$160

On December 31, there were 26 units remaining in ending inventory. These 26 units

consisted of 2 from January, 4 from February, 6 from May, 4 from September, and 10

from November. Using the specific identification method, what is the cost of the ending

inventory?

A.$3,500.

B.$3,800.

C.$3,960.

D.$3,280.

E.$3,640.

13) The difference between the actual cost incurred and the standard cost is called the:

A.Flexible variance.

B.Price variance.

C.Cost variance.

D.Controllable variance.

E.Volume variance.

14) A company that uses the net method of recording purchases made a purchase of

$400 with terms of 2/10, n/30. The entry to record the purchase would be:

A.Debit Merchandise Inventory $392; credit Accounts Payable $392.

B.Debit Merchandise Inventory $400; credit Discounts Lost $8; credit Accounts

Payable $392.

C.Debit Merchandise Inventory $392; credit Cash for $392.

D.Debit Merchandise Inventory $392; debit Discounts Lost $8; credit Accounts Payable

$400.

E.Debit Accounts Payable $400; credit Discounts Lost $8; credit Cash $392.

15) Carter Company reported the following financial numbers for one of its divisions

for the year; average total assets of $4,100,000; sales of $4,525,000; cost of goods sold

of $2,550,000; and operating expenses of $1,372,000. Assume a target income of 10%

of average invested assets. Compute residual income for the division:

A.$203,000.

B.$193,000.

C.$150,500.

D.$60,300.

E.$197,500.

16) Zhang Company reported Cost of goods sold of $835,000, beginning Inventory of

$37,200 and ending Inventory of $46,300. The average Inventory amount is:

A.$37,200.

B.$46,300.

C.$83,500.

D.$41,750.

E.$9,100.

17) The appropriate section in the statement of cash flows for reporting the purchase of

land in exchange for common stock is:

A.Operating activities.

B.Financing activities.

C.Investing activities.

D.Schedule of noncash investing or financing activity.

E.Reconciliation of cash balance.

18) The combined costs of direct labor and factory overhead per equivalent unit used by

many businesses with process operations is called:

A.Physical cost per equivalent unit

B.Overhead cost per equivalent unit

C.Combined cost per equivalent unit

D.Conversion cost per equivalent unit

E.Finished cost per equivalent unit

19) A corporation issued 2,500 shares of its no par common stock at a cash price of $11

per share. The entry to record this transaction would be:

A.Debit Cash $27,500; credit Paid-in Capital in Excess of Par Value, Common Stock

$2,500; credit Common Stock $25,000.

B.Debit Cash $27,500; credit Common Stock $27,500.

C.Debit Common Stock $27,500; credit Cash $27,500.

D.Debit Treasury Stock $27,500; credit Cash $27,500.

E.Debit Treasury Stock $2,500; debit Paid-in Capital in Excess of Par Value, Treasury

Stock $25,000; credit Common Stock $27,500.

20) Obligations not expected to be paid within the longer of one year or the company’s

operating cycle are reported as:

A.Current assets.

B.Current liabilities.

C.Long-term liabilities.

D.Operating cycle liabilities.

E.Bills.

21) Wallace, Simpson, and Prince are partners and share income and losses in a 3:4:3

ratio. The partnership’s capital balances are Wallace, $68,000; Simpson, $90,000; and

Prince, $42,000. Royal is admitted to the partnership on July 1 with a 20% equity and

invests $50,000. The partnership would record the admission of Royal into the

partnership as:

A.Debit Wallace, Capital $15,000; debit Simpson, Capital, $20,000; debit Prince,

Capital $15,000; credit Royal, Capital $50,000.

B.Debit Cash $20,000; credit Prince, Capital $20,000.

C.Debit Cash $40,000; debit Wallace, Capital $3,000; debit Simpson, Capital, $4,000;

debit Prince, Capital $3,000; credit Royal, Capital $50,000.

D.Debit Cash $50,000; credit Royal, Capital $50,000.

E.Debit Cash $50,000; credit Simpson, Capital $10,000, credit Royal, Capital $40,000.

22) In regard to joint cost allocation, the ‘split-off point” is:

A.A physical basis method to allocate costs based on ratio of some physical

characteristic.

B.The difference between the actual and market value of joint costs.

C.The point at which some products are sold and some remain in inventory.

D.The point at which separate products can be identified.

E.Not acceptable when using the value basis for allocating joint costs.

23) Manufacturing costs other than direct materials and direct labor, and are not readily

traceable to specific units or batches of production are called:

A.Administrative expenses.

B.Nonmanufacturing costs.

C.Prime costs.

D.Factory overhead.

E.Preproduction costs.

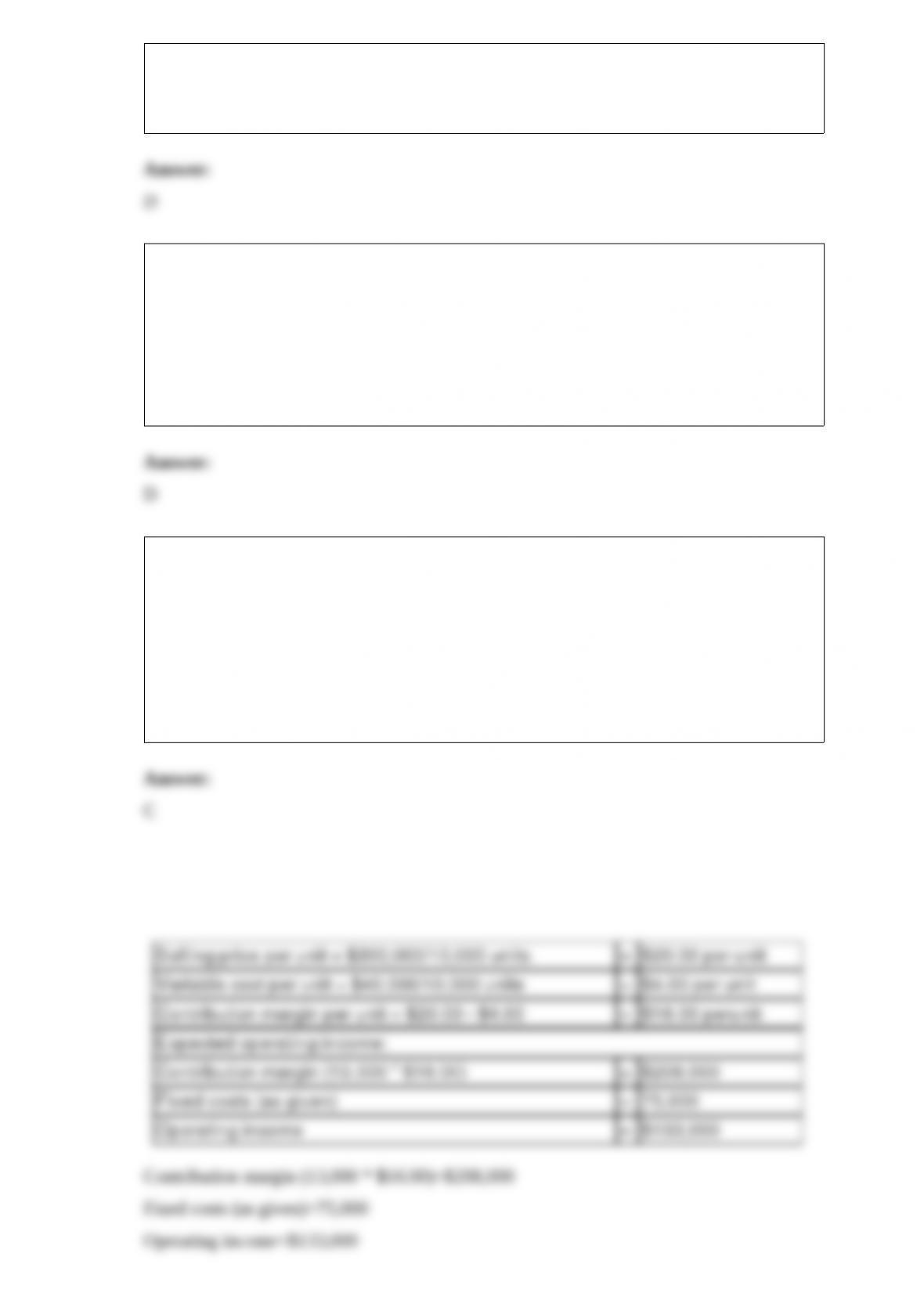

24) A company’s flexible budget for 10,000 units of production reflects sales of

$200,000; variable costs of $40,000; and fixed costs of $75,000. Calculate the expected

level of operating income if the company produces and sells 13,000 units.

A.$110,500.

B.$85,000.

C.$133,000.

D.$100,000.

E.$50,500.

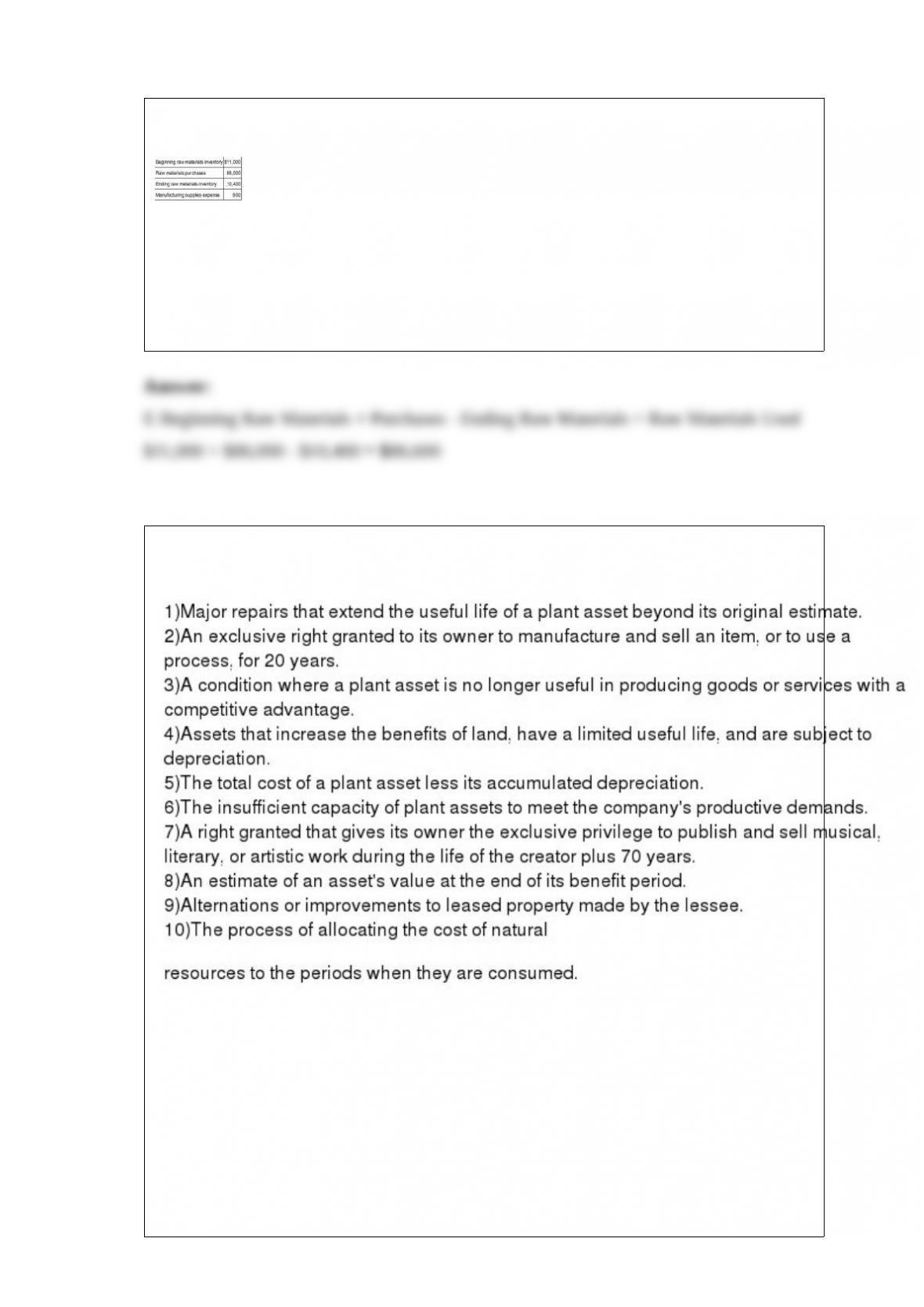

25) The following information is available for the year ended December 31:

The amount of raw materials used in production for the year is:

A.$87,500.

B.$85,700.

C.$86,900.

D.$85,400.

E.$86,600.

26) Match each of the following terms with the appropriate definitions.

A. Salvage value

B. Extraordinary repairs

C. Leasehold improvements

D. Copyright

E. Obsolescence

F. Book value

G. Depletion

H. Patent

I. Inadequacy

J. Land improvements

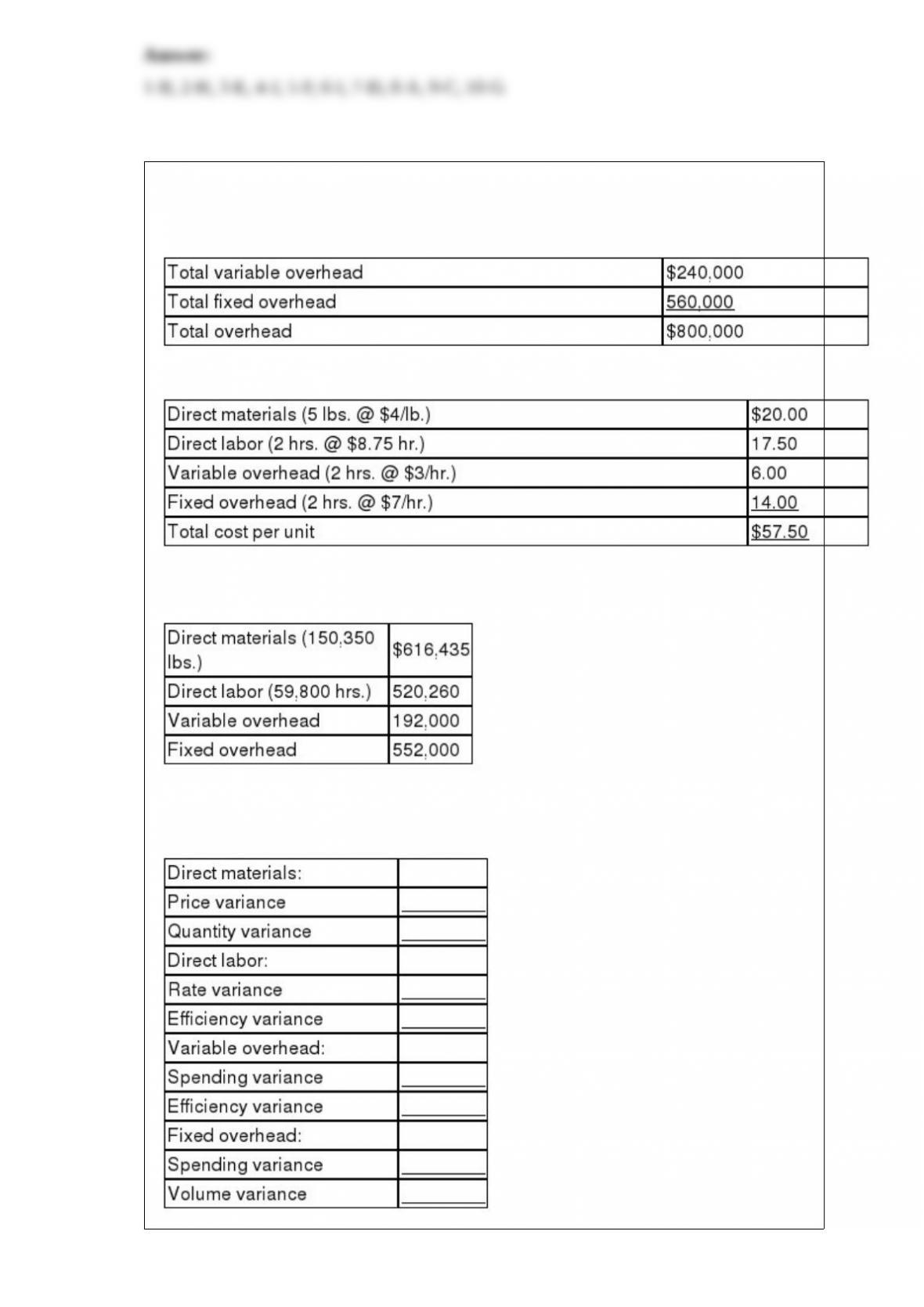

27) Tiger, Inc. budgeted the following overhead costs for the current year assuming

operations at 80% of capacity, or 40,000 units:

The standard cost per unit when operating at this same 80% capacity level is:

The actual production achieved in the current year was 60% of capacity, or 30,000

units. The actual costs were:

Calculate the following variances and indicate whether each is favorable or

unfavorable.

28) Identify at least three reasons for managers to favor the internal rate of return (IRR)

over other capital budgeting approaches.

29) A _____________________ shows the pay period dates, hours worked, gross pay,

deductions, and net pay of each employee for every pay period.

30) Wallace Company had a building that was destroyed by fire. The building originally

cost $650,000, and its accumulated depreciation as of the date of the fire was $300,000.

The company received $320,000 cash from an insurance policy that covered the

building and will use that money to help rebuild. Prepare the single journal entry to

record the disposal of the building and the receipt of cash from the insurance company.

31) What is meant by equivalent units of production, and why are they important when

a process costing system is used?

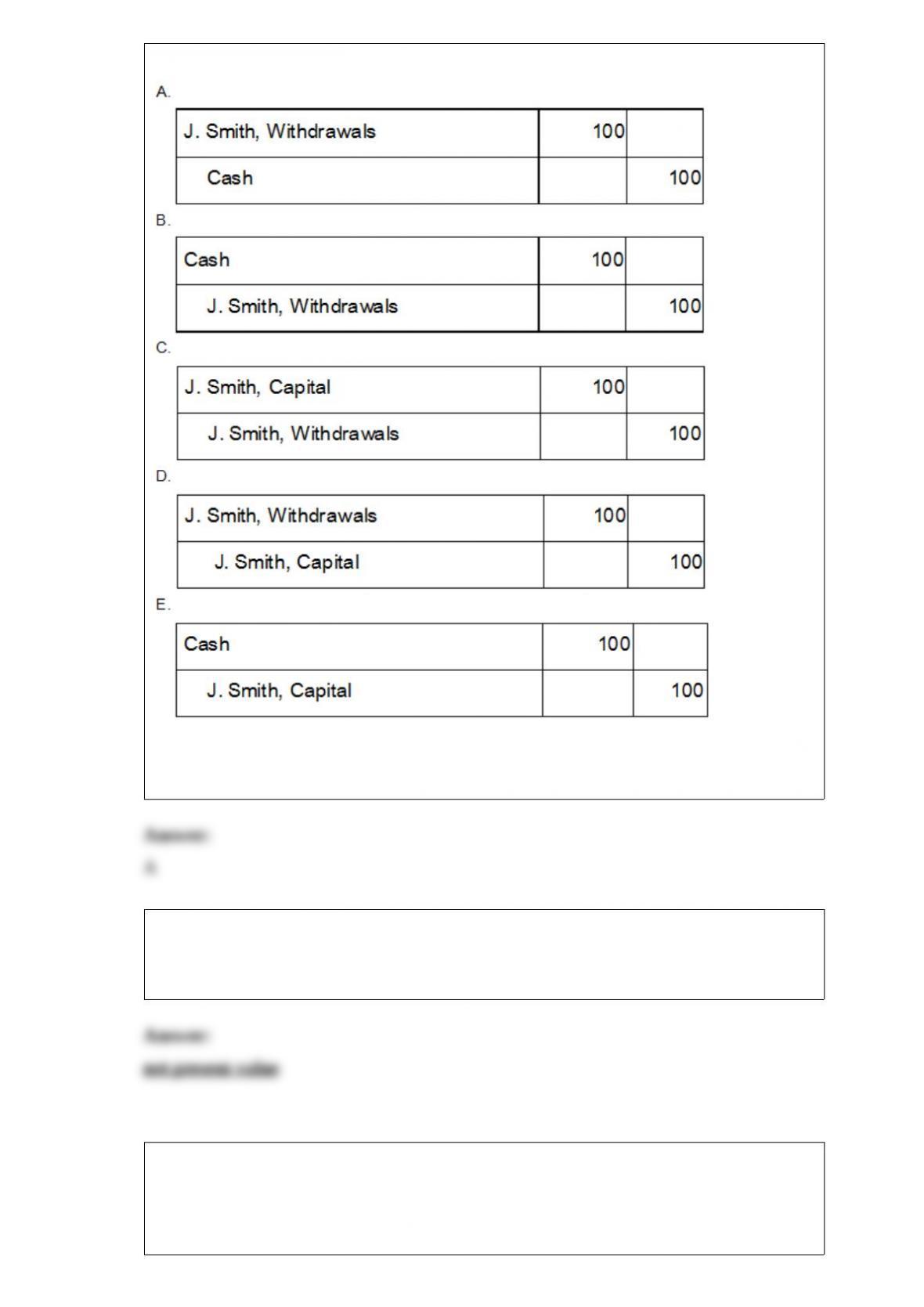

32) J. Smith withdrew $100 from Jay’s Limo Services for personal use. Which of the

following general journal entries will Jay’s Limo Services make to record this

transaction?

33) The ___________ is computed by discounting the future net cash flows from the

investment at the project’s required rate of return and then subtracting the initial amount

invested.

34) In preparing a budget for the last three months of the current year, Country Cozy

Company is planning the units of merchandise it must order each month. The

company’s policy is to have 15% of the next month’s sales in its inventory at the end of

each month. Projected sales for October, November, and December are 27,000 units,

29,500 units, and 31,000 units, respectively. How many units must be ordered in

November?

35) A _________________ system means that a company acquires or produces

inventory only when needed.