A liability for an unasserted claim must be accrued if it is reasonably possible that the

claim will be asserted.

When the right of return exists and a seller cannot make reliable estimates of future

returns, the installment sales method can be used.

The payment of cash to a supplier would be recorded in a purchases journal.

Under IFRS, accounts receivable impairments are not recognized.

Under IFRS, one of the conditions for revenue from product sales to be recognized is

when the risks and rewards of ownership have been transferred to the customer.

According to International Financial Reporting Standards (IFRS), property, plant, and

equipment must be valued at cost less accumulated depreciation.

Under IFRS No. 9, debt investments are classified as either “available for sale” or “fair

value through profit and loss (FVPL).”

When a long-term contract does not qualify for revenue recognition over time, all gross

profit and loss recognition occurs when the contract is completed.

Which of the following is not an indicator that the constraint on recognizing variable

consideration should be applied?

a. Poor (limited) evidence on which to base an estimate

b. A broad range of outcomes that could occur

c. A short delay before uncertainty resolves

d. A history of the seller changing payment terms on similar contracts

Stock options, rights, and warrants are different from convertible securities in that

they:

a. Typically increase cash upon exercise.

b. Usually reduce total assets upon exercise.

c. Often reduce liabilities upon exercise.

d. Normally increase retained earnings upon exercise.

On July 1, 2016, Tremen Corporation acquired 40% of the shares of Delany Company.

Tremen paid $3,000,000 for the investment, and that amount is exactly equal to 40% of

the book value of identifiable net assets on Delany’s balance sheet. Delany recognized

net income of $1,000,000 for 2016, and paid $150,000 of dividends each quarter to its

shareholders. After all closing entries are made, Tremen’s “Investment in Delany

Company” account would have a balance of:

a. $3,200,000.

b. $3,160,000.

c. $3,000,000.

d. $3,080,000.

On September 30, 2016, Bricker Enterprises purchased a machine for $200,000. The

estimated service life is 10 years with a $20,000 residual value. Bricker records

partial-year depreciation based on the number of months in service. Depreciation for

2017, using double-declining balance, would be:

a. $32,000.

b. $34,000.

c. $38,000.

d. $40,000.

Nontrade receivables do not include:

a. Sales to customers.

b. Loans to employees.

c. Income tax refund receivable.

d. Advances to affiliated companies.

Which of the following would not be a cash inflow from financing activities?

a. Cash from issuing common stock.

b. Cash from issuing bonds.

c. Cash from issuing preferred stock.

d. Cash from the sale of stock of a supplier.

Independent auditors express an opinion on the:

a. Fairness of financial statements.

b. Accuracy of financial statements.

c. Soundness of a company’s future.

d. Quality of a company’s management.

GG Inc. uses LIFO. GG disclosed that if FIFO had been used, inventory at the end of

2016 would have been $15 million higher than the difference between LIFO and FIFO

at the end of 2015. Assuming GG has a 40% income tax rate:

a. Its reported cost of goods sold for 2016 would have been $9 million higher if it had

used FIFO rather than LIFO for its financial statements.

b. Its reported cost of goods sold for 2016 would have been $15 million higher if it had

used FIFO rather than LIFO for its financial statements.

c. Its reported net income for 2016 would have been $9 million higher if it had used

FIFO rather than LIFO for its financial statements.

d. Its reported net income for 2016 would have been $15 million higher if it had used

FIFO rather than LIFO for its financial statements.

Popeye Company purchased a machine for $300,000 on January 1, 2015. Popeye

depreciates machines of this type by the straight-line method over a five-year period

using no salvage value. Due to an error, no depreciation was taken on this machine in

2015. Popeye discovered the error in 2016. What amount should Popeye record as

depreciation expense for 2016? The tax rate is 40%.

a. $120,000.

b. $60,000.

c. $36,000.

d. $72,000.

Red Co. can estimate the amount of loss that will occur if a foreign government

expropriates some of the company’s assets in that country. If expropriation is probable,

a loss contingency should be:

a. Disclosed but not accrued as a liability.

b. Disclosed and accrued as a liability.

c. Accrued as liability but not disclosed.

d. Neither accrued as a liability nor disclosed.

The FASB’s stated preference for reporting operating cash flows is the:

a. Indirect method.

b. Direct method.

c. Working capital method.

d. All financial resources method.

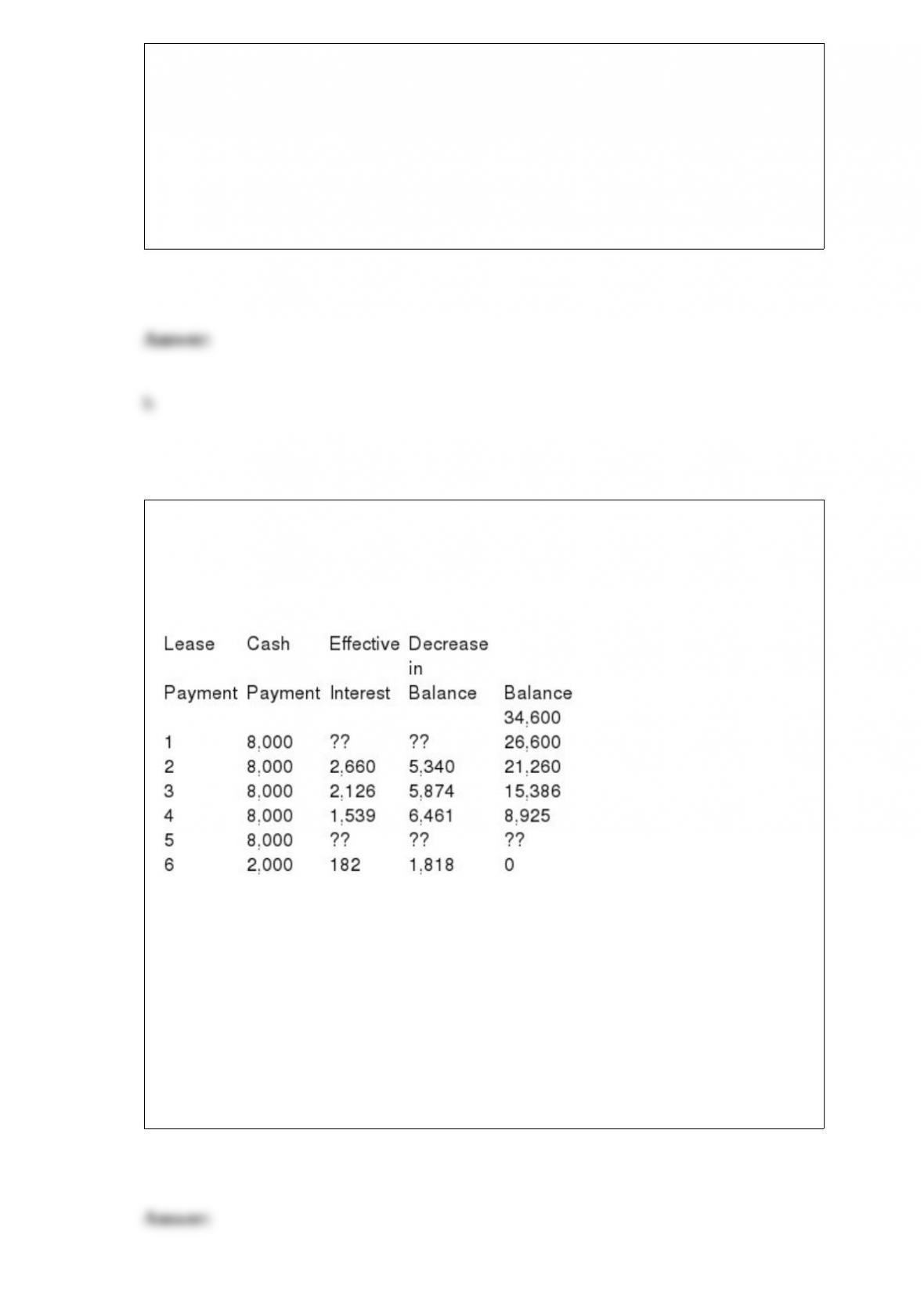

Refer to the following lease amortization schedule. The five payments are made

annually starting with the inception of the lease. A $2,000 bargain purchase option is

exercisable at the end of the five-year lease. The asset has an expected economic life of

eight years.

What is the total interest paid over the term of the lease?

a. $42,000.

b. $ 8,200.

c. $ 7,400.

d. $ 3,460.

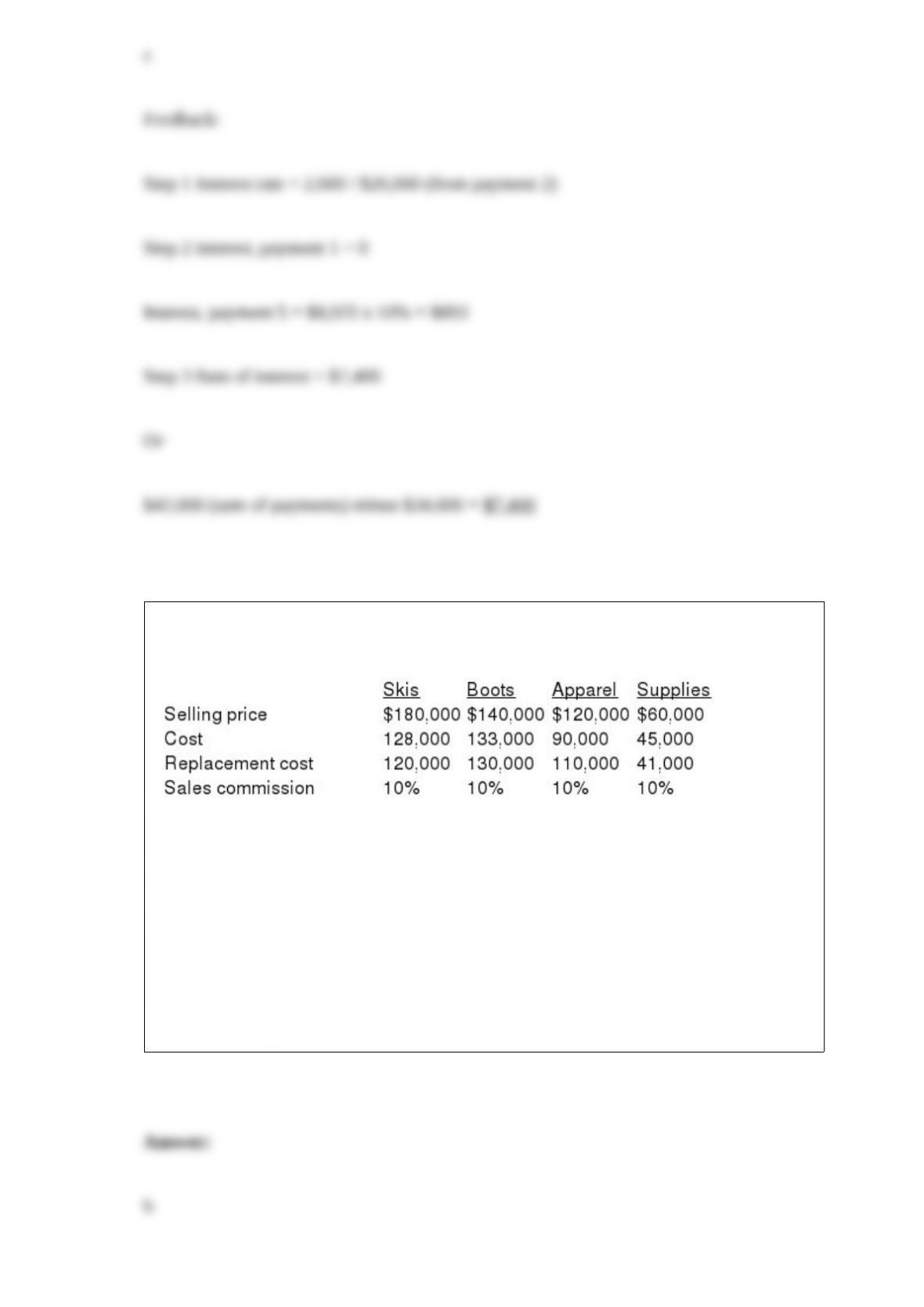

Data related to the inventories of Alpine Ski Equipment and Supplies is presented

below:

In applying the lower of cost and net realizable value rule, the inventory of skis would

be valued at:

a. $162,000.

b. $128,000.

c. $120,000.

d. $180,000.

Wang Corporation purchased $100,000 of Hales Inc. 6% bonds at par with the intent

and ability to hold the bonds until they matured in 2020, so Wang classifies its

investment as held to maturity. Unfortunately, a combination of problems at Hales and

in the debt market caused the fair value of the Hales investment to decline to $70,000

during 2016. Wang views this decline as an other-than-temporary (OTT) impairment.

Wang calculates that, of the $30,000 drop in fair value, $10,000 of it relates to credit

losses and $20,000 relates to non-credit losses. If Wang accounts for the Hales bonds

under IAS No. 39, before-tax net income for 2016 will be reduced by: a. $0.

b. $10,000.

c. $20,000.

d. $30,000.

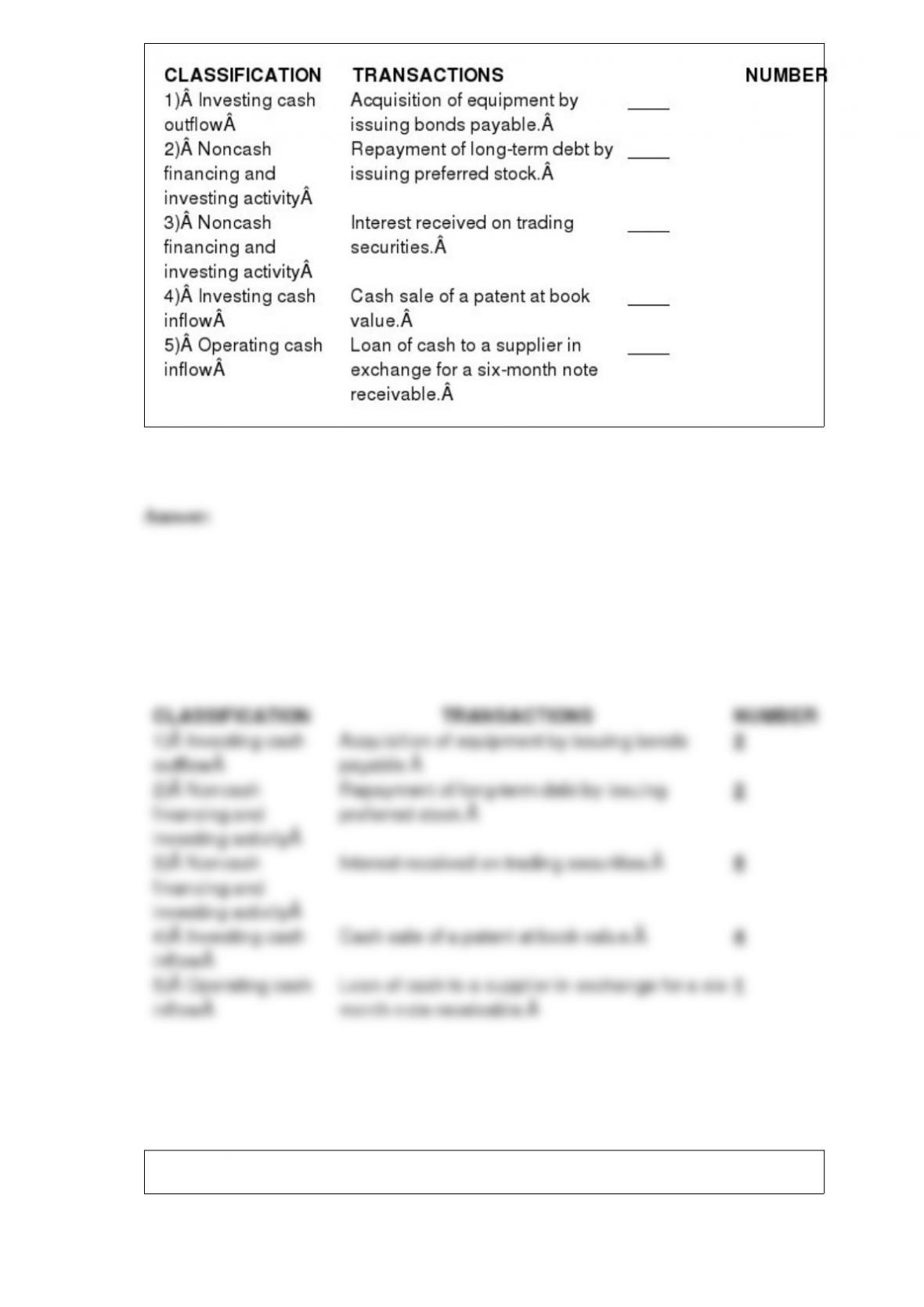

Listed below are the reporting classifications for a statement of cash flows using the

direct method for reporting operating cash flows. Indicate the reporting classification

that would apply to each of the five transactions described below by placing the number

of the reporting classification in the space provided by each transaction.

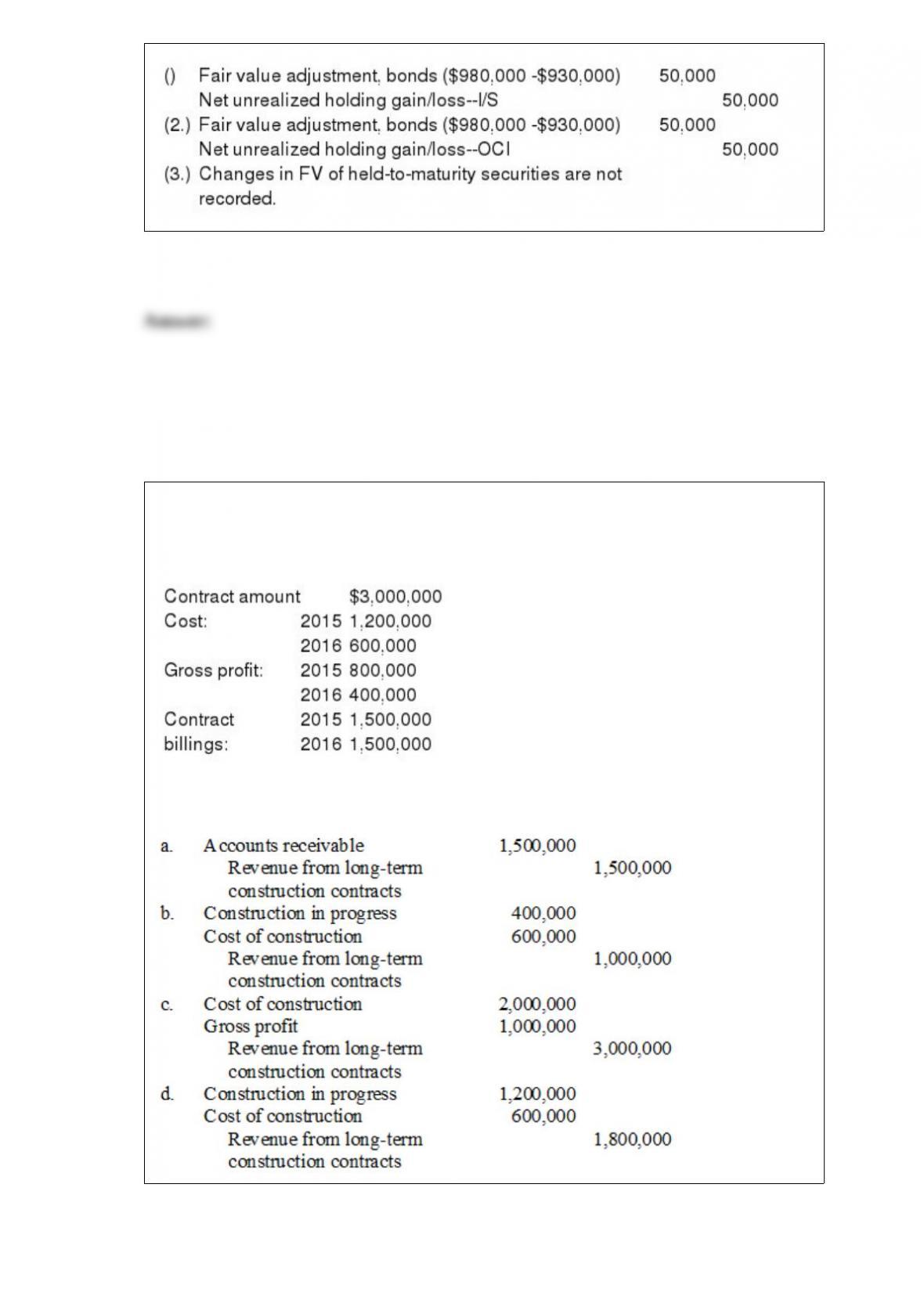

Sahara Desert Homes (SDH) reports under IFRS and constructed a new subdivision

during 2015 and 2016 under contract with Cactus Development Co. Relevant data are

summarized below:

SDH uses the cost recovery method under IFRS to recognize revenue. What is SDH’s

journal entry to record revenue in 2016?

Shown below is the activity for one of the products of Random Creations: January 1

balance, 80 units @ $50 $4,000

Purchases:

January 18: 40 units @ $51

January 28: 40 units @ $52

Sales:

January 12: 30 units

January 22: 30 units

January 31: 45 units Required: Compute the January 31 ending inventory and cost of

goods sold for January, assuming Random Creations uses average cost and a periodic

inventory system.

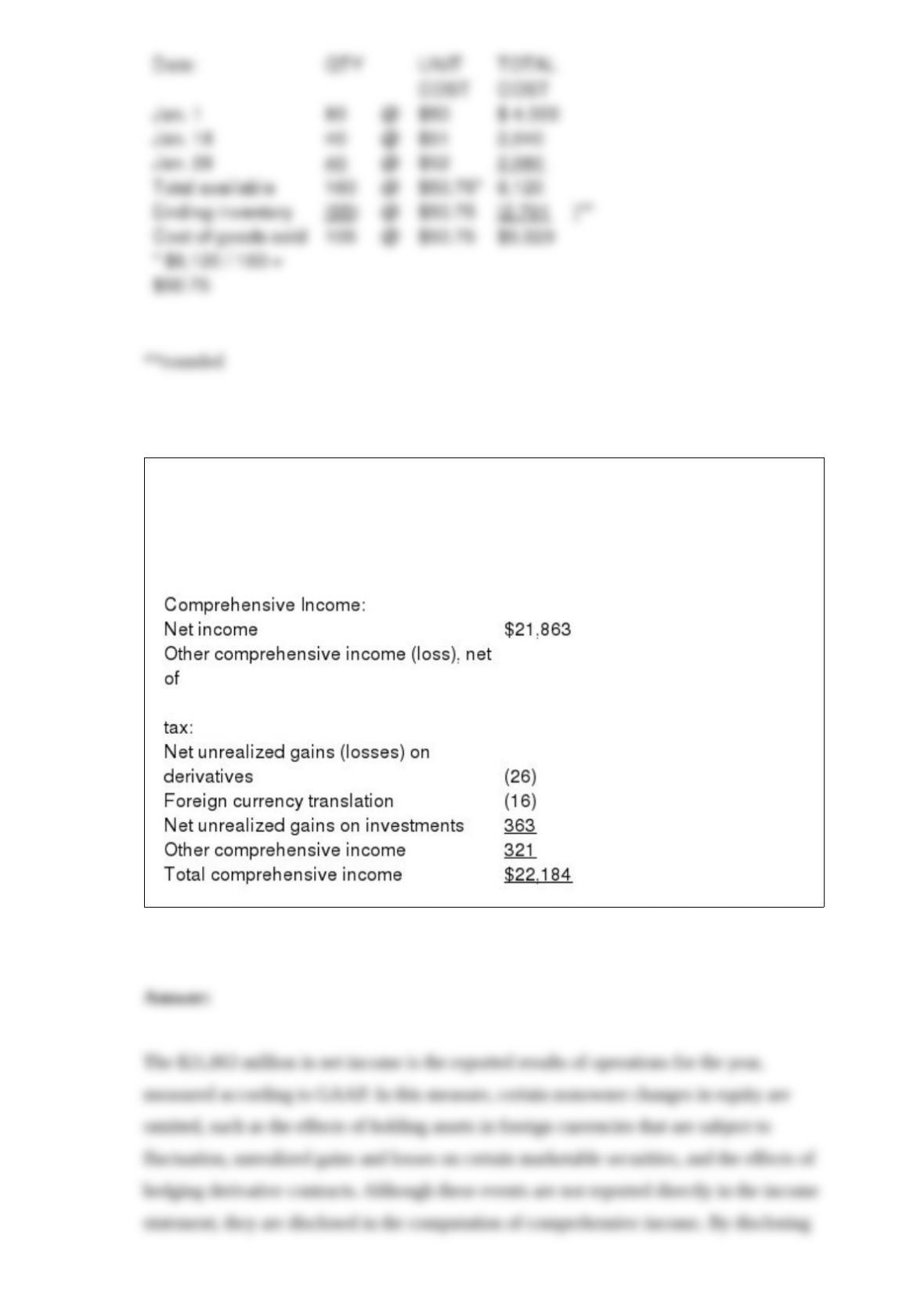

Presented below is an excerpt ($ in millions) from the 2014 annual report to

shareholders of Microsoft Corporation. Explain how the shareholder should interpret

the difference between the net income and total comprehensive income for Microsoft in

2014.

Brunetti Co. designed and installed customized signs for Di Antonio CPA, Inc.

Brunetti’s contract specifies that it will receive a flat fee of $15,000 for providing the

customized signs, and an additional $1,000 if 30% of Di Antonio’s new customers

indicate they first learned of Di Antonio because of the signs. Based on historical

experience, Brunetti estimates that there is a 90% chance it will achieve the threshold to

receive a bonus.

Assuming Brunetti uses the most likely value to estimate the variable consideration,

calculate the transaction price.

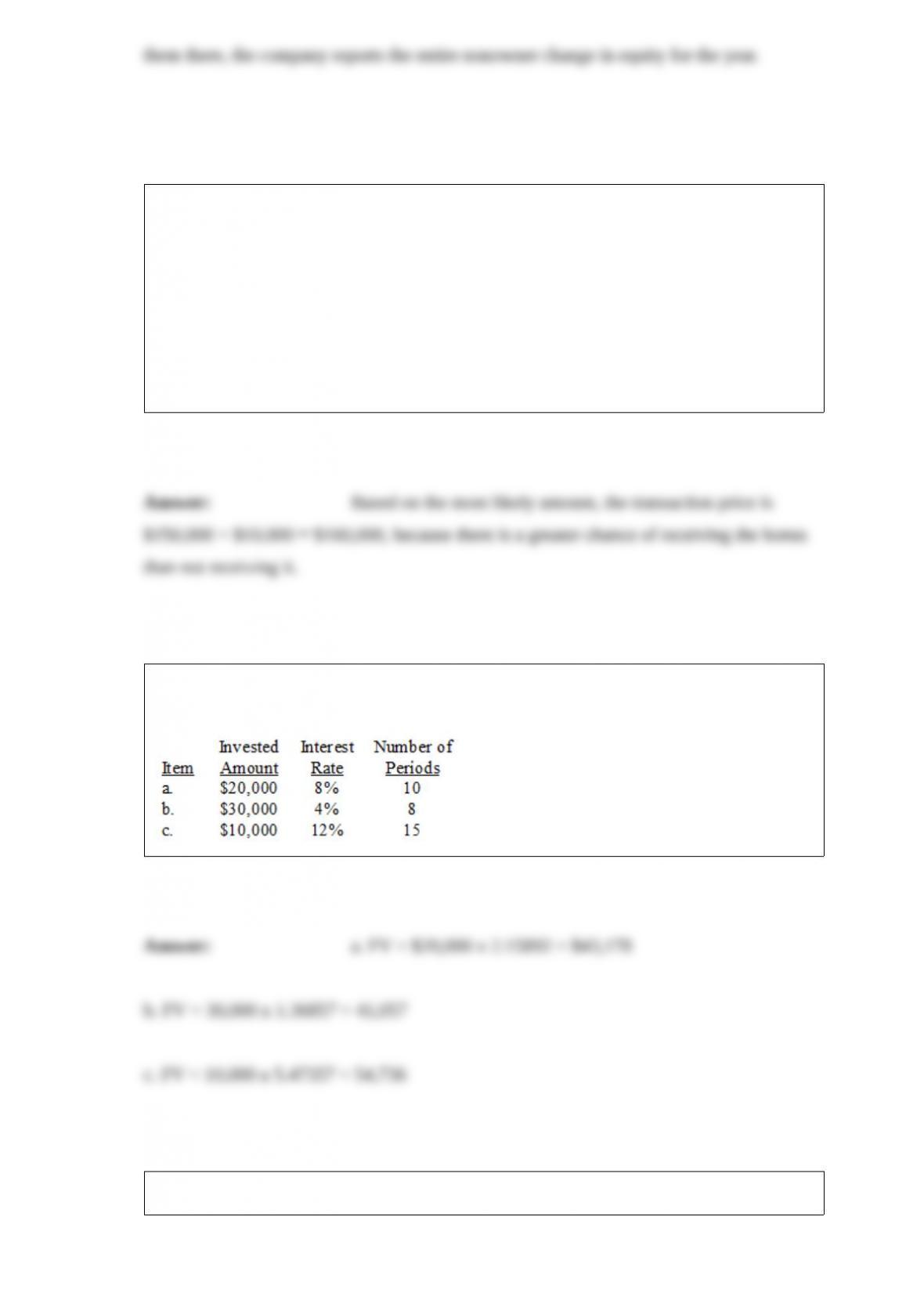

Compute the future value of the following invested amounts at the specified periods and

interest rates.

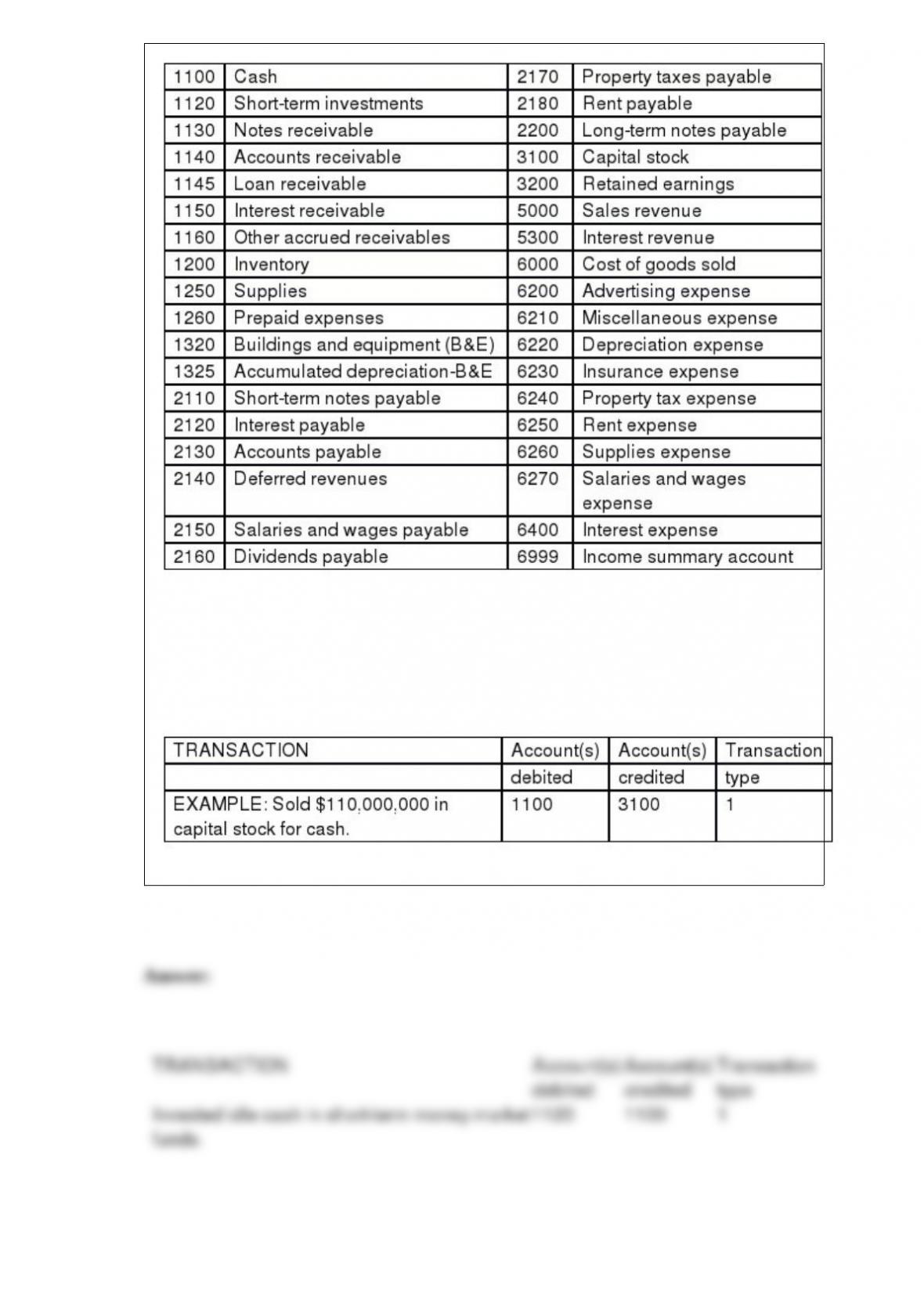

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Invested idle cash in short-term money market funds.

Romano Services provides room cleaning arrangements for hotels in Ohio. On April 1,

Silvia Hotels & Resorts signed an agreement to outsource its room cleaning functions to

Romano. The contract specifies the service fee to be $15,000 per month, and all

payments are to be made shortly after the end of each quarter. It also specifies that

Romano will receive an additional quarterly bonus of $3,000, if during that quarter,

Silvia receives no more than five complaints from customers about room cleanliness. –

On April 1, based on historical experience, Romano estimated that there is a 75%

chance that it will earn the quarterly bonus.

– On May 5, Romano learned that, during March, there were two complaints from

customers related to room cleanliness. Based on this new information, Romano revised

its estimate downward to 40% that it would earn the quarterly bonus.

– On June 30, Silvia notified Romano that, for the quarter ended, there were four

complaints associated with room cleanliness, so Romano would receive the bonus. Two

days later, Romano received all payments due for all services rendered in the second

quarter, including the bonus. Romano bases estimates of variable consideration on the

expected value of the consideration it expects to receive.

Prepare Romano’s April 30 journal entry to account for the revenue earned in April.