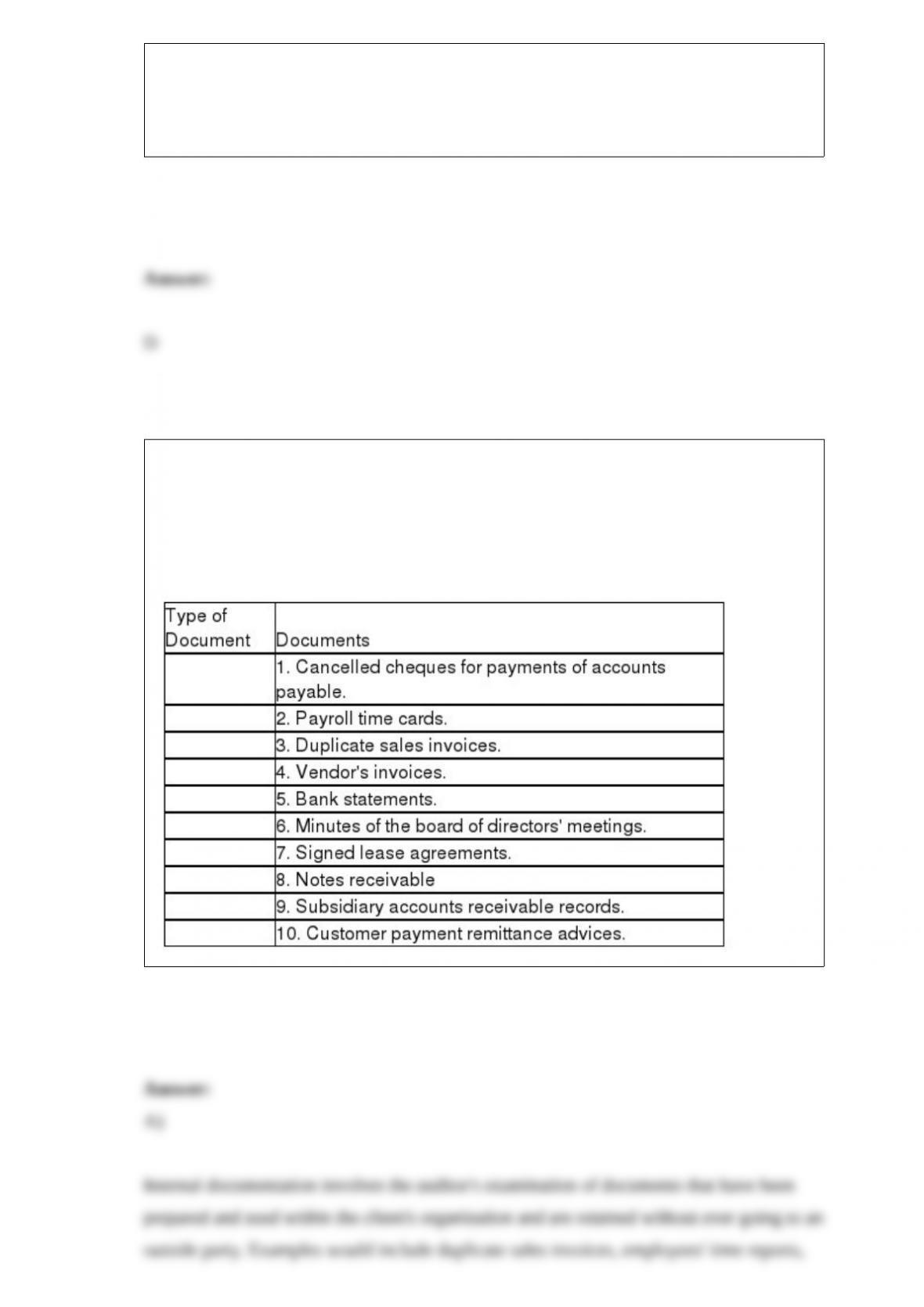

If a potential loss on a contingent liability is likely and the amount of the loss can be

reasonably estimated, the liability should be

A) accrued and indicated in the body of the financial statements.

B) disclosed in footnotes, but not accrued.

C) neither accrued nor disclosed in footnotes.

D) disclosed in the auditor’s report but not disclosed on the financial statements.

The auditor would like to design a test of control to test the following key control:

‘statements are mailed to all customers each month.” Which of the following typical

tests of controls would be suitable?

A) inquire about who is responsible for mailing the statements

B) find out whether customers pay by statement or by invoice

C) reconcile subsequent payments to particular invoices

D) match remittance advices from customers to customer statements

A wage rate form that also documents a change in job responsibility for one of the

warehouse employees should be approved by the

A) human resources and the corporate controller.

B) warehouse supervisor and human resources.

C) warehouse supervisor.

D) human resources.

Donna sees a large variation in the gross margin percentage as a result of analytical

procedures she performed. This means that

A) Donna should perform more tests.

B) the financial statements contain an error.

C) Donna cannot rely on the company’s internal controls.

D) Donna should document this difference.

The auditor uses a proof of cash to determine whether

A) internal controls over cash have been functioning effectively in the period under

audit.

B) all recorded cash receipts were deposited and whether all recorded cash

disbursements were paid by the bank.

C) accounts receivable was properly recorded and whether cash receipts transactions

were properly recorded.

D) accounts payable was properly recorded and whether cash disbursement transactions

were properly recorded.

The bias in recording inventory would be toward

A) overstatement.

B) understatement.

C) increasing share price.

D) income smoothing.

One of the most controversial parts of the auditor’s report is the meaning of the term

“presents fairly.” What does the auditor’s opinion mean when these words are used? The

A) values in the financial statements represent the net realizable values of the assets of

the entity.

B) financial statements are accurate and provide a true and fair representation of the

entity’s current financial position.

C) values in the financial statements represent the value of the entity now, if it were

liquidated on an open market.

D) financial statements are fairly presented in accordance with the financial reporting

framework described in the opinion paragraph.

The independent auditor’s opinion explains how much evidence the auditor collects

during the independent audit. How much evidence is collected?

A) sufficient and appropriate to provide a basis for the audit opinion

B) sufficient to state that there are no material errors in the financial statements

C) appropriate to be able to evaluate the exact accuracy of the accounting estimates

D) sufficient and appropriate to conclude the financial statements present a true and fair

view of the economic events of the organization

If a potential loss on a contingent liability is unlikely and the event will not likely have

a significant adverse financial effect, the liability should be

A) accrued and indicated in the body of the financial statements.

B) disclosed in footnotes, but not accrued.

C) neither accrued nor disclosed in footnotes.

D) disclosed in the auditor’s report but not disclosed on the financial statements.

The auditor will obtain a copy of the client’s articles of incorporation (if applicable) and

retain a copy in the permanent file. Important information in the articles of

incorporation includes

A) the interest rates currently being paid for bonds that have been issued.

B) voting rights of each class of shares issued by the company.

C) which shares have been redeemed by the company in the current year.

D) the interest rates that are being received on long term notes invested.

During final review of working papers and financial statements, possible oversights in

the audit can be identified by

A) the partner’s knowledge of the client’s business combined with effective analytical

procedures.

B) conducting a closing interview with management of the client.

C) conducting a meeting with the audit team.

D) review the minutes from the board meetings.

The internal control which requires “approval of acquisitions at the proper level”

satisfies the objective of

A) occurrence.

B) completeness.

C) accuracy.

D) posting and summarization.

There is a greater risk of defalcation for cash than for other types of assets because

A) it is easier to steal.

B) most other assets must be converted to cash to make them usable.

C) companies usually have weak internal controls surrounding cash.

D) most employees have access to cash.

Responsibility for the issuance of new notes should be vested in the

A) board of directors.

B) accounting department.

C) accounts payable department.

D) purchasing department.

A) Discuss the key control procedures relating to the client’s physical count of

inventory.

B) State the primary determinants of the amount of time needed to perform the physical

observation of inventory.

An effective board of directors helps ensure that the company takes only appropriate

risks. The audit committee can

A) reduce the likelihood of fraud and financial statement errors through oversight of the

entity level controls.

B) reduce the likelihood of financial statement errors by helping management of the

company with complex financial reporting issues.

C) reduce the likelihood of financial statement errors by helping management in the

preparation of the financial statements and related notes.

D) reduce the likelihood of overly aggressive accounting through oversight of financial

reporting.

As part of audit planning, you have calculated accounts receivable turnover for the last

five years, and compared it to industry averages. Your client’s accounts receivable has

decreased by about 1.25 times in the current year, while the industry rate has improved.

One possible cause of this lowered accounts receivable turnover is

A) higher cost of goods sold.

B) increased bad debt expenses.

C) fictitious revenue.

D) fictitious expenses.

Camilla is preparing the audit program for the inventory of Summers, a large

department store. Camilla listed ‘select a sample of invoices from suppliers to verify

that the risks and rewards of the inventory were transferred to Summers”. Camilla is

concerned that some of the inventory in the store might be on consignment. The

account balance related objective that Camilla is concerned about is

A) rights and obligation (ownership).

B) accuracy.

C) valuation.

D) existence.

The tests of details of balances procedure which requires the auditor to trace the totals

of the notes payable list to the general ledger satisfies the objective of

A) existence.

B) completeness.

C) accuracy.

D) rights and obligations.

“Recorded payroll payments are for work actually performed by existing employees” is

the control objective of

A) authorization.

B) completeness.

C) occurrence.

D) accuracy.

An important part of evaluating whether the financial statements are fairly stated is

summarizing the misstatements uncovered in the audit. Whenever the auditor uncovers

misstatements that are in themselves material,

A) entries should be proposed to the client to correct the statements.

B) no entries need be made but footnote disclosure is required.

C) it is necessary to combine individually immaterial misstatements with the material

misstatements and make entries to correct the statements.

D) it is necessary to combine individually immaterial misstatements with the material

misstatements and make full disclosure in the footnotes.

A) Explain what is meant by a cutoff bank statement and discuss the purpose of the

cutoff bank statement in the audit of cash.

B) Explain the purpose of testing the client’s bank reconciliation and discuss the major

audit procedures involved.

A branch bank account is helpful for

A) limiting the impact of a fraud.

B) improving internal controls.

C) empowering the different branches of the company.

D) building public relations in local communities.

A) Distinguish between internal documentation and external documentation as types of

audit evidence. Give two examples of each. Which type is considered more reliable?

B) Below are 10 documents typically examined by auditors. Classify each document as

either internal or external.

The auditor has conducted tests of controls of the write off of accounts receivable and

found two exceptions. These exceptions are

A) an indication of the likelihood of errors or fraud and other irregularities.

B) confirmation that controls are not functioning as designed throughout the year.

C) information about the quantity of the dollar error in accounts receivable.

D) indications that employee training is required in the accounting area.

An important type of protective measure for safeguarding assets and records is

A) adequate segregation of duties among personnel.

B) proper authorization of transactions.

C) the use of physical precautions.

D) adequate documentation.

A secondary objective of the auditor’s study and evaluation of internal control is that the

study and evaluation provide

A) a basis for constructive suggestions concerning improvements in internal control.

B) a basis for reliance on the accounting system.

C) an assurance that the records and documents have been maintained in accordance

with existing company policies and procedures.

D) an indication that management and employees are trustworthy.

PA is auditing a client where the accounts receivable are in worse shape than last year:

many accounts are significantly overdue. How would this fact be dealt with in the audit

risk model?

A) increase inherent risk for accounts receivable

B) decrease inherent risk for accounts receivable

C) increase control risk for accounts receivable

D) decrease control risk for accounts receivable

What situation represents a fiduciary duty?

A) A professional accountant acts as a director of an organization.

B) A professional accountant performs an audit.

C) The owner of a private company prepares financial statements.

D) A professional accountant performs a non-assurance engagement.

A public accountant examining inventory may appropriately apply sampling for

attributes in order to estimate the

A) average price of inventory items.

B) percentage of slow-moving inventory items.

C) dollar value of inventory.

D) physical quantity of inventory items.

Formal frameworks have been developed to help people resolve ethical dilemmas. After

obtaining the relevant facts and identifying the ethical issues from the facts, what is the

next step in the six-step ethical framework?

A) Decide on the appropriate action to be taken in resolving the ethical dilemma.

B) Identify the likely consequences of actions that will be taken.

C) Determine who is affected by the outcome of the dilemma and how they are

affected.

D) Identify the alternatives available to the person who must resolve the dilemma.

Your client, Macilbink Ltd., manufactures calendars, books and magazines. The

printing presses that they use are only three years old, yet new technology has been

developed that would result in cuts in ink and electricity costs by over 20%, while

simplifying the set up process (the new equipment can read in PDF files directly),

making lower production runs more feasible. Macilbink Ltd. is facing lowered demand

for its products, and will need to change direction or innovate to stay in business. The

effect of the new printing technology has resulted in the following risk assessment

changes by Macilbink Ltd.’s auditors:

A) decrease control risk

B) increase control risk

C) decrease client business risk

D) increase client business risk

When external users place heavy reliance on the financial statements it is appropriate

that

A) audit risk be increased.

B) inherent risk be decreased.

C) inherent risk be increased.

D) audit risk be decreased.

Renaldo compared shipping reports to sales documents, checking to see that the sales

invoice date matched the shipping date, and that quantities invoiced matched quantities

shipped. On his working paper, he said that he vouched invoices. What else should his

working paper include with respect to the audit procedure conducted?

A) details of tests conducted, with results

B) results of analytical review procedures on the aging of accounts receivable

C) employee number and wage rate of the employees he spoke to

D) a statement that the information will be held confidential

Adequate planning and execution to reduce risk to an acceptable level is a requirement

of which category of generally accepted auditing standard?

A) General

B) Examination

C) Reporting

D) Quality