Control risk has been assessed at 100% for your client. What audit approach will you

follow?

A) combined approach.

B) substantive approach.

C) reliance on analytical review and tests of controls.

D) reliance on tests of controls and tests of details.

Which of the following is a factor that relates to “incentives or pressures” to commit

fraudulent financial reporting?

A) Significant accounting estimates involving subjective judgments

B) Excessive pressure for management to meet debt covenant requirements

C) Management’s practice of making overly achievable forecasts

D) High turnover of accounting, internal audit and information technology staff

You generally consider your audit client’s management to be honest. However, they do

have a bias towards wanting to understate their income to lower income taxes. How

would this bias be implemented in the audit risk model?

A) reduce audit risk and reduce inherent risk

B) increase audit risk and reduce inherent risk

C) reduce audit risk and increase inherent risk

D) increase audit risk and increase inherent risk

One difference between auditors and other professionals is that most professionals

A) need not be concerned about maintaining independence.

B) don’t have requirements for continuing education beyond university.

C) don’t have to pass a rigorous examination.

D) aren’t expected to act in the public interest.

How frequently does the auditor make a decision with respect to the sample size to be

selected?

A) once for the entire audit

B) for each transaction cycle

C) once for each type of audit procedure

D) for each audit procedure

A public accounting firm can issue a compilation report

A) only if the partners are independent.

B) only if all the partners and the staff in the office performing the engagement are

independent.

C) if the partners have no material or direct immaterial interest in client.

D) even if it is not independent.

The first step in the financial statement audit using a risk assessment approach is to

A) identify risks of material misstatement.

B) gather evidence to assess the likelihood of material misstatement.

C) evaluate audit evidence.

D) evaluate the reporting framework.

Carrie found an error in the sample she tested from the population of accounts

receivable that was over 90 days old. The error found by Carrie should be extrapolated

to the population of

A) all past due accounts receivable.

B) accounts receivable over 90 days.

C) all accounts receivable.

D) current accounts receivable.

If a PA firm provided corporate finance services to a company during the year, which of

the following engagements could the PA firm accept to provide to the same company?

A) Non-assurance services

B) Audit of listed entity

C) Audit of non-listed entity

D) Other assurance engagement

A) List the four items which a defendant must prove in an action for negligence against

a public accountant.

B) Describe each of the six defences a public accounting firm can normally use when

facing legal claims by clients.

C) Discuss what is meant by the term “expectation gap.”

Both disclaimers of opinion and adverse opinions are used

A) only when the condition is highly material and pervasive.

B) whether the condition is material or not.

C) regardless of the auditor’s independence.

D) regardless of the client’s choice of accounting method.

The overall objectives of the audit test must be stated in terms of the

A) anticipated results.

B) transaction cycle being tested.

C) risks addressed and the transaction cycle being tested.

D) risk addressed and the anticipated results.

The factor which distinguishes an error from fraud and other irregularity is

A) materiality.

B) intent.

C) whether it is a dollar amount or a process.

D) whether it is a caused by the auditor or the client.

To detect an overstatement or understatement of inventory and cost of goods sold, the

auditor may perform an analytical procedure such as comparing

A) gross margin percentage with previous years.

B) inventory turnover with previous years.

C) current year manufacturing costs with previous years.

D) extended inventory value with previous years.

PAs are members of a professional association that can impose sanctions for violations

of the professional code of conduct. What is an example of a severe penalty that can be

imposed by a professional association?

A) Publication of information about the offence in a newsletter

B) Requirement of the completion of training courses

C) Requirement to have another peer review conducted within one year

D) Expulsion from the professional association

Frontenac Construction, your audit client, is a construction company. In the initial

planning phase of the audit, you identified that it has many contracts with severe

non-performance clauses if any of the current constructions are not completed on the

dates set in the contracts over the next three years. As the auditor, you would set the

inherent risk for sales and penalties as

A) high.

B) moderate.

C) low.

D) cannot be determined until more procedures are performed.

Enron and Equity Funding are companies that suffered from large frauds by corporate

management. One important lesson with respect to such cases is that

A) when a company does really well financially it is important to suspect that such

results are always inflated.

B) an investigation of the integrity of management is an important part of deciding

upon the extent of audit work.

C) securities and exchange commissions expect auditors to be perfect in their

assessment of management.

D) partners and staff should cooperate in preparing working papers that prove the

accuracy of the financial statements.

Under what circumstances would an auditor prepare a proof of cash? When

A) the client has material internal control weaknesses in cash.

B) control risk is set at minimum.

C) inherent risk in cash is considered to be low.

D) an enterprise resource system is in use for processing of cash transactions.

The Ultramares doctrine is that ordinary negligence is insufficient for liability of

auditors to third parties because of the lack of privity of contract between the third party

and the auditor. What type of behaviour on the part of an auditor would result in

liability to more general third parties according to this doctrine?

A) conducting an audit engagement when a review engagement had been contracted

B) completing work in accordance with a contract that was signed with the client

C) deliberate misstatement of the financial statements by management remaining

undetected

D) fraud or constructive fraud with respect to the working papers

Your client has two sets of financial statements. One set is in compliance with IFRS,

while the other set is in compliance with local tax legislation, and will be used only

with the tax returns. How do these events affect the independent auditors report? The

auditor would use

A) an unqualified audit report for both financial statements, with an Emphasis of Matter

paragraph that describes to readers the nature of the other set of financial statements.

B) a standard unqualified auditor’s report for both financial statements, labeling the

auditor’s report “for IFRS only” and “for tax purposes only.”

C) an unqualified audit report for both financial statements, with an Other Matter

paragraph that describes to readers the nature of the other set of financial statements.

D) a qualified audit report would be issued as the client may not have two different sets

of financial statements.

Which one of the following would the auditor consider to be an incompatible operation

if the cashier receives remittances from the mailroom? The cashier

A) prepares the daily deposit.

B) makes the daily deposit at a local bank.

C) records the receipts to the customer files.

D) endorses the cheques with the company endorsement stamp.

When manufacturing labour affects inventory valuation, a knowledgeable manager

should approve wage rate allocations to make sure that labour is distributed to the

proper accounts. Which of the following controls helps to prevent error in the resulting

job costing?

A) comparison of wage rates to the authorized payroll master file

B) independent comparison of the approved amounts to the data entered

C) continuity check of the payroll cheque numbers issued

D) reconciliation of gross pay on the payroll register with gross pay according to the

payroll master file

Which one of the following forms of advertisement would violate solicitation rules? PA

A) placed an advertisement in a newspaper indicating the opening of a new office.

B) conducted a cold-calling campaign where companies were asked if they would like

to change PA firms.

C) placed a media advertisement listing the different types of expertise available at the

firm’s major office locations.

D) conducted a survey asking companies about the types of services that are provided

by their accounting firms.

If a lawyer refuses to provide the auditor with information that is within the lawyer’s

jurisdiction and may directly affect the fair presentation of financial statements about

material existing lawsuits (asserted claims) or unasserted claims, the audit report would

have to be

A) an adverse opinion.

B) a qualified opinion.

C) an unqualified opinion with an explanatory paragraph.

D) modified to reflect the lack of available evidence (ie. scope limitation).

The process which requires the calculation of an interval and then selects the items

based on the size of the interval is

A) statistical sampling.

B) random selection.

C) systematic selection.

D) computerized selection.

The auditor is determining which specific inventory items should be selected for pricing

tests. The auditor has selected a representative sample, and those items that have a large

dollar amount. In addition, the auditor should select those items that

A) are prone to breakage or theft.

B) have wide fluctuations in price.

C) are stored in multiple locations.

D) are likely to have been miscounted during the inventory count.

Which of the following tests of controls would pertain to whether existing payroll

transactions are recorded?

A) Compare cancelled cheques with payroll journal details

B) Compare cancelled cheques with payroll records

C) Foot payroll journal and trace details to general ledger

D) Conduct gap testing for a sequence of payroll cheques

During discussion and inquiry with management, the auditor determined that the

company has started a new line of business, requiring a substantial investment in

manufacturing equipment. The company has also implemented wireless scanning for its

warehouse and inventory. Which of the following techniques will the auditor likely use

to corroborate these statements?

A) further inquiry of the accounting personnel

B) inspection of recent sales invoices for types of sales

C) use of analytical procedures, comparing last year to this year

D) observation during the plant tour

If from last year to the current year’s audit, inherent risk has stayed constant, but control

risk is higher (it is more likely that controls do not detect material errors), what is the

likely effect on detection risk? Detection risk will

A) increase.

B) decrease.

C) stay the same.

D) need less documentation.

The following are two unrelated situations. For each situation outline possible

deviations (if any) from a standard auditor’s report that may be necessary, and give

reasons. State your assumptions.

A) Queen Lake Construction Ltd. uses an aggressive revenue recognition policy under

the percentage of completion method for long-term construction contracts. Your review

of this year’s contracts indicates that several projects look as if they will be high in

revenue for the first two years, and then have negligible earnings for the next three

years.

B) Maple Manufacturing Limited constructs furniture out of maple wood. The furniture

is prized for its durability and craftsmanship. Last year, the company received a letter

from a governmental agency advising that it had been found that the factory was

located on contaminated land that leached hazardous chemicals into the air. This was a

preliminary letter stating that a full investigation into the health effects was underway.

Management stated that everything is OK – the investigation was terminated. However,

the lawyer refused to sign the legal letter with respect to several lawsuits with respect to

employee claims for long term disability due to a nervous disorder that affected

employees’ ability to work. Neither the investigation nor the lawsuits are disclosed in

the notes to the financial statements.

The auditor selects several transactions in each functional area and traces them through

the entire accounting system, paying special attention to evidence about whether or not

the control features are in operation. This is an example of a

A) sequence test.

B) test of controls.

C) substantive test.

D) functional test.

The procedures to test effectiveness of control policies and procedures in support of a

reduced assessed control risk are called

A) tests of details of balances.

B) tests of controls.

C) analytical procedures.

D) a walk-through.

At the completion of the audit, management is asked to make a written statement that it

is not aware of any undisclosed contingent liabilities. This statement would appear in

the

A) management letter.

B) representation letter.

C) engagement letter.

D) letters testamentary.

Comparison of the total balance in notes payable, interest expense and accrued interest

with these accounts in the prior year could detect what type of possible misstatement?

A) Misstatement of interest expense or accrued interest, or omission of a note payable

B) Omission or misstatement of a note payable

C) Misclassification of a note payable as long term rather than current

D) Misstatement of notes payable, interest expense or accrued interest

A) One step in the planning phase of an audit is to obtain information about the client’s

legal obligations. Identify the types of legal documents and records that auditors

examine to obtain this information.

B) Discuss the audit-relevant information contained in each of these three types of

documents that an auditor should be aware of early in the audit.

State five specific balance-related audit objectives for physical inventory observation

and, for each objective, describe one common test of details of balances related to that

objective.

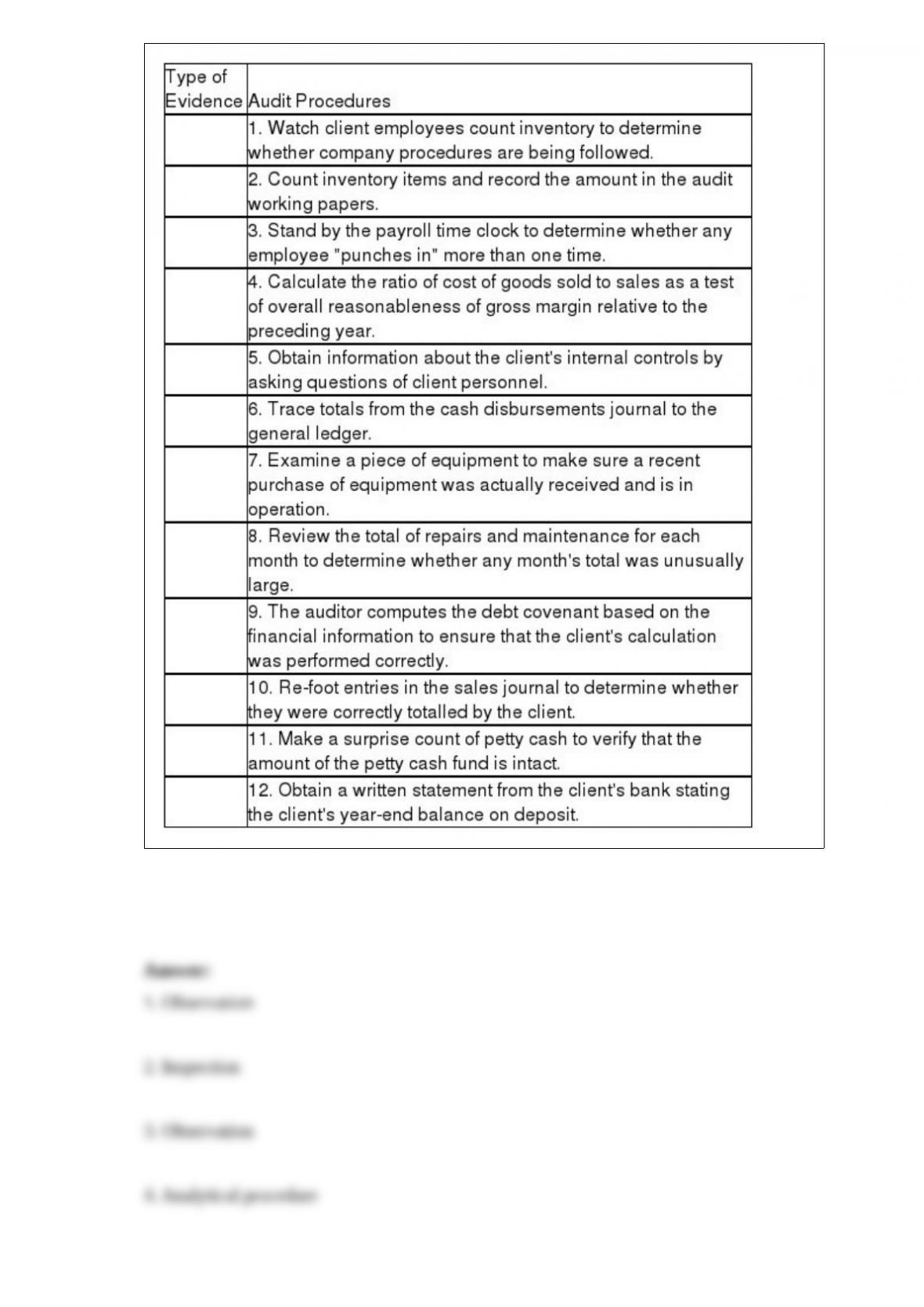

Below are 12 audit procedures. Classify each procedure according to the following

types of audit evidence: (1) inspection, (2) external confirmation, (3) recalculation, (4)

observation, (5) inquiry of the client, (6) reperformance, and (7) analytical procedure.

Outline the audit procedures that would be performed when testing electronic receipts

and payments.

Your preliminary discussion with European Real Estate Management (EREM)

Corporation indicated that the company was owned by three Swedish individuals who

sold limited liability partnerships of shopping malls, office buildings and large

residential apartment buildings to European investors. Often, a single shopping mall

was broken up into several limited liability partnerships to make the ownership pieces

small enough to sell easily.

In some cases, these partnership units were sold to European companies, who

diversified and bought units in several buildings. Other units were purchased by

individuals. If a property looked particularly promising, the owners of EREM

occasionally purchased units or advised their wives and family members to purchase

units.

Required:

Explain why it is important for the auditor to identify related party transactions. Why

are related party transactions a high risk area for the EREM audit?

You have just been given the approval to conduct statistical sampling for the audit of

capital assets acquisitions. Previously, this work was completed using a judgmental

sample.

Required:

Explain the key areas where decisions need to be made when conducting audit work

using a statistical sample.

As part of your audit of the payroll for Jones Chu Company Limited (JCC), you used

generalized audit software. You had available to you the payroll transactions for the

month of September and the employee master file as of the date of September 30. You

conducted the following tests, with results noted:

1. Ran a duplicates test on employee number in the transaction file. You found that one

employee, employee number 320, had been paid twice, using cheque numbers 12376

and 12377.

2. Check the calculation of “pay per period” in the employee master file. (Divide the

salary field by 12 to derive the monthly pay). It was found that for two employees these

calculations did not match. Employee #20 had a pay of $200 higher than the

calculation, while employee # 220 had a pay that was $65 higher than the calculations.

3. Check that “gross pay” less “unemployment insurance, Canada Pension Plan and

income taxes deducted” equals “net pay.” No errors were found.

Required:

For each audit test

(i) Describe the audit assertion associated with your audit test.

(ii) Discuss the results that the auditor would have expected before running the test.

(iii) Discuss the implications of the findings upon the audit process or upon specific

audit procedures.

Identify three analytical procedures commonly used when auditing accounts in the

inventory and distribution cycle.

The CICA is the professional accounting organization for Chartered Accountants (CAs).

Describe the role and responsibilities of the organization in serving its members.

White Top Telephones is the largest telephone distributor in the province, distributing

wired and wireless phones, as well as cellular phones. Management always seems to be

in a rush, and difficult to approach. Unfortunately, this attitude has permeated down to

all of the staff, and everyone seems to be hurrying about, doing what needs to be done.

Sometimes, it seems as if they don’t even have time for the customers, moving on to the

next task.

Yet everything seems to get done. The company’s web site has a lengthy privacy policy

statement indicating that customers are number one, and that all data are kept secure.

Required:

Explain the importance of the control environment and corporate governance structure.

During what phases of the risk assessment and planning process would the control

environment and corporate governance structure be documented and assessed?

Discuss three examples of analytical procedures an auditor might perform while

auditing the sales and collection cycle. Also discuss the potential misstatement(s) that

may be revealed by each analytical procedure.

Note: students could also be asked to separately discuss ratios for planning and ratios as

substantive tests.

Klein Corporation has reported a loss for the 6th year in a row. Klein also has a large

bank loan due in the coming year, bringing its current ratio to .60. Further, due to the

economic crisis, Klein had to increase its bad debt expense by 4% and also saw its

largest client, Forest Prairie filing for bankruptcy. Forest Prairie’s purchases made up

18% of the total sales of Klein in the past year. Forest Prairie also had an unpaid

balance to Klein at year end.

In trying to reduce expenses, Klein has reduced the employee training from 5 days to 1

day. During the year, an employee was seriously injured in the production process when

his arm was caught in a press. The employee has filed a lawsuit against Klein for

$1,000,000 as he claims that he was not properly trained to use the equipment. The

legal proceeding for this case should begin in the next fiscal year. Since Klein has never

been involved in such as lawsuit before, the legal counsel indicated that they were not

able to estimate the amount and likelihood that Klein would have to pay.

Required: Evaluate the going concern situation at Klein and indicate what the auditor

would be required to do under CAS 570.

Your audit client is a large retail chain with its own credit card, with annual sales of

about $100 million. On December 31, there were approximately 40,000 open accounts

with total receivables of approximately $18.5 million. Very few customer balances

exceed $1,000. The company’s general office maintains the accounts receivable records.

The large volume of transactions processed by the company has necessitated extensive

segregation of duties and frequent balancing of data during processing. Accordingly, the

company’s general and system controls are considered to be very good. A complete

record of each customer’s account is stored on a relational database and includes the

following information:

Source transactions are store purchase invoices, payments, and adjustments. Daily, all

the orders are received and entered into the computer and processed against the

customer master file. Each account is updated and automatically analyzed to determine

whether the transactions just processed have created a condition that should be brought

to the attention of the authorization or collection sections. Exception reports are

automatically printed and forwarded to these groups.

The company sends monthly statements to customers on a cyclical basis. About 2,000

statements are mailed each billing day. As the accounts are updated, the day’s

transactions are accumulated and added to the starting control figure for each cycle. The

new control figures are balanced with the sum of all the individual accounts in the cycle

(accumulated as each account is processed). In addition, a detailed transaction and cycle

control report is prepared, providing an audit trail in customer account number

sequence.

Required:

Describe the audit procedures you would perform in your year end audit work of

accounts receivable for this company. For each audit test, state the relevant audit

assertion(s). Be sure to include different types of tests as necessary (e.g. manual, or

using computer assisted audit techniques), and clearly identify those tests that can be

completed using CAATs.

There are two conditions requiring a departure from an unqualified audit report. Discuss

each of these conditions and state the appropriate audit report for each condition.

PA has been recently appointed auditor of Foible Ltd., a company that sells high cost

knickknacks to third world countries. To facilitate the rapid preparation of the financial

statements, management had the physical inventory counted in October, rather than at

the December year end. During the inventory count, PA noticed that several of the

boxes were labelled with receiving documents from a competitor. PA was told that the

new warehouse supervisor worked part time at the competitor, and must have picked up

the wrong boxes.

Several employees have sued Foible Ltd. for wrongful dismissal, claiming that they

were promised a job that would last at least one year, with low cost accommodations as

well. They are suing for the balance of the year’s wages and claiming that they were

brought into the country under false pretenses. These employees are all from an eastern

European country. The law firm has responded in the legal letter that this suit is without

merit.

During the year Foible obtained legal services from a firm in which the Chairman of the

Board of the company is a partner. Fees and disbursements for these services for the

year was $125,000, a material amount.

During the audit, employees often spoke in a foreign language among themselves

before responding to PA, then one employee would respond after some often heated

discussion.

Subsequent to the year end, the warehouse supervisor was arrested on criminal charges

of theft, and Foible charged with selling stolen goods. PA was charged as an accomplice

to money laundering, as all of the management for Foible were members of a criminal

group laundering money from eastern Europe.

Required:

Discuss the actions that PA could have taken during the engagement to prevent these

charges.

Knowledge of the client’s industry and external environment can be obtained in

different ways. Discuss some of the ways that this knowledge can be obtained.