Process costing is applied to operations with repetitive production and heterogeneous

products.

Financial accounting and tax accounting require the same recordkeeping and there

should be no difference in results between the two accounting systems.

If a department that applies process costing starts the reporting period with 100,000

physical units that were 20% complete with respect to direct labor, it must add 80%

direct labor in the current period to complete the units.

If a company purchases land paying cash, the journal entry to record this transaction

will include a debit to Cash.

Larger, more complex organizations usually require a longer time to prepare their

budgets than smaller organizations because of the considerable effort to coordinate the

different units within the business.

A high value for the times interest earned ratio means that a company is a higher risk

borrower.

If the dividends account is not recorded as a reduction to Retained Earnings on the date

of declaration, the dividends account is closed to Retained Earnings at the end of the

accounting period.

A department can never be considered to be a profit center.

The income statement is a financial statement that shows revenues earned and expenses

incurred during a specified period of time.

A columnar journal is any journal with only one column.

A trial balance that balances is not proof of complete accuracy in recording

transactions.

Mutual agency means each partner can commit or bind the partnership to any contract

within the scope of the partnership business.

A perpetual inventory system continually updates accounting records for inventory

transactions.

A cost variance equals the sum of the quantity variance and the price variance.

Four factors come together in the manufacturing process: beginning goods in process

inventory, direct materials, direct labor, and factory overhead.

A corporation can issue two kinds of stock ” common and preferred.

Using the retail inventory method, if the cost to retail ratio is 60% and ending inventory

at retail is $45,000, then estimated ending inventory at cost is $27,000.

Retained earnings generally consist of a company’s cumulative net income less any net

losses and dividends declared since its inception.

When a process cost accounting system records the purchase of raw materials, the Raw

Materials Inventory account is debited.

The entry to increase the balance in petty cash from $50 to $75 would include a credit

to Petty Cash of $25.

Technology such as cash registers, check protectors, time clocks and personal

identification scanners can improve internal control.

Accounting for the exchange of assets depends on whether the transaction has

commercial substance; commercial substance implies that it alters the company’s future

cash flows.

Stocks with a price-earnings ratio of less than 5 to 8 are likely to be overpriced.

An income statement reports the revenues earned less expenses incurred by a business

over a period of time.

The four methods of inventory valuation are SIFO, FIFO, LIFO, and average cost.

If the internal rate of return (IRR) of an investment is below the hurdle rate, the project

should be accepted.

Budgets are normally more effective when all levels of management are involved in the

budgeting process.

An out-of-pocket cost requires a current and/or future outlay of cash.

If a company sells merchandise with credit terms 2/10 n/60, the credit period is 10 days

and the discount period is 60 days.

In a process costing system, factory labor costs incurred in a reporting period are

presented on the income statement as Factory Labor Expense.

When standard costs are used, factory overhead is assigned to products with a

predetermined standard overhead rate.

The person that borrows money and signs a promissory note is called the payee.

Corporations are subject to substantially fewer regulations and laws than are

proprietorships and partnerships.

Adjusting entries are used to bring asset or liability accounts to their proper amount and

update the related expense or revenue account.

The use of internal controls provides guaranteed protection against losses due to

operating activities.

The debt ratio is calculated by dividing total assets by total liabilities.

A high level of expected risk suggests a low price-earnings ratio.

On a bank reconciliation, the amount of an unrecorded bank service charge should be:

A.Added to the book balance of cash.

B.Deducted from the book balance of cash.

C.Added to the bank balance of cash.

D.Deducted from the bank balance of cash.

E.Noted in memorandum form only.

The inventory valuation method that has the advantages of assigning an amount to

inventory on the balance sheet that approximates its current cost, and also mimics the

actual flow of goods for most businesses is:

A.FIFO.

B.Weighted average.

C.LIFO.

D.Specific identification.

E.All of these.

The control principle for accounting information systems requires that the:

A.Benefits from an activity outweigh the costs of the activity.

B.System report useful, understandable, timely, and pertinent information for effective

decision making.

C.System must have internal controls.

D.System adapt to changes in the company, business environment, and needs of

decision makers.

E.System conform with a company’s activities, personnel, and structure.

A company paid $37,800 plus a broker’s fee of $525 to acquire 8% bonds with a

$40,000 maturity value. The company intends to hold the bonds to maturity. The cash

proceeds the company will receive when the bonds mature equal:

A.$37,800.

B.$38,325.

C.$40,000.

D.$40,525.

E.$43,200.

The assets of a company total $700,000; the liabilities, $200,000. What are the claims

of the owners?

A.$900,000.

B.$700,000.

C.$500,000.

D.$200,000.

E.It is impossible to determine unless the amount of this owners’ investment is known.

The right side of a T-account is a(n):

A.Debit.

B.Increase.

C.Credit.

D.Decrease.

E.Account balance.

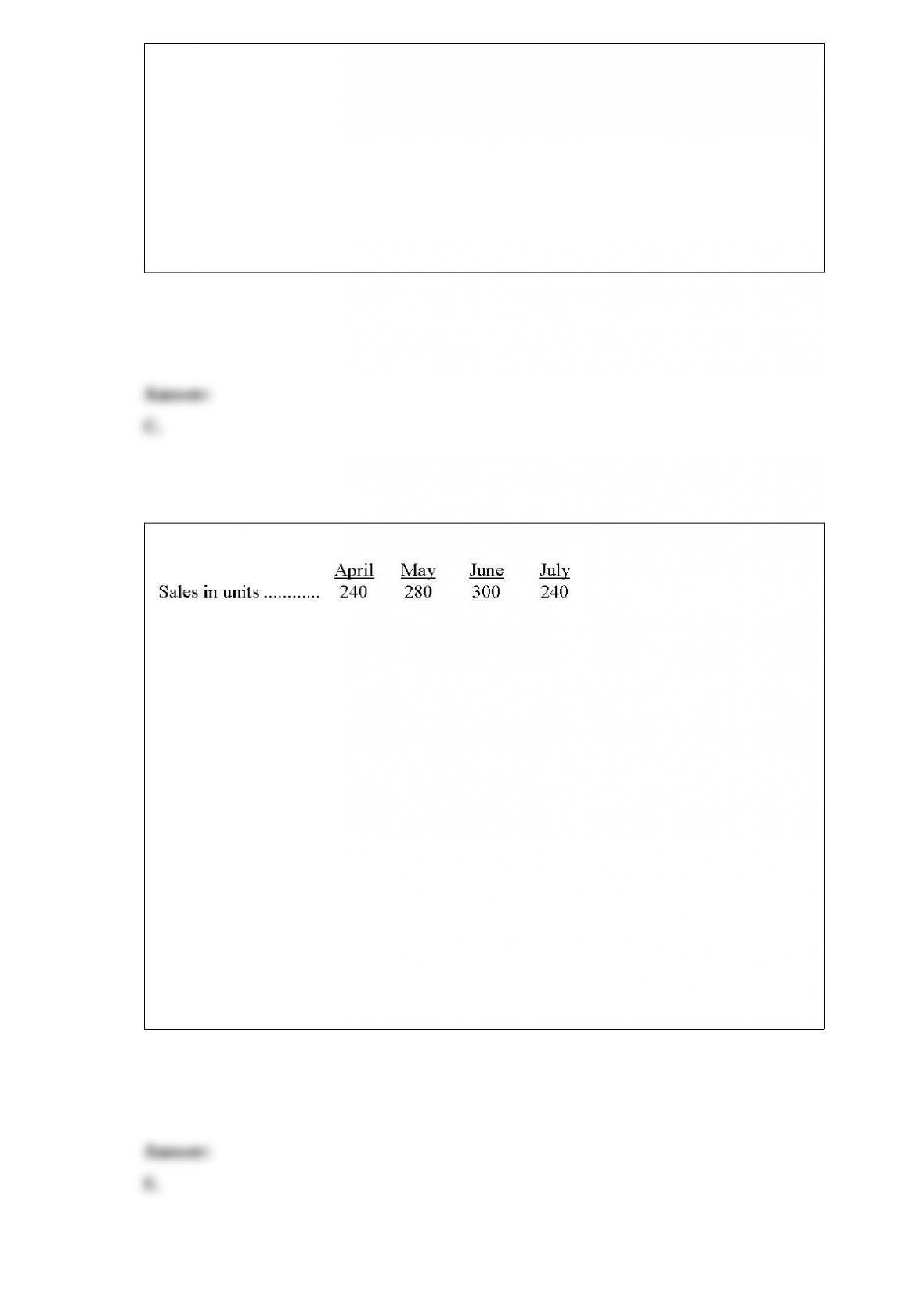

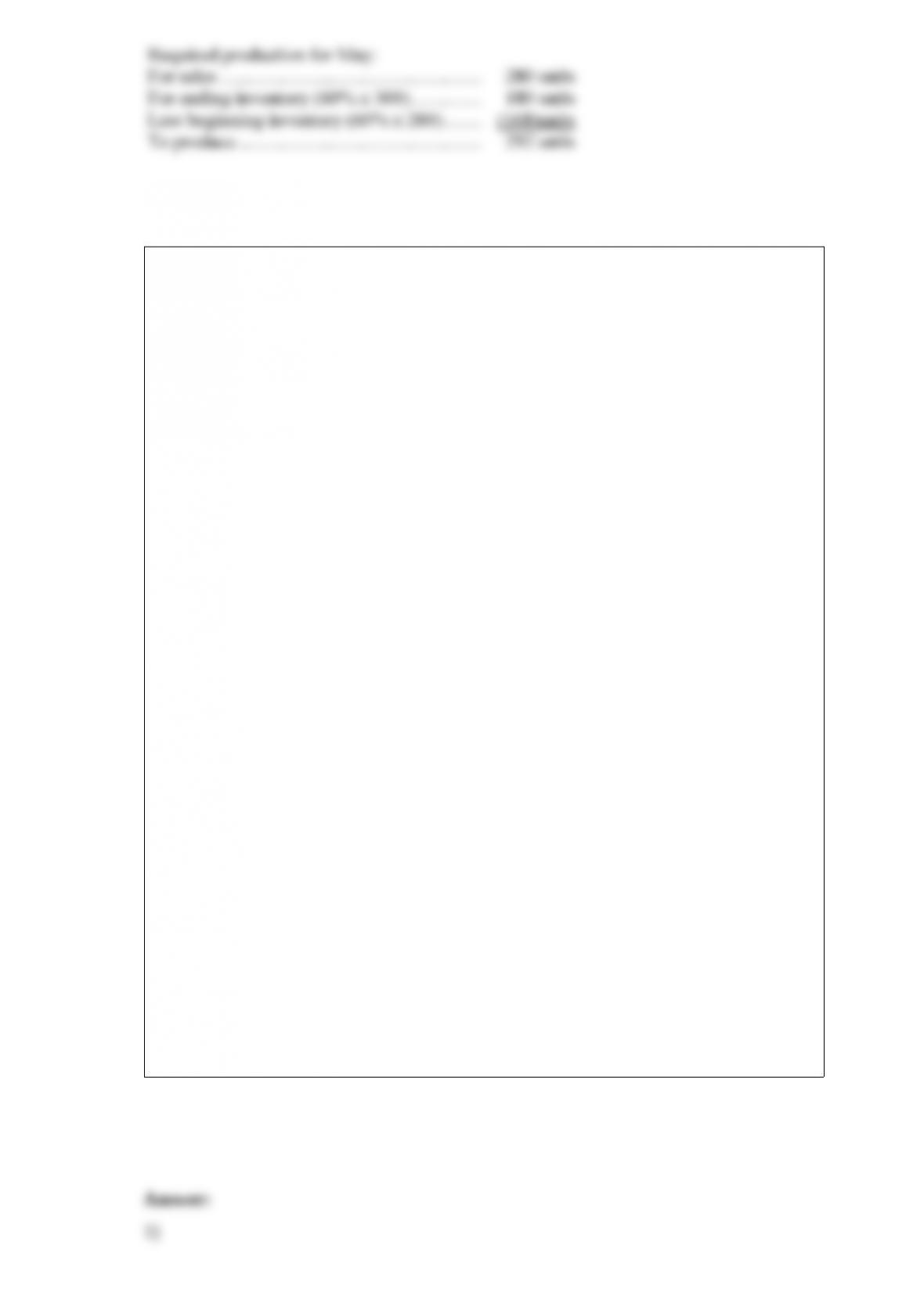

Kyoto, Inc. predicts the following sales in units for the coming four months:

Although each month’s ending inventory of finished units should be 60% of the next

month’s sales, the March 31 finished goods inventory is only 100 units. A finished unit

requires five pounds of raw material B. The March 31 raw materials inventory has 200

pounds of B. Each month’s ending inventory of raw materials should be 30% of the

following month’s production needs.

The budgeted production for May is:

A.200 units.

B.212 units.

C.268 units.

D.280 units.

E.292 units.

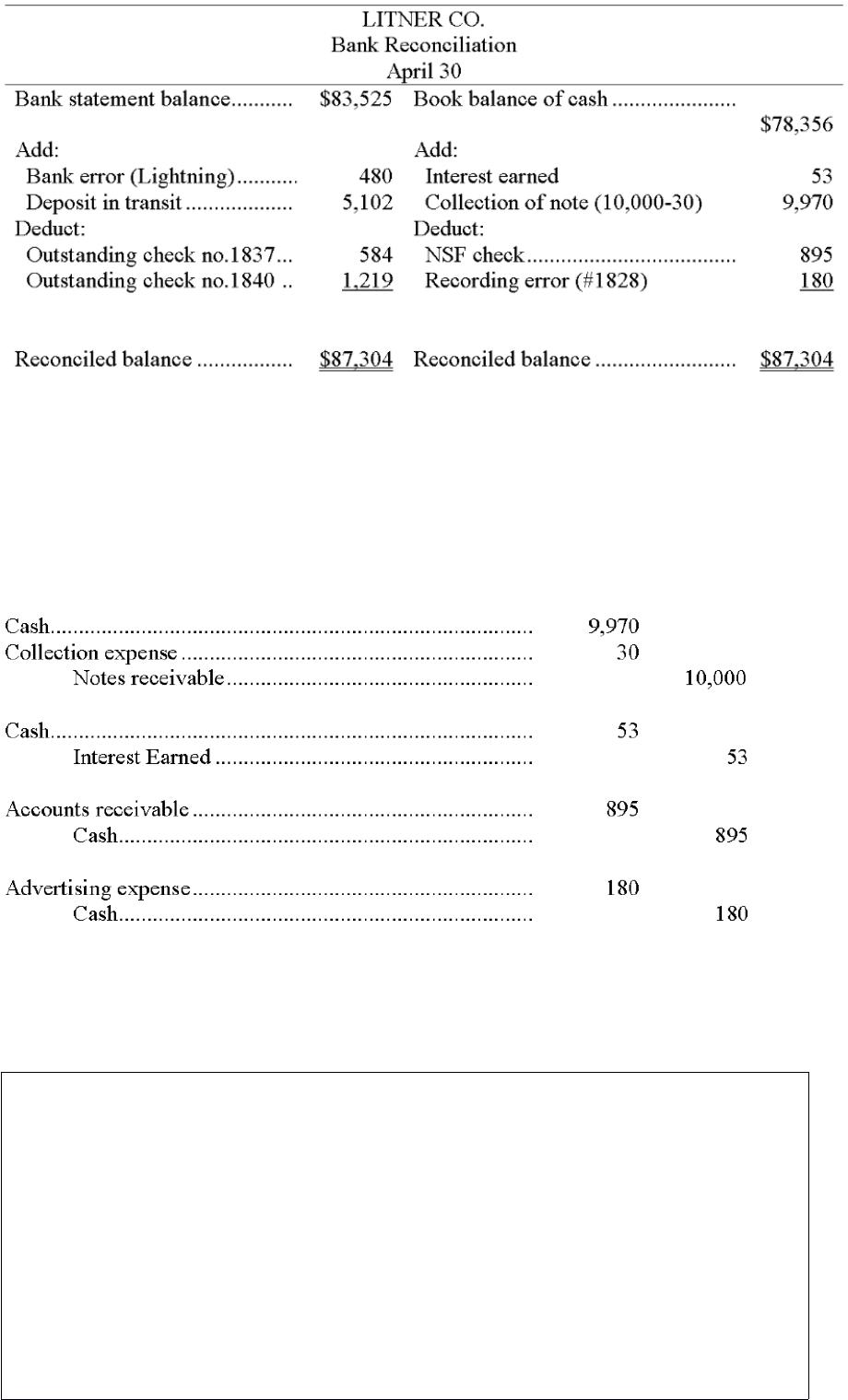

The following information is available to reconcile Litner Co.’s book balance of cash

with its bank statement cash balance as of April 30. The April 30 cash balance

according to the accounting records is $78,356, and the bank statement cash balance for

that date is $83,525.

a. The bank erroneously cleared a $480 check against the account in April that was not

issued by Litner. The check documentation included with the bank statement indicates

the check was actually issued by Lightning Co.

b. On April 30, the bank issued a credit memorandum for $53 interest earned on Litner’s

account.

c. When the April checks are compared with entries in the accounting records, it is

found that Check No. 1828 had been correctly drawn for $1,530 to pay for advertising

but was erroneously entered in the accounting records as $1,350

d. A credit memorandum indicates that the bank collected $10,000 cash on a note

receivable for Litner, deducted a $30 collection fee, and credited the balance to the

company’s Cash account. Litner did not record this transaction before receiving the

statement.

e. A debit memorandum of $895 is enclosed with the bank statement for an NSF check

for $870 received from a customer. The bank assessed a $25 fee for processing it.

f. Litner’s April 30 daily cash receipts of $5,102 were placed in the bank’s night

depository on that date, but do not appear on the April 30 bank statement.

g. Litner’s April 30 cash disbursements journal indicates that Check No. 1837 for $584

and Check No. 1840 for $1,219 were both written and entered in the accounting

records, but are not among the canceled checks.

1) Prepare the bank reconciliation for this company as of April 30.

2) Prepare the journal entries necessary to bring the company’s book balance of cash

into conformity with the reconciled cash balance as of April 30.

A company had a beginning balance in retained earnings of $43,000. It had net income

of $6,000 and paid out cash dividends of $5,625 in the current period. The ending

balance in retained earnings equals:

A.$108,625.

B.$(12,625).

C.$11,375.

D.$43,375.

E.$(11,375).

Another name for equity is:

A.Net income.

B.Expenses.

C.Net assets.

D.Revenue.

E.Net loss.

Career opportunities in accounting include:

A.Budgeting.

B.Auditing.

C.Cost accounting.

D.Internal Auditing.

E.All of these.

Amounts received in advance from customers for future products or services:

A.Are revenues.

B.Increase income.

C.Are liabilities.

D.Are not allowed under GAAP.

E.Require an outlay of cash in the future.

Dresden, Inc., has four departments. Information about these departments follows:

If maintenance costs are allocated to the other departments based on floor space

occupied by each, the amount of maintenance cost allocated to the Cutting Department

is:

A.$ 2,769.

B.$ 3,000.

C.$ 3,724.

D.$ 6,000.

E.$18,000.

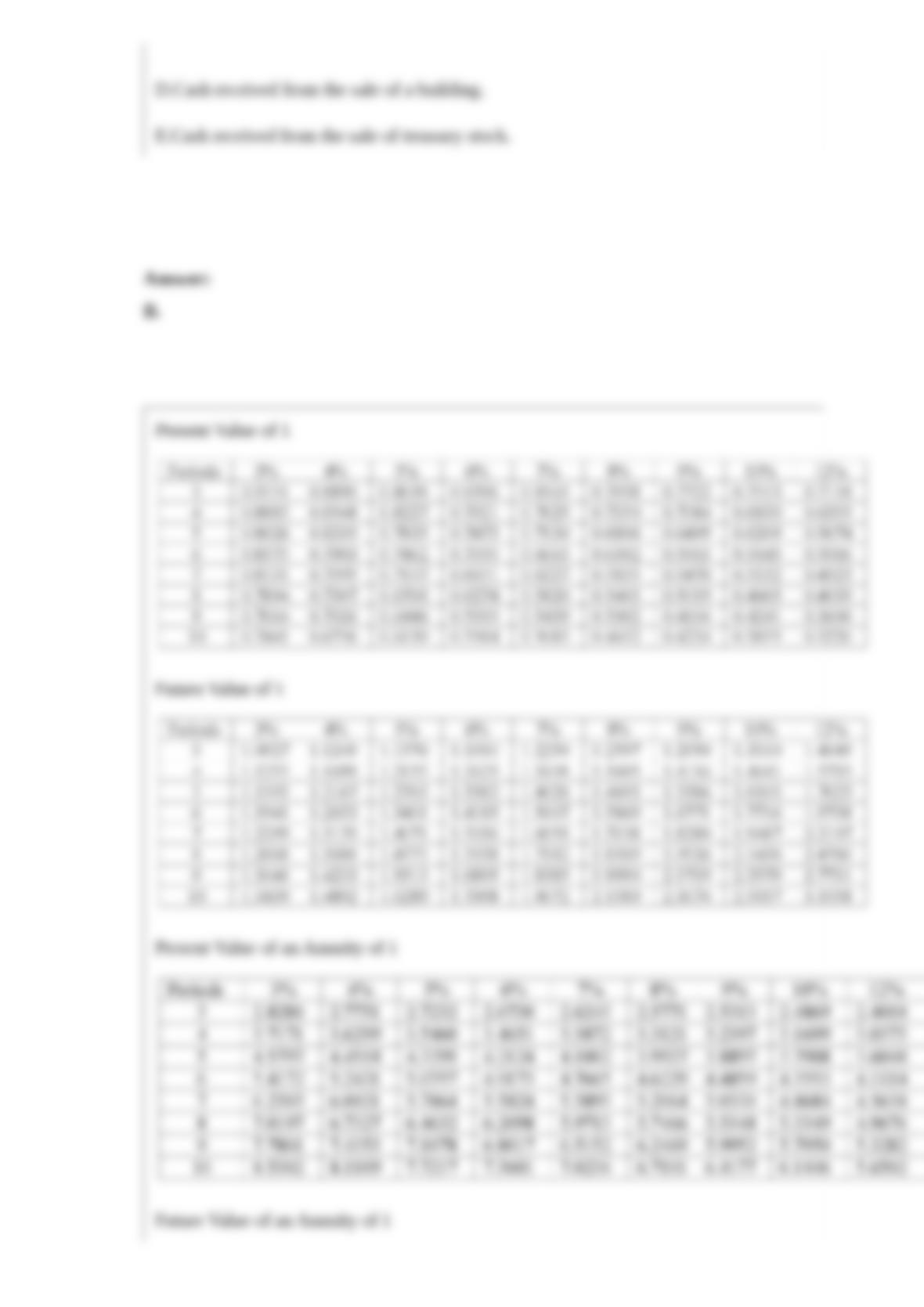

Which of the following transactions or events should be reported as a source of cash

from operating activities when using the direct method?

A.Credit sales.

B.Cash collections from customers.

C.Depreciation expense.

D.Cash received from the sale of a building.

E.Cash received from the sale of treasury stock.

Present Value of 1

Future Value of 1

Present Value of an Annuity of 1

Future Value of an Annuity of 1

What interest rate is required to accumulate $6,802.50 in four years from an investment

of $5,000?

A.5%.

B.8%.

C.10%.

D.12%.

E.15%.

An analysis that explains any differences between the checking account balance

according to the depositor’s records and the balance reported on the bank statement is

a(n):

A.Internal audit.

B.Bank reconciliation.

C.Bank audit.

D.Trial reconciliation.

E.Analysis of debits and credits.

If a company owns more than 20% of the stock of another company and the stock is

being held as a long-term investment, which method would the investor normally use to

account for this investment?

A.Equity method.

B.Market value method.

C.Historical cost method.

D.Straight-line method.

E.Effective method.

The straight-line depreciation method and the double-declining-balance depreciation

method:

A.Produce the same total depreciation over an asset’s useful life.

B.Produce the same depreciation expense each year.

C.Produce the same book value each year.

D.Are acceptable for tax purposes only.

E.Are the only acceptable methods of depreciation for financial reporting.

Preferred stock on which the right to receive dividends is forfeited for any year that the

dividends are not declared is referred to as:

A.Participating preferred stock.

B.Callable preferred stock.

C.Cumulative preferred stock.

D.Convertible preferred stock.

E.Noncumulative preferred stock.

Another title for goods in process inventory is:

A.Indirect materials inventory.

B.Work in process inventory.

C.Conversion costs.

D.Direct materials inventory.

E.Raw materials inventory.

A contingent liability:

A.Is always of a specific amount.

B.Is a potential obligation that depends on a future event arising from a past transaction

or event.

C.Is an obligation not requiring future payment.

D.Is an obligation arising from the purchase of goods or services on credit.

E.Is an obligation arising from a future event.

Rosser Company sold supplies in the amount of 25,000 euros to a French company

when the exchange rate was $1.21 per euro. At the time of payment, the exchange rate

decreased to $0.82. Rosser must record a:

A.gain of $9,750.

B.gain of $20,500.

C.loss of $9,750.

D.loss of $20,500.

E.neither a gain nor loss.

After posting is completed, there may be an error if:

A.The sum of the customer account balances does not equal the total in the sales

journal.

B.The sum of the accounts receivable ledger does not equal the balance in the Sales

account.

C.The sum of the customer account balances does not equal the general ledger

Accounts Receivable controlling account balance.

D.The balance in the sales journal does not equal the Accounts Receivable account

balance.

E.The sum of the accounts receivable ledger does not equal the balance in the sales

journal.

A perpetual record of a raw materials item that records data on the quantity and cost of

units purchased, units issued for use in production, and units that remain in the raw

materials inventory, is called a(n):

A.Materials ledger card.

B.Materials requisition.

C.Purchase order.

D.Materials voucher.

E.Purchase ledger.

A company’s board of directors votes to declare a cash dividend of 75 per share. The

company has 15,000 shares authorized, 10,000 issued, and 9,500 shares outstanding.

The total amount of the cash dividend is:

A.$ 375.

B.$ 4,125.

C.$ 7,125.

D.$ 7,500.

E.$11,250.

A company had net sales and cost of goods sold of $752,000 and $543,000,

respectively. Its net income was $17,530. The company’s gross margin ratio equals:

A.18.9%

B.24.5%

C.27.8%

D.34.7%

E.35.2%

A company has a market value per share of $73.00. Its net income is $1,750,000 and the

weighted-average number of shares outstanding is 350,000. The company’s

price-earnings ratio equals:

A.20.9.

B.4.2.

C.14.6.

D.20.0.

E.6.8.

Achieving an increased return on common stock by paying dividends on preferred stock

at a rate that is less than the rate of return earned with the assets invested from the

preferred stock issuance is called:

A.Financial leverage.

B.Discount on stock.

C.Premium on stock.

D.Preemptive right.

E.Capital gain.

Interest is:

A.Time.

B.A borrower’s payment to the owner of an asset for its use.

C.The same as a savings account.

D.Always a liability.

E.Always an asset.

The buyer who purchases and takes ownership of another company’s accounts

receivable is called a:

A.Payer.

B.Pledgor.

C.Factor.

D.Payee.

E.Pledgee.

The accounting guideline that requires financial statement information to be supported

by independent, unbiased evidence other than someone’s belief or opinion is the:

A.Business entity principle.

B.Monetary unit principle.

C.Going-concern principle.

D.Cost principle.

E.Objectivity principle.

ParFour’s total liabilities are $130,000 and its equity is $340,000. Calculate the

company’s total assets.

A company had net sales of $230,000 for 2008 and $288,000 for 2009. The company’s

average total assets for 2008 were $150,000 and $180,000 for 2009. Calculate the total

asset turnover for each year and comment on the company’s efficiency in the use of its

assets.

Identify and discuss the key characteristics of partnerships. Also, identify other

organizations that possess the positive aspects of both partnerships and corporations.

_________ are beliefs that separate right from wrong.

Define the return on total assets and explain how it is used to measure a company’s

financial performance.

The difference between the flexible budget sales and the fixed budget sales is called the

__________________________ variance.

Explain the concept of the future value of an annuity.

What are the steps that must be completed before an invoice approval is complete and a

voucher prepared?

A company reported the following year-end information:

Required:

1) Explain the purpose of the acid-test ratio.

2) Calculate the acid-test ratio for this company.

3) What does the acid-test ratio reveal about this company?