The adjusted trial balance contains only permanent accounts.

The tax benefit of a net operating loss carried back two years represents a current

receivable for income tax to be refunded.

According to International Financial Reporting Standards, the costs to successfully

defend an intangible right normally are capitalized and amortized.

Income from continuing operations sometimes includes gains from nonoperating

activities.

The FASB’s due process invites various interested parties to indicate their opinions

about whether financial accounting standards should be changed.

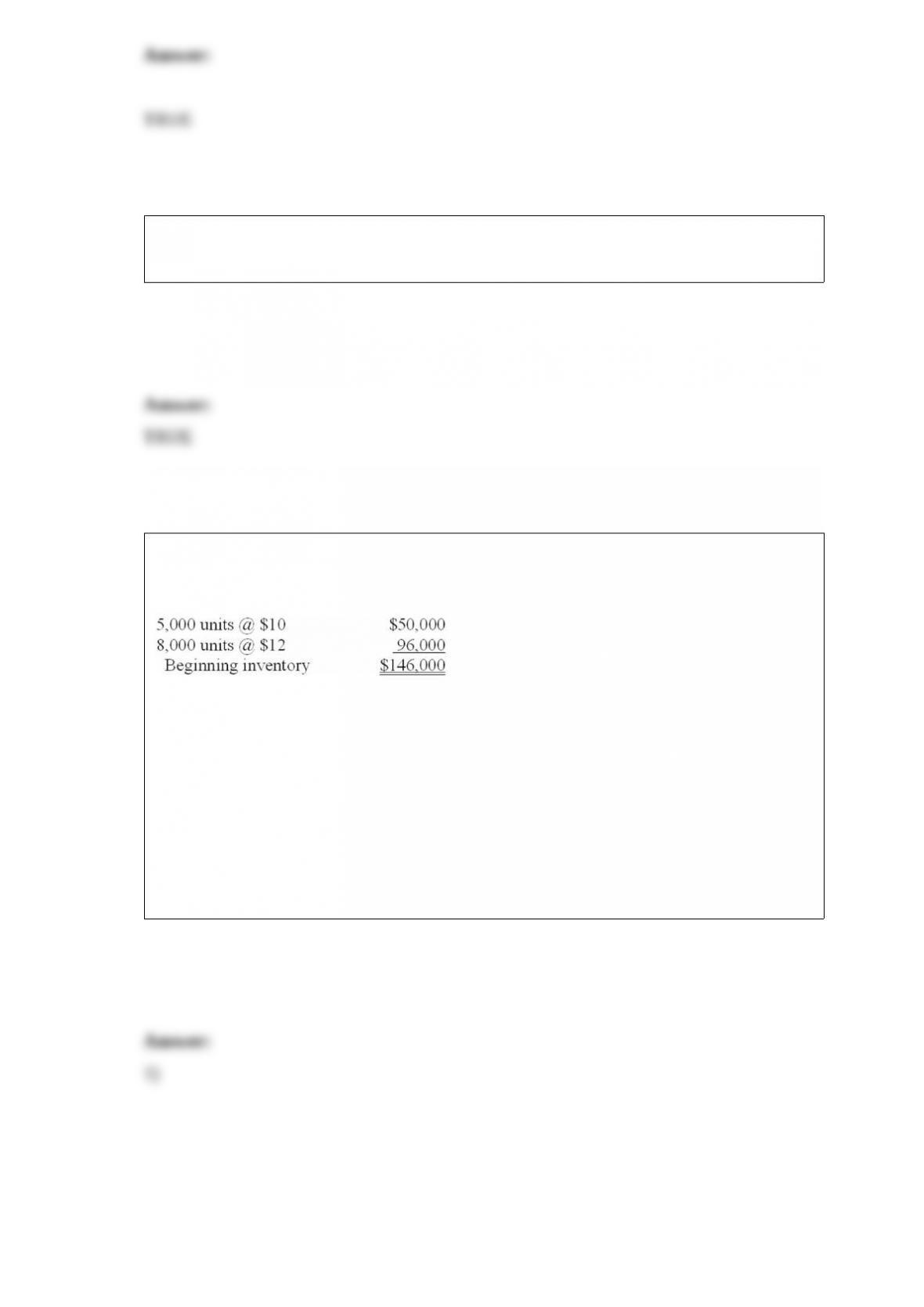

Bettencourt Clothing Corporation uses a periodic inventory system and the LIFO cost

method. The company began 2013 with the following inventory layers (listed in

chronological order of acquisition):

During 2013, 20,000 units were purchased for $15 per unit. Sales for the year totaled

30,000 units at various prices, leaving 3,000 units in ending inventory.

Required:

1) Calculate cost of goods sold for 2013.

2) Determine the amount of LIFO liquidation profit that the company must report in a

disclosure note to its 2013 financial statements, assuming the amount is material.

Assume an income tax rate of 40%.

Under the percentage-of-completion method, the percent complete is often estimated by

comparing the cost incurred to date with the total estimated cost to complete.

Unlike the Social Security tax there is no maximum wage base for the Medicare portion

of the FICA tax.

The definition of what constitutes an extraordinary item should be independent of the

operating environment.

The purpose of the conceptual framework is to provide a structure and framework for a

consistent set of GAAP.

The FASB is currently the public-sector organization responsible for setting accounting

standards in the United States.

Expenditures currently deducted in the tax return but not included with expenses in the

income statement until subsequent years create deferred tax liabilities.

Bonds will sell for a premium when the market rate of interest exceeds their stated rate.

Equity is a residual amount representing the owner’s interest in the assets of the

business.

If the seller is a principal, the seller typically is vulnerable to risks associated with

collecting payment from the customer.

The cost-to-retail percentage used in the retail method to approximate average cost

incorporates both markdowns and markups.

The balance sheet can be considered a change or flow statement.

Adjusting journal entries are required to comply with the realization and matching

principles.

Prior years’ financial statements are restated when the prospective approach is used.

According to the FASB’s Statements of Financial Accounting Concepts, conservatism is

a desired qualitative characteristic of accounting information.

Net purchases are reduced for discounts taken whether the net method is used or the

gross method is used.

The statement of shareholders’ equity discloses the changes in the temporary

shareholders’ equity accounts.

Initial franchise fees are always recognized on the date they are received.

Dividends in arrears on cumulative preferred stock are liabilities to be paid at a later

date.

The journal entry to record the replenishment of a petty cash fund includes a credit to

the petty cash fund.

A change to the LIFO method of valuing inventory usually requires use of the

retrospective method.

Over the life of a particular account receivable, the same total amount of gross profit is

recognized under the installment method and the cost recovery method.

When several types of potential common shares exist, the one that enters the

computation of diluted EPS first is the one with the: A. Highest incremental effect.

B. Higher numerator.

C. Median incremental effect.

D. Lowest incremental effect.

The journal entries for the _____________, ___________, and __________ approaches

under the proposed ASU correspond to those used for the held-to-maturity, trading

security, and available-for-sale approaches, respectively, in current GAAP. A. FV-NI,

FV-OCI, amortized cost

B. FV-OCI, amortized cost, FV-NI

C. Amortized cost, FV-NI, FV-OCI

D. The journal entries do not correspond.

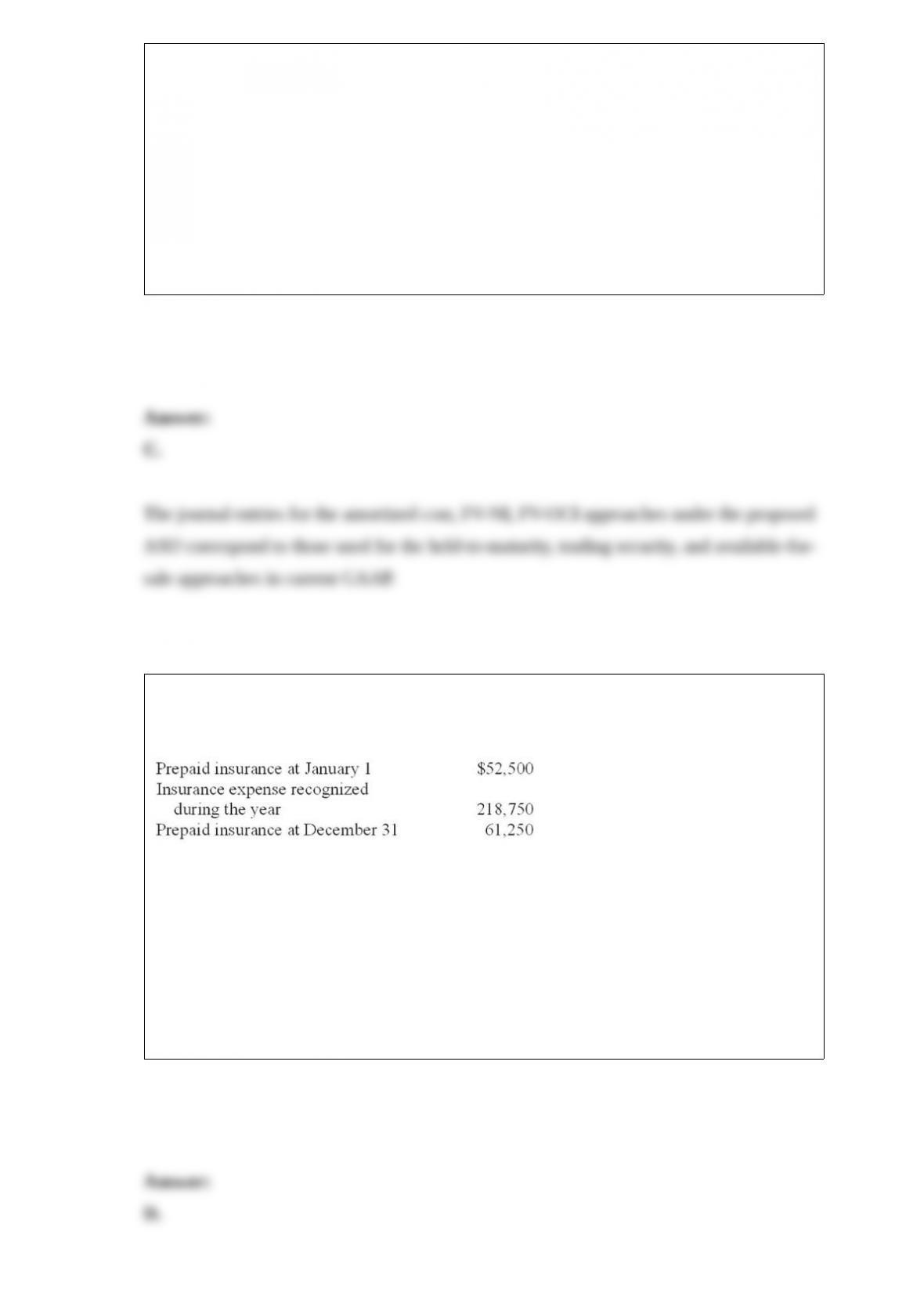

When Castle Corporation pays insurance premiums, the transaction is recorded as a

debit to prepaid insurance. Additional information for the year ended December 31 is as

follows:

What was the total amount cash paid by Castle for insurance premiums during the year?

A. $218,750

B. $166,250

C. $210,000

D. $227,500

Amortizing a net loss for pensions will: A. Increase retained earnings and increase

accumulated other comprehensive income.

B. Decrease retained earnings and decrease accumulated other comprehensive income.

C. Increase retained earnings and decrease accumulated other comprehensive income.

D. Decrease retained earnings and increase accumulated other comprehensive income.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Normal profit margin

2)Retail inventory method

3)Markdown cancellation

4)Markup on cost

5)Gross profit ratio

A. Ideal for high volume, low cost inventory

B. Elimination of a price reduction

C. Gross profit percentage times selling price

D. Gross profit divided by cost

E. Gross profit divided by sales.

The revenue/expense approach emphasizes: A.Recognition of revenues (typically

applying the realization principle).

B.Recognition of expenses (typically applying the matching principle).

C.The income statement.

D.All of the above are correct.

Accounting for costs of incentive programs for customer purchases: A. Requires

probability estimation.

B. Follows the matching principle.

C. Is a loss contingency situation.

D. All of the above are correct.

Prior to 1993, postretirement benefits other than pensions generally were accounted for

on the: A. Accrual basis.

B. Cash basis.

C. Modified accrual basis.

D. Hybrid basis.

If the lessor retains title to leased property under the terms of the lease: A. The amount

to be recovered through periodic lease payments is reduced by the present value of the

residual amount.

B. The amount to be recovered through periodic lease payments is increased by the

present value of the residual amount.

C. The amount to be recovered will be the same as if there were no residual value.

D. The lessor will record a greater amount of depreciation due to the residual value.

Cinnamon Buns Co. (CBC) started 2013 with $52,000 of merchandise on hand. During

2013, $280,000 in merchandise was purchased on account with credit terms of 2/10,

n/30. All discounts were taken. Purchases were all made f.o.b. shipping point. CBC paid

freight charges of $9,000. Merchandise with an invoice amount of $4,000 was returned

for credit. Cost of goods sold for the year was $316,000. CBC uses a perpetual

inventory system

Cost of goods sold is given by: A. Beginning inventory – net purchases + ending

inventory.

B. Beginning inventory + accounts payable – net purchases.

C. Net purchases + ending inventory – beginning inventory.

D. Net Purchases + beginning inventory – ending inventory.

Collection of accounts receivable that previously have been written off results in an

increase in cash and an increase in: A. Accounts receivable.

B. Allowance for uncollectible accounts.

C. Bad debts expense.

D. Retained earnings.

Which of the following is not true about net operating cash flow? A.It is the difference

between cash receipts and cash disbursements from providing goods and services.

B.It is a measure used in accrual accounting and is recognized as the best predictor of

future operating cash flows.

C.Over short periods, it may not be indicative of long-run cash-generating ability.

D.It is easy to understand and all information required to measure it is factual.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the most correct term. 1) Loss-other

comprehensive income

2) Accumulated benefit obligation

3) Funded status

4) Interest cost

5) Pension Benefit Guaranty Corp

A. Future salary levels estimated to be higher than previously expected

B. Current pay levels implicitly assumed

C. Created by “ERISA” legislation

D. Difference between PBO and plan assets

E. Created only by the passage of time

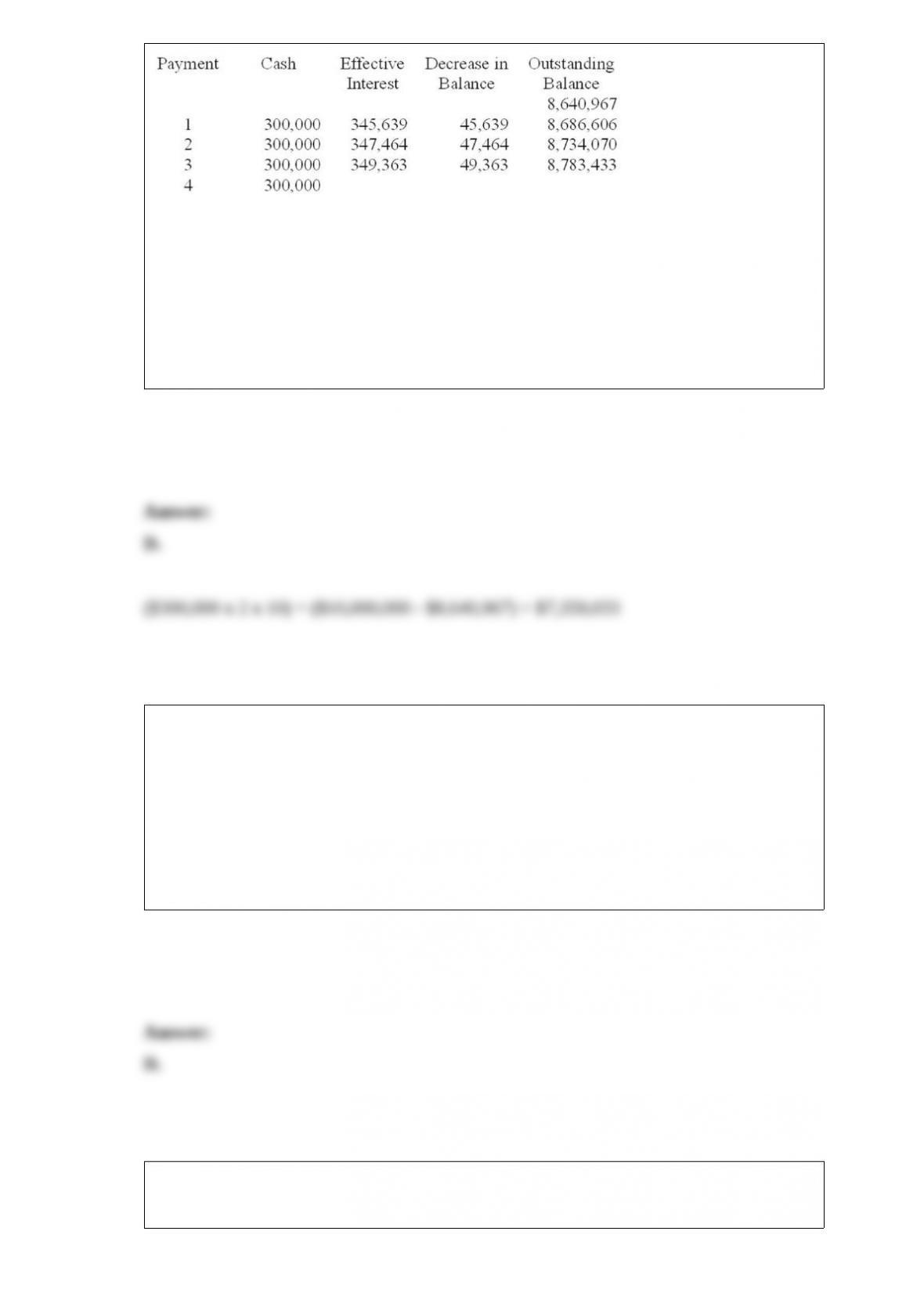

Discount-Mart issued ten thousand $1,000 bonds on January 1, 2013. The bonds have a

10-year term and pay interest semiannually. This is the partial bond amortization

schedule for the bonds.

What would be the total interest cost of the bonds over their full term? A. $1,359,033.

B. $4,640,967.

C. $6,000,000.

D. $7,359,033.

The usual difference between accounts payable and notes payable is: A. Legally

enforceable debt.

B. Current-noncurrent classification.

C. Known payment terms.

D. Explicitly stated interest.

JRE2 Inc. entered into a contract to install a pipeline for a fixed price of $2,200,000.

JRE2 uses the completed contract method of revenue recognition.

In 2014, JRE2 would report (rounded to the nearest thousand) gross profit (loss) of: A.

$(100,000).

B. $50,000.

C. $123,000.

D. $2,000.

Which of the following best demonstrates the full disclosure principle? A.The

multi-step income statement.

B.The auditors’ report.

C.The company’s tax return.

D.Disclosure notes to financial statements.

Branch Company, a building materials supplier, has $18,000,000 of notes payable due

April 12, 2014. At December 31, 2013, Branch signed an agreement with First Bank to

borrow up to $18,000,000 to refinance the notes on a long-term basis. The agreement

specified that borrowings would not exceed 75% of the value of the collateral that

Branch provided. At the date of issue of the December 31, 2013, financial statements,

the value of Branch’s collateral was $20,000,000. On its December 31, 2013, balance

sheet, Branch should classify the notes as follows: A. $15,000,000 long-term and

$3,000,000 current liabilities.

B. $4,500,000 short-term and $13,500,000 current liabilities.

C. $18,000,000 of current liabilities.

D. $18,000,000 of long-term liabilities.

Lite Travel Company’s accounting records include the following information:

What is the amount of net cash provided by operating activities indicated by the

amounts provided? A. $50,000.

B. $73,000.

C. $94,000.

D. $129,000.

A customer of Razor Sharpeners alleges that Razor’s new razor sharpener had a defect

that resulted in serious injury to the customer. Razor believes the customer has a 51%

chance of winning the case, and that if the customer wins the case, there is a range of

losses of between $1,000,000 and $3,000,000 in which any number is equally likely to

occur. Under IFRS, Razor should accrue a liability in the amount of: A. $0.

B. $1,000,000.

C. $2,000,000.

D. $3,000,000.

Which one of the following assumptions is needed to estimate both postretirement

health care benefits and pension benefits? A. Per capita claims cost.

B. Expected cost trend rate.

C. Benefits provided by other governmental or private plans.

D. Employee turnover.

Assets acquired in a lump-sum purchase are valued based on: A. Their assessed

valuation.

B. Their relative fair values.

C. The present value of their future cash flows.

D. Their cost plus the difference between their cost and fair values.

Two independent situations are described below. Each involves future deductible

amounts and/or future taxable amounts produced by temporary differences:

The enacted tax rate is 40% for both situations.

Required:

For each situation determine the:

(a.) Income tax payable currently.

(b.) Deferred tax asset – balance at year-end.

(c.) Deferred tax asset change dr or (cr) for the year.

(d.) Deferred tax liability – balance at year-end.

(e.) Deferred tax liability change dr or (cr) for the year.

(f.) Income tax expense for the year.

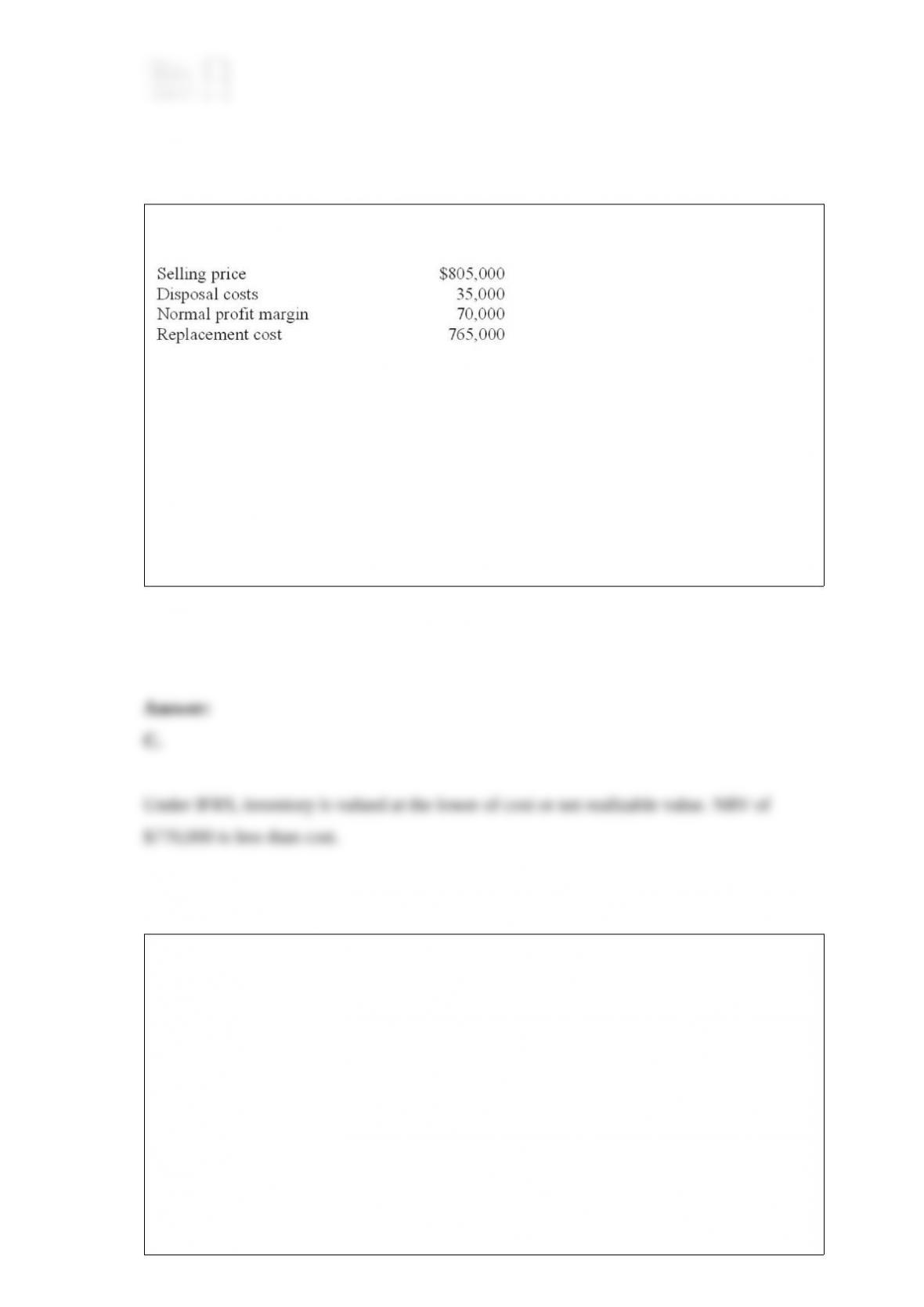

Haskell Corporation. has determined its year-end inventory on a FIFO basis to be

$785,000. Information pertaining to that inventory is as follows:

What should be the carrying value of Sullivan’s inventory if the company prepares its

financial statements according to International Financial Reporting Standards? A.

$765,000.

B. $785,000.

C. $770,000.

D. $700,000.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Sales returns

2)Write-off of accounts receivable

3)Accounts receivable

4)Separation of duties

5)Balance sheet approach

A. Has no effect on net receivables when using the allowance method

B. Is a contra revenue account

C. Is of vital importance for good internal control

D. Indirectly determines bad debt expense by estimating realizable value

E. Are reported at their net realizabl value

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Gains

2)Periodic system

3)Perpetual system

4)Prepayments

5)Losses

A. Requires adjusting entries to update the inventory account.

B. When cash flow precedes either expense or revenue recognition.

C. Requires entries to cost of goods sold account when merchandise is sold.

D. Recorded when there are dispositions of assets for consideration less than book

values.

E. Recorded when there are dispositions of assets for consideration in excess of book

values.

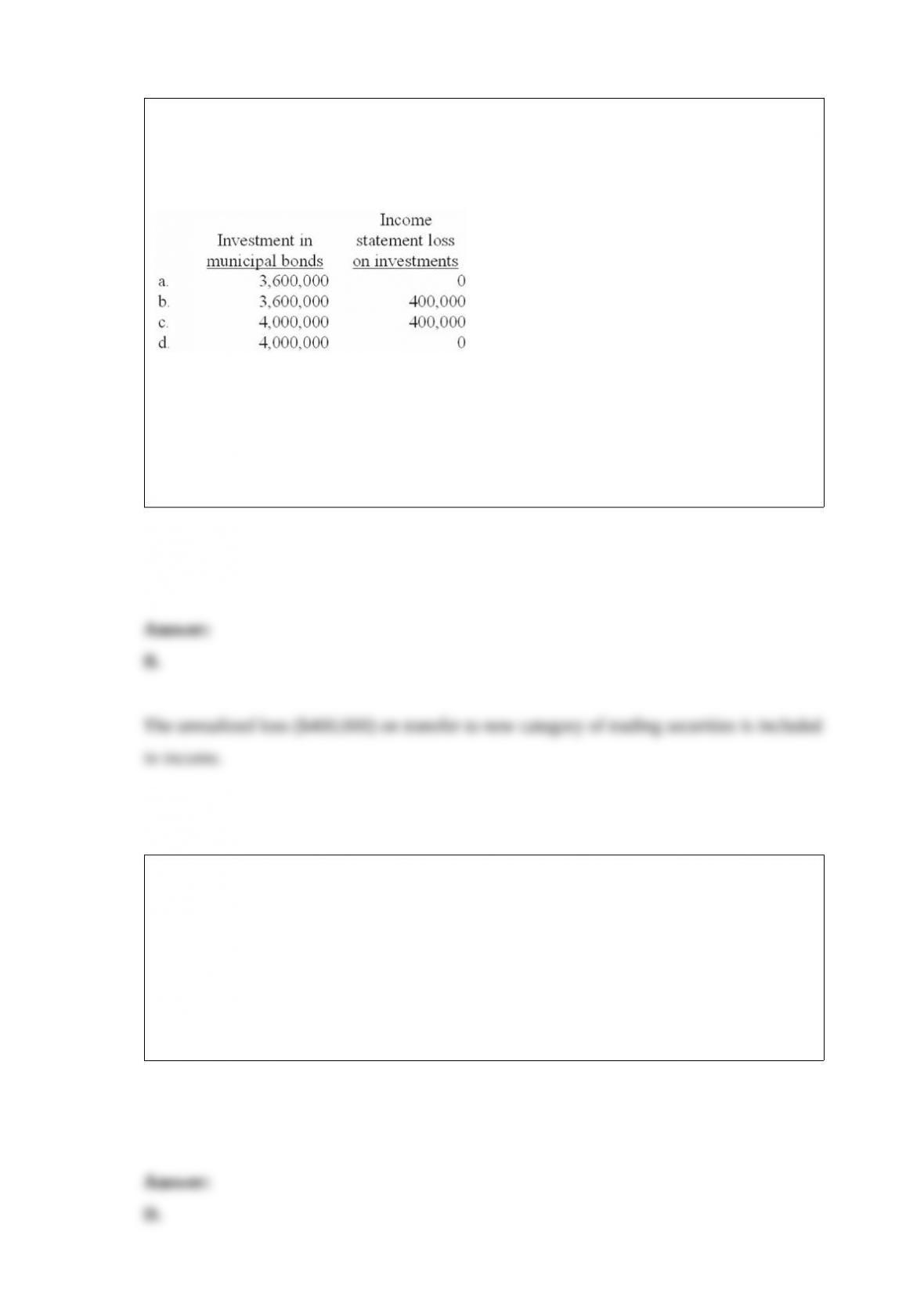

In 2011, Osgood Corporation purchased $4 million in 10-year municipal bonds at face

value. On December 31, 2013, the bonds had a market value of $3,600,000 and Osgood

reclassified the bonds from held to maturity to trading securities. Osgood’s December

31, 2013, balance sheet and the 2013 income statement would show the following:

A. Option a

B. Option b

C. Option c

D. Option d

Providing a monetary rebate program for purchasing a product: A. Is accounted for

similarly to product warranties.

B. Creates an expense for the seller in the period of sale.

C. Creates a contingent liability for the seller at the time of sale.

D. All of the above are correct.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct term. 1)Income from continuing

operations

2)Income from discontinued operations

3)Operating activities (income statement)

4)Change in accounting estimate

5)Matching principle

A. Is directly related to the principal revenue-generating activities.

B. Expenses are recognized in the same period as the related revenues.

C. More useful to analysts in predicting future income than current net income.

D. Income from an identifiable component will cease.

E. Requires note disclosure, if material.

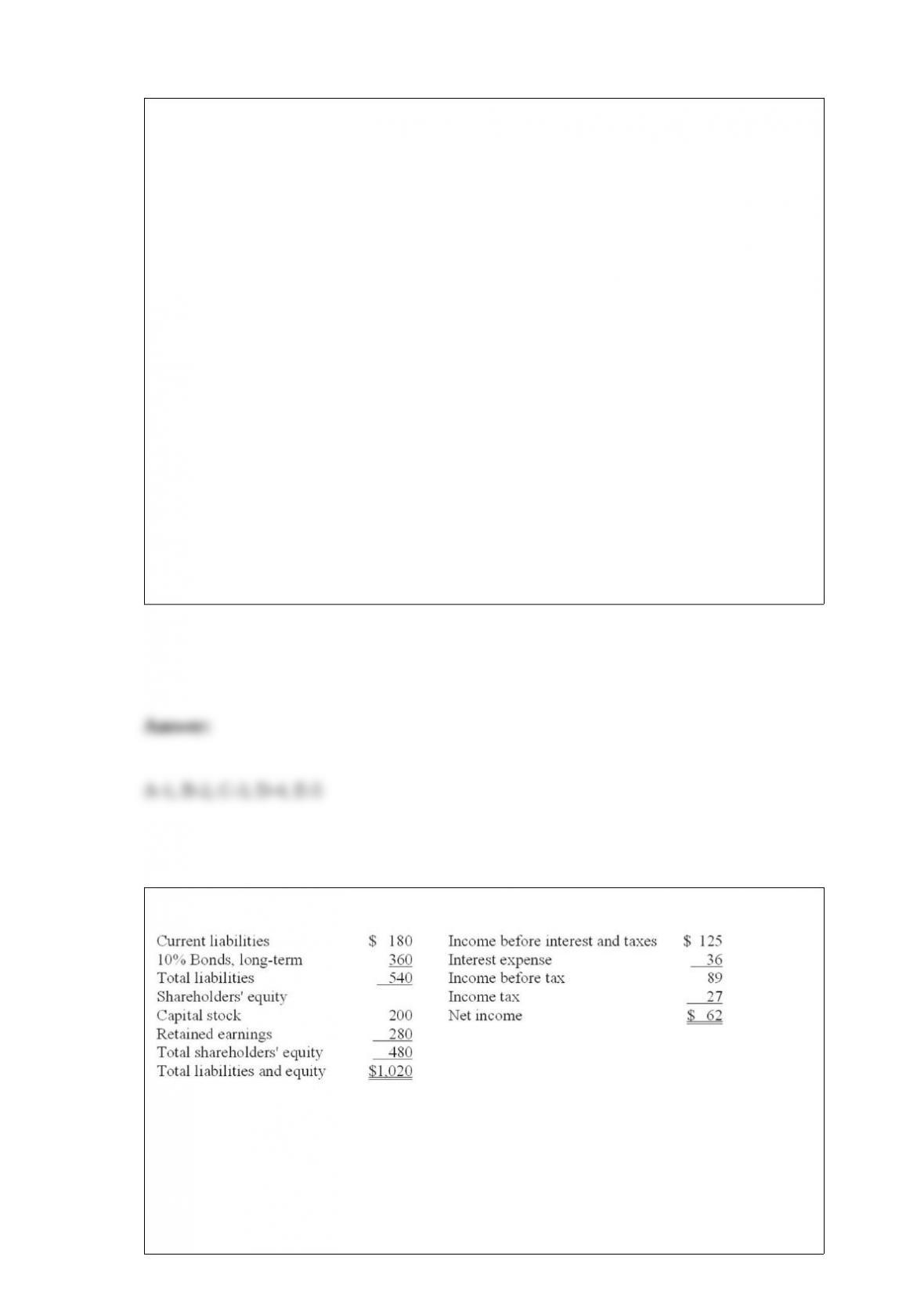

Recent financial statement data for Harmony Health Foods (HHF) Inc. is shown below.

HHF’s long-term debt to equity ratio equity is: A. 133.3%.

B. 75%.

C. 180%.

D. 0%.

When a company issues a stock dividend, which of the following would be affected? A.

Earnings per share.

B. Total assets.

C. Total liabilities.

D. Total shareholders’ equity.

Making insurance payments in advance is an example of: A. An accrued receivable

transaction.

B. An accrued liability transaction.

C. An unearned revenue transaction.

D. A prepaid expense transaction.

The following facts apply to TinyPart Toy Company’s pending litigation as of

December 31, 2013:

a. TinyPart is defending against a lawsuit and believes there is a 51% chance it will lose

in court. If it loses, TinyPart estimates that damages will be $100,000.

b. TinyPart is defending against another lawsuit for which management believes it is

virtually certain to lose in court. If it loses the lawsuit, management estimates damages

will fall somewhere in the range of $30,000 to $50,000, with each amount in that range

equally likely to occur.

c. TinyPart is defending against another lawsuit that is identical to item (b), but the

relevant losses will only occur far into the future. The present values of the endpoints of

the range are $15,000 and $25,000. TinyPart’s management believes the effects of time

value of money on these amounts are material, but also believes the timing of these

amounts is uncertain.

d. TinyPart is defending against a fourth lawsuit and believes there is only a 25%

chance it will lose in court. If TinyPart loses, it believes damages will fall somewhere in

the range of $35,000 to $40,000, with each amount in that range equally likely to occur.

Indicate how TinyPart would disclose or account for the lawsuit described in part (d)

under U.S. GAAP and under IFRS in the financial statements for the year ended

December 31, 2013.

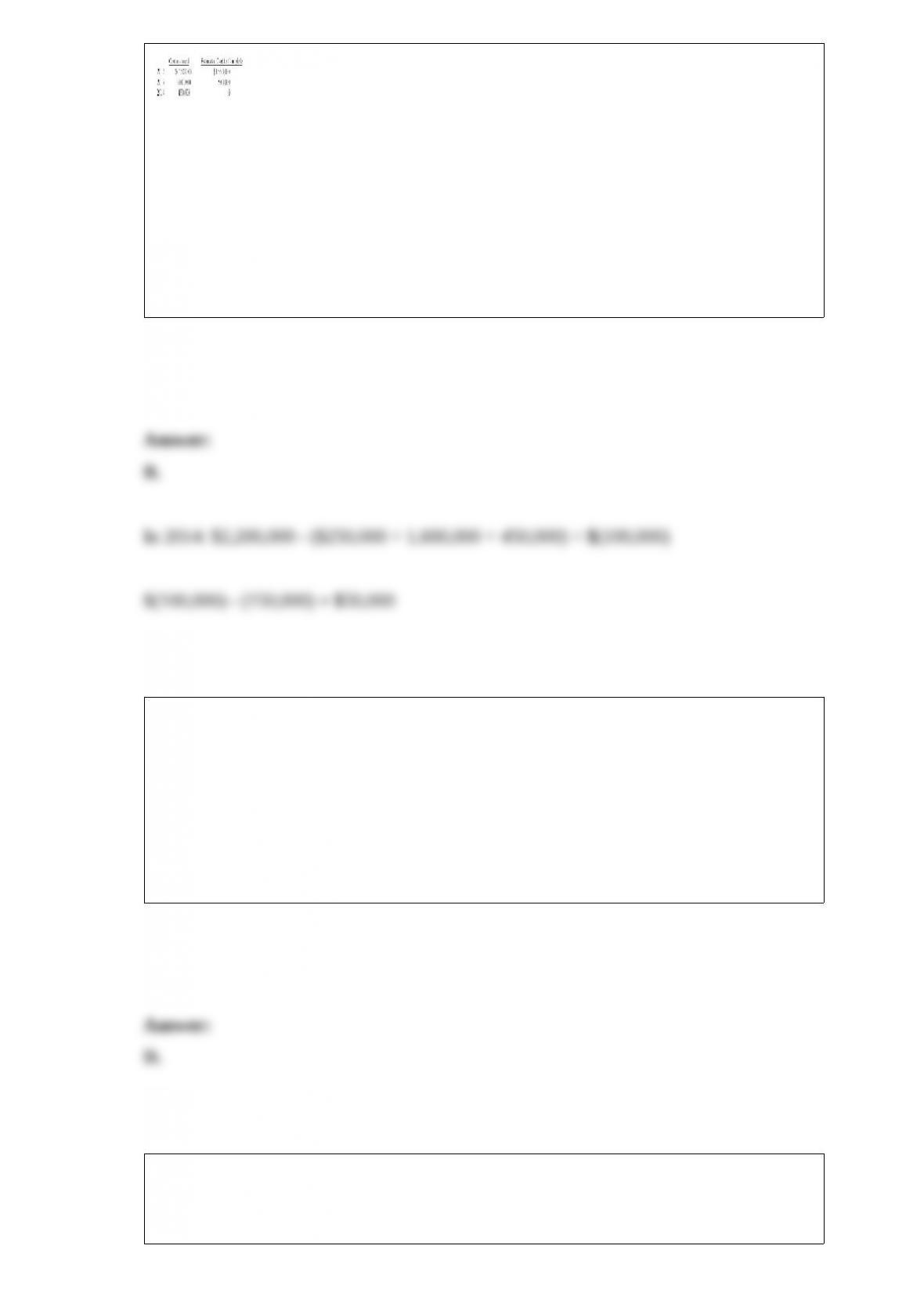

On January 1, 2013, Badger Inc. adopted the dollar-value LIFO method. The inventory

cost on this date was $100,000. The 2013 ending inventory, valued at year-end costs,

was $126,000. The relative cost index for this inventory in 2013 was 1.05.

Suppose that Badger’s 2015 ending inventory, valued at year-end costs, was $153,600

and that the relative cost index for this inventory in 2015 was 1.20. What inventory

balance would Badger report on its 12/31/15 balance sheet? A. $128,000.

B. $129,800.

C. $153,600.

D. None of the above is correct.

On January 1, 2013, Jeans-R-Us Company awarded 15 million of its $1 par common

shares to key personnel, subject to forfeiture if employment is terminated within three

years. On the date of the grant, the stock had a market price of $3 per share.

Required:

(1) Determine the total compensation cost pertaining to the restricted shares.

(2) Prepare the appropriate journal entry to record the award on January 1, 2013.

(3) Prepare the appropriate journal entry to record compensation expense on December

31, 2013.

(4) Prepare the appropriate journal entry to record compensation expense on December

31, 2014.

(5) Prepare the appropriate journal entry to record compensation expense on December

31, 2015.

(6) Prepare the appropriate journal entry to record the lifting of restrictions on

December 31, 2015.

On February 1, 2013, Sanford & Son issued 10% bonds dated February 1, 2013, with a

face amount of $200,000. The bonds sold for $239,588 and mature in 20 years. The

effective interest rate for these bonds was 8%. Interest is paid semiannually on July 31

and January 31. Sanford & Son’s fiscal year is the calendar year.

Required:

1) Prepare the journal entry to record the bond issuance on February 1,

2) Prepare the entry to record interest on July 31, 2013, using the straight-line method.

3) Prepare the necessary journal entry on December 31, 2013.

4) Prepare the necessary journal entry on January 31, 2014.

IFRS No. 9 is a standard that indicates accounting for investments when the investor

does not have significant influence under the investee.

Required:

Explain how debt investments are accounted for under IFRS No. 9. What alternative

accounting approaches are available, what determines whether an investment qualifies

for each approach, and what are the key features of each approach with respect to

accounting for unrealized gains and losses?

Describe in detail the way companies report most voluntary changes in accounting

principle.

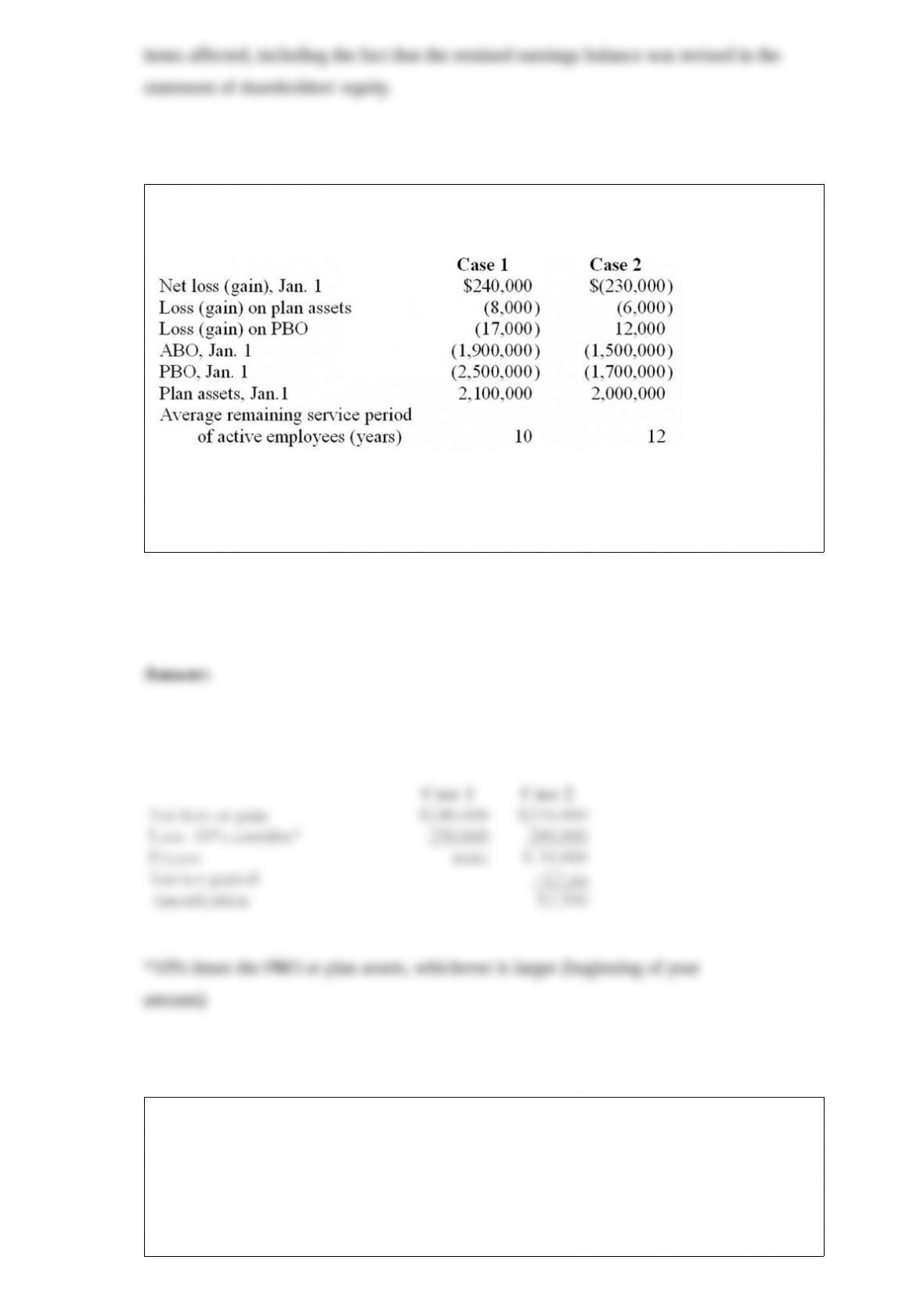

Vrable Corporation has a defined benefit pension plan. Two alternative possibilities for

pension-related data for the current calendar year are shown below:

Required:

For each independent case, calculate amortization of the net loss or gain that should be

included as a component of pension expense for the current year.

Hart Corporation has an unfunded postretirement health care benefit plan. Life

insurance and medical care benefits are provided to employees who render 12 years of

service and attain age 55 while in service to the company. At the end of 2013, John

Sousa is 35. He was hired by Hart five years ago at age 30 and is expected to retire at

the age of The expected postretirement benefit obligation for John is $50,000 at the end

of 2013.

Required:

Calculate the accumulated postretirement benefit obligation at the end of 2013 and the

service cost for 2013 pertaining to John.

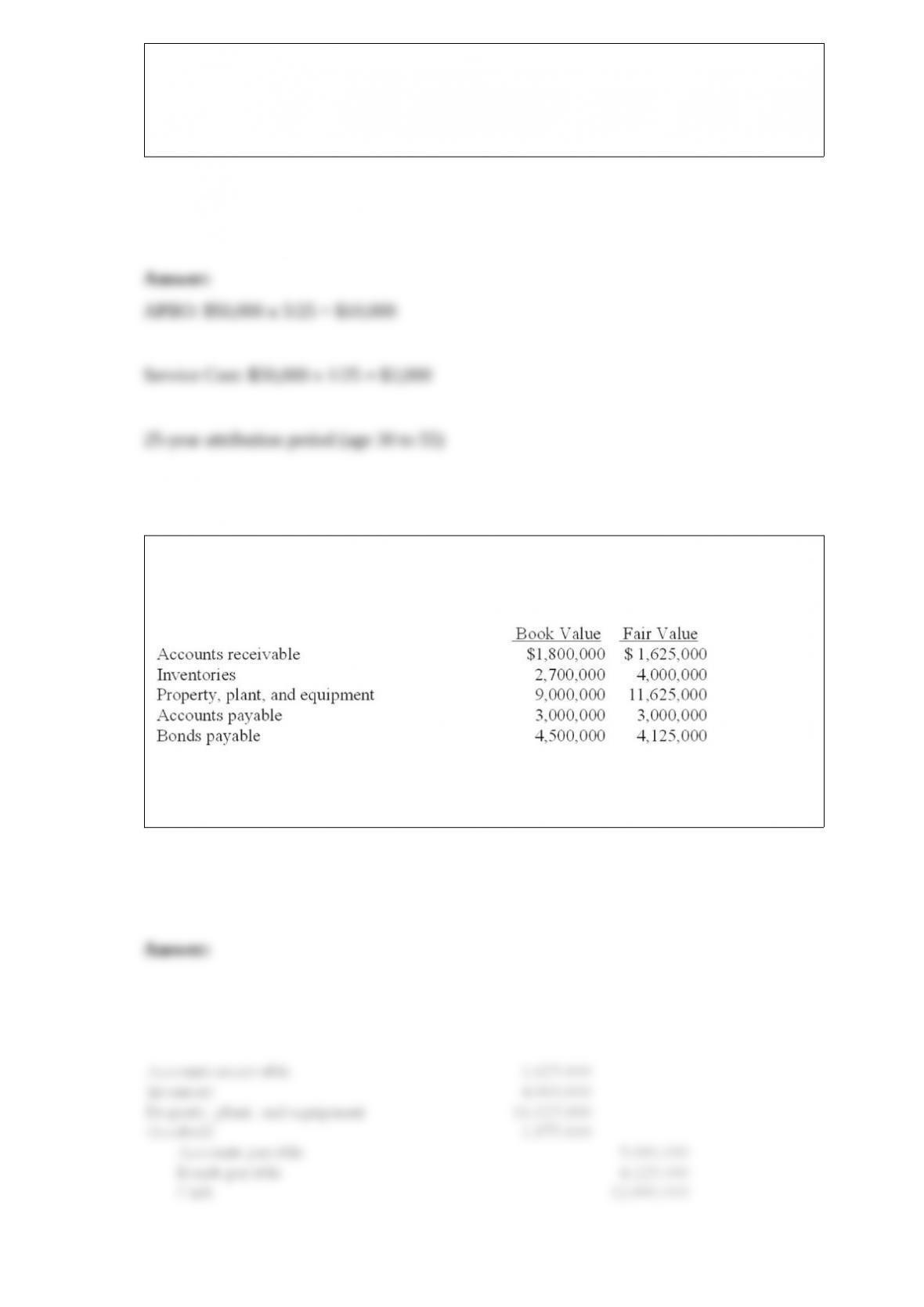

During the current year, Brewer Company acquired all of the outstanding common

stock of Miller Inc. paying $12,000,000 cash. The book values and fair values of

Miller’s assets and liabilities acquired are listed below:

Required:

Prepare the journal entry to record the acquisition by Brewer Company.

Parsley Corporation had 250,000 shares of common stock and 5,000 shares of 8%, $100

par, preferred stock outstanding on December 31, 2012. The preferred stock is

cumulative, nonconvertible preferred stock. On June 1, 2013, Parsley sold 36,000

shares of common stock for cash. No cash dividends were declared for 2013. Parsley

reported a net loss of $320,000 for the year ended December 31, 2010.

Required:

Calculate Parsley’s loss per share (rounded to 2 decimal places) for the year ended

December 31, 2013.

Cherokee Company’s auditor discovered some errors. No errors were corrected during

2012. The errors are described as follows:

(1) Beginning inventory on January 1, 2012, was understated by $5,000.

(2) A two-year insurance policy purchased on April 30, 2012, in the amount of $24,000

was debited to Prepaid Insurance. No adjustment was made on December 31, 2012, or

on December 31,

Required:

Prepare appropriate journal entries (assume the 2013 books have not been closed).

Ignore income taxes.

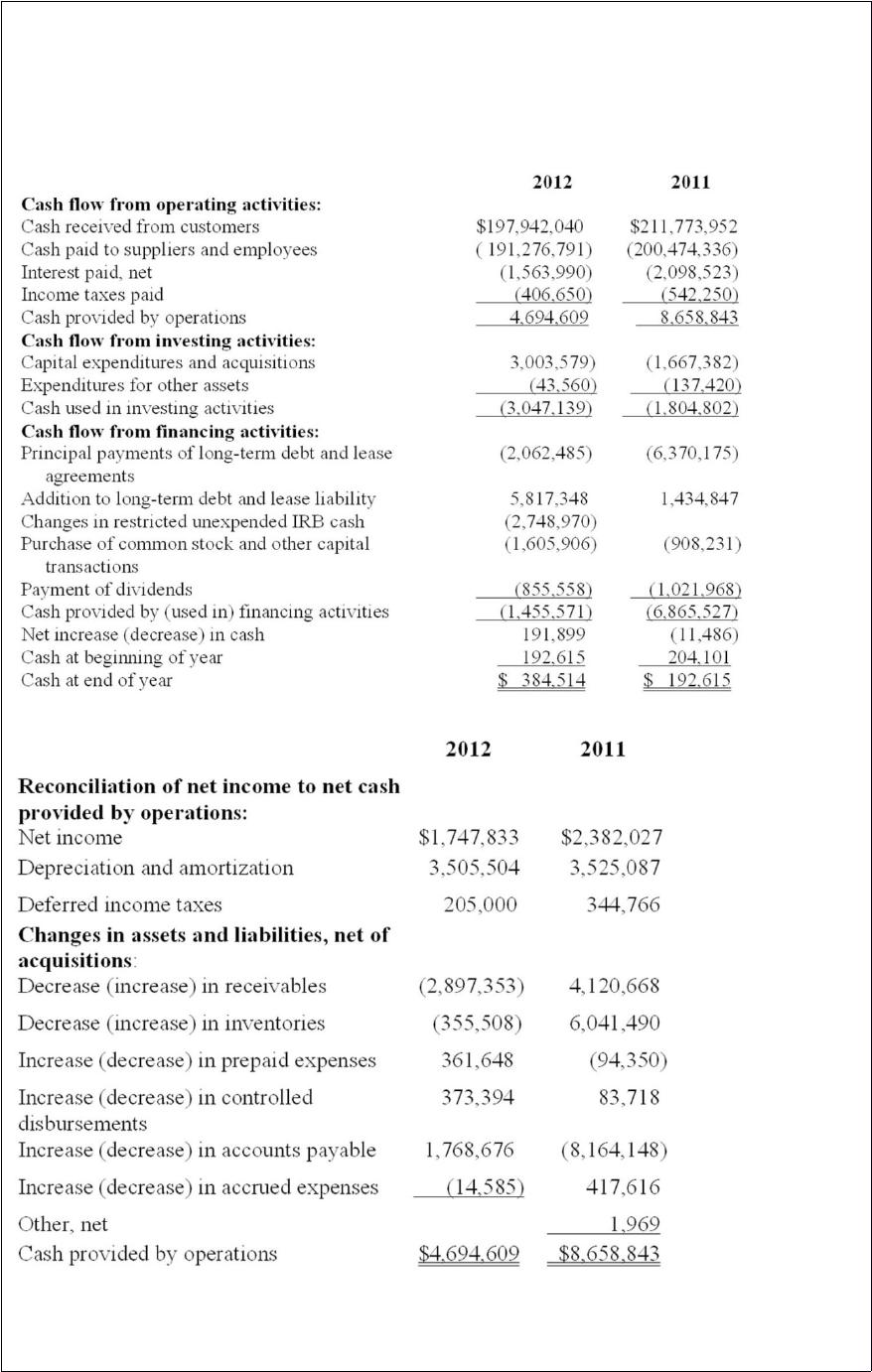

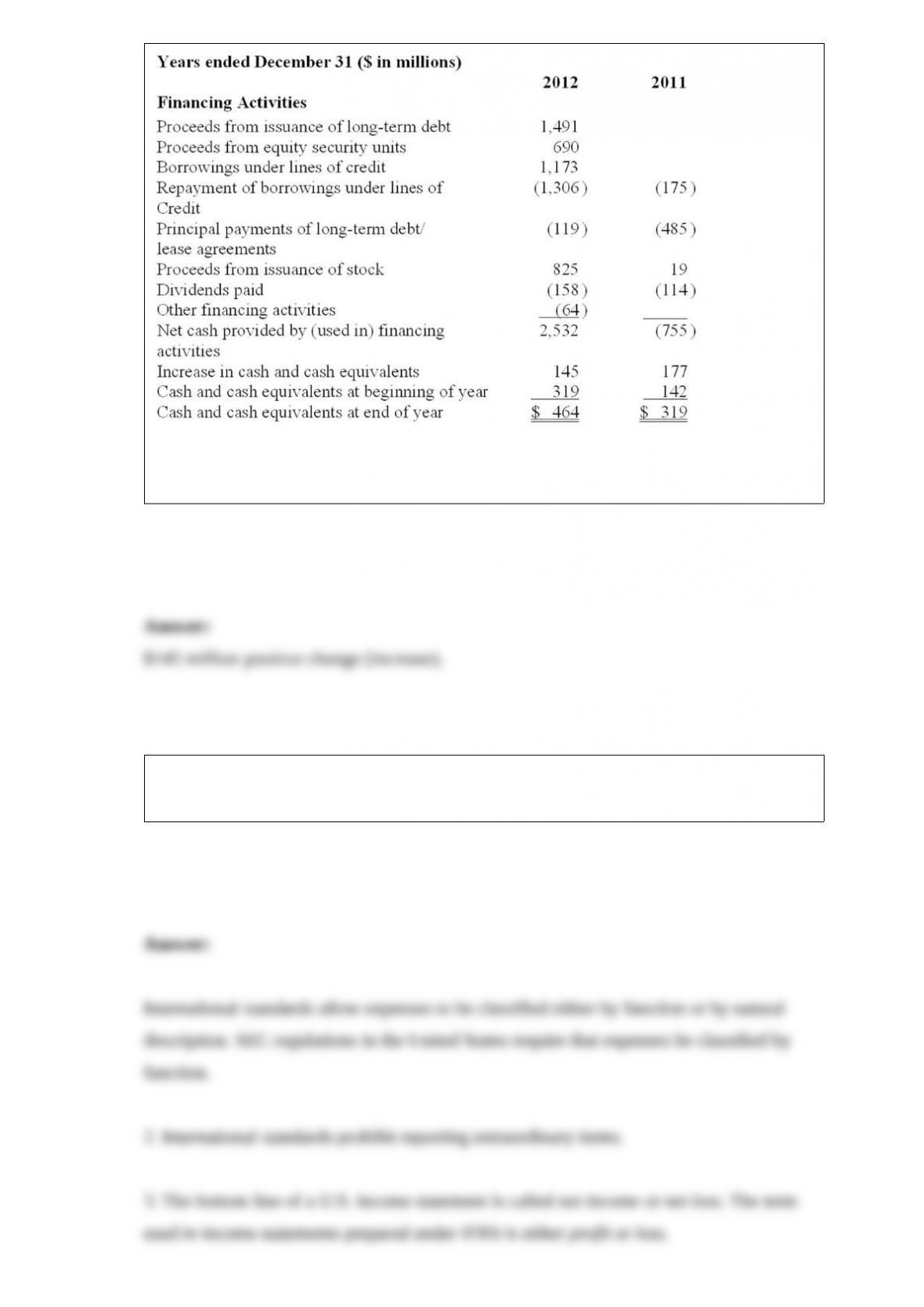

In its 2012 Annual Report to Shareholders, Kinney Inc. reported the following

Consolidated Statement of Cash Flows:

For the years ended December 31,

Kinney reported cost of goods sold of $168,114,150 in its fiscal 2012 income statement.

Compute its net inventory purchases during the year.

In its 2013 annual report to shareholders, Douglas-Roberts International Corporation

disclosed the following:

In 2013, the company entered into three sale-leaseback arrangements with various

financial institutions. Under the first arrangement, truck cab assembly machinery with a

net book value of $58 million was sold for $60 million and leased back under an

eight-year operating lease agreement. Under the second arrangement, tooling and

related engine manufacturing equipment with a net book value of $261 million was sold

for $260 million and leased back under an 11.5-year operating lease agreement. The

third arrangement consisted of additional engine manufacturing equipment with a net

book value of $62 million that was sold for $65 million and leased back under a 10-year

operating lease agreement. The gain on these transactions was deferred and is being

amortized over the terms of the lease agreements.

Discuss the most likely reasons for these three transactions, and explain the basis for the

last sentence of the disclosure.

On January 2, 2013, MBH Inc. acquired 30% of the voting common stock of

Construction Corporation as a long-term investment. Data from Construction

Corporation’s financial statements for the year ended December 31, 2013, include the

following:

Required:

Prepare any necessary journal entries for MBH at December 31, 2013, under the equity

method of accounting for investments.

If inventory is understated at the end of 2012 and the error is not discovered, how will

net income be affected in 2013?

Explain the appropriate accounting method used to account for lump-sum purchases of

a group of long-term assets.

In its 2012 Annual Report to Shareholders, Henchman & Co. provided the following

Statement of Cash Flows:

What was the net change in cash and cash equivalents experienced by Henchman & Co.

during 2012? Was it positive or negative?

Briefly discuss at least two differences between income statements prepared under U.S.

GAAP and IFRS.

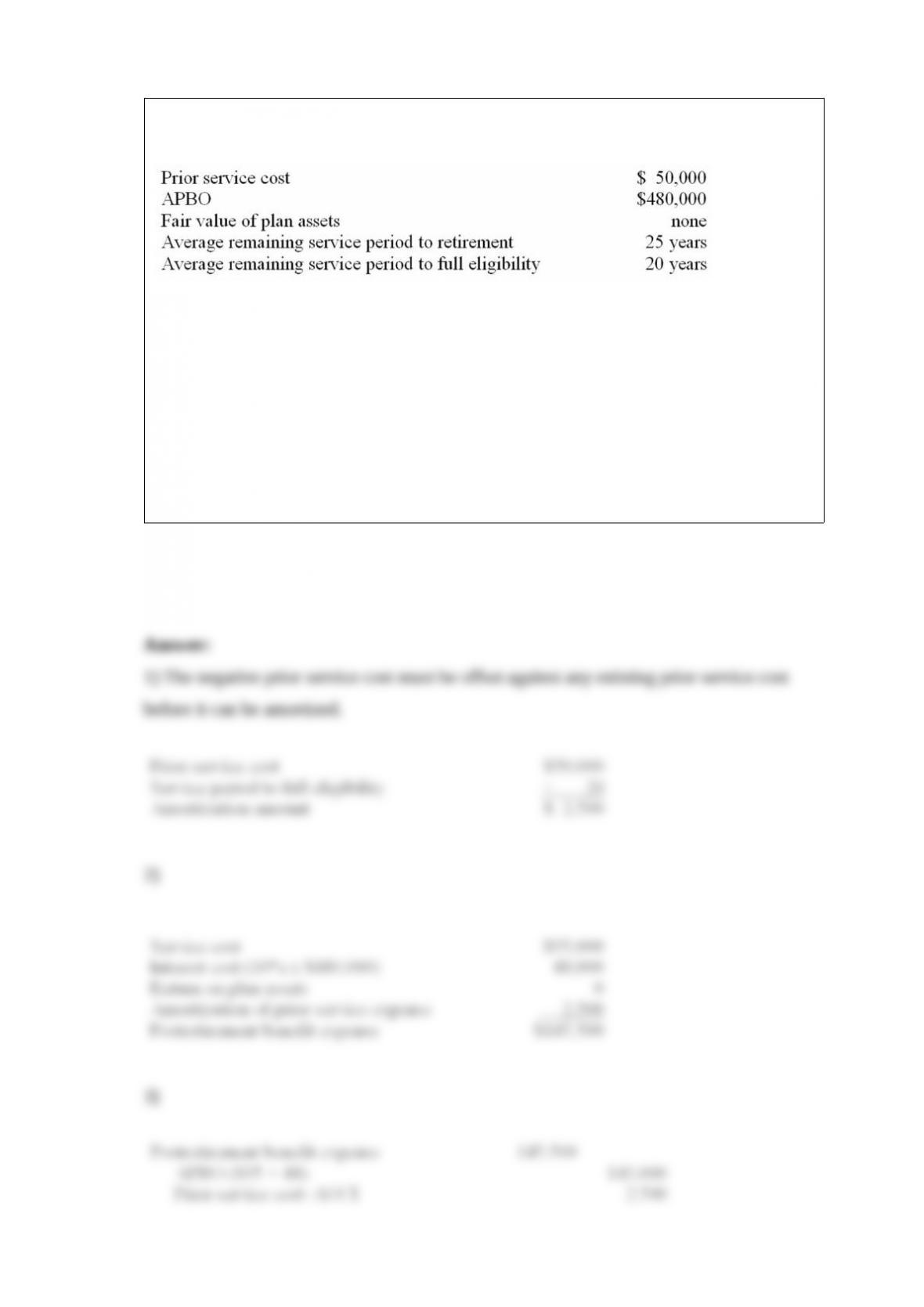

Brown Industries provides postretirement health care benefits to employees. On January

1 of the current calendar year, the following data were available.

Management amortizes prior service cost on a straight-line basis. The interest rate is

10%. Service cost for the current year is $95,000.

Required:

1) Calculate the prior service cost amortization for the current year.

2) Calculate the postretirement benefit expense for the current year.

3) Prepare the entry to record the postretirement benefit expense for the current year.

When an investor owns 20% to 50% of the voting stock of an investee company, the

investor is presumed to exercise significant influence over the investee unless there is

evidence to the contrary.

Required:

1) What factors could be evidence of significant influence?

2) What factors could be evidence of lack of significant influence?