1) At a volume of 8,000 units, Pwerson Company incurred $32,000 in factory overhead

costs, including $12,000 in fixed costs. If volume increases to 9,000 units and both

8,000 units and 9,000 units are within the relevant range, then the company would

expect to incur total factory overhead costs of:

A) $22,500

B) $32,000

C) $34,500

D) $20,000

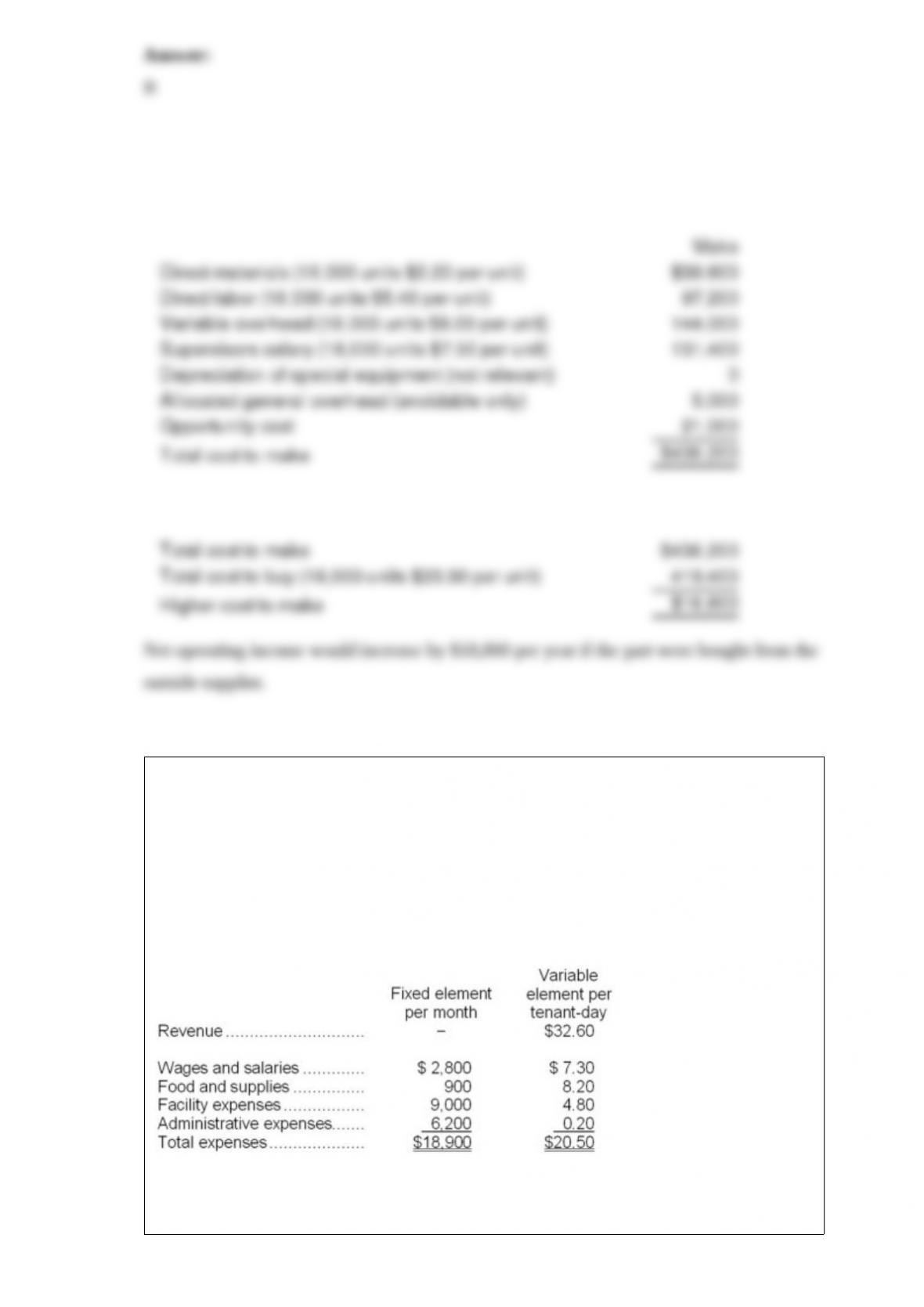

2) Ramon Corporation makes 18,000 units of part E44 each year. This part is used in

one of the company’s products. The company’s Accounting Department reports the

following costs of producing the part at this level of activity:

An outside supplier has offered to make and sell the part to the company for $23.30

each. If this offer is accepted, the supervisor’s salary and all of the variable costs,

including direct labor, can be avoided. The special equipment used to make the part was

purchased many years ago and has no salvage value or other use. The allocated general

overhead represents fixed costs of the entire company. If the outside supplier’s offer

were accepted, only $5,000 of these allocated general overhead costs would be avoided.

In addition, the space used to produce part E44 would be used to make more of one of

the company’s other products, generating an additional segment margin of $21,000 per

year for that product.

What would be the impact on the company’s overall net operating income of buying

part E44 from the outside supplier?

A) Net operating income would increase by $21,000 per year.

B) Net operating income would increase by $18,800 per year.

C) Net operating income would decrease by $123,000 per year.

D) Net operating income would decrease by $165,000 per year.

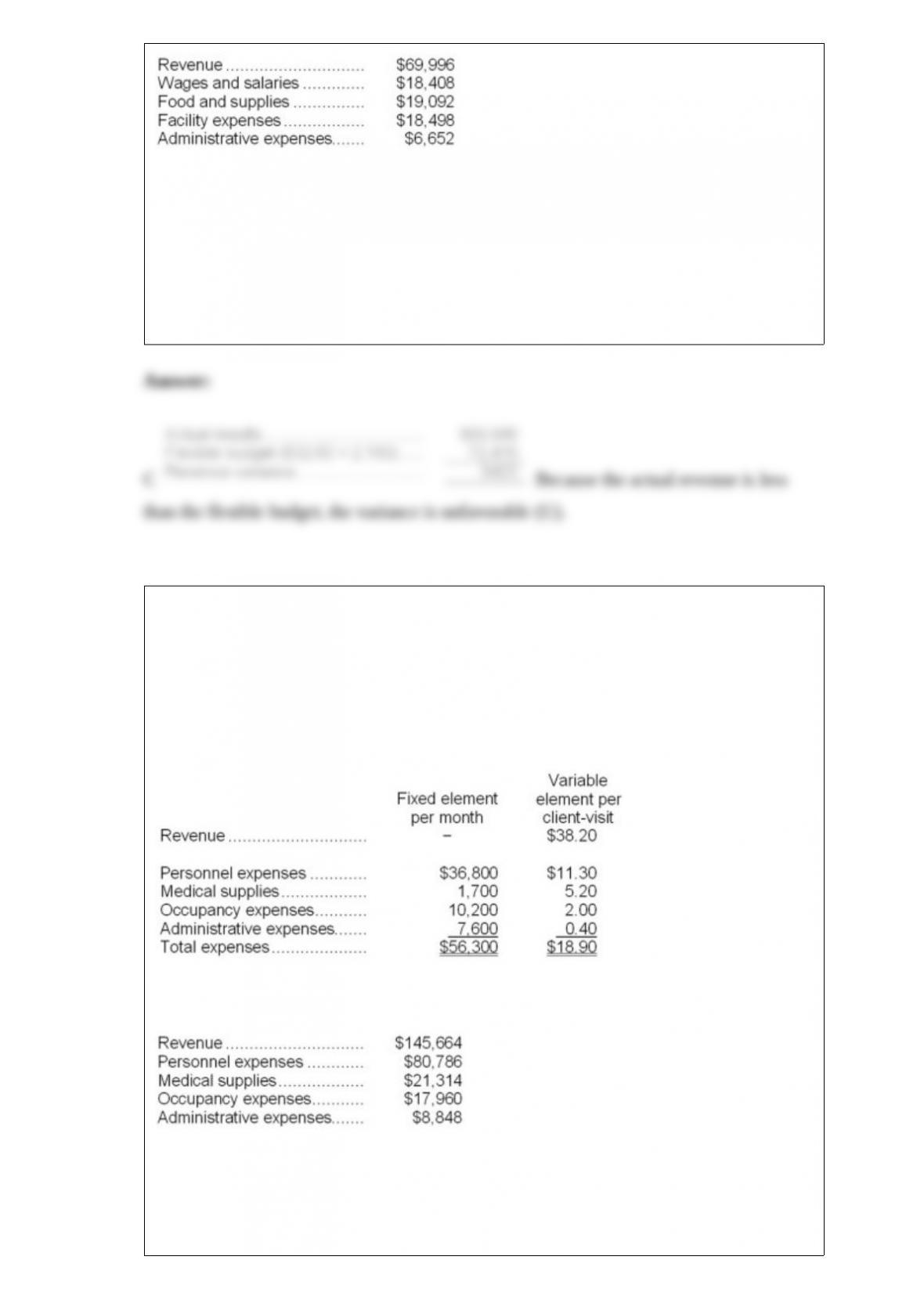

3) Perla Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During March, the kennel budgeted for

2,200 tenant-days, but its actual level of activity was 2,160 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for March:

Data used in budgeting:

Actual results for March:

The revenue variance for March would be closest to:

A.$420 F

B.$1,724 F

C.$420 U

D.$1,724 U

4) Lantagne Clinic uses client-visits as its measure of activity. During May, the clinic

budgeted for 3,800 client-visits, but its actual level of activity was 3,820 client-visits.

The clinic has provided the following data concerning the formulas used in its

budgeting and its actual results for May:

Data used in budgeting:

Actual results for May:

The net operating income in the flexible budget for May would be closest to:

A.$16,668

B.$17,426

C.$16,844

D.$17,040

5) In a statement of cash flows, a change in an income taxes payable account would be

recorded in the:

A.operating activities section.

B.financing activities section.

C.investing activities section.

D.stockholders’ equity section.

6) Johnston Corporation manufactures a single product that it sells for $30 per unit. The

company has the following cost structure:

Last year there was no beginning inventory. During the year, 20,000 units were

produced and 17,000 units were sold.

Under absorption costing, the unit product cost would be:

A.$20 per unit

B.$12 per unit

C.$13 per unit

D.$8 per unit

7) If salespersons are paid commissions that are a set percentage of sales, which product

would they prefer to sell? In other words, if it is a choice between selling one unit of

one product and one unit of another, which product would they prefer to sell?

A.I100

B.I200

C.I300

D.I400

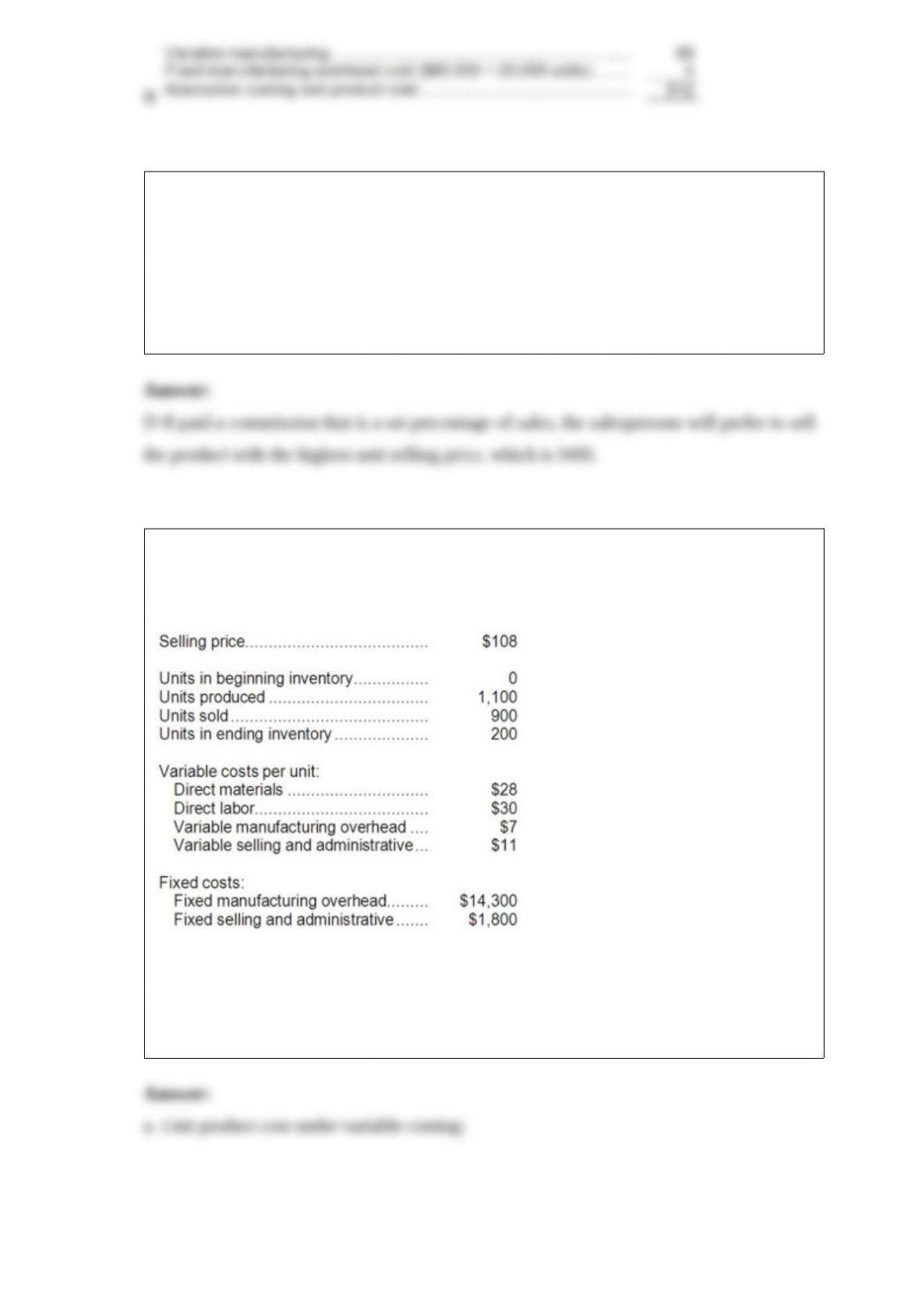

8) Oakes Corporation, which has only one product, has provided the following data

concerning its most recent month of operations:

Required:

a. Prepare a contribution format income statement for the month using variable costing.

b. Prepare an income statement for the month using absorption costing.

9) What would be the total internal failure cost appearing on the quality cost report?

A.$127,000

B.$217,000

C.$85,000

D.$146,000

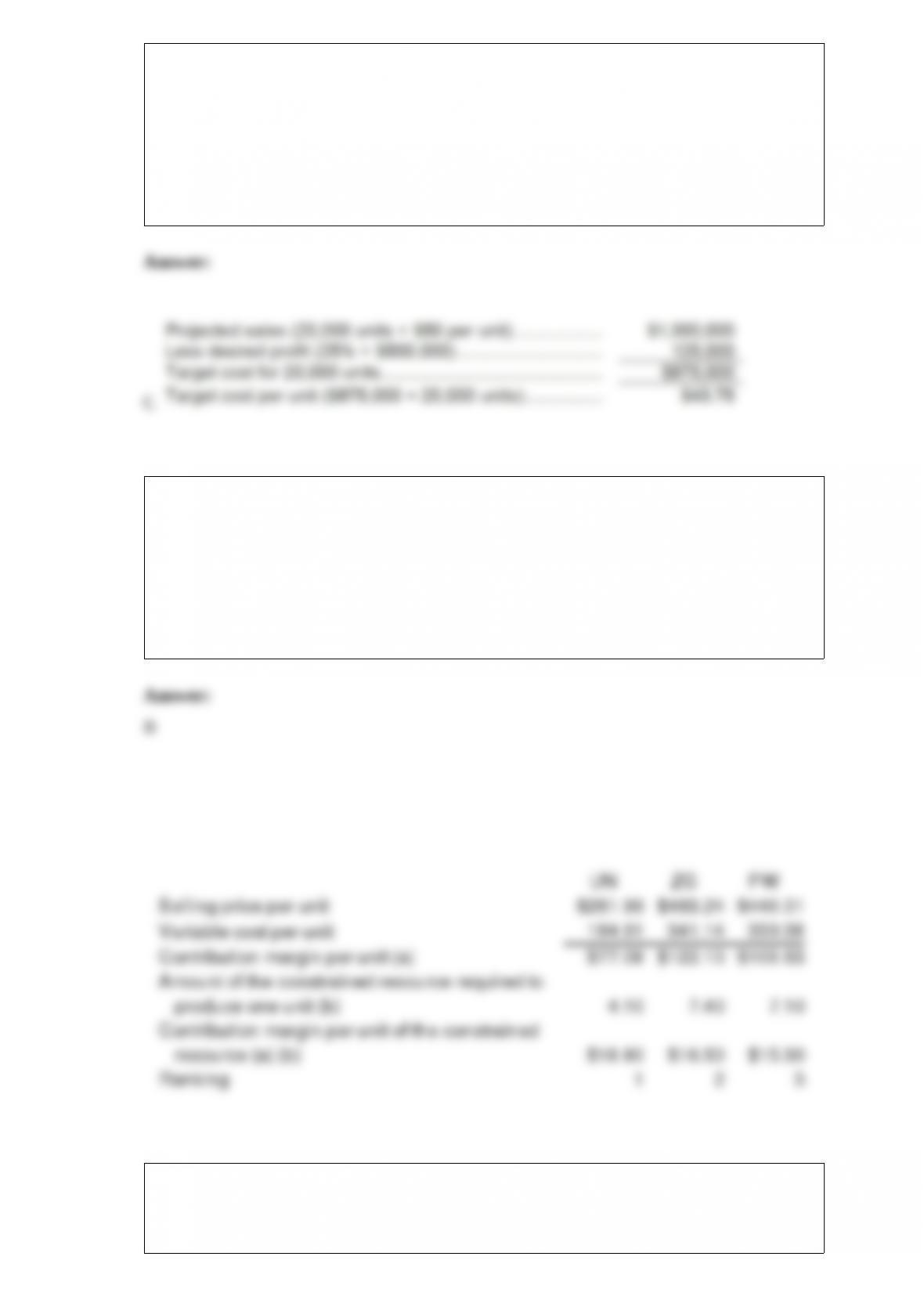

10) Timax Corporation, a manufacturer of moderate-priced time pieces, would like to

introduce a new electronic watch. To compete effectively, the watch could not be priced

at more than $50. The company requires a return on investment of 25% on all new

products. The plan is to produce and sell 20,000 watches each year. This would require

a $500,000 investment. The target cost per watch would be:

A.$64.00

B.$25.00

C.$43.75

D.$39.00

11) Rank the products in order of their current profitability from most profitable to least

profitable. In other words, rank the products in the order in which they should be

emphasized.

A) PW,UN,ZG

B) UN,ZG,PW

C) ZG,PW,UN

D) UN,PW,ZG

12) The product’s price elasticity of demand as defined in the text is closest to:

A.-3.19

B.-2.02

C.-2.70

D.-4.13

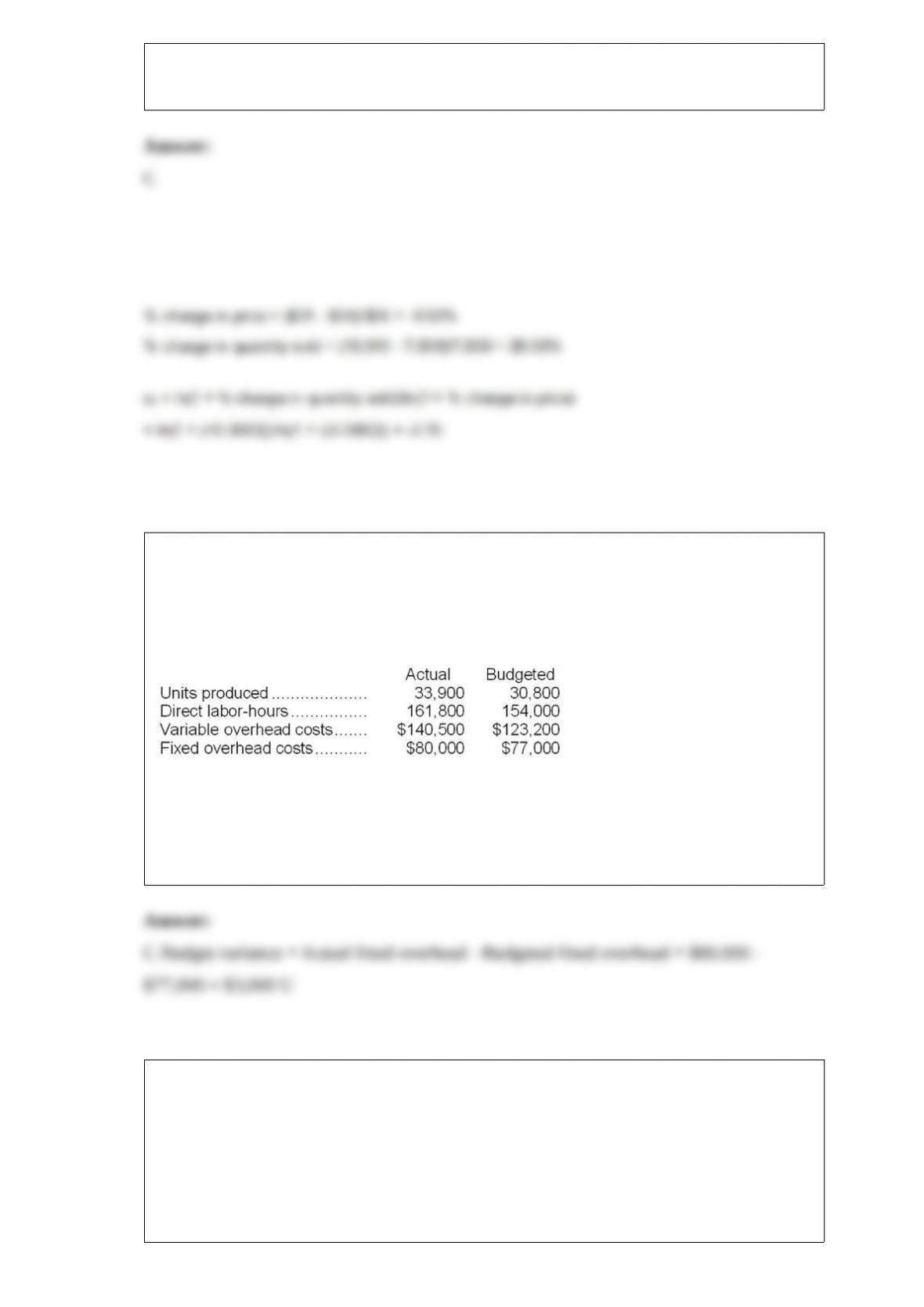

13) The Dillon Corporation makes and sells a single product. Overhead costs are

applied on the basis of standard direct labor-hours. The standard cost card shows that 5

direct labor-hours are required per unit. The Dillon Corporation had the following

budgeted and actual data for March:

The fixed manufacturing overhead budget variance for March is:

A.$900 F

B.$3,900 F

C.$3,000 U

D.$7,750 F

14) Holding all other things constant, an increase in how sensitive customers are to

price would affect:

A.the markup under the absorption costing approach to cost-plus pricing.

B.the markup used to compute the profit-maximizing price.

C.both the markup under the absorption costing approach to cost-plus pricing and the

markup used to compute profit-maximizing price.

D.neither the markup under the absorption costing approach to cost-plus pricing nor the

markup used to compute profit-maximizing price.

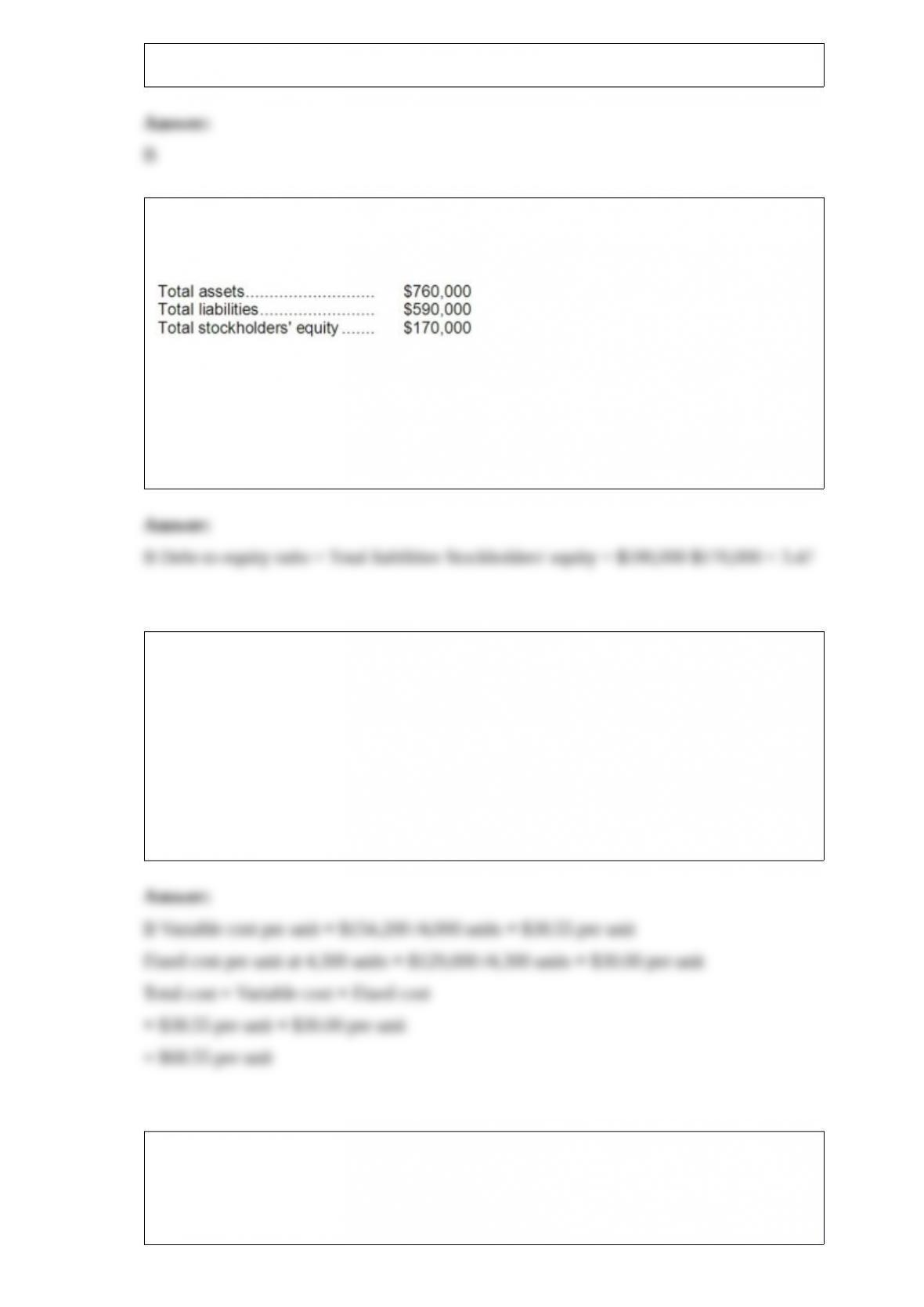

15) Shipley Corporation has provided the following data from its most recent balance

sheet:

The debt-to-equity ratio is closest to:

A.0.29

B.3.47

C.0.22

D.0.78

16) At an activity level of 4,000 machine-hours in a month, Curt Corporations total

variable production engineering cost is $154,200 and its total fixed production

engineering cost is $129,000. What would be the total production engineering cost per

unit, both fixed and variable, at an activity level of 4,300 machine-hours in a month?

Assume that this level of activity is within the relevant range.

A) $68.33

B) $68.55

C) $70.80

D) $65.86

17) The total cash flow net of income taxes in year 2 is:

A.$111,500

B.$150,000

C.$46,500

D.$110,000