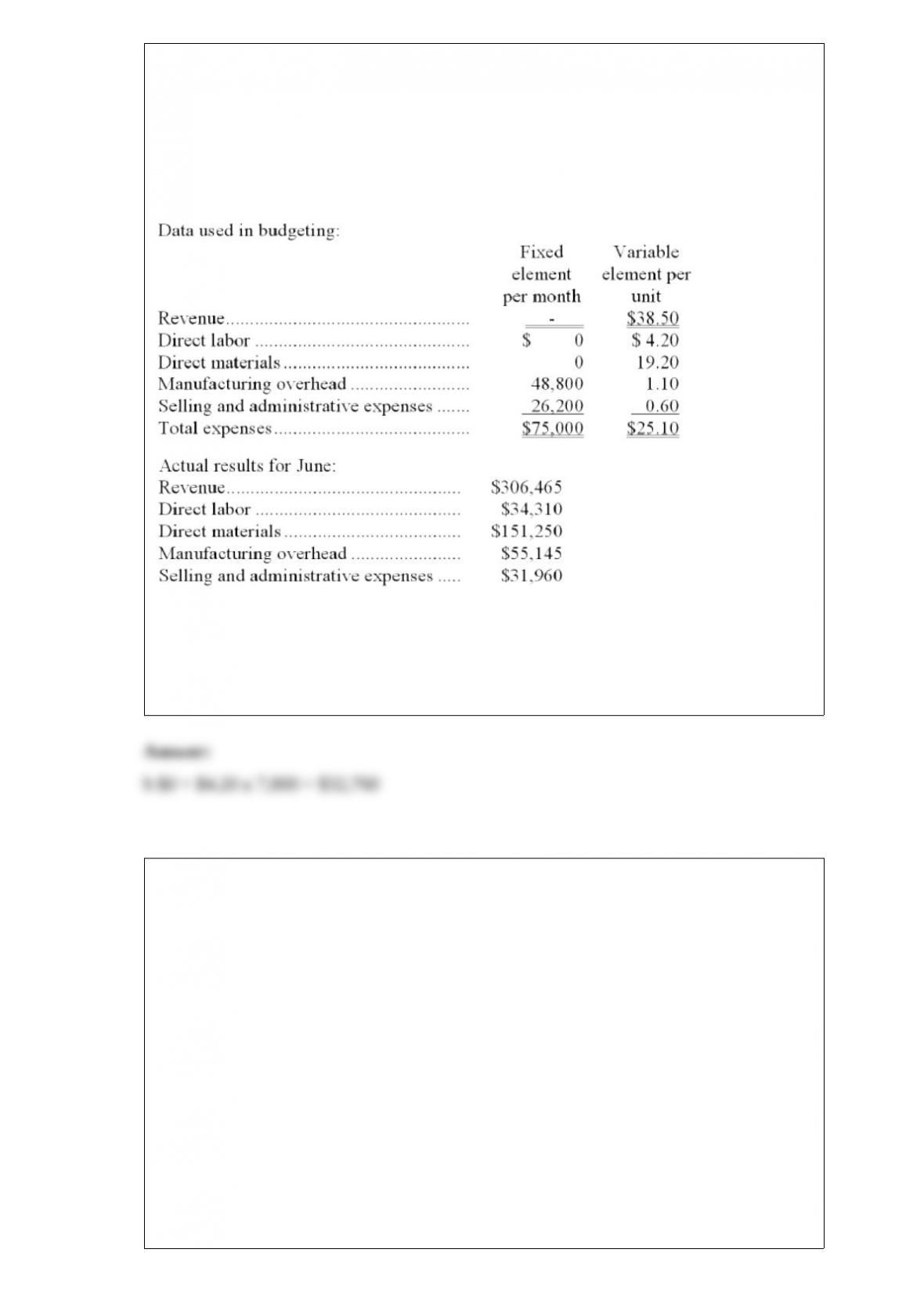

1) witherington corporation manufactures and sells a single product. the company uses

units as the measure of activity in its budgets and performance reports. during june, the

company budgeted for 7,800 units, but its actual level of activity was 7,850 units. the

company has provided the following data concerning the formulas used in its budgeting

and its actual results for june:

the direct labor in the planning budget for june would be closest to:

a.$32,970

b.$32,760

c.$34,310

d.$34,091

2) corado corporation has in stock 77,000 kilograms of material n that it bought five

years ago for $7.15 per kilogram. this raw material was purchased to use in a product

line that has been discontinued. material n can be sold as is for scrap for $4.50 per

kilogram. an alternative would be to use material n in one of the company’s current

products, m01y, which currently requires 2 kilograms of a raw material that is available

for $7.15 per kilogram. material n can be modified at a cost of $0.94 per kilogram so

that it can be used as a substitute for this material in the production of product m01y.

however, after modification, 4 kilograms of material n is required for every unit of

product m01y that is produced. corado corporation has now received a request from a

company that could use material n in its production process. assuming that corado

corporation could use all of its stock of material n to make product m01y or the

company could sell all of its stock of the material at the current scrap price of $4.50 per

kilogram, what is the minimum acceptable selling price of material n to the company

that could use material n in its own production process?

a.$1.86

b.$2.64

c.$4.52

d.$4.50

3) trevor company is contemplating the introduction of a new product. the company has

gathered the following information concerning the product:

the company uses the absorption costing approach to cost-plus pricing as described in

the text.

required:

a. compute the markup on absorption cost.

b. compute the selling price.

c. if the price computed in “b” above is charged, and costs turn out as projected, can the

company be assured that no loss will be sustained on the new product? explain.

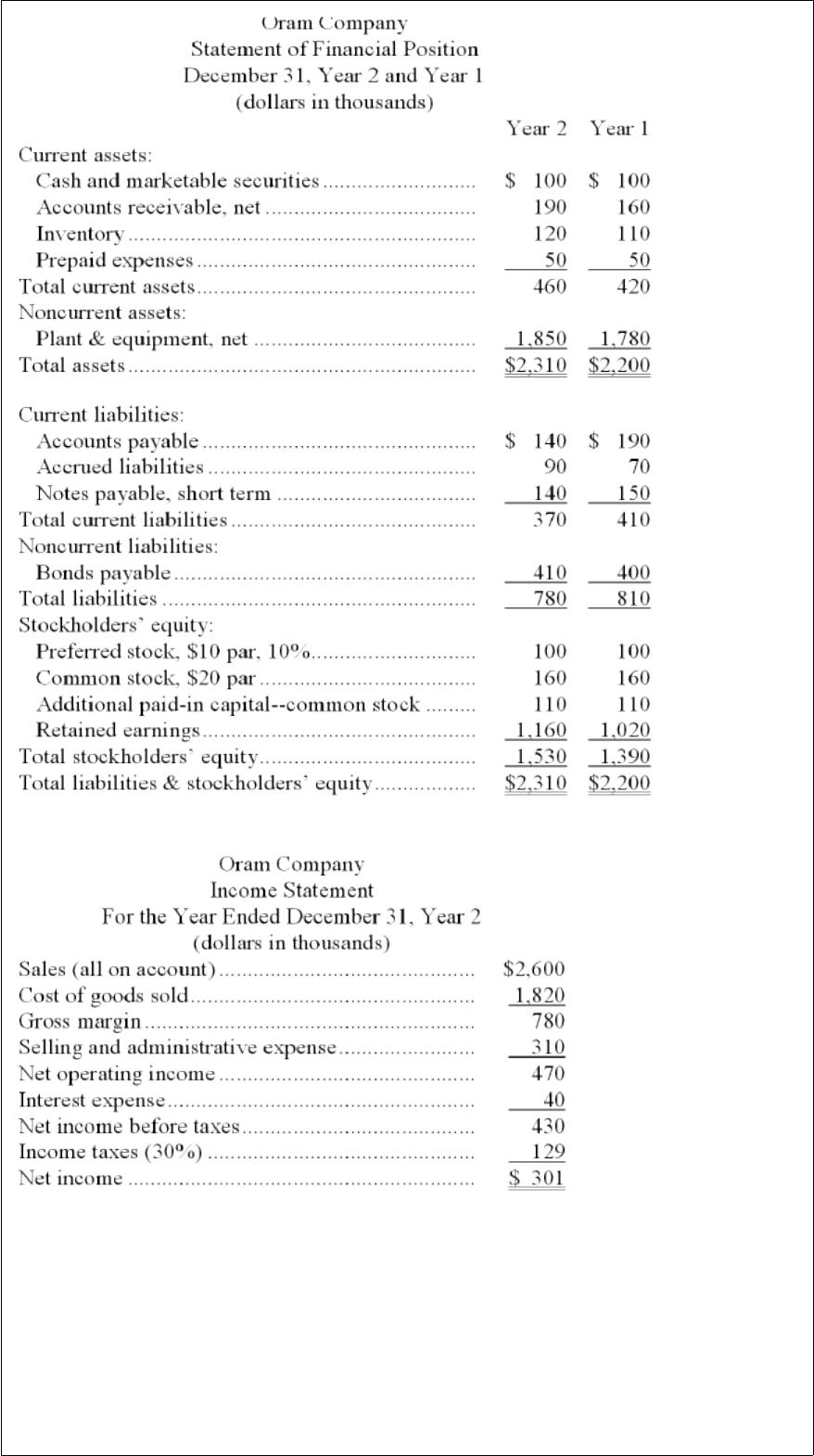

4) financial statements for oram company appear below:

dividends during year 2 totaled $161 thousand, of which $10 thousand were preferred

dividends. the market price of a share of common stock on december 31, year 2 was

$610.

oram company’s return on total assets for year 2 was closest to:

a.12.1%

b.13.3%

c.14.6%

d.13.9%

5) a company’s average operating assets are $220,000 and its net operating income is

$44,000. the company invested in a new project, increasing average assets to $250,000

and increasing its net operating income to $49,550. what is the project’s residual income

if the required rate of return is 20%?

a.($450)

b.$450

c.$600

d.($600)

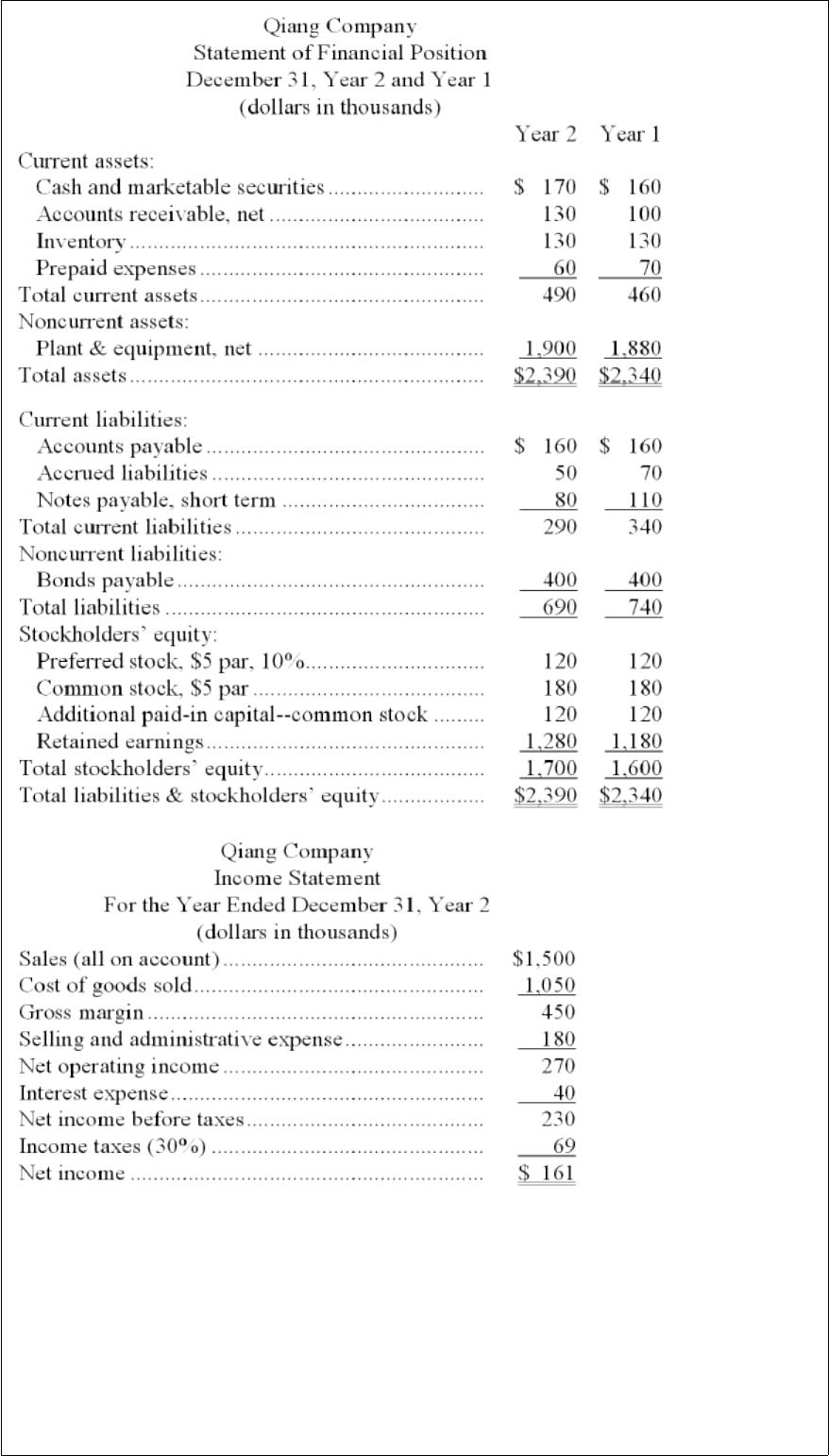

6) financial statements for qiang company appear below:

dividends during year 2 totaled $61 thousand, of which $12 thousand were preferred

dividends. the market price of a share of common stock on december 31, year 2 was

$50.

required:

compute the following for year 2:

a. earnings per share of common stock.

b. price-earnings ratio.

c. dividend yield ratio.

d. return on total assets.

e. return on common stockholders’ equity.

f. book value per share.

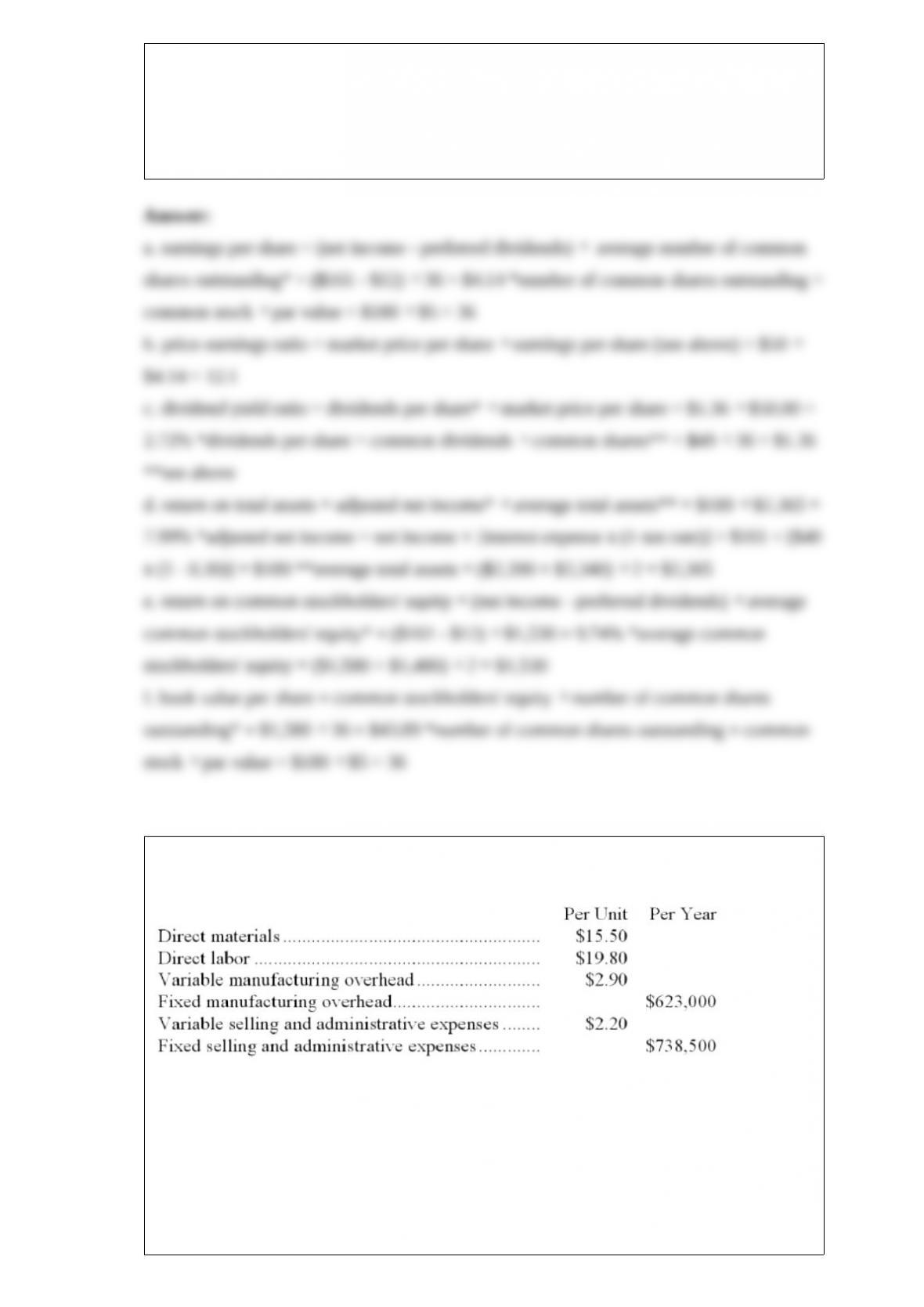

7) quare company makes a product that has the following costs:

the company uses the absorption costing approach to cost-plus pricing as described in

the text. the pricing calculations are based on budgeted production and sales of 35,000

units per year.

the company has invested $100,000 in this product and expects a return on investment

of 11%.

required:

a. compute the markup on absorption cost.

b. compute the selling price of the product using the absorption costing approach.

c. assume that every 10% increase in price leads to a 14% decrease in quantity sold.

assuming no change in cost structure and that direct labor is a variable cost, compute

the profit-maximizing price.

8) assuming that direct labor is a variable cost, product costs under variable costing

include only:

a.direct materials and direct labor

b.direct materials, direct labor, and variable manufacturing overhead

c.direct materials, direct labor, variable manufacturing overhead, and variable selling

and administrative expenses

d.direct material, variable manufacturing overhead, and variable selling and

administrative expenses

9) what was the cost per equivalent unit for conversion during the month?

a.$5.45

b.$6.95

c.$4.00

d.$3.05

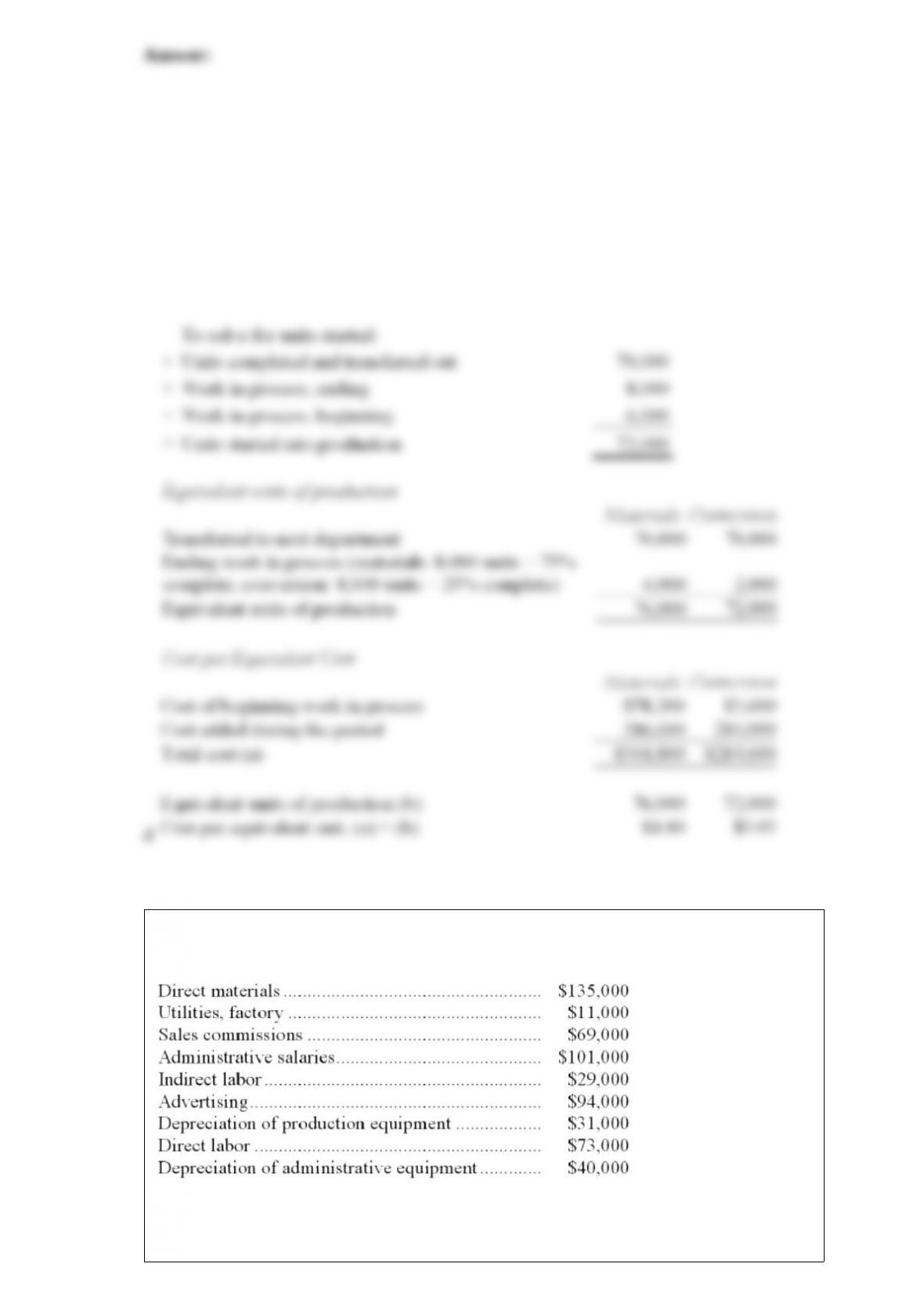

10) a partial listing of costs incurred at rust corporation during august appears below:

required:

a. what is the total amount of product cost listed above? show your work.

b. what is the total amount of period cost listed above? show your work.

11) the management of bauza corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. the company’s controller

has provided an example to illustrate how this new system would work. in this example,

the allocation base is machine-hours and the estimated amount of the allocation base for

the upcoming year is 12,000 machine-hours. in addition, capacity is 14,000

machine-hours and the actual level of activity for the year is 11,400 machine-hours. all

of the manufacturing overhead is fixed and is $20,160 per year. for simplicity, it is

assumed that this is the estimated manufacturing overhead for the year as well as the

manufacturing overhead at capacity. it is further assumed that this is also the actual

amount of manufacturing overhead for the year.

if the company bases its predetermined overhead rate on capacity, by how much was

manufacturing overhead underapplied or overapplied?

a.$1,008 overapplied

b.$1,008 underapplied

c.$3,744 overapplied

d.$3,744 underapplied

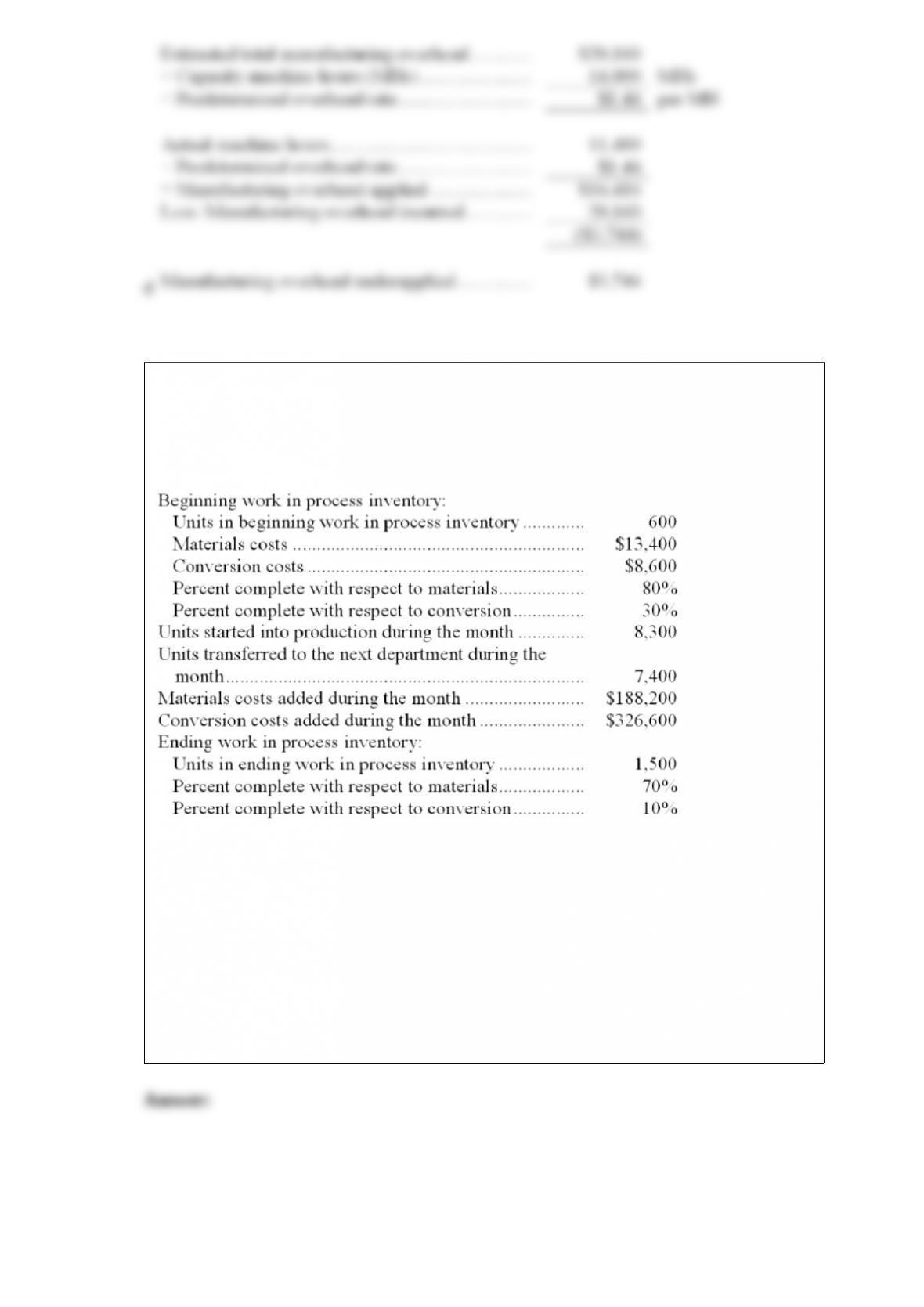

12) lowler corporation uses the weighted-average method in its process costing system.

data concerning the first processing department for the most recent month are listed

below:

note: your answers may differ from those offered below due to rounding error. in all

cases, select the answer that is the closest to the answer you computed. to reduce

rounding error, carry out all computations to at least three decimal places.

what are the equivalent units for materials for the month in the first processing

department?

a.1,050

b.8,450

c.8,900

d.7,400

13) the linear equation y = a + bx is often used to express cost formulas. in this

equation:

a.the b term represents variable cost per unit of activity

b.the a term represents variable cost in total

c.the x term represents total cost

d.the y term represents total fixed cost

14) (ignore income taxes in this problem.) prince company’s required rate of return is

10%. the company is considering the purchase of three machines, as indicated below.

consider each machine independently.

required:

a. machine a will cost $25,000 and have a life of 15 years. its salvage value will be

$1,000, and cost savings are projected at $3,500 per year. compute the machine’s net

present value.

b. how much will prince company be willing to pay for machine b if the machine

promises annual cash inflows of $5,000 per year for 8 years?

c. machine c has a projected life of 10 years. what is the machine’s internal rate of

return, to the nearest whole percent, if it costs $30,000 and will save $6,000 annually in

cash operating costs? would you recommend purchase? explain.

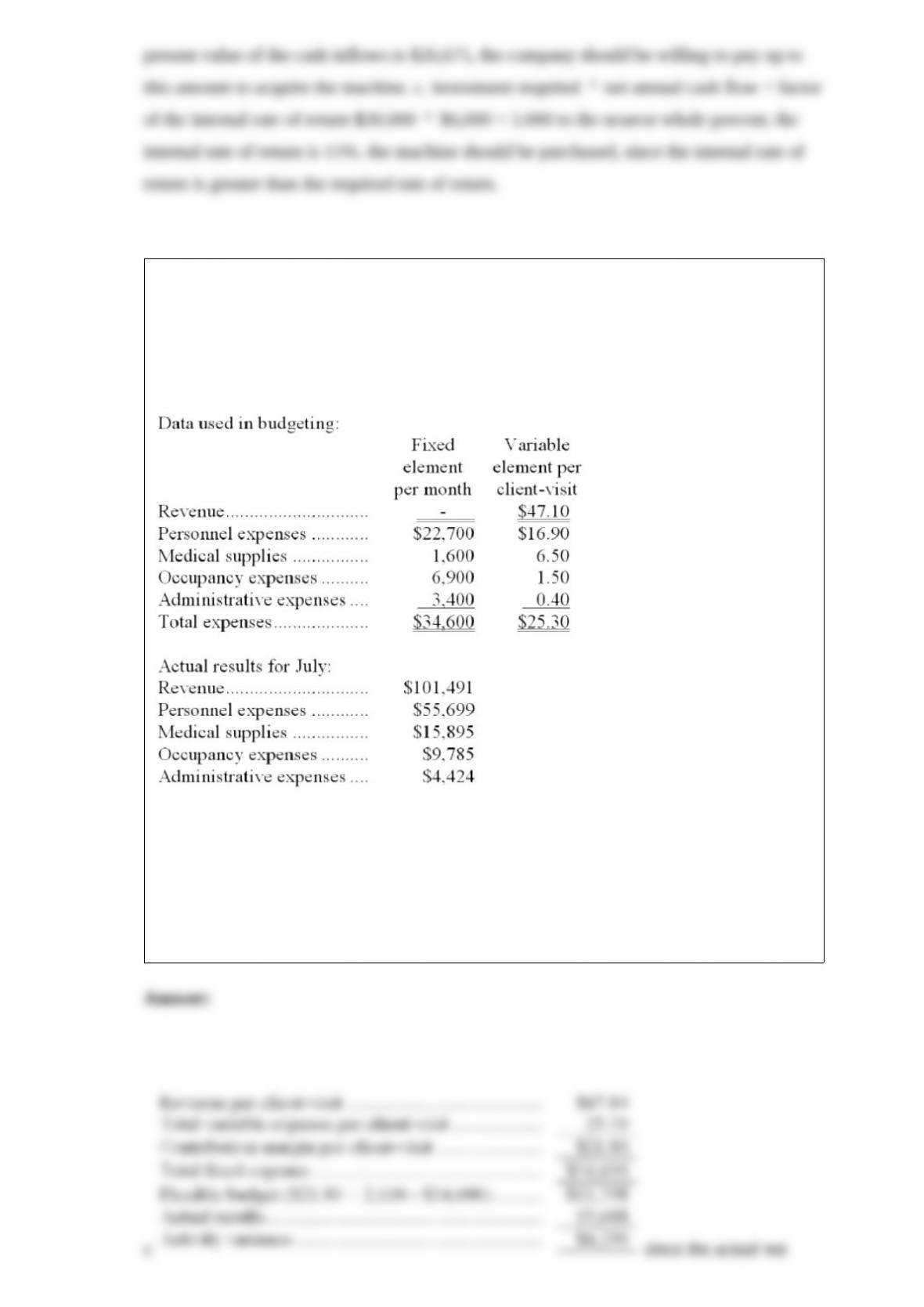

15) burget clinic uses client-visits as its measure of activity. during july, the clinic

budgeted for 2,100 client-visits, but its actual level of activity was 2,110 client-visits.

the clinic has provided the following data concerning the formulas used in its budgeting

and its actual results for july:

the overall revenue and spending variance (i.e., the variance for net operating income in

the revenue and spending variance column on the flexible budget performance report)

for july would be closest to:

a.$4,508 f

b.$4,290 u

c.$4,290 f

d.$4,508 u

16) which of the following would decrease the net present value of a project?

a.a decrease in the income tax rate

b.a decrease in the initial investment

c.an increase in the useful life of the project

d.an increase in the discount rate

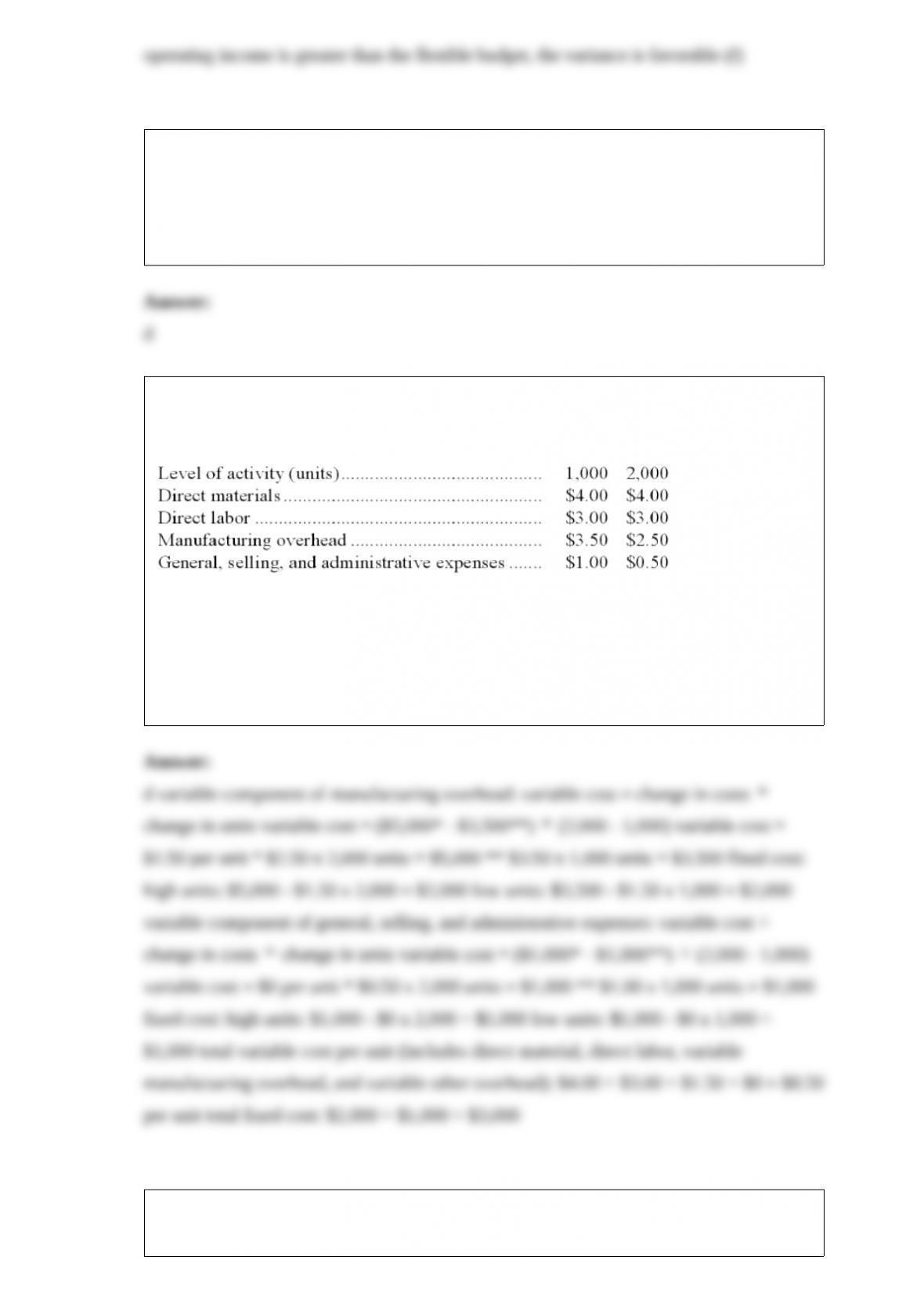

17) a company that produces and sells a single product has provided the following

volume and average cost data for two accounting periods:

the best estimates of the total fixed cost and variable cost per unit are closest to:

a.$2,000 fixed; $1.50 variable

b.$2,000 fixed; $7.00 variable

c.$3,000 fixed; $7.00 variable

d.$3,000 fixed; $8.50 variable

18) the best estimate of the total variable cost per unit is:

a.$84.50

b.$100.90

c.$106.90

d.$105.70

19) in december, one of the processing departments at stiel corporation had ending

work in process inventory of $38,000. during the month, $119,000 of costs were added

to production and the cost of units transferred out from the department was $92,000.

in the department’s cost reconciliation report for september, the total cost to be

accounted for would be:

a.$34,000

b.$185,000

c.$370,000

d.$355,000