You form a partnership with your best friend. You have contributed 65% of the capital

and can claim 65% of the net income. At the end of the first year, you discover that your

partner has run up $40,000 in debt using the business’ credit card. The maximum you

could be liable for is:

A. $0.

B. $40,000.

C. $20,000.

D. $26,000.

Answer:

The ratio that measures the percentage of financing from creditors is the:

A. Current ratio.

B. Times interest earned ratio.

C. Debt to assets ratio.

D. Price/earnings ratio.

Answer:

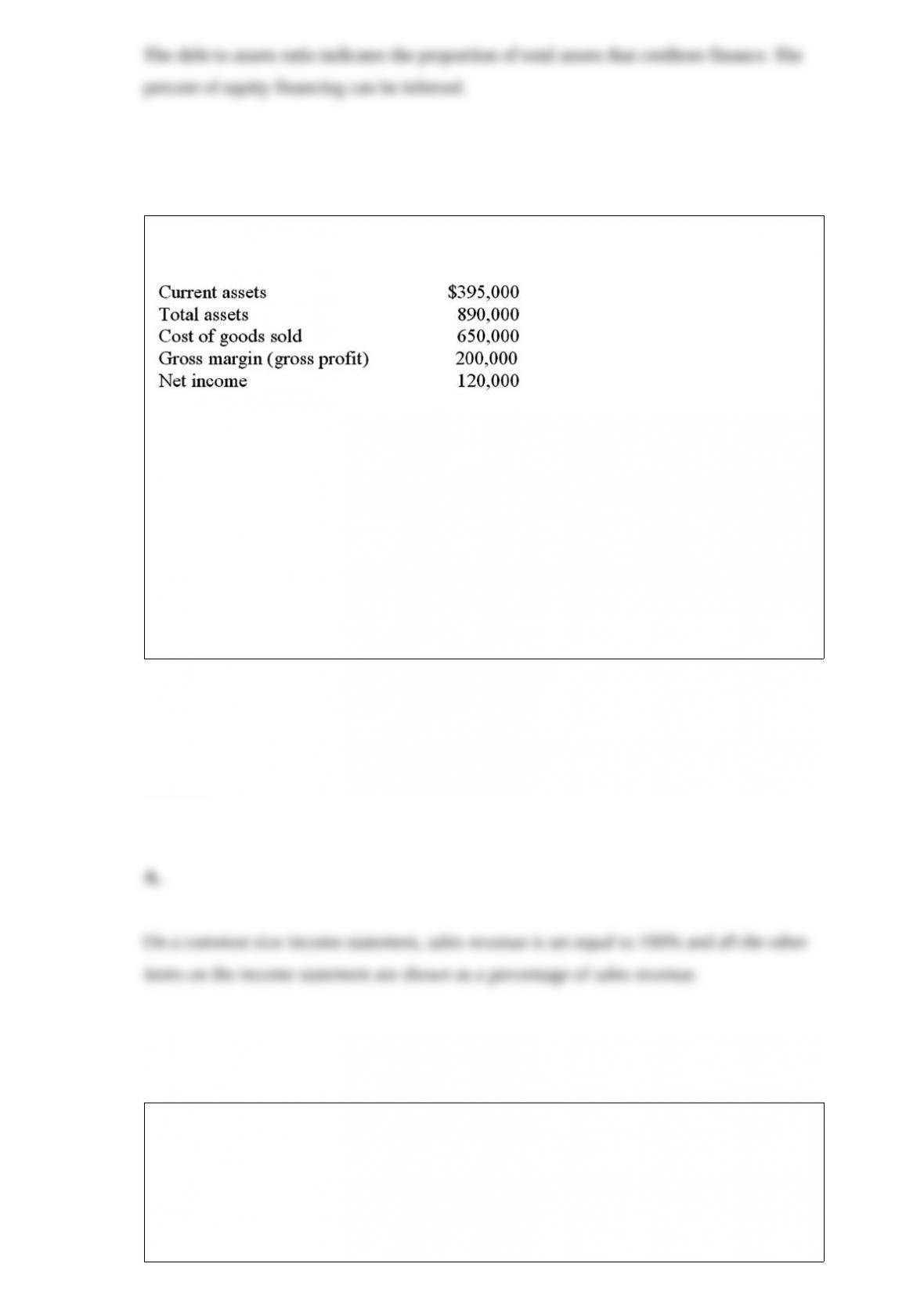

The following information is taken from the financial statements of a company for the

current year:

Use the information above to answer the following question. On a common size income

statement for the year, what is the percentage that would be shown for sales revenue?

A. 100%

B. 14%

C. 60%

D. 13%

Answer:

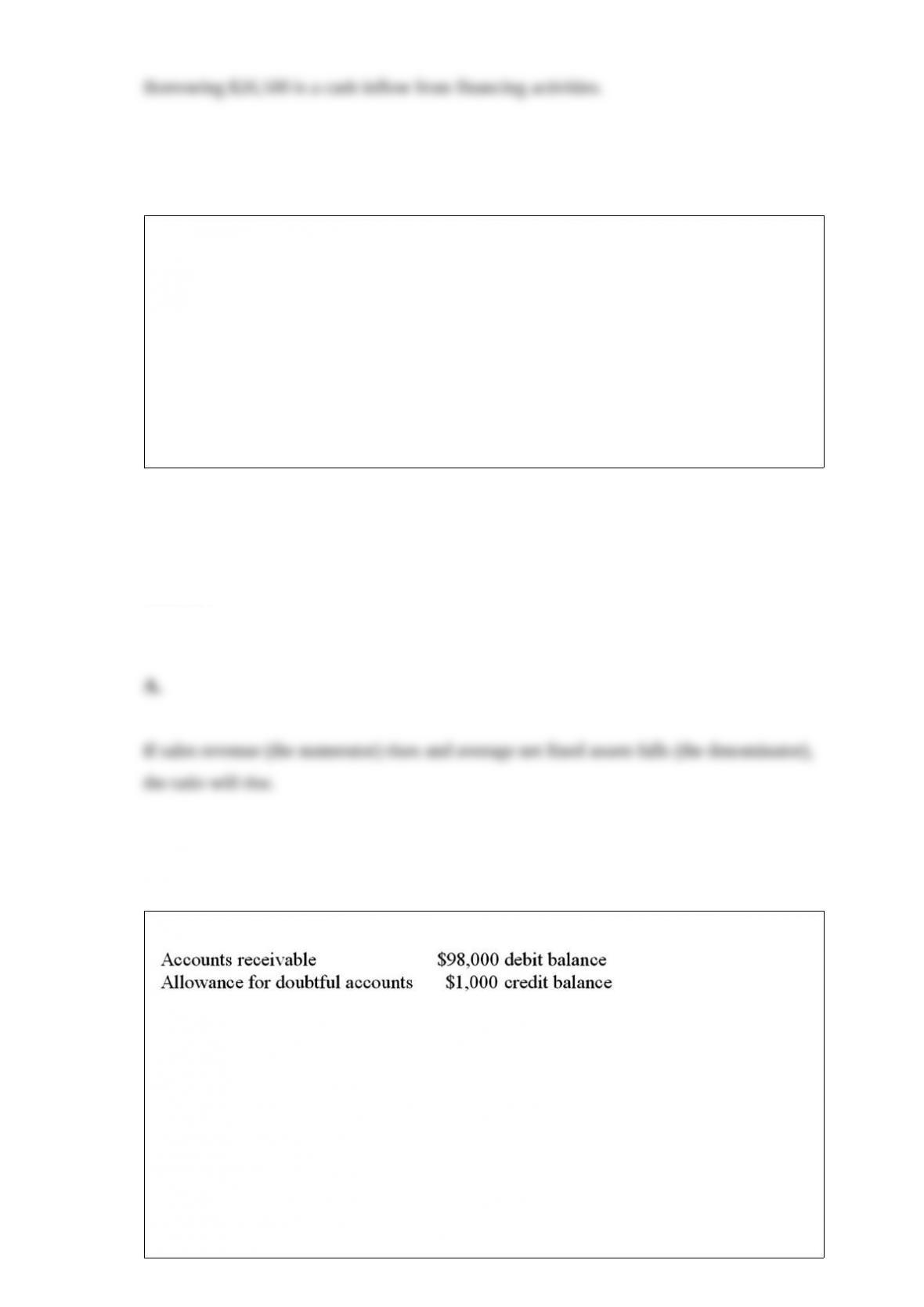

Your company has previously averaged about 26% of its accounts receivable in the

“over 90 days past due” category but now forecasts 18% in this category. You use the

aging of accounts receivable method of estimating bad debt expense. If the total of

credit sales remains unchanged from previous months and no write offs are made, the

estimate of bad expense based on the new forecast will:

A. increase over the estimate for previous months.

B. decrease over the estimate for previous months.

C. not change.

D. will depend on the percentage of credit sales deemed uncollectible.

Answer:

The WC Company borrowed $26,500 from a bank during 2013.

A. This would be listed as ($26,500) under investing activities on the statement of cash

flows.

B. This would be listed as ($26,500) under operating activities on the statement of cash

flows.

C. This would be listed as $26,500 under investing activities on the statement of cash

flows.

D. This would be listed as $26,500 under financing activities on the statement of cash

flows.

Answer:

If net sales revenue rises 5% while the average book value of fixed assets falls 5%:

A. the fixed asset turnover ratio will rise.

B. the fixed asset turnover ratio will fall.

C. the fixed asset turnover ratio will stay the same.

D. the impact on the fixed asset turnover ratio cannot be determined since the beginning

values are unknown.

Answer:

The unadjusted trial balance at the end of the year includes the following:

The company uses the allowance method and has completed the aging schedule which

indicates $5,800 of accounts are estimated uncollectible. What is the amount of bad

debt expense to be recorded for the year?

A. $5,800

B. $4,800

C. $6,800

D. $7,800

Answer:

As of November 29, it appears that Notel will report earnings per share (EPS) of $1.15

for the quarter ended November 30. Which of the following events would cause this

EPS number to decrease, assuming the event occurs the morning of November 30?

A. The company pays a supplier for inventory bought on account.

B. The company declares, but does not pay, a cash dividend.

C. The company purchases 10 shares of common stock in another company.

D. The company reissues the treasury stock it holds.

Answer:

A decrease in accounts receivable turnover ratio is indicative of:

A. an increase in sales revenue.

B. slower-selling inventory.

C. an increase in accounts receivable.

D. a decline in cost of goods sold.

Answer:

When a company makes an adjustment in anticipation of future uncollectible

receivables:

A. it debits an asset account and credits a liability account.

B. it debits an expense account and credits an asset account.

C. it debits an expense account and credits a revenue account.

D. it debits an expense account and credits a contra-asset account.

Answer:

Presented below are selected accounts from the unadjusted trial balance of Sneetch Star

Makers Inc., a talent agency, at 12/31/13 (debit and credit labels have been omitted;

assume all balances are normal).

The office equipment depreciates at a rate of $1,000 per year. The adjusting entry would

include

A. a debit to accumulated depreciation for $1,000.

B. a credit to office equipment for $1,000.

C. a credit to depreciation expense for $1,000.

D. a credit to accumulated depreciation for $1,000.

Answer:

Choose the appropriate letter to match the term and the definition. More definitions are

provided than terms.

Term

_____ 1/ SOX

_____ 2/ Time-series analysis.

_____ 3/ 10-K.

_____ 4/ Qualified.

_____ 5/ Loan covenant.

_____ 6/ Debt-to-assets ratio.

_____ 7/ Management’s Discussion & Analysis.

_____ 8/ Valuation role.

_____ 9/ The fraud triangle

Definition

A. Total liabilities divided by total assets.

B. An audit performed by a certified public accountant.

C. A detailed discussion of a company’s performance that appears in the annual report.

D. Compares a company’s performance in one time period relative to prior periods.

E. A company’s current event report to the SEC.

F. Means that data are complete and up-to-date.

G. An audit opinion in which the auditors cannot say that GAAP was followed.

H. When accounting information is used by potential investors to estimate the worth of

a company.

I. The components of which are incentive, opportunity, rationalize and conceal.

J. Compares a company’s performance in one time period to the industry during the

same time period.

K. A company’s annual report to the SEC.

L. Laws intended to improve financial reporting and restore investor confidence.

M. A business reason why managers might be tempted to misstate a company’s TRUE

performance.

Answer:

Which of the following are generally recorded as liabilities on the balance sheet?

A. Remote likelihood liabilities.

B. Possible contingent liabilities.

C. Probable contingent liabilities.

D. Immaterial contingent liabilities.

Answer:

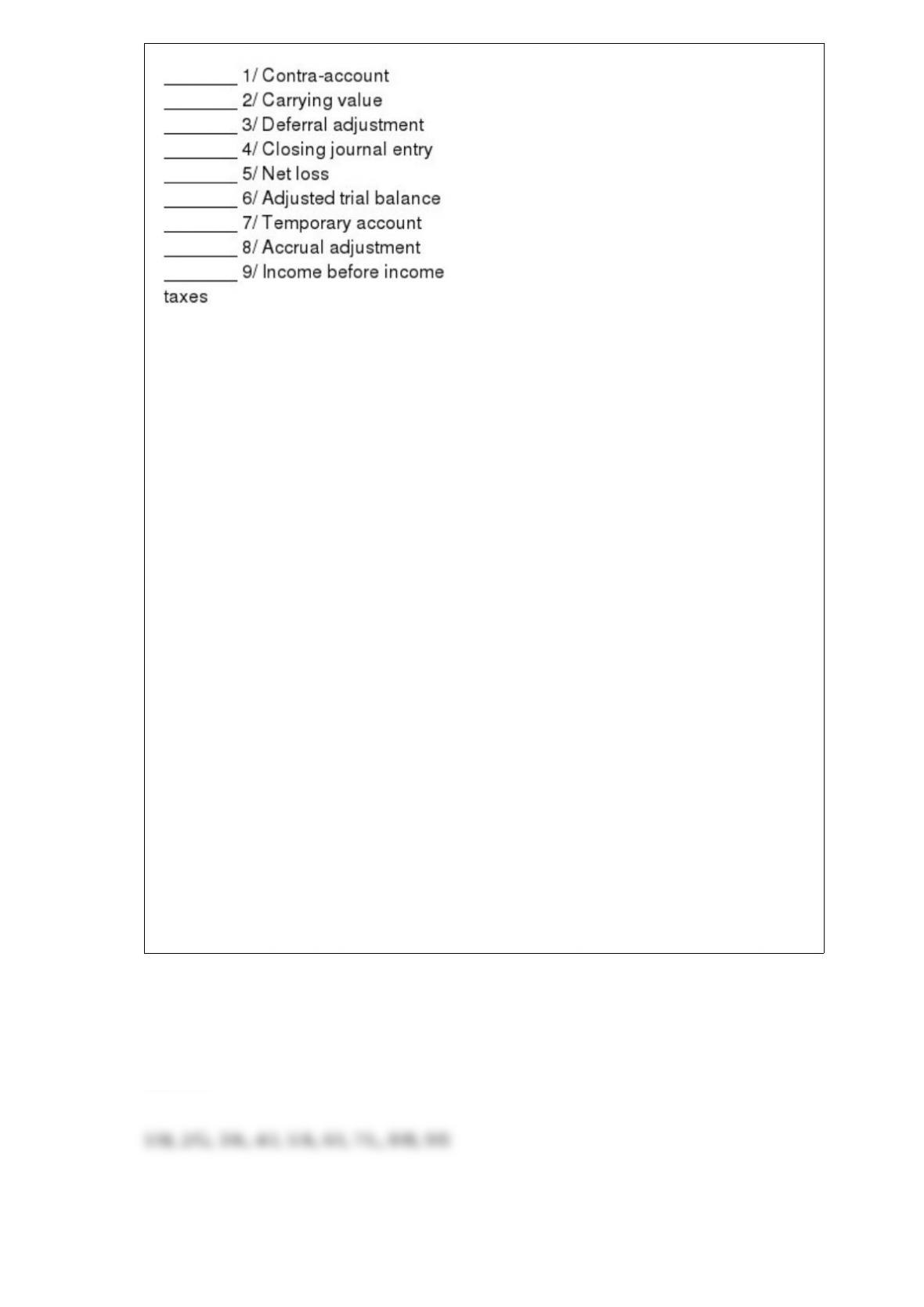

Match the term with the letter corresponding to the definition in the list below. There

are more definitions than terms.

Terms

Definitions

A. When revenue minus expenses is a negative number.

B. Adds new values into the balance sheet and income statement accounts.

C. Also known as balance sheet accounts.

D. Entries made to update existing accounts and record new events.

E. The level of profit prior to considering income tax.

F. Lists the balances of all accounts to check that revenues equal expenses.

G. The amount at which an asset or liability is reported in the financial statements.

H. An account that is paired with another account to reduce its book value.

I. Lists the balances of all temporary and permanent accounts to check that debits equal

credits.

J. A journal entry that transfers net income or loss to the retained earnings account.

K. Converts some of an asset’s or liability’s book value into an expense or revenue.

L. An account that must have a zero balance after Closing entries have been made.

M. Lists the balances of all permanent accounts to check that debits equal credits.

Answer:

A book manufacturing company sells equipment for $450,000 when the book value of

the equipment is $400,000. The company would record the extra $50,000 as:

A. a gain, increasing net income and stockholders’ equity.

B. revenue, increasing net income and stockholders’ equity.

C. expenses, decreasing net income and stockholders’ equity.

D. a loss, decreasing net income and stockholders’ equity.

Answer:

An expense:

A. will decrease the amount of net income on the income statement.

B. will decrease the amount of contributed capital on the balance sheet.

C. will be increased with a credit to the account.

D. normally has a credit balance.

Answer:

The annual interest payment on bonds:

A. increases over the life of the bonds when bonds are issued at a discount.

B. decreases over the life of the bonds when bonds are issued at a discount.

C. stays constant over the life of the bonds, regardless of whether bonds are issued at

par, a discount, or a premium.

D. increases over the life of the bonds under the effective-interest method, but stays

constant under the straight-line method of amortization.

Answer:

Using straight-line amortization, when a bond is sold at a premium:

A. the amortized premium is added to the interest payable to calculate interest expense.

B. bonds payable rises by a constant amount each year.

C. interest expense is calculated by subtracting the amortized premium from the interest

payment that is to be made.

D. interest expense rises each year.

Answer:

As of the beginning of 2013 a company had total contributed capital of $300,000 and

total retained earnings of $35,000. Total liabilities were $100,000. During the year

2013, the company had the following transactions:

– Issued stock for cash of $60,000.

– Declared and paid a cash dividend of $15,000.

– Reported total revenue of $160,000 and total expenses of $90,000.

The debt-to-assets ratio at the beginning of 2013 was closest to:

A. 0.23

B. 0.30

C. 0.33

D. 0.25

Answer:

IBM signs an agreement to lend one of its customers $200,000 to be repaid in one year

at 5.5% interest. IBM would record this loan as:

A. notes payable.

B. accounts receivable.

C. notes receivable.

D. unearned revenue.

Answer:

Which of the following will happen if the accrual adjusting entry is not made for

revenue earned but not yet recorded?

A. Assets will be understated and revenues will be overstated.

B. Revenues will be understated and assets will be overstated.

C. Both revenues and assets will be overstated.

D. Both revenues and assets will be understated.

Answer:

On September 1, a company purchased a vehicle for $23,000 with a residual value of

$3,000. The estimated useful life is 5 years and the company uses the straight-line

method. What is the depreciation expense for the year ended December 31?

A. $1,333.

B. $1,000

C. $4,000.

D. $1,533.

Answer:

All other things being equal, when companies make stock repurchases:

A. EPS falls and ROE rises.

B. EPS rises and ROE stays the same.

C. EPS rises and ROE falls.

D. EPS and ROE both rise.

Answer:

Your company received payment last month for a service that you provided this month.

How will the business activity of the current month affect the basic accounting

equation?

A. Assets will not change; liabilities (Unearned Revenue) will decrease; and

stockholders’ equity (Service Revenue) will increase.

B. Assets (Cash) will increase, liabilities (Unearned Revenue) will increase, and

stockholders’ equity will not change.

C. Assets (Cash) will increase, liabilities will not change, and stockholders’ equity

(Service Revenue) will increase.

D. Assets (Prepaid Expenses) will decrease, liabilities will not change, and

stockholders’ equity (Service Revenue) will increase.

Answer:

If a company returns an item to a supplier, the supplier will record the return as:

A. sales returns and allowances.

B. shrinkage.

C. sales discounts.

D. purchase returns and allowances.

Answer:

If insurance expense is $7,000 and the beginning and ending balances of prepaid

insurance are $1,500 and $2,000, respectively, the cash paid for insurance is

A. $7,000

B. $6,500

C. $5,000

D. $7,500

Answer:

Your company’s president donates a large amount of her own money to charity and

receives significant publicity that includes the company’s name. How would the

benefits of this publicity appear on the balance sheet?

A. It would appear as a current asset.

B. It would appear as contributed capital.

C. It would appear as a long-term asset.

D. It would not appear on the balance sheet.

Answer:

A company issues a 5-year bond with a $7,500 discount. Using straight-line

amortization, the company should:

A. debit discount on bonds payable for $1,500 per year.

B. credit discount on bonds payable for $1,500 per year.

C. debit interest payable for $1,500 per year.

D. credit interest expense for $1,500 per year.

Answer:

Which of the following accurately describes how the collection of cash on account from

a customer would affect the ratios indicated?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

A company reported a gross profit percentage of 25% with net sales of $347,800. What

is the amount of cost of goods sold?

A. $86,950

B. $260,850

C. $326,063

D. $108,688

Answer:

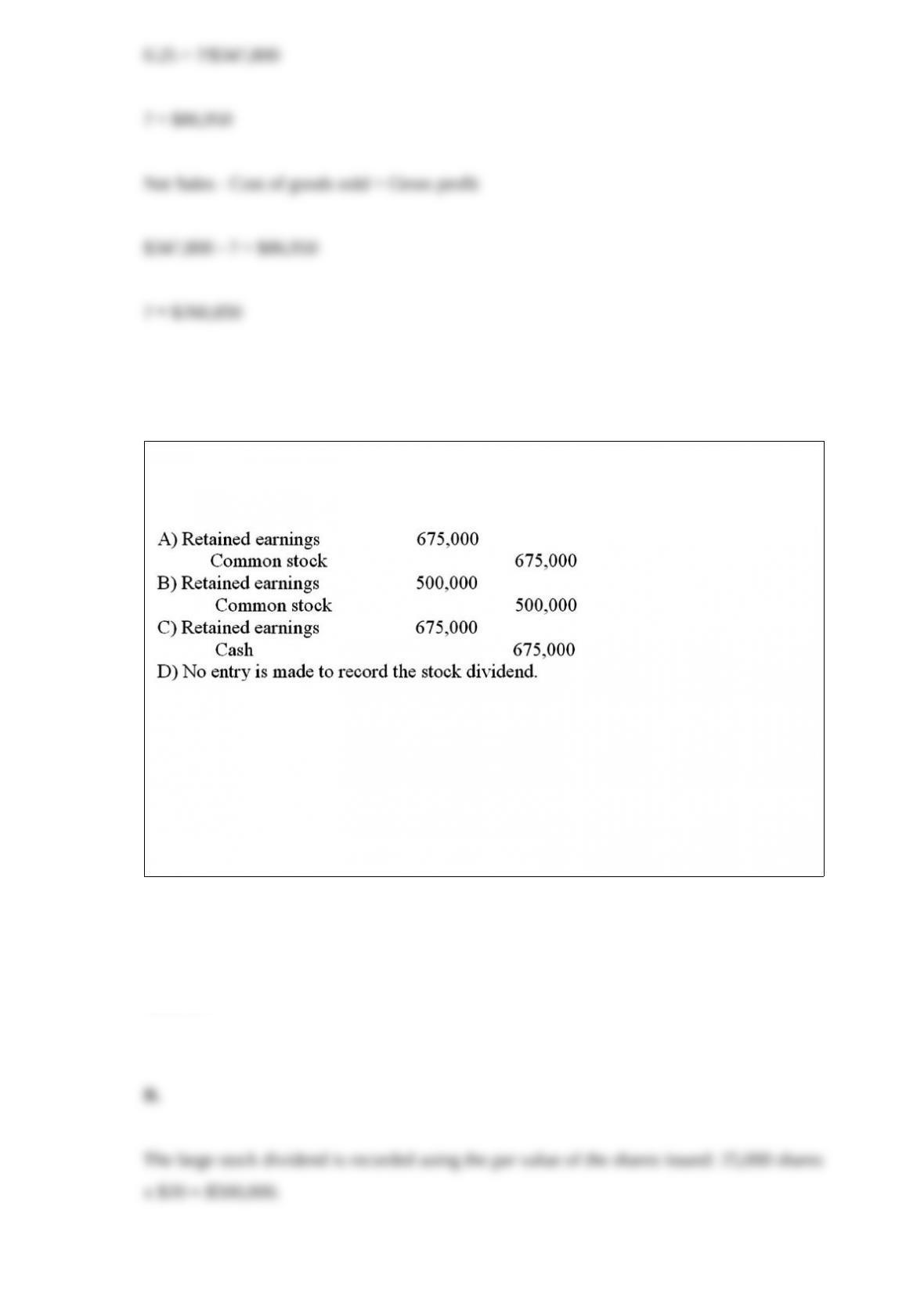

A corporation had 50,000 shares of $20 par value common stock outstanding. The

board of directors declared and issued a 50% stock dividend. The market value of the

stock was $27 per share. What is the journal entry to record this stock dividend?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

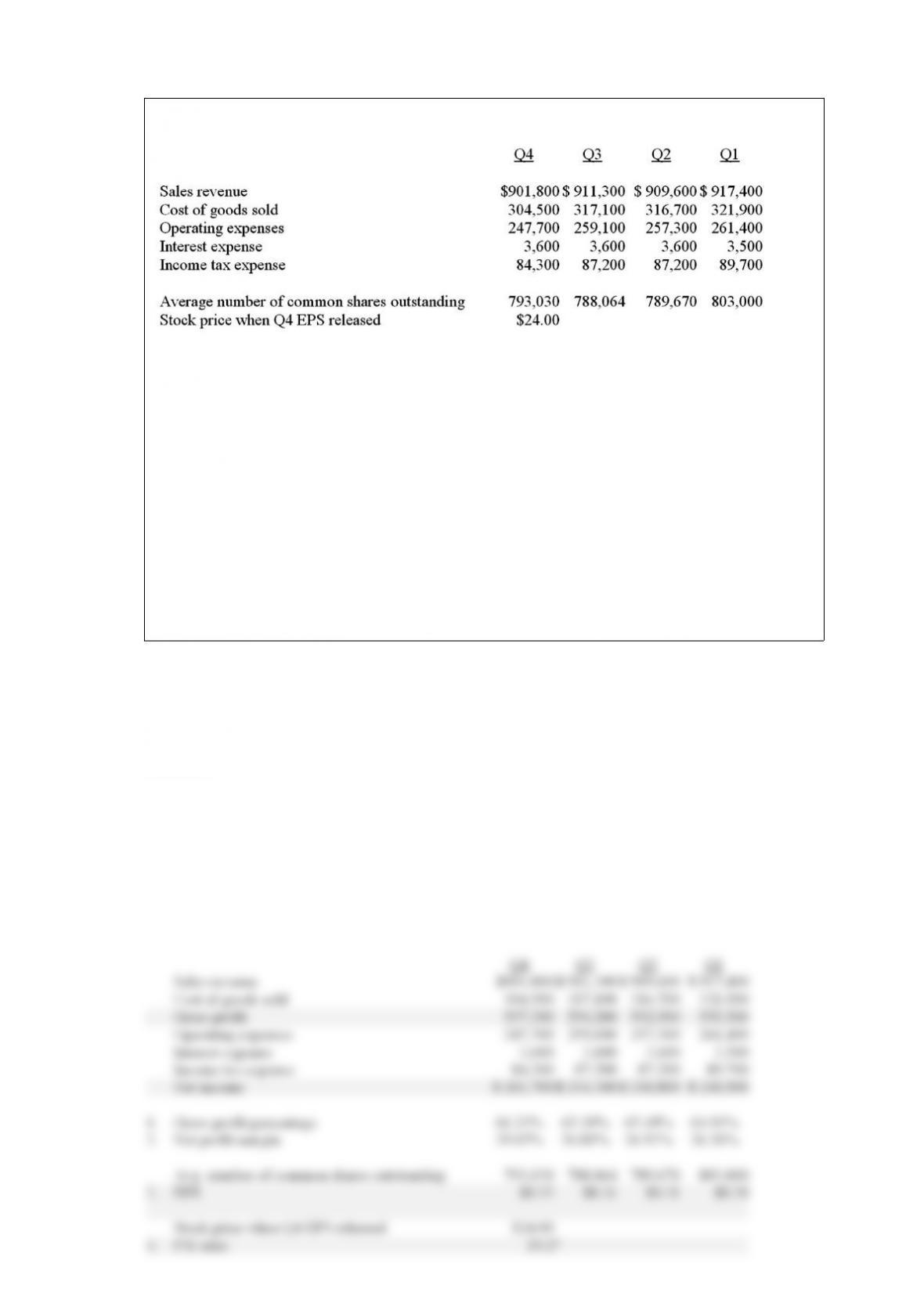

Mercedes, Co. has the following quarterly financial information.

A. Use the financial information above to calculate the following. Round to two

decimal places (e.g., 0.1234 as 12.34%.)

1.) Gross profit percentage for each quarter.

2.) Net profit margin for each quarter.

3.) EPS for each quarter.

4.) P/E ratio at the end of the year.

B. Evaluate the company’s profitability.

Answer:

A corporation prepared its statement of cash flows for the year. The following

information is taken from that statement:

What is the amount of net cash provided by (used in) financing activities?

A. $15,400

B. ($3,300)

C. ($15,400)

D. $3,300

Answer: