Which of the following statements about job-order cost sheets is true?

a. All job-order cost sheets serve as the general ledger control account for Work in

Process Inventory.

b. Job-order cost sheets can serve as subsidiary ledger information for both Work in

Process Inventory and Finished Goods Inventory.

c. If material requisition forms are used, job-order cost sheets do not need to be

maintained.

d. Job-order cost sheets show costs for direct material and direct labor, but not for

manufacturing overhead since it is an applied amount.

Indirect costs should be allocated for all of the following reasons except to

a. motivate managers.

b. determine the full cost of a product.

c. motivate general administration.

d. compare alternatives for decision making.

Which of the following changes would not decrease the present value of the future

depreciation deductions on a specific depreciable asset?

a. a decrease in the marginal tax rate

b. a decrease in the discount rate

c. a decrease in the rate of depreciation

d. an increase in the life expectancy of the depreciable asset

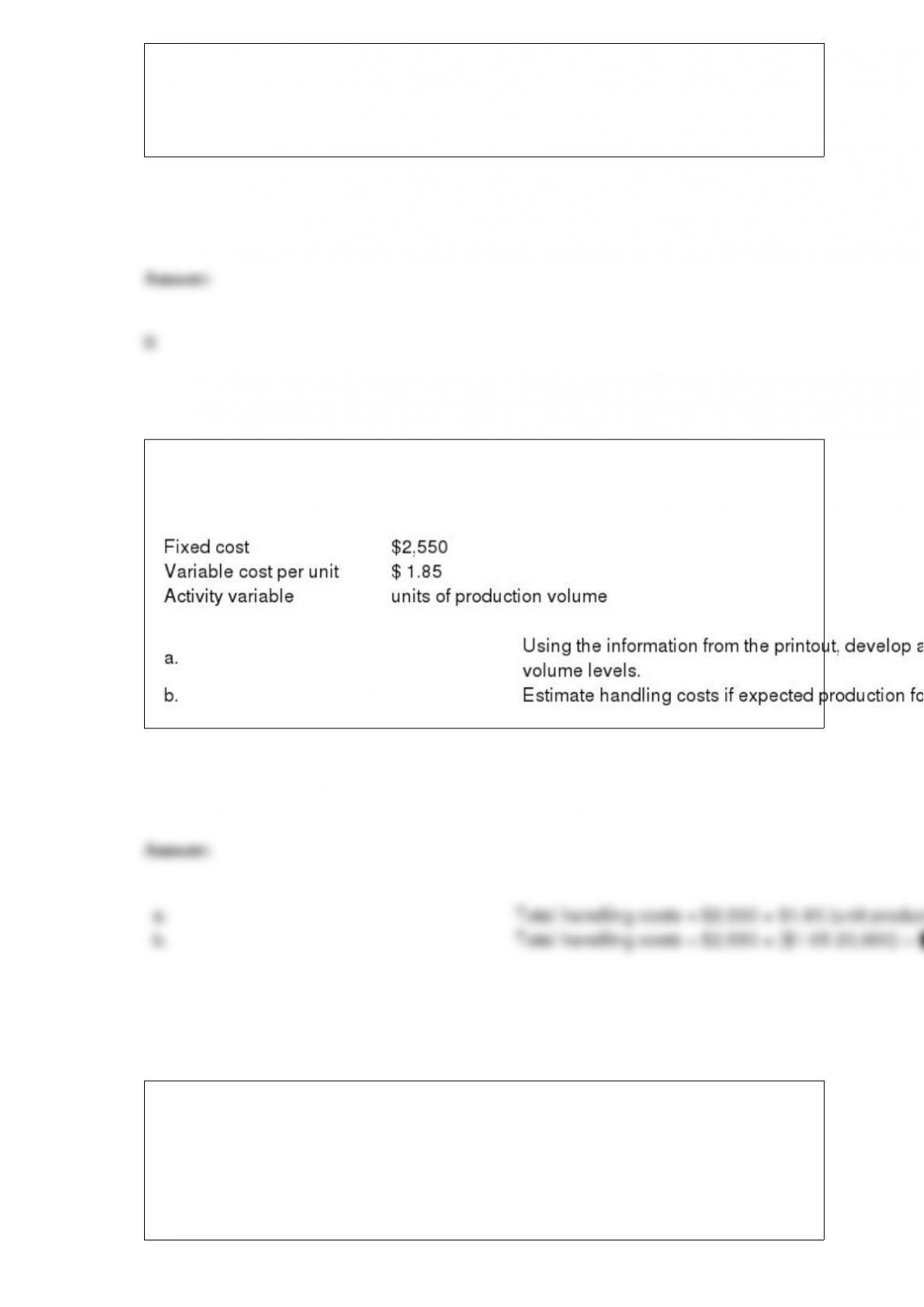

The facility manager of Tovar Corporation asked the systems analyst for information to

help in forecasting handling costs. The following printout was generated using the least

squares regression method.

In evaluating the performance of a profit center manager, the manager

a. and the sub-unit should be evaluated on the basis of the same costs and revenues.

b. should only be evaluated on the basis of variable costs and revenues of the sub-unit.

c. should be evaluated on all costs and revenues that are controllable by the manager

d. should be evaluated on all costs and revenues that can be directly traced to the

sub-unit.

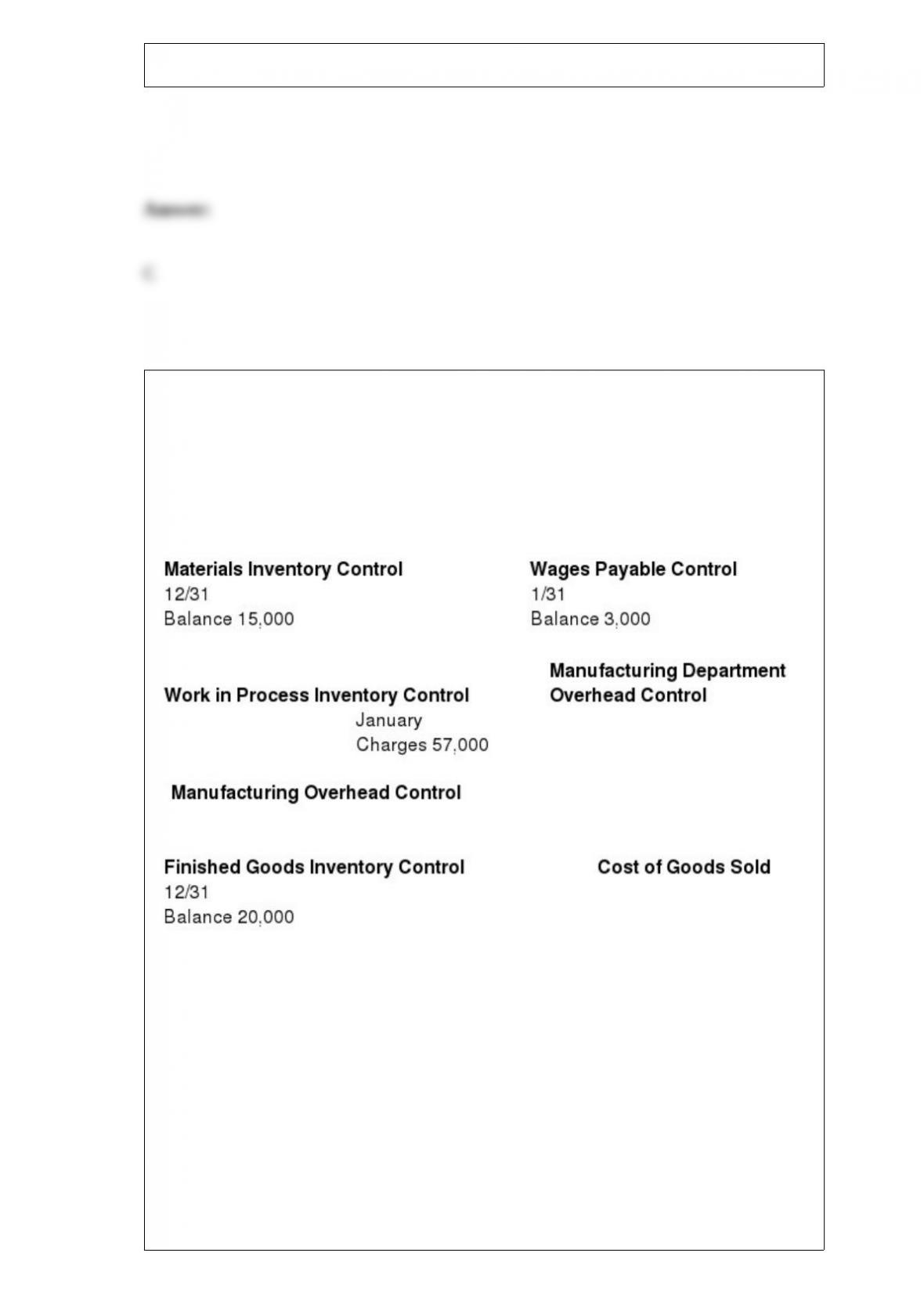

You are asked to bring the following incomplete accounts of Parrish Printing

Corporation up to date through January 31 of the current year. Consider the data that

appear in the T-accounts as well as additional information given in items (a) through (i).

Parrish’s job-order costing system has two direct cost categories (direct material and

direct manufacturing labor) and one indirect cost pool (manufacturing overhead, which

is allocated using direct manufacturing labor costs).

Additional Information:

a. Manufacturing department overhead is allocated using a budgeted rate set every

December. Management forecasts next year’s overhead and next year’s direct

manufacturing labor costs. The budget for the current year is $400,000 of direct

manufacturing labor and $600,000 of manufacturing overhead.

b. The only job unfinished on January 31 is No. 419, on which direct manufacturing

labor costs are $2,000 (125 direct manufacturing labor hours) and direct material costs

are $8,000.

c. Total material placed into production during January is $90,000.

d. Cost of goods completed during January is $180,000.

e. Material inventory as of January 31 is $20,000.

f. Finished goods inventory as of January 31 is $15,000.

g. All plant workers earn the same wage rate. Direct manufacturing labor hours for

January total 2,500. Other labor and supervision totals $10,000.

h. The gross plant payroll for January pay periods totals $52,000. Ignore withholdings.

All personnel are paid on a weekly basis.

i. All “actual” manufacturing department overhead incurred during January has already

been posted.

Required:

a. Material purchased during January

b. Cost of Goods Sold during January

c. Direct Manufacturing Labor Costs incurred during January

d. Manufacturing Overhead Allocated during January

e. Balance, Wages Payable Control, December 31, prior year

f. Balance, Work in Process Inventory Control, January 31, current year

g. Balance, Work in Process Inventory Control, December 31, prior year

h. Balance, Finished Goods Inventory Control, January 31, current year

i. Manufacturing Overhead underapplied or overapplied for January

Ineffectivebudgets and/or control systems are characterized by the use of

a. budgets as a planning tool only and disregarding them for control purposes.

b. budgets for motivation.

c. budgets for coordination.

d. the budget for communication.

The sum of the labor mix and labor yield variances equals

a. the labor efficiency variance.

b. the total labor variance.

c. the labor rate variance.

d. nothing because these two variances cannot be added since they use different costs.

The most valid reason for using something other than a full-cost-based transfer price

between units of a company is because a full-cost price

a. is typically more costly to implement.

b. does not ensure the control of costs of a supplying unit.

c. is not available unless market-based prices are available.

d. does not reflect the excess capacity of the supplying unit.

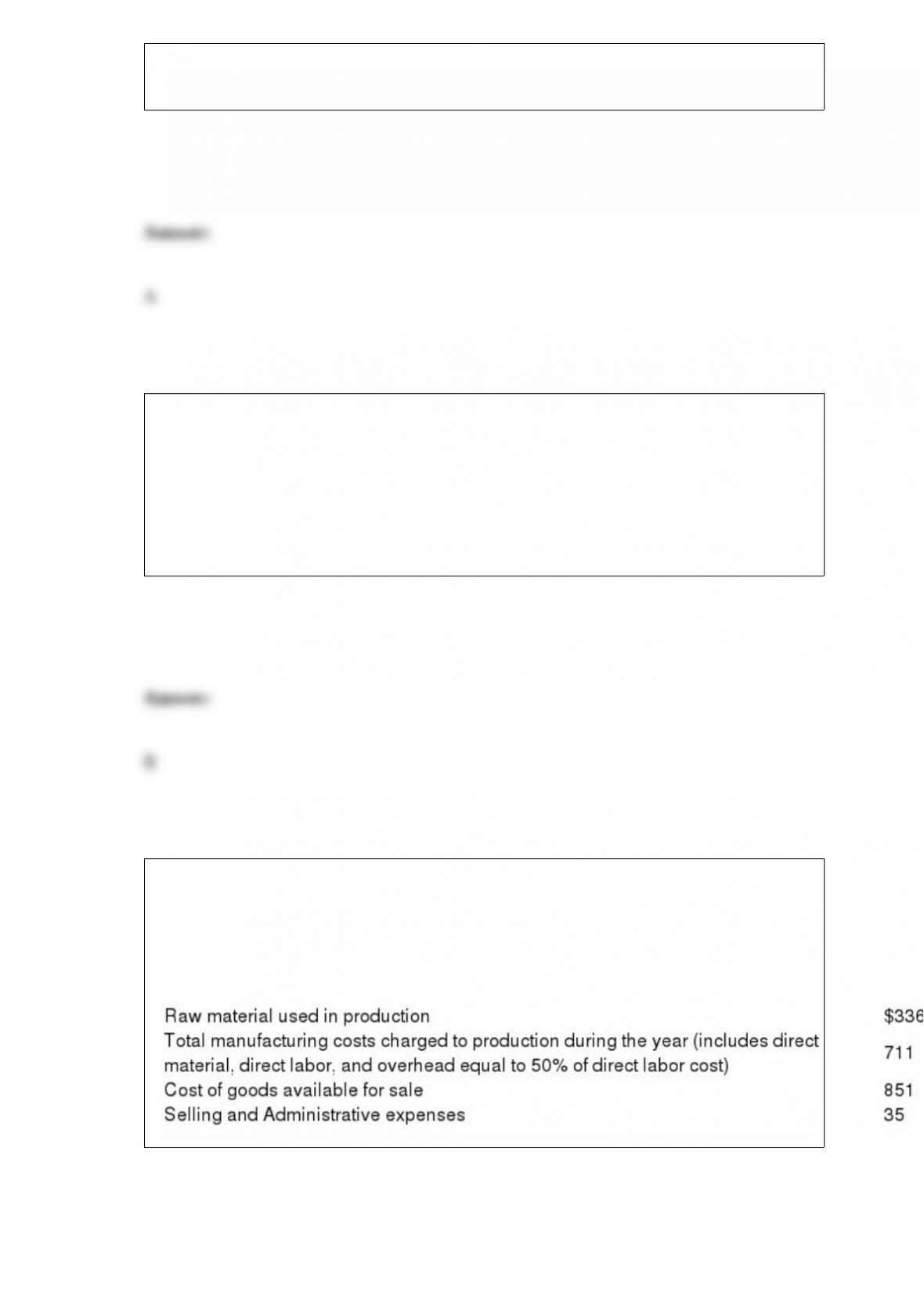

Bridges Corporation

The following information has been taken from the cost records of Bridges Corporation

for the past year:

Refer to Bridges Corporation. The cost of raw material purchased during the year was

a. $326.

b. $346

c. $375

d. $426

Key variables that are identified in strategic planning are

a. normally controllable if they are internal.

b. seldom if ever controllable.

c. normally controllable if they occur in a domestic market.

d. normally uncontrollable if they are internal.

The master budget is a

a. static budget.

b. flexible budget.

c. qualitative expression of a prior goal.

d. qualitative expression of a future goal.

Information concerning Thompson Corporation’s Product A follows:

Assuming that Thompson increased sales of Product A by 20 percent, what should the

profit from Product A be?

a. $20,000

b. $24,000

c. $32,000

d. $80,000

Moore Company.

Moore Company uses a job-order costing system and the following information is

available from its records. The company has three jobs in process: #6, #9, and #13.

Direct material was requisitioned as follows for each job respectively: 30 percent, 25

percent, and 25 percent; the balance of the requisitions was considered indirect. Direct

labor hours per job are 2,500; 3,100; and 4,200; respectively. Indirect labor is $33,000.

Other actual overhead costs totaled $36,000.

Refer to Moore Company. What is the prime cost of Job #6?

a. $42,250

b. $57,250

c. $73,250

d. $82,750

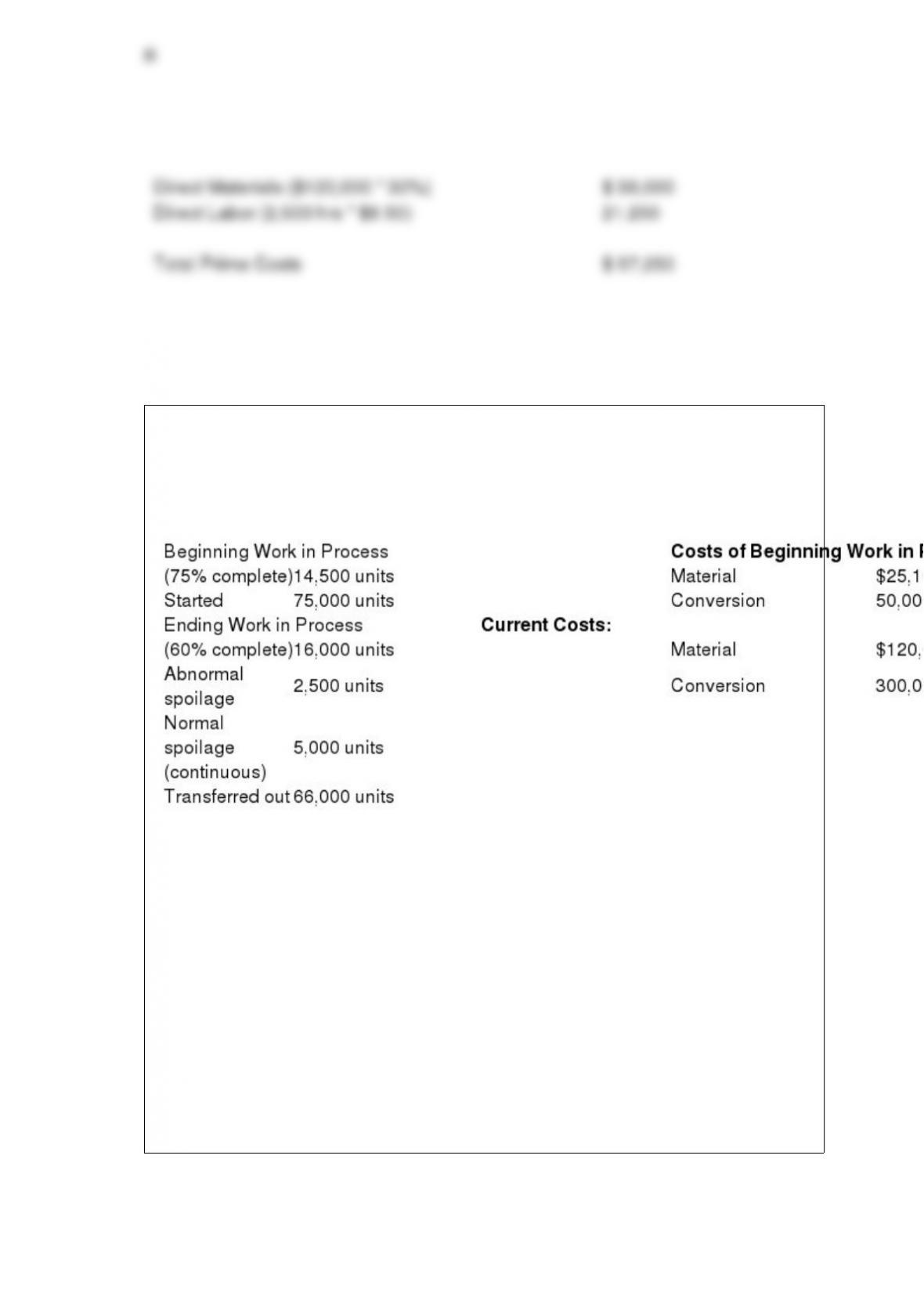

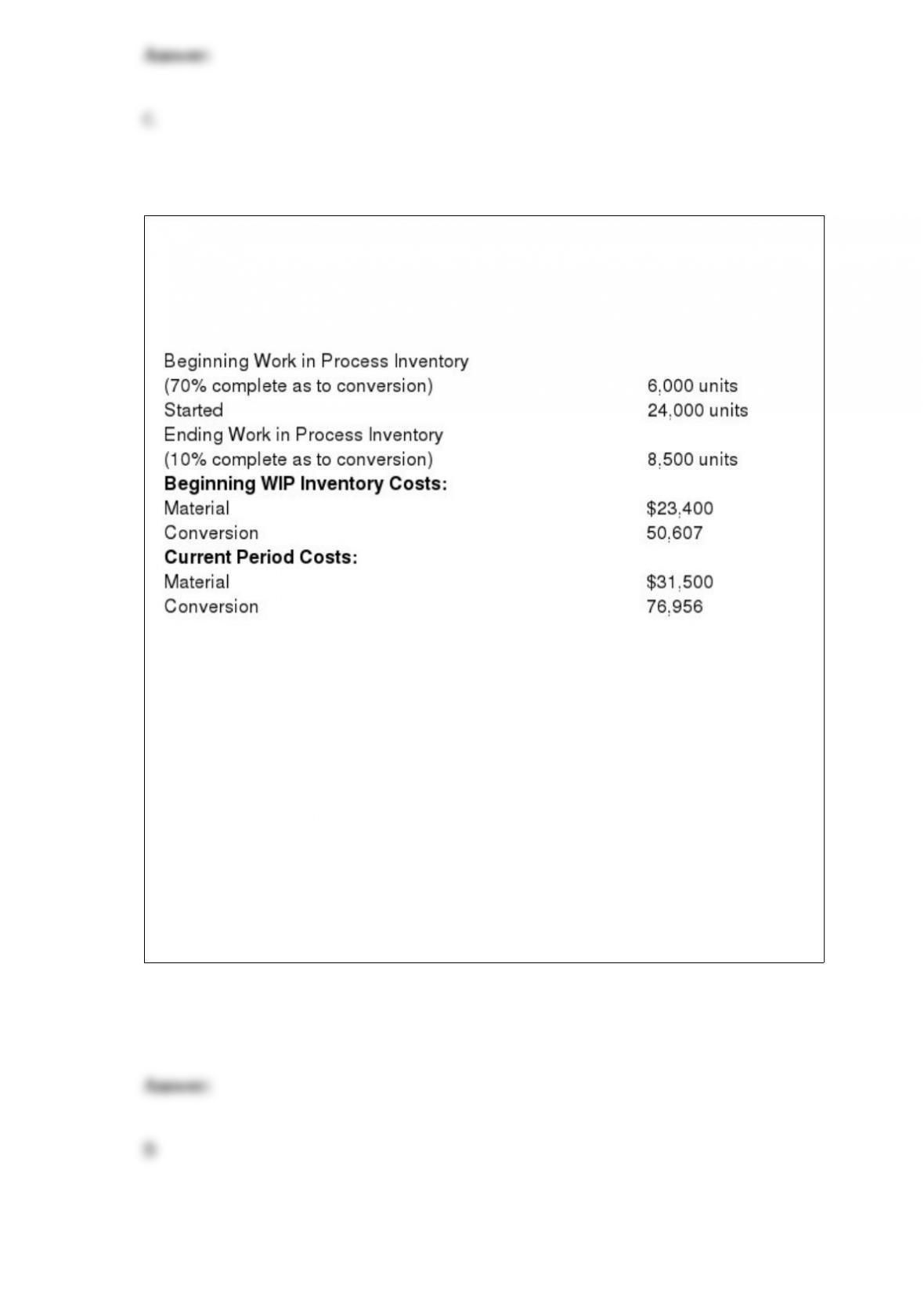

Stillwater Corporation

The following information is available for Stillwater Corporation for the current year:

All materials are added at the start of production.

Refer to Stillwater Corporation. Assume that the cost per EUP for material and

conversion are $1.75 and $4.55, respectively. What is the cost assigned to ending Work

in Process?

a. $100,800

b. $87,430

c. $103,180

d. $71,680

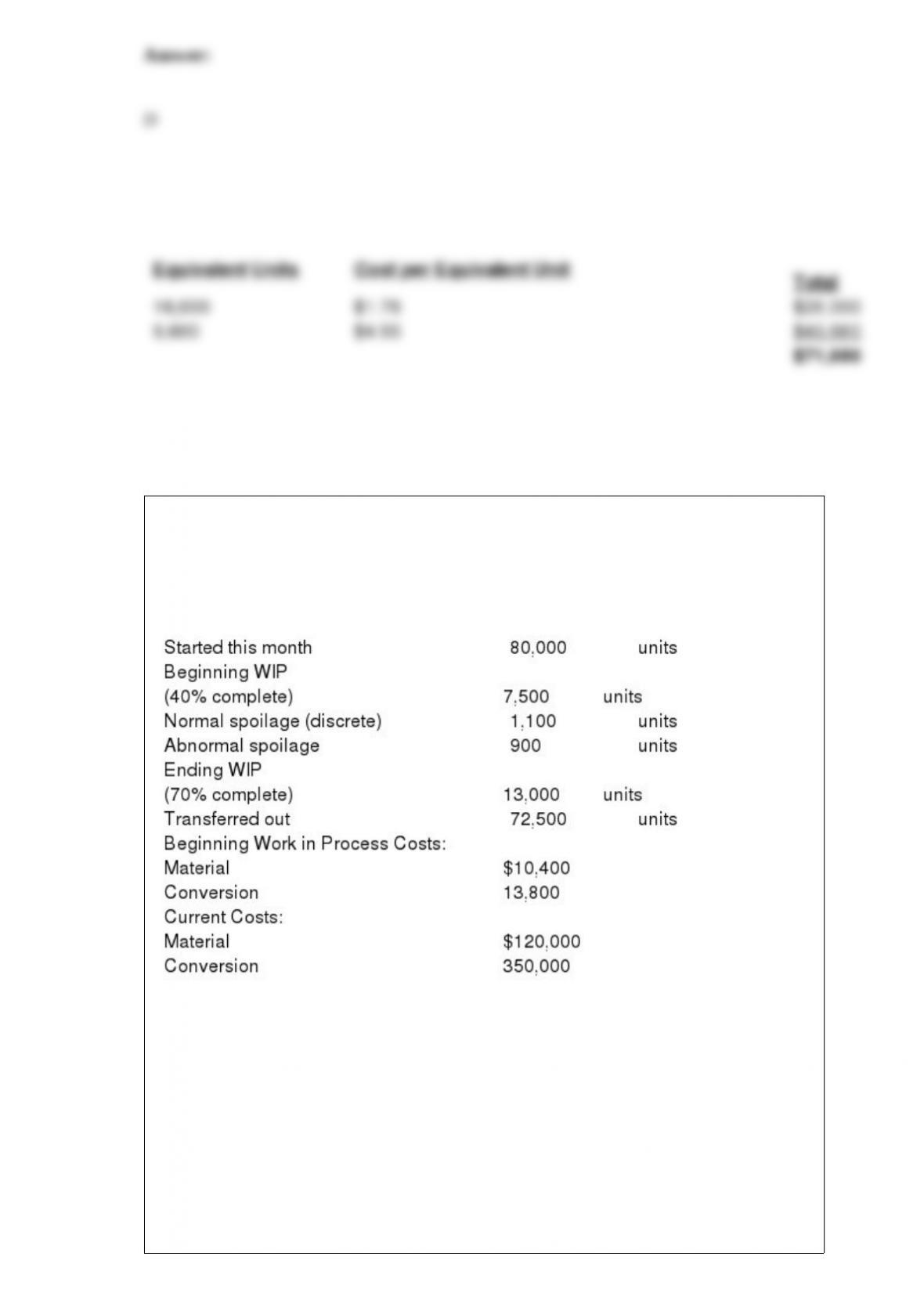

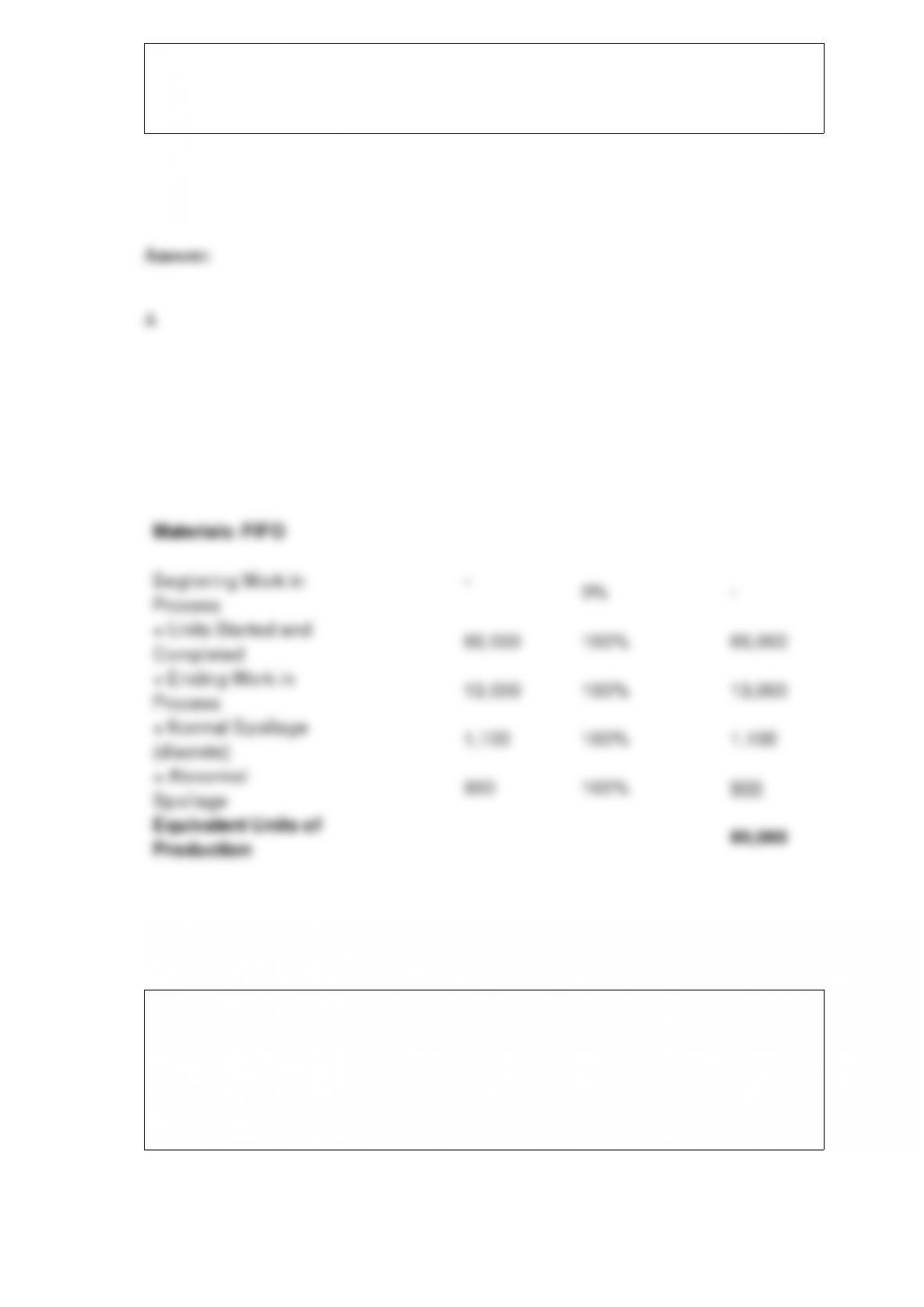

Grant Corporation

The following information is available for Grant Corporation for the current month:

All materials are added at the start of production and the inspection point is at the end

of the process.

Refer to Grant Corporation. What are equivalent units of production for material using

FIFO?

a. 80,000

b. 79,100

c. 78,900

d. 87,500

In the least-squares equation, y = a + bX, a represents

a. the coefficient of determination.

b. the level of activity.

c. the fixed component of a cost.

d. the variable cost per unit.

Fox Corporation

Fox Corporation. has the following information for August:

All material is added at the start of the process and all finished products are transferred

out.

Refer to Fox Corporation. Assume that FIFO process costing is used. What is the cost

per equivalent unit for conversion?

a. $3.44

b. $4.24

c. $5.71

d. $7.03

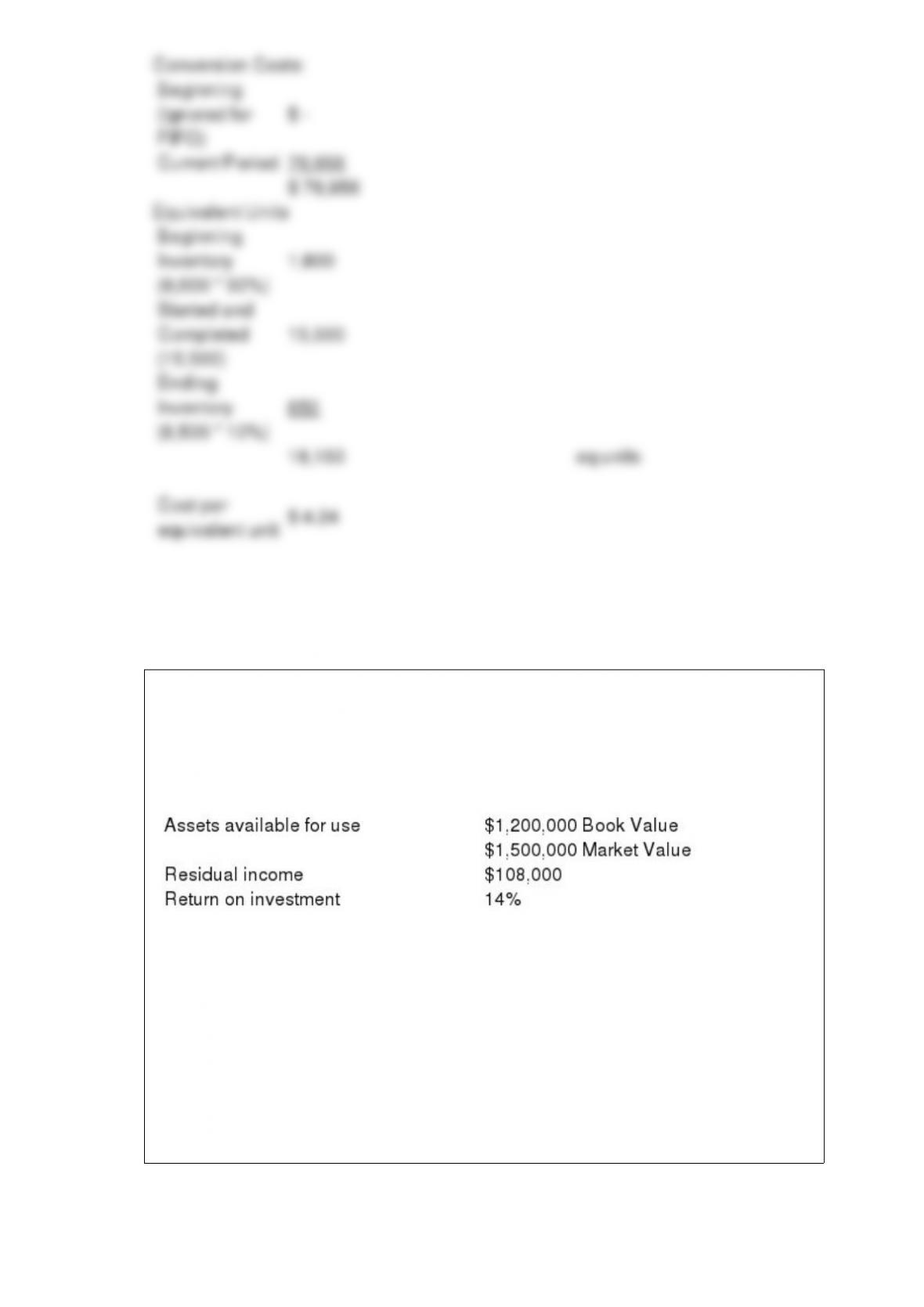

Thunder Sports Enterprises

The Basketball Division of Thunder Sports Enterprises reported the following financial

data for the year:

Refer to Thunder Sports Enterprises. What was the Basketball Division’s segment

income?

a. $168,000

b. $125,000

c. $269,000

d. $ 19,000

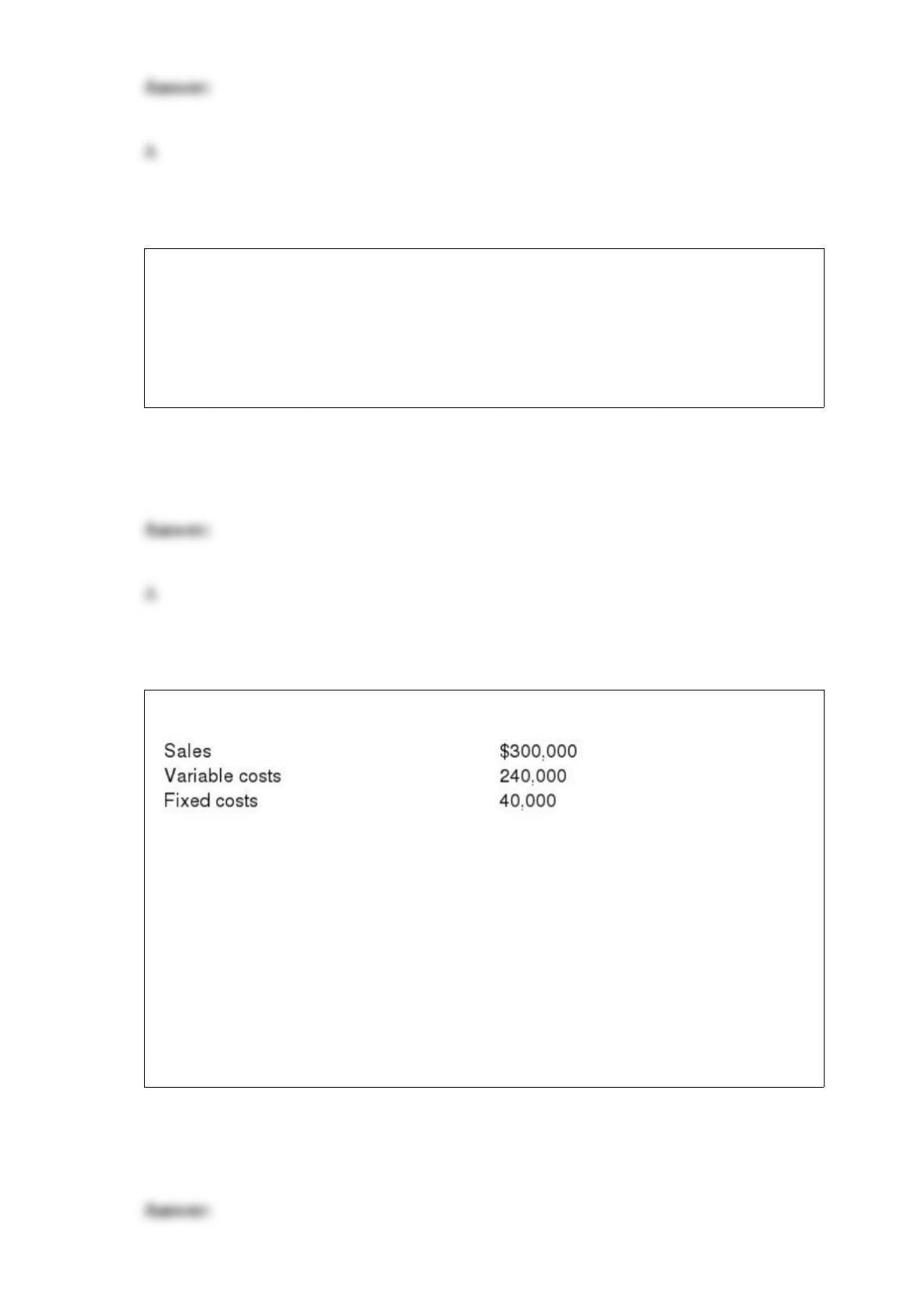

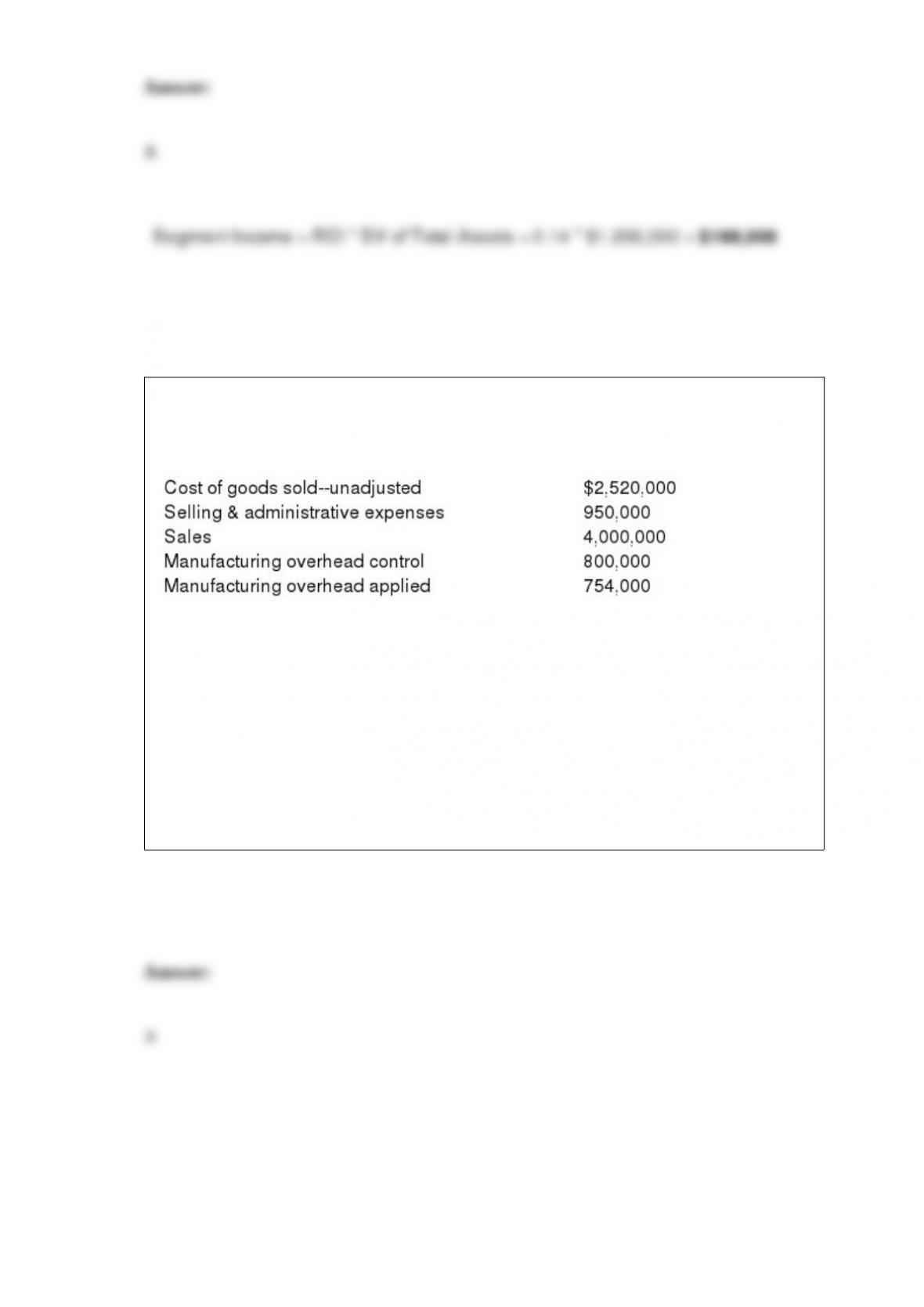

Sloane Products has no Work in Process or Finished Goods inventories at the close of

business on December 31 of the current year. The balances of Sloane Products’ accounts

as of December 31 are as follows:

Pretax income for the current year is:

a. $484,000

b. $530,000

c. $576,000

d. $680,000

The master budget is a static budget because it

a. is geared to only one level of production and sales.

b. never changes from one year to the next.

c. covers a preset period of time.

d. always contains the same operating and financial budgets.

All other factors equal, a large number is preferred to a smaller number for all capital

project evaluation measures except

a. net present value.

b. payback period.

c. internal rate of return.

d. profitability index.

When assessing performance, one way to compensate for differences among divisions

of a multinational organization would be for the parent company to

a. use different target rates of return to compute residual incomes.

b. modify the return on investment calculation so that foreign currency fluctuations are

removed from all financial statement figures.

c. classify all domestic divisions as investment centers and all foreign divisions as profit

centers.

d. use financial performance measures for units whose records are kept in the domestic

currency and non-financial measures for units whose records are kept in a foreign

currency.

Qualitative non-financial performance measures

a. are usually the most well-received by managers.

b. often reflect long-term organizational goals better than financial performance

measures.

c. can only be developed in the production area of an organization.

d. is limited by the number of critical success factors defined by the organization.

Which of the following would fall within the range of tolerance for a production cycle?

a. yes yes

b. yes no

c. no no

d. no yes

Cost of Goods Sold is an

a. unexpired product cost.

b. expired product cost.

c. unexpired period cost.

d. expired period cost.

The flow of goods through a production process cannot be at a faster rate than the

slowest bottleneck is the definition for

a. mass customization.

b. business process reengineering.

c. the theory of constraints.

d. the Pareto principle.

The amount of raw material purchased in a period may be different than the amount of

material used that period because

a. the number of units sold may be different from the number of units produced.

b. finished goods inventory may fluctuate during the period.

c. the raw material inventory may increase/decrease during the period.

d. companies often pay for material in the period after it is purchased.

The performance measurement system should encourage each manager to act in a

manner that

a. makes the manager’s units profits as high as possible.

b. most positively supports the organization’s mission and competitive strategies.

c. increases his/her performance reward in the form of profit sharing.

d. reduces the need for informational elements in support of the manager’s planning

function.

A balanced scorecard

a. records the variances between budgeted and actual revenues and expenses.

b. can be used at multiple organizational levels by redefining the categories and

measurements.

c. is most concerned with organizational financial solvency and business processes.

d. all of the above.

Reed Company

Reed Company produces 50,000 units of Product Q and 6,000 units of Product Z during

a period. In that period, four set-ups were required for color changes. All units of

Product Q are black, which is the color in the process at the beginning of the period. A

set-up was made for 1,000 blue units of Product Z; a set-up was made for 4,500 red

units of Product Z; a set-up was made for 500 green units of Product Z. A set-up was

then made to return the process to its standard black coloration and the units of Product

Q were run. Each set-up costs $500.

Refer to Reed Company. Assume that Reed Company has decided to allocate overhead

costs using levels of cost drivers. What would be the approximate per-unit set-up cost

for the green units of Product Z?

a. $1.00.

b. $0.25.

c. $0.04.

d. None of the responses are correct.

A company will not achieve world-class status unless a quality focus

a. allows that company to achieve one or more major quality awards.

b. becomes an integral part of the organization’s culture.

c. emphasizes the elimination of all quality costs for compliance and noncompliance.

d. has been mandated by management for workers to pursue.

Which of the following would be classified as a non-financial critical success factor?

a. no no no

yes

b. yes no no

no

c. yes yes yes

yes

d. yes yes no

yes

Perry Corporation is composed of three operating divisions. Overall, the Perry

Corporation has a return on investment of 20%. Division A has a return on investment

of 25%. If Perry Corporation. evaluates its managers on the basis of return on

investment, how would the Division A manager and the Perry Corporation president

react to a new investment that has an estimated return on investment of 23%?

a. accept accept

b. accept reject

c. reject accept

d. reject reject

Cost accounting serves as a bridge between financial and managerial accounting.

Activity-based costing conforms to GAAP with regard to which costs should be

expensed.

Joint costs occur before the split-off point in a production process.

The high-low method excludesoutliers from the calculation of the slope of a regression

line.

Costs that can be conveniently traced to a cost object are referred to as

____________________ costs.

The budget is an important source of feedback for an organization.

In a pull system of production control, inventory is produced in anticipation of

customer or work center demand.

Decentralization is a transfer of authority from the bottom to the top of an organization.

What does the term “pull” mean in the context of production control?

When a flexible manufacturing system (FMS) is used, worker tasks are more diverse

than under a traditional manufacturing system.

When using the risk-adjusted discount rate method, a manager increases the rate used

for discounting future cash outflows.

When a company has work performed by an external supplier, it is engaging in

____________________.

Discuss the application of the high-low method.

The ratio of income to assets invested is referred to as

___________________________________.

A budget variance is a controllable variance.