On the last day of the month, a company receives $8,000 of cash from customers. Of

that amount, $1,000 was for services performed and $7,000 represented payments on

account. The journal entry to record the $8,000 cash receipt would include a debit to:

A) Accounts Receivable for $7,000, a debit to Service Revenue for $1,000, and a credit

for $8,000 to Cash.

B) Cash for $8,000, a credit to Accounts Receivable for $7,000, and a credit to Service

Revenue for $1,000.

C) Accounts Receivable for $7,000, a debit to Unearned Revenue for $1,000, and a

credit to Cash for $8,000.

D) Cash for $8,000, a debit to Service Revenue for $1,000, and a credit to Accounts

Receivable for $7,000.

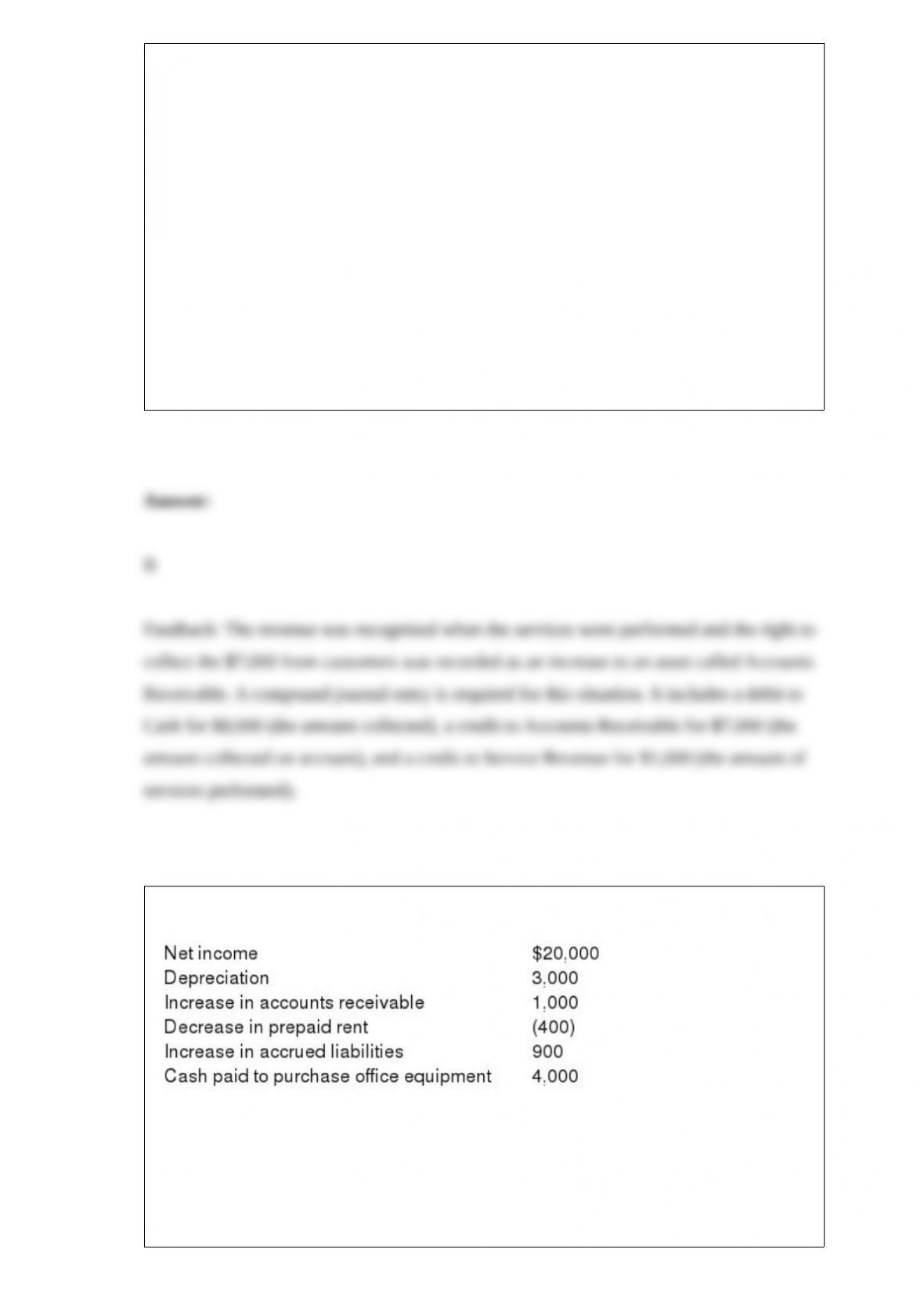

Consider the following information:

What is the net cash provided by operating activities?

A) $17,500

B) $18,500

C) $21,500

D) $23,300

Indicate whether each of the following items is a characteristic of the allowance method

and/or the direct write-off method by placing an “X” in the appropriate column. If an

item is a characteristic of both methods, place an “X” in both columns.

Allowance Method Direct Write-off Method

a. Conforms to the expense recognition (matching) principle.

b. Not used very often for external financial reporting.

c. Required for tax purposes.

d. Required by IFRS.

e. Reports receivables at their net realizable value.

f. May overstate assets.

g. Distorts net income in the period of the sale as well as in later periods when bad

debts are discovered.

h. Estimates amount of uncollectibles using percentage of net sales or an aging of

receivables.

i. Bad Debt Expense is debited when the company estimates its uncollectible accounts.

j. Requires an adjusting entry that uses a contra account.

k. Accounts Receivable is credited when a customer account is written off.

l. Bad Debt Expense is debited when a customer account is written off.

m. The write off of a customer’s account affects only balance sheet accounts.

n. Decreases net income when an uncollectible account is written off.

n. Not considered a generally accepted accounting method.

The book value of a long-lived tangible asset is equal to:

A) its acquisition cost less the accumulated depreciation from the acquisition date to the

balance sheet date.

B) its acquisition cost plus accumulated depreciation from the acquisition date to the

balance sheet date.

C) the amount that could be obtained for the asset on the balance sheet date if it were

sold.

D) the annual cost of carrying the asset in inventory.

Multistep income statements:

A) are required for merchandise companies.

B) contain more detail than just listing revenues and expenses.

C) are required when the perpetual inventory method is used.

D) classify Cost of Goods Sold as a selling expense.

Jay-Cee Corporation had 20,000 shares of $4 par value common stock outstanding on

January 1. On January 20, the company purchased 2,000 of its stock for $16 per share.

On July 3, the company reissued 1,000 of the shares at $20 per share. Jay-Cee uses the

cost method to account for its treasury stock. Assume the company paid a dividend of

$5 per share on August 3. What is the total amount of the dividends that would be paid

to the common stockholders?

A) $95,000

B) $100,000

C) $90,000

D) $76,000

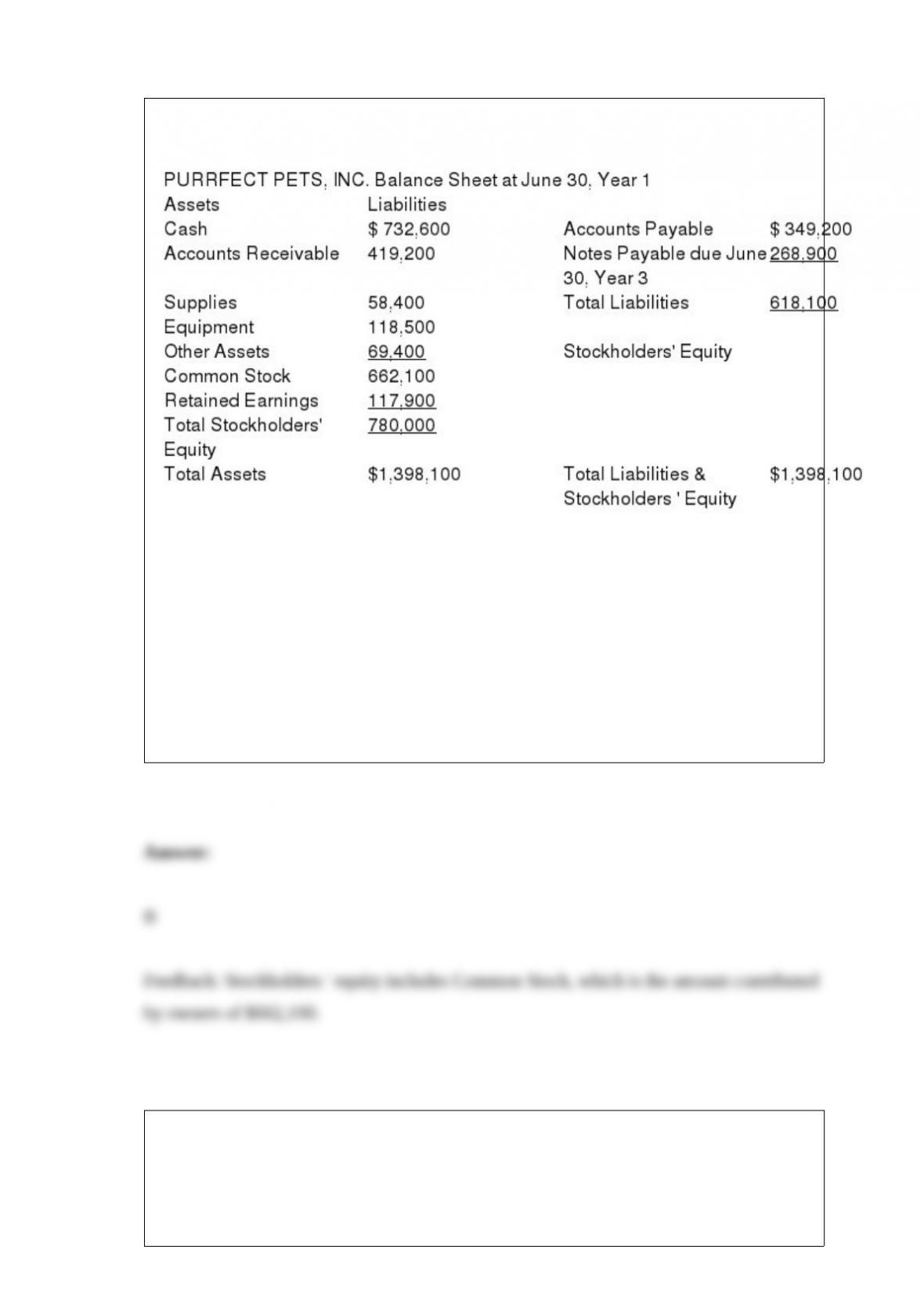

Use the information above to answer the following question. How much financing did

the stockholders of Purrfect Pets, Inc. directly contribute to the company?

A) $117,900.

B) $662,100.

C) $780,000.

D) $1,398,100.

Which of the following would not affect a company’s net income?

A) A change in the company’s income taxes

B) Changing the selling price of a company’s product

C) Paying a dividend to stockholders

D) Advertising a new product

Bailey Company uses a periodic inventory system and its inventory records contain the

following information:

The company sold 1,000 units during June. There were no additional purchases or sales

during the remainder of the year. The company had 500 units were in its ending

inventory at the end of the year.

Use the information above to answer the following question. If Bailey Company uses

the weighted average inventory costing method, what is the cost of its ending

inventory? (Round the per unit cost to two decimal places and then round your answer

to the nearest whole dollar.)

A) $4,200

B) $2,700

C) $1,400

D) $1,365

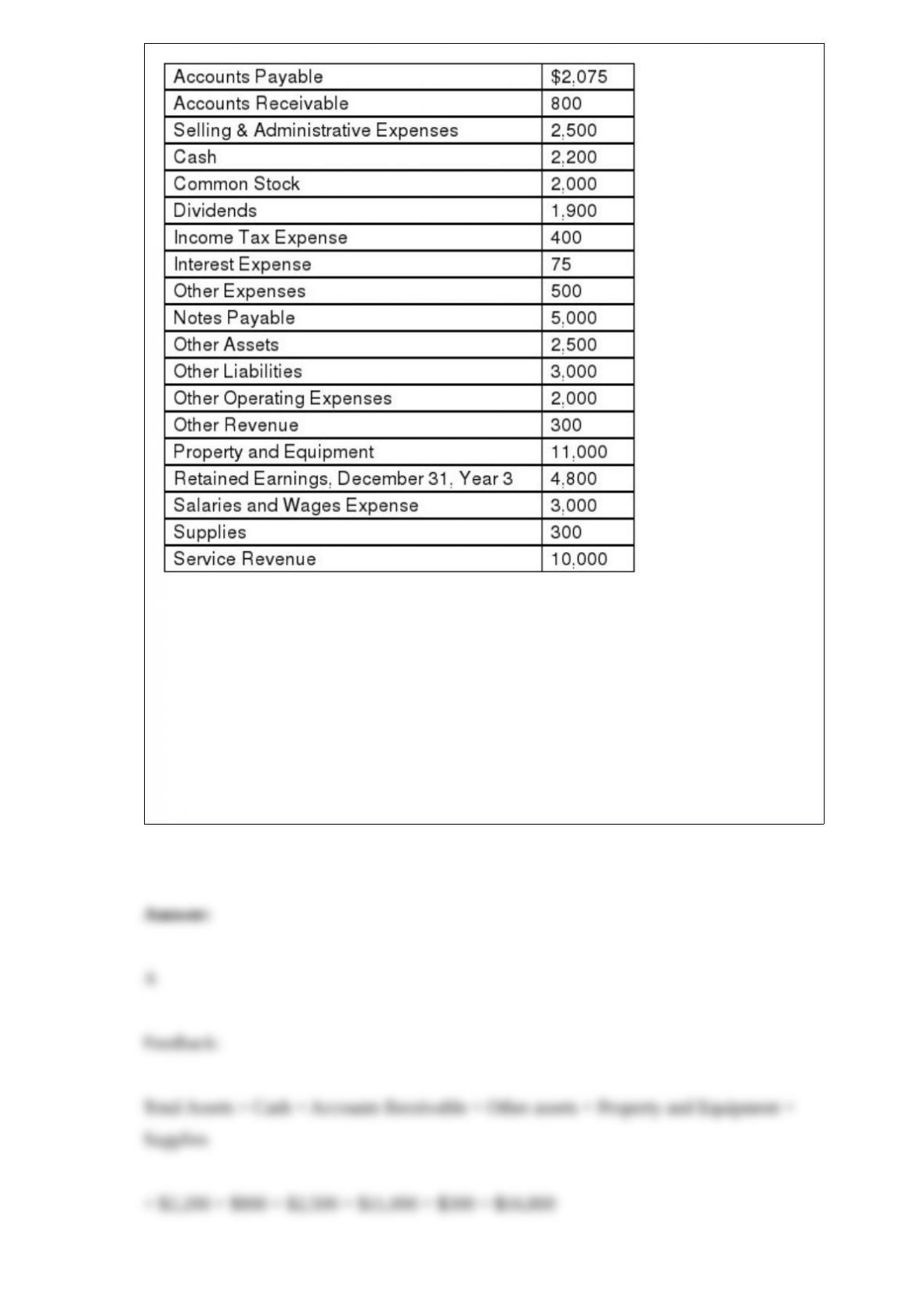

The following accounts are taken from the December 31, Year 4 financial statements of

a company.

Use the information above to answer the following question. What is the amount of

total assets at the end of Year 4?

A) $16,800.

B) $16,500.

C) $21,600.

D) $23,500.

On September 1, a corporation with 50,000 shares of $5 par value common stock and

$1,000,000 of Retained Earnings issues a 2-for-1 stock split. The market price of the

stock on that date is $12 per share. Which of the following statements is correct

concerning this stock split?

A) Contributed capital will increase by $250,000.

B) Retained Earnings will decrease by $600,000.

C) Dividends payable will increase by 250,000.

D) No entry will be made for this transaction.

Free cash flow may be used for all of the following except:

A) expanding the business.

B) paying off debt.

C) building up the cash balance.

D) paying employees.

McEwan Company has outstanding 10 million shares of $2 par value common stock

and 1 million shares of $4 par value preferred stock. The preferred stock is

noncumulative and has a 7% current dividend preference. The company declares total

dividends amounting to $50,000, $250,000, and $600,000 during 2015, 2016, and 2017,

respectively.

Required:

Part a. Compute the amount of dividends to be distributed to preferred and common

shareholders during 2015.

Part b. Compute the amount of dividends to be distributed to preferred and common

shareholders during 2016.

Part c. Compute the amount of dividends to be distributed to preferred and common

shareholders during 2017.

Choose the appropriate letter to match the term and the definition. There are more

definitions than terms.

Term

1> ____ Fraud

2>____ Imprest System

3>____ Internal Control

4> ____ Loan Covenants

5>____ Sarbanes-Oxley Act (SOX)

6>____ Segregation of Duties

7> ____ Voucher System

Definition

A. A process for approving and documenting all purchases and payments on account.

B. A process that controls the amount paid to others by limiting the total amount of

money available for making payments to others.

C. A set of regulations passed by Congress in 2002 in an attempt to improve financial

reporting and restore investor confidence.

D. Actions taken to promote efficient and effective operations, protect assets, enhance

accounting information, and adhere to laws and regulations.

E. An attempt to deceive others for personal gain.

F. An internal control designed into the accounting system to prevent an employee from

making a mistake or committing a dishonest act as part of one assigned duty and then

also covering it up through another assigned duty.

G. An internal report prepared to verify the accuracy of both the bank statement and the

cash accounts of a business or individual.

H. Another name for bounced checks. They arise when the check writer (your

customer) does not have sufficient funds to cover the amount of the check.

I. Money or any instrument that banks will accept for deposit and immediately credit to

a company ‘s account.

J. Not available for general use but rather restricted for a specific purpose.

K. Short-term, highly liquid investments purchased within three months of maturity.

L. Terms of a loan agreement that if broken, entitle the lender to renegotiate loan terms

or force repayment.

An adjusting journal entry that includes an increase to an asset contra-account would

also include an increase in a(n):

A) related asset account.

B) liability account.

C) revenue account.

D) expense account.

Your company’s president donates a large amount of her own money to charity and

receives significant publicity that includes the company’s name. How would the

benefits of this publicity appear on the balance sheet?

A) It would appear as a current asset.

B) It would appear as Common Stock.

C) It would appear as a noncurrent asset.

D) It would not appear on the balance sheet.

The attitude that people in the organization hold regarding internal control is referred to

as the:

A) control environment.

B) control atmosphere.

C) risk assessment.

D) monitoring activities.