The Cash account in the ledger of Hensley, Inc. showed a balance of $3,100 at June 30.

The bank statement, however, showed a balance of $3,900 at the same date. The only

reconciling items consisted of a $700 deposit in transit, a bank service charge of $7, and

a large number of outstanding checks.

Refer to the information above. Upon completion of the bank reconciliation, a journal

entry will be required to update the depositor’s accounting records. This entry will

include a:

A. Credit to Cash for $700.

B. Debit to Cash for $700.

C. Debit to Cash for $7.

D. Debit to Bank Service Charge Expense for $7.

When a corporation issues capital stock at a price higher than the par value:

A. The amount received over par value increases retained earnings.

B. The entire issue price is credited to the Capital Stock account.

C. The amount received in excess of par value constitutes profit to the issuing

corporation.

D. The amount received in excess of par value becomes part of paid-in capital.

The accounting principle that assumes that a company will operate in the foreseeable

future is:

A. Going concern.

B. Objectivity.

C. Liquidity.

D. Disclosure.

A journal entry to recognize an expense could include each of the following, except:

A. A debit to an expense account.

B. A credit to Accounts Payable.

C. A debit to a liability account.

D. A credit to Cash.

If sales are $540,000, expenses are $440,000 and dividends are $50,000, Income

Summary:

A. Will have a credit balance of $50,000.

B. Will have a debit balance of $50,000.

C. Will have a debit balance of $100,000.

D. Will have a credit balance of $100,000.

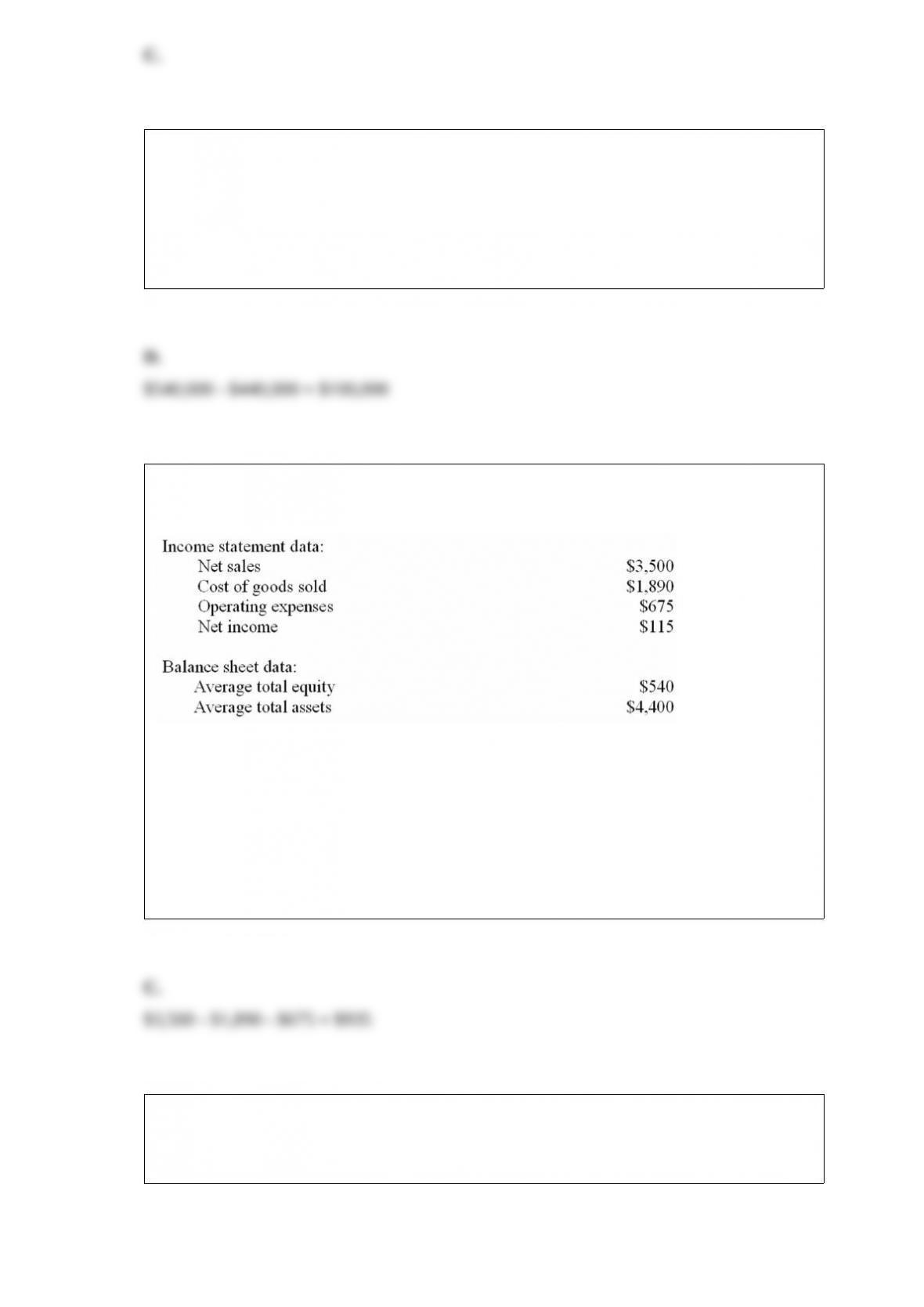

Shown below are selected data from the financial statements of Noble Computers.

(Dollar amounts are in millions, except for the per share data.)

Noble reported earnings per share for the year of $6 and paid cash dividends of $2.00

per share. At year-end, the Wall Street Journal listed Noble’s capital stock as trading at

$81 per share.

Refer to the information above. Noble’s operating income was:

A. $1,610.

B. $675.

C. $935.

D. $115.

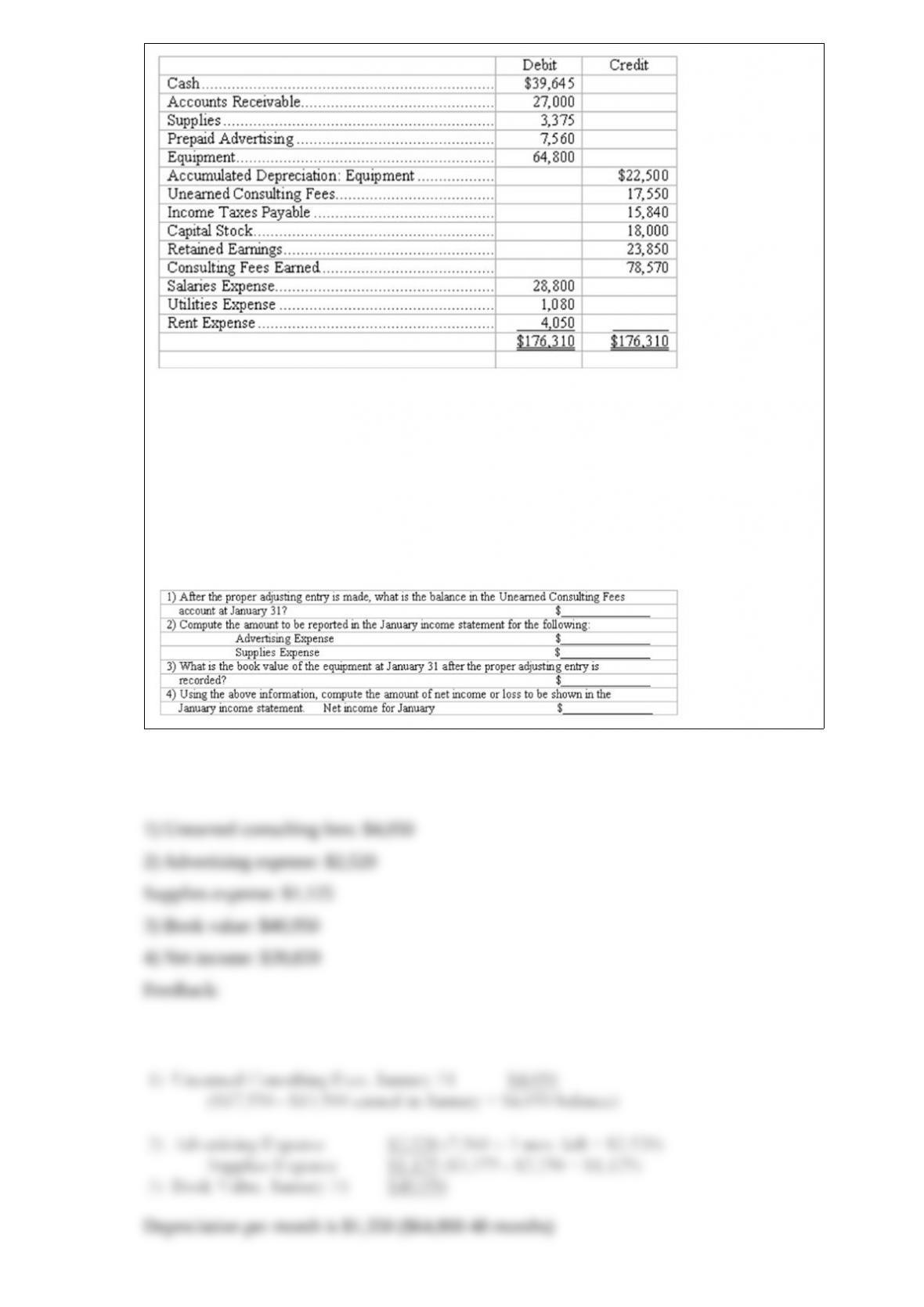

End-of-period adjustments – selected computations

Allied Architects adjusts its books each month and closes its books at the end of the

year. The trial balance at January 31, 2015, before adjustments is as follows:

The following information relates to month-end adjustments:

(a) According to contracts, consulting fees received in advance that were earned in

January total $13,500.

(b) On November 1, 2015, the company paid in advance for 5 months’ advertising in

professional journals.

(c) At January 31, supplies on hand amount to $2,250.

(d) The equipment has an original estimated useful life of 4 years.

(e) The corporation is subject to income taxes of 25% of taxable income. (Assume

taxable income is the same as “income before taxes.”)

All of the following ratios are considered measures of profitability except:

A. Earnings per share.

B. Gross profit rate.

C. Price earnings ratio.

D. Return on assets.

The section of the annual report titled “Management Discussion and Analysis” is:

A. Required by the SEC.

B. Not required but may be included by management.

C. Required by GAAP.

D. Reported to the SEC but not included in the annual report.

Bernice Beverages is not satisfied with the quality of merchandise purchased from

Reade Supplies. If Reade Supplies agrees to settle this matter by granting Bernice

Beverages a sales allowance, Bernice Beverages will:

A. Return the entire shipment to Reade Supplies and receive a full refund.

B. Return only that portion of the merchandise that it is unable to sell within the

discount period.

C. Keep the merchandise, but pay a reduced purchase price.

D. Keep the merchandise and sell it at a reduced sales price.

A system that considers the earnings per sales dollar and the investment used to

generate those sales dollars is called:

A. The economic value added system.

B. The balanced scorecard system.

C. The DuPont system.

D. The residual income system.

Treasury stock should most often be recorded:

A. At cost.

B. Par value.

C. Fair market value at year end.

D. Face value.

Responsibility for selection of the depreciation methods used in financial reporting rests

with:

A. Company management.

B. The FASB.

C. The IRS.

D. The CPA firm that audits the company’s financial statements.

A capital lease is recorded in the accounting records of the lessee by an entry:

A. Debiting Rent Expense and crediting Cash each time a lease payment is made.

B. Debiting Cash and crediting Rental Revenue each time a lease payment is received.

C. Debiting an asset account and crediting a liability account for the present value of

the future lease payments.

D. Debiting an asset account and crediting Sales for the present value of the future lease

payments.

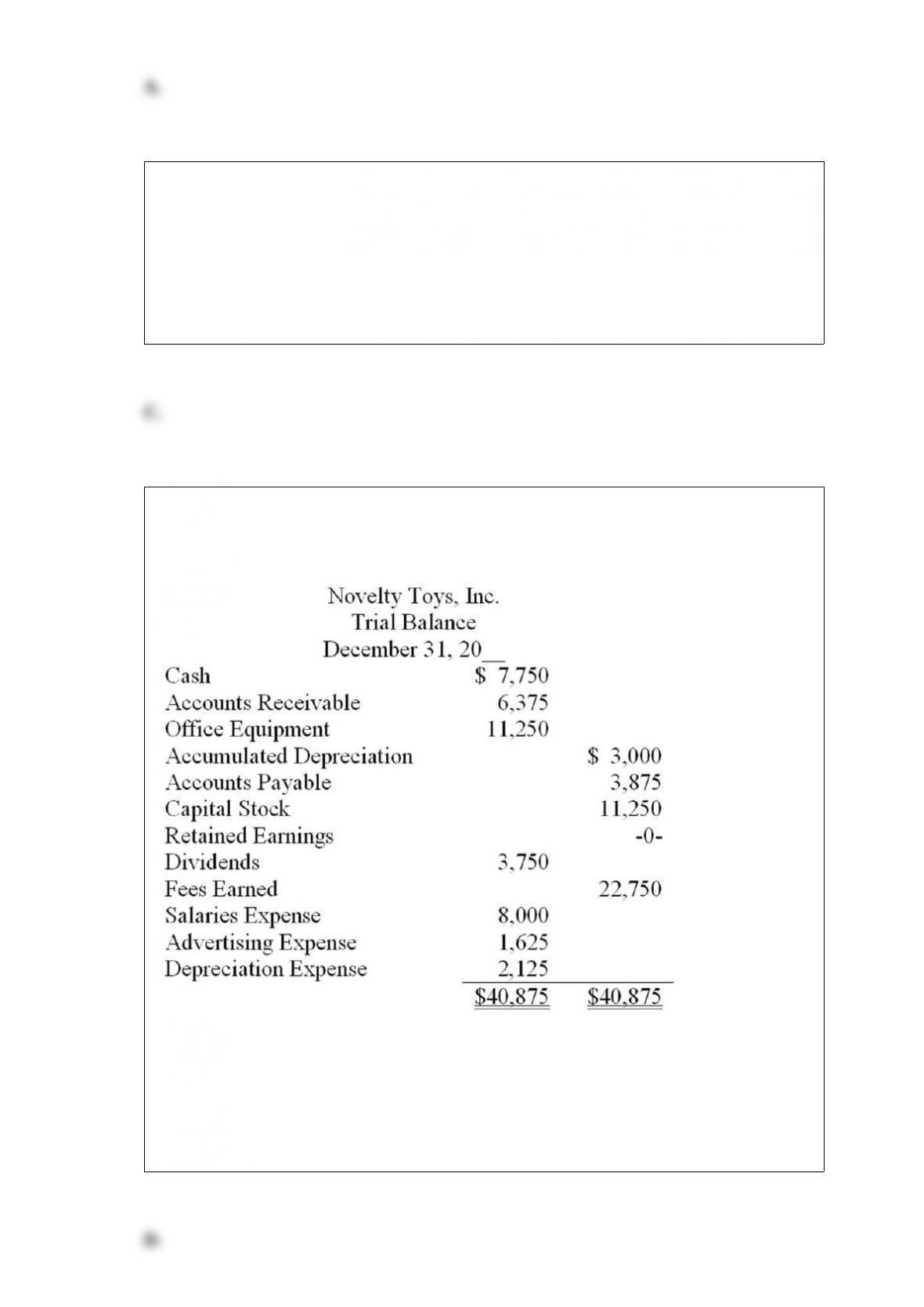

Shown below is a trial balance for Novelty Toys Inc., on December 31, after adjusting

entries:

Refer to the information above. Income Summary will have what balance before it is

closed?

A. Zero.

B. $11,750.

C. $7,250.

D. $11,000.

Which of the following would indicate a cash disbursement?

A. Selling equipment at a loss.

B. A decrease in accounts receivable.

C. An increase in prepaid expenses.

D. A decrease in inventory.

Which of the following would be classified as an extraordinary item?

A. A large gift given to the company.

B. A loss from obsolete inventory.

C. A loss from a natural disaster that affects the company at infrequent intervals.

D. A loss from an enacted law that made inventory unsalable.

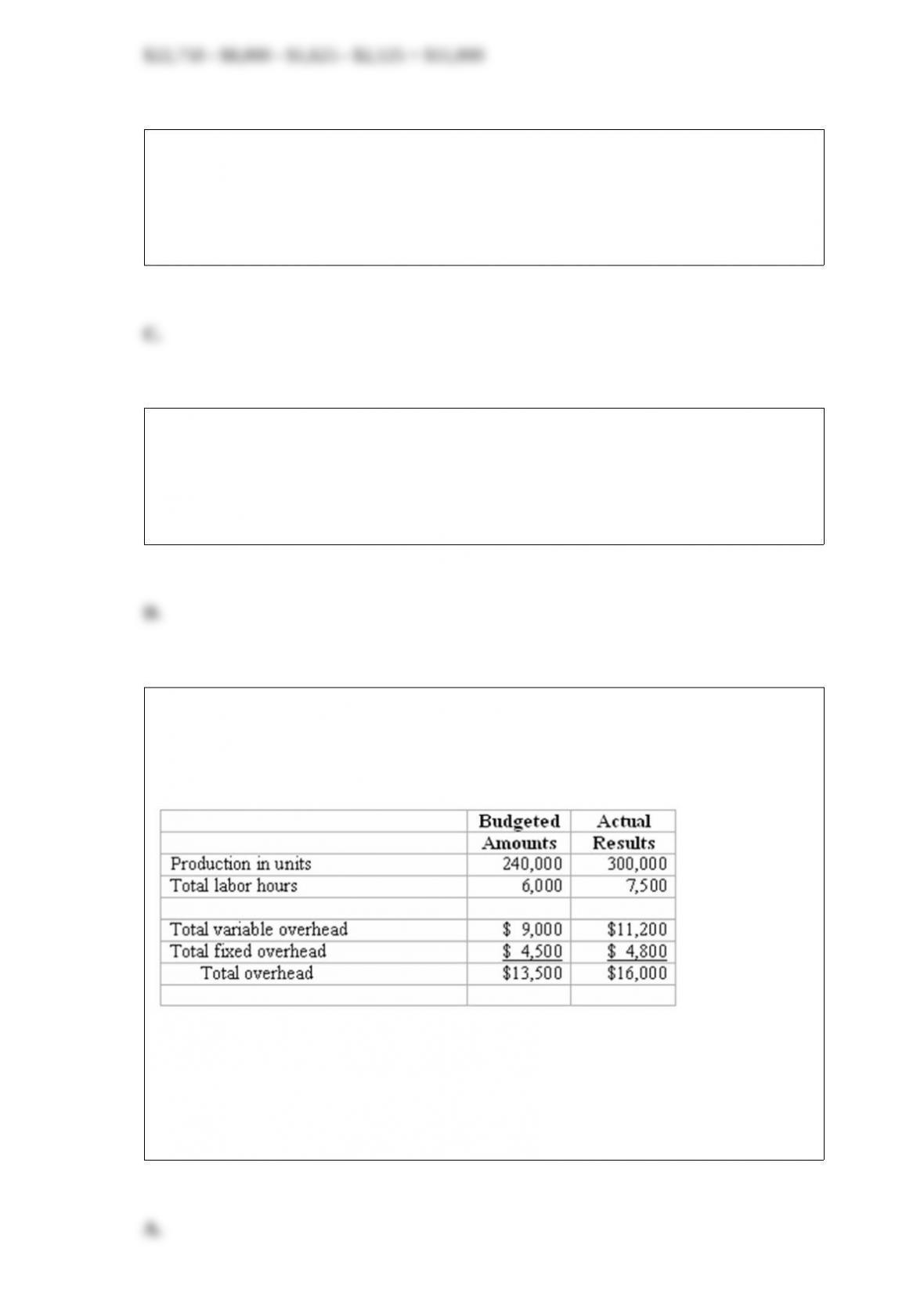

Cooper Corporation produces decorator wall coverings. Budgeted production is

240,000 square feet per month, and the standard direct labor requirement to make this

amount is 6,000 hours. All overhead is allocated based on direct labor hours. The

following information is available:

Refer to the information above. The overhead spending variance for the month in

question was:

A. $250 unfavorable.

B. $2,500 unfavorable.

C. $875 favorable.

D. $3,375 unfavorable.

Collection of an accounts receivable:

A. Increases the total assets of a company.

B. Decreases the total assets of a company.

C. Does not change the total assets of a company.

D. Reduces a company’s total liabilities.

Unique Corp. had 50,000 shares of $5 preferred stock, $100 par, and 100,000 shares of

$1 par common stock outstanding throughout the year. Net income for the year was

$780,000, and Unique declared and distributed a cash dividend of $1 per share on its

common stock. Earnings per share amounted to:

A. $7.80.

B. $1.00.

C. $5.30.

D. $2.30.

Large stock dividends tend to:

A. Increase stock prices.

B. Have no effect upon stock prices.

C. Keep stock prices down.

D. Decrease total assets.

Omega Company adjusts its accounts at the end of each month. The following

information has been assembled in order to prepare the required adjusting entries at

December 31:

(1) A one-year bank loan of $720,000 at an annual interest rate of 12% had been

obtained on December 1.

(2) The company pays all employees up-to-date each Friday. Since December 31 fell on

Tuesday, there was a liability to employees at December 31 for two day’s pay

amounting to $6,800.

(3) On December 1, rent on the office building had been paid for four months. The

monthly rent is $6,000.

(4) Depreciation of office equipment is based on an estimated useful life of six years.

The balance in the Office Equipment account is $9,360; no change has occurred in the

account during the year.

(5) Fees of $9,800 were earned during the month for clients who had paid in advance.

Refer to the information above. After the appropriate adjusting entry is recorded, the

balance in the liability account Unearned Fees will:

A. Decrease by $9,800.

B. Increase by $9,800.

C. Equal $9,800.

D. Be unaffected.

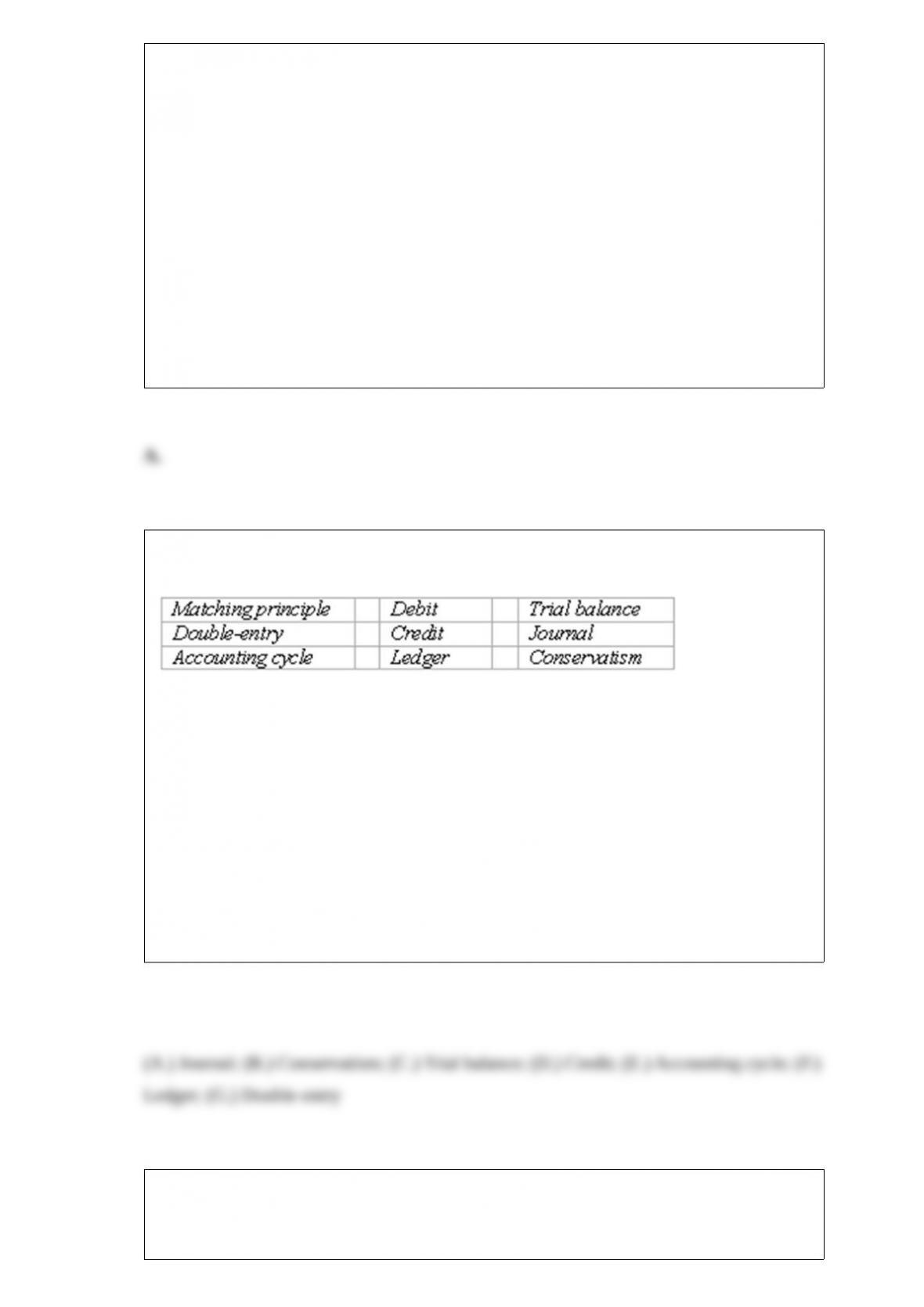

Accounting terminology

Listed below are nine technical accounting terms introduced in this chapter:

(A.) The accounting record in which transactions are initially recorded.

(B.) A concept designed to avoid overstatement of the financial strength of a company.

(C.) A schedule prepared to determine the equality of the debit and credit amounts in

the ledger.

(D.) An amount entered in the right side of a ledger account.

(E.) The sequence of procedures involved in recording transactions, processing the

information in the accounting system, and summarizing the information in the form of

financial statements.

(F.) The accounting record that contains a separate account for each type of asset and

liability, and for each element of owners’ equity appearing in the balance sheet.

(G.) The system of accounting in which every business transaction is recorded by equal

dollar amounts of debit and credit entries.

Working capital is calculated by:

A. Dividing current assets by total assets.

B. Dividing current assets by total liabilities.

C. Subtracting current liabilities from total assets.

D. Subtracting current liabilities from current assets.

The type of cost accounting system best suited to a particular company depends on:

A. The nature of the company’s manufacturing operations.

B. The requirements set forth by the FASB.

C. Government regulations.

D. The type of cost drivers available.

Evans Products uses a process costing system with two processing departments: the

Mixing Department and the Finishing Department. In June, unit costs incurred by the

Mixing Department amounted to $4.00 per unit. Unit costs transferred to the finished

goods warehouse during the month amounted to $22. Work-in-process inventories are

reduced to zero each month.

Refer to the information above. The transfer of 35,000 units to the Finishing

Department in June required:

A. A debit to Finished Goods Inventory of $770,000.

B. A credit to Work-in-Process Inventory, Mixing Department of $770,000.

C. A credit to Work-in-Process Inventory, Finishing Department of $140,000.

D. A debit to Work-in-Process Inventory, Finishing Department of $140,000.

The price of one currency stated in terms of another currency is the:

A. Current ratio.

B. Exchange rate.

C. Facilitating payment.

D. International clearing price.

Sally Smith had expenses of $800 in June which she paid in July. She reported these

expenses on her June income statement. By doing this, she is following the accounting

principle of:

A. Revenue realization.

B. Adequate disclosure.

C. Matching.

D. Conservatism.

On April 30, 2014, Tilton Products purchased machinery for $88,000. The useful life of

this machinery is estimated at 8 years, with an $8,000 residual value.

Refer to the information above. Assume that in its financial statements, Tilton Products

uses the 150%-declining-balance method and the half-year convention. Depreciation

expense in 2014 and 2015 will be:

A. $8,250 in 2014 and $14,953 in 2015.

B. $16,500 in 2014 and $12,964 in 2015.

C. $16,500 in 2014 and $16,500 in 2015.

D. $15,000 in 2014 and $11,786 in 2015.

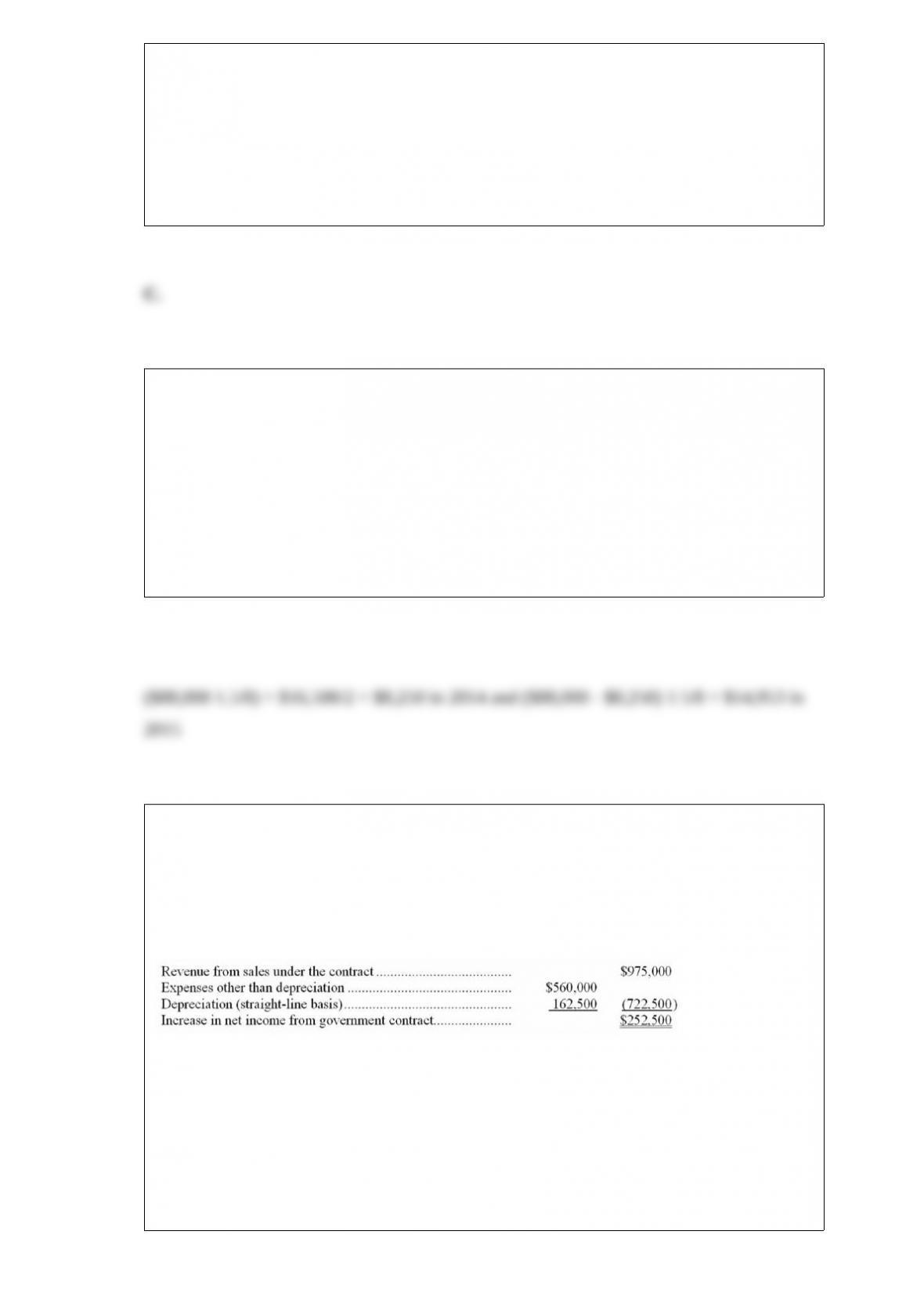

Capital budgeting

Golden Flights, Inc. is considering buying some specialized machinery which would

enable the company to obtain a six-year government contract for the design and

engineering of a futuristic plane. The machinery costs $975,000 and must be destroyed

for security reasons at the end of the six-year contract period. The estimated annual

operating results of the project are as follows:

All revenue from the contract and all expenses (except depreciation) will be received or

paid in cash in the same period as recognized for accounting purposes. You are to

compute the following three factors for this project:

(a) Payback period: __________ years

(b) Return on average investment: __________%

(c) Net present value of the investment in this machinery, discounted at an annual rate

of 12% (an annuity table shows that the present value of $1 received annually for six

years discounted at 12% is 4.111): $__________

In a manufacturing company, the cost of finished goods manufactured is equal to:

A. The beginning inventory of finished goods, plus net purchases, less the ending

inventory of finished goods.

B. The sum of the manufacturing costs charged (debited) to the Work in Process

Inventory account during the period.

C. The costs of direct materials, direct labor, and manufacturing overhead incurred in

manufacturing the goods sold during the period.

D. The beginning inventory of Work in Process, plus total manufacturing costs for the

period, less the ending inventory of Work in Process.